4. The future of Nordic fisheries

Commercial capture fisheries play a central role in the Nordic blue economy (Sepponen et al., 2021; ICES, 2025a). The region ranks among Europe’s leading seafood producers, with capture fisheries providing essential contributions to food, culture and trade. By mid-century, fisheries in the Nordics will likely experience large changes, as the ecosystems respond to cumulative environmental changes caused by climate change and a variety of human activities at sea (see Chapter 3). This chapter presents an outlook for the Nordic fisheries, outlining key trends, opportunities, and barriers.

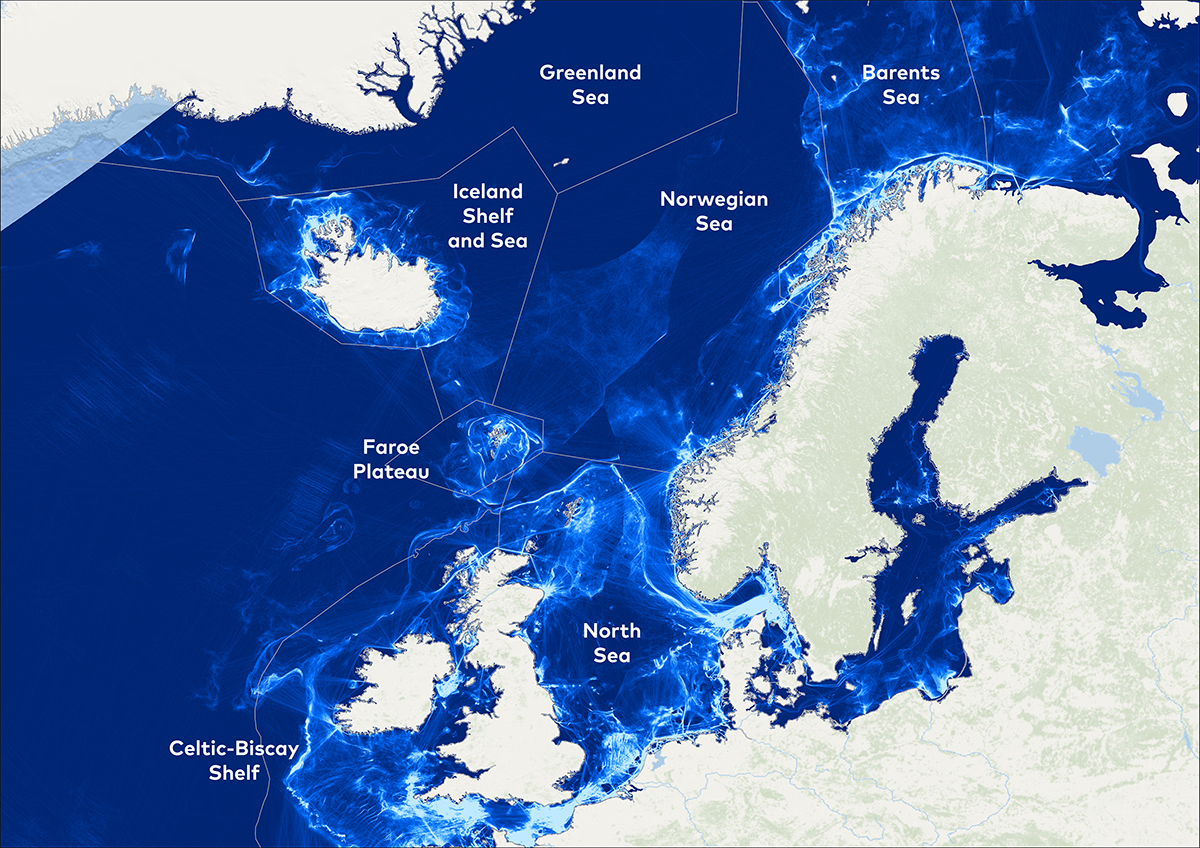

Figure 4-1 maps fisheries activity in the Nordic sea areas in 2024, excluding Greenland, based on AIS (automatic identification system) data. Key fishing hot spots include the waters offshore Iceland; on the Faroe Plateau; in the heavily trawled Kattegat and Skagerak areas between Denmark, Norway, and Sweden; in North Sea fishing grounds in Danish and Norwegian waters, including along the Norwegian trench; and along the coast of central and northern Norway and into the Barents Sea.

Figure 4-1 Overview of 2024 fishing activity in the Northern European and Nordic large marine ecosystems, excluding Greenland

4.1 Fisheries in the Nordic countries

4.1.1 Trends in production

In 2022, the Nordic region produced nearly 5.7 million tonnes of seafood through fisheries (FAO, 2025c). All Nordic countries contribute to fisheries production, but the leading producers by weight and landed value are Norway and Iceland (Figure 4-2). Nordic production by weight has gradually decreased in recent years but the trend varies by country. Since 2000, production by weight has generally decreased in Denmark, Iceland, and Sweden, and increased in the Faroe Islands, Greenland, and Åland (FAO, 2025c; ÅSUB, 2025). In contrast, production by value has generally increased for all Nordic countries except Denmark (Pauly et al., 2020).

Between 2019 and 2024, the catch value of Icelandic fisheries increased 12.45% (Statistics Iceland, 2025b). During this period, the value of Norwegian fisheries exports increased 45.8% (Norwegian Seafood Council, 2020, 2025a). This trend suggests that Nordic fisheries are generating more economic value per unit of catch, despite overall volume reductions. It is also a signal that fish supplies generally do not keep up with increases in seafood demand, leading to higher sales prices, and providing excellent conditions for aquaculture to meet unmet demand for fish (see Chapter 5).

Nordic fisheries production is closely tied to the species being caught. According to the UN Food and Agriculture Organization's (FAO) capture fisheries data collection for Nordic countries, over 300 distinct common names are recorded, highlighting the diversity of landings in the region (FAO, 2025c). These species span categories including pelagic fish, demersal fish, crustaceans, and seaweed. Despite this diversity, Nordic fisheries production is dominated by several main species, many of them pelagic (Figure 4-3). Some of the pelagic species driving production by weight include Atlantic herring, blue whiting (Micromesistius poutassou), capelin (Mallotus villosus), and Atlantic mackerel. The demersal species Atlantic cod also makes significant contributions to the overall production by weight. Some of the main species driving production by value include Atlantic cod, Atlantic herring, Northern prawn (Pandalus borealis), Atlantic mackerel, and Saithe (Pollachius virens).

Figure 4-2 Production of Nordic capture fisheries by weight, 2000–2023 (FAO, 2025b), and value, 2000–2018 (Pauly et al., 2020)

Source FAO (2025b); Pauly et al. (2020)

Figure 4-3 Production of Nordic capture fisheries by weight (million tonnes) since 2000 for a selection of key species (FAO, 2025c), by weight (FAO, 2025c) or value (Pauly et al., 2020)

Source FAO (2025c); Pauly et al. (2020)

Trends in Nordic fisheries production are shaped by factors such as stock dynamics, fisheries management practices, and socioeconomic and technological changes. The following examples illustrate how some of these elements have influenced catch trends across different Nordic regions and species.

Blue whiting catch decline and sustainability setbacks: Across the Nordics, blue whiting production by weight declined significantly between 2003 and 2011, primarily due to poor recruitment and high catches (Figure 4-3; Payne et al. 2012). Although catch volumes later rebounded following improved recruitment, persistent overfishing beyond scientific advice, driven by quota disagreements, led to the loss of Marine Stewardship Council (MSC) certification (Marine Stewardship Council, 2024).

Shifting targets in Åland fisheries: During the early 2010s, Åland commercial fisheries underwent a notable shift in focus, moving predominantly away from cod and toward herring and sprat (ÅSUB, 2025). This transition reflects a broader trend across the Baltic Sea, driven by a decline in the cod stock and a parallel regime shift towards increased predominance of small pelagic species like herring and sprat (see Chapter 3).

Blue mussel fishery reform in Denmark: Denmark, the heart of the Nordic blue mussel (Mytilus edulis) fishery, experienced a 77% reduction in mussel catches between 2001 and 2010. This transition reflects a series of actions undertaken by the fishery to achieve MSC certification, which occurred in 2010 and has since been maintained (Marine Stewardship Council, 2025).

4.1.2 Fleet structure and gear use

The structure of the fisheries sector has undergone significant changes over the previous decades, marked by substantial reductions in the size of the European fishing fleet. Between 2008 and 2023, vessel numbers fell 27% in Sweden, 27% in Finland, and 36% in Denmark (European Commission, 2024d). In Norway, the number of registered vessels declined by around 19.3% during the same period (Norwegian Directorate of Fisheries, 2025c), except for industrial fishing vessels, whose number increased more than 20%. In Iceland, the number of fishermen has decreased approximately 30% since 2000 (Statistics Iceland, 2025a), while in Norway, the decline is closer to 50% (Norwegian Directorate of Fisheries, 2025d).

The changes in the structure of the fisheries industry are also observed in the use of fishing technology. Due to the geographical and ecological differences as well as culturally specific techniques, fishing practices vary widely across the Nordic region in terms of techniques used and species targeted. Figure 4-4 shows the development in catch from 2004 to 2019 for the three most common gear types; bottom trawling, pelagic trawl, and purse seine.

While producing protein with a low-carbon footprint relative to other food sources, the fisheries are also under increasing pressure to decarbonize, including calls for renewing the fleet with vessels operating on alternative fuels (see also Chapter 7). In the EU, fishing vessels are exempt from the Emissions Trading System (ETS), which applies to most cargo vessels (DNV, 2025c). In Norway, the planned introduction of a carbon dioxide (CO2) tax for fisheries was recently delayed following protests from the fisheries organizations. The Norwegian fisheries organizations argue that the tax would risk putting the industry at a competitive disadvantage relative to EU fishermen (Fiskebåt, 2023).

Figure 4-4 Production of Nordic capture fisheries for main gear types by weight (million tonnes) and value (billion 2024 euros) from 2004 to 2019

Source Pauly et al., 2020

We make two corrections for outliers in this data set: 1) Icelandic pelagic trawl landed values are presented without outliers for ‘high seas’ catches in 2018 and 2019; 2) Norwegian blue whiting catches are corrected by being reassigned from bottom trawl to pelagic trawl after 2010, which is the gear specified before 2010.

4.2 Trade patterns for Nordic fisheries products

Nordic capture fisheries are a huge source of export revenue for the economies of Greenland, the Faroe Islands, and Iceland, and are a considerable contributor to Norwegian exports. For Greenland, wild-caught fish alone account for more than 90% of national exports by value, a large share being unpeeled shrimp, indicating a large economic dependency on fisheries, and low maturity in the processing sector (Hendriksen and Hoffmann, 2025). The Faroe Islands has been able to reduce its dependency on wild-caught fish through scaling of aquaculture and fish processing, but seafood overall still contributes more than 90% of Faroese exports by value (Statistics Faroe Islands, 2023; Hendriksen and Hoffmann, 2025).

Figure 4-5 shows the trade flows of seafood from the Nordic region to the 15 biggest importer markets in 2023 (the rest of the world is also included as a separate entry). Figure 4-5 intentionally excludes seafood products from salmon and trout aquaculture but includes fish feed ingredients like fish oil and meal, and fish waste products. Norway, Denmark, Iceland, and the Faroe Islands were the biggest exporters in absolute terms, with Denmark and Norway as the largest destinations. Denmark is a net importer but plays a key role in fish processing and production of marine ingredients for fish feed used in aquaculture (see trade flow from Denmark to Norway). Besides trades internally in the Nordic region, the largest trading partners are China and a variety of European countries.

Figure 4-5 Most important export destinations (right) for wild caught fish from the Nordic countries (left) in 2023, measured by weight, including exports to unknown destinations 'Other NEI' ('not elsewhere included')

Source FAO, 2025b

4.3 Opportunities and barriers

4.3.1 Growth opportunities for Nordic fisheries

Globally, wild-capture fisheries have plateaued since the 1980s, with most increases in aquatic food supply coming from aquaculture (FAO, 2024). The Nordic region reflects this trend: while capture fisheries remain economically and culturally important, future growth in seafood supply will largely originate from aquaculture expansion.

Sustainability, marine conservation and restoration: For capture fisheries, adequate management of fish stocks generally represents the most reliable avenue for growth and resilience (FAO, 2024; Costello et al., 2016; 2020). Marine protected areas (MPAs) and seasonal closures can provide additional benefits, where the clearest effects are seen for local or more sedentary species (Halpern and Warner, 2002). Spatial closures are less effective for highly mobile stocks unless vast areas are covered. This is shown by the limited outcomes of the ‘plaice box’ and ‘Norway pout box’ in the North Sea, two spatial closures designed to reduce bycatch and protect juvenile fish (Pastoors et al., 2000; ICES, 2017).

Diversification into new species: Novel resources such as mesopelagic fish and Antarctic krill are currently explored as potential ‘new’ fisheries resources (Fjeld et al., 2023; Grimaldo et al., 2020). The Northeast Atlantic mesopelagic biomass is estimated to be large (Hidalgo and Browman, 2019; St. John et al., 2016), and exploratory surveys have identified species with commercial potential. However, their ecological roles in marine food webs are poorly understood, and any development would require precautionary, ecosystem-based approaches to their management and new harvesting technologies (Olson et al., 2016).

Climate-change driven redistribution Climate change is already reshaping Nordic fisheries by driving poleward shifts in commercially important species (Pinsky et al., 2020). This has created both opportunities and governance challenges, exemplified by the Northeast Atlantic mackerel dispute, where shifts in stock distribution led to contested quota allocations (Spijkers and Boonstra, 2017; Østhagen et al., 2022). Anticipatory and flexible governance, including adaptive harvest control rules, transboundary cooperation, and dynamic spatial management, will be essential to ensure redistributions can be harnessed rather than destabilizing fisheries. If stocks expand northward, catches could increase in Arctic waters. The potential for growth in fishing activity in new Arctic areas needs to be approached with extreme caution due to limited knowledge about the ecosystem impacts. International agreements take a precautionary approach to fisheries in the Central Arctic (currently covered by sea ice); The International Agreement to Prevent Unregulated Fishing in the High Seas of the Central Arctic Ocean prevents commercial fishing in this area until 2037 by the signatory states, including Denmark, Iceland, Norway, and the EU (Arctic Council, 2021).

Technological innovations: Advances in selective gear designs, vessel monitoring systems, AI-driven catch forecasting, and improved hydroacoustic methods are making fisheries more efficient and selective (Jenkins et al., 2023; Dunn et al., 2016). These technological innovations can reduce bycatch, reduce ecosystem impacts, and increase the economic return per unit of effort, raising the efficiency of fisheries. If managed sustainably, this might also reduce operational costs of fisheries and increase efficiency.

Value-chain and market innovations: Eco-labelling, traceability, and branding (e.g. MSC, Nordic sustainable seafood initiatives) can increase product value, while investments in onshore processing, cold-chain logistics, and product diversification (e.g. omega-3 concentrates from novel species) strengthen competitiveness (Kaiser and Edwards-Jones, 2006). Such approaches generate higher value per tonne landed, even when total catches remain stable. Novel value-added products from fisheries are also discussed in Chapter 9.

4.3.2 Barriers to fisheries growth

Ecosystem conditions: Several human-induced pressures (see Section 3.2) can act as barriers to developing the fisheries sector through effects on the abundance and quality of captured fish. Natural determinants of fish abundance and distribution include aspects like depth, temperature, proximity to the coast, hydrodynamics, habitat structure, predation and food availability. Overfishing is among the most impactful disturbances in most Nordic ecosystems (see Chapter 3) and can also be a long-term barrier to developing the fisheries sector.

Bycatch: Unintentional catching of protected species remains a concern in Nordic waters, particularly affecting marine mammals, such as harbour porpoise and seals, and fish-eating seabirds (ICES, 2024c). Bycatch is most associated with gillnet fisheries in coastal areas, and some trawl fisheries (ICES, 2024c). Although monitoring and reporting have improved in recent years, data gaps remain, hampering robust assessments of bycatch mortality. Measures to improve the conditions and support the development of effective mitigation strategies include expanded observer coverage, adoption of electronic monitoring, and more comprehensive sampling across different fisheries to ensure reliable bycatch estimates (ICES, 2024c). Mitigation approaches such as acoustic deterrent devices (‘pingers’), gear modifications, and spatial-temporal fishing restrictions are under development for some Nordic fisheries, though their potential effectiveness varies across fisheries (ICES, 2024c).

Lack of cooperation in fisheries management: Many stocks are harvested by multiple Nordic countries (Figure 4.2), as well as by other countries, which makes internationally coordinated fisheries management essential. If stock distributions shift across national boundaries, prevailing quota agreements may come under pressure. For example, mackerel catches were driven by the UK, EU, and Norway until the early 2000s. Since then, mackerel stocks have migrated northwestward, increasing fishing opportunities for Iceland and the Faroe Islands (Figure 4.2). Without a comprehensive quota-sharing agreement between all parties, total mackerel catch has consistently exceeded tolerable limits for the stock. Consequently, the Atlantic mackerel fishery lost its MSC certification in 2019 (Østhagen et al., 2022). Progress was made in 2024 with a tripartite deal between the UK, Norway, and the Faroe Islands. However, this deal was criticized by the EU and Iceland (Welling and Sandvik, 2024), highlighting ongoing tensions and the need for broader cooperation, and how a lack of cooperation can operate as a barrier to sustainable growth.

Spatial competition with new ocean activity: The rapid expansion of offshore wind drives growing spatial competition with commercial fisheries. For the fisheries, an immediate consequence is exclusion from areas where safety zones and operational restrictions prevent either access or the use of specific types of fishing gear. Fishing with mobile or bottom-contacting gear types is typically excluded, while passive fishing methods such as pots and gillnets can in some cases be operational. In Denmark’s Kriegers Flak wind farm, static gears are permitted under regulated conditions, while trawling remains prohibited. At Horns Rev 3, small-scale gillnetting is technically allowed, but in practice it has been limited due to safety concerns and changing catch opportunities. In addition to the loss or reduction of profits from catches from some traditional fishing grounds, fleets can be affected by offshore wind development through costs related to additional steaming time, fuel costs, and crowding in remaining fishing grounds, which can erode margins and create new types of conflicts (van Hoey et al., 2021; ICES, 2025b). Hence, with reduced access to fishing areas comes the risk of income instability for fishers and challenges in ensuring fair and transparent compensation for losses.

Offshore wind farms alter local habitats through reef effects from turbine foundations and scour protection, attracting benthic and demersal species, while also introducing noise, electromagnetic fields, and sediment disturbance that may stress sensitive species (van Hoey et al., 2021). See Section 6.2. for an overview of coexistence-related issues for fisheries and ecosystems, relating to offshore wind.

4.4 Scenarios for the Nordic fisheries sector

Nature First | Strong international fisheries management guided by sustainable exploitation and precautionary approaches. Quota agreements are generally respected, and no species are fished above their sustainable yields. Fisheries are displaced in large areas in the North Sea and the Baltic Sea by offshore wind build-out and marine conservation, but the general increase in ecosystem productivity balances fisheries yield. Fishers are being increasingly included in marine restoration efforts. Byproducts from fish processing are increasingly utilized for value-added products. Carbon emissions are largely curbed, but residual effects of climate change are felt in the fishing sector, particularly through shifting species distributions. Improvements in ocean monitoring and efficient data sharing drives dynamic management that takes this into account. |

Constant Compromise | Fisheries management and pressures on the marine ecosystems continue along the same trends as today. This leads to some improvements where international cooperation succeeds in some instances, with remaining difficulties in others. For instance, large ecosystem challenges such as high nutrient loads in the Baltic Sea continue to impact local fisheries. Pressures on the fishing fleet to decarbonize lead to a continued but slow consolidation of fishing efforts among larger vessels. Fisheries displacement by offshore wind continues in the North Sea, exacerbating the difficult situation for small-scale and coastal fisheries. |

Regional Rivalry | Little coordination of fisheries management of transnational fish stocks, potentially leading to overexploitation as nations set their own quotas. Demand for seafood declines due to increased prices in the short term and weakening of international trade, eventually causing prices for seafood exports to drop. National security, including food security, prioritized over marine protection and conservation. The seafood industry maintains its level of activity through active government subsidies in the sector, and an increased focus on building fish processing locally (e.g. in Northern Norway and Greenland). |

Growth First | Fisheries are optimized for profit, leading to exploitation for short-term gains to supply demand for both human consumption and aquaculture feed. The fishing fleet moves towards fewer, larger and more efficient vessels, strongly focused on improving economic productivity. Regulations are enforced only when stocks are close to collapsing and when threatened, fisheries move to lower trophic levels (e.g. meso-pelagics). Fisheries impacted by ecosystem collapse due to weak environmental management and high nutrient loads in densely populated areas such as the Baltic Sea and North Sea. Fisheries increasingly exploit opportunities in Arctic waters, where warming waters see an influx of species from waters further south, driving rapid economic development in areas like Greenland. |