2. Approach and methods

2.1 Key definitions

In this study, waste prevention and reuse were defined according to the EU Waste Framework Directive (EUR-Lex, 2008):

Waste prevention means measures taken before a substance, material or product has become waste, that reduce:

- the quantity of waste, including through the re-use of products or the extension of the life span of products;

- the adverse impacts of the waste generated on the environment and human health; or

- the content of harmful substances in materials and products.

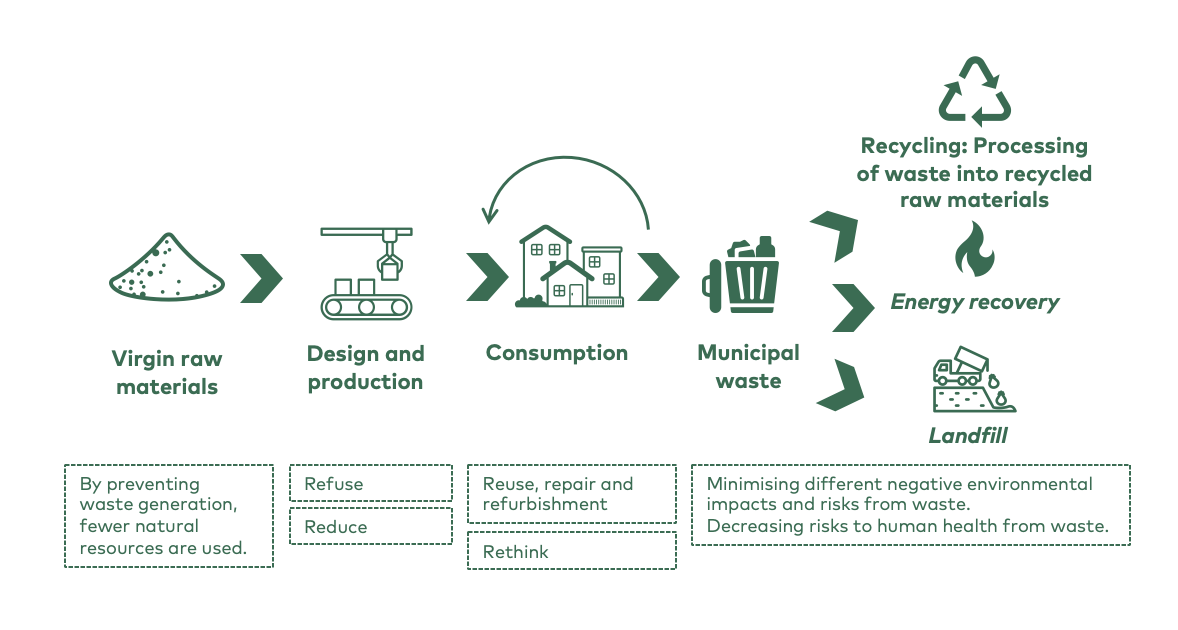

This means that this study focused on all of the R-strategies of the circular economy, with the exception of the recycling of materials and energy recovery, which were agreed to be beyond the scope of this project. Strategies like minimalism and degrowth, aiming for less material use mainly through decreasing consumption, were also agreed to be beyond the scope of this project, even though broadly speaking, they will also ultimately reduce the amount of waste.

Figure 3. This study focused on the circular economy strategies of refusing, reducing, reusing, repairing, refurbishing, and rethinking. These strategies relate to the production and consumption phases of materials and products. Recycling and recovery were decided to be beyond the scope of the project.

A steering instrument refers to a policy or tool that is used to guide, regulate, or influence practices and behaviours. These instruments are typically implemented by governments or other relevant authorities. Steering instruments can be categorised in different ways. In this study, we included the following types of steering instrument (European Environment Agency, 2023a):

- Regulatory steering instruments: Waste prevention measures that actors are obliged to implement by law, including bans, restrictions and other requirements or obligations.

- Economic steering instruments: Tax regulations, subsidies, the introduction of fees and other waste management operations that make 'waste-light' products or services more competitive, incl. green public procurement.

- Voluntary steering instruments: Actions taken by both governmental and non-governmental stakeholders that are not legally binding/obligatory, as well as voluntary agreements between stakeholders that do not necessarily require a political decision-making process but instead require negotiations. Research and pilot initiatives, establishment of reuse centres and networks, and other projects.

- Informative steering instruments: Communication campaigns, educational and training activities, and awareness-raising materials for consumers, businesses, or other target audiences.

- Extended Producer Responsibility: Establishment of EPR schemes, whether legally binding at EU level or voluntary, as well as activities that affect the core strategy and operation of EPR schemes. EPR schemes mean extending the producer's financial responsibility for a product to include the waste management stage.

2.2 Scope defined for the study

Geographical boundaries of the study

The aim of the study was to develop findings relevant to the whole Nordic region (Denmark, Finland, Iceland, Norway, Sweden, Åland, the Faroe Islands, and Greenland). Part 1 of the study included a light mapping of the national waste strategies and plans in each country or region. To ensure the policy relevancy of the study, the analysis included looking at EU-level regulatory development that affects the development in the countries. When identifying effective policy measures and steering instruments, the Nordic project team made an effort to pick examples from across the Nordic region. In order to provide some additional inspiration, good practices were also identified in some benchmark countries (Germany, Slovakia, Belgium, the United Kingdom, and the Netherlands).

Municipal waste fractions in the scope of Part 1 of the study

Municipal waste fractions within the scope of Part 1 were chosen with a view to the potential to reduce the environmental impacts, risks, or hazardous substance content. The choice was made to intentionally pay less attention to some waste fractions for which there are already well-functioning recycling markets. Thus, paper and cardboard, glass, metals, and wood waste were excluded because, in terms of municipal waste, waste prevention was deemed more important for other fractions. As a result, in Part 1 the following waste fractions were included in the scope of the project:

- plastics

- textiles

- biowaste

- waste from electrical and electronic equipment (WEEE)

- hazardous waste

- mixed waste.

Plastics, textiles, WEEE, and hazardous waste were selected to be included in the scope due to their high negative environmental impacts. Biowaste and mixed waste, on the other hand, represent a significant portion of the volume of municipal waste, and preventing the generation of mixed waste is crucial because its recyclability level is often the lowest of all the waste fractions.

Municipal waste fractions in scope of Part 2 of the study

In Part 2 of the project, it was decided to further narrow the scope, concentrating first on the three waste streams of textiles, plastics and WEEE, and later on, conducting an in-depth case study on textiles. Biowaste was at this stage excluded as the measures identified in Part 1 focused primarily on decreasing food waste, which does not fully align with the concept of reuse. Mixed waste was excluded from the project's focus at this stage, as it is a very diverse waste category and would have necessitated several parallel studies. Reducing hazardous waste is very important for the environment, but as a focus area it is very challenging and diverse, and those working on project made the choice to focus more on material streams for which the quantitative reduction of waste is more eminent.

Economic instruments in the scope of Part 2 of the study

The economic instruments in the scope of Part 2 are presented in Figure 4.

Taxes | Fees | Subsidies |

|---|---|---|

Resource tax | Charges for the use of natural resources | R&D funding |

Environmental tax | Waste fees | Business subsidies |

Product tax/import tax | Targeted fees for non-sustainable products | Investment aid |

Changes to VAT | Refund deposit system | Tax deductions |

Labour taxation | Emissions trading | Cutting harmful subsidies and reductions |

Figure 4. Economic instruments in scope of Part 2.

The taxes section includes instruments such as a resource tax, environmental tax, product and/or import tax, changes to VAT and labour taxation relief. A resource tax is a tax imposed on the extraction of natural resources, such as minerals, oil, and gas. The aim is to ensure that the depletion of these resources is accounted for in terms of environmental impact and economic value. An environmental tax is designed to encourage environmentally friendly practices by taxing activities that harm the environment. It can include taxes on carbon emissions, pollution, and other ecological degradation. A product and/or import tax refers to taxes levied on specific goods and services at the time of sale or importation. It can be used to protect local industries, regulate consumption, and generate revenue for the government. Changes in VAT can impact prices and consumer behaviour, influencing overall economic activity. VAT is a consumption tax placed on a product whenever value is added at each stage of production and distribution. Labour taxation relief involves reducing taxes on wages or salaries to encourage employment and stimulate economic growth. It can include tax credits or deductions for employers, making it more affordable to hire and retain staff.

In terms of fees, the economic instruments were charges for the use of natural resources, waste fees and targeted fees for non-sustainable products. Refund deposit systems and emissions trading also belong to this group, but they were outside of the scope of this study. Charges for the use of natural resources are fees imposed on individuals or companies for the extraction or use of natural resources (like water, minerals, or forests). The goal is to encourage sustainable use and limit environmental degradation. Waste fees are charges levied on individuals or businesses for the disposal of waste. They are designed to promote responsible waste management, reduce landfill use, and encourage recycling and waste reduction practices. Targeted fees for non-sustainable products apply to products that are deemed harmful to the environment or not sustainable (such as single-use plastics). The intention is to disincentivise the consumption of these products and promote more sustainable alternatives.

Regarding subsidies, the economic instruments investigated were R&D funding, business subsidies, investment aid, tax deductions and cutting harmful subsidies and reductions. R&D funding covers financial support provided by governments or organisations to encourage research and development activities. This funding helps businesses innovate and develop new products or technologies. Business subsidies are financial aid provided by the government to support businesses, especially in certain sectors or regions. Subsidies can lower operational costs and promote economic growth. Investment aid is a financial incentive aimed at encouraging businesses to invest in specific areas, such as technology, infrastructure, or renewable energy. This can come in the form of grants, loans, or tax breaks. Tax deductions are reductions in taxable income that businesses can claim for specific expenses, such as R&D costs, which can lower their overall tax liability. Cutting harmful subsidies and reductions refers to the process of eliminating or reducing government financial support for activities or products that have negative environmental impacts, encouraging more sustainable practices.

2.3 Methods

The methods used in Part 1 included a literature review and data analysis, a survey, and analysis of effectiveness and feasibility, which led to policy cards presenting existing good practices for preventing waste and promoting reuse.

The work began with mapping waste management strategies and plans in the countries, as well as mapping good practices regarding steering instruments for preventing waste. The screening of waste management strategies was done to give a quick overview of how waste prevention and reuse is emphasised in the current policies. The overview of waste prevention and reuse measures was done to gather a catalogue of good practices that could be assessed for scaling. The measures for the catalogue were chosen based on their potential for:

- decreasing the quantity or adverse impact of waste;

- decreasing the harmful substance content in waste;

- contributing to waste prevention and/or longer lifespans in products; and

- dematerialisation.

The good practice examples were then assessed for feasibility and effectiveness by the project team and through an expert survey conducted in Finland, Sweden, Norway, Denmark, and Iceland. The expert survey had the dual objective of validating the preliminary assessments carried out by the consultants and providing in-depth insights on the most relevant measures and steering instruments.

The assessment was carried out using a tool for assessing the effectiveness and feasibility of each measure, where effectiveness was assessed as the potential to reduce the quantity of waste, and/or potential to reduce harmful substances in / adverse impacts of waste. The feasibility was measured based on the following dimensions: ease of implementation (e.g. time, resources, money, mindset), ease of monitoring, and applicability in the Nordics. Each dimension was scored on a scale of 0–3, and the definitions are presented in Table 1.

Table 1. Framework for feasibility and effectiveness assessment of relevant measures and steering instruments in Nordics.

0 | 1 | 2 | 3 | |

Potential to reduce quantity of waste | Impact on reducing the quantity of waste cannot be evaluated or the impact is marginal. For example, the measure is too unclear to be judged or measures are taken within only one company. | Has a slight impact on volumes, but quite marginal. The impact is mostly on a municipal, but not national level, for example, local campaigns. | Could have a moderate impact on volumes. National-level impact, for example, national green deals. | Could have a substantial impact on volumes at Nordic level. |

Potential to reduce harmful substances in/adverse impacts of waste | The ability to reduce the harmful substance content/adverse impacts of waste cannot be evaluated or the impact is marginal. | Harmful substance levels/adverse impacts of waste reduced slightly, e.g. in a few companies’ consumer products. | Could have a moderate impact on harmful substance levels/adverse impacts of waste, e.g. through affecting several product lines. | Could have a substantial impact on harmful substance levels/adverse impacts of waste at Nordic level. |

Ease of implementation (e.g. time, resources, money, mindset) | Extremely difficult or impossible to implement. | Implementing the measure would be challenging and could require a substantial amount of time, effort, and resources. | While there may be some challenges or complexities involved, the measure is generally feasible and can be implemented with a reasonable amount of effort. | Easy to implement. |

Ease of monitoring | Extremely difficult or impossible to monitor the impact. | Monitoring the impact of the measure would be challenging. | Monitoring of the impact can be implemented with a reasonable amount of effort. | Easy to monitor. |

Applicability in the Nordics | Extremely difficult or impossible to apply in the Nordics. | Applying the measure in the Nordics would be challenging or the measure has clear geographical limitations. | The measure can be applied with a reasonable amount of effort in all or most of the Nordic countries. | Easy to implement in all the Nordic countries. |

The output of Part 1 was a review of effective measures and steering instrument to prevent municipal waste production and promote reuse in the Nordics. This part can serve independently as inspiration for enforcing and scaling measures through different kinds of policy tools (including voluntary and informative tools).

Part 2 of the project focused specifically on economic steering instruments and their potential in driving significant change. The work began with describing the potential role of economic instruments in the value chains of textiles, consumer electronics and plastic packaging. A range of potential economic instruments were identified, and the same assessment tool that had been used in Part 1 was applied to tentatively assess the effectiveness and feasibility of these, resulting in a reduced number of alternatives for in-depth case study.

Case studies are used to provide in-depth insights and real-world examples that help illustrate concepts and inform decision-making by showcasing practical applications and outcomes. It was therefore decided to do a case study focusing on a few selected economic instruments that were seen to have potential effects on consumer behaviour and therefore municipal waste. Textiles were chosen as the object of the study. The key methods used were desk study, individual interviews and targeted group interviews with a number of Nordic experts, organised as one sprint in September 2024. Desk study was used to create the basis for four light case studies on selected economic instruments for promoting a circularity-based textile sector. The group interviews were organised with selected experts from the Nordic countries, representing different substance areas and perspectives (public officials, NGOs, advocacy organisations or the research sector). The interviews focused on the effectiveness and feasibility of each instrument, as well as elaborating on the need for policy action. The experts evaluated each instrument’s strengths and weaknesses, challenges and factors supporting their implementation and the possible next steps for Nordic decision-makers to proceed with each instrument discussed. The findings were validated and summarised by the project group as light case studies.

In the final phase of the work, the project group came together and developed the findings of the study into conclusions and policy recommendations. The outcomes of the work were discussed with the steering group of the project, the Nordic Waste Group, and the Nordic Circular Economy Working Group, as well as being presented to wider audiences, at a webinar in June 2024, as well as at the Nordic Circular Summit in November 2024.