4. Denmark

Introduction

The Danish seafood value chain is located between the rich fishing grounds in the North Atlantic Ocean and large salmon farming in Norway, on the one hand, and the European market, on the other. While domestic fisheries and aquaculture exist, the intermediate part of the value chain, represented by processors and wholesalers using imported raw materials and taking advantage of well-established ties to customers across Europe, is most important in terms of jobs and contribution to GDP.

There is a Danish seafood value chain for human consumption and another for fish for reduction. The value chain for seafood for human consumption is supplied by Danish fisheries, Danish aquaculture, and imports. Processing takes place before a large seafood wholesale sector sells raw materials, semi-processed products, and processed seafood, especially for export but also for domestic consumption.

The value chain for fish for reduction is supplied by Danish and foreign fishers. All catches are processed into fishmeal and Fish oil, together with residues from the processing of seafood for human consumption in Denmark and neighbouring countries. Most fishmeal and fish oil are used in feed mixes for aquaculture produced by Danish fish feed firms, mainly exported, but to a minor extent also used in Danish aquaculture. Some amounts are also used domestically as feed for young pigs.

The contribution of the seafood value chain to gross value added (GVA) and employment is shown in Table 4.1. The fishery for reduction includes only large vessels (>40 m), which account for 84% of total catches. Hence, the remaining catch for reduction is included in the economic numbers in the value chain of seafood for human consumption.

Table 4.1: Key economic numbers for the Danish seafood value chain, 2023, numbers and DKK Million, current prices

Firms (number) | Turnover (DKK Million)3 | EBIT (DKK Million)4 | Gross value added (DKK Million)5 | FT-employment (persons)6 | |

Seafood human consumption | |||||

Fishery1 | |||||

- Vessels < 18 m | 254 | 575 | -29 | 276 | 299 |

- Vessels 18-40 m | 76 | 899 | 22 | 427 | 358 |

- Vessels > 40 m | 20 | 954 | 313 | 673 | 60 |

- Fishery total | 350 | 2,428 | 306 | 1,375 | 717 |

Aquaculture | |||||

- Traditional pond farms | 59 | 258 | 30 | 77 | . |

- Recirculated farms | 62 | 786 | 24 | 178 | . |

- Marine farms | 19 | 601 | 89 | 150 | . |

- Other | 36 | 47 | 0 | 25 | . |

- Total aquaculture | 176 | 1,692 | 143 | 431 | 406 |

Processing factories2 | |||||

- Salmon and trout | 39 | 9,371 | 245 | 825 | 1,013 |

- Whitefish and flatfish | 5 | 609 | 27 | 121 | 180 |

- Herring and mackerel | 13 | 2,080 | 19 | 368 | 484 |

- Shrimp and mussels | 11 | 1,426 | 623 | 771 | 197 |

- Mixed processing | 19 | 819 | -91 | 48 | 216 |

- Processing total | 87 | 14,306 | 823 | 2,133 | 2,089 |

Total | 613 | 18,426 | 1,271 | 3,939 | 3,212 |

Fish for reduction | |||||

Fishery1 | . | 874 | 286 | 616 | 55 |

Fishmeal factories | 2 | 3,538 | 384 | 608 | 176 |

Fish feed firms | 2 | 1,990 | 16 | 58 | 178 |

Total | 4 | 6,402 | 686 | 1,282 | 409 |

Total | 617 | 24,828 | 1,958 | 5,221 | 3,621 |

1: Fishery includes only commercial active vessels with an annual landing value of more than DKK 415 801, but both landings in Denmark and elsewhere. More than 98% of the total landing value originates from commercially active vessels. Some vessels target both fish for human consumption and reduction. 84% of the total landing value is caught by vessels >40 m, also targeting pelagic fish. The economic numbers for the fishery for reduction include only catches from vessels >40 m.

2: Processing factories all specialize in seafood and are grouped according to their main use of raw materials. The group ”Herring and mackerel processing factories” included in the source Nielsen (2025) also includes fishmeal factories, but these are removed from the seafood for human consumption value chain and moved to the fish for reduction value chain, based on numbers from the annual accounts of the two active companies (Triple Nine Thyborøn A/S and FF Skagen A/S).

3: Turnover is the sum of the turnover of all companies. In more cases, there is double-counting, indicating that turnover exceeds total production value. The reason is that products are traded between Danish firms. That happens, e.g., in processing, where one Danish firm makes the first processing and sells to other firms that make the final product. It also happens in aquaculture, where one firm produces trout fry and sells them to marine fish farms.

4: EBIT is Earnings Before Interest and Taxes.

5: Gross value added is a measure of the contribution of the value chain to the Gross Domestic Product, calculated as turnover minus operating costs excluding salary costs, depreciation, and interest.

6: Full-time employment is for fisheries calculated as the number of working days on all vessels (onshore and offshore) divided by 220 working days per year, assuming 7.4 hours of work a day. For vessels with long fishing trips and around-the-clock fishing, full-time employment may be underestimated. For fishmeal factories and fish feed firms, the numbers include employment, not full-time employment.

Sources: For aquaculture Statistics Denmark (2025a), for fisheries, Statistics Denmark (2025b), for firms processing seafood for human consumption, Nielsen (2025), for fishmeal firms Triple Nine Thyborøn A/S (2024) and FF Skagen A/S (2024), and for fish feed companies BioMar A/S (2024) and Aller Aqua A/S (2024).

In the Danish seafood value chain, 617 firms operate, with a turnover of DKK 24.8 billion, an EBIT (profit) of DKK 2.0 billion, a gross value-added of DKK 5.2 billion, and full-time employment of 3 621. Hence, the seafood value chain contributes 0.18% to total Danish GDP and 0.14% to full-time employment. However, seafood sales from wholesale firms (importers, exporters, and domestic wholesalers), supermarkets, and fishmongers are not included in these numbers because 2023 data are unavailable. For 2020, Nielsen (2023) identified total gross value added at DKK 2.7 billion and total full-time employment in seafood activities across these three sectors at 3 924 full-time employees. Assuming the three sectors remain unchanged in size, adding downstream activities to the value chain increases the value chain's total contribution to 0.27% of GDP and 0.29% of full-time employment.

The value chain of seafood for human consumption contributes DKK 3.9 billion in gross value added and 3 212 full-time employees, and thereby covers 76% of 89%. The value chain for seafood for human consumption is supplied by fisheries, which generate DKK 1.4 billion in gross value added and employ 717 full-time employees, while aquaculture contributes DKK 431 million in gross value added and employs 406 full-time employees. In fisheries, vessels >40 m have the largest gross value added, while full-time employment is largest in medium-sized and small vessels. In aquaculture, recirculated farms and marine farms are the largest contributors to gross value added. However, processing is the main contributor with gross value added of DKK 3.9 billion and 2 089 full-time employees. In processing, about half of gross value added and full-time employment comes from salmon and trout, while a large contribution to gross value added also comes from shrimp.

The value chain for fish for reduction is supplied by fisheries with a gross value added of DKK 616 million and 55 full-time employees. These numbers include only activities of vessels >40 m that make up 84% of the landing value, since fishing for reduction is a side activity to fishing for consumption. Fish meal factories contribute a gross value added of DKK 608 million and employ 176 people, while the gross value added in fish feed firms is DKK 58 million and the employment is 178.

Gross value added per full-time employed person is largest in vessels >40 m, at DKK 11.2 million, followed by shrimp processing at DKK 3.9 million and fish meal factories at DKK 3.5 million. It reveals that these segments are efficient in terms of employment but also indicates that firms are capital-intensive.

Regulation and management

Danish fisheries are regulated as part of the Common Fisheries Policy ruled by the principle of relative stability, where each country receives a total allowable catch (TAC) of the EU's part of fish stocks, based on a fixed percentage. The EU part is fixed after negotiations with non-EU parties. The most important agreement for Danish fisheries is the Brexit agreement (United Kingdom and the European Union 2020), which specifies allocations of each TAC between the UK and the EU. Bilateral and multilateral agreements are also in place, fish-stock-wise, with, among others, Norway and the Faroe Islands. The Commission also applies a system of capacity limits based on gross tonnage and engine power. This system, however, does not impose any limitations on Danish vessels.

The Danish TAC for each stock is allocated to fishers under the individual transferable quota scheme, in which each fisher has the right to catch a share of the TAC for that stock. That accounts for demersal, pelagic, and reduction fisheries. It is possible to sell this right to other fishers both permanently and annually. Moreover, small vessels below 17 m have special arrangements in which a minor share of the TACs is held back and allocated freely to vessels that voluntarily join the arrangement and thereby abstain from selling quotas or quota shares to vessels outside the arrangement.

The most important waters for Danish vessels in terms of landing value are the North Sea from where 59% of the total value on DKK 3.2 billion originate (2019-2023), followed by Skagerrak (18%), Kattegat (5%), the Baltic Sea (5%), West of Scotland (4%) and Norwegian Sea (2%). In terms of zones, 74% of the landing value originated from the EU zone, 25% from other countries' zones, mostly the British zone, and 1% from international waters. Since Denmark is part of the Common Fisheries Policy, Danish fishing takes place in the EU zone; a separate Danish fishing zone doesn’t exist. Hence, parts of Danish catches originate in the exclusive economic zones of other EU countries, such as Sweden, Germany, the Netherlands, and Poland. Catches of fishers from these countries also partly originate from the Danish extended economic zone.

Danish vessels land 77% in value terms in Denmark (2019-2023), 7% in other EU countries, mainly Sweden and the Netherlands, and 16% outside the EU, including Norway and the UK. In Denmark, 47% is landed in Northern Jutland and 24% in Central Jutland. The main harbours are Skagen, Hanstholm, Thyborøn, Hirtshals, and Hvide Sande. Mackerel landed in Norway is the most important species landed in foreign harbours.

Aquaculture production in Denmark requires a permit and is regulated because nutrient discharges negatively affect ecosystems in freshwater streams and lakes, as well as in coastal waters, when combined with runoff from agriculture and wastewater. Since the water environment is in good or very good condition only in 30% of catchment areas, a “Not good ecological state” prevails in 70% of the areas. Hence, spillover effects on the environment of many coastal waters exist, especially in the Baltic Sea and inner waters (European Commission 2025). Danish aquaculture is thus very strictly regulated. Aquaculture has traditionally been regulated by non-transferable feed quotas to limit discharges of nitrogen, phosphorus, and organic material. That regulation has, over the last decade, been combined with the voluntary option of choosing non-transferable output regulation. Such a choice is important because recirculating aquaculture systems have been developed that limit nitrogen and phosphorus discharges per kilo of farmed fish. Aquaculture in freshwater ponds is in Jutland, marine aquaculture is present in the inner Danish waters along the East coast of Jutland and at Southern Zealand, while mussel farming prevails in the Limfjord.

Seafood processing and wholesale are mainly located along the Northwest coast of Jutland, where fish are landed, although processing also occurs in other parts of the country, for example close to the large market area in Copenhagen. Given the large presence of intermediate seafood firms in Denmark between rich fishing grounds in the Northeast Atlantic Ocean and the EU seafood market, the ownership structure of processing and wholesale is complex. A number of firms in Denmark are owned by Danes, but a large part of the firms' activities is owned by Greenlandic and Norwegian firms. Moreover, seafood processing and wholesale companies in other countries are under Danish ownership. Especially at the main EU market, but also internationally.

Recreational fishing takes place along rivers and streams, on the coast, from shore, from small vessels, and in put-and-take lakes. Sport fishers, leisure fishers, and part-time fishers are regulated separately. Sport fishing requires an annual license. Leisure fishing is done from small dinghies and is limited to a few nets per person. Part-time fishing claim quotas, allocated from a minor part held back in the TACs. Part-time fishing contributes less than 2% of the Danish landing value. Hence, while sport, leisure, and part-time fishing may induce a substantial recreational value to the practitioners, the contribution to seafood security at the national level is negligible.

Supply of seafood from primary production is shown in Table 4.2.

Table 4.2: Primary supply of seafood in Denmark 2019-2023, quantity and value, current prices.

Quantity (tonnes live weight) | Value (DKK Million) | |||||||||

2019 | 2020 | 2021 | 2022 | 2023 | 2019 | 2020 | 2021 | 2022 | 2023 | |

Aquaculture1 | ||||||||||

Trout | 33,693 | 32,955 | 28,477 | 26,741 | 24,624 | 830 | 820 | 727 | 818 | 786 |

Salmon | 1,473 | 1,940 | 1,668 | 1,165 | 1,222 | 59 | 72 | 61 | 0 | 60 |

Blue mussels | 7,333 | 6,317 | 8,485 | 8,522 | 6,210 | 41 | 25 | 41 | 38 | 32 |

Other | 1,282 | 1,416 | 2,059 | 1,496 | 1,066 | 90 | 85 | 137 | 177 | 88 |

Total | 43,781 | 42,628 | 40,689 | 37,924 | 33,122 | 1,019 | 1,002 | 967 | 1,034 | 966 |

Fishery | ||||||||||

Seafood for consumption2 | ||||||||||

Demersal fish | ||||||||||

Cod | 12,397 | 6,964 | 4,433 | 3,630 | 5,394 | 272 | 174 | 123 | 122 | 166 |

Plaice | 14,453 | 13,676 | 10,701 | 7,631 | 7,108 | 263 | 214 | 190 | 180 | 165 |

Hake | 3,099 | 3,804 | 3,346 | 3,585 | 2,973 | 70 | 73 | 85 | 89 | 84 |

Monkfish | 2,894 | 1,996 | 2,141 | 2,132 | 1,955 | 90 | 58 | 65 | 72 | 65 |

Haddock | 1,454 | 1,095 | 2,403 | 4,039 | 3,970 | 19 | 12 | 24 | 44 | 45 |

Turbot | 470 | 468 | 537 | 489 | 416 | 33 | 28 | 43 | 49 | 41 |

Other | 13,865 | 11,238 | 9,233 | 7,759 | 6,948 | 231 | 178 | 185 | 186 | 155 |

Total | 48,631 | 39,242 | 32,794 | 29,265 | 28,764 | 979 | 738 | 714 | 743 | 721 |

Pelagic fish | ||||||||||

Herring | 110,643 | 105,069 | 72,336 | 85,202 | 60,637 | 483 | 480 | 381 | 494 | 416 |

Mackerel | 27,360 | 34,614 | 30,895 | 20,218 | 26,441 | 295 | 338 | 312 | 233 | 320 |

Other | 7,783 | 5,481 | 5,891 | 5,190 | 1,031 | 43 | 34 | 44 | 46 | 10 |

Total | 145,786 | 145,164 | 109,123 | 110,610 | 88,109 | 821 | 851 | 736 | 773 | 746 |

Crustaceans/mussels | ||||||||||

Nephrops | 6,039 | 4,283 | 5,419 | 5,019 | 4,726 | 298 | 197 | 289 | 328 | 291 |

Deepwater shrimp | 6,866 | 6,603 | 5,905 | 6,902 | 6,360 | 227 | 207 | 208 | 265 | 245 |

Common shrimp | 1,393 | 1,163 | 995 | 1,062 | 1,255 | 32 | 38 | 39 | 57 | 65 |

Blue mussels | 37,032 | 22,233 | 24,805 | 23,824 | 17,074 | 42 | 30 | 40 | 33 | 29 |

Other | 12,478 | 5,381 | 11,765 | 12,188 | 5,567 | 83 | 39 | 67 | 91 | 61 |

Total | 63,808 | 39,662 | 48,889 | 48,994 | 34,982 | 683 | 511 | 644 | 774 | 691 |

Other | 1,693 | 1,568 | 16,510 | 9,141 | 1,639 | 45 | 48 | 90 | 66 | 39 |

Total for consumption | 259,919 | 225,637 | 207,316 | 198,010 | 153,493 | 2,528 | 2,148 | 2,185 | 2,356 | 2,198 |

Fish for reduction3 | 378,344 | 506,749 | 259,025 | 260,056 | 340,865 | 737 | 996 | 582 | 612 | 987 |

Total fisheries | 638,263 | 732,385 | 466,341 | 458,066 | 494,359 | 3,265 | 3,144 | 2,766 | 2,968 | 3,185 |

Total primary production | 682,044 | 775,013 | 507,030 | 495,990 | 52,7481 | 4,284 | 4,146 | 3,733 | 4,002 | 4,151 |

1: Net production excluding sales to other Danish farms.

2: While 121 different species were landed by Danish vessels, those included are those with the largest landing value in Denmark and elsewhere in 2023, selected to cover at least 90% of the total landing value. After selection, they are grouped into demersal fish, pelagic fish, and crustaceans/mussels.

3: Landings used to produce fishmeal and Fish oil of all species. The main species in 2023 were, in quantity terms, sandeel (34.7%), sprat (29.9%), and blue whiting (24.1%).

Sources: Danish Agricultural and Fisheries Agency (2025b).

Total seafood supply from primary production in 2023 is 527,000 tonnes, corresponding to DKK 4.2 billion. DKK 966 million is aquaculture production, DKK 2.2 billion is wild-caught seafood for human consumption, and DKK 987 million is fish for reduction.

Trout is by far the largest species farmed, originating both as portion-sized portions of 200-400 grams per fish from freshwater ponds and larger sizes from marine farms. Salmon is also produced in recirculated aquaculture systems, and blue mussels are farmed. Total quantities farmed are reduced by 24% in the 2019–2023 period, while production values remain stable.

Fish for reduction include species such as sprat, sandeel, blue whiting, and Norway pout. Landing fluctuates due to fishing on low-year classes with varying recruitment. Prices are increasing over the 2019–2023 period, following the scarcity of supply and increased demand for feed in global aquaculture.

The total supply of seafood for human consumption in value is allocated equally between demersal fish, pelagic fish, and crustaceans/mussels in 2023. The most important species are herring, mackerel, nephrops, deepwater shrimp, cod, and plaice. Quantities fall in the period 2019–2023, both for demersal and pelagic fish, while they vary for crustaceans/mussels.

The status of the main fish and shellfish stocks for Danish fisheries is presented in Table 3. The current stock level is compared to the stock level that provided the largest possible catch in the long run (the Maximum Sustainable Yield, the MSY-level), and the current fishing pressure is compared to the fishing pressure providing the largest possible catch in the long run.

Table 4.3: Status of main stocks for Danish fisheries in terms of biological stock status and fishing pressure, 2023.

Species/stock | Danish catches from stock 20231 | F ≤ FMSY2 | SSB ≥ MSY Btrigger2 | |

Quantity (tonnes) | Value (DKK million) | |||

Herring North: Sea, Skagerrak, Kattegat | 67,301 | 462 | Not good | Good |

Mackerel: Northeast Atlantic | 28,209 | 341 | Not good | Not good |

Nephrops: Skagerrak, Kattegat | 4,454 | 274 | Good | |

Blue whiting: Northeast Atlantic | 87,119 | 252 | Not good | Good |

Sprat: North Sea, Skagerrak, Kattegat | 86,855 | 252 | Good | |

Sandeel: Central western North Sea | 85,160 | 247 | Good | |

Cod: North Sea, Skagerrak | 2,998 | 92 | Not good | Not good |

Deepwater shrimp: Skagerrak, Norw. Depth | 2,224 | 86 | Good | Not good |

Plaice: North Sea, Skagerrak | 3,306 | 77 | Good | Good |

Notes:

1: Quantity of catch of Danish vessels on each stock and the value of the catches at the average price of total landings of the species (not the exact stock).

2: For fishing pressure, a green box indicates that current fishing mortality (F) is smaller than the fishing mortality corresponding to the Maximum Sustainable Yield, while a red box indicates larger fishing mortalities. For stock status, a green box indicates that the current spawning stock biomass (SSB) is larger than the spawning stock biomass corresponding to the trigger value, a precautionary threshold value below which management action, in form of a reduction in fishing pressure, is triggered.

Sources: International Council for Exploration of the Sea (2025) and Danish Agricultural and Fisheries Agency (2025b)

For the nine fish and shellfish stocks shown, five are above the trigger values, three are below, and the reference points are undefined for nephrops in Skagerrak and Kattegat. The current fishing pressure is above MSY for four stocks, below MSY for three, and undefined for two. Hence, a simultaneous good status of both stock and fishing pressure only prevails for one stock, plaice in the North Sea and Skagerrak. Hence, the biological foundation for Danish fisheries is under pressure. A poor status, either for stock levels or fishing pressure, prevails across demersal, pelagic, and shellfish species.

The status of cod stocks in both the Western and Eastern parts of the Baltic Sea is not shown because fishing over the last 5-6 years has largely stopped following recurrent advice to set zero quotas. The bad status of the cod stocks results from a mixture of more pressures, including environmental pollution, earlier severe overfishing and changing water temperature following climate change (Möllmann et al 2021; Bossier et al 2021; Froese et al 2022). The implication is that the large-scale historical fishing in the Baltic Sea has almost disappeared.

Trade flows of Aquatic food: Denmark

The Danish value chain for seafood for human consumption

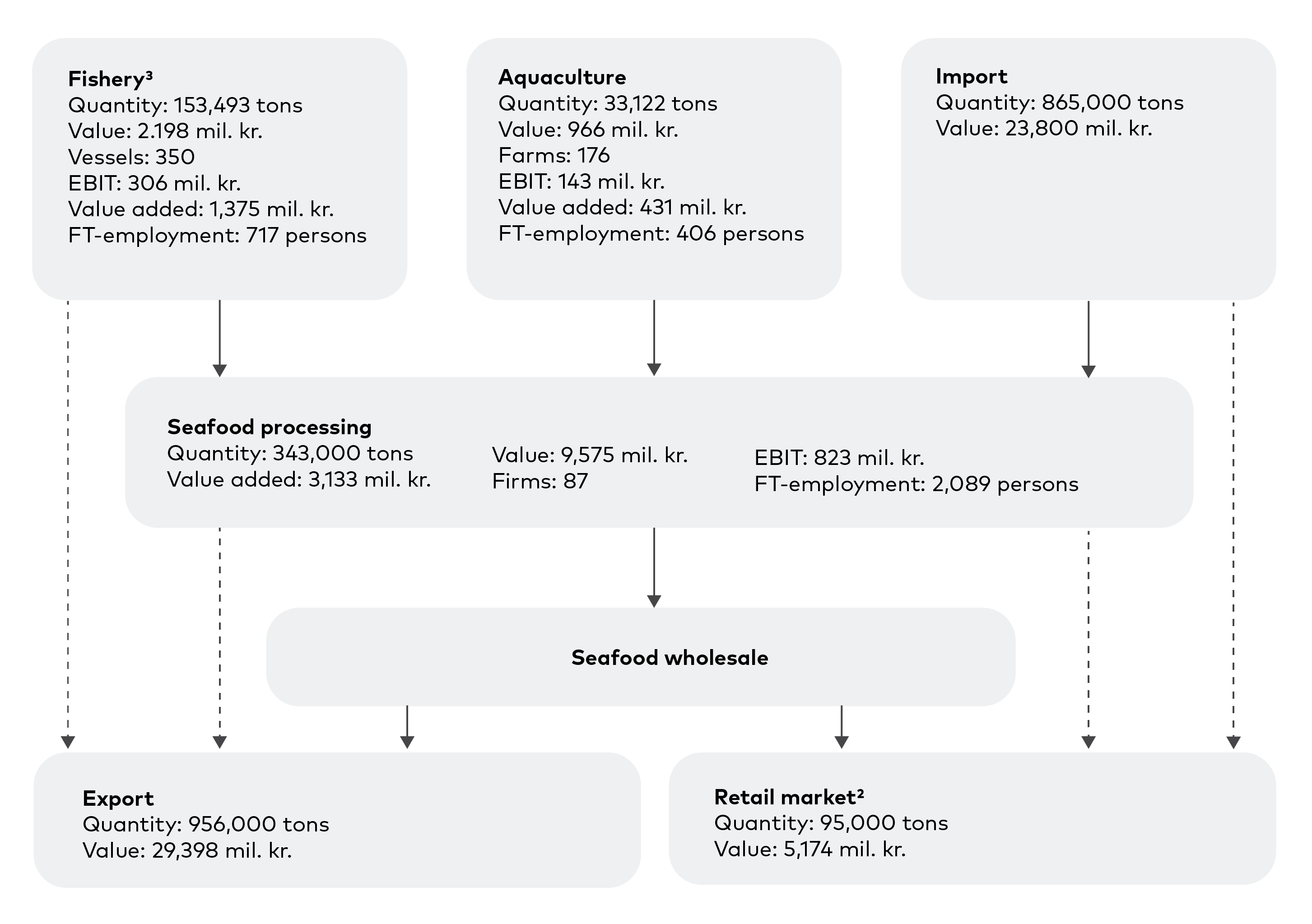

The structure of the Danish value chain for seafood for human consumption is identified using key numbers on quantities sold at different nodes of the chain. Economic numbers appear in Table 4.1, and all quantities are presented in live weight. The value chain is shown in Figure 4.1.

Figure 4.1: The Danish value chain for seafood for human consumption 2023, live weight1. Values in current value terms. FT= full time. EBIT= earnings before interest and tax.

Notes:

1: Quantities in live weight are known for fishery and aquaculture, while the quantities in live weight equivalents are calculated for seafood processing, import, and export using conversion factors from processed or traded weight to live weight. Conversion factors are inspired by the Food and Agriculture Organization of the United Nations (2025) but fitted to the Danish context. The same conversion factors are applied to all unprocessed products (live, fresh, and frozen) within each species group, and to all processed products (fillets, smoked, salted, dried, and final processed) within each species group. For unprocessed seafood products, the conversion factors are 1.30 for salmon/trout and whitefish/flatfish, 1.0 for pelagic fish, 1.0 for crustaceans/mussels, and 1.0 for others/mixed. For processed fish products, the conversion factors are for salmon/trout 2.0, for whitefish/flatfish 2.60, for pelagic fish 2.3, and for others/mixed 2.6. For processed products in the crustaceans/mussels group, the conversion factors are for shrimp 1.64, for cuttlefish 2.0, for nephrops/lobster 3.6, for mussels/other aquatic invertebrates 4.0, and for oysters/scallops 10.0.

2: The total quantity is identified in Table 4.6, while the total value is known per capita from Statistics Denmark (2023c).

Sources: Danish Agricultural and Fisheries Agency (2025ab), Nielsen (2025), and Statistics Denmark (2025a-e).

In 2023, 350 fishing vessels were commercially active with an annual landing value of more than DKK 415,801. Estimated full-time employment on those vessels is 772 persons, of which 717 fall in the segment of seafood for human consumption (allocated based on weighted landing values). Some vessels are specialized in fishing for human consumption, while others also target fish for reduction. Numbers for individual vessels are not available for 2023, but in 2020, 80% of the vessels specialized in fishing for human consumption. The remaining vessels both fished for human consumption and for reduction, except for two that specialized in fishing for reduction. The catch value for human consumption was DKK 2.2 billion, equally allocated between the three groups: whitefish/flatfish, pelagic fish, and crustaceans/mussels. The main species in value terms are herring, mackerel, nephrops, deepwater shrimp, cod, and plaice. 77% of the value is landed in Denmark from 2019 to 2023.

176 fish farms exist with a turnover of DKK 1.7 billion and a full-time employment of 406 persons. The production in 2023 is 33,122 tonnes, corresponding to a value of DKK 966 million. Turnover is larger than production value, among other things, due to the sale of fish fry for release into marine fish farms by Danish firms, which count in turnover but not in production. Rainbow trout is the dominant species. Both meat and the roe are important for trout from marine farms. Salmon, blue mussels, and oysters have gained importance in recent years, and tuna and pikeperch are also farmed. Farming in freshwater ponds is most important, with an annual turnover of DKK 1,044 million, while the turnover of marine farms is DKK 601 million. Farming in traditional freshwater ponds is declining, while farming in recirculating aquaculture systems with varying degrees of recirculation is increasing. Danish trout production is mostly exported, primarily in fresh, frozen, and smoked forms. The most important export markets are the areas with a tradition of eating freshwater fish in Central Europe, with Germany being the largest market.

In 2023, 87 seafood processing factories exist with a turnover of DKK 14.1 billion. Production is 343,000 tonnes live weight, corresponding to a value of DKK 9.6 billion. Turnover is larger than the production value, as the factories perform wholesale as a side activity. With a full-time employment of 2,089 persons, this part of the value chain contributes the largest employment. Processing of seafood in Denmark is detailed on groups of species and products in Table 4.4, together with import and export, both in total and specifying imports from Nordic countries and exports to Nordic countries.

Table 4.4: Processing, import totally and from Nordic countries and export totally and to Nordic countries of seafood for human consumption, 2023, quantity and current value.

Product and species1 | Quantity (1,000 tonnes live weight) | Value (DKK million current price level) | ||||||||

Processing | Import | Import | Export | Export | Processing | Import | Import | Export | Export | |

Total | Nordic | Total | Nordic | Total | Nordic | Total | Nordic | |||

Salmon and trout | ||||||||||

- Fresh, live | 9 | 153 | 153 | 95 | 2 | 335 | 6,795 | 6,759 | 4,352 | 83 |

- Frozen | 6 | 20 | 8 | 29 | 1 | 209 | 836 | 341 | 1,131 | 48 |

- Fillets | 53 | 43 | 20 | 90 | 3 | 2,848 | 1,844 | 1,034 | 4,615 | 120 |

- Smoked, Salted, Dried | 32 | 5 | 0 | 21 | 0 | 1,996 | 293 | 29 | 1,461 | 17 |

- Processed | 3 | 3 | 0 | 10 | 0 | 119 | 120 | 13 | 440 | 22 |

Total | 103 | 224 | 182 | 246 | 7 | 5,508 | 9,888 | 8,175 | 11,999 | 290 |

Whitefish and flatfish | ||||||||||

- Fresh, live | 3 | 90 | 66 | 82 | 6 | 125 | 1,679 | 1,260 | 2,141 | 149 |

- Frozen | 0 | 39 | 32 | 29 | 1 | 2 | 834 | 655 | 716 | 23 |

- Fillets | 16 | 60 | 22 | 53 | 6 | 273 | 1,186 | 528 | 1,217 | 144 |

- Smoked, Salted, Dried | 6 | 8 | 8 | 13 | 0 | 191 | 144 | 144 | 300 | 3 |

- Processed | 0 | 24 | 3 | 47 | 4 | 6 | 377 | 45 | 881 | 74 |

Total | 25 | 221 | 130 | 224 | 16 | 597 | 4,220 | 2,631 | 5,254 | 394 |

Pelagic fish | ||||||||||

- Fresh, live | 1 | 99 | 81 | 73 | 63 | 11 | 662 | 485 | 782 | 684 |

- Frozen | 7 | 8 | 7 | 13 | 0 | 113 | 96 | 83 | 174 | 4 |

- Fillets | 9 | 2 | 1 | 10 | 1 | 59 | 21 | 7 | 76 | 8 |

- Smoked, Salted, Dried | 1 | 1 | 0 | 9 | 2 | 26 | 10 | 3 | 66 | 11 |

- Processed | 115 | 10 | 5 | 76 | 6 | 1,278 | 122 | 46 | 862 | 70 |

Total | 132 | 120 | 95 | 181 | 72 | 1,488 | 910 | 624 | 1,960 | 777 |

Crustaceans and mussels | ||||||||||

- Fresh, live | 4 | 2 | 1 | 21 | 7 | 106 | 136 | 40 | 659 | 280 |

- Frozen | 0 | 74 | 60 | 77 | 13 | 0 | 2,960 | 2,203 | 3,380 | 581 |

- Fillets | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

- Smoked, Salted, Dried | 3 | 4 | 1 | 12 | 3 | 83 | 60 | 15 | 416 | 126 |

- Processed | 34 | 68 | 37 | 49 | 12 | 1,095 | 2,105 | 1,206 | 1,791 | 519 |

Total | 41 | 149 | 99 | 159 | 35 | 1,284 | 5,261 | 3,463 | 6,245 | 1,505 |

Other and mixed | ||||||||||

- Fresh, live | 7 | 34 | 22 | 20 | 12 | 16 | 482 | 324 | 591 | 91 |

- Frozen | 2 | 52 | 40 | 55 | 5 | 85 | 2,004 | 1,510 | 2,312 | 56 |

- Fillets | 5 | 25 | 6 | 29 | 8 | 36 | 458 | 84 | 506 | 82 |

- Smoked, Salted, Dried | 1 | 16 | 16 | 17 | 1 | 41 | 160 | 147 | 268 | 17 |

- Processed | 27 | 25 | 1 | 26 | 19 | 521 | 417 | 13 | 263 | 70 |

Total | 42 | 152 | 84 | 147 | 45 | 699 | 3,521 | 2,078 | 3,940 | 317 |

Total | ||||||||||

- Fresh, live | 23 | 379 | 323 | 291 | 90 | 593 | 9,753 | 8,869 | 8,524 | 1,287 |

- Frozen | 14 | 192 | 147 | 202 | 20 | 409 | 6,729 | 4,792 | 7,713 | 712 |

- Fillets | 83 | 131 | 49 | 183 | 18 | 3,217 | 3,509 | 1,653 | 6,414 | 354 |

- Smoked, Salted, Dried | 42 | 34 | 25 | 72 | 6 | 2,337 | 667 | 337 | 2,510 | 173 |

- Processed | 180 | 130 | 46 | 209 | 41 | 3,019 | 3,140 | 1,322 | 4,237 | 756 |

Total | 343 | 865 | 591 | 956 | 174 | 9,575 | 23,800 | 16,972 | 29,398 | 3,282 |

Notes:

1: Fresh and live products includes all codes in the Harmonized System under 0301 and 0302 and selected codes under 0306, 0307, 0308 and 0309, frozen products codes under 0303 and selected codes under 0306, 0307, 0308 and 0309, fillets codes under 3004, smoked, salted and dried products codes under 0305 and selected codes under 0306, 0307, 0308 and 0309, and processed products codes under 1604 and 1605. The group salmon/trout includes only codes of salmonids, the whitefish/flatfish group codes for cod, haddock, saithe, pollack, hake, whiting, ling, redfish, plaice, turbot, sole, lemon sole, monkfish, flounder, greater forkbeard, megrim and other flatfish, the pelagic group herring, mackerel, anchovies, sardine and horse mackerel, the crustaceans/mussels group all codes under 0306, 0307, 0308, 0309 and 1605, and the other/mixed group all other codes, both with other species and with a mixed content of species.

Sources: Statistics Denmark (2025d-e).

The value of domestically processed seafood is largest for salmon and trout, at DKK 5.5 billion (57%), followed by pelagic fish at DKK 1.5 billion (16%) and crustaceans and mussels at DKK 1.3 billion (14%). Processing is differentiated by product forms. Fillets are the largest with DKK 3.2 billion, followed by processed seafood with DKK 3.0 billion and smoked, salted, and dried products with DKK 2.3 billion. Packing, filleting, souring, pickling, smoking, canning, and ready meals products are sold, and activities include both packaging of unprocessed products, semi-processed products for further processing in other countries, and ready-made products for direct sale in supermarkets at export markets and in Denmark. The main individual processed items include salmon fillets, smoked salmon, souring of herring, mackerel in tomato, shrimp in brine, and peeled shrimp, single frozen (Statistics Denmark 2025e).

The import of 865,000 tonnes and DKK 23.8 billion in 2023 was brought as raw material for processing firms and for direct sales by both processing and wholesale firms. Raw materials (fresh, live, and frozen) accounted for DKK 16.5 billion (69%), fillets for 3.5 billion (15%), processed seafood for 3.1 billion (13%), and smoked, salted, and dried products for 0.7 billion (3%). Processing factories receive several species, with salmon, shrimp, and cod being the most important. 71% of the import value originates in the Nordic countries, with Norway being the largest supplier (DKK 8.0 billion), followed by Greenland (5.5) and the Faroe Islands (1.5). Imports account for 80% of the total quantities supplied by landings, aquaculture production, and imports. Salmon is mainly imported from Norway, but also from the Faroe Islands, shrimp from Greenland and Canada, cod and whitefish from several countries fishing in the Northeast Atlantic Ocean, while the “Other and mixed” category includes large quantities of Greenland halibut, mainly from Greenland, imported and directly exported mainly to China.

While statistics on seafood wholesale firms are unavailable for 2023, data from 2020 are available from Nielsen (2023). In 2020, 226 firms were registered in the branches of seafood wholesalers, fish importers, fish exporters, fish auctions, and centrals that collect and sort fish from fishers for the auctions. Full-time employment was 1,817 persons, and the turnover was DKK 21.0 billion. Like processing companies, wholesalers depend on imported seafood and on the resale of catches from Danish fishers.

The largest market for processors and wholesalers is the EU, accounting for DKK 19.6 billion, corresponding to 67% of total exports for human consumption. The simultaneous presence of both large seafood imports and large seafood exports indicates that Danish seafood processors and wholesalers have established a position in the intermediate part of the value chain as suppliers to the European seafood market, sourcing raw materials from the entire Northeast Atlantic Ocean. The distribution channels from fisheries in the Northeast Atlantic Ocean and salmon farming in Norway and the Faroe Islands, via Denmark, to the important final markets in the rest of the EU and in the UK are well-functioning. Fresh fish typically reaches large wholesale markets, e.g., in Paris or Madrid, within less than 24 hours of landing. Germany is the largest buyer country (DKK 4.1 billion, 14%), followed by China (3.4), France (2.4), and Poland (2.2). Total exports to Nordic countries account for DKK 3.3 billion (11%).

Seafood retail sales in Denmark in 2023 are estimated at DKK 5.2 billion, based on per capita seafood consumption of DKK 870 (Statistics Denmark, 2023c). Seafood is mainly sold in supermarkets and by fishmongers. Nielsen (2023) estimates the market share of supermarkets in seafood sales in 2020 at 84% and of fishmongers at 16%. Moreover, the share of seafood in total turnover was found to be 2.8% in 2020, corresponding to an estimated 1 518 full-time employees working with seafood in supermarkets. Moreover, Nielsen (2023) found that 173 fishmongers were registered with 589 full-time employees. Sales from cars selling fish directly to consumers are not included. The demand from supermarket chains reveals consumer preferences, though supermarkets also impose additional requirements on their suppliers. Suppliers must guarantee delivery, prices, and quality, and must be able to provide traceability documentation and deliver certified products. In recent years, fresh fish have increasingly been sold through online ordering with delivery directly to consumers.

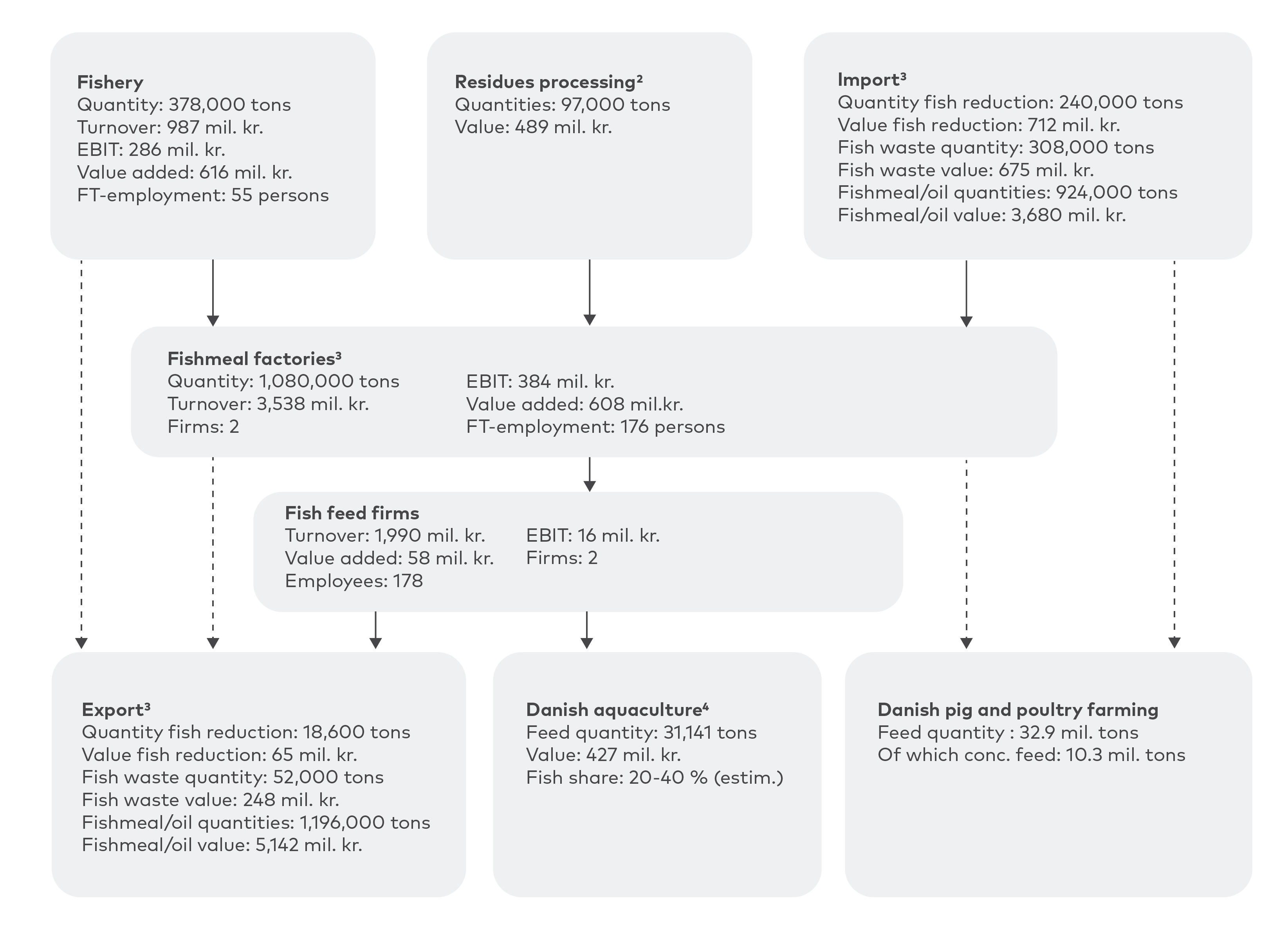

The Danish value chain for seafood for fish for reduction

The structure of the Danish value chain for fish for reduction is sketched in Figure 4.2, with key numbers showing quantities sold at different nodes in the chain. Economic numbers appear in Table 4.1. Quantities are presented in live weight, except for fish waste, which is only the wasted quantity.

Figure 4.2: The Danish value chain for fish for reduction 20231

Notes:

1: The value chain includes fish feed produced and applied in Denmark. Import and export of fish feed mixed with plant-based ingredients and pet feed are not included. Quantities are calculated in live-weight equivalents, assuming that one kilo of fish for reduction yields both 220 grams of fishmeal and 60 grams of fish oil. With fishmeal and fish oil accounted for separately, it is assumed that half of the live weight goes to fishmeal and the other half to Fish oil.

2: Marine residues include mainly cuttings from processors of seafood for human consumption, known from group 051191 in the harmonized system.

3: Import of fish for reduction is landings of foreign fishers in Denmark and export Danish fishers’ landings in foreign ports. Processing, import, and export of fishmeal and fish oil includes the groups 23012000, 23099010, 150410, and 150420 in the harmonized system.

4: The share of fishmeal and fish oil is both estimated to be 10-20% in feed for trout, summing to 20-40%.

Sources: Aller Aqua A/S (2024), BioMar A/S (2024), Danish Agricultural and Fisheries Agency (2025ab), FF Skagen A/S (2024), Statistics Denmark (2025abdef), and Triple Nine Thyborøn A/S (2024).

Danish vessels' total landings of fish for reduction in 2023 were 378,000 tonnes worth DKK 987 million. 350 commercially active vessels fished for human consumption and reduction. For 2023, numbers for individual vessels are not available, but in 2020, 20% of the vessels were fishing for reduction, while also engaged in fishing for consumption (Nielsen, 2023). The 25 largest vessels accounted for 81% of the total landing value of fish for reduction. Since the vessels both fish for consumption and for reduction, full-time employment is not known separately; based on landing values, it is roughly estimated at 55 persons. Catches are mainly sprat, sandeel, blue whiting, and Norway pout. Almost all is landed at the Danish fishmeal factories.

The sole application of fish for reduction is in the processing of fishmeal and fish oil in a co-production, where meals and oils are separated. Processing of fishmeal and fish oil in Denmark is shown in Table 4.5 together with landings of foreign fishers in Denmark (import) and of Danish fishers in other countries (export), of import and export of fish waste, fishmeal, and fish oil, both totally and with other Nordic countries.

Quantity (1,000 tonnes live weight) | Value (DKK Million current prices) | |

Processing | ||

- Fishmeal | 461 | 2,856 |

- Fish oil | 619 | 2224 |

Total | 1,080 | 5,080 |

Import totally | ||

- Fish for reduction | 240 | 712 |

- Fish waste | 308 | 675 |

- Fishmeal | 152 | 933 |

- Fish oil | 772 | 2746 |

Total | 1,415 | 4,406 |

Import Nordic | ||

- Fish for reduction | 162 | 506 |

- Fish waste | 238 | 418 |

- Fishmeal | 113 | 702 |

- Fish oil | 349 | 1,011 |

Total | 862 | 2637 |

Export totally | ||

- Fish for reduction | 19 | 65 |

- Fish waste | 52 | 248 |

- Fishmeal | 370 | 2,353 |

- Fish oil | 826 | 2,789 |

Total | 1,264 | 5,444 |

Export Nordic | ||

- Fish for reduction | 17 | 62 |

- Fish waste | 36 | 100 |

- Fishmeal | 197 | 1,220 |

- Fish oil | 678 | 2,296 |

Total | 928 | 3,678 |

Table 4.5: Processing, import totally and from Nordic countries, and export totally and to Nordic countries of fish for reduction, fish waste, fishmeal, and fish oil, 2023, quantity live weight and value.

Sources: Statistics Denmark (2025d-e).

Foreign fishers landed 240,000 tonnes of fish for reduction, corresponding to a value of DKK 712 million. Swedish, British, Norwegian, and Faroese vessels contribute the most. Fishers from the other Nordic countries contributed DKK 506 million (71%). Marine residues, mainly in the form of cutoffs from Danish and foreign processors of seafood for human consumption, also contribute as raw material in processing fishmeal and fish oil. Fish waste in 2023 from Danish factories was 97,000 tonnes, while 308,000 tonnes were imported mainly from Sweden, Norway, and Poland. Hence, fish waste has become an important additional raw material for processing fishmeal and fish oil, although being considered of lower quality and more expensive to process than fish for reduction. This development followed the closure of the large Danish fur industry during the COVID-19 pandemic in 2020, when fish waste was an important feed component. Hence, today, fishmeal factories buy marine residuals formerly used as mink feed.

In 2023, 152,000 tonnes of fish meal in live weight were imported for DKK 933 million, while 772,000 tonnes of Fish oil were imported for DKK 2.7 billion. The Nordic countries together accounted for 45% with Norway being the largest fishmeal and Fish oil supplier (DKK 406 million). Hence, 55% of the import value of fishmeal and fish oil originates outside the Nordic area, with the USA (DKK 377 million) and Peru (298) being the largest sourcing countries.

Two firms, Triple Nine A/S and Skagen FF A/S, with 176 employees in total, are registered as fishmeal factories. The co-production of fishmeal and fish oil amounted to 461,000 tonnes and 619,000 tonnes, respectively, in live weight. Fishmeal and fish oil are sold in large quantities to Danish fish feed firms, which produce aquaculture feed by mixing them with plant-based ingredients. Furthermore, 370,000 tonnes live weight of fishmeal and 826 000 tonnes of fish oil are exported, corresponding to a total amount of DKK 5.1 million. Salmon farming in Norway brought in DKK 3.4 billion (67%), followed by the UK with DKK 384 million (7%). The whole EU received DKK 720 million (14%), while Nordic countries together received 68%. Fishmeal and fish oil are also applied in feed mixes for pig and poultry farming in Denmark.

With 55% of imported fishmeal and Fish oil originating outside the Nordic area, with import of Fish oil being larger than domestic processing, with import of fishmeal being 41% of export, with 67% of export going to Norway and with Norwegian import of fishmeal and Fish oil from Denmark forming a substantial part of feed in salmon farming, a strong dependency of Norwegian salmon farming on fishmeal and Fish oil from sources abroad is revealed. Hence, Norwegian salmon farming is vulnerable to potential supply shortages of fishmeal and Fish oil sourced worldwide via Denmark. Moreover, around 70% of salmon feed is typically plant-based, consisting of raw materials such as soy and rapeseed. The plant-based materials and in particular soy are also mostly sourced outside the Nordic areas from countries like Brazil, the USA, and Canada, further adding to the vulnerability of salmon farming to the global sourcing of feed.

Aquaculture feed in Denmark is processed solely by the two firms BioMar A/S and Aller Aqua A/S. These two firms had a total of 178 employees in 2023 and are part of two Danish-owned groups that produce feed for aquaculture worldwide. Production data are not available, but their turnover is DKK 2.0 billion in 2023. Production is done by mixing ingredients for targeting different fish species, including salmon and trout. Feed mixes vary, but may consist of 20–40 percent fishmeal and fish oil, of which about half is produced from waste products. The rest may be plant-based products, such as soy and rapeseed. Worldwide, most fish oil and fishmeal are used as ingredients for aquaculture feed. Hence, fishmeal and fish oil can partly be substituted with plant-based products, although this may reduce the content of the healthy omega-3 fatty acids and micronutrients in the fish farmed. Since plant-based feed is cheaper than feed based on fishmeal and oil, feed with a higher content of fishmeal and fish oil is typically used in the last weeks before slaughter. This results in a high omega-3 fatty acid content in the finished product.

Fish feed is also sold to Danish aquaculture, which applied an estimated feed quantity of 31,100 tonnes in 2023. Fishmeal and fish oil are also sold in minor quantities as additives to poultry feed and feed for small pigs weighing less than 15 kg. One kilo of trout is typically raised based on 0.9–1.1 kilos of feed in freshwater pond farming and 1.1–1.3 kilos in marine farming. Hence, feed use per kilo is smaller in aquaculture than in pig- and poultry farming.

Aquatic food available for consumption in Denmark

There is no statistic on seafood consumption in Denmark, although it has been roughly estimated in a few studies. However, the main aim of these studies is not to provide an overview of fish consumption, which implies that the estimates are subject to considerable uncertainty. Hence, reliable knowledge on the consumption of seafood in Denmark doesn’t exist.

Statistics Denmark (2023c) reports that, in 2023, per capita seafood consumption, including fresh, frozen, smoked, preserved, and processed seafood, amounted to DKK 870 (excluding consumption in restaurants, cantinas, etc.). This corresponds to a total retail sale of seafood of DKK 5.2 billion. Smoked, preserved, and processed fish and shellfish account for 61% of the consumption value, while fresh fish and shellfish cover 28%. The survey does not identify consumption volumes.

EUMOFA (2025) estimates for 2022 a per capita fish consumption in Denmark of 20–25 kg in live weight equivalents based on a residual calculation.

Due to limited knowledge, seafood consumption is estimated as the residual of total supply minus exports, acknowledging the uncertainties. Total supply comes from fisheries, aquaculture, and imports. Consumption is the total supply minus exports. The calculation is made by converting all quantities into live weight equivalents and is made for groups of species, based on the numbers above. Estimated quantities supplied in Denmark and quantities available for human consumption are identified in Table 4.6, in total and per capita.

Primary production | Import | Total supply | Export | Consumption | |

Total quantities (1,000 tonnes) | |||||

Salmon and trout | 26 | 224 | 250 | 246 | 4 |

Whitefish and flatfish | 29 | 221 | 250 | 224 | 26 |

Pelagic fish | 88 | 120 | 208 | 181 | 27 |

Crustaceans and mussels | 41 | 149 | 190 | 159 | 31 |

Other and mixed | 3 | 152 | 154 | 147 | 7 |

Total | 187 | 865 | 1,052 | 956 | 95 |

Quantities per capita (kg.) | |||||

Salmon and trout | 4.3 | 37.6 | 42.0 | 41.3 | 0.6 |

Whitefish and flatfish | 4.8 | 37.1 | 41.9 | 37.6 | 4.4 |

Pelagic fish | 14.8 | 20.1 | 34.9 | 30.4 | 4.5 |

Crustaceans and mussels | 6.9 | 25.1 | 32.0 | 26.7 | 5.3 |

Other and mixed | 0.5 | 25.5 | 26.0 | 24.7 | 1.3 |

Total | 31.4 | 145.4 | 176.8 | 160.7 | 16.1 |

Table 4.6: Estimated Danish total supply and human consumption of seafood in 2023.

The total supply of seafood for human consumption in 2023 is estimated at 1,052,000 tonnes, of which 187,000 tonnes (18%) originate from domestic fisheries and aquaculture, while 865,000 tonnes (82%) are imported. Measured per capita, the average Danish seafood consumption in 2023 was 16.1 kg. per person in live weight. The crustaceans/mussels group with 5.3 kg is the largest, followed by pelagic fish with 4.5 kg and whitefish/flatfish with 4.4 kg. Per capita consumption of salmon/trout and other/mixed species is calculated to be smaller.

The total supply per capita is estimated 176.8 kg, implying that in the speculative case where the full supply is consumed domestically, seafood consumption could increase 10-fold. Moreover, in another speculative case in which trade occurs only between Nordic countries, per capita seafood consumption in Denmark could increase 8.4-fold, since 71% of imports originate from other Nordic countries.

While the finding of a secure Nordic and Danish seafood supply in times of crisis is robust, substantial uncertainty exists regarding the Danish per capita seafood consumption of 16.1 kg per person. The uncertainty is due to calculations being made on live weight, with varying conversion factors, and the exact product form not always being known. Secondly, domestic processing generates waste that may vary, leading to uncertainty. Third, since fish are used both for human consumption and for reduction, the exact amount applied for human consumption may, in some cases, be difficult to identify. Fourth, the harmonized system doesn’t, in all cases, allow for identifying species and product forms, adding to the uncertainty of conversion factors.

While reduced international trade in times of crisis can substantially affect the economics of the Nordic and Danish fishing industry, the effect on Danish and Nordic self-sufficiency in seafood for human consumption is limited. Security in the Danish and Nordic seafood supply is robust due to the very large volumes supplied. However, the salmon farming industry, especially in Norway, is vulnerable to the global sourcing of the feed ingredients fishmeal, fish oil, and soy, where a substantial part of fishmeal and fish oil is imported via Denmark.

Challenges, threats, and opportunities

More developments may negatively affect Danish seafood supply, both for human consumption and for reduction, although it is not certain whether this will occur.

The first development is the poor biological state of the most important stocks for Danish fisheries, with stock sizes below and fishing pressure above the MSY level. That accounts for both demersal and pelagic fish, crustaceans, and reduction stocks. Based on the application of the precautionary principle in fisheries management, the implication may be reduced catches over periods of stock recovery.

Second, while the Brexit agreement is in force and settles quota allocation between British and EU fishers (United Kingdom and the European Union 2020), problems for Danish fishing in the British zone persist. Currently, a moratorium on bottom trawling is in force at the Dogger Bank as part of a bird protection regulation, where a substantial share of sandeel has historically been caught. Moreover, many marine areas in the British zone are under consideration for the closure of bottom trawling due to environmental and biodiversity protection. The closures may be decided on and introduced over the coming years, potentially affecting Danish catches of demersal and reduction species.

Third, TACs for cod in the Baltic Sea are largely zero, reflecting the poor biological state of both the western and eastern stocks. Since the causes of the poor biological situation are not fully known, it is unclear whether cod fishing will reappear.

Fourth, international management agreements are currently not in force for Atlantic-Scandic herring and mackerel. The implication is that quotas have been set larger than the biological recommendation for both stocks. For mackerel, the total quota across all coastal states has, on average, been more than 40% above the biological recommendation for the past 10 years (Bjorndal et al., 2022). The consequences are that both stock size and fishing pressure are not favourable. Provided that an agreement is made, the implication may be a quota reduction over the coming years. If an agreement remains unsettled, catch rates may also fall.

Fifth, the closure of several marine areas in Danish waters is either decided or debated. An area in the Danish inner waters covering 19% of the Danish zone was decided in July 2025 and will be implemented over the next two years (Danish Ministry of Food, Agriculture and Fisheries 2025). Moreover, as part of environmental protection considerations, the closure of bottom trawling is under debate to improve marine biodiversity in Natura 2000 bird and habitat protection areas, in wildlife reserves, and in the new protected areas under the European Marine Strategy Framework Directive (Biodiversity Council, 2024ab). If decided and implemented, reduced catches from bottom trawling result.

Finally, the Green Tripartite agreement has been agreed upon in Parliament to reduce nutrient discharges. It is currently under implementation in Danish agriculture (Danish Ministry of Environment 2024). Given that nutrient discharges from agriculture will be reduced in the coming years, it is unlikely that aquaculture will be allowed to increase discharges. And growth in traditional freshwater ponds and marine aquaculture necessitates greater nitrogen and phosphorus discharges. By that, growth in the coming years will be limited to recirculated aquaculture systems and bivalve farming, sectors with smaller earnings than freshwater pond farms and marine farms.

Although not all the above developments may come true, several separate trends point towards a reduced supply of seafood from Danish fisheries, while growth in aquaculture doesn’t seem likely with the current nutrient regulation of agriculture.