5. Better recycling of waste containing CRMs

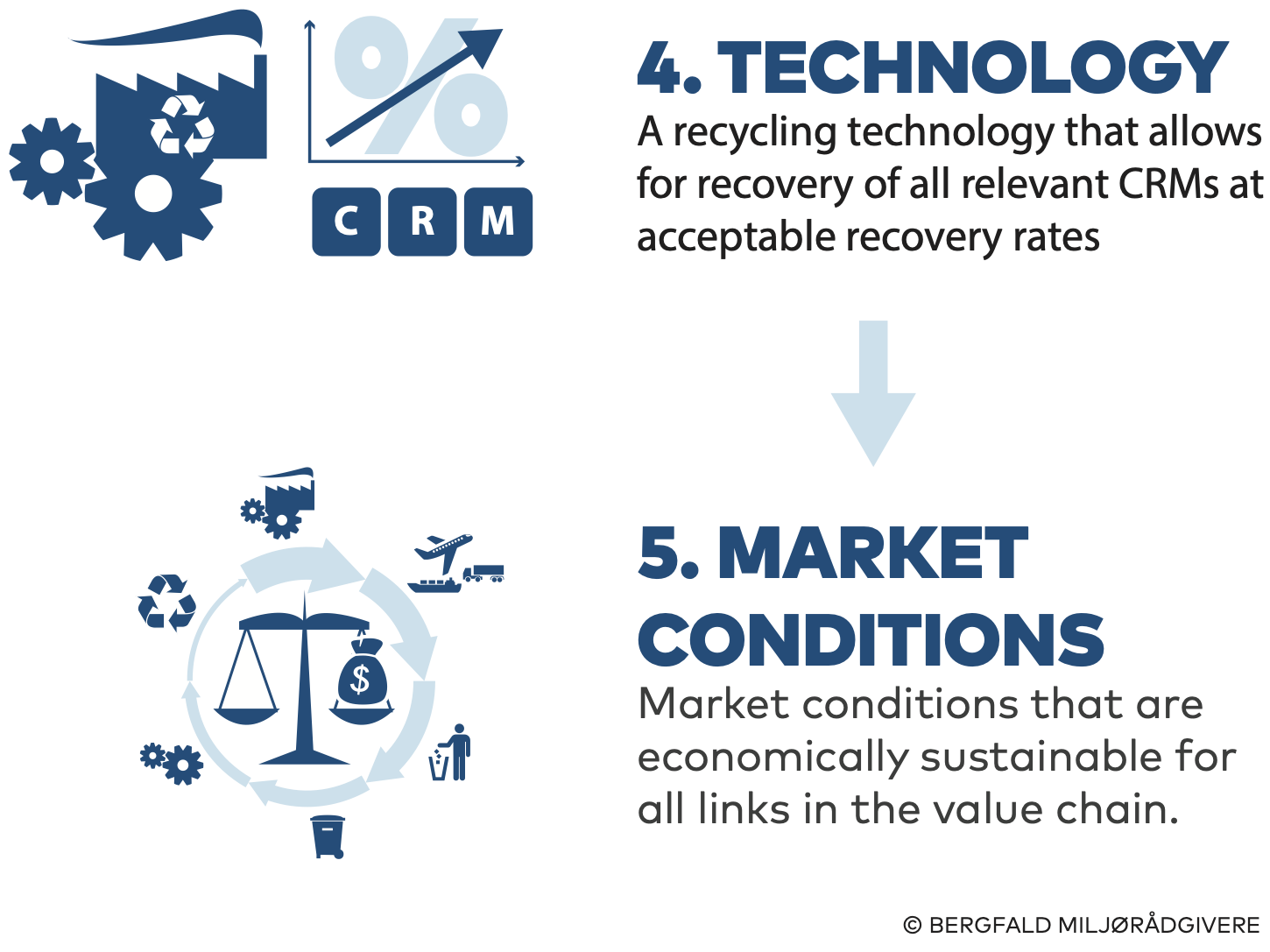

If necessary feedstock for recycling of CRMs is available, two main conditions must be met for successful recycling to take place as illustrated in figure 5.1.

Figure 5.1 Necessary conditions for successful recycling of CRMs.

Illustration Bergfald Miljørådgivere.

Illustration Bergfald Miljørådgivere.

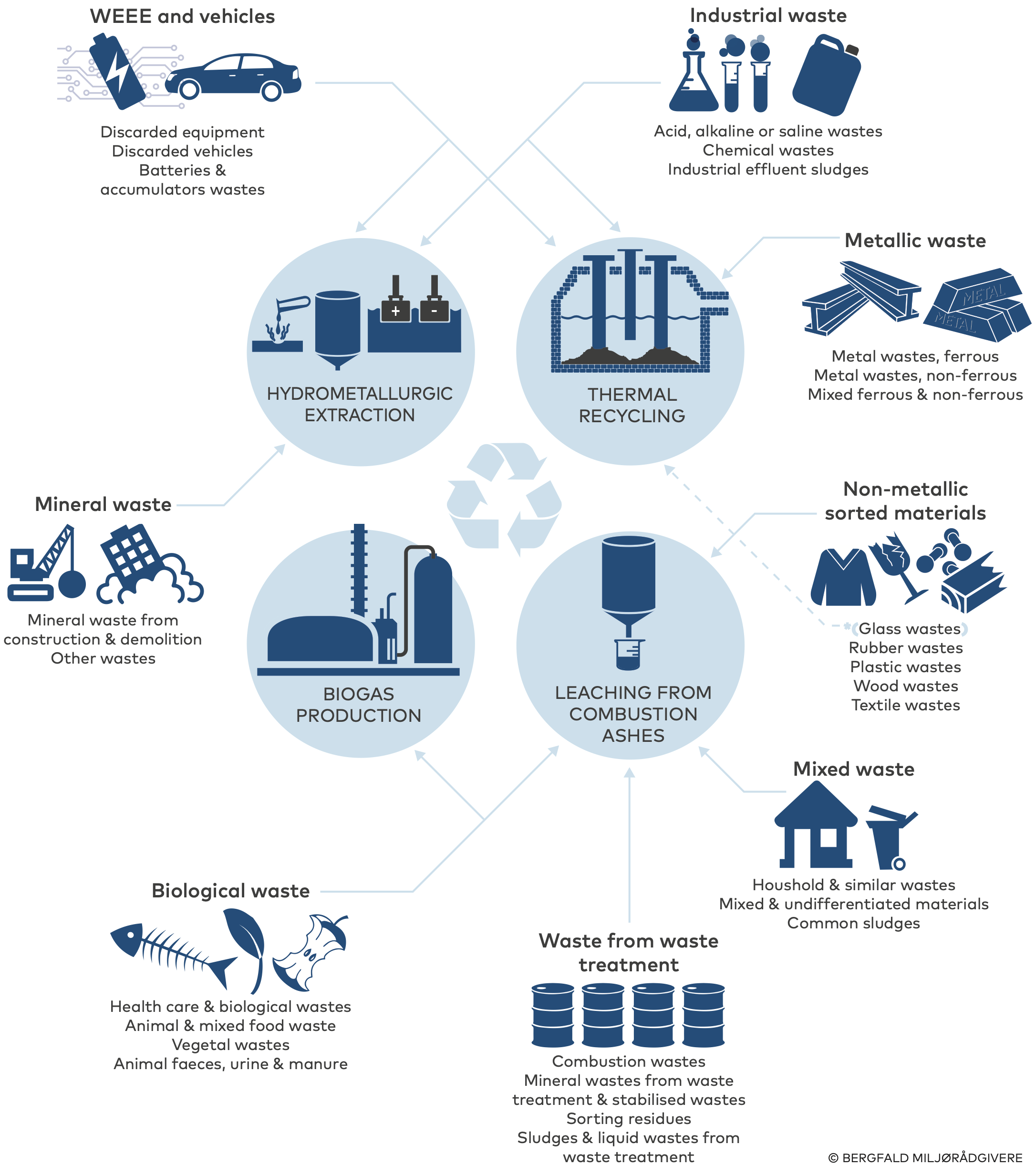

There are many technologies that can be used for recycling of CRMs, and they can be grouped into four main categories as illustrated in figure 5.2. Relevant waste streams for each main recycling option are also indicated.

Figure 5.2 Main technological CRM-recycling options.

Illustration Bergfald Miljørådgivere.

5.1 Recycling of CRM-waste in the Nordics

This section describes to what degree individual CRMs are recycled in the Nordics, and summarizes key industries that either currently recover CRMs or have technological advantages when it comes to establishing new or expanded CRM-recycling

Aluminium/bauxite

Aluminium is recycled as metal and alloy, and aluminum oxide is downcycled to clinker. There is no recycling of bauxite, and neither should there be, as this mineral has no applications except as a raw material for primary aluminium.

Speira

Bergfald Environmental Consultants is a HSE/permitting consultant to Speira.

Antimony

There is to our knowledge no dedicated recycling operations in the Nordics for antimony. As antimony is commonly used as alloying element in lead, it is indirectly recovered when lead is recovered. In the Nordics this happens at the Boliden Bergsøe plant in Landskrona and at Sala Bly in Sweden.

Arsenic

There is to our knowledge no relevant recycling of arsenic in the Nordics. There are dedicated incineration plants for CCA-waste, which brings forth a waste with high arsenic content. The arsenic-loaded ash is landfilled as hazardous waste and not recycled.

Baryte

There is to our knowledge no relevant recycling of baryte in the Nordics. There are waste treatment facilities for discarded drilling fluids, but these are concerned with reducing environmental footprint of the waste, not recycling the barium, although some barium containing drilling fluids may be reused.

Beryllium

There is no recycling capacity for beryllium or beryllium-containing alloys in the Nordic countries, neither in EU/EEA. WEEE sorting schemes are systematically sorting out beryllium-containing components during WEEE dismantling, but all of this is delivered as hazardous waste. The closest recycling capacity, to our knowledge, is Japan. There are industrial operations also in Kazakhstan and USA, but attempt to reach those with supplies of beryllium WEEE scrap from Europe have consistently failed.

Bismuth

There is to our knowledge no recycling capacity for postconsumer bismuth or bismuth-containing materials in the Nordic countries.

Boron

There is to our knowledge no relevant recycling of boron in the Nordics, nor in EU/EEA.

Copper

There is a huge capacity for copper recycling in the Nordics. The Boliden plant in Skelleftå is by far the most important. Indeed, most of copper containing WEEE scrap is currently sent there for recycling. There are also other possibilities for recycling, both in the Nikkelverk plant in Norway and the Boliden plant in Harjavalta.

Cobalt

There is a sufficient capacity of downstream cobalt recycling in the Nordics, if cobalt in the future is recovered from wastes. From the refining and smelter side, there is the Nikkelverk plant in Norway and the Boliden plants. From batteries, the lithium-ion-battery recycling plants are taking out black mass containing cobalt that in the future will be recycled in these refineries.

Feldspar

Sweden, Finland and Norway extract feldspar through the companies Sibelco and North Cape, but except for some glass recycling, no recycling operations are known to take place in the Nordics.

Fluorine

There is to our knowledge no relevant recycling operations for fluorine in the Nordics. However, that could be possible to develop. There is an aluminium fluoride production plant in Odda, Norway, currently owned by the Fluorsid group, based on imported fluorspar from Morocco. Wastes with high level of fluoride could in principle be processed at this plant. To achieve that, the plant needs an updated operational permit, and the fluor-containing waste needs to be properly characterized to avoid contamination of the products. Indeed, preprocessing might be needed. Capacity-wise, this plant would probably be able to absorb any tonnage that can be extracted from Nordic waste fractions.

Gallium

There is no recycling capacity for postconsumer gallium or gallium-containing alloys in the Nordic countries, nor in EU/EEA. There are gallium recycling operations for ingot scrap in Germany, but the requirements there are unreachable for any kind of scrap and extracts possible to produce from Nordic waste.

Germanium

There is no recycling capacity for postconsumer germanium or germanium-containing alloys in the Nordic countries. There is a recycling plant for high concentration germanium sludges in Belgium. That plant is currently idle, as all germanium-rich fractions are sent to Russia and China.

Graphite, natural

There is recycling capacity for postconsumer lithium batteries in the Nordics. These plants are currently focusing on extracting the metals, such as nickel and cobalt. However, they represent an infrastructure that could make recycling of graphite possible. However, the need for graphite in other industries, such as cast iron, is high, so downcycling is also an opportunity.

Hafnium

There is no recycling capacity for postconsumer hafnium or hafnium-containing alloys in the Nordic countries. There has been some low-volume hafnium processing on-and-off in France.

Helium

There is no recycling capacity for postconsumer helium in the Nordic countries, but it will be rather straightforward to establish recycling solutions for spent waste gas. There are established return systems for helium bottles, and systems for the collection and processing of gases could be expanded.

HREE

There is no recycling capacity for postconsumer HREE or HREE-containing materials in the Nordic countries, nor in EU/EEA. Currently, there is only limited capacity in China. There is a plant under construction in USA for the processing of virgin HREE, but that will not be easily available for Nordic or European countries. There is also a LREE-processing plant under construction in Norway, which can be expanded to recycle HREE if provided incentives to do so.

Disclosure: One of the report authors is a minority shareholder in the REEtec plant.

Lithium

There is recycling capacity for post-consumer lithium batteries in the Nordics. So far, these processes do not recover lithium, but focus on extracting metals such as nickel and cobalt. However, the infrastructure for recycling of lithium is established. Recycling technology from batteries that include lithium is expected to be commercially available in the near future.

LREE

There is no recycling capacity for postconsumer LREE or LREE-containing materials in the Nordic countries, nor in EU/EEA. There have been plants in the recent past, for example in France, Belgium, Germany, Italy, Spain and Austria, recycling specific LREE containing materials. As neither of these plants have received legal or financial support to protect them from market manipulation, they have all closed. There is a virgin material LREE-processing plant under construction in Norway, and it can be expanded to recycle LREE if provided incentives to do so.

There is no recycling capacity for postconsumer LREE or LREE-containing materials in the Nordic countries, nor in EU/EEA. There have been plants in the recent past, for example in France, Belgium, Germany, Italy, Spain and Austria, recycling specific LREE containing materials. As neither of these plants have received legal or financial support to protect them from market manipulation, they have all closed. There is a virgin material LREE-processing plant under construction in Norway, and it can be expanded to recycle LREE if provided incentives to do so.

Disclosure: One of the report authors is a minority shareholder in the REEtec plant.

Magnesium

There is no recycling capacity for post-consumer magnesium in the Nordic countries. There is a substantial European capacity for recycling both sorted magnesium components and industrial scrap. Until 2005, there was a recycling operation in Norway for complex magnesium scrap, able to handle a wider range of waste than what is currently available in Europe. This plant is currently idle and possible to restart – given the right incentives. There is a substantial consumption of magnesium as an alloying element in the Nordic aluminium and steel industries of more than 20,000 tons that could have been converted from primary to secondary magnesium – if the necessary incentives were provided, this could reduce dependence on the current three primary magnesium suppliers to Europe; China, Russia and Israel.

Manganese

There is some industrial recycling capacity for manganese in the Nordics. The Eramet and Ferroglobe manganese alloy plants have the possibility to receive high-manganese wastes as feedstocks. Indeed, they are currently operating advanced dust/fines recycling operations and can receive much more. Stavanger Staal in Norway is recycling high manganese steels. There are also plans to establish a manganese sludge recycling plant in a Scandinavian country.

Nickel

There is a huge capacity for nickel recycling in the Nordics. The Nikkelverk plant in Norway and Boliden plant in Harjavalta are both able to receive high-nickel feedstock for recycling. Indeed, both have declared their intention to increase the secondary feedstock supplies if such materials become available.

Niobium

There is no recycling capacity for postconsumer niobium or niobium-containing materials in the Nordic countries. There are several stakeholders trading and processing minor volumes of high-niobium materials in EU.

PGM

There is substantial recycling capacity for PGM metals in the Nordics. The Nikkelverket plant in Norway, Boliden Rönnskär in Sweden and Boliden Harjavalta in Finland are all able to receive different PGM-containing secondary feedstocks for processing, even low-grade materials. The K.A. Rasmussen plant in Norway is able to process high grade metals such as industrial catalysts.

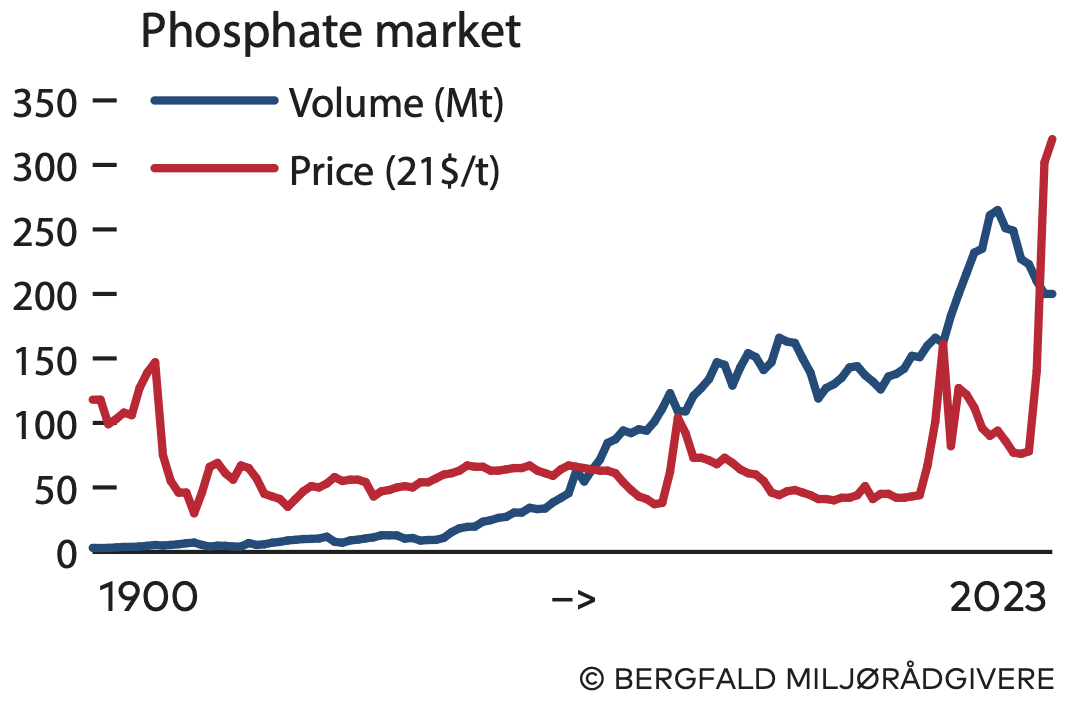

Phosphate

The most developed method for recycling of phosphate seems to be through biogas production where the nutrient-rich residue from the anaerobe digestion process can be used as phosphate rich fertilizer. All Nordic countries have extensive biogas production. There are also interesting projects extracting phosphate from incineration ashes and wastewater.

Scandium

There is no recycling capacity for postconsumer scandium or scandium-containing materials in the Nordic countries, nor in the Western hemisphere. Both primary and secondary scandium need processing in either Russia or China.

Silicon

There is no recycling capacity for postconsumer silicon or silicon-containing materials in the Nordic countries. There is ongoing research and tests for recycling of certain high-end silicon products, such as solar panels. Indeed, substantial such work has been carried out at the Elkem/REC test center in Norway. However, as it was recently decided to close the two Norwegian REC plants, recycling is not expected to be industrialized. The Wacker plant in Norway may consider recycling opportunities in the future, but no timeline has been provided.

Strontium

There is no recycling capacity for postconsumer strontium or strontium-containing materials in the Nordic countries.

Tantalum

There is no recycling capacity for postconsumer tantalum or tantalum-containing materials in the Nordic countries. However, there is advanced processing capacities in Estonia and Germany that could easily be expanded if extraction of tantalum containing wastes in the Nordics is started.

Titanium

There is no recycling capacity for post-consumer titanium or titanium-containing materials in the Nordic countries. There is from time to time the use of titanium metal turnings in the production of primary aluminium alloys. However, this is industrial scrap, a globally traded byproduct. Currently, all titanium metal consumption in the Nordics is based on imported material from China or Russia.

Tungsten

There is significant recycling capacity for tungsten waste, organized by Swedish company Sandvik. The key recycling furnace is in Austria, but Sandvik operate a high-quality collection scheme and reclaiming operation in the Nordics to get feedstock. If tungsten recovery from WEEE or slags are increased, this value chain would be valuable to cooperate with.

Vanadium

There is no recycling capacity for postconsumer vanadium or vanadium-containing materials in the Nordic countries. Neometals in Finland have a project to upgrade vanadium-containing blast furnace slags currently produced and landfilled in Sweden and Finland to a commercial ferrovanadium alloy. The project has received funding from the European Investment Bank as a strategic project. If built, this plant will probably be able to receive also other high-vanadium waste streams.

5.2 Barriers to better recycling of CRM waste

Many CRMs are distributed in products and materials at low levels that make recycling challenging.

Although CRMs are chemical components of many waste streams, the concentrations are often too low for profitable extraction. Many applications of CRMs like pigments, catalysts and additive in glass and ceramics require only small amounts in each product. High prices and uncertain supply chains also limit the use of many CRMs. Although large amounts of CRMs are consumed in the manufacture of products and materials due to large overall product volumes, a limited number of waste streams arise containing high concentrations of CRMs that can be easily recycled. CRMs are also often bound strongly in chemical structures that make extraction even harder.

Large amounts of CRMs are also available in tailings from mining operations and in slag, dust and sludge from metal processing industries. Even so, the concentration of CRMSs is often low and not easily extractable.

Substitution with less valuable materials and micronization of components with increasingly heterogeneous chemical composition makes recycling less profitable.

High prices and concern over supply risks has led to substitution of many costly raw materials with less expensive ones, exemplified by increasing substitution of cobalt with less expensive nickel in batteries. There are also examples of shifts in technological applications where new solutions that replace older ones demand lower input of expensive materials, which is the case for data storage when conventional hard disks (HDD) are replaced with solid state drives (SSD).

In addition, the use of high value materials is becoming more efficient through micronization of many components which have led to reduced levels of high value materials in many products, especially in the EE-sector. From a resource efficiency standpoint this is a favourable development but creates a rising concern in the recycling sector where recycling processes create outputs with lower economical value. This conflict between more efficient product design and less profitable recycling may also lead to reduced economic incentives for recycling of CRMs.

Large amounts of CRMs are lost during metal recycling.

One main application of many CRMs is as additives in alloys. When these alloys are scrapped and recycled currently available technology often only allow for recovery of base metals while most minor metals are either lost in the slag or follows the recovered base metal as a pollutant. This is a significant challenge for recycling of both aluminium and steel, not only because important CRM-resources are lost, but also because CRMs that unintentionally follow the recycled steel or aluminium metal often lower the quality of the recycled material and restricts the use of secondary metal products.

PCBs contain more than seventy elements including a large number of CRMs. When gold and copper is extracted from PCB significant amounts of tantalum, gallium, germanium and rare earth elements are lost in the recycling process. Additional metals can be recovered with current technology but often at the cost of diminished recovery rates of the main metals.

No recycling technology is available for CRM-recycling from multiple feedstocks.

Although tailings, industrial slag, dust and sludge, together with other collected waste streams contain large amounts of CRMs, not all waste streams and not every individual CRM have currently mature technology options when it comes to recycling. This means that even if new recycling of certain CRMs were to be required through legal instruments or made economically incentivised, no process can still be designed to ensure efficient recycling. The development of mature recycling technologies for many CRMs will most likely take many years and require massive R&D-efforts.

Many applied technologies for recycling of CRMs operate with low recovery efficiencies and extract only a limited number of CRMs that are available in the feedstock. Improving the recovery efficiency of these processes is also a huge undertaking that cannot be expected to be solved quickly. However, there is a lot to learn from the established mineral processing industry. Companies active in processing of complex nickel or copper ores, such as Glencore and Boliden, are familiar with complex multiprocessing schemes to extract even very low grades of precious metals such as gold and PGM. The competence and technology developed by these companies have matured over decades. Indeed, even if the political will exist to significantly increase recovery of CRMs from complex and mixed waste streams, one should not underestimate the time and effort needed to develop this.

CRM-recycling is often less cost-effective than production of virgin CRMs.

Compared to extraction of CRMs from a mineral ore, recycling of the same CRMs from waste materials are often more costly due to more heterogenic feedstock and lower concentrations of CRMs. Gallium is for instance found as 100–300 ppms in dissolved bauxite liquor, but are only used as a few tens of ppms in most LED. Another example is germanium, which is typically found in +1000 ppms in lead and coal ash concentrates, but only used in a few tens of ppms in PCBs and special optics. In both cases there are components with higher grades – but the bulk of the waste tonnage holds very low concentrations.

Small volumes and large fluctuations in prices make recycling of products containing CRMs economically challenging.

Although CRMs are essential chemical components of countless products and materials, many CRMs are only used in very small amounts in each product which limits the market size for the same CRMs. This creates challenges when scaling recycling processes to fit the market, and at the same time allow for a profitable production volume. In addition, the market price for many CRMs is historically known to be volatile and fluctuate in unpredictable ways that creates additional financial risks for a recycling operation.

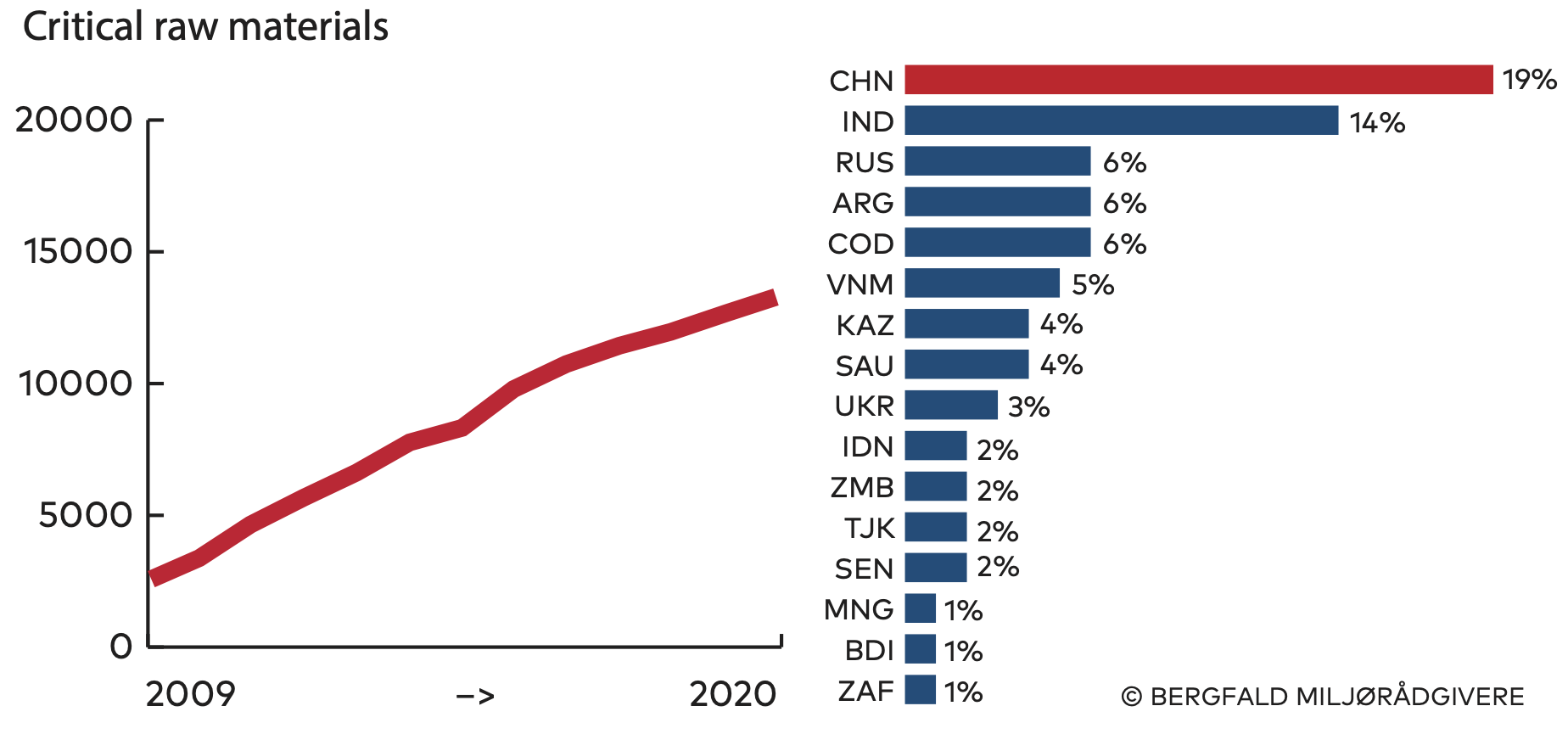

Market manipulations from dominant CRM-suppliers disrupt European CRM-recycling.

A few countries have obtained market dominance when it comes to both extraction and processing capacity for individual CRMs and have used this position to disrupt downstream industries in other countries through market manipulations that include disputed export restrictions.

Figure 5.3 OECD is mapping export restrictions of critical raw materials.

Illustration Bergfald Miljørådgivere.

OECD 2023. Raw Materials Critical for the Green Transition: Production, International Trade and Export Restrictions.

Illustration Bergfald Miljørådgivere.

Figure 5.4 Global market size and prize for phosphate rock.

Source: Bergfald Miljørådgivere

Source: Bergfald Miljørådgivere

NIMBY-responses blocks new CRM-recycling projects or necessary support infrastructure.

Increased CRM-recycling will require the construction of new process plants and industrial support facilities that can be expected to face significant resistance from local communities that are becoming increasingly hostile to new industrial projects in their own region. This phenomenon, often referred to as the NIMBY-effect (Not In My Backyard) is on the rise in many European countries, and may disrupt efforts to establish new CRM-recycling projects.