Cost and employment implications

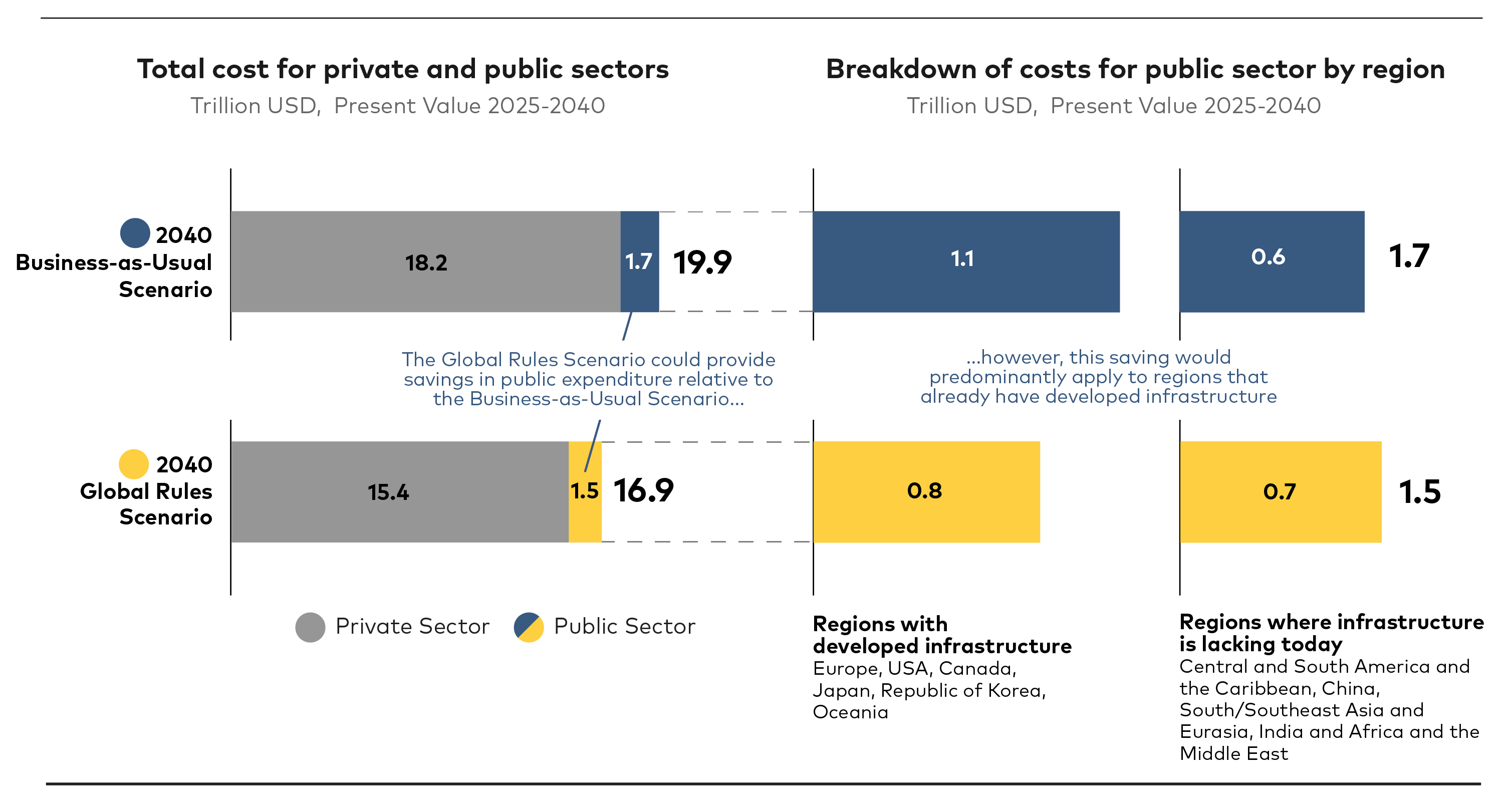

The Global Rules Scenario would yield important savings in public expenditure relative to the Business-as-Usual Scenario. The cumulative public expenditure from 2025 to 2040 in the Global Rules Scenario would total US$1.5 trillion, compared to US$1.7 trillion in the Business-as-Usual Scenario. The savings would mainly accrue from reductions in plastic volumes, resulting in less plastic waste to be collected and managed. However, this would primarily apply to regions with well-developed infrastructure; other regions would still need to invest in expanding their waste management systems.

Implementing the Global Rules Scenario would still require important investments from the public and private sectors.

This analysis estimates the inv

Collection, sorting and recycling should be maximised for all plastics not prevented, to minimise controlled disposal and reduce virgin plastic volumes.

estment requirements for annualised operating expenses (OpEx) and capital expenses (CapEx) at each step of the plastic lifecycle, as well as for alternative materials. These costs are then compared with total volume flows at each step of the plastic lifecycle or alternatives. However, the model does not include the costs of managing legacy plastics; the costs relating to externalities to health or biodiversity; or the impact of mismanaged plastics on industry (eg, fisheries, tourism, infrastructure). In addition, it does not include estimates for the investments required to launch solutions for microplastics, due to a lack of available data.

The Business-as-Usual Scenario would require significant investments from 2025 to 2040 to expand plastic production and conversion capacity. The overall cumulative estimate for the Business-as-Usual Scenario, considering OpEx and CapEx from 2025 to 2040, is US$20 trillion at present value (see Figure 17).

By contrast, the Global Rules Scenario would require lower levels of investment: the cumulative estimate for the Global Rules Scenario, considering OpEx and CapEx from 2025 to 2040, is US$17 trillion at present value. The main drivers would be the operational costs of virgin plastic production and conversion industries (to cover the remaining virgin plastics in the Global Rules Scenario); investments in production capacity for alternative materials; investments in expanding new business models (eg, reuse models); and investments in scaling collection, sorting, recycling and disposal infrastructure.

Of this US$ 17 trillion in the Global Rules Scenario, it is estimated that US$15.4 trillion would be covered by the private sector and US$1.5 trillion by governments.

Public spending is presenting as a total cost estimate, without balancing that cost versus revenues from EPR schemes or other policies.

Reducing plastic production, and hence waste to be collected and managed, would decrease public expenditure

The comparison of cumulative public expenditure between the Business-as-Usual Scenario and the Global Rules Scenario (see Figure 17) presents a different trend for regions that currently have well-developed waste infrastructure

In the analysis, Europe, the USA, Canada, Japan, the Republic of Korea and Oceania

In the analysis, Central and South America and the Caribbean, China, South/Southeast Asia, Central Asia, India and Africa and the Middle East.

The Global Rules Scenario would also require a lower level of investment from the private sector than the Business-as-Usual Scenario. This reduction would mainly be driven by lower production and conversion of virgin plastic, which require high investments. However, some of the investments in the Global Rules Scenario would be in new businesses or models (eg, reuse) that have yet to prove their economic viability and would thus have higher risk. Implementing the right policies across the five pillars discussed in this report would de-risk these investments and allow private capital to flow into the required solutions, such as reuse, material substitution, recycling and advanced sorting.

FIGURE 17

Estimated costs by scenario

Public expenditure from 2025–2040 in the Business-as-Usual Scenario would equate to $1.7 trillion at present value; while that under the Global Rules Scenario would equate to $1.5 trillion. This saving, however, would predominantly apply to high-income regions that already have well-developed infrastructure.

Figures show the net present value of OpEx and CapEx from 2025–2040 in the Business-as-Usual Scenario and the Global Rules Scenario, divided between the public sector (collection, sorting and disposal systems) and the private sector (production of plastic and substitute materials, recycling capacity, new business models such as reuse). All numbers are subject to rounding.

In the Global Rules Scenario, virgin plastic fees and EPR schemes would operate on a net cost basis. This means that fees would be set at a level that fully funds this public expenditure cost, while also allocating revenues for solutions across the plastic lifecycle. In practical terms, however, each region implementing these policies would need to conduct specific studies to ensure that fees are set at the right level in the local context, in order to account for any unintended consequences. In addition, these funds could be deployed to cover important areas that are not modelled in this study, such as research and innovation, testing to prevent health and biodiversity risks, and support for vulnerable communities.

New business models, substitute materials and recycling systems would generate employment through a shift away from virgin plastic

The Global Rules Scenario would have a net-neutral impact on employment at the global level. However, it would require a transition in labour between regions and industries from virgin plastic production to other materials and new models (e.g., reuse).

The analysis estimates annual employment by forecasting the number of jobs required at each stage of the plastic lifecycle for a given tonne of plastic. It also includes estimates for when plastic is substituted with other materials. However, the analysis does not provide an estimate of the regions in which most of these jobs will be created, as jobs linked to production would rely on international supply chains that are not modelled here. The analysis does not include estimates of how automation over time would impact employment creation by unit of output, by industry.

The Business-as-Usual Scenario would result in 12 million jobs by 2040. Most of these (80%) would be in the virgin plastic production and conversion industries, with the remainder in waste management. The Global Rules Scenario, with its virgin plastic reduction targets and uptake in recycled plastics, as well as new sustainable business models, would result in an equivalent number of 12 million jobs. These would be distributed among virgin plastic production and conversion (40%), new models such as reuse (16%), production of other materials (20%) and waste management (24%). Thus, the Global Rules Scenario would result in a transition of labour from plastic production and conversion to the production of other materials and new business models. This transition would not be balanced between industries or sectors; and importantly, it would not be balanced from a geographical perspective – some regions could end up losing employment. It would thus be critical to put in place controls to ensure a socially just transition, as this scale of change could have unintended consequences for livelihoods – particularly among vulnerable communities.