3. Nordic companies and industrial projects that may lead or take part in new or better CRM-recycling operations

The Nordic fleet of base metals industries is an important platform for developing increased CRM recycling quickly. Setting up new secondary CRM-value chains from scratch has proved to be very difficult. It might be even worse in today’s market situation with Asian market dominance and unpredictable price fluctuations. New industrial enterprises often need an economic edge to succeed, either in terms of cheap and readily available raw materials, comparatively low energy price or labour costs, superior technology or expertise and so on. It is, therefore, often easier for existing companies with comparable products, processes and an existing market position to branch out from than for a start-up company to succeed at such an endeavour. An industrial company can often use in-house expertise in their planning and design of the project, raise investment capital more efficiently, and obtain necessary governmental permits and offtake agreements

Off take agreements are long-term legal contracts where a buyer undertakes to buy the future production from a supplier. Off-take agreements are an important tool for reducing financial risk when establishing new production capacities.

Sometimes it is also possible to use CRM-containing waste as additional feedstock in primary production processes, although contamination issues and technical considerations will often limit these options. In situations where CRM-containing waste streams can serve as additional feedstock in primary production processes, this may eliminate the need for additional infrastructure serving a secondary production process.

This chapter, therefore, highlights some existing Nordic industries or projects that could potentially have a role in creating new or strengthening existing secondary value chains.

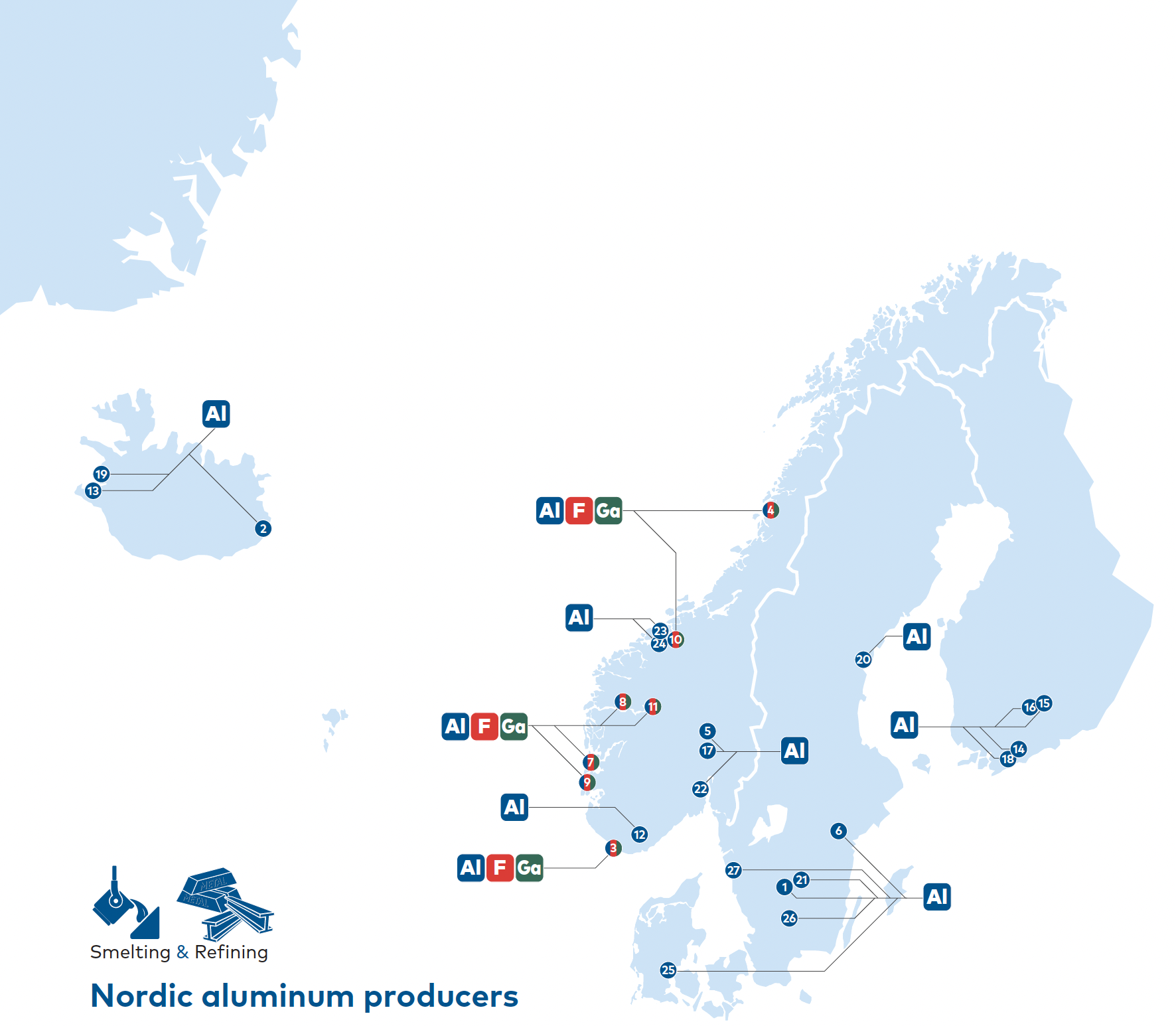

3.1 The Nordic aluminium industry

Aluminium is a CRM in its own right, but many aluminium alloys also contain other CRMs like scandium, magnesium, manganese and silicon. Better recycling solutions in this sector may, therefore, reduce supply risks for these CRMs as well as for aluminium. In addition, the aluminium oxide used as feedstock for primary aluminium production contains the CRM gallium that may be extracted from waste streams leaving the electrolytic process. During both primary and secondary aluminium processing, some aluminium oxide escapes as waste from the process. This aluminium oxide is typically lost either when it is landfilled or downcycled as a raw material in clinker production in the cement industry.

With a more circular perspective on alloy design and collection and sorting of aluminium waste streams, more aluminium can potentially be recycled, and a larger portion of other CRM-alloy components can potentially obtain meaningful roles in future product lives instead of becoming a diluted pollutant or being lost in waste streams from the recycling operation. There are also R&D initiatives worldwide to develop technologies that eliminate the need for the CRMs fluorine as a chemical input in the electrolysis process and graphite for anodes and cathodes.

There is a large Nordic aluminium industry both when it comes to primary and secondary production capacity. In addition, there are also several refineries for more advanced aluminium products. Norway has the largest production capacity for primary aluminium with five plants operated by Hydro and two plants operated by Alcoa. Iceland has three primary production plants operated by Rio Tinto, Alcoa and Norðurál. Sweden has a large primary production plant in Sundsvall operated by Rusal.

There are also many production plants for secondary aluminium in the Nordics. Most of these plants recycle a blended mix of aluminium alloys, which can lead to reduced material quality compared to primary aluminium, and also lose the utility value of much of other CRMs in the aluminium scrap used as feedstock. Better sorting of individual aluminium alloys and selective recycling of specific alloys in dedicated recycling plants could potentially reduce the CRM-loss at the end of the aluminium product life.

Norway also has a production plant for high-purity primary aluminium, the Vigeland plant. This plant refines high-grade primary aluminium from 99.7% to 99.99%, extracting typical contaminants such as iron, silicon and gallium. If feedstock for such production was changed from high-grade aluminium to 99.5% purity with high content of CRMs (such as primary aluminium from Alcoa with high gallium) or speciality alloy scrap with high CRM, the refining waste from this process might be relevant CRM-feedstocks. The competence in refining high and ultrahigh aluminium is, in any case, highly relevant to understanding possible circular value chain adaptions.

Recycling options to recover CRMs should be considered not only for aluminium scrap but also for relevant waste streams leaving the aluminium production processes. Speira operates two recycling plants for such waste in Norway. Several CRMs could potentially be recovered from these plants if additional extraction and refining units were added to the existing infrastructure.

There is also a potential for recycling waste fluorine from primary aluminium production through the aluminium fluoride production plant in Odda, currently owned by the Fluorsid group. Waste fluorine from the aluminium sector could potentially replace fluorspar imported from Morocco as feedstock to produce aluminium fluoride, although this will require some technical adjustments to the current process.

Figure 3.1 shows an overview of the Nordic aluminium industry. A detailed list of Nordic aluminium plants can be found in Annex Table 2.

Company / Potential CRM / Process / Country |

1. AB Lundbergs Pressgjuterie, Vrigstad / Al / Secondary smelter / Sweden |

2. Alcoa Fjarðarál / Al / Primary aluminium smelter / Iceland |

3. Alcoa Lista / Al, F, Ga / Primary smelter / Norway |

4. Alcoa Mosjøen / Al, F, Ga / Primary smelter / Norway |

5. Benteler Aluminium Systems, Raufoss / Al / Foundry / Norway |

6. Gränges Aluminium, Finspång / Al / Secondary smelter / Sweden |

7. Hydro Aluminium, Husnes / Al, F, Ga / Primary smelter / Norway |

8. Hydro Aluminium, Høyanger / Al, F, Ga / Primary smelter / Norway |

9. Hydro Aluminium, Karmøy / Al, F, Ga / Primary smelter / Norway |

10. Hydro Aluminium, Sunndal / Al, F, Ga / Primary smelter / Norway |

11. Hydro Aluminium, Årdal Metallverk / Al, F, Ga / Primary smelter / Norway |

12. Hydro Vigelands Brug AS Vennesla / Al / Reffinery / Norway |

13. Isal (Rio Tinto) Hardarfjördur / Al / Secondary smelter / Iceland |

14. Kuusakoski Oy, Espoo / Al / Secondary smelter / Finland |

15. Kuusakoski Oy, Heinola / Al / Secondary smelter / Finland |

16. Kuusakoski Oyj, Myllyoja / Al / Secondary smelter / Finland |

17. Metallco aluminium AS, Vestre Toten / Al / Foundry/recycling / Norway |

18. Nordic Aluminium Ltd, Kirkkonummi / Al / Secondary smelter / Finland |

19. Century, Grundartangi / Al / Primary smelter / Iceland |

20. Rusal i Kubal, Sundsval / Al / Primary aluminium smelter / Sweden |

21. Sapa (Hydro), Sjunnen / Al / Secondary smelter / Sweden |

22. Speira, Holmestrand / Al / Secondary smelter / Norway |

23. Speira, Rausand / Al / Recycling aluminium from slag and dross / Norway |

24. Speira, Rød / Al / Recycling aluminium from slag and dross / Norway |

25. Stena Gotthard, Kolding / Al / Secondary smelter / Denmark |

26. Stena Gotthard, Älmhult / Al / Secondary smelter / Sweden |

27. Volvo, Torslanda / Al / Secondary smelter / Sweden |

Figure 3.1 Overview of the Nordic aluminium industry. Illustration: Bergfald Miljørådgivere.

3.2 The Nordic zinc, copper and nickel industry

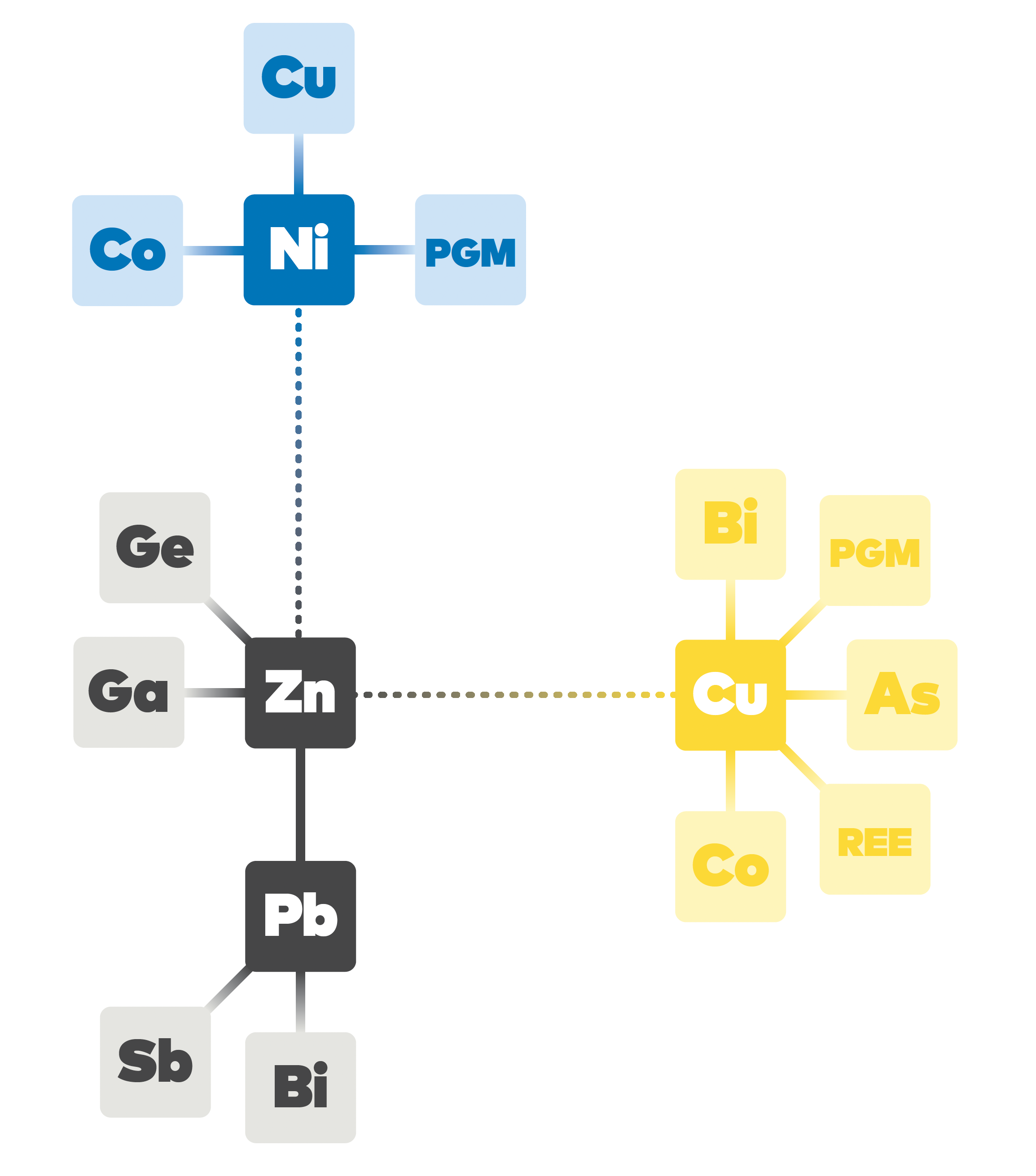

Zinc, copper and nickel are often found in overlapping ores, as illustrated in Figure 3.2, and are therefore often extracted and refined together in common industrial processes, sometimes with additional CRMs as byproducts. Because the same components are also commonly found in similar waste streams like batteries, WEEE and End-of-life - vehicles, secondary production of these CRMs together from a joint recycling operation may sometimes also be sensible. Both pyrometallurgical and hydrometallurgical technologies are used for recovering these CRMs from waste streams.

Figure 3.2 Typical elements that can often be found in common ores. As shown by the figure, the main CRM-elements Nickel and copper are sometimes associated with additional CRM-byproducts like antimony, arsenic, bismuth, cobalt, gallium, germanium, PGM and REE. Even silver, tellurium and selenium, elements that are considered CRMs by other powers than the EU, are commonly found in these ores. Illustration: Bergfald Miljørådgivere.

Boliden has a central position in the primary and secondary production of the CRMs copper, cobalt and nickel in the Nordics. The company operates several Nordic primary production plants based on mines in Sweden and Finland, including smelters in Rönnskär in Sweden, Kokkola and Harjavalta in Finland, and Odda in Norway. Boliden also has a secondary production capacity that can recover copper, cobalt and PGM in both Rönnskär where much WEEE is recycled and in the smelter in Harjavalta. Nickel and associated CRMs can be recovered in the hydrometallurgical plants at Glencore Nikkelverk in Kristiansand in Norway and Nornickel at Harjavalta in Finland. Umicore also has a large cobalt recycling and refinery plant in Kokkola, Finland. All these companies have publicly expressed interest in getting hold of more recycled feedstock.

Important Nordic mines of copper, cobalt and associated CRMs include Atik, Garpenberg, Renström, Katrineberg and Kankberg in Sweden and Terrafame and Kevitsa, Finland.

The processing of ore at Bolidens smelters generates large amounts of waste that sometimes contains recoverable residual levels of CRMs. Boliden has tested technologies for additional recovery of metals from a large waste stream called jarosite sludge, although existing market conditions have so far made the implementation of this process economically unfavourable.

An important application of copper, nickel and cobalt and, by extension, potential feedstock for recycling operations are Li-ion batteries at the end of their product life. For this reason, battery recycling operations can be seen as an integrated part of the Cu-Co-Ni value chain, although other CRMs like lithium and graphite may also be recovered from black mass from discarded batteries. Companies that operate or plan to operate battery recycling plants including Northvolt in Sweden and Hydrovolt in Norway, will extract blackmass from discarded batteries that are then processed at Nothvolt or other plants with similar recycling capacity. Terrafame operates a plant in Finland that will produce similar battery chemicals. Although Li-ion batteries contain lithium, no Nordic recycling capacity for this exists so far, although this is expected to become available in the near future. Keliber is however developing a lithium mine in Finland and considering additional technological recycling options.

Antimony is often alloyed with lead and is, therefore, indirectly recovered when lead is recycled. In the Nordics, this happens at the Boliden Bergsøe plant in Landskrona in Sweden.

Figure 3.3 shows an overview of the Nordic industry that can process copper, nickel and cobalt with associated byproducts. A detailed list of Nordic plants in this sector can be found in Annex Table 2.

Company / Potential CRM / Process / Country |

1. Boliden Aitik / Cu / Mine / Sweden |

2. Boliden Bergsöe / Sb / Secondary lead smelter / Sweden |

3. Boliden Garpenberg / Cu / Mine / Sweden |

4. Boliden Harjavalta / Cu, Ni / Smelter / Finland |

5. Boliden Kevitsa / Cu, Ni, Co & PGM / Mine / Finland |

6. Boliden Kokkola / Cu / Zinc Smelter / Finland |

7. Boliden Mines (Renström, Katrineberg & Kankberg) / Cu, (Au, Te) / Mine / Swe. |

8. Boliden Odda / Zn / Zinc Smelter / Norway |

9. Boliden Rönnskär / Cu, PGM, etc / Pri./sec. smelter w/hydrometalurgical steps / Swe. |

10. Kronos Titan / Ti / TiO2 refinery / Norway |

11. Mondo Minerals / Ni / Mine / Finland |

12. Nikkelverk, Kristiansand / Ni, Cu, Co & PGM / Hydrometallurgic plant / Norway |

13. Nordic Mining / Ti / Rutile mine / Norway |

14. Nornickel, Harjavalta / Ni, Co / Hydrometallurgic plant / Finland |

15. Pyhäsami, First Quantum Minerals / Cu / Cu-Zn Mine / Finland |

16. Sala Bly / Sb / Secondary lead smelter / Sweden |

17. Terrafame / Cu, Ni, Co / Mine, refinery (batt. chem.) black shale processing / Finland |

18.Titania / Ti, Ni Co & Cu / Ilmenite mine / Norway |

19.Tizir Titanium & Iron / Ti / Titanium concentrate / Norway |

20. Umicore Kokkola / Co, Cu, PGM / Co recycling and refinery / Finland |

21. Zincgruvan, Lundin Mining / Cu / Mine / Sweden |

Figure 3.3 Overview of the Nordic industrial plants that can process copper, nickel and cobalt with some associated CRM-byproducts. Illustration: Bergfald Miljørådgivere.

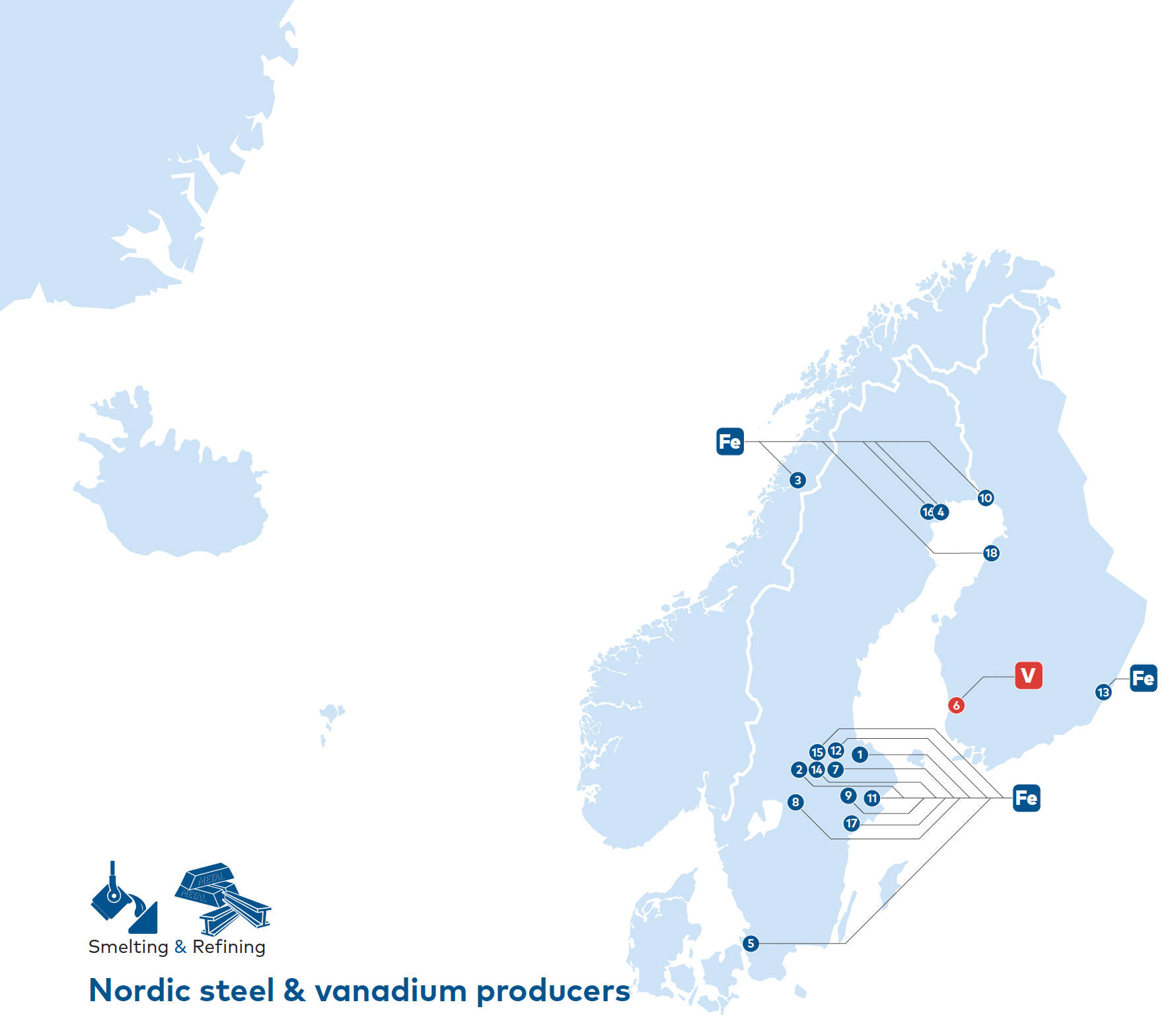

3.3 Steel industry

Steel or iron is not currently listed as a CRM in Europe.

China and South Africa classify iron ore as CRM, while some other countries are concerned with some specialty steels.

There are many steel mills in the Nordics that could potentially adopt a more alloy-specific recycling operation. Steel mills in Sweden include Outokompo mills in Avesta, Degerfors and Nyby in Sweden, and Torino in Finland. SSAB operate blast furnaces at Oxelösund and Luleå. Different levels of alloying are performed at the EAF mills in, amongst others, Höganäs, Allmeia, Björneborg, Uddeholm and Ovako. There is also a secondary steel mill in Norway at Mo i Rana (Celsa Armeringsstål). Several minor and niche operators are also active.

One example of projects aiming at CRM-recycling of steel alloy components is the vanadium project of Neometals

The Nordic steel industry also has a close relationship with producers of ferroalloys such as ferrosilicon, ferromanganese and ferrochromium. Some waste fractions might also be returned to these plants for upgrading.

It should be noted that both the global and the Nordic steel industries are undergoing a substantial transformation. The traditional large blast furnace plants based on virgin iron ore and with limited support from smaller EAF based on scrap iron are shifting towards a new model. This involves direct the reduction of pig iron plants supported by a larger fleet of EAFs for steel production. This transformation will, on the one hand, demand new and more expensive iron feedstocks but will also reduce the availability of slags. Access to higher-purity pig iron will eventually increase flexibility in steel recycling.

Rebars from scrap – the CRM end station?

Some of the lost CRMs can be found if properly investigated, such as in typical end stations such as concrete or rebars. Indeed, rebars are globally heavily based on scrap steel, and a co-dependency has developed over time between the recycling industry and the rebar industry. The rebar industry gets secure, inexpensive and relatively consistent feedstock, and the recycling industry gets a secure offtake for the fractions of scrap steel that they are not able to sell into higher-grade steel segments.

The requirements for rebars are mainly performance-based on elongation, tensile strength, etc. As such, the key international standards, such as ASTM A706, regulate the maximum levels of certain deleterious elements such as phosphorous, sulphur and copper. However, as rebars get the feedstock from mixed steel scrap, both performance-enhancing and performance-reducing alloys are included, and almost all of the periodic table is represented. When CRMs are represented in steel scrap and used in the production of rebar, it must be assumed that it is practically lost, as extraction, separation, and high grading will be very difficult.

The European production of rebars has been stable at around 12 million tonnes for many years, and we expect that this represents mostly also the consumption.

As the Nordic countries represent 10% of the European, we assume an average Nordic consumption of 1.2 million tonnes of rebars. In these rebars, approximately 3,000 tonnes of copper and 1,500 tonnes of nickel are dispersed,

Ramadan et al. Identification of copper precipitates in scrap based recycled low carbon rebar steel. Materials and design. 2017.

Odusote et al. Chemical and Mechanical Properties of Reinforcing Steel Bars from Local Steel Plants. J Fail. Anal. and Preven. 2019.

Figure 3.4 presents an overview of the Nordic steel industry that could potentially recycle steel alloy CRM-components more efficiently. A detailed list of Nordic plants in this sector can be found in Annex Table 2.

Company / Potential CRM / Process / Country |

1. Alleima / Fe / Steel production / Sweden |

2. Bjørneborg / Fe / Steel mill / Sweden |

3. Celsa Armeringsstål, Mo i Rana / Fe / Sec. steel smelter and foundry / Norway |

4. HYBRIT / Fe / Steel mill / Sweden |

5. Höganäs / Fe / Steel production / Sweden |

6. Neometals / V / Recycling V from steel slag / Finland |

7. Outokumpu Avesta / Fe / Steel mill / Sweden |

7. Outokumpu Avesta Operations / Fe / Steel production / Sweden |

8. Outokumpu Degerfors Operations / Fe / Steel production / Sweden |

9. Outokumpu, Nyby Operations / Fe / Steel production / Sweden |

10. Outokumpu, Tornio Works / Fe / Steel production / Finland |

11. Ovako / Fe / Steel production / Sweden |

12. Ovako Hofors / Fe / Steel mill / Sweden |

13. Ovako Imatra / Fe / Steel mill / Finland |

14. Ovako Smedjebacken / Fe / Steel mill / Sweden |

15. SSAB Borlänge / Fe / Steel production / Sweden |

16. SSAB Luleå / Fe / Steel mill / Sweden |

17. SSAB Oxelösund / Fe / Steel mill / Sweden |

18. SSAB Raahe / Fe / Steel mill / Sweden |

Figure 3.4 Overview of important Nordic steel mills. Illustration: Bergfald Miljørådgivere.

3.4 Silicon industry

There is a significant Nordic primary production capacity for silicon metal that currently covers 35% of the EU supply need.

Secondary silicon production is absent in the Nordics and worldwide. However, R&D efforts toward an industrial process that can recycle silicon from waste materials like discarded solar panels are ongoing, and the Norwegian primary producers may have a role in this development. Some projects are looking at recycling silicon from slag. Given the right incentives, the Nordic silicon industry, with its technology base, expertise, and market position for primary products, should have a good platform from which a secondary value chain could be developed.

As silicon is a CRM because of a certain lack of refining capacities in the IT and solar market, and not due to lack of access to the element, recycling might play a lesser role for silicon than for most other CRMs.

A new plant for recycling silicon swarf from solar cell production is under development in Norway. Silicon swarf and aluminium swarf are mixed and extruded under high pressure to an aluminium-silicon alloy.

3.5 Graphite production

Natural graphite has been mined from close to 100 Nordic locations over the last centuries, but currently, only one mine is operational – the MRC Skaland Graphite at Senja in Norway, which supplies 9% of the current European consumption.

Synthetic graphite is produced at three locations: the experienced Superior Graphite plant in Sweden and the new Vianode plant in Norway. In addition, a Chinese plant is planned in association with the Northvolt plant in Sweden.

Several companies have proposed recycling graphite from waste sources like end-of-life batteries or discarded industrial refractories.

So far, the Nordic battery recycling projects have focused on recovering metals like nickel and cobalt, but graphite recycling could become possible in future recycling solutions.

Another option is the production of synthetic graphite from CO2 or another carbon source. Bergen Carbon Solutions and Vianode are examples of start-ups developing graphite products based on this technology.

Graphite is not a homogenous commodity but is traded in different types and qualities. Graphite for advanced technological applications like Li-ion batteries require quality levels that secondary and synthetic graphite materials have struggled to reach so far. Superior Graphite is an example of a Swedish company that is working towards closing the quality gap between natural and synthetic graphite for several application areas, including batteries.

3.6 Manganese industry

Manganese can be recovered from waste streams from the production and end-of-life products like steel alloys and batteries. There is a significant Nordic primary production capacity for manganese alloys that currently covers 32% of the EU supply need.

There has until recently been a recycling plant for high-manganese steels, in Norway. While ferromanganese alloys normally have >80% Mn, and regular steels have 0.5–1% Mn, this plant operated in the niche market for 15–25% Mn-steels. However, this plant was closed in 2023. While parts of this recycling plant have already been dismantled and exported out of Europe, some parts are still left and could be restarted.

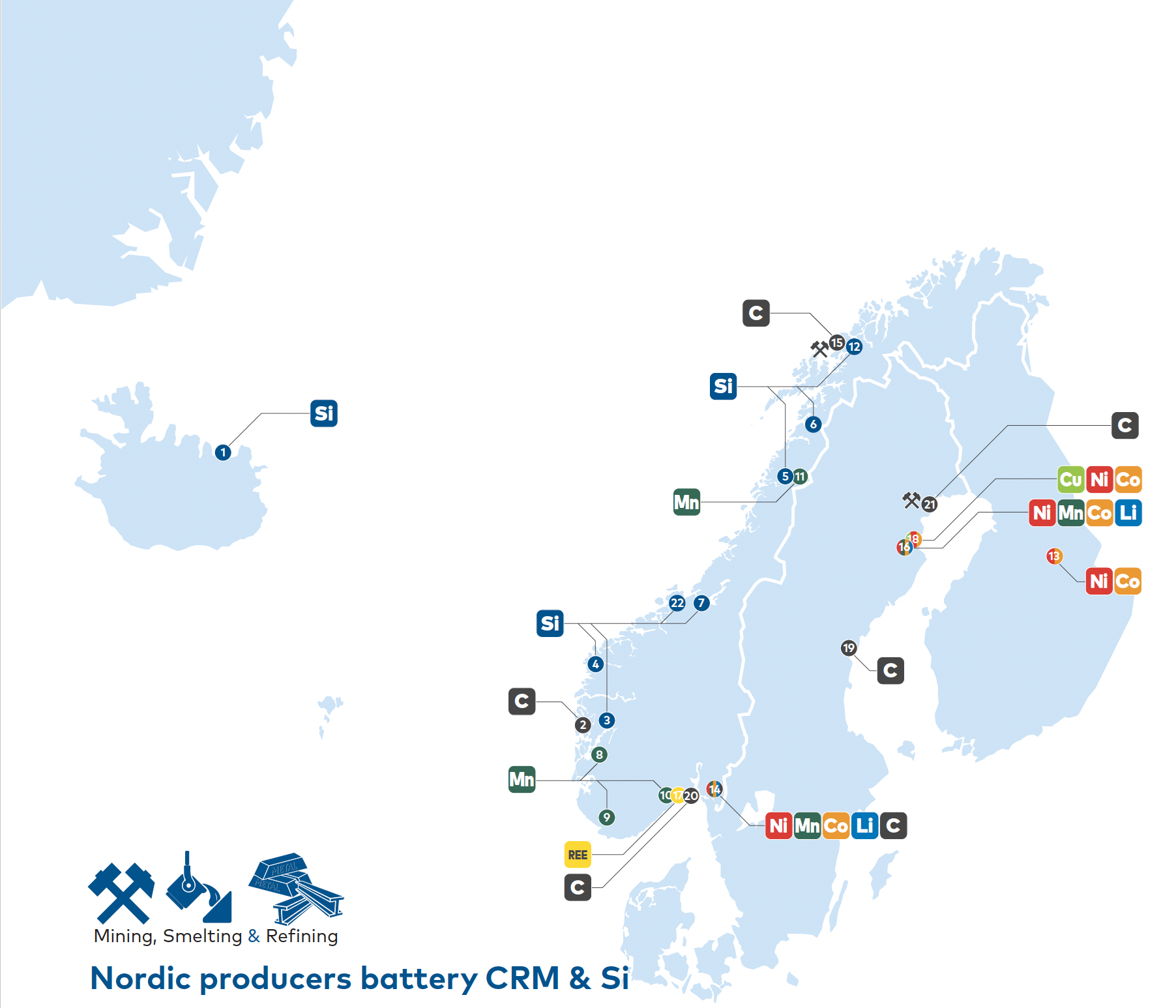

Figure 3.5 shows an overview of the Nordic industry that can process silicon, manganese, graphite and lithium. A detailed list of Nordic plants in this sector can be found in Annex Table 2.

Company / Potential CRM / Process / Country |

1. Bakkisilicon / Si / Si metal smelter / Iceland |

2. Bergen Carbon solutions / Graphite / Syntetic graphite production / Norway |

3. Elkem ASA Bjølvefossen / Si / Fe-Si & Mg-Fe-Si-smelter / Norway |

4. Elkem Bremanger / Si / Si & Fe-Si smelter / Norway |

5. Elkem Rana AS Rana / Si / Fe-Si smelter / Norway |

6. Elkem Salten / Si / Smelter / Norway |

7. Elkem Thamshavn / Si / Si & Fe-Si smelter / Norway |

8. Eramet Norway AS, Sauda / Mn / Fe-Mn smelter / Norway |

9. Eramet Norway Kvinesdal / Mn / Si-Mn smelter / Norway |

10. Eramet Porsgrunn / Mn / Fe-Mn smelter / Norway |

11. Ferroglobe Mangan, Mo i Rana / Mn / Fe-Mn & Si-Mn smelter / Norway |

12. Finnfjord, Lenvik / Si / Fe-Si Smelter / Norway |

13. FMG / Ni, Co / Battery materials (CAM and pCAM) / Finland |

14. Hydrovolt / Ni, Mn, Co, Li, graphite / Li-ion battery recycling / Norway |

15. MRC Skaland Graphite / Graphite / Graphite mine / Norway |

16. Northvolt Skellefteå / Ni, Mn, Co, Li / Li ion battery recycling / Sweden |

17. REEtec / REE / Refinery / Norway |

18. Stena Recycling / Cu, Ni, Co / Battery recycling / Sweden |

19. Superior Graphite / Graphite / Syntetic graphite production / Sweden |

20. Vianode / Graphite / Syntetic graphite production / Norway |

21. Vittangi, Talga Rescources/Talga AB / Graphite / Mine and refinery / Sweden |

22. Wacker Chemicals, Hemne / Si / Smelter / Norway |

Figure 3.5 Overview of the Nordic industrial plants that can process silicon, manganese, graphite and lithium with some associated CRM-byproducts. Illustration: Bergfald Miljørådgivere.

3.7 The phosphate industry

The largest consumer of phosphates is the agricultural sector, where phosphate is a main chemical component of synthetic fertiliser. Finland is the only Nordic producer of rock phosphate and currently supplies 18% of the European consumption from the Yara Siilinjärvi mine.

Currently, all synthetic phosphate fertiliser production is based on mined rock phosphate, imported from outside of Europe. Primary rock phosphate could, to a large extent, be replaced by secondary phosphate from mining byproducts and recycling. There is a large biogas sector in the Nordics that, through anaerobic digestion, converts different organic waste streams into biogenic methane and a phosphate-rich bio residue that is currently used locally as organic fertiliser and could potentially be utilised as a secondary phosphate feedstock for synthetic fertiliser. Another source of secondary phosphate is wastewater, where dissolved phosphate may be captured in the form of struvite as done at the water cleaning plant of HIAS in Hamar, Norway. A third source of secondary phosphate comes from ash from incineration of organic waste or biomass. Ragnsells is building a plant in Helsingborg, Sweden, based on their Ash2Phos-technology that will recover phosphate from incinerated sewage sludge.

3.8 Rare earth element production

Several new Nordic mining projects are looking at rare earth element extraction from Nordic locations, including LKAB at Per Gejer and Leading-Edge Materials at Norra Kärr in Sweden. The largest Nordic REE mineral reserves have so far been identified at the Fensfeltet in Norway, currently under development by the company Rare Earth Norway. There are also projects developing REE-recycling operations from tailings including Grangex at Grängesberg and LKAB with its ReeMap-project at Luleå in Sweden and Yara from the phosphate mine at Sillinjärvi in Finland.

Many junior mining companies talk about REE levels in their resources, but the probability of any of these coming into production is, at best, limited.

Although there is currently no Nordic REE recycling capacity from post-consumer waste streams, a LREE processing plant recently built at Herøya in Norway could potentially be expanded to produce secondary REE-concentrates. Indeed, the newly built REEtec plant has successfully tested the recycling of several post-consumer REE waste streams. However, several bottlenecks in the sorting and recovering REE-rich post-consumer wastes must be overcome before secondary materials become a relevant and significant source. Many relevant R&D projects are ongoing in several Nordic countries to overcome these constraints.

3.9 Titanium production

Some Nordic titanium alloy production capacity exists, mainly in Finland.

There is also significant production of titanium ore concentrate in the form of ilmenite (FeTiO3) produced at Titania and rutile (TiO2) produced at Nordic Mining in Norway and could serve as raw material for a Nordic titanium plant.

3.10 Platina Group Metal Production

There are several essential stakeholders in PGM production and recycling in the Nordics. Glencore in Norway and Nornickel in Finland extract and refine PGMs from imported nickel ores as byproducts. Part of the production in Finland comes from domestic concentrates. Finland also has the largest undeveloped PGM resources in the Nordic region, amongst others, and the largest and most important Sakatti mine in the north of the country.

Several companies are also active in different levels of recycling. Boliden extracts some PGMs from WEEE, as well as from mining byproducts. Most advanced is K.A. Rasmussen in Norway, with advanced recycling and processing of separated PGMs from several complex waste fractions. These plants may be expanded both in complexity and volume.