↑ Photos: iStock

7. Assessment

This section evaluates the shortlisted capacity mechanism designs from multiple perspectives aligned with key design objectives, including cross-border participation and opportunities for Nordic harmonisation. The analysis begins with a discussion of the general opportunities and challenges associated with capacity mechanisms, followed by an exploration of market-wide versus targeted approaches—two overarching design principles that shape the choice of mechanism. The evaluation framework is then introduced, outlining the assessment criteria applied to each design. Subsequently, each shortlisted mechanism is analysed in detail, considering both its internal coherence and external implications. The final part of the section focuses on interoperability, the potential for cross-border participation, and second-order building blocks necessary for implementation. This approach aims to provide a comprehensive understanding of the key trade-offs involved in mechanism selection.

7.1 Summary

Opportunities: CRMs and NFFSS offer several benefits, including:

- Enhanced financial incentives to spur new investments

- Improved system security

- Potentially broader capacity mix, improving stability and opening for targeting technology-specific solutions based on need

- Allowing tailoring of solutions to address local needs

Challenges: However, despite these advantages, they also introduce several challenges:

- They can be expensive

- Risk of theory and practice mismatch

- Risk of market distortion in the form of:

- Merit order distortion

- Crowding out effect - Risk of windfall profits

- Risk of perverse incentives

Main differences between market-wide and targeted mechanisms

Market-wide and targeted support schemes have different impacts on market dynamics. The choice between these two alternatives is one of the most critical initial decisions, as it influences the degree of market distortion and complexity, which in turn affects the risk of theory & practice mismatches.

Market-wide and targeted support schemes have different impacts on market dynamics. The choice between these two alternatives is one of the most critical initial decisions, as it influences the degree of market distortion and complexity, which in turn affects the risk of theory & practice mismatches.

Market-wide mechanisms remunerate all capacity providers, mitigating the crowding-out effect while compensating electricity generators for price distortions. While these mechanisms involve high-capacity payments, they are partly offset by lower and more stable consumer prices.

Targeted mechanisms, if not carefully designed (e.g., without restricting or ringfencing), can lead to significant crowding-out effects. Conversely, if ringfenced, they may contribute to merit order distortions. This trade-off is examined in detail in this chapter.

To better understand the risks associated with crowding-out effects, further analysis of investment behaviour and the determination of appropriate activation trigger prices is recommended. Mechanisms such as dispatchable flexible reserve should be designed based on insights from such studies.

Another key distinction between market-wide and targeted mechanisms is their complexity. Targeted mechanisms, while simpler, focus on direct financial support for specific capacity or flexibility gaps. In contrast, market-wide mechanisms involve higher financial stakes and are more susceptible to misalignment between theoretical design and market realities.

Assessment criteria

This chapter also evaluates the shortlisted designs against a set of predefined criteria (see Chapter 7.4). Exhibit 7.2 provides an overview of the key strengths and weaknesses of each design.

This chapter also evaluates the shortlisted designs against a set of predefined criteria (see Chapter 7.4). Exhibit 7.2 provides an overview of the key strengths and weaknesses of each design.

Interoperability, cross-border participation and Nordic harmonisation

In terms of interoperability, the assessment concludes that multiple market mechanisms can coexist, provided that their design minimises potential distortions. Implementing multiple market mechanisms simultaneously may even be beneficial to address distinct challenges.

In terms of interoperability, the assessment concludes that multiple market mechanisms can coexist, provided that their design minimises potential distortions. Implementing multiple market mechanisms simultaneously may even be beneficial to address distinct challenges.

Furthermore, the chapter examines cross-border participation, concluding that while this is generally beneficial, it introduces specific challenges that must be carefully addressed. For some targeted mechanisms, domestic security of supply might take priority, making cross-border participation less suitable in certain cases.

Several other aspects of harmonisation could also provide benefits to the Nordic region, including:

- Standardised needs assessments, improving coordination across markets.

- Common procurement platforms, facilitating efficiency and transparency.

- Harmonised regulatory frameworks, reducing market fragmentation.

The assessment highlights the advantages of harmonisation in these areas while acknowledging the complexities involved.

The final section of this chapter examines second-order design elements, drawing lessons from existing CRMs in Europe. Many European mechanisms have faced challenges due to suboptimal design choices at this level. Getting these elements right is crucial for ensuring a well-functioning mechanism. Key elements include:

- Contract duration and lead-times, ensuring investor confidence and operational feasibility.

- Short market time units, incentivising a diverse mix of flexibility resources.

- Balanced penalty structures for non-delivery, maintaining market discipline while avoiding excessive financial risk.

These insights provide a foundation for designing potential future CRM or NFFSS for the Nordic Region.

7.2 Opportunities and challenges

Capacity mechanisms and NFFSS, are designed to address the missing money problem, ensuring sufficient investment in generation and flexibility resources. However, these mechanisms come with inherent trade-offs. Decision-makers must carefully consider the synergies, risks, and unintended consequences of introducing additional market mechanisms on top of the existing energy-only market structure in the Nordic region.

Before evaluating specific designs, this chapter outlines the key opportunities and challenges associated with capacity mechanisms and NFFSS, setting the stage for the subsequent assessment.

7.2.1 Opportunities

Implementing capacity mechanisms or NFFSS can unlock several benefits, including:

- Enhanced financial incentives: Provides additional revenue streams for maintaining existing resources and promote investments in new generation, storage or DSR.

- Improved system security: Ensuring resource availability during critical system stress periods, supporting security of supply.

- Stable and predictable capacity: Allows remuneration to be structured based on availability likelihood, using derating factors to ensure sufficient reliable capacity.

- Targeting specific technology: Enables targeted support for innovative solutions, fostering the transition towards net-zero goals.

- Addressing local needs: Allows tailoring to specific local, domestic or regional requirements, complementing existing market structures.

7.2.2 Challenges

Despite their advantages, capacity mechanisms and NFFSS introduce several challenges that must be addressed to ensure their effectiveness:

- Expensive: Requires substantial payments, ultimately borne by consumers or taxpayers, without guaranteeing solving the problem.

- Theory & practice mismatch: Market behaviours are difficult to predict – design choices and country-specific circumstances can lead to unexpected and unwanted outcomes.

- Market distortion:

- Merit order distortion: Occurs when higher-margin assets are dispatched before lower-margin ones.

- Crowding-out effect: Risk of displacing merchant investments, potentially failing to increase the total amount of new capacity in the system.

- Low resource utilisation: Targeted mechanisms risk inefficient use of awarded assets if not properly designed.

- Slippery slope effect: Authorities may be tempted to expand the mechanism’s use beyond its original intent and dispatch the providers more often, increasing market distortions.

- Over procurement: Difficulties in accurately predicting future capacity and flexibility needs may lead to over-procurement.

- Windfall profits: Revenue uncertainties can result in some participants earning significantly higher-than-expected returns, raising concerns over fairness and efficiency.

- Risk of perverse incentives: Market participants may engage in strategic behaviour to exploit the mechanism for financial gain, such as deliberately decommissioning assets to qualify for new investment support, rather than genuinely adding new capacity.

Conclusion

Capacity mechanisms and NFFSS can be useful tools for ensuring resource adequacy and system flexibility, but their implementation requires careful balancing of benefits and risks. Poorly designed mechanisms can lead to high costs, inefficiencies, and unintended market distortions that may undermine the effectiveness of the energy-only market.

Understanding these challenges is crucial, as misaligned policies risk creating a dependency on capacity payments, reducing market efficiency and leading to a negative spiral where competitive price signals weaken over time. Thoughtful design choices will be key to ensuring that these mechanisms complement, rather than compromise, the long-term sustainability of the electricity market.

7.3 Market-wide vs. targeted mechanisms

Before evaluating individual designs, this chapter examines the fundamental differences between market-wide and targeted mechanisms, as these categories represent two distinct approaches. The choice between these alternatives is one of the most critical initial decisions, as it significantly influences market dynamics, cost distribution, and system efficiency.

This chapter will compare market-wide and targeted mechanisms. The assessment focuses on opportunities and challenges where it differs between the two mechanisms.

7.3.1 Market-wide mechanisms

Market-wide mechanisms provide capacity payments to all eligible assets, including both existing generation and new investments, as long as they commit to delivering capacity within a specified timeframe (e.g., four years ahead). This broad participation enhances market liquidity but may also result in higher total payments and potential over-procurement.

Opportunities:

- Avoids the crowding-out effect, if implemented efficiently, since all capacity providers receive payments, reducing the risk of investment displacement.

- Compensates for the price distortion effect (lower prices) more evenly across the market, preventing disproportionate impacts on specific asset classes.

- Ultimately leads to lower wholesale prices for consumers, offsetting some of, or all, the costs associated with capacity payments.

- Facilitates efficient dispatching and utilisation of assets, as payments apply to all market participants, allowing for market-driven optimisation.

Challenges:

- Expensive: Since the entire market is remunerated, the capacity payments will be very high. In other words, high financial stakes are required that ultimately may burden consumers or taxpayers.

- Theory & practice mismatch: The complexity of market-wide capacity mechanisms, combined with the risk of suboptimal design choices, makes these schemes particularly vulnerable to failing in their intended purpose. In the worst case, they may be unable to secure any additional capacity at all.

- Increases administrative and operational complexity for all, as implementation requires extensive coordination and monitoring.

- Derating factor: Determining accurate capacity contributions (derating factors) is challenging, especially for hydropower, where seasonal variations significantly affect its role in system security. While this challenge exists for both market-wide and targeted mechanisms, it is far more pronounced in market-wide schemes. Since all existing capacity must be derated correctly, inaccuracies can significantly distort procurement outcomes, impacting both fairness and the total amount of capacity secured.

7.3.2 Targeted mechanisms

Targeted schemes, in contrast, restrict capacity payments to a specific subset of the market. This could be based on factors such as location, technology type, or the need for new investments. By limiting payments to only those resources deemed necessary, targeted mechanisms aim to reduce overall costs and better align with policy objectives, such as promoting non-fossil flexibility solutions.

While traditional CRMs can be classified as either market-wide or targeted, NFFSS mechanisms are inherently targeted due to their regulatory framework.

Opportunities:

- Limited theory & practice mismatch: A simpler and more pragmatic approach, reducing the risk of unintended outcomes due to market unpredictability.

- Efficiency through selective payments: Targeted mechanisms follow a more straightforward approach by directing payments only to the specific resources needed, rather than compensating all available capacity. This contrasts with market-wide mechanisms, where payments are distributed across all resources. By focusing only on selected capacity, targeted mechanisms can be more efficient and cost-effective, ensuring that payments go directly to securing the required assets.

- Lower financial stakes: Total payments are limited, as compensation is directed toward a specific subset of capacity rather than the entire market.

- Enables precise targeting of technologies or needs, fostering innovation and ensuring alignment with policy goals.

Challenges:

- Market price distortion and crowding-out risks (if not ringfenced): Assets that receive targeted capacity payments while simultaneously participating in regular market operations pose a significant risk of market price distortion and crowding out other resources. This can undermine market efficiency and, in the worst case, result in little to no additional capacity being secured. This is the primary challenge of targeted mechanisms, which is why CRMs are typically ringfenced when targeted, such as strategic reserves, ensuring they are only dispatched when other resources have been exhausted. However, most of the state aid-approved flexibility support schemes implemented in recent years have been targeted but not ringfenced. Their approval in the EU can largely be attributed to the timing, during the energy crisis, and the urgent need for additional flexibility in the countries where they were introduced.

- Risk of low resource utilisation (if ringfenced or restricted): Ringfenced or restricted mechanisms ensure security of supply but risk paying for resources that are rarely or never used. Low utilisation of low margin resources can cause merit order distortion. This is raising concerns about cost-effectiveness and market efficiency. If allowed to operate based on marginal costs, they could reduce price spikes, although that is not their intended role. However, this would interfere with market signals that drive private investment in new capacity, causing crowing-out effect.

- Slippery slope effect: Policymakers may be tempted to change the rules and dispatch the reserve more often, causing more market distortion than initially intended.

- Risk of perverse incentives, where existing assets strategically decommission to qualify for capacity payments as new investments.

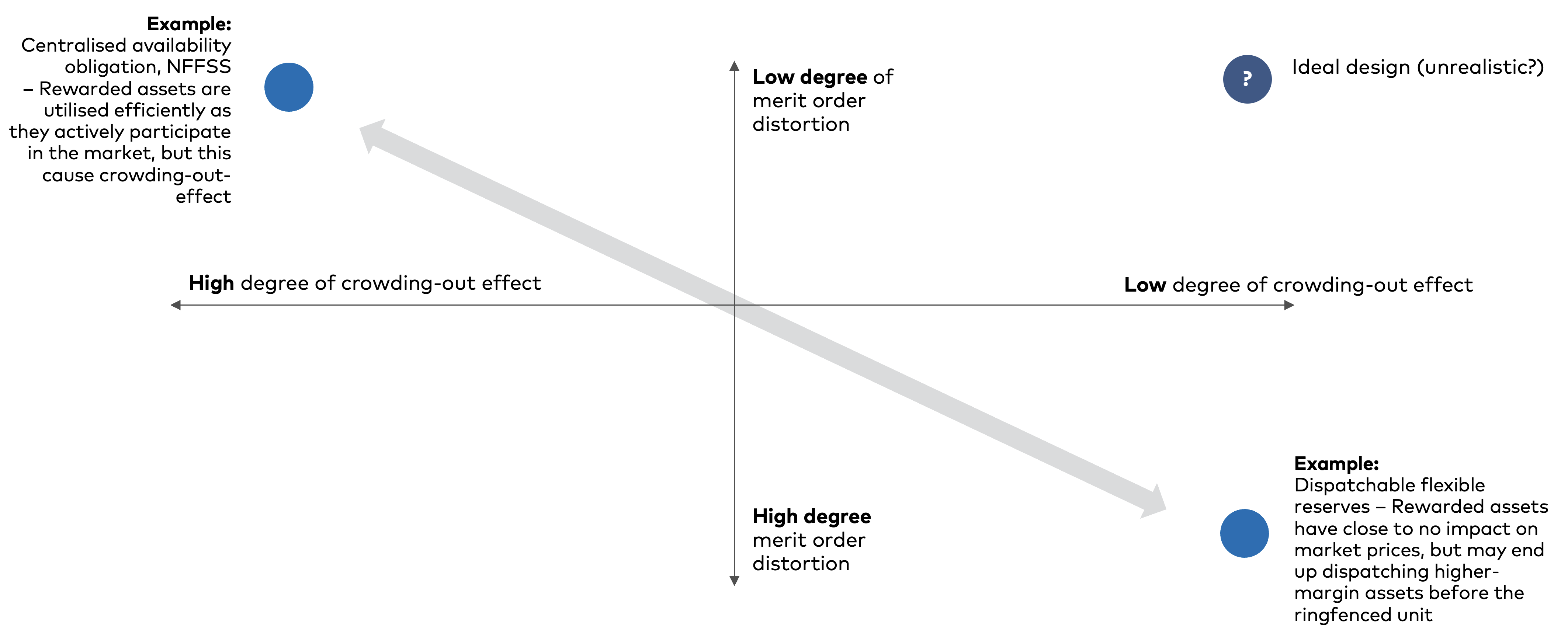

The primary trade-off in designing targeted mechanisms lies between the crowding-out effect and merit order distortion. Completely ringfencing an asset eliminates the crowding-out effect but risks dispatching higher-margin assets or resorting to costlier interventions, such as load curtailment, instead of utilising the ringfenced unit.

Designing a targeted mechanisms that simultaneously minimises market distortions and ensures efficient resource utilisation is inherently challenging, as these two objectives often conflict with each other. The following Exhibit 7.1 illustrates this trade-off.

Exhibit 7.1 – Trade-off between the crowding-out effect and merit order distortion

Source: AFRY.

The theoretical dilemma outlined above assumes perfect information and rational decision-making based on market fundamentals. However, this assumption is debatable. It is worth investigating to what extent investors base their decisions on the expectation that energy prices will reflect VoLL during scarcity periods.

There is significant uncertainty regarding how frequently, if ever, the market fails to reach equilibrium, resulting in scarcity events with prices at VoLL. Some investors may not even expect prices to reach the market’s maximum price. For instance, SDAC currently caps prices at €4,000, a threshold not derived from VoLL but rather intended to mitigate buyers' financial exposure and bankruptcy risks. This cap is not guaranteed to remain unchanged and could be adjusted in either direction. By contrast, the intraday continuous market has a higher cap of €10,000, arguably allowing for pricing at VoLL in a Nordic context. However, reaching such extreme price levels raises the question of whether the resources offering flexibility at these prices are genuinely reflecting their costs or simply acting opportunistically.

Ultimately, preventing the activation of a ringfenced or restricted unit at a high but sub-maximal price, such as the SDAC cap of €4,000, does not necessarily cause a crowding-out effect. While it may limit the potential revenues of other flexible units bidding into the SIDC market at higher prices, the issue becomes one of fairness rather than market efficiency. This shifts the trade-off: activating a ringfenced or restricted unit at a price below VoLL does not crowd out other resources but instead prevents certain assets from capturing additional profits.

This remains speculative, and it is recommended that decision-makers conduct further analysis to understand investment behaviour better and determine appropriate activation trigger prices. The design of mechanisms such as dispatchable flexible reserve should reflect the insights gained from such studies.

7.4 Assessment criteria

As different market designs is explored in the following chapters, it is essential to establish a structured framework for evaluation. The assessment criteria outlined in this chapter provide a consistent basis for comparing and contrasting the proposed designs against the key objectives of an effective market structure. These criteria ensure that the chosen market design aligns with broader policy goals, supports the integration of non-fossil flexibility solutions, and maintains a well-functioning, efficient, and fair electricity market.

The assessment criteria are directly linked to the overarching design objectives and will be systematically applied to each of the shortlisted market designs. This structured approach ensures a transparent and balanced evaluation, highlighting the strengths and potential trade-offs of each alternative. A more comprehensive overview is provided in Annex A.

7.4.1 Overview of criteria

- Low degree of distortion: The solution should have a neutral or positive impact on existing business models and price signals, respecting past investments.

- Market efficiency and inclusivity: Ensures capacity is delivered at the lowest cost by fostering liquidity, innovation, and broad market participation.

- Resource efficiency: Maximises the utilisation of procured generation, storage, and DSR resources at both national and Nordic levels.

- Effectiveness (in a Nordic context): Ensures security of supply in a robust and reliable manner, independent of cost and complexity considerations.

- Non-fossil: Evaluates the extent to which the design promotes or prioritises non-fossil flexibility solutions.

- Transparency: Enhances market confidence by promoting clear decision-making, participation rules, and price formation mechanisms.

- Investor confidence: Provides sufficient incentives for investment while ensuring appropriate risk allocation for market participants.

- Practical

- Ease of implementation: Considers technical, political, and regulatory complexity, as well as feasibility within a reasonable timeframe.

- Operational simplicity: Assesses the ease of compliance, administration, and overall usability for both market participants and operators.

By systematically applying these assessment criteria to each shortlisted market design, an accurate and objective evaluation process is ensured. This approach enables a clear identification of trade-offs, synergies, and potential risks associated with different market structures. The evaluation framework provides a structured comparison, ensuring that each design is assessed in a transparent and comprehensive manner.

The upcoming chapters will evaluate each design against these criteria, ultimately guiding the selection of the most suitable approach to address varying adequacy needs. The assessment is structured into primary objectives, which represent the fundamental goals of the market design, and secondary objectives & design constraints, which encompass additional factors influencing feasibility, implementation, and operational effectiveness.

7.5 Assessment based on criteria

Each market mechanism presents trade-offs between different objectives. Centralised mechanisms (centralised availability obligation and centralised reliability option) offer liquidity and stability but can suppress price signals and require strong regulatory oversight. Decentralised reliability option allows more market-driven decisions but introduce transparency and coordination challenges. Strategic reserve 2.0 is highly targeted, minimising market distortions but restricting resource flexibility, while a dispatchable flexible reserve provides higher degree of flexibility but have higher degree of merit order distortion.

The chosen mechanism should ultimately strike a balance between the various criteria, ensuring market efficiency, optimal resource utilisation, and security of supply, while also promoting non-fossil resources and a fair distribution of costs and benefits.

Exhibit 7.2 provides a high-level overview of the strengths and weaknesses of different designs, supporting decision-making in achieving the optimal balance for the Nordic context while addressing country-specific needs.

Exhibit 7.2 – Assessment based on first order building blocks

The table give a high-level overview of the different strengths and weaknesses of different designs

The table give a high-level overview of the different strengths and weaknesses of different designs

Low degree of distortion | Market efficiency and inclusivity | Resource efficiency | Effectiveness (in a Nordic context) | Non-fossil | Transparency | Investor confidence | Practical* | |||

|---|---|---|---|---|---|---|---|---|---|---|

CRM | Centralised availability obligation | |||||||||

Centralised reliability option | ||||||||||

Decentralised reliability option | ||||||||||

T | Strategic reserve 2.0 | |||||||||

NFFSS | Centralised availability obligation | |||||||||

FRR availability obligation | ||||||||||

Dispatchable flexible reserve |

Source: AFRY.

* ease of implementtion and operational simplicity

* ease of implementtion and operational simplicity

The following sub-section explains the rationale behind the scoring of different designs against the specified criteria in the table above.

7.5.1 Low degree of distortion

Market-wide CRMs exhibit a low degree of distortion, both in terms of crowding-out effects and merit order distortion, assuming they function as intended. However, this is seldom the case in practice, preventing them from achieving the highest possible score.

Strategic reserve 2.0 ranks highest in this category as it is entirely ringfenced and targets high-margin units, effectively limiting merit order distortion. Conversely, the targeted centralised availability obligation, i.e. NFFSS version, receives the lowest score due to its high level of market distortion by design, as it supports units that can operate freely in the wholesale market. This is a key reason why this mechanism is not recommended.

Dispatchable flexible reserve rank just below strategic reserve 2.0, as they permit dispatch not only as a last resort but also at a predefined high price. Furthermore, their restriction to new investments increases the risk of ringfencing low-margin units, which, in some cases, might otherwise have been dispatched in the market.

7.5.2 Market efficiency and inclusivity

Market-wide CRMs score relatively low in comparison to targeted mechanisms. While they enable broad participation, they may disproportionately favour incumbent players and established technologies. One notable challenge is defining the derating factor for hydropower with storage in hydro-dominant markets. Scarcity in these markets typically occurs during dry years, making it more of an energy issue than a capacity issue. This limitation is particularly pronounced in market-wide CRMs.

Additionally, these mechanisms have historically been sensitive to design failures, resulting in substantial costs due to the high-capacity payments embedded in the scheme.

In contrast, the NFFSS, being inherently targeted, mitigates these risks by compensating only for the required capacity or flexibility. Compared to strategic reserve 2.0, the NFFSS is specifically designed to incentivise new investments, thereby enhancing market liquidity and fostering innovation.

7.5.3 Resources efficiency

Market-wide CRMs generally promote efficient resource use, as they allow the awarded units to participate freely in the market. However, the FRR availability obligation risks ringfencing units that might otherwise be optimally deployed in other markets. Similarly, dispatchable flexible reserve carry a risk of underutilising flexible assets.

7.5.4 Effectiveness (in a Nordic context)

Strategic reserve 2.0 and dispatchable flexible reserve are considered the most effective mechanisms for ensuring security of supply in a robust and reliable manner. These mechanisms directly target resources capable of addressing the problem, and since they do not cause crowding-out effects, they contribute to securing supply provided they attract the right resources and are operated efficiently.

The FRR availability obligation also scores highly due to its targeted nature. However, it may displace other investments, reducing its overall effectiveness compared to a ringfenced alternative.

The NFFSS version of the centralised availability obligation, despite being a targeted mechanism, scores lower due to its crowding-out effects. By displacing other investments, it may fail to secure the intended capacity.

Market-wide CRMs generally score lower due to the mismatch between theoretical expectations and practical implementation, as discussed earlier in this chapter. The centralised reliability option is considered somewhat more efficient than the availability obligation due to its stronger financial incentives for delivery during scarcity periods. The decentralised reliability option is slightly less effective, as it is market-driven and more susceptible to under-procurement, whereas centralised CRMs tend to lean towards over-procurement.

7.5.5 Non-fossil

NFFSS mechanisms are explicitly designed to incentivise non-fossil resources, whereas CRMs do not inherently impose such restrictions. However, eligibility criteria can be used to encourage non-fossil participation within CRMs. Implementing this approach, however, can introduce new complexities, such as difficulties in attracting sufficient capacity, particularly in the case of strategic reserve 2.0.

7.5.6 Transparency

All mechanisms can be designed to ensure transparency. However, decentralised reliability option is generally considered less transparent due to their reliance on over-the-counter (OTC) trading and their inherent complexity.

7.5.7 Investor confidence

The centralised availability obligation provides predictability through centralised procurement, though it may favour established providers over new entrants.

The centralised reliability obligation offers stability but increases investors' risk exposure due to strike price uncertainty.

The decentralised reliability option presents higher counterparty risks, making it less attractive for investors.

strategic reserve 2.0 offers stability through fixed payments, with activations compensated by cost-based payments, yet they do not directly incentivise new investments.

The NFFSS version of the centralised availability obligation allows for fixed long-term contracts, which provide stability, but revenue estimation from market participation remains challenging.

Dispatchable flexible reserve also provides stability through fixed payments, with activations compensated through cost-based mechanisms.

Finally, the FRR availability obligation ensures stability through TSO-backed payments, with potential financial upside from market participation.

7.5.8 Practical (ease of implementation and operational simplicity)

Targeted mechanisms are generally easier to monitor and operate due to the limited number of assets involved. Strategic reserve 2.0 and the FRR availability obligation are particularly straightforward to implement, as they closely resemble existing mechanisms within the Nordic market.

By contrast, centralised CRMs are relatively complex, as they would introduce an entirely new framework into the Nordic system. These mechanisms require the definition of derating factors, a challenge that has proven difficult in other markets, and involve the operational complexity of monitoring all participating assets.

Decentralised reliability obligations are considered even less practical due to their innovative nature and the lack of practical implementation examples to draw from.

7.6 Interoperability

In some cases, implementing multiple market mechanisms simultaneously may be beneficial to address distinct challenges within the power market. While there are currently no indications that any Nordic market is pursuing such an approach, nor any formal recommendations to do so in the near future, it is important to explore the feasibility of such a setup. Ensuring that regulatory frameworks do not preclude future implementation can help preserve flexibility in policy design.

This chapter analyses the interoperability of different mechanisms, with a focus on CRMs and NFFSS. The key finding is that combining these mechanisms should not present fundamental obstacles, provided that implementation is carefully designed.

No regulatory blockers

Current EU regulations permit the simultaneous implementation of CRMs and NFFSS. Specifically:

Current EU regulations permit the simultaneous implementation of CRMs and NFFSS. Specifically:

- Paragraph 1, Article 19g of the Electricity Regulation states:

“… Member States which apply a capacity mechanism shall consider making the necessary adaptations in the design of the capacity mechanisms to promote the participation of non-fossil flexibility such as demand-side response and energy storage, without prejudice to the possibility for those Member States to use the non-fossil flexibility support schemes referred to in this paragraph.” - Paragraph 2, Article 19g further clarifies that:

“The possibility for Member States to apply non-fossil flexibility support measures pursuant to paragraph 1 of this Article shall not preclude Member States from addressing their indicative national objectives defined pursuant to Article 19f by other means.”

The regulation allows for the parallel implementation of CRMs and NFFSS, provided that their design is adapted to ensure effective participation and avoid unintended consequences. The regulation does suggest that the CRM design (if already in place) could be adjusted to also include assets that could potentially be procured via a NFFSS, instead of having both.

Existing examples of multiple mechanisms in operation

Several markets have already implemented both flexibility support schemes and CRMs (Ireland, France, Italy), demonstrating that coexistence is feasible. This can be seen from the overview in Chapter 5, Exhibit 5.2.

Several markets have already implemented both flexibility support schemes and CRMs (Ireland, France, Italy), demonstrating that coexistence is feasible. This can be seen from the overview in Chapter 5, Exhibit 5.2.

Practical considerations and risks

From a technical and regulatory standpoint, there are no inherent barriers to operating CRMs and NFFSS in parallel. For instance, a market-wide CRM could be implemented to address adequacy concerns, while a targeted NFFSS could be introduced to incentivise specific types of flexibility.

From a technical and regulatory standpoint, there are no inherent barriers to operating CRMs and NFFSS in parallel. For instance, a market-wide CRM could be implemented to address adequacy concerns, while a targeted NFFSS could be introduced to incentivise specific types of flexibility.

However, challenges may arise in terms of market interactions and behavioural responses, including:

- Potential for double payments: Without clear design rules, assets could seek remuneration from both mechanisms, potentially leading to inefficiencies. Proper structuring and eligibility criteria can mitigate this risk.

- Risk of over-procurement: While different mechanisms may target distinct challenges, they may also address overlapping issues. For example, an NFFSS designed to incentivise flexible assets could inadvertently contribute to system adequacy, reducing the need for a CRM. If not carefully accounted for, this could lead to excessive capacity procurement and unnecessary costs.

Conclusion

The interoperability of multiple market mechanisms is feasible, provided that the design is carefully structured to avoid distortions. While regulatory frameworks allow for the coexistence of CRMs and NFFSS, successful implementation requires a clear strategy to prevent double payments, ensure cost efficiency, and manage interactions between mechanisms.

The interoperability of multiple market mechanisms is feasible, provided that the design is carefully structured to avoid distortions. While regulatory frameworks allow for the coexistence of CRMs and NFFSS, successful implementation requires a clear strategy to prevent double payments, ensure cost efficiency, and manage interactions between mechanisms.

Future policy considerations should focus on dynamic market monitoring, ensuring that flexibility incentives remain aligned with overall adequacy goals without creating inefficiencies or unnecessary redundancies.

7.7 Nordic harmonisation

7.7.1 Cross-border participation

Both the regulation covering CRMs and NFFSS, as well as state aid rules, require the mechanisms to promote cross-border participation. CRM regulations impose stricter standards, while NFFSS guidelines may be perceived as less rigid. Cross-border participation can have big impact on the efficiency of the mechanisms and impact both the country implementing the mechanisms and its neighbouring countries. For the Nordic, this is particularly true, considering the close connected nature of the markets.

Rational for cross-border participation

The rationale behind these requirements is to prevent negative distortions in neighbouring markets and to improve global welfare. It is particularly true for market-wide mechanisms, as they are designed to compensate all generation and flexibility providers that commit to being available during periods of scarcity. Given the interconnected nature of the European electricity market through market coupling, assets in neighbouring markets inherently contribute to system adequacy whenever cross-border transmission capacity is available.

Unless interconnection constraints prevent power flows at the time of critical need, or if the neighbouring market is also facing stress conditions, external capacity will support the region security of supply. In cases where both markets are under strain, electricity should ideally flow to the market with the highest VoLL, though VoLL may not always accurately reflect the true willingness to pay. Alternatively, there may be no flow between markets, which some may perceive as the fairest solution in situations of widespread scarcity.

Considering this, the following outlines key risks of market distortions in neighbouring countries if cross-border participation is excluded, especially in market-wide mechanisms:

Market fragmentation and inefficient capacity allocation: By excluding foreign capacity providers, a CRM effectively limits competition to domestic participants, potentially leading to over-procurement and higher costs for consumers in the implementing country. Meanwhile, surplus capacity in neighbouring countries remains unaccounted for, despite being available to contribute to system adequacy. This fragmentation prevents optimal resource sharing across borders, reducing the overall efficiency of capacity allocation in the region.

Market distortion in the form of crowing-out effect: If a country implements a CRM without allowing foreign participation, domestic generators receive additional revenues, enabling them to bid lower in the wholesale market. This can suppress electricity prices, which in turn affects generators in neighbouring countries that do not benefit from the CRM. As a result, investors in those markets may face reduced profitability. This effect could ultimately lead to unintended consequences for both markets, where the effect of the CRM is reduced.

Misallocation of investments: Neighbouring markets that are interconnected but excluded from a CRM may experience distorted investment signals. If generators in the CRM country receive guaranteed capacity payments while those in neighbouring markets rely solely on market revenues, investors may be incentivised to prioritise capacity expansion in the CRM country rather than in locations where it could be more efficient from an energy-only perspective. This can lead to an unbalanced distribution of resources and underinvestment in flexible capacity where it is needed most.

Inefficient interconnector use and distorted trade flows: A market-wide CRM without cross-border participation may alter electricity trade patterns by making domestic capacity artificially competitive. Since the CRM country’s generators receive additional payments, they can afford to offer lower prices in the wholesale markets, potentially crowing-out imports that would otherwise be cost-effective. This reduces the efficient use of interconnectors, leading to suboptimal cross-border electricity flows and increasing the risk of uneconomic exports or imports that do not reflect the true underlying cost of supply.

Spillover effects on security of supply in neighbouring countries: If a CRM over-procures capacity domestically while excluding foreign participation, it may inadvertently reduce the incentives for investment in neighbouring markets. This could result in reduced security of supply in those countries, making them more reliant on imports during stress events.

Challenges with cross-border participation

While cross-border participation within CRMs and NFFSS is ensuring efficient capacity allocation and minimising market distortions across countries, it introduces several practical and regulatory challenges. The nature and severity of these challenges can vary depending on whether the mechanism is market-wide or targeted.

Incomplete mitigation: Cross-border participation does not fully mitigate the negative externalities of capacity markets on neighbouring consumers, generators, and interconnectors.

Unfair welfare distribution: The distribution of welfare may be perceived as unfair to consumers in the implementing market, as they indirectly remunerate capacity abroad. In Belgium, 47% of capacity awarded contracts during last auction in 2024 were located outside of Belgium, meaning Belgian consumers are remunerating Dutch and German generators.

Domestic security of supply: Depending on the availability of interconnectors during periods of scarcity, cross-border participation may undermine the primary objective of ensuring domestic security of supply. Even if foreign assets are technically available, the ability to deliver their capacity depends on the availability of transmission capacity during a scarcity event.

Political risk: In the long run, there is a political risk that there might be less available cross-zonal interconnection than today.

Regulatory compliance: Monitoring and enforcing commitments from foreign capacity providers can be challenging, as these assets operate under a different regulatory authority. Mechanisms must be established to verify that foreign capacity is:

- Available when needed.

- Not simultaneously committed to another mechanism in its home market.

- Delivering its promised contribution during system stress events.

Risk of unequal treatment: Market-wide CRMs typically set uniform remuneration levels for all participating assets. However, foreign capacity may face different cost structures, such as different regulatory charges or support mechanisms in their home market. If these differences are not accounted for, the CRM could unintentionally favour either domestic or foreign capacity, distorting investment signals.

Complexity of capacity contribution calculation: Market-wide CRMs require robust methodologies to determine the contribution of foreign capacity to system adequacy. This involves modelling probabilistic availability, considering potential scarcity events in both markets, and assessing how cross-border flows behave under stress conditions. Failure to account for these factors correctly could lead to over- or under-procurement of capacity.

Risk of reduced effectiveness of targeted schemes: Targeted mechanisms are often implemented to correct specific domestic missing money problem. Allowing foreign capacity participation could weaken the intended impact. For instance, if a targeted mechanism is aimed at addressing local flexibility shortfalls, but a significant portion of the contracted capacity comes from foreign sources, the scheme may fail to deliver the intended reliability benefits.

7.7.2 Harmonised needs assessment

Today, each Nordic country conducts its own capacity adequacy assessment and flexibility needs assessment, using different methodologies, assumptions, and risk tolerances to determine how much capacity is required to ensure security of supply. When integrating cross-border participation in capacity mechanisms or NFFSS, these differences can create several challenges:

Inconsistent definitions of adequacy: Some markets assess adequacy based on loss of load expectation (LoLE), while others may use expected energy not served (EENS) or different reliability criteria. This variation can lead to misalignment in how much capacity is deemed necessary and which resources qualify for support.

Diverging risk assumptions: Capacity adequacy assessments often rely on assumptions about peak demand, weather conditions, interconnector availability, and generator outages. If a foreign capacity provider is assessed under a less conservative methodology than the importing country’s mechanism, it might not be as reliable as expected during stress periods.

Timing of needs assessments: Different markets conduct their assessments at different intervals, meaning that a generator might be deemed essential in its home market at the same time it is contracted as foreign capacity elsewhere. This could lead to conflicts in capacity obligations if scarcity events occur simultaneously.

Impact on cross-border contracting: If countries do not recognise each other's methodologies, there may be reluctance to rely on foreign capacity, reducing the effectiveness of cross-border participation and potentially leading to over-procurement in some markets.

To mitigate these challenges, greater harmonisation of capacity adequacy methodologies and flexibility needs assessment across Nordic markets is needed, ensuring that cross-border contributions are assessed consistently and can be relied upon when needed.

7.7.3 Harmonised rules

One of the key challenges in integrating mechanisms across European electricity markets is the variation in national rules and regulatory frameworks. Differences in eligibility criteria, payment structures, capacity obligations, and penalty mechanisms can create barriers to effective cross-border participation and lead to inefficiencies in capacity procurement.

A harmonised approach to CRM or NFFSS rules across the Nordic region could improve efficiency, security of supply, and investment certainty by addressing the following challenges:

Inconsistent eligibility criteria: Some countries impose stricter requirements on which assets can participate in capacity mechanisms or NFFSS, such as excluding certain technologies or setting specific environmental performance standards. This can limit cross-border participation if foreign assets do not meet the same criteria as domestic ones.

Conflicting capacity obligations: Market participants may face different commitment periods, testing requirements, and performance expectations across jurisdictions. A capacity provider operating in multiple markets may struggle to comply with overlapping or conflicting obligations.

Misaligned procurement and payment structures: Differences in auction design, clearing prices, and contract durations can distort investment signals. For example, a generator might be incentivised to participate in a CRM with higher payments, rather than in the market where its capacity is most needed.

Disparities in penalty and enforcement mechanisms: Some markets impose strict penalties for non-delivery of capacity, while others have more lenient enforcement mechanisms. This could lead to unequal risk allocation, where foreign providers may be subject to weaker penalties than domestic participants.

Uniform trigger price: For strategic reserve 2.0 or dispatchable flexible reserve, distortions occur when trigger prices vary between countries. Using maximum prices in existing markets, which are consistent across all EU markets due to market coupling, eliminates this issue. Alternatively, if the VoLL or other rules determine the trigger price, establishing a common VoLL or trigger price can mitigate distortions.

7.7.4 Harmonised procurement platform

Harmonising the procurement of capacity and/or flexibility across the Nordic countries can help mitigate some of the challenges related to cross-border participation. Although the different markets seek to procure different products, it should be feasible to design a common platform. A harmonised approach offers several advantages:

Cost sharing: Enables the sharing of costs associated with implementing and operating the mechanisms, leading to greater economic efficiency.

Sharing of resources: When scarcity events are unlikely to occur simultaneously across different markets, a single capacity or flexibility provider can ensure security of supply in multiple connected markets. This reduces costs by decreasing the number of required providers within the region and utilising a broader range of plants. Consequently, cost for end consumers decline as markets share the costs for the same volumes.

Streamlined: Ensuring similar functions across the Nordic region reduces administrative and operational burden, both for operators and market participants operating in multiple markets.

Example to illustrate the feasibility of a harmonised solution

A common Nordic mechanism is feasible. Drawing inspiration from the SDAC platform, the Nordic market can be divided into zones, each managed by a centralised single buyer from each country. Zones with verified needs for additional capacity or flexibility would specify their demand quantities, creating a comprehensive demand map across Nordic price zones. In zones where no additional capacity is needed, demand would be set to zero. For example, Norway could opt out of purchasing reserves while still participating in the market and supporting the mechanism. This approach is equitable, allowing Norwegian assets to participate, ensuring increased competition and efficient allocation of resources.

Similar to SDAC, a central entity, such as the Nordic TSOs, would forecast available cross-zonal capacity between zones over the entire contract period (e.g., 15 years). This forecast would establish ‘efficiency factors’ or ‘locational derating factors’, indicating how much MW capacity an asset in one zone can provide to another zone during scarcity events.

For example, an asset in Zone A may supply capacity to Zone B but be derated by X% to reflect its ability to provide electricity cross-border during a scarcity in Zone B. This locational derating factor could work in combination with efficiency factors such as:

- Technology-specific derating factor: Assessing the asset's reliability during scarcity events.

- Ramping speed: The capability to quickly adjust output levels (seconds, minutes or hours).

- Operational limits: Maximum continuous operation time and required resting time.

To ensure the system's reliability, national regulators should commit to maintaining the physical cross-zonal capacity capabilities. This commitment guarantees that capacity providers can fulfil their obligations during scarcity events, preventing undermining the results of the mechanism.

7.8 Second order building blocks

Second-order building blocks apply to all designs, and their decisions are not dependent on which shortlisted design is ultimately chosen. As a result, these decisions can be made separately and typically at a later stage, once the overall direction has been clarified. However, this does not diminish their importance. As outlined in this paper, many existing CRMs in Europe have encountered challenges due to suboptimal design choices at this level. The following sections outline key considerations for each of the five second order building blocks.

7.8.1 Contract type and duration

Generally, longer contracts are positive for investors who typically seek stability and predictability, particularly if the construction of new assets are envisioned. However, as the identified adequacy concerns might not materialise, long contracts lead to a higher risk of over-procurement. Conversely, shorter contracts can be more adaptable to changing market conditions, reducing the risk of over-commitment. Shorter contract will typically also attract “low hanging fruits” like DSR, BESS, lifetime extensions, and refurbishments. However, it is likely to fail in attracting new-build assets with higher initial investment costs.

Furthermore, long-term contracts can potentially distort market signals by locking in certain capacities, thereby affecting the flexibility of the market to adapt to new technologies or changing demand patterns.

It is possible to accommodating different types of capacity providers through varied contract durations. This can help to ensure a balanced mix of resources, enhancing overall system reliability and resilience. It may also lower the risk of both over- and under-procurement as the amount of resources secured via short contracts can be adjusted to reflect changing market conditions. This gives a higher degree of freedom for the TSO.

A shaped contract can allow assets to seasonally shut down, thereby lowering direct procurement costs. This approach is particularly relevant for large thermal units, which can benefit from reduced costs during periods of low need. With shaped contracts, it is also possible to allow the unit to operate freely in the market in periods where the TSO deems the need to be low. This would increase the resource efficiency but also lead to higher market distortion – especially if the unit is competitive in the wholesale market.

Lessons learned

Attracting new investments vs. retaining existing capacity: In the UK's CRM, new generation projects could secure contracts up to 15 years, whereas existing plants were limited to one-year contracts. This disparity led to challenges in balancing the encouragement of new investments with the retention of existing capacity

Newbery, D. (2020). Capacity Remuneration Mechanisms: Comments on Experience and Implementation Challenges. Cambridge: Energy Policy Research Group, University of Cambridge. Available at: https://www.jbs.cam.ac.uk/wp-content/uploads/2024/02/eprg-D.-Newbery_Comment_24Mar2020.pdf

Technology lock-in: Some European countries have implemented CRMs to ensure sufficient levels of flexible and dispatchable capacity. However, these markets have predominantly allocated payments to thermal technologies like gas, coal, and nuclear plants, with gas-fired assets accounting for about half of the capacity payments. This allocation may not align with long-term decarbonisation goals.

7.8.2 Duration of need and market time unit (MTU)

The duration of need is becoming an increasingly critical challenge with the growing reliance on variable RES, leading to periods of dunkelflaute. To address this, the design of support mechanisms must be adapted accordingly. While eligibility criteria should consider the duration of need, overly strict requirements could limit competition and risk failing to deliver an effective solution.

To enhance market efficiency and inclusivity, the mechanism should accommodate a diverse range of market participants by segmenting the duration of need into smaller MTUs during procurement. This approach would not only foster competition but also support welfare distribution, as a wider variety of assets could generate revenues by providing services.

Lowering entry barriers, such as reducing MW thresholds or MTU sizes, has proven effective in several markets, including day-ahead, intraday, and mFRR markets. There is reason to believe that similar adjustments would enhance competition in capacity and flexibility mechanisms and as well, and this aligns with ACER’s report on barriers to demand response and other distributed sources from 2023

ACER (2023) ‘Demand response and other distributed energy resources: what barriers are holding them back? 2023 Market Monitoring Report. Available at: https://www.acer.europa.eu/sites/default/files/documents/Publications/ACER_MMR_2023_Barriers_to_demand_response.pdf

Furthermore, new system technologies, such as the automatic activation of units directly from the TSO’s control centre, enable greater reliance on a fleet of smaller assets to ensure security of supply. This fleet can be procured directly by the TSO or offered as a service by aggregators, further increasing flexibility and resilience in the system.

7.8.3 Procurement mechanism

Auctions trading platforms facilitate transparency, where price discovery is public, and all bids are treated equally given pre-defined criteria (i.e. high visibility to the procurement process, results, needs, commitments, etc.). A pay-as-clear auction provides additional profits for cost-efficient solutions, potentially making their participation more attractive than in a tender. However, launching a new auction platform is time consuming and potentially costly and is therefore less attractive if procurements are rarely taking place and overall procured volume low.

Tenders are easier to launch relative to an auction platform, but selection of successful bidders is more complex, and the bid selection process may be considered less transparent than an auction. Tenders is preferable when there are few potential suppliers and other criteria than price are crucial.

Lessons learned

Complexity in decentralised approaches: France's decentralised capacity market, which relied on over-the-counter trading, resulted in complex transactions, reducing transparency and liquidity.

7.8.4 Lead-time and frequency

When designing capacity and flexibility mechanisms, policymakers must align procurement timelines with the lead-times of different technologies. A short lead-time in effect disqualifies new build generation and attracts “low hanging fruits” like DSR and BESS.

Key considerations include:

- Early procurement: To ensure long-lead-time technologies, providers must receive commitments well in advance to secure investment and timely deployment.

- Short-term flexibility: Fast-responding resources like DSR and BESS, as well as extending lifetime of existing assets, can quickly be procured to manage near-term adequacy risks.

- Regulatory streamlining: Before the procurement process, permitting and grid connection processes must be streamlined to avoid delays and secure project delivery.

- Diversified support structures: Policymakers should consider using differentiated contract structures tailored to the lead-times of the different technologies that can solve the adequacy need.

Another aspect is that frequent (annual) procurements will attract more providers as projects can be re-submitted in later auctions. It also allows for flexibility with regards to new needs assessments and allows for learning from the previous rounds for all stakeholders.

Lessons learned

Insufficient lead-time for new-build: In I-SEM, most of the new-build capacity awarded contracts in 2017 withdrew as they did not manage to bring new capacity into operations within the four-year long lead-time between contract award and delivery. This led to delayed capacity and resulting in contract terminations and penalties, illustrating the importance of realistic lead-times for new investments.

Balancing short and long-term: A critical lesson from GB is the strategic importance of determining how much capacity to procure well in advance (T-4 auctions, for delivery four years ahead) versus closer to the actual delivery year (T-1 auctions). In GB’s first capacity auction, a significant shortfall emerged due to over-reliance on the T-4 auction. This occurred because some contracted new-build projects failed to materialise within the four-year lead-time, resulting in a notable gap in available capacity. Although this shortfall was later mitigated by allowing interconnectors into subsequent auctions, it underscores the inherent tension in procurement timing: earlier auctions provide the necessary lead-time to attract a broader range of investment, while later auctions offer greater precision in determining actual system needs but significantly limit the choice of technologies that can feasibly be deployed within a short timeframe.

Newbery, D. (2020). Capacity Remuneration Mechanisms: Comments on Experience and Implementation Challenges. Cambridge: Energy Policy Research Group, University of Cambridge. Available at: https://www.jbs.cam.ac.uk/wp-content/uploads/2024/02/eprg-D.-Newbery_Comment_24Mar2020.pdf

7.8.5 Nature of penalty

Penalties play a critical role in ensuring that providers deliver services in accordance with their commitments and that consumers receive the quality and reliability for which they have paid.

Providers who operate a diverse portfolio of assets may financially benefit from non-delivery during periods of system stress, as increased market prices can offset penalties through enhanced revenues from their remaining operational assets. It is therefore worth considering whether administered penalties should vary depending on specific provider characteristics, such as portfolio composition.

However, policymakers must carefully balance penalty levels, as excessively high penalties could deter providers from participating in procurement processes. Reduced participation can ultimately lead to higher overall system costs, whereas more moderate penalties may encourage greater participation and thus more competitive procurement outcomes.

Lessons learned

Effectiveness of penalty structures: An important lesson from GB’s CRM is the critical role of penalty design in ensuring contracted capacity delivery. During the early GB auctions, modest penalties allowed providers, such as a large-scale CCGT project contracted at a relatively low clearing price, to relinquish their contracts without substantial financial repercussions. This created significant gaps in procured capacity, highlighting the necessity for penalties sufficiently stringent to deter non-delivery, yet balanced enough to avoid discouraging participation altogether.