2. Legislative frameworks and circular economy impacts

2.1 In the Nordics

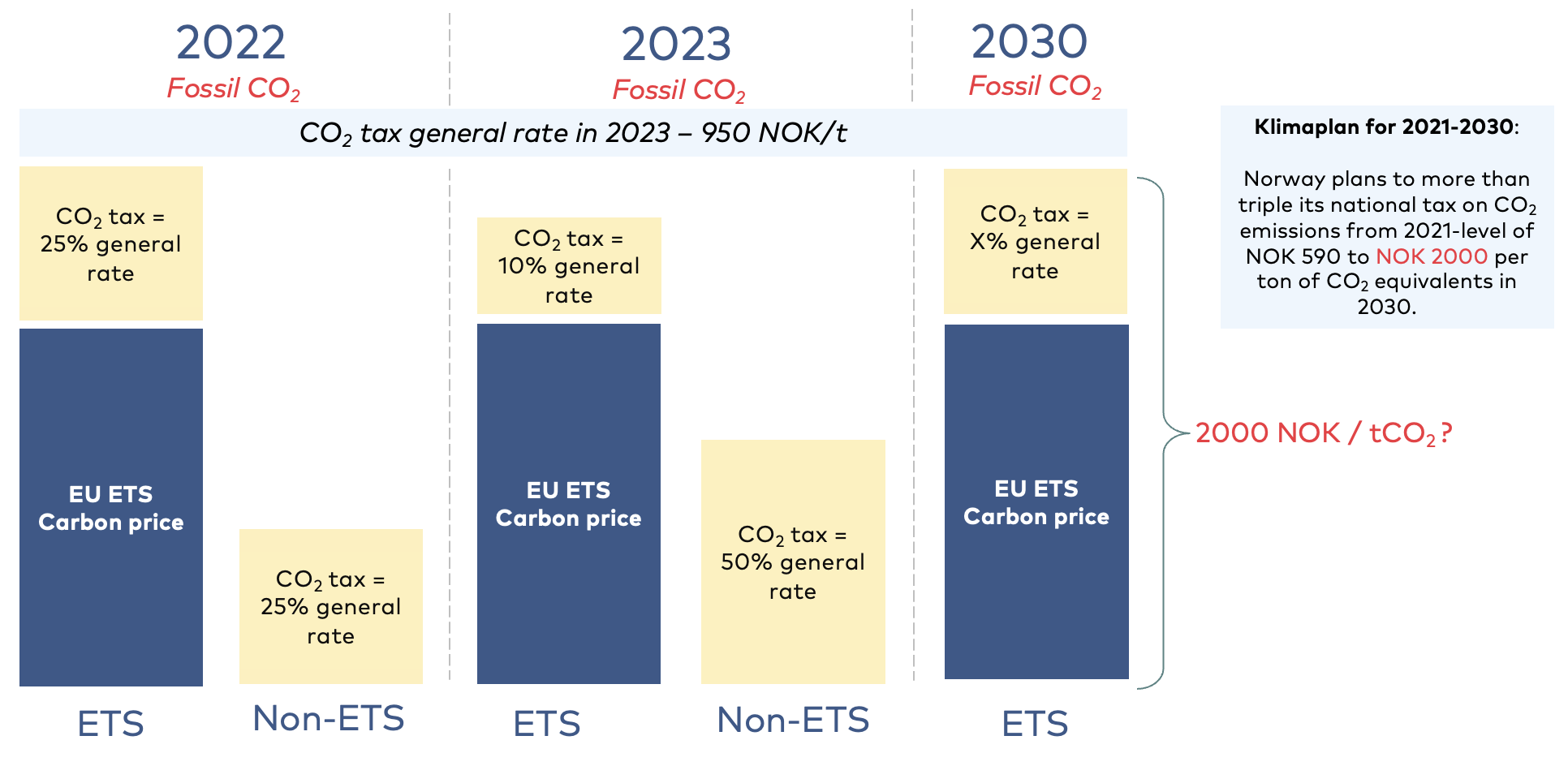

2.1.1 Norway

ETS

Emissions from waste incineration are included in the EU ETS if they result from “the combustion of fuels in installations with a total rated thermal input exceeding 20 MW (except in installations for the incineration of hazardous or municipal waste)”.

Directive 2003/87/EC of the European Parliament and of the Council of 13 October 2003 establishing a scheme for greenhouse gas emission allowance trading within the Community and amending Council Directive 96/61/EC (Text with EEA relevance), EP, CONSIL, 275 OJ L (2003). http://data.europa.eu/eli/dir/2003/87/oj/eng , Annex I (ETS Directive)

Directive 2010/75/EU of the European Parliament and of the Council of 24 November 2010 on industrial emissions (integrated pollution prevention and control) (recast) (Text with EEA relevance), EP, CONSIL, 334 OJ L (2010). http://data.europa.eu/eli/dir/2010/75/oj/eng

Taxes & Fees

Emissions from Norwegian municipal waste incinerators outside the EU ETS fall within the scope of the ESR, which establishes emissions reduction targets for non-ETS sectors. Under the climate agreement with the EU, Norway has agreed to cut its non-ETS emissions by 40% by 2030 compared to the 2005 level. This target can be achieved either through national cuts in emissions and/ or by using the flexibility mechanisms set out in the ESR. According to the National Climate Action Plan (Klimaplan), the Norwegian government plans to exceed the non-ETS target of 40%, aiming to reduce non-ETS emissions by 45% through domestic measures.

Meld. St. 13 (2020 – 2021) Report to the Storting (white paper) Norway’s Climate Action Plan for 2021–2030, 3.7.3.3.

Commission Implementing Decision (EU) 2019/2010 of 12 November 2019 establishing the best available techniques (BAT) conclusions, under Directive 2010/75/EU of the European Parliament and of the Council, for waste incineration, OJ/L 312/55. https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:32019D2010&from=EN

As of January 2022, Norwegian waste incineration installations pay a mandatory waste incineration tax that covers emissions to air of fossil CO2 when burning waste and is calculated by multiplying the amount of waste delivered to the incineration facility measured in tons by a factor of 0.5498 ton fossil CO2 per ton of waste, with the option to apply for facility-specific factors.

Waste incineration tax. (n.d.). The Norwegian Tax Administration. Retrieved October 12, 2023, from https://www.skatteetaten.no/en/business-and-organisation/vat-and-duties/excise-duties/about-the-excise-duties/avfallsforbrenning/

Climate Action Plan for 2021–2030

Figure 20 WtE: EU ETS and CO2 tax – Possible Scenario

2.1.2 Denmark

ETS

As of 1 January 2013, waste incineration plants which are primarily used for district heating were included in the EU ETS in Denmark.

EU Energy Union – Denmark’s National Energy and Climate Plan (NECP). (2020, January 13). Energistyrelsen. https://ens.dk/en/our-responsibilities/energy-climate-politics/eu-energy-union-denmarks-national-energy-and-climate , Annex 8

Taxes & Fees

In Denmark, several taxes apply to incineration. A waste heat tax is levied on the amount of heat produced from waste incineration, including heat used at the plant for indoor and water heating (20.7 DDK/GJ in 2022).

European Environmental Agency. (2022). Early warning assessment related to the 2025 targets for municipal waste and packaging waste—Denmark. https://www.eea.europa.eu/publications/many-eu-member-states/denmark/view

European Environmental Agency. (2022). Early warning assessment related to the 2025 targets for municipal waste and packaging waste—Denmark. https://www.eea.europa.eu/publications/many-eu-member-states/denmark/view

European Environmental Agency. (2022). Early warning assessment related to the 2025 targets for municipal waste and packaging waste—Denmark. https://www.eea.europa.eu/publications/many-eu-member-states/denmark/view

Ekspertgruppen for en grøn skattereform—1. Delrapport. (n.d.). Skatteministeriet. Retrieved October 23, 2023, from https://www.skm.dk/aktuelt/publikationer/rapporter/ekspertgruppen-for-en-groen-skattereform-1-delrapport/

2.1.3 Sweden

ETS

According to Article 24 of the EU ETS Directive, Member States may introduce additional institutions and emissions into the trading system, provided that the Commission and Member States give their approval.

Directive 2003/87/EC of the European Parliament and of the Council of 13 October 2003 establishing a scheme for greenhouse gas emission allowance trading within the Community and amending Council Directive 96/61/EC (Text with EEA relevance), EP, CONSIL, 275 OJ L (2003). http://data.europa.eu/eli/dir/2003/87/oj/eng

Emission Trading Ordinance (2004:1205); Bill 2005/06:184

COMMISSION DECISION of 7 July 2004 concerning the national allocation plan for the allocation of greenhouse gas emission allowances notified by Sweden in accordance with Directive 2003/87/EC of the European Parliament and of the Council, (2004). https://climate.ec.europa.eu/system/files/2016-11/sweden_final_en.pdf; COMMISSION DECISION of 23/01/2007 concerning the unilateral inclusion of additional activities by Sweden in the Community emissions allowance trading scheme pursuant to Article 24 of Directive 2003/87/EC of the European Parliament and of the Council, (2007). https://climate.ec.europa.eu/system/files/2016-11/sv2ndexclusions_en.pdf

Taxes and fees

Until recently, the CHP-sector, and thus also waste incineration, was burdened with a separate tax of 125 SEK per ton. The tax was waived with effect from January 2023, arguing that the intended control effects had not materialized. Without the tax, the government hopes that necessary investments in maintaining existing and building new CHP capacity will become more cost-effective.

Including the sector in the ETS scheme has led to a higher cost per ton incinerated waste as emission allowances increased in price. In 2022, the average cost was 740 SEK/ton, a 12% increase from 2021.

As mentioned above, not a lot of waste is landfilled anymore in Sweden. Apart from a landfill ban on sorted combustible waste in 2005, a ban on organic waste landfilling in 2005, and obligatory collection of food waste, a landfill tax has been in place since the year 2000, which in 2023 amounts to 634 SEK/ton.

Sector goals

Swedens national waste strategy defines a number of goals that will impact the waste incineration sector:

- By 2025, reuse and recycling of municipal waste shall increase to 55% by weight, with a further increase to 60% in 2030 and 65% in 2035, respectively. For 2020, around 40% were reached.Svensk Avfallshantering 2022. Avfall Sverige

- For non-hazardous building material, the corresponding goal is 70% by weight (up from 52% in 2020).

- The policy focus is therefore on reducing waste streams, increased reuse and more effective sorting and recycling. The role of waste incineration in the long term is thus limited to handling reject streams from sorting facilities, treating hazardous materials and provide end-of-use energy recovery from materials that cannot be recycled anymore.

In addition, the branch goal defined by Avfall Sverige in 2019 is to cut fossil emissions in half by 2030 and reduce them to close to zero by 2045.

2.1.4 Finland

Waste incineration and its emissions, as well as emissions of co-incineration are subject to regulation in Finland. Waste legislation is largely based on EU legislation but is stricter in some cases.

Legislation and instruments. (n.d.). EastCham Finland ry. Retrieved October 17, 2023, from https://www.eastcham.fi/finnishwastemanagement/municipal-solid-waste/legislation-and-instruments/

General Waste legislation:

- Waste Act (646/2021)

- Waste Decree (978/2021)

The environmental impacts of waste are also addressed in legislation on environmental protection:

- Environmental Protection Act (527/2014)

- Environmental Protection Decree (713/2014)

Finland has also a National Waste Plan to 2027 that sets objectives for waste management and waste prevention.

National Waste Plan. (n.d.). Ministry of the Environment. Retrieved October 17, 2023, from https://ym.fi/en/national-waste-plan

In a report,

Possibilities to impact CO2 emissions and to promote circular economy by different policy instruments targeting waste incineration. http://urn.fi/URN:ISBN:978-952-383-093-6

There have been negotiations about voluntary agreements (i.e., green deal) for waste incineration companies to decrease emissions, but it looks like the companies are willing to utilize new technologies to decrease emissions in the future.

A study on the impacts of inclusion of waste incineration in the EU ETS has been carried out. The report suggests that the ETS would not necessarily give the desired results on reducing incineration, minimizing production of wastes and improving recycling.

Including waste incineration in emission trading, Finnish Ministry of Economic Affairs and Employment 2023

2.1.5 Iceland

Iceland is a member of the EEA, which binds it to implement EU environmental directives. The country has a Waste Management Law no. 55/2003 and a Regulation no 737/2003 on waste treatment, which aim to decrease the quantity of waste by preventing the generation of waste, increase recycling, and recovery and reduce the quantity of waste deposited in landfills. Further regulation (no. 738/2003) provides for a ban on landfill and no. 739/2003 frames the incineration of waste. So far in the research, nothing pointed out that the waste incineration sector is included in the EU ETS.

2.2 European (and global) legislative framework

EU Legislation Specifically Applicable to Waste Incineration

Directive 2010/75/EU on industrial emissions (Industrial Emissions Directive or IED) lays down rules on integrated prevention, control or reduction of pollution arising from industrial activities, including waste management activities and energy industries.

Directive 2010/75/EU of the European Parliament and of the Council of 24 November 2010 on industrial emissions (integrated pollution prevention and control) (recast) (Text with EEA relevance), EP, CONSIL, 334 OJ L (2010). http://data.europa.eu/eli/dir/2010/75/oj/eng

Commission Implementing Decision (EU) 2019/2010 of 12 November 2019 establishing the best available techniques (BAT) conclusions, under Directive 2010/75/EU of the European Parliament and of the Council, for waste incineration (notified under document C(2019) 7987) (Text with EEA relevance), 312 OJ L (2019). http://data.europa.eu/eli/dec_impl/2019/2010/oj/eng

The EU ETS was established by the ETS Directive.

Directive 2003/87/EC of the European Parliament and of the Council of 13 October 2003 establishing a scheme for greenhouse gas emission allowance trading within the Community and amending Council Directive 96/61/EC (Text with EEA relevance), EP, CONSIL, 275 OJ L (2003). http://data.europa.eu/eli/dir/2003/87/oj/eng

European Commission. (2019). COMMISSION DELEGATED REGULATION (EU) 2019/ 331 determining transitional Union-wide rules for harmonised free allocation of emission allowances pursuant to Article 10a of Directive 2003/ 87/ EC of the European Parliament and of the Council. 62.

Directive 2003/87/EC of the European Parliament and of the Council of 13 October 2003 establishing a scheme for greenhouse gas emission allowance trading within the Community and amending Council Directive 96/61/EC (Text with EEA relevance), EP, CONSIL, 275 OJ L (2003). http://data.europa.eu/eli/dir/2003/87/oj/eng , Annex I (ETS Directive)

Directive 2010/75/EU of the European Parliament and of the Council of 24 November 2010 on industrial emissions (integrated pollution prevention and control) (recast) (Text with EEA relevance), EP, CONSIL, 334 OJ L (2010). http://data.europa.eu/eli/dir/2010/75/oj/eng

In the first half of 2023, important amendments were adopted to reform the EU ETS. As part of these developments, in June 2022, the European Parliament approved an inclusion of the municipal waste incineration sector in the ETS as of 2026, pricing waste incinerator’s fossil CO2 emissions with the aim of levelling the playing field within national ETS systems already covering the sector and incentivizing further decarbonization.

Amendments adopted by the European Parliament on 22 June 2022 on the proposal for a directive of the European Parliament and of the Council amending Directive 2003/87/EC establishing a system for greenhouse gas emission allowance trading within the Union, Decision (EU) 2015/1814 concerning the establishment and operation of a market stability reserve for the Union greenhouse gas emission trading scheme and Regulation (EU) 2015/757 (COM(2021)0551 – C9-0318/2021 – 2021/0211(COD)). Retrieved October 12, 2023, from https://www.europarl.europa.eu/doceo/document/TA-9-2022-0246_EN.html

EUR-Lex—32023R2122—EN - EUR-Lex. (n.d.). Retrieved November 28, 2023, from https://eur-lex.europa.eu/eli/reg_impl/2023/2122/oj

Other EU Laws Affecting Waste Incineration

Directive 2008/98/EC on waste (Waste Framework Directive or WFD) establishes the legal framework for treating waste in the EU. According to the WFD, the EU’s approach to waste management builds on the waste hierarchy defined in Article 4 of the WFD, which sets the following priority order: prevention, preparing for re-use, recycling, other recovery (i.e. energy recovery), and lastly, disposal.

Directive 2008/98/EC of the European Parliament and of the Council of 19 November 2008 on waste and repealing certain Directives (Text with EEA relevance), EP, CONSIL, 312 OJ L (2008). http://data.europa.eu/eli/dir/2008/98/oj/eng, art. 4

Directive (EU) 2018/851 of the European Parliament and of the Council of 30 May 2018 amending Directive 2008/98/EC on waste (Text with EEA relevance), CONSIL, EP, 150 OJ L (2018). http://data.europa.eu/eli/dir/2018/851/oj/eng

Directive (EU) 2018/851 of the European Parliament and of the Council of 30 May 2018 amending Directive 2008/98/EC on waste (Text with EEA relevance), CONSIL, EP, 150 OJ L (2018). http://data.europa.eu/eli/dir/2018/851/oj/eng, Annex IVa.

Directive 1999/31/EC on the landfill of waste (Landfill Directive) introduces stringent technical requirements to prevent, or reduce as much as possible, any negative impact from landfill. In addition, EU countries are required to implement national strategies to progressively reduce the amount of biodegradable waste sent to landfills. In 2018, amendments to the Landfill Directive introduced restrictions on landfilling from 2030 of all waste that is suitable for recycling or energy recovery, limited the share of municipal waste landfilled to less than 10% by 2035.

Directive (EU) 2018/850 of the European Parliament and of the Council of 30 May 2018 amending Directive 1999/31/EC on the landfill of waste (Text with EEA relevance), CONSIL, EP, 150 OJ L (2018). http://data.europa.eu/eli/dir/2018/850/oj/eng

Currently, the European Parliament and the Council are also discussing a proposal to update the EU legislation of cross-border waste shipments.

Waste shipments: Council ready to start talks with Parliament. (n.d.). Retrieved October 13, 2023, from https://www.consilium.europa.eu/en/press/press-releases/2023/05/24/waste-shipments-council-ready-to-start-talks-with-parliament/

The European Waste incineration sector may also see itself increasingly influenced by EU Climate Law and strategy. In December 2021 the EU Commission published a communication on sustainable carbon cycles, in which it, among other things, highlighted the need to push for innovation to capture CO2 and use it as feedstock for the production of fuel, chemicals and materials as well as to kick-start and upscale industrial carbon management approaches such as CCS and CDR (carbon dioxide removal) more generally.

COMMUNICATION FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL Sustainable Carbon Cycles, (2021). https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=COM:2021:800:FIN

2.3 The circular economy framework (with focus on the Nordics)

Turning waste into resources is an essential building block of the circular economy according to the European Commission.

From the point of view of the circular economy, utilization as a material takes precedence over waste incineration. The better the materials are recovered, the smaller proportion of them is burned. The recovery of plastic and wood in particular reduces the share of material with a high calorific value in incinerable waste, while bio-waste is poorly combustible and has a low calorific value due to its high-water content. In general, an improvement in the recycling rate leads to an increase in the proportion of unburnt material and relatively high ash concentrations in combustion.

In general, the share of waste going to incineration will decrease in all the Nordic countries.

Table 7 National goals related to the recycling of plastic waste

Sweden | Norway | Finland | Denmark | Iceland | |

Waste frame-works and goals |

|

|

|

|

|

On the other hand, valuable raw materials can be obtained from the ashes of waste incineration in the future. Nowadays the metals removed from ash can be calculated as recirculation, but utilization of other components of ash or ash in total cannot.