3. Synthesis of results

3.1 Common aspects and potential synergies among the Nordic countries

Waste incineration & district heating – a perfect match?

Common for all Nordic countries is a considerable integration between waste incineration and the district heating sector. A colder climate and being able to use the district heating system as a heat sink (or additional income in economic terms) for waste incineration is a strategic advantage for the Nordic countries that is often raised as an argument in favor of maintaining (or even expanding) the Nordic district heating sector. The waste incineration sector is pointed out to primarily having been established for handling waste streams and minimizing waste volumes and thus landfill, but also to reduce potential toxic or infectious properties.

Waste Incineration and Public Health, Committee on Health Effects of Waste Incineration, Board on Environmental Studies and Toxicology, 2000

Waste incineration policies differ between the Nordic countries

The national strategies for the Nordic countries with respect to the waste incineration sector, however, differ to some extent, with the inclusion of the waste incineration sector in Denmark and Sweden in the EU ETS system being one of the most obvious differences. Denmark, in addition, has an active policy goal to reduce the waste incineration capacity. The other countries in the Nordics, on the other hand, currently do not have any goals to reduce their waste incineration capacity. For Finland in particular, waste incineration plants have been installed more recently, resulting in incentives for the energy companies to continue using the existing infrastructure at least for its technical lifetime. A political goal of reducing the capacity in turn would be counteractive to these incentives.

Well-established waste sorting systems

All Nordic countries operate well-established systems for sorting and handling large fractions of waste – in particular household waste. The fulfillment of recycling goals and increase in material recycling will lead to decreased domestic generation of waste for incineration and may impact the heating value of waste being incinerated. However, the achievement of the ambitious goals set on material recycling is not self-evident, as impurities in waste, many steps prone to human error (e.g., low sorting performance in complicated sorting systems) being involved in the waste handling process and high costs for handling and sorting waste may lead to lower recycling rates in reality.

Nordic countries waste incineration solution for landfill in Europe?

In addition, there currently are substantial amounts of waste imported to the Nordic countries (and transferred between the Nordic countries) with the Nordic waste incineration sector as alternative to landfill for the rest of Europe. Denmark has set a policy goal to avoid import of waste – in line with their planned decrease in incineration capacity - but within the other Nordics countries, energy and waste management companies still are free to import waste to supply their incineration plants.

As mentioned earlier, Nordic conditions allow for high rates of energy recovery due to cold climate and established district heating networks. However, the focus on national policies sometimes can be considered to suboptimize the waste incineration systems with respect to emission reductions from a European or global perspective: national climate targets and conflicting economic incentives can for example be a barrier for European landfill waste being combusted in the Nordic countries. There are a large number of existing landfill sites where climate benefits – from e.g., avoiding methane emissions from these landfills – would motivate the case of transporting and handling the waste in Nordic incineration plants from an environmental (global) perspective.

Waste management market not a transparent business

The varying ownership structure (public/private) of waste incineration plants and waste management companies across the Nordics also has an impact on the opportunities to effectively influencing/changing the sector by policy measures. A common Nordic/European market for waste, as well as an international perspective on emissions caused by waste handling (both from landfill and incineration) could help to address a number of challenges but is of course difficult to realize. Missing data and varying levels of details on statistics across the different countries is also an aspect making international comparisons difficult.

Higher costs for waste handling increase risk for illegal business

Increasing efforts on waste sorting, recycling, improved handling in general, as well as stricter requirements on waste incineration plant operators with respect to emission handling has in general increased waste handling costs. Increasing gate fees, caused by higher environmental and emissions standards operators need to adhere to, also might provide a stronger driving force for illegal actions. Illegal waste handling, both through export and illegal dumping or incineration, has increased notably in Europe since 2018, when China, which until then had been the most important waste importer globally, introduced stricter rules on import of solid waste.

INTERPOL’s strategical analysis on emerging criminal trends in the global plastic waste market since January 2018

Nordic islands may become a show case

The islands in the Nordic countries vary in both population in size, resulting in different challenges with respect to waste management. There are several ambitious strategies for reducing waste generation and improving recycling to move towards a more circular economy. Bornholm in Denmark is such an example, trying to inspire and foster international collaboration for addressing the challenges within the sector with its “Without waste 2032” strategy. Also, the Faroe Islands have ambitious goals with respect to waste management and circularity. There is a potential for collaboration among the Nordic countries to lift waste management and waste incineration related topics for islands to an international level, with the Nordic islands becoming an international show case.

Waste incineration will not become redundant in the foreseeable future

Even if the recycling rates based on the Nordic countries’ national plans and EU ambitions and regulations are intended to increase, there will still be massive amounts of plastic waste that can be expected to end up in incineration. The waste incineration sectors (at least in Sweden) does not expect the fossil stream of waste to decrease drastically. A recent study investigating private households’ “combustible waste” fraction (after sorting for fractions in the household according to the local rules) showed that there remains a considerable amount of plastic and paper waste in the fraction sent to incineration, indicating that goals set up by the municipalities will hardly be reached in the near future.

Accumulation of impurities in plastic waste streams complicates circularity – hazardous content either needs to be sorted and rejected upstream, selectively cleaned/incapacitated during the process (technologies for this will be hard to find and commercialize) or plastic waste must be divided up into more different streams than today, which is more expensive.

Proximity to potential CO2 storage sites in Norway (and Denmark)

Norway being a global frontrunner within storage of captured CO2 also could leverage strategic investments within the waste incineration in the Nordics, given proper conditions. All Nordic countries – except Finland, where companies within the waste incineration sector have focused carbon capture and utilization as there are no domestic sites for CO2 storage available – have investigations and plans for CCS within the waste incineration sector. Denmark has recently opened up for CCS storage site establishment as well, with three companies having been awarded licenses to store CO2 in North Sea oil and gas reservoirs, hoping to store up to 13 Mtons of carbon per year.

3.2 The potential role of CCUS

Across the Nordic countries, CCUS is increasingly recognized as a crucial technology for mitigating CO2 emissions from waste incineration. This development must be seen in the context of European and Nordic climate ambitions. Norway was the first Nordic country to formulate a strategy for CCUS promoting technology development and cost-effectiveness. Also, Sweden, Denmark and Finland mention CCUS in their climate action plans although strategies for promotion and commercialization exist to varying degrees. For all the Nordic countries, the focus is on equipping existing waste incineration facilities, exploring pilot projects, and actively testing CCUS technologies. However, the type and the status of projects, the scope of initiatives beyond waste and the specific approaches to collaboration differ among the countries. For example, in Norway, several waste incineration actors are already testing out CCS technologies and through the Longship Project, the Norwegian government has decided to take an active role in supporting the implementation of a full-scale industrial CCS value chain by making substantial funding commitments to the Hafslund Oslo Celsio waste-to-energy (WtE). To the contrary, Finnish waste incineration installations presently do not plan to introduce CCS, but rather focus on the implementation of CCU while in Sweden industrial pilots for CCS are still at a very early stage.

Despite the few first operational experiences with CCUS, lacking incentives, investment and infrastructures hampered progress across all Nordic countries. As an example, the Danish government decided to reduce its incineration activity by 30% following a decision to stop importing waste from other countries.

Nevertheless, there are indicators for a change in dynamics. Where countries have chosen to implement carbon taxes and/or include the waste incineration sector in the ETS, waste incineration operators have a clearer incentive to consider the deployment of CCUS technology, given the expected rise of carbon prices. Emissions verified as captured, transported, and permanently stored may eliminate the obligation to surrender emission allowances or pay carbon taxes. This will be harmonized to a larger extent between the Nordic (and European) countries when the waste incineration sector is included in the EU ETS across the whole European Union towards 2030.

A greater role for CCUS is also foreshadowed in recent legislative initiatives at the EU level. The 2023 proposal for the Net-Zero Industry Act (NZIA) now lists CCUS as one of the 8 strategic net-zero technologies for which scaling up manufacturing capacity is critical. NZIA sets out measures and action lines to facilitate strategic CCUS projects which may benefit the introduction of these technologies in waste incineration installations given the hard-to-abate nature of the sector. The adoption of the proposed Carbon Removal Certification Framework (CRCF) may also bring more certainty for waste incineration operators who plan to deliver negative emissions with BECCS. If the CRCF succeeds in establishing a regulatory framework for robust and transparent carbon removal this might not only create a growing market for BECCS credits generated from biogenic waste incineration but could also pave the way to an integration of negative emissions technologies into the EU ETS, adding to the circle of incentives for the waste incineration sector.

All in all, the role of CCUS for the waste incineration industry is to reduce emissions, reduce related taxes and give more operation stability for the plants as they would comply with authorities’ goals. CCUS will not influence the amount of waste being sent to incineration. However, if a carbon removal certification scheme is implemented, the price of certificates may incentivize incineration plants to burn a higher share of biomass and compete to a larger extent with other waste treatment alternatives for biomass, depending on the respective market prices for CDRs and biomass.

3.3 The role of circular economy

The incineration of wastes conflicts with targets of circular economy such as reduction, reuse, or recirculation of materials. Reaching recirculation targets would decrease the amounts of materials such as plastics in mixed waste and decrease both amount and heating value of the incinerated waste. An example from Finland for the effects on increase in circularity illustrates these effects:

In 2021 38% of municipal waste was material utilized, which is much less than the targets 55% (2025) or 60% (2023). Assuming the total amount of municipal waste (3.5 Mtons) will not increase, the amounts of waste to incineration should decrease based on the target to about 560 000 tons and 730 000 tons, respectively. On the other hand, the recirculation rates of package plastics are also far behind targets, being at 34% while targets are 50% and 55% for the years 2025 and 2030, respectively. The content of plastics in mixed waste will decrease with increasing recycling, leading to lower fossil CO2 emissions but also to a lower heating value (as the share of plastics decrease). This, in turn, may lead to a need for supporting fuel or a need to increase the amount of other waste derived fuels.

The municipal waste companies have recirculation targets, but, on the other hand, they may have long-term contracts with the energy company for delivering waste for incineration. If the amount of municipal waste decreases, there is a strong need for other waste fuels – such as construction waste – for incineration. There will be competition between incineration and material recycling of waste. On the other hand, imported waste may replace some domestic municipal waste.

The material utilization of ash can be considered as recirculation. According to recirculation rate calculation, metals removed from waste incineration ash can be allocated to the recirculation rate, but the rest of the ash cannot.

There has been discussion of calculating products of CCU as recirculation of carbon. The concepts of CCU will produce methanol, which can be used for the production of chemicals or fuels. However, there is no decision on how this will be treated. Fortum Recycling and Waste has a concept to produce plastics from incineration CO2.

Demolition waste can contain, for example, plastic containing polybrominated diphenyl ethers, polyurethane insulation and wood impregnated with wood preservatives. Short chain chlorinated paraffins have been used in paints and in the fire protection of products made of PVC. Hexabromocyclododecane has been used as a fire retardant for polystyrene insulation.

Demolition waste can contain, for example, plastic containing polybrominated diphenyl ethers, polyurethane insulation and wood impregnated with wood preservatives. Short chain chlorinated paraffins have been used in paints and in the fire protection of products made of PVC. Hexabromocyclododecane has been used as a fire retardant for polystyrene insulation.

It has been suggested that these substances should be incinerated at high temperatures for destruction, but to date it remains unclear whether waste incineration is effective enough in destroying long-lived pollutants such as PFAS.

Sofie Björklund, Eva Weidemann, Stina Jansson:

Emission of Per- and Polyfluoroalkyl Substances from a Waste-to-Energy Plant ─ Occurrence in Ashes, Treated Process Water, and First Observation in Flue Gas.

Environmental Science & Technology, 2023

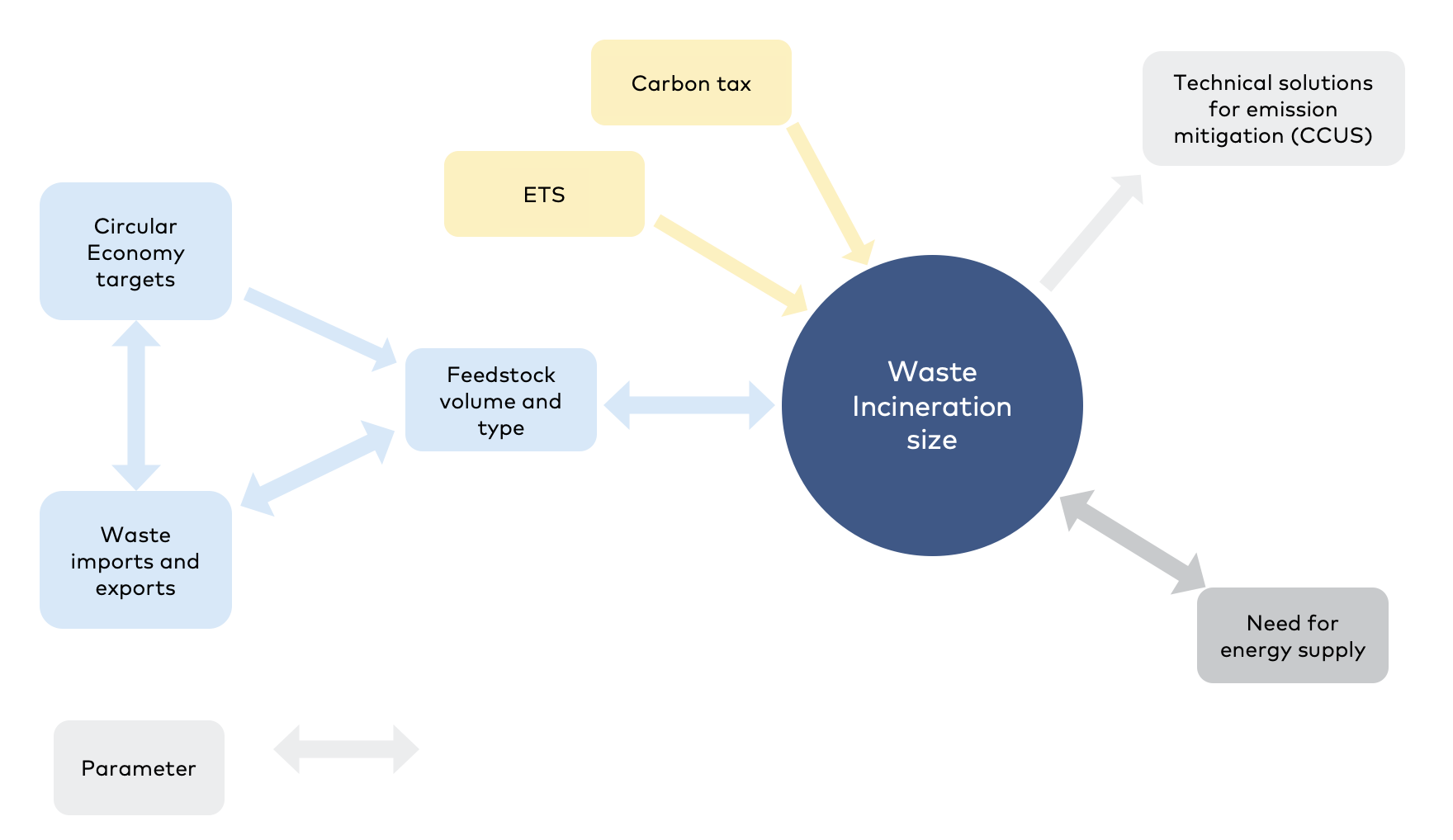

3.4 Considerations on optimal sizing of the waste incineration sector

Although defining an optimal sector size is not within the scope of this report, it can help to find the relevant questions which need to be answered for such a definition. The data found in chapters 1 and 2 points toward a potential conflict between the availability of waste as feedstock in competition with material or chemical recycling, the fulfilment of circular economy goals, and the cost of running waste incineration plants, see Figure 21.

Figure 21 Schematic overview of parameters impacting the waste incineration sector and their interdependence.

Table 8 shows a scenario for incineration capacity in 2030 in Finland, Norway, Sweden and Denmark, provided that policy and/or sector goals are fulfilled.

Table 8 Waste incineration capacity in 2030 based on policy or sector goals.

Country | Waste incineration capacity required in 2030 |

Denmark | Plan for 2020–2030: reduction with 480 ktons/year of waste generation, reduction of incineration capacity from 4 to 2.7 Mtons/year. |

Sweden | 500–670 ktons/year less plastics to incineration 2030 according to 50%-goal set by EU’s plastics strategy – concrete recycling projects and sector goals cover only 164 ktons/year. |

Norway | Based on national numbers, Norway will have to prepare for reuse and recycling of 65% of household waste and similar waste from the industry. This means that 4% more plastic and 57% more mixed waste will have to be recycled or reused compared to 2021 numbers. |

Finland | 700 ktons/year less municipal waste to incineration 2030 according to 60%-goal, 26 ktons/year less plastics, 55% goal. |

The table clearly shows the ambition to reduce the generation of waste in general and plastic waste in particular, while only Denmark has a clearly stated goal to reduce incineration capacity.

What do we optimize for?

When asking for the optimal size of something, it is important to know what shall be optimized. Depending on whether the optimization shall be directed towards global CO2e emissions, recycling rates, energy use, fossil feedstock utilization, physical footprint, local pollution, or something entirely different, the answer will differ. Assuming that material or chemical recycling in general is preferable to incineration, a first step might be to determine how much waste will be left once an economically viable portion (or what is defined by circularity goals and policies) has been recycled. Any recycling on top of this will only be competitive with incineration if recycling costs can be pressed below the level of incineration.

The availability of biogenic feedstock in plastics production, but also to the economy as a whole, is another important input parameter. Just as recycling rates, it will largely depend on policy measures and the willingness to pay in a free or regulated market.

A potential future carbon tax will also impact the economic feasibility of running a waste incineration plant with reduced availability of feedstock. Such a tax, if introduced, will probably be transferred to municipalities and ultimately consumers, but it remains unclear whether higher fees will be enough for a measurable change in behavior or the deployment of new technologies such as CCS.

3.4.1 High-level estimation of waste volumes sent to incineration: a Norwegian case study.

The objective of this section is to provide an indication of the remaining volume of waste sent to incineration if the national circular economy targets are met, starting with an assumption on the evolution of waste sent to treatment in Norway. Assuming that waste volumes continue to grow at the same rates they have since 2012, the total amount of waste treated has been projected to a 2030–2035-time horizon. To that end, the growth rate observed between 2012 and 2019 has been applied to the 2021 level. 2020 and 2021 have not been considered in the growth rate assessment to exclude the potential pandemic effect on waste streams. Figure 22 shows the resulting projection until 2035, which represents a growth of 21% compared to 2021 levels.

Volume of waste generated in Norway | |||

2021 | 2030 | 2035 | |

Total | 11.6 | 13.5 | 14.6 |

Figure 22 Projected Waste Volumes treated in Norway.

The distribution of waste treatments from the year 2021 was subsequently taken as a reference to estimate the volume of waste that will be sent to material recycling. It was assumed that the pandemic did not influence the way waste was treated. From that reference, the distribution of treatments was modified over time to reach the Circular Economy target of 65% (2030) and 70% (2035) of waste prepared for reuse and material recycling of household waste and similar waste from the industry, assuming that this target would be influencing material recycling, biogas production and composting. Not all waste types are included in this projection. In fact, wastes such as wood, sludge, concrete and brick, slag, dust, bottom ash, fly ash, scraped vehicles, radioactive waste, hazardous waste and lightly polluted masses are assumed to be excluded from the Circular Economy target, keeping the same treatment distribution as in 2021 over the projection period. For those waste categories covered by the target that are already being sent to recycling at a higher percentage than the targets, the same distribution over the projected period has been kept. For those waste types assumed to be influenced by the Circular Economy target which were below the 2030–2035 targets in 2021 (mixed waste, wood waste, plastic and rubber), a linear growth to 65 and 70% was applied to the share sent to recycling.

Finally, the 2021 share of waste sent to incineration was applied to the remaining volumes to obtain the projection for each waste type going to incineration. The results are shown in Figure 23, revealing a total waste stream reduction of 29% in 2030.

Figure 23 Waste volumes sent to incineration until 2035 in Norway – Scenario 1.

Historical and future projection of volume of waste sent to incineration by type in Norway. Considered target: Preparation for reuse and material recycling of household waste and similar waste from the industry.

The results suggest that mixed waste will remain the main waste stream going to incineration, with wood waste and hazardous waste following. Moreover, mixed waste is decreasing over time due to the increase in preparation for reuse and recycling, while wood waste and hazardous waste are not impacted by the target and are likely to keep growing in accordance with the total stream of waste generated in Norway.

Furthermore, the projections reveal that even though the target increases by another 5% in 2035, the waste generated actually compensates and increases slightly the waste stream sent to incineration so the actual reduction compared to 2021 will decrease to -28%.

While the aim of the projection was to test the effect of the preparation for reuse and recycling target on the future waste streams, it may also be run for the reduction in food waste target, which specifies a 30% reduction by 2025 and 50% in 2030. A reference year for this target has not been identified and, therefore, was assumed to be 2021. The reduction in food waste streams was applied to the wet organic waste and food waste share of the mixed waste category. To estimate the food waste share in the mixed waste category, the results of the waste picking studies showed earlier in chapter 1 (32.3% and 20.9%) were averaged to represent 27% of mixed waste.

The effect of this additional measure can be seen in Figure 24, where a further 4% reduction is reached.

Figure 24 Waste volumes sent to incineration until 2035 in Norway – Scenario 2.

Historical and future projection of volume of waste sent to incineration by type in Norway. Considered target: Preparation for reuse and material recycling of household waste and similar waste from the industry + Reduction in food waste.

The mixed waste category is further reduced, and wood waste actually becomes the main waste stream sent to incineration. All in all, testing the fulfillment of Circular Economy targets shows that the total volume of waste sent to incineration in 2030 could be 2 Mtons. The current incineration capacity in Norway is about 1.7–2 Mtons.

Sveinung, B., Frode, S., & Andreas, D. (2019). Avfallsmengder fram mot 2035—Energigjenvinningens rolle i sirkulørækonomi (07/2019; p. 32). Mepex Consult AS. https://avfallnorge.no/fagomraader-og-faggrupper/rapporter/avfallsmengder-fram-mot-2035

Import og eksport av avfall. (2022, June 20). Miljøstatus. https://miljostatus.miljodirektoratet.no/tema/avfall/import-og-eksport-av-avfall/

Sveinung, B., Frode, S., & Andreas, D. (2019). Avfallsmengder fram mot 2035—Energigjenvinningens rolle i sirkulørækonomi (07/2019; p. 32). Mepex Consult AS. https://avfallnorge.no/fagomraader-og-faggrupper/rapporter/avfallsmengder-fram-mot-2035

The notion of "household waste and similar waste from the industry” remains unclear. The actual waste categories that will be impacted by the targets might slightly differ. However, the assessment captured and highlighted the main forces at play. Mixed waste is one of the main waste feedstocks and the effect of such targets is likely to happen the way it was modelled for this category. On the other hand, if hazardous waste is actually influenced by the target, the effect on the overall volume reduction would be less important than a change in the mixed waste category. The result sensitivity is smaller and to a certain extent unsignificant to other waste categories than mixed and wood waste.

The assessment does not consider the possibility that new types of waste could be sent to incineration in the future. It has been mentioned in chapter 1 that a larger share of hazardous waste could be sent to incineration. The volume compensation that hazardous waste could bring is challenging to estimate within the scope of this study. Moreover, allowing more of this type of waste will depend on the decision of each regional authority but also on the incineration temperature of each plant to ensure a clean incineration of such substances. Another consideration to have after this assessment is to know if the reduction in waste streams will happen everywhere across the country to the same extent or if we observed a regionalization of effects with some facilities that will be more impacted than others.

Another possible phenomenon mentioned in the previous chapter is the increase in plastic waste generation. If that waste stream increased to the same extent it is projected by some sources, it might have a compensating effect on the total volume sent to incineration.

The assessment relies on the assumption that all the waste sent to incineration is generated in Norway. The effect of waste imports and exports is not considered. If waste imports are included in the statistical basis used for this assessment, the effect of Circular Economy targets will be reduced as a waste stream not subject to those targets will still be imported. As Norway mainly imports waste from the UK, the effect of imports on the 2030–35 Norwegian waste volumes also relies on the policy and targets that will be set in the UK.

Finally, under the growth assumption of the total waste generated in Norway, it is possible to foresee that if the 2035 target is reached, the actual amount of waste sent to incineration actually starts to increase again afterwards due to the increase in waste generated. Thus, the reduction in waste volumes might also be a temporary effect of the target. The waste incineration plant would have to deal with that temporary reduction in waste availability.

The likelihood of the second growth of waste streams after 2035 is high. Indeed, increasing the recycling targets above 70% might become more and more challenging as there will always be a share of waste that will not be able to be recycled. Moreover, the waste stream generated in Norway might still grow even with a reduced waste per capita production. Thus, the incineration sector is expected to still play a role in the future.

Perspective of the case study on the optimal sizing of the waste incineration sector

The amount of waste sent to incineration is considered as the most important influencing parameter to be able to estimate the “optimal size” of the waste incineration sector.

The fact that the assessment suggests a 30% reduction in waste volumes sent to incineration is the most important indicator to consider.

The fact that incineration plants play an important role in district heating or electricity generation is secondary; other power generation technologies (electric heated boilers with heat storage, heat pumps,...) could replace them - provided their maturity, ease of implementation and available feedstock.

The implementation of CCS will certainly allow for cleaner power production but will not compensate for the loss of feedstock for incineration plants. The first ones to implement it might be the ones to survive, provided that the loss of feedstock is even across the country or not happening for the given plants.

The influence of carbon taxes and ETS is expected to accelerate the adoption of CCS and influence to a lesser extent the willingness to incinerate waste due to higher taxes. But it will not counterbalance the effect of the feedstock loss for the incineration sector.