Appendix 5: Life Event 2

User Story 7 – Working in Sweden while living in Denmark

Jesper has significant experience in working abroad and has worked in Sweden twice. Initially, Jesper worked for a big company for several years, starting in Denmark, later transitioning to the Nordic division. In 2011, Jesper started commuting from Denmark to Sweden following a company restructuring that required the relocation of their work. It did not seem like a significant change to work cross-border, as he considered it a natural part of working in a Nordic company. After leaving the company in 2017, Jesper briefly worked for another company in Denmark before being headhunted back to a new workplace in Sweden.

Jesper obtained financial assistance from his company to understand the implications of the move and the company connected him with an independent accounting firm knowledgeable about Swedish tax regulations, covering the cost of the advice. This guidance was considered effective overall, and Jesper is generally satisfied with the support received and his decision to work cross-border.

The latest available data from 2022 shows that approximately 1,650 people commute from Denmark to Sweden. Of these 1,650 commuters, the majority—around 1,000—travel to either Malmö or Lund. About 62% of the commuters are men.

However, significantly more people commute from Sweden to Denmark. According to the latest 2022 data, around 18,500 people commute from Sweden to Denmark. According to Øresunddirekt, this is mainly due to better salary conditions in Denmark and more affordable living costs in Sweden.

The following visualization illustrates Jesper’s journey through the system and is divided into seven steps.

Figure 10 Journey Map for User Story 7

Note: The figure and related text boxes are based on information from interviews with users and stakeholders (authorities and companies appointed by the users).

Personal Identification (ID) When Jesper started working in Sweden, he needed to ensure he could pay income taxes in Sweden. To do so, he had to acquire a Samordningsnummer from the Swedish Tax Agency, Skatteverket. This process required an in-person meeting at a tax office, where he had to present proof of his identity and show his work contract to verify the purpose of his employment.

Jesper found the process of acquiring a Swedish Samordningsnummer to be challenging. The process requires in-person meetings, and an automatic 60-day delay is added to his date of birth, which causes discrepancies in systems and leads to errors. The requirement for in-person meetings, combined with an automatic 60-day delay added to his date of birth, caused discrepancies in the system and led to errors. Despite eventually receiving the Samordningsnummer, Jesper was frustrated to find that he still could not access Swedish digital services.

Øresunddirekt confirms Jesper's experience, noting that acquiring a Samordningsnummer is a slow process, with processing times that can extend up to six weeks. They further emphasize that the Samordningsnummer does not provide full integration into Swedish systems. For instance, individuals with a Samordningsnummer cannot obtain a digital identity, which means they are unable to access their Swedish bank accounts or perform administrative tasks online. Consequently, they are required to complete these processes on paper.

Tax payment Jesper chose to be taxed under the Swedish SINK scheme, meaning he pays a flat 25% tax on his income without any opportunities for deductions. He considered the alternative – being taxed under Swedish income tax law—which would have allowed for certain deductions, such as travel expenses. However, since at least 90% of his total work income would have needed to be taxed in Sweden to qualify for personal deductions like the basic allowance and employment deductions, he opted for the SINK scheme. He was also aware that Danish tax regulations could influence his deductions if he had chosen regular income tax instead.

Jesper applied for both a personal Identification number and tax registration at the same time by visiting a Skatteverket service office. He submitted the application for a personal identification number and SINK tax, presented his identification (passport), and provided his employment contract.

Alternatively, Jesper could have applied for the SINK tax online via Skatteverket’s website. In this case, he would have received an invitation to a service center for identity verification before being issued a personal identification number and having his tax status determined.

Jesper found the process of paying taxes in Sweden to be quite easy. However, since he works in Sweden and lives in Denmark, he is taxable in both countries and must submit annual tax filings to both the Danish and Swedish authorities.

Bank account To receive a Swedish salary, Jesper needed a Swedish bank account. To open an account, he was required to provide an employment contract, proof of residence in Denmark or Sweden, a Samordningsnummer, and Danish identification.

Jesper learned that to obtain e-identification, a Swedish personal identification number is necessary, and a Samordningsnummer alone is not sufficient.

Jesper does not have a Swedish bank ID, and as a result, all correspondence with bank authorities must be conducted by letter. He finds it frustrating not to have access to digital services because of this lack of a bank ID, which is an issue confirmed by Øresunddirekt.

Øresunddirekt further points out that cross-border workers, like Jesper, who want to apply for a bank loan or purchase something on credit, face significant challenges due to their financial status. Danes working in Sweden have no registered income in Denmark, making it impossible for them to take out a loan in Denmark since they do not earn money in their home country. Neither Danish nor Swedish banks are willing to assist with this, as it remains an unresolved issue.

Insurance and social security Jesper had to join a Swedish unemployment insurance fund (a-kassa) from his first day of work. He also needed to be a member of a Swedish union, as Danish unions have no influence in Sweden. Some Danish a-kassas and unions have Swedish counterparts, which Jesper was able to explore.

Jesper’s Samordningsnummer was also necessary to obtain social security in Sweden alongside his Danish coverage. He had to contact the Swedish authority, Försäkringskassan, which administers social security and payment of benefits. Jesper found the process of getting insurance and social security to be smooth. For him, the insurance fund primarily covered long-term sickness and dental reimbursements. His insurance ensured social security in both Denmark and Sweden, which provided him with peace of mind.

Pension While working in Sweden, Jesper earned a Swedish pension. The Swedish pension system consists of three parts: the public pension (allmän pension), occupational pension (tjänstepension), and private pension savings.

Jesper, however, cannot access live pension information digitally and instead receives annual statements by mail due to his lack of a digital identity. To get additional details, he must request them over the phone as email communication is restricted for security reasons, which he finds inconvenient.

Transportation When travelling across the border, Jesper is required to carry identification with a picture. He typically works three days in Sweden and two days in Denmark each week. Jesper is responsible for paying his own travel expenses, as the SINK tax does not allow for deductions related to travel costs.

Moving back When Jesper decided to return to Denmark to work, he made sure to transfer his unemployment insurance and union membership.

He didn’t experience any complications during this process. However, he is aware that the situation might have been different if he had been fired instead of choosing to leave voluntarily, particularly regarding unemployment insurance.

User Story 8 – Working in Sweden while living in Finland

Eino moved from Finland to Sweden in 2016 to work. The offered position was attractive to Eino due to its focus on sustainability, something that was less prominent in similar roles in Finland. After working in Sweden for a few years, Eino later moved back to Finland due to family reasons and began commuting between Finland and Sweden, working two days a week in Sweden. This was Eino’s first experience working cross-border. Eventually, Eino transitioned to working full-time in Finland for the Swedish-based employer, continuing the cross-border arrangement.

Eino's employer supported the move, ensuring that tax payments were correctly registered. The company also provided assistance for the necessary paperwork and regulations, making the initial relocation relatively smooth. However, as Eino began commuting, the process became more complicated due to the lack of coordination between Finnish and Swedish authorities. Eino had to research the applicable rules and regulations independently, receiving only limited support from both authorities. The lack of proactive support from either the Finnish or Swedish authorities made this phase much more difficult. Despite this, Eino was generally satisfied with the guidance received during the initial relocation but found the transition to cross-border commuting more challenging.

Figure 11 Journey Map for User Story 8

Note: The figure and related text boxes are based on information from interviews with users and stakeholders (authorities and companies appointed by the users).

Personal Identification (ID) When Eino first moved to Sweden, the process of obtaining a personal identification number was straightforward. The Swedish tax authorities required Eino to provide proof of identity and the employment contract in person. Once the personal identification number was obtained, it was easy to open a Swedish bank account, as Eino had all the necessary documentation.

However, when Eino later transitioned to commuting between Finland and Sweden, this process became more complicated. Eino now needed a Samordningsnummer, and that did not allow Eino to easily access all services in Sweden, as certain digital services required a Swedish personal identification number, which is separate from the Samordningsnummer.

Øresunddirekt confirms Eino’s experience, noting that the Samordningsnummer does not provide full integration into Swedish systems.

Tax payment Eino was initially taxed under the Swedish system, but as Eino began commuting, the taxation process became more complex. In Finland, Eino was required to report and pay taxes on travel activities, while in Sweden, the SINK tax scheme required Eino to track the days worked in each country. This meant Eino had to submit information to both Finnish and Swedish tax authorities, leading to confusion and a lack of coordination between the two systems.

In Finland, Eino had to manage advance payments and ensure proper tracking of all travel activities associated with work. The Finnish Tax Authority required detailed reporting, which was time-consuming and complicated. Simultaneously, Sweden's SINK tax necessitated thorough documentation of workdays spent in Sweden. Eino often found it challenging to keep accurate records and comply with both countries' tax regulations.

Eino experienced multiple instances of overpaying taxes, as navigating the complex, fragmented systems led to errors. Overpaying taxes was preferable to Eino rather than risking underpayment, but this caused significant stress and financial strain. The lack of a more integrated system between the Finnish and Swedish tax authorities contributed notably to Eino's frustration.

In the absence of a coordinated system, Eino had to rely on personal research and limited employer support to decipher the tax rules. Proactive support from either Finnish or Swedish tax authorities was minimal, which further complicated ensuring proper tax compliance. Eino's double-taxation experience highlights the need for automated and streamlined processes to alleviate the administrative burden on cross-border workers.

Overall, Eino emphasizes that overpaying taxes might not be an option for all cross-border workers. A more automated system and better cooperation between authorities would have been beneficial, as managing parallel taxation systems was challenging, even with support from both authorities.

Bank account To receive a Swedish salary, Eino needed a Swedish bank account, which was set up without issue during the initial relocation. However, when Eino started commuting between Finland and Sweden, problems arose. Although Eino had the Samordningsnummer, due to change of phone, it was difficult to access digital banking services. This led to Eino having to conduct all banking correspondence by letter, which was frustrating and time-consuming.

In addition, without a Swedish bank ID, Eino faced barriers when trying to apply for loans or make purchases on credit. Due to the lack of financial integration between the two countries, Eino could not easily access services that would have been available if the banking systems were more interconnected.

Insurance, social security and pension Eino had to join a Swedish unemployment insurance fund (a-kassa) from the first day of work. Eino also needed to be a member of a Swedish union, as Finnish unions have no influence in Sweden. Some Finnish a-kassas and unions have Swedish counterparts that Eino could explore. The Samordningsnummer was also necessary to obtain social security in Sweden alongside Finnish coverage. Eino had to contact the Swedish authority, Försäkringskassan, which administers social security and payment of benefits. The process of obtaining insurance and social security was smooth, covering long-term sickness and dental reimbursements, ensuring social security in both Finland and Sweden and providing peace of mind.

While working in Sweden, Eino earned a Swedish pension. The Swedish pension system consists of three parts: the public pension (allmän pension), occupational pension (tjänstepension), and private pension savings. Eino cannot access live pension information and instead receives annual statements by mail due to the lack of a digital identity. To get additional details, Eino must request them over the phone as email communication is restricted for security reasons, which is inconvenient.

Transportation When travelling across the border, Eino is required to carry identification with a picture. Eino typically works two days a week in Sweden. Eino's employer covers accommodation and travel expenses. She describes commuting as time-consuming and negatively impacting overall health. Eventually, the COVID-19 pandemic completely halted travel, leading Eino to work full-time from Finland.

Moving back When Eino decided to resign and end cross-border work, she did not experience any complications. The resignation naturally ended the basis for Swedish taxation, ensuring a smooth transition back to working full-time in Finland.

User Story 9 – Working in both Latvia and Estonia

Maria is originally from Estonia and has significant experience working abroad. She has been living in Latvia since 2004 and working cross-border between Latvia and Estonia. Initially, Maria moved to Latvia for family reasons, as her partner already worked there. After six months, she began working in an international company, marking her first and only cross-border work experience.

Following her initial work experience, Maria transitioned into a sector, engaging in business activities in both Latvia and Estonia. During this time, Maria has navigated various challenges related to cross-border work, including cultural adjustments and bureaucratic hurdles. She considers this cross-border work to be a natural part of her career progression given her extensive experience.

Maria received support from her partner, who had prior experience in navigating the bureaucratic processes in Latvia, greatly aiding in her preparations for the move. Despite the complexity of the process, the assistance proved effective, and Maria is generally satisfied with her decision to work cross-border.

Figure 12 Journey Map for User Story 9

Note: The figure and related text boxes are based on information from interviews with users and stakeholders (authorities and companies appointed by the users).

Personal Identification (ID) When Maria started working in Latvia, she needed to ensure she could access essential services such as healthcare and education for her children. To do so, she had to acquire a residence permit and a social security number from the Latvian authorities. This process required in-person meetings at both immigration offices and local municipal authorities, where she had to present proof of her identity and show her work contract to verify the purpose of her employment. The process was complex and time-consuming, but her partner’s prior experience helped in preparing everything beforehand. Further, the Estonian embassy in Latvia proved helpful in this as well as many other administrative processes.

Initially, Maria found the process of acquiring a Latvian residence permit and social security number to be challenging. The requirement for in-person meetings and bureaucratic hurdles made it a cumbersome process. Additionally, there was the requirement that new residents in Latvia take a Latvian first name with Latvian spelling for official documents, which Maria strongly opposed on behalf of her children, fighting for the preservation of their names in all official matters.

Today, Maria helps other new residents navigate the systems and notes that interactions with government offices, tax authorities, and municipal institutions are now much simpler and more transparent, with better online resources and more helpful, often English-speaking officials. However, the system remains bureaucratic and can alienate cross-border workers as it still does not proactively meet their needs.

Tax payment Maria has navigated cross-border taxation between Estonia and Latvia, which has been time-consuming and costly. As information is not shared between the authorities, she must file monthly tax declarations in both countries, adding a constant layer of paperwork. Despite some improvements in taxation systems, the process remains complex and prone to bureaucratic delays.

Maria chose to be taxed under a scheme appropriate for her circumstances, ensuring compliance with both Estonian and Latvian regulations. She submitted the necessary documents and met the requirements to facilitate the tax payment process. She must balance tax filings in both countries, which adds complexity but is necessary due to her work engagements and business activities.

Bank account To receive payments from her business engagements, Maria needed bank accounts in both Estonia and Latvia. Opening accounts required providing her employment contract, proof of residence in both countries, and identification documents.

Maria faced additional complexity with digital banking services due to frequent identity re-verification, which banks imposed because of regulatory requirements for non-resident accounts. She often finds it frustrating not to have seamless access to these services due to bureaucratic hurdles and cross-border financial regulations.

Insurance, social security and pension Maria had to ensure comprehensive coverage under the social security systems in both Estonia and Latvia. This included enrolling in the healthcare system and joining relevant unemployment insurance funds and unions. To ensure higher-quality healthcare coverage, Maria opted to maintain Estonian health insurance by paying herself a minimum salary in Estonia, complementing the basic healthcare provided through her Latvian employment. Obtaining a permanent residence permit was essential for accessing social security benefits in Latvia without barriers, which added another bureaucratic hurdle to clear.

Navigating the different social security systems required coordination with authorities in both countries. Despite initial challenges, Maria found the process manageable due to her prior experiences and partner's support. Ensuring full coverage healthcare and social benefits in both countries provided her peace of mind.

While working in Latvia, Maria earned a Latvian pension, which consists of multiple components. However, accessing real-time pension information was restricted due to bureaucratic processes, and she often receives annual statements by paper mail.

To get additional details about her pension, she had to contact the relevant authorities over the phone, facing restrictions on digital communications for security reasons. This process can be inconvenient, but necessary for maintaining her pension records.

Transportation When traveling between Estonia and Latvia, Maria is required to carry appropriate identification and navigate various travel expenses. Her travel activity varies, influenced by her work and personal circumstances.

Currently, she aims to visit Estonia once a month for a few days, balancing both personal and professional matters. The lack of deductions related to travel costs adds to her expenses, complicating the financial management of her cross-border engagements.

User Story 10 – Working in Norway while living in Sweden, with both Norwegian and Swedish citizen-ship

Ingrid moved from Norway to Sweden because she was studying in the borderland and it was cheaper to live in Sweden. After completing her studies, Ingrid decided to stay in Sweden when she started a family and grew accustomed to living there. Ingrid then got a job in Norway and began commuting back and forth between Norway and her home in Sweden. This was Ingrid’s first experience working cross-border. Eventually, Ingrid transitioned to commuting full-time from Sweden to Norway for her Norwegian-based employer.

Ingrid's employer supported her, ensuring that tax payments were correctly registered. She used links from the Swedish website specifically designed for those starting to work in a new country. They have not found a similar comprehensive portal in Norway but since Ingrid was familiar with the systems, she handled the preparation independently. However, as Ingrid began commuting, the process required extensive coordination between Norwegian and Swedish authorities.

Figure 13 Journey Map for User Story 10

Note: The figure and related text boxes are based on information from interviews with users and stakeholders (authorities and companies appointed by the users).

Personal Identification (ID) Ingrid already held both a Norwegian and a Swedish personal number. When Ingrid first moved to Sweden, she obtained a Swedish personal number since she resided there and used it for employment.

Official documents from both sides contain both of Ingrid’s personal identification numbers. She faces no challenges related to health services, and communication with public authorities on both sides of the border works seamlessly.

Maintaining these two active personal identification numbers is one of the most significant challenges Ingrid faces. She has to ensure that both her Norwegian and Swedish personal numbers are up to date, which requires meticulous handling of official documents and tax returns in both countries. Ingrid submits tax returns to both Norway and Sweden, a task that has become routine but still requires extra time. She estimates spending an additional evening on tax returns annually due to the dual system. Furthermore, renewing her passport and managing related administrative tasks take up approximately 12 extra hours each year.

Ingrid has been able to maintain her Norwegian personal number even though she lives in Sweden. As a Norwegian citizen, she has a fødselsnummer, which remains in the Population Register regardless of her place of residence or employment. She ensures her information is kept up to date with Norwegian authorities, including the National Registry, Social Insurance Agency, and Tax Office. This helps maintain correct records and ensures she can access relevant services.

Despite these additional efforts, Ingrid has adapted to the process, ensuring both her personal identification numbers are active, which is essential for seamless interaction with authorities in both Norway and Sweden.

Tax payment As Ingrid works in Norway, she pays taxes in Norway and fills out the Norwegian tax return, benefiting from deductions related to her commute. This means Ingrid deals with tax returns in both the country of residence and the country of employment. She receives a Swedish tax return as well, although there is little activity there.

Handling tax obligations in both countries has become a routine for Ingrid, but it requires careful management. Maintaining two active identification numbers is crucial for Ingrid’s tax process. She spends an additional evening on tax returns annually due to managing the dual system. Each year, she automatically receives an amount of money from Norway to cover cross-border worker expenses. Ingrid handles her advance payments and ensures proper tracking of all travel activities associated with work. The Norwegian tax authorities require detailed reporting, which can be time-consuming.

Ingrid benefitted from using both a Norwegian and a Swedish personal number for tax purposes, legitimizing her tax responsibilities and simplifying the coordination with authorities. She ensures her tax information is regularly updated with both Norwegian and Swedish tax offices, maintaining compliance with her obligations.

Since Ingrid is a Norwegian citizen, she has not faced any significant problems. The process for handling taxes is well-defined but requires coordination with authorities in both countries. Her Norwegian tax card is automated, which simplifies the process. Despite the complexity, Ingrid has adapted to these requirements, ensuring her double taxation obligations are met accurately and efficiently.

Bank account Ingrid faces some trivial problems related to ensuring timely transfers of money between her Norwegian and Swedish accounts. However, this process functions smoothly for her because she uses a bank that has branches in both Sweden and Norway. This allows for direct account transfers, and transactions are completed instantly.

She experiences challenges with another bank, as they do not offer personal banking services in Sweden like they do in Norway. Ingrid’s situation, while complex, is not unique; many others in her municipality have worked in Norway at some point. She frequently receives tips and tricks from other cross-border workers, which helps her manage her situation effectively.

Maintaining both personal numbers has been crucial for Ingrid's ability to navigate the system smoothly. Had she been a refugee in Sweden working in Norway, the challenges would have been significantly more difficult.

To address such situations, some banks have resolved issues by offering temporary personal numbers to log people into systems while waiting for permanent identities—providing interim digital identities to integrate them into systems promptly.

Insurance, social security and pension Ingrid manages her social insurance, healthcare, and pensions seamlessly, with automatic integration and recognition of her identification across both countries. She ensures that both her social identification numbers remain active.

While working in the Nordic region, Ingrid was able to handle residence and work agreements and received tax cards as usual. Her labor organization status shifted according to her employment location; organized in Norway when working there and in Sweden when working there. She has received dental coverage through Sweden’s Försäkringskassan, which she renews annually.

Ingrid has built up pensions in both countries. She worked in Sweden for a couple of years, establishing a small pension tied to her Swedish personal number. She is unsure what will happen once she becomes a pensioner living in Sweden, although she believes maintaining her Norwegian employment has provided better pension benefits.

Transportation Due to a post-COVID law that prohibited working for a Norwegian company while residing abroad, Ingrid must be physically present in Norway to work. Consequently, she drives into Norway every day. The strict enforcement of this rule requires compliance with her employer’s regulations. Ingrid occasionally faces issues with her employer lacking awareness of her situation. Ingrid's employer covers her travel expenses.

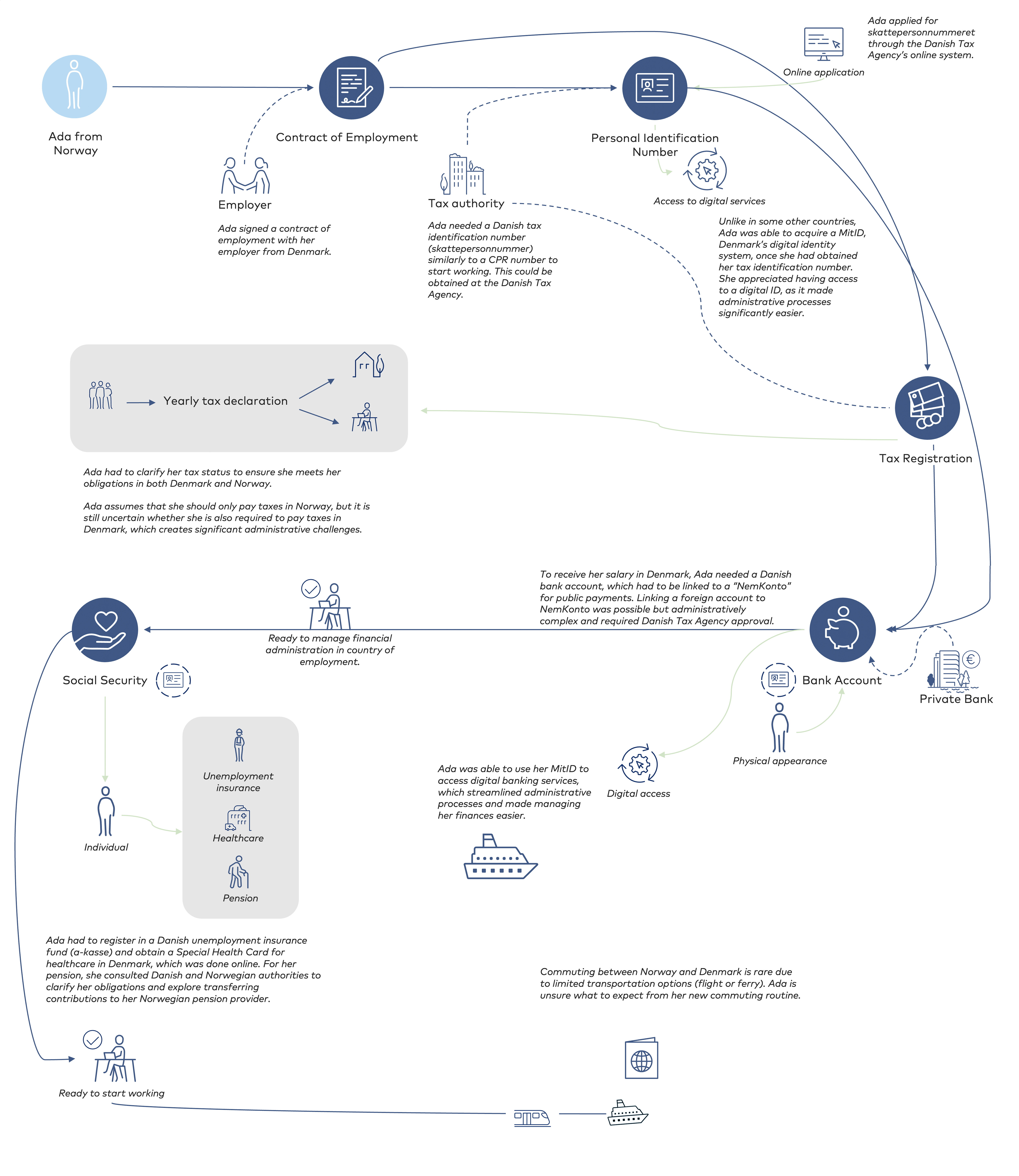

User Story 11 – Working in Denmark while living in Norway

Ada has been managing a project from Norway for the past two years. The project continues, but now from Denmark. Therefore, Ada needs to commute between Norway and Denmark for work. She started the new project in January 2025, making this a completely new situation for her. As a result, she has little experience with navigating the systems and is going through many administrative processes for the first time.

Ada assumes that she should only pay taxes in Norway, but it is still uncertain whether she is also required to pay taxes in Denmark, which creates significant administrative challenges.

There are no precise figures for how many people commute between Norway and Denmark. However, it is expected that the number is relatively low, as commuting between Norway and Denmark is not very widespread due to transportation options (flight or ferry). In comparison, more people commute between Sweden and Denmark or Sweden and Norway, especially in the border regions.

Figure 14 Journey Map for User Story 11

Note: The figure and related text boxes are based on information from interviews with users and stakeholders (authorities and companies appointed by the users).

Personal Identification (ID) When Ada started working in Denmark, she needed to obtain a Danish tax identification number (skattepersonnummer), which functions similarly to a CPR number. She applied for this number through the Danish Tax Agency’s online system. The application required proof of employment, including a signed document from both her and her employer. She also needed to present her national ID as part of the verification process.

The application for a skattepersonnummer could be completed digitally, with an expected processing time of 4–6 weeks. Unlike in some other countries, Ada was able to acquire a MitID, Denmark’s digital identity system, once she had obtained her tax identification number. She appreciated having access to a digital ID, as it made administrative processes significantly easier.

Tax registration In addition to obtaining a tax identification number, Ada needed a Danish tax card (skattekort) to ensure correct tax payments. The tax card application was part of the same process as obtaining her tax number and was submitted through the same form. The processing time for the tax card was typically 1–2 weeks.

The tax card functions digitally and informs her employer about the correct tax rate to apply. In Denmark, there are three types of tax cards: a primary card (hovedkort), a secondary card (bikort), and a tax-exempt card (frikort). Since Ada worked in Denmark, she had to use the primary card. She was required to submit a preliminary income assessment (forskudsopgørelse), estimating her expected annual earnings.

Ada initially assumed that her Norwegian tax obligations would remain unchanged, but she soon discovered that working in Denmark also subjected her to Danish tax regulations. She found the taxation process confusing and was concerned about the risk of double taxation. She was in the process of clarifying her tax status to ensure she met her obligations in both Denmark and Norway.

Bank account To receive her salary in Denmark, Ada needed to open a Danish bank account. The bank required her to provide a valid passport (her Norwegian passport was accepted), a Danish tax identification number, proof of employment, proof of residence, and documentation of her tax status.

Once her Danish bank account was opened, it had to be linked to a NemKonto, the official Danish account system for receiving public payments. In most cases, the bank handled this automatically. While it was possible to link a foreign account to NemKonto, the process was administratively complex and required approval from the Danish Tax Agency (SKAT).

Ada was able to use her MitID to access digital banking services, which streamlined administrative processes and made managing her finances easier.

Health Insurance, Social Security, and pension As a Norwegian resident working in Denmark, Ada was entitled to medical treatment in both countries. However, to access Danish healthcare services, such as visiting a general practitioner in Denmark, she needed a Special Health Card. This card was free and could be obtained digitally via borger.dk. The application required supporting documentation, such as her employment contract and proof of social security coverage (A1 certificate). Processing typically took 2–3 weeks, and the card was valid for two years.

To secure unemployment benefits, Ada had to be a member of a Danish unemployment insurance fund (a-kasse), as her Norwegian membership with NAV or a Norwegian a-kasse did not cover work in Denmark. To ensure her insurance history was transferred correctly, she needed to obtain a PD U1 certificate from NAV and submit it to her Danish a-kasse. If she lost her job while living in Norway, she would generally need to apply for benefits through NAV rather than in Denmark.

Regarding pension, Ada's situation involved multiple factors. Her Danish employer contributed to a pension scheme, which she remained part of despite living in Norway. She was also entitled to Norway’s national pension (Folketrygd) based on her previous work history. However, navigating pension rights across both systems was complicated, and Ada was concerned about the risk of double taxation. She was in the process of consulting Danish and Norwegian authorities to clarify her pension obligations and to explore whether she could transfer contributions to her Norwegian pension provider instead.

Transportation Ada lived in Norway and commuted to Denmark twice a month for work. When crossing the border, she was required to carry valid photo identification.

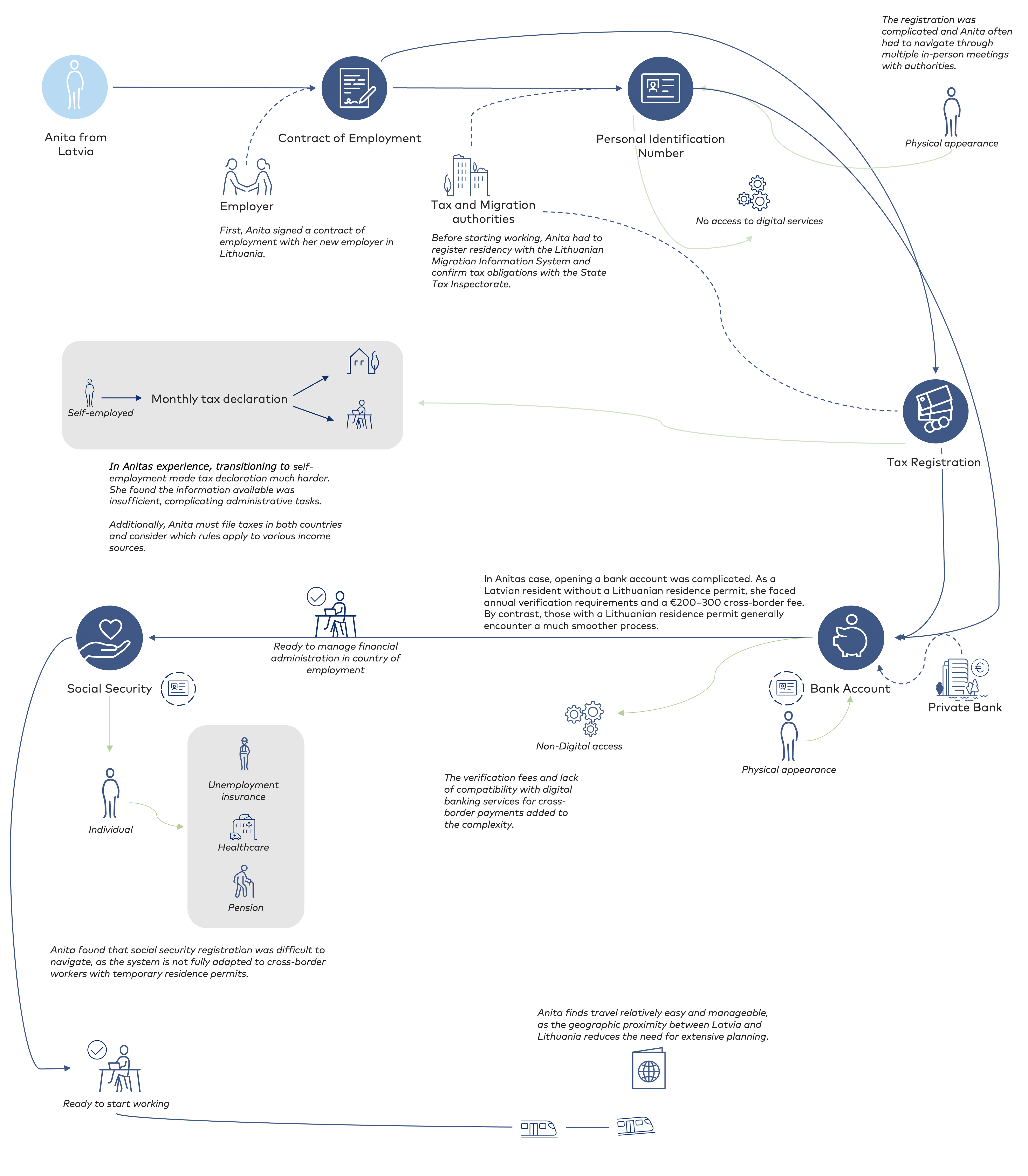

User Story 12 – Working in Lithuania while maintaining partial residency in Latvia

Anita has significant experience in working abroad and has worked in Latvia since 2001. Initially, Anita moved to Lithuania due to an attractive job offer and familiarity with Lithuanian language and culture. Anita frequently travels to Latvia for both personal and professional activities. Her relocation to Lithuania was primarily motivated by better career opportunities, and her knowledge of the local language and culture, alongside support from her partner, made the transition smoother.

Figure 15 Journey Map for User Story 12

Note: The figure and related text boxes are based on information from interviews with users and stakeholders (authorities and companies appointed by the users).

Personal Identification (ID) When Anita started working in Lithuania, she needed to ensure she could meet the administrative and tax obligations there. She had to go through various processes, including residency registration and confirming tax obligations. Despite the EU free movement laws, the registration was complicated with unexpected demands on documentation and proof of residency. She often had to present identification and employment contracts and navigate through multiple in-person meetings with authorities.

Additionally, cross-border payments sometimes did not match her personal identification number, preventing payments from going through.

Anita found the process of acquiring residency registration to be challenging, especially due to the lack of clear guidance for cross-border workers. The Latvian Chamber of Commerce and the Latvian Embassy in Lithuania support cross-border workers with guidance on residency permits and interactions with Lithuanian institutions, but the bureaucratic inefficiencies and lack of coordination between authorities remain a significant barrier. The need for repeated proof of residency and documentation led to errors and frustrations for Anita.

Tax payment Anita pays taxes in both Lithuania and Latvia due to her periodic travel for business activities. The absence of automated information sharing between Latvian and Lithuanian tax authorities means she is required to file separate tax declarations in each country, significantly complicating the process of ensuring compliance and avoiding double taxation. She received initial support from his employer, which simplified tax registration and social contributions, but transitioning to self-employment made it much harder. The Latvian Chamber of Commerce and the Latvian Embassy in Lithuania provide support for tax registration and compliance, but the lack of automatic information sharing and cooperation between the two countries creates difficulties.

Anita found the process of paying taxes to be intricate due to the dual filing requirement and the need to constantly navigate rules from both countries. The insufficient clarity in tax regulations and the additional effort required to manage tax obligations in two countries were particularly cumbersome.

Bank account To manage finances, Anita needed bank accounts in both Lithuania and Latvia. Opening a bank account in Lithuania was more challenging than expected due to the stringent verification requirements and additional fees imposed for cross-border banking policies (€200–300 for verification), compounded by her non-resident status which required annual verification. By contrast, individuals who already hold a Lithuanian residence permit (temporary 5 years, renewable toward a 10-year permanent permit) generally face a much smoother process when opening a personal account. The lack of guidance for cross-border workers further complicated the process. The Latvian Chamber of Commerce and the Latvian Embassy could not assist Anita directly with opening a bank account; they can only point applicants to the relevant registration authorities. Consequently, the bureaucratic hurdles and additional verification fees still pose challenges.

Anita found the process of opening a bank account to be frustrating. She had to provide extensive documentation, including proof of identity, work contracts, and residency permits. The verification fees and lack of compatibility with digital banking services for cross-border payments added to the complexity.

Insurance and Social Security Anita had to join social security systems in both Lithuania and Latvia, which posed significant challenges due to temporary residence permits. She had to repeatedly provide proof of residency and the system's lack of adaptation for cross-border workers led to unexpected gaps in essential services. The Latvian Chamber of Commerce and the Latvian Embassy in Lithuania assist with social security enrollment, but inconsistencies and unclear procedures create further difficulties.

Anita found the process of getting insurance and social security coverage to be difficult. The manual and repetitive nature of providing documentation and ensuring contributions were recognized added to the stress and inefficiency.

Pension While working in Latvia, Anita earned pensions according to Latvian regulations. However, accessing pension information was complicated due to a lack of digital integration and cross-border coordination. The Latvian Chamber of Commerce and the Latvian Embassy offer guidance on pension registration and compliance.

Anita found the process of managing pensions to be inconvenient, especially without access to digital services. She relied on annual statements by mail and had restricted communications options, which she found frustrating.

Transportation When travelling across the border, Anita is required to carry identification and manage travel costs personally. These costs are not tax-deductible due to the complexities of cross-border taxation. The Latvian Chamber of Commerce and the Latvian Embassy provide information on travel regulations and necessary documentation.

Anita found the process of commuting manageable due to the geographic proximity but noted the additional travel expenses as a significant burden.