1. Introduction

Raw materials are defined by the EU as substances in the processed or unprocessed state used as input for the manufacturing of intermediate or final products. Substances predominantly used as food, feed or combustion fuel are, however, excluded from this definition and not considered as raw materials.

EU Critical Raw Material Act.

Critical raw materials (CRM) are raw materials defined by the EU as having a combination of high economic importance and significant supply risk. To mitigate future supply risks for CRMs, the EU has launched the Critical Raw Materials Act, which provides regulations to strengthen European extraction and refinery capacity. This strategy also includes increased recycling operations and the creation of a market for secondary CRM materials.

This report is the second of three reports considering how to ensure better resource efficiency regarding critical raw materials (CRM) in the Nordics. Whereas the first report presented an overview of potential recycling options for CRMs in the Nordics, this report contains an extended list of possible measures and instruments that may increase CRM-recycling in the Nordics and takes a more in-depth view of a selected number of these.

Since the first report was published in February 2024, the Critical Raw Material Act of the EU has entered into force, which means that the regulation already bound Denmark, Finland and Sweden, while Norway, Iceland and Liechtenstein are currently assessing its EEA relevance.

Article 26 of the Critical Raw Materials Act (CRMA) requires states bound by the regulation to adopt and implement a national programme containing measures designed to increase waste collection with high CRM recovery potential and ensure their introduction into the appropriate recycling system. The goal is to maximise the availability and quality of recyclable material for critical raw material recycling facilities. This report suggests possible measures and instruments to consider when designing these programmes.

It should also be mentioned that since the first report was published, the United Nations has opened a panel on critical raw materials, highlighting that CRM-supply risk is a global concern,

1.1 Scope of work

This report is the second of three reports that evaluate how Nordic countries can help the EU reach the benchmarks for a more resource-efficient use of critical raw materials (CRM) set by the Critical Raw Materials Act.

This report presents a more in-depth view of a selected number of waste streams and possible recycling options.

1.1.1 Methodology

16 measures were selected for a more thorough evaluation after a dialogue with representatives from the Nordic countries.

1.2 Recycling of critical raw materials (CRM)

The EU defines critical raw materials (CRMs) as materials of high economic importance associated with a high supply risk. The CRMA also defines a group of raw materials as strategic (SRMs). All strategic raw materials listed in 2024 are CRMs, but not all CRMs are considered strategic. Table 1.1 provides an overview of CRMs and SRMs. It summarises key applications and producing countries (including refinery capacity), and estimated total annual global production of primary CRMs. The table also includes the expected annual growth rate (CAGR) for CRM consumption and recycling rates (EOL-RIR). Additionally, Table 1.1 indicates which CRMs currently have Nordic production or recycling operations. A “YES” in brackets indicate marginal production volumes or operations in early phases.

Table 1.1 Critical and strategic raw materials defined by EU. An Asterix indicates that Nordic secondary production exists. Data source: rmis.jrc.ec.europa.eu/rmp

Critical raw materials | Strategic raw material | Applications | Largest producer inc. refining | Nordic production or recycling operations? | Global annual production 2021 (tonnes) | CAGR (%) | EOL-RIR (%) |

Antimony | No | Flame retardant, lead batteries, lead alloys, plastic, glass & ceramics | China, Tajikstan | Yes* | 94,000 | -5 | 28 |

Arsenic | No | Zn production, glassmaking, chemicals, alloys and electronics | China Peru | No | 55,000 | 3.7 | 0 |

Bauxite/Alumina/Aluminium | Yes | Automotive and other transport, construction, packaging, enginering, consumer durables | Australia, Guinea, China | Yes* | 67,669,000 | 4.3 | 21 |

Baryte | No | Drilling fluid, rubber and plastic, chemicals | India, China, Kazakhstan | (Yes)* | 8,369,000 | -2.4 | 0 |

Beryllium | No | Telecom & electronics, industrial components, aerospace & defence | USA, China | No | 272 | 0.4 | 0 |

Bismuth | Yes | Chemicals, fusible alloys, metallurgy | China, Vietnam | No | 21,000 | 1.8 | 0 |

Boron | Yes | Glass & fiberglass, frits and ceramics, fertilisers, chemicals, construction | Turkey | No | 4,920,000 | -0.2 | 1 |

Cobalt | Yes | Batteries, super alloys, hard metals, catalysts | DR Congo, China | Yes* | 166,000 | 7.3 | 22 |

Coking coal | No | Iron & steel production, industrial use, chemicals | China, Australia | No | 1,056,000,000 | 0.4 | 0 |

Copper | Yes | Construction, electronics and electrical, industrial, transport, consumer goods | Chile, Peru, DR Congo, China | Yes* | 24,949,000 | 2.5 | 30 |

Feldspar | No | Bricks & tiles, ceramics, glass | Turkey | No | 36,453,000 | 4.3 | |

Fluorspar | No | Steelmaking, fluorchemicals refrigriants & coating, primary aluminium production, | China | (Yes)* | 8,391,000 | 2.1 | 1 |

Gallium | Yes | Integrated circuits, optoelectronics, sensors, magnets, PV | China | No | 434 | 4.3 | 0 |

Germanium | Yes | Infrared optics, optical fibres | China | No | 179 | 2.6 | 2 |

Graphite | Yes | Refractories, batteries, friction material, Lubricants | China | Yes* | 1,253,000 | 2.2 | 3 |

Hafnium | No | Super alloys, plasma cutting, nuclear control rods, catalysts | France, USA | No | 70 | 0 | ND |

Helium | No | MRI &NMR, controlled athmosphere, lifting gas, analytical gas, welding gas | USA, Quatar | No | 164 MSm3 | -0.6 | 1 |

Heavy Rare Earth Elements (Dysprosium) | Yes | Magnets | China, Myanmar, Australia | Yes | 3,100 | 8.8 | ND |

Heavy Rare Earth Elements (Erbium) | No | Glass | China, Myanmar, Australia | Yes | 1,700 | 8.4 | ND |

Heavy Rare Earth Elements (Holmium) | No | Magnets | China, Australia | Yes | 400 | 3.7 | ND |

Heavy Rare Earth Elements (Lutetium) | No | Phosphors | China, Australia | Yes | 150 | 1.4 | ND |

Heavy Rare Earth Elements (Terbium) | Yes | Magnets, phosphors | China, Myanmar, Australia | Yes | 700 | 9.1 | ND |

Heavy Rare Earth Elements (Thulium) | No | Phosphors, glass | China, Australia | Yes | 150 | 3.8 | ND |

Heavy Rare Earth Elements (Ytterbium) | No | Glass | China, Australia | Yes | 1,000 | 4.8 | ND |

Heavy Rare Earth Elements (Yttrium) | No | Ceramics, phosphors | China, Myanmar, Australia | Yes | 19,000 | 7.6 | ND |

Light Rare Earth Elements (Cerium) | Yes | Catalysts (aut &FCC), metallurgical, polishing powder, magnets, glass | China, USA | Yes | 106,500 | 9.7 | ND |

Light Rare Earth Elements (Europium) | No | Phosphors | China, Myanmar, Australia | Yes | 900 | 10.6 | ND |

Light Rare Earth Elements (Gadolinium) | Yes | Magnets, metallurgical, glass, phosphors | China, Myanmar, Australia | Yes | 5,100 | 10.2 | ND |

Light Rare Earth Elements (Lanthanum) | No | Catalysts (FCC), metallurgical, polishing powder | China, Myanmar, Australia | Yes | 73,500 | 11 | ND |

Light Rare Earth Elements (Neodymium) | Yes | Magnets, catalyst | China | Yes | 47,500 | 10.3 | 1 |

Light Rare Earth Elements (Praesodymium) | Yes | Magnets, pigments, metallurgical, ceramics | China | Yes | 15,000 | 10.2 | ND |

Light Rare Earth Elements (Samarium) | Yes | Magnets | China, Myanmar, Australia | Yes | 5500 | 11.7 | ND |

Lithium | Yes | Glass & ceramics, batteries, lubricants & greases, continous casting | Australia, Chile | (Yes) | 339000 | 13.8 | 0 |

Magnesium | Yes | Automotive, packaging (Al-alloys), pig iron, construction, Mg powder | China | No | 1,057,000 | 2.5 | 7 |

Manganese | Yes | Steel | South Africa, Gabon, Australia, China | Yes | 21,219,000 | 1.8 | 9 |

Nickel - battery grade | Yes | Steel, CU-alloys, plating, batteries | Indonesia, Philipphines, China | Yes* | 2,658,000 | 5 | 16 |

Niobium | No | Steel | Brasil | No | 122,000 | 5.7 | 0 |

Phosphate rock | No | Fertilisers, food additives, detergents | China, Morocco | (Yes)* | 75,371,000 | 1.8 | 17 |

Phosphorous | No | Plastic industry, food industry, water treatment, metal treatment, pharmaceuticals | China | No | 1,156 | ND | 0 |

Platinum Group Metals (Iridium) | Yes | Electronics, chemical, medical, automotive | South Africa | Yes* | 8 | -2.2 | 16 |

Platinum Group Metals (Palladium) | Yes | Autocatalysts, electronics, chemical, dental & biomedical, jewellery | South Africa, Russia | Yes* | 318 | 0.5 | 33 |

Platinum Group Metals (Platinum) | Yes | Autocatalysts, jewellry, chemical, medical & biomedical | South Africa | Yes* | 246 | -0.7 | 25 |

Platinum Group Metals (Rhodium) | Yes | Autocatalysts, chemical, glass | South Africa | Yes* | 36 | 1.4 | 36 |

Platinum Group Metals (Ruthenium) | Yes | Electronics, chemical, electrochemical | South Africa | Yes* | 34 | -1.6 | 6 |

Scandium | No | Aluminum alloys, SOFC | China, Japan | No | 20 | ND | 0 |

Silicon metall | Yes | Aluminum alloys, chemicals, electronics | China | Yes | 3,285,000 | 4.1 | 0 |

Strontium | No | Magnets, pyrotechnics, Zn-production, alloys, pigments and fillers | Spain, Iran | No | 584,000 | 5.8 | 0 |

Tantalum | No | Capacitators, superalloys, mill products, sputtering targets, carbides | DR Congo, Brasil, Rwanda | No | 2,243 | 7.3 | 13 |

Titanium metal | Yes | Aerospace, industrial equipment, defence, consumer products | China, Japan, Russia | Yes | 244,000 | 2 | 6 |

Tungsten | Yes | Carbide, metal, alloys, chemicals | China | (Yes) | 101,000 | 3.3 | 42 |

Vanadium | No | Steel, alloys, chemicals | China | (Yes)* | 116,000 | 5.2 | 1 |

Until around 1890, more than half of the global mining production occurred in Europe. Today, although Europe accounts for only 3–4% of the global mining products, the consumption is nearly ten times greater.

Utmaningar för att möta ökade behov av metaller och mineral Rapport inom IVAs projekt Vägval för metaller och mineral, 2024.

European CRM-recycling projects face a range of challenges, including limited access to capital and uncertain, fluctuating and heterogeneous feedstock. In addition to regulatory barriers, there is a lack of necessary process technology, competence and skilled workforce. In order to increase CRM-recycling in Europe and the Nordics, these challenges must be addressed through appropriate measures and market instruments.

Recycling of CRMs means that waste streams that contain recoverable levels of one or several CRMs are collected, prepared for recycling and used as feedstock in a recycling process that recovers CRM as a new secondary raw material. The Theoretical Recycling Potential (TRP) refers to the maximum amount of critical raw material that can be recovered from a waste stream and is given as the product of the amount of available waste and the mean CRM concentration in the waste stream, as shown in the following equation:

TRP = Available waste (tonnes) X Mean CRM concentration in waste \left(\frac{kg}{tonnes}\right) (1.1)

Due to unavoidable material loss throughout the product life and waste treatment, some CRM materials will not reach recycling operations, as illustrated in Figure 1.1. Because no known recycling process achieves a 100% recovery rate due to technical and thermodynamic limitations, some CRM will also be lost during this operation. CRM-recovery rates between different stages in the product life are described by various terms, as shown in Figure 1.1, and will always be less than 100%. The relative amount of discarded products and materials collected as waste is called the End-Of-Life - Collection Rate (EOL-CR). The relative amount of waste delivered to recycling operations is referred to as End-Of-Life – Recycling Rate (EOL-RR). The relative amount of CRM recovered from the waste feedstock during recycling is called End-Of-Life - Recovery Rate (EOL-R). Finally, the relative amount of CRM that enters as a secondary material into a new product life is referred to as End-Of-Life - Recycling Input Rate (EOL-RIR). In other words, the EOL-RIR can be described as the accumulated recovery during EOL-CR, EOL-RR and EOL-R.

Figure 1.1 CRM-material loss during different stages of the product life. Illustration: Bergfald Miljørådgivere.

Measures and instruments aimed at increasing CRM-recycling should contribute to reduced material loss at one or more stages in the product life, as illustrated in Figure 1.2. For instance, reducing aluminium loss to dross in an aluminium recycling furnace is just as important for achieving the overall recycling target as increasing collection of waste feedstock. Indeed, all parts of a circular value chain require proper attention and an operational framework.

Figure 1.2 The intended effect of instruments and measures designed to increase CRM-recycling. Illustration: Bergfald Miljørådgivere.

In addition to the quantitative perspective on increasing the CRMs recovery rate, there is also a qualitative aspect where the purity of recycled materials compared to virgin equivalents are addressed. Downcycling occurs when recycling processes result in secondary products of lower quality that allow for fewer applications than their equivalent primary product alternatives. Downcycling can also result from insufficient recycling processes that cannot match the same quality as virgin equivalents or from poor sorting and pretreatment of waste material used as feedstock for the recycling operation. This is illustrated in Figure 1.3. For instance, when metal from a car is shredded initially with little or no separation of primary alloys, the material fractions that are sorted contain high levels of mixed materials and alloys. Ideally, these should be recycled separately. Instead, these mixed materials, including many CRMs, often go into a single smelting process, where most components end up as pollutants of the resulting secondary raw material or are lost in slag or other waste residues. This scenario is illustrated in the upper pathway of Figure 1.3. In contrast, if the car is more thoroughly separated into individual parts with homogenous chemical composition, as shown in the lower pathway of Figure 1.3, recycling operations can produce materials with significantly higher quality, often closer to the primary products.

Better sorting and pretreatment are often more expensive and labour-intensive as they may require manual separation or cutting of components with similar chemical compositions. They also involve removing electrical and electronic components that would otherwise be shredded with metal scrap, resulting in a mechanical mixture of various CRMs. However, improved sorting and pretreatment may significantly increase both the recovery rate and quality of recycled CRM products. Thus, measures and instruments to facilitate such a development should be considered an essential part of any CRM-recycling strategy.

A car typically consists of approximately 50 different metals, many of which are CRMs. Improved manual pretreatment prior to shredding can enhance the separation of individual alloys with distinctive chemical compositions, along with magnets and other electrical components, which should be recycled separately. Such pretreatment can also be made more effective through vehicle design that facilitates easy separation and enables straightforward removal of electrical components.

Figure 1.3 Careful sorting and pretreatment of waste used as feedstock in a recycling operation may improve the quality of resulting secondary CRM-products. Illustration: Bergfald Miljørådgivere.

*The alloys mentioned are for simplified illustration only. All alloys contain more elements, and many more alloys are used, complicating the overall picture.

Suboptimal pretreatment prevents efficient CRM-recycling in Europe and the Nordics. While more careful pretreatment is possible, technical and economic barriers currently stand in the way. Because advanced solutions for disassembly and high-quality sorting of scrapped cars, WEEE and other CRM-intensive waste streams have yet to be fully developed such operations currently rely heavily on manual labour, which is both expensive and time-consuming. Furthermore, regulatory mechanisms that compensate for additional costs regarding high-quality sorting and pretreatment have yet to be introduced, making such solutions less competitive in the market.

The two most common CRM-recycling technologies are pyrometallurgical and hydrometallurgical extraction. Pyrometallurgical extraction typically involves introducing the CRM waste, used as feedstock, into a furnace that separates the CRMs from other chemical constituents. In contrast, hydrometallurgical extraction generally entails dissolving the waste material in acid, followed by the separation of CRMs through various chemical methods. The recycling of certain CRMs can be particularly challenging compared to others. European and Nordic CRM-recycling faces limitations due to economic, technical and regulatory barriers which are summarised in the first report and will be further addressed in this report through discussions of potential measures and instruments

1.2.1 CRM-recycling benchmarks set by the EUs critical raw materials act

The Critical Raw Materials Act (CRMA) came into effect on May 23, 2024, aiming to ensure the EU access to a secure, resilient and sustainable supply of critical raw materials. Promoting resource efficiency and circularity throughout the value chains is emphasised as a central strategy towards achieving this objective.

Article 5 of the CRMA sets several benchmarks for future CRM production capacities in the EU, covering CRM extraction, processing and recycling. As illustrated in Figure 1.4, by 2030 EU’s CRM-extraction capacity shall meet at least 10 % of its total annual consumption of strategic raw materials (see Table 1.1 for CRMs). Within the same timeframe, EU processing capacity, including all intermediate steps, must account for at least 40% of its annual consumption of strategic raw materials. At the same time, the EU must establish a recycling capacity capable of meeting at least 25% of its annual SRM consumption, also considering all intermediate recycling steps.

Figure 1.4 CRMA capacity benchmarks for SRM-value chains within 2030. Illustration: Bergfald Miljørådgivere.

Figure 1.5 provides an overview of the current recycling status for various critical raw materials compared to the 25% capacity goal set for 2030. Although all CRMs are included in the illustration, the capacity goal specifically applies to the CRM subgroup of strategic raw materials (SRMs). The diagram indicates that only four CRMs currently meet the 25% capacity requirement: tungsten, copper, PGMs and antimony.

Antimony has its high recycling rate due to its use as alloying element in lead accumulators. Extraction of pure antimony from lead is costly and current not performed in Europe.

When considering CRMs that currently lack established recycling options in Europe, it is important to understand that absence is often due to unfavourable market conditions, which make such operations unprofitable. However, in some cases, it stems from the lack of commercially viable recycling technologies, meaning no recycling operations can be established, even with political mandates. For secondary CRM value chains where relevant process technology is unavailable, substantial R&D efforts will be necessary to develop these solutions.

Figure 1.5 Current EOL-recycling input rates compared to the CRMA 25% recycling benchmark for 2030. Data source: rmis.jrc.ec.europa.eu/rmp. Illustration: Bergfald Miljørådgivere.

Compared to more developed secondary CRM value chains that currently maintain a relatively high rate of CRM-recycling, less developed secondary CRM value chains may require distinct support mechanisms to reach the CRMA 25% recycling benchmark, as illustrated in Figure 1.6.

The 25% benchmark in CRMA formally only applies to strategic raw materials which per 2024 includes bismuth, boron, cobalt, copper, gallium, germanium, lithium, magnesium, manganese, natural graphite, nickel, PGMs, magnetic REE, silicon- and titanium metal and tungsten. All these materials are also classified as critical. CRMA does however encourage increased recycling for all critical raw materials, and the 25% benchmark can therefore be used as a voluntary target, although not legally binding.

For secondary CRM value chains with limited process capacity, the main strategy would likely benefit from focusing on identifying and demonstrating the best available recycling technology options and supporting recycling projects in the early development phases.

For CRMs and relevant waste streams where no recycling technology is currently available, substantial R&D efforts should be prioritised to drive innovation in this direction.

MATURE VALUE CHAINS | VALUE CHAINS UNDER DEVELOPMENT | NO EUROPEAN RECYCLING | |

✓ Support and further develop the existing recycling industry | ✓ Pilot and demonstrate available recycling technology | ✓ R&D efforts for the development of new recycling technology | |

✓ Improve the collection and sorting of waste streams that are raw material for this recycling | ✓ Improve the collection and sorting of waste streams that can be recycled outside the Nordic region | ✓ Prepare collection arrangements for waste streams that can be raw material for future recycling |

Figure 1.6 Different perspectives and considerations when designing support mechanisms for individual secondary CRM-value chains that differ in development maturity. Illustration: Bergfald Miljørådgivere.

1.2.2 Other EU-legislation with impact on CRM-recycling

In addition to the CRMA, several other EU regulations affect the framework conditions for CRM recycling. The most critical regulations in this regard are the following:

- Waste Framework Directive

- Extractive Waste Directive

- WEEE Directive

- Battery Directive

- End of Life Vehicle Regulation

- The Eco-design for Sustainable Products Regulation (ESPR)

Waste Framework Directive

The European Waste Framework Directive sets the basic concepts and definitions related to waste management. It requires a national waste policy where these treatments are given priority according to the waste hierarchy. The directive lists the following methods as part of the hierarchy:

- prevention

- preparing for re-use

- recycling

- other recovery, e.g. energy recovery

- disposal

The directive requires member states to take measures to encourage the options that deliver the best overall environmental outcome.

The directive also defines the boundaries between waste and by-products while proposing guidelines for End of waste criteria. These are significant for CRMA-recycling and secondary CRM products, as they establish quality standards for when recycled CRMs from waste can be considered a secondary product.

The directive also provides overall guidelines for Extended Producer Responsibilities (EPR), which regulate the EPR schemes that are responsible for important CRM-waste streams like scrapped cars, WEEE and batteries. Additionally, individual EPR schemes are governed by more specific regulations found in separate EU directives.

The directive requires member states to establish national waste management plans that include measures to improve environmentally sound preparations for re-use, recycling, recovery and disposal of waste. These measures will clearly overlap with the national program for CRM recycling and other risk-reducing measures for CRM supply lines. As a result, both plans may be integrated into a single document.

Unlike EU regulations like the Battery Directive or CRMA, the Waste Framework Directive does not include substance-specific recycling benchmarks for individual chemical elements. Instead, it focuses on more broadly defined waste categories such as plastic, metals and others.

Extractive Waste Directive

While the Extractive Waste Directive mainly focuses on the safe disposal of non-useable minerals, the directive also requires operators to perform proper characterisation of the composition. Minor concentrations of CRM minerals may occasionally be present in extractive waste. Thus, such characterisation is the first line of defence to prevent landfilling of CRMs that could be extracted. The directive also emphasises that the recovery should be a focus of all extractive waste management plans.

WEEE Directive

The first version of the WEEE Directive entered into force in 2003 and has since been updated several times. The EU is currently evaluating the need for further revisions.

The directive describes required measures to reduce the adverse impacts of the generation and management of Waste from Electrical and Electronic Equipment (WEEE). The directive covers regulations regarding product design, waste collection and collection rates, treatment facilities and recovery rates. The current version of the directive contains overall benchmarks for recovery and preparation for reuse and recycling. However, unlike the Battery regulation and ELV regulation, recycling benchmarks for specific CRMs are not included.

The Battery regulation

On August 17th 2023, the new Batteries Regulation of the EU entered into force, thus replacing the Battery directive from 2006.

The regulation applies to all categories of batteries, including portable batteries, Starting, Lighting and Ignition batteries (SLI batteries), Light Means of Transport (LMT) batteries, electric vehicle batteries and industrial batteries. It also covers batteries that are incorporated into or added to products, or that are specifically designed to be incorporated into or added to products.

Article 11 of the regulations introduces requirements for the removability and replaceability of portable batteries and LMT batteries. These requirements will also benefit CRM-recycling operations as they allow easier and more cost-effective dismantling of the battery component from the product. Furthermore, they prohibit the use of welding and glued connections, which make disassembly challenging and time-consuming.

The regulation also contains requirements for minimum shares of secondary CRM-battery materials like lithium, cobalt and nickel in new batteries that are placed on the European market.

Article 70 prohibits end disposal like landfilling or incineration, which render discarded batteries unavailable for recycling. In contrast, Article 71 outlines benchmarks for the efficiency of recycling and the recovery of materials in battery recycling operations. Within 2027, all European battery recycling operations are required to achieve a recycling efficiency of at least 90% for cobalt, copper and nickel, and 50% for lithium. By 2030, these requirements will be increased to 95% and 80%, respectively.

The Battery regulation also requires all batteries above a minimum size to be associated with a battery passport that is interoperable with other digital product passports required by the Eco design directive. The passport and battery labelling will include information about CRMs present in the battery.

End-of-Life Vehicle Regulation

The End-of-Life Vehicle Regulation (ELV Regulation) contains regulations regarding the treatment of scrapped vehicles and their components. It includes circularity requirements related to the design and production of the vehicles, focusing on aspects such as reusability, recyclability and recoverability. Furthermore, the regulation mandates the use of recycled content, which must be verified during the type-approval process of vehicles. It also outlines information and labelling requirements for parts, components and materials used in vehicles. The regulation lays down requirements on extended producer responsibility, as well as the collection and treatment of end-of-life vehicles, including the export of used vehicles from the EU to third countries. Among these requirements are design standards that facilitate the easy removal and replacement of recyclable parts and components, as well as the mandatory removal of certain parts and components to enhance the efficiency of CRM recycling.

Article 4 of the regulation requires new vehicles to be designed and constructed to allow for reuse or recycling to a minimum of 85% by mass, and recovery of at least 95% by mass. Article 6 states that, following a feasibility study, the Commission may introduce minimum recyclability shares for CRMs such as aluminium, magnesium and REE in the coming years.

Article 13 requires all new vehicles to have a digital passport similar to equivalent passports required by the Battery Directive and Eco-design regulation.

A proposal for a revised directive was presented in 2023 and has yet to be adopted. The proposal is supposed to replace not only the existing ELV directive but also several other directives, including the Directive on the type-approval of motor vehicles regarding their reusability, recyclability and recoverability.

The Eco-design for Sustainable Products Regulation (ESPR)

The Eco-design for Sustainable Products Regulation (ESPR) entered into force on July 18th 2024 and is the primary legislative initiative of the EU towards more environmentally sustainable and circular products.

The regulation defines Eco-design as the integration of environmental sustainability considerations into the characteristics of a product and the processes taking place throughout the product’s value chain.

The regulation provides a framework for eco-design requirements that products must fulfil to be placed on the European market or put into service. The regulation also provides guidelines for a digital product passport and mandatory green public procurement requirements. The regulation also sets up a framework to prevent unsold consumer products from being destroyed.

The ESPR requires that products, components and materials covered by the regulation be associated with a digital product passport. This passport must contain accurate, complete and up-to-date information as described in ESPR and its delegated acts. The goal is to support the sustainability and circularity of the products while also strengthening their legal compliance. The information included will cover manuals on disassembling products for repair and recycling. A final and detailed description of the required data for the digital passport will be provided by the EU Commission at a later stage.

- Product’s technical performance

- Materials and their origins

- Repair activities

- Recycling capabilities

- Lifecycle environmental impacts

CRM recycling is often limited by incomplete information about the chemical composition of waste materials. The best possible treatment of these materials is to achieve optimal CRM-recovery safely. A digital passport can potentially be an important tool for better sorting and recycling procedures by making this information more readily available.

1.3 Socio-economic consequences of CRM-recycling

CRM recycling has socioeconomic effects on many levels of society. The most important of these is the potential for increased self-sufficiency in recycled materials. Without access to the critical raw material, modern society, as we know it, would face severe disruptions. Key sectors such as electronics, transportation, industry and defence would come to a standstill. Recycling CRMs will reduce the risk and consequence of external supply limitations. Indeed, increased CRM-recycling will make society safer and more resilient, reducing stress and uncertainties of the future.

Raw materials carry a societal significance comparable to energy, as they are the building blocks that all products and materials around us are based on. Without raw materials, there are very few ways to utilise energy. Access to enough necessary raw materials is therefore essential for sustained industrial production and value creation, as well as to ensure that crucial human needs can be met and critical welfare schemes can be upheld.

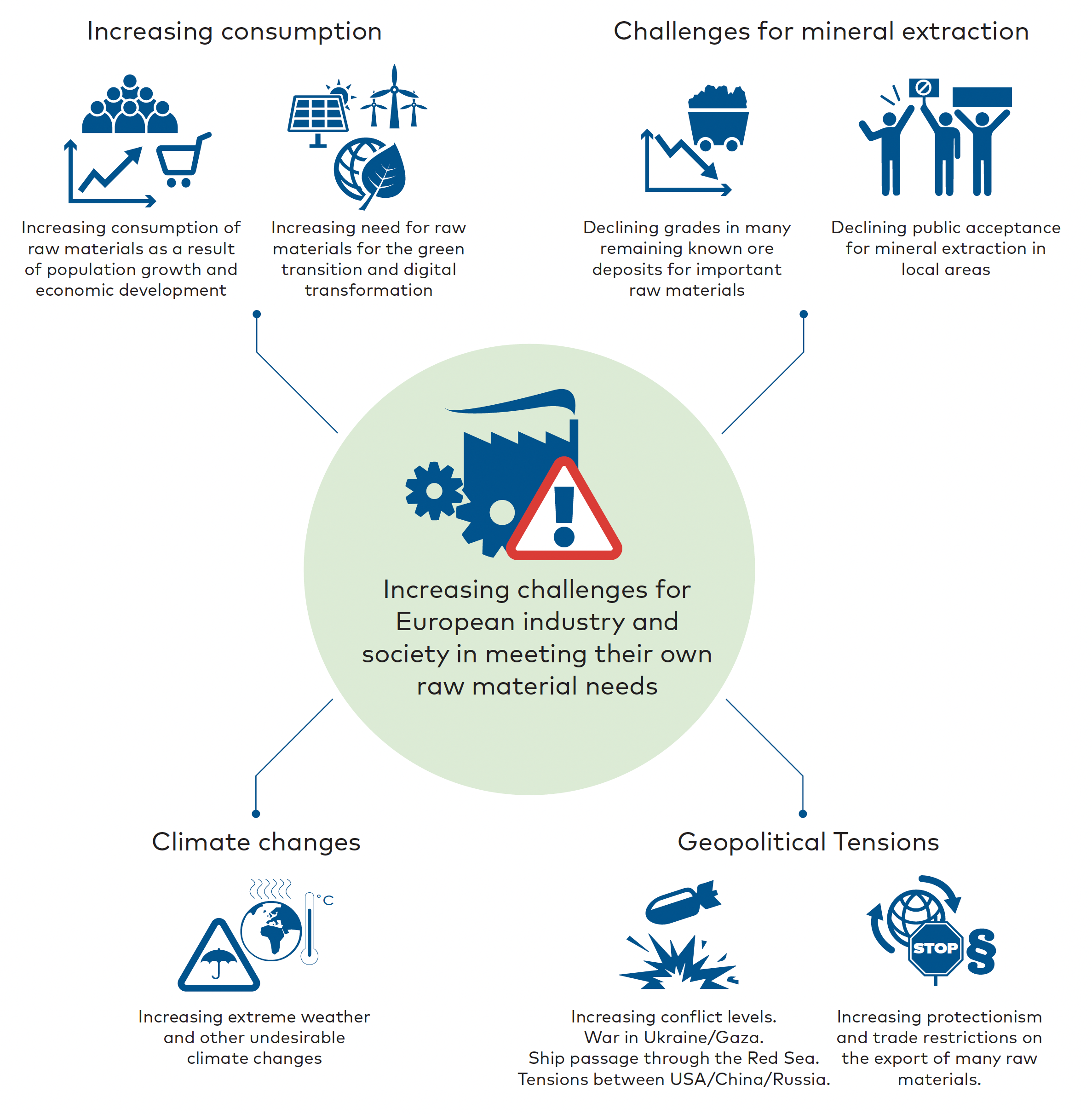

Since the EU first announced its plan to introduce a regulation on CRMs in 2023, the rationale for increased efforts towards reducing CRM supply risks is becoming even more abundantly clear. Modern society relies heavily on products and services that require CRMs as an input, and a disruption in the value chains that supply these CRMs will damage downstream industries that require CRMs as feedstock for further production and may lead to disruption or collapse in living conditions and welfare schemes that are expected in modern society. Figure 1.7 summarises factors that are causing increased supply risks for most CRMs.

Figure 1.7 Factors that is causing increased CRM-supply risks. Illustration: Bergfald Miljørådgivere.

As the global human population and the GDP of most countries continue to grow, CRM consumption increases correspondingly. This CRM consumption growth is accelerated further by technology shifts regarding the de-fossilisation and digitalisation of the economy, which both require increased CRM inputs compared to the technology platforms they replace. Renewable energy production like wind turbines and solar panels, together with electrification of the transport sector, is expected to multiply the need for CRMs such as silicon, gallium, lithium, nickel and rare-earth metals in the coming years. In contrast, the current consumption rates are far beyond the expected growth rate of many other raw materials.

At the same time, because the extraction of minerals for economic reasons is always based on the richest available ores, over time, this leads to decreasing CRM levels in remaining ore reserves, increasing relative costs and environmental footprints for future primary CRM production.

There is also a declining social acceptance of mining operations in many countries, not only in the developed world but also in several countries that today are crucial providers of many CRMs. Another supply concern is increasing protectionism and trade restrictions on exporting raw materials from important suppliers of CRMs. Taken as a whole, this situation would alone be cause for high concern but is aggravated further by ongoing wars in Ukraine and the Middle East, together with rising tensions between China, Russia and the US leading to a destabilised security situation and threatened trade routes like the important passage through the Red Sea. Increasing extreme weather and other undesirable climate events can also be added to the list of issues that threaten future CRM supply.

1.4 Environmental consequences of CRM-recycling

CRM-production at different stages of the value chain creates impacts on the environment that may be climatic or affect water, soil, fauna or flora, and these effects must be considered when setting up new or expanding existing CRM value chains. Although the production of both primary and secondary CRMs has unfavourable or detrimental environmental impacts, the overall footprint of primary production will most often be more extensive than that of similar amounts of secondary CRM.

A quantitative comparison of the total environmental footprint from primary and secondary CRM-production for a specific CRM is possible through a life cycle assessment. However, this requires knowledge about what type of technology and process techniques are applied at each step for both value chains and involves complex calculations that go beyond the mandate of this project. Some semi-quantitative statements can be made, though, regarding differences in environmental footprints between value chains for primary and secondary CRMs.

The negative from the secondary CRM-production footprint is mainly due to the consumption of energy and chemicals used as input during the collection and preparation of selected waste streams and later during the recycling process, in addition to emissions and waste materials generated during the same process steps.

Unlike the production of secondary CRM, almost all primary CRM materials are based on ore mining and processed through a series of steps that include ore dressing and further refining. For many CRMs, the materials are extracted as a byproduct to a primary ore, such as gallium from aluminium ore or germanium from zinc ores, which limits process parameters and volumes to the primary ores (in the mentioned examples; aluminium and zinc). Mined mineral ores often disrupt large areas, both during ore excavation and later when waste minerals from ore dressing are deposited in landfills.

Landfilling waste minerals covers areas where immobile biological life will be eliminated when buried in sediments. Mineral particles from the landfill may also be transported to the surroundings and cause unwanted effects. Particle loss may happen through dust dispersion, run-off water or dam failure.

Run-off water is sometimes acidic and may contain dissolved heavy metals and residual chemicals from the ore dressing process. Mining operations also often require a large consumption of water and chemicals and much energy to move, crush and mill the ore, as well as to separate valuable minerals from the remaining waste minerals.

Processing ore concentrate through either pyrometallurgical, or hydrometallurgical methods requires substantial energy inputs (often both electricity and coal/coke) and chemicals, generating significant waste in the form of slag and dust that must undergo waste treatment. Hydrometallurgical processes typically consume less energy than pyrometallurgical methods but may be chemical-intensive. Pyrometallurgical processes, however, also require chemical inputs such as flux and slag formers.

When secondary CRMs replace primary CRMs, the environmental footprint of primary production is eliminated and typically replaced by a smaller footprint from secondary production processes. Collecting and preparing waste streams for CRM recycling may require additional energy compared to the standard end treatment for these wastes. However, recycling generally reduces the amount of residual waste needing landfilling and, if it replaces incineration, eliminates related emissions and ash production. While the CRM recycling process consumes significant amounts of energy and often chemicals, these requirements are typically much lower than those of primary production. For instance, secondary aluminium production consumes only about a tenth of the energy required to produce the same amount of primary aluminium. The exact environmental footprint of a specific CRM-recycling process depends on various factors, including the type of CRM being recycled, waste feedstock, the technology employed, and the quality standards of the final product.

Just as many virgin ores are contaminated with environmental toxins, so are many fractions of secondary CRMs. WEEE commonly contains high concentrations of lead and minor levels of beryllium, thallium and mercury. Post-consumer products may contain organic toxins, asbestos, microplastics, synthetic rubber and other materials. These undesirable elements and contaminants may influence the processing of CRM-rich waste but can also result in local emissions or the formation of hazardous waste.