↑ Photos: iStock and Johnér

5. Longlist of design alternatives

This chapter provides an overview of existing mechanisms, primarily in Europe, as well as theoretical concepts not implemented. The chapter is meant to give a general overview of the different design variants both for CRMs and NFFSS and develop a longlist of design alternatives. This will serve as the basis for the selection of some designs to be explored and assessed in detail in later chapters – the shortlist – to do a deep-dive analysis.

5.1 Summary

A range of CRMs and flexibility support schemes are already implemented across Europe, with several additional conceptual designs proposed. While no support scheme has yet been implemented under the NFFSS regulation, similar schemes that are likely to fall under its scope in the future have already been approved under state aid rules and are either in operation or under development.

This chapter explore various design alternatives, describing them using the building blocks outlined in Chapter 4. A key takeaway is that all CRMs and flexibility support schemes are different. Each is tailored to the specific needs and circumstances of the country in which it is implemented. The longlist presented here provides the foundation for selecting a subset of designs for more detailed analysis in subsequent chapters—the shortlist—where a deeper evaluation of their relevance and applicability to the Nordic context is undertaken.

5.2 Capacity Remuneration Mechanisms (CRMs)

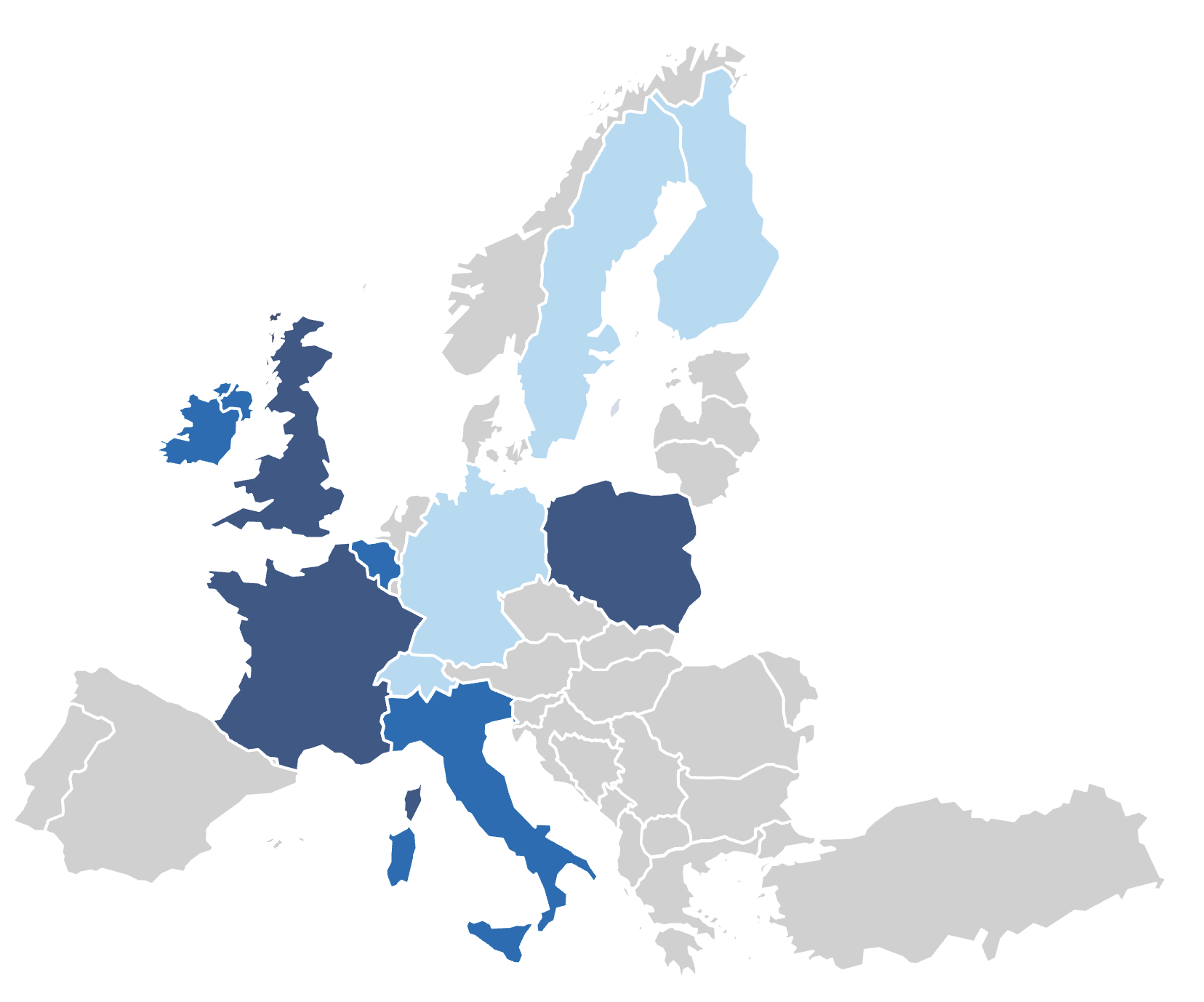

This sub-chapter explores the various CRMs that have been conceptualised and implemented across Europe. It begins with exploring a longlist of CRMs, encompassing both conceptual models and those that have been practically applied in different markets. By examining existing implementations, it provides insights into the effectiveness and challenges of different CRM designs, setting the stage for identifying the most relevant alternatives for the Nordic market. Exhibit 5.1 shows an overview of current CRMs in Europe.

Exhibit 5.1 – A range of different CRMs exists in Europe today

Different countries have chosen different mechanisms to deal with adequacy issues, but most markets operate on an energy-only basis

Different countries have chosen different mechanisms to deal with adequacy issues, but most markets operate on an energy-only basis

FI: Strategic reserve

SE: Strategic reserve

I-SEM: Reliability option, centralised, market-wide

GB: Availability obligation, centralised, market-wide

DE: Strategic reserve

PL: Availability obligation, centralised, market-wide

BE: Reliability option, centralised, market-wide

FR: Availability obligation, decentralised, market-wide

CH: Strategic reserve

IT: Reliability option, centralised, market-wide

Source: AFRY, ACER.

5.2.1 Longlist of CRM design alternatives

The longlist comprises both existing implementations and conceptual designs, each described using the first-order building blocks introduced in Chapter 4.2.

Design alternative | Description Outlining if the mechanism is market-wide or targeted, the eligibility, and how the volume is determined and procured. | Product obligation | Recover scheme |

Targeted tender | Fully centralised procurement, targeted at new assets, with fixed eligibility. | Contracted providers have no availability obligation, and receive an annual payment, throughout the contract period. The units can freely operate in wholesale markets. | The TSO recovers costs through grid tariffs or via other means. Clawback mechanism ensures that potential windfall profits are shared between the provider and the TSO. |

Strategic reserve 2.0 | Fully centralised procurement, targeted at existing capacity with fixed eligibility. | Contracted providers, generation and/or DSR, are ring-fenced from the wholesale market, only being available for dispatch on the instruction of the TSO. | The TSO recovers costs through grid tariffs or via other means. |

Targeted capacity payment | Fully centralised procurement, targeted at new or existing capacity, with fixed eligibility. | Contracted providers have no availability obligation and receive an annual payment. The units can freely operate in wholesale markets. | The TSO recovers costs through grid tariffs or via other means. |

Market-wide capacity payment | Fully centralised market-wide procurement of existing capacity, with fixed eligibility. | Contracted providers have no availability obligation, and receive an annual payment. The units can freely operate in wholesale markets. | The TSO recovers costs through grid tariffs or via other means. |

Centralised availability obligation | Fully centralised market-wide procurement of new or existing capacity, with dynamic eligibility. | Providers have an availability obligation and commit to making the awarded capacity available when called upon. The capacity can otherwise be operated freely in the market. | The TSO recovers costs through grid tariffs or via other means. |

Decentralised availability obligation | Fully decentralised market-wide procurement of new or existing capacity, with dynamic eligibility. | Providers have an availability obligation and commit to making the awarded capacity available when called upon. The capacity can otherwise be operated freely in the market. | The retailers and PIUs pay for the availability of capacity to improve security of supply and to lower wholesale prices. Costs are recovered through the prices retailers charge end-users. |

Centralised reliability option | Fully centralised procurement, targeted at new capacity with dynamic eligibility. | Providers have issued physically backed energy reliability options, rights (options) to buy electricity at a predetermined strike price, and must pay a ‘difference’ charge if the market price exceeds a predefined strike price. | The TSO recovers costs through grid tariffs or via other means. “Clawback” in form of the providers returning any positive difference between wholesale and strike price to the TSO, who is the buyer of the option. |

Decentralised reliability option | Fully decentralised market-wide procurement of new or existing capacity, with dynamic eligibility. | Providers have issued physically backed energy reliability options, rights (options) to buy electricity at a predetermined strike price, and must pay a ‘difference’ charge if the market price exceeds a predefined strike price. | The retailers and PIUs pay for the option as an insurance against high wholesale prices, and the providers return any positive difference between wholesale and strike price. Remaining costs are recovered through the prices retailers charge end-users. |

5.2.2 Existing implementations in Europe

This chapter present insights into implementations across various countries, highlighting key lessons learned. While this is not an exhaustive overview of all implementations of the longlisted designs, it offers a curated selection of markets where valuable lessons can be drawn, particularly in relation to the assessment of second-order building blocks discussed in Chapter 7.8.

I-SEM, Ireland: Centralised reliability option

All interconnectors, dispatchable and non-dispatchable-but-controllable generator units are required to participate

Participation by generators below the de minimis threshold, variable units above the minimum threshold (10MW), units that have not come online and units that plan to close before the end of the capacity year is voluntary.

The maximum volume the participants can offer is limited by two factors. First, their net derated capacity, which adjusts their total capacity based on the reliability of their technology and size. Second, their firm offer requirement, which is a specific limit set for them. They must offer the lower of these two values.

If a participant wins capacity in the auction, their commitment is based on the derated capacity they were awarded. This means their obligation is tied to an adjusted availability level rather than their full installed capacity, reflecting how reliable their technology is expected to be.

They have difference payment obligation when the market reference price exceeds the strike price. The participants have to pay the positive differences between the imbalance price and the strike price for the portion of contracted capacity which has not been sold in the markets, regardless of whether they generate or not in the balancing market. They are therefore incentivised to run at times of scarcity and avoid incurring difference payments without any offsetting market revenue. This is creating a financial risk to contracted generators, when unsold generation is settled against the imbalance price.

In I-SEM, successful providers struggled to bring new capacity into operation within the four-year lead-time. This effectively resulted in a large withdrawal from capacity providers, which then needed to pay a termination fee, resulting in the CRM not being able to address the adequacy concerns.

Belgium: Centralised reliability optionEuropean Commission (2021), State aid SA.56848 (2020/N) – Belgium – Capacity mechanism, C(2021) 6518 final, 27 August 2021. Available at: ec.europa.eu; Elia (n.d.), Capacity Remuneration Mechanism, available at: elia.be

European Commission (2021), State aid SA.56848 (2020/N) – Belgium – Capacity mechanism, C(2021) 6518 final, 27 August 2021. Available at: ec.europa.eu; Elia (n.d.), Capacity Remuneration Mechanism, available at: elia.be

The Belgium CRM is a market-wide CRM, open to all capacities that can contribute to resource adequacy, both existing and new capacity, storage and DSR – and for cross-border participation. Derating factors are calculated for each technology reflecting its reliability and its contribution to solve the security of supply concern. Capacity providers can therefore only get capacity contracts up to their derated capacity. The amount of capacity that can participate from neighbouring countries is calculated on a border-by-border basis. The strike price of the option is based on the SDAC.

The European energy crisis led to a massive shift in Belgium’s energy policy. From being determined to phase out nuclear power, which to a large extent was the motivation for implementing a CRM, Belgium decided to extend the lifetime of its nuclear units. This massively reduced the need for the capacity already procured via the CRM.

Belgium has also seen a large share of the payments going to providers in neighbouring countries, as state aid rules require cross-border participation. There are several both positive and negative aspects of this:

- Derating factors are applied based on how much capacity is believed to be available when activation is needed. The Belgium TSO has also taken steps to ensure that the market algorithm, Euphemia, better reflects the CRM obligations.

- It may be politically challenging to implement a CRM that transfer money from the Belgian electricity consumers to electricity generators in other countries. On the other hand, from a cost perspective, if the required capacity was only procured in Belgium, the capacity payments would likely be significantly higher as foreign providers were successful in the procurement process.

Finland: Strategic reserveEuropean Commission (2022), State aid SA.55604 (2020/N) – Finland – Strategic reserve, C(2022) 7399 final, 11 October 2022. Available at: https://competition-cases.ec.europa.eu/cases/SA.55604

European Commission (2022), State aid SA.55604 (2020/N) – Finland – Strategic reserve, C(2022) 7399 final, 11 October 2022. Available at: https://competition-cases.ec.europa.eu/cases/SA.55604

The Finnish strategic reserve is designed to ensure the security of electricity supply during peak demand periods in the winter months. This mechanism involves maintaining a reserve of electricity generation, DSR, and/or storage units outside the wholesale electricity market (i.e. ring-fenced).

The units need to be ready to respond within 12 hours from when they receive a dispatch order from the TSO and must be able to respond up to at least 200 hours, but are not open for cross-border participation as it is deemed “technically unfeasible”. The strategic reserve is only to be used when all balancing reserves are likely to be exhausted. The imbalances in the market are at this point settled at minimum VoLL or at a higher value than the SIDC price limit.

The reserve operates by keeping certain electricity generation and storage units on standby, ready to supply electricity when needed. Additionally, DSR are prepared to reduce electricity consumption during critical times. These units do not participate in the regular electricity market, which helps to minimise any potential market distortions. The selection of units for the reserve is conducted through a transparent and competitive bidding process, ensuring that the most efficient and environmentally friendly alternatives are chosen.

Sweden: Strategic reserveSvenska kraftnät (n.d.), Effektreserv, available at: svk.se

Svenska kraftnät (n.d.), Effektreserv, available at: svk.se

Sweden is currently reviewing the future of its CRM

Svenska kraftnät (2023), A Future Capacity Mechanism to Ensure Resource Adequacy in the Electricity Market, Case No. Svk 2022/3774, 31 March 2023. Available at: svk.se

In the late 2010s, the strategic reserve opened for DSR participation, which was expected to increase procurement in the short term and enhance demand flexibility in the long term

Regeringen (2010), Proposition 2009/10:113 – Effektreserven i framtiden, submitted 18 February 2010. Available at: riksdagen.se

Swedish Government (2010), Förordning (2010:2004) om effektreserv, issued 22 December 2010, repealed 1 July 2016. Available at: riksdagen.se

Holmberg, Pär & Tangerås, Thomas (2022), En teknikneutral elmarknad – med en effektiv elmarknadsdesign och nättariffstruktur, Institutet för Näringslivsforskning (IFN), 28 March 2022. Available at: https://www.ifn.se/media/tvfnip3s/holmbergtanger%C3%A5s220328.pdf

Svenska kraftnät (2023), A Future Capacity Mechanism to Ensure Resource Adequacy in the Electricity Market, Case No. Svk 2022/3774, 31 March 2023. Available at: svk.se

Poland: Centralised availability obligationEuropean Commission (2018), State aid SA.46100 (2017/N) – Poland – Planned Polish capacity mechanism, C(2018) 601 final, 7 February 2018. Available at: https://ec.europa.eu/competition/state_aid/cases/272253/272253_1977790_162_2.pdf

European Commission (2018), State aid SA.46100 (2017/N) – Poland – Planned Polish capacity mechanism, C(2018) 601 final, 7 February 2018. Available at: https://ec.europa.eu/competition/state_aid/cases/272253/272253_1977790_162_2.pdf

The Polish CRM is a market-wide CRM, open to all capacities that can contribute to resource adequacy, both existing and new capacity, storage and DSR – and for cross-border participation. The capacity providers are obliged to deliver energy in the contracted period to ensure security of supply.

Poland has been facing some challenges with their CRM. In the initial years of implementation, capacity payments were predominantly awarded to coal-fired plants, rather than to gas-fired units as originally intended by the scheme’s designers. Questions have also been raised regarding whether the volume of capacity procured is sufficient to meet identified system needs. Similar to the case in Belgium, a portion of the capacity payments is allocated to foreign capacity, which, as previously discussed, may be viewed negatively.

Great Britain: Centralised availability obligation

The GB was introduced a capacity mechanism in 2014 as part of the Electricity Market Reform (EMR) to ensure security of supply by providing predictable revenue streams for capacity providers. The mechanism operates through competitive auctions where participants bid for capacity agreements, committing to be available during system stress events. Successful bidders receive capacity payments in exchange for this availability, with penalties applied if they fail to deliver when required.

The mechanism is a market-wide, centralised capacity mechanism open to a broad range of technologies, including thermal generation, storage, DSR, and interconnectors. Auctions are typically held four years (T-4) and one year (T-1) ahead of the delivery period to secure long-term investments while allowing adjustments closer to real-time needs. The mechanism has been subject to ongoing reforms to improve cost efficiency and alignment with decarbonisation objectives, including changes to how carbon-intensive assets participate and the integration of low-carbon flexibility resources.

The GB availability obligation scheme attracted a large fleet of small diesel and gas engines and turbines, as units below 50MW would not require a longer and more complect permitting and connection process. This was unintended as the CRM aimed at promoting new CCGT plants. The CRM also excluded DSR, but after being challenged by market participants, DSR needed to be allowed to participate in the mechanism. This shows that a CRM inevitably creates winners and losers, and that it can be challenging to promote the “right” capacity.

France: Decentralised availability obligation

Suppliers have an obligation to ensure they have a certain volume of capacity certificates to cover for their consumers’ demand during selected peak days. This happens via OTC trading with a central registry.

Capacity providers can trade based on certified availability and all technologies are eligible to participate. Capacity certification rules include specific rules for renewables to account for their intermittent generation profile. Contracted capacity participates as normal in the wholesale market.

New capacity is contracted by the TSO for a seven-year period under a CfD through a competitive tendering process. This capacity is in the next round offered by the TSO to the in the OTC market where suppliers procure their required volume.

The decentralised setup has been criticised for being too complex, while the overall CRM is considered to be too expensive. These issues may be linked, as it may be challenging in a fragmented market to spur the needed market liquidity and competition to move towards the “missing money” threshold – especially if the market is already dominated by a few large players. Also, a complex scheme may make it challenging for market participants to reduce peak demand and maximise available resources at times of system stress.

5.2.7 Conceptual designs

Not all longlisted designs have been implemented across Europe, the most relevant being the decentralised reliability option.

Decentralised reliability option (DRO)AFRY Management Consulting (2015), Decentralised Reliability Options – Securing Energy Markets, Full Report v3.00, March 2015. Available at: https://afry.com/sites/default/files/2020-07/decentralisedreliabilityoptionsfullreport_v300.pdf; AFRY Management Consulting (2015), Decentralised Reliability Options – Securing Energy Markets, Summary Report v1.00, March 2015. Available at: https://afry.com/sites/default/files/2020-07/dro_mar2015_v100.pdf

AFRY Management Consulting (2015), Decentralised Reliability Options – Securing Energy Markets, Full Report v3.00, March 2015. Available at: https://afry.com/sites/default/files/2020-07/decentralisedreliabilityoptionsfullreport_v300.pdf; AFRY Management Consulting (2015), Decentralised Reliability Options – Securing Energy Markets, Summary Report v1.00, March 2015. Available at: https://afry.com/sites/default/files/2020-07/dro_mar2015_v100.pdf

Unlike centralised CRMs, DRO operate on a decentralised basis. Retailers and large consumers are required to buy reliability options to meet their demand at critical times. Providers are committing their availability and receive an upfront payment (the price the buyer pays for the option) and forgo the revenue from price spikes. If the market price exceeds a predefined strike price, the capacity provider compensates the buyer for the difference.

The decentralised nature of the mechanism allows for market participants to themselves defined strike prices and other criteria for the option contract.

5.3 Non-fossil flexibility support schemes (NFFSS)

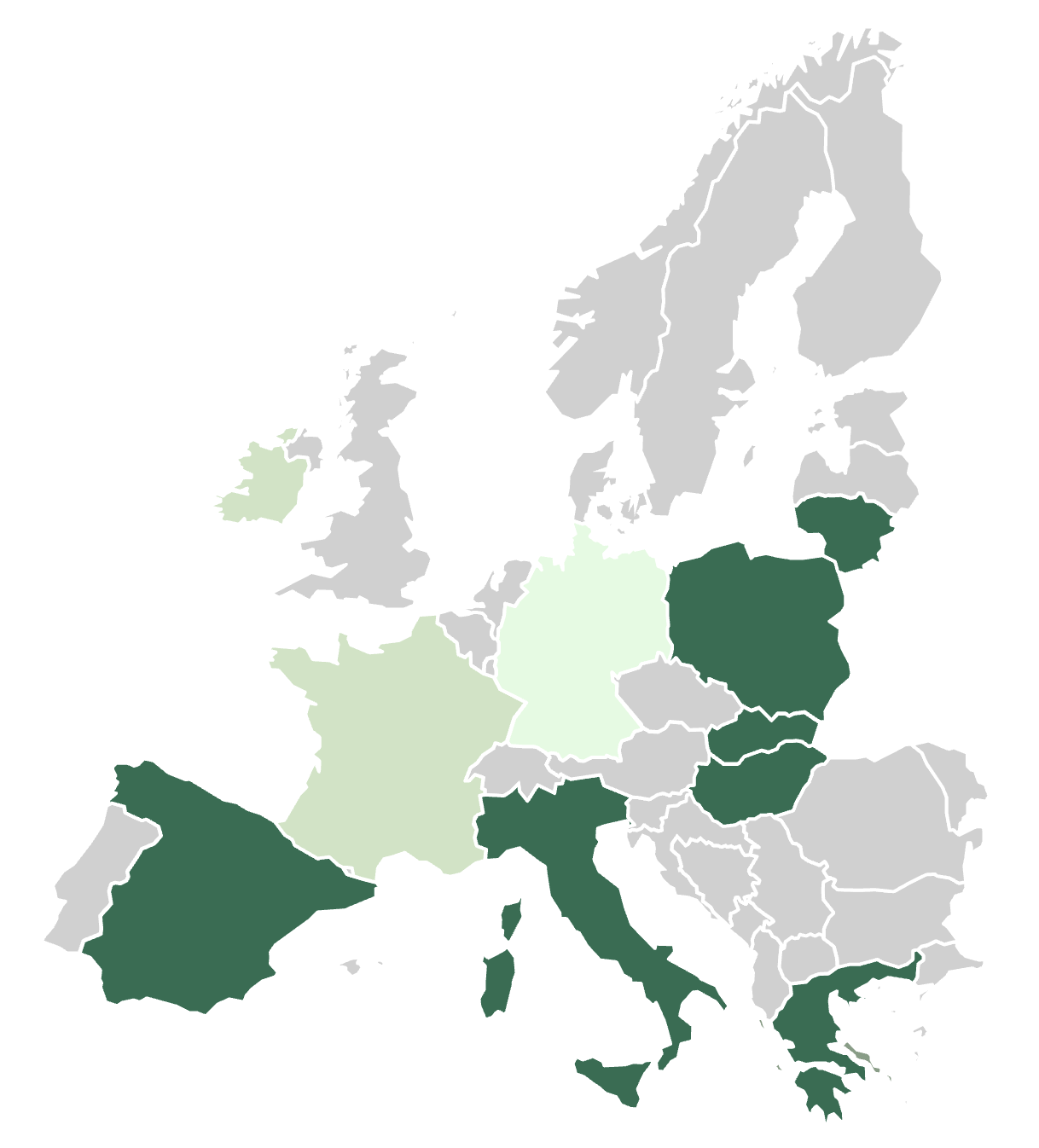

In addition to CRMs, several European countries have introduced other mechanisms aimed at increasing the flexibility of the power system, as shown in Exhibit 5.2. These schemes are primarily focused on enabling resources such as BESS, DSR, and other flexible capacity to better integrate renewable energy, improve grid reliability, and provide essential services like frequency regulation and peak load management.

It is important to note that these support schemes are not implemented under the new NFFSS regulation, as this regulation is still in the early stages and not yet in place across the EU, but they can provide potential examples of mechanisms that could be integrated under the NFFSS once it becomes operational.

Exhibit 5.2 – Different support schemes for flexible technologies are approved under the state aid regulation

The current support scheme typically supports DSR and BESS.

The current support scheme typically supports DSR and BESS.

LT: BESS

IR: DSR

PL: BESS

DE: Thermals, BESS

FR: DSR

SK: BESS

HU: BESS

IT: BESS

ES: BESS

GR: BESS

IR: DSR

PL: BESS

DE: Thermals, BESS

FR: DSR

SK: BESS

HU: BESS

IT: BESS

ES: BESS

GR: BESS

Source: AFRY, ACER.

5.3.1 Longlist of NFFSS design alternatives

The longlist of design alternatives includes mechanisms that resemble established capacity remuneration mechanisms (CRMs), existing support schemes approved under state aid regulations, and newly proposed concepts. While many of these may be considered conceptual in nature, this chapter does not provide further detail on the CRM-type designs beyond the summary provided in the accompanying table.

Each design is described using the first-order building blocks introduced in Chapter 4.2.

Design alternative | Description Outlining if the mechanism is market-wide or targeted, the eligibility, and how the volume is determined and procured. | Product obligation | Recover scheme |

Targeted flexibility tender | Fully centralised procurement, targeted at new assets, with fixed eligibility. | Contracted providers have no availability obligation, and receive an annual payment, throughout the contract period. The units can freely operate in wholesale markets. | The TSO recovers costs through grid tariffs or via other means. Clawback mechanism ensures that potential windfall profits are shared between the provider and the TSO. |

Dispatchable flexible reserve | Fully centralised procurement, targeted at new assets, with dynamic eligibility. | Contracted providers are ring-fenced from the wholesale market, only being available for dispatch on the instruction of the TSO. | The TSO recovers costs through grid tariffs or via other means. Clawback mechanism ensures that potential windfall profits are shared between the provider and the TSO. |

Centralised availability obligation – NFFSS | Fully centralised procurement, targeted at new capacity with dynamic eligibility. | Providers have an availability obligation and commit to making the awarded capacity available when called upon. The capacity can otherwise be operated freely in the market. | The TSO recovers costs through grid tariffs or via other means. |

Centralised reliability option – NFFSS | Fully centralised procurement, targeted at new capacity with dynamic eligibility. | Providers have issued physically-backed energy reliability options, rights (options) to buy electricity at a predetermined strike price, and must pay a ‘difference’ charge if the market price exceeds a predefined strike price. | The TSO recovers costs through grid tariffs or via other means. “Clawback” in form of the providers returning any positive difference between wholesale and strike price to the TSO, who is the buyer of the option. |

Decentralised reliability option – NFFSS | Fully decentralised procurement, targeted at new capacity with dynamic eligibility. | Providers have issued physically-backed energy reliability options, rights (options) to buy electricity at a predetermined strike price, and must pay a ‘difference’ charge if the market price exceeds a predefined strike price. | The retailers and PIUs pays for the option as an insurance against high wholesale prices, and the providers return any positive difference between wholesale and strike price. Remaining costs are recovered through the prices retailers charge end-users. |

MACSE | Fully centralised procurement, targeted at new BESS, with fixed eligibility. | Providers have an service-specific availability obligation and commit to making the awarded capacity available to the TSO who offer it as time-shifting products to the market. The capacity can otherwise be operated freely in the market. | The TSO recovers costs through grid tariffs or via other means. |

FRR availability obligation | Fully centralised procurement, targeted at new assets, with fixed eligibility. | Providers have an availability obligation and commit to making the awarded capacity available in the FRR EAM when called upon. The capacity can otherwise be operated freely in the market. | The TSO recovers costs through grid tariffs or via other means. |

5.3.2 Existing implementations in Europe – ‘state aid’

A range of support mechanisms are implemented across various European countries. Most of these state aid-approved support schemes fall under the ‘targeted flexibility tender’ category, the simplest form of support scheme, in which flexible technologies receive subsidies without any direct obligations or commitments beyond their construction.

France: Demand response call for tenderRTE (2024), Demand Response Call for Tenders, published 12 January 2024. Available at: rte-france.com

RTE (2024), Demand Response Call for Tenders, published 12 January 2024. Available at: rte-france.com

In addition to the CRM, the demand response call for tenders is designed to promote demand-side flexibility by incentivising electricity consumers to reduce consumption when needed. The scheme is open to consumption sites that can lower their electricity usage.

The tenders are structured into four categories based on the size of the consumption site and if the demand response is explicit or supply linked. Explicit demand response involves direct reductions in consumption when requested, whereas supply-linked demand response allows reductions to be integrated into broader electricity procurement strategies.

Ireland: DSO demand flexibility product procurementCommission for Regulation of Utilities (2024), DSO Demand Flexibility Product Procurement Decision Paper, CRU202469, published 12 July 2024. Available at: https://cruie-live-96ca64acab2247eca8a850a7e54b-5b34f62.divio-media.com/documents/CRU202469_DSO_Demand_Flexibility_Product_Procurement_Decision_Paper.pdf

Commission for Regulation of Utilities (2024), DSO Demand Flexibility Product Procurement Decision Paper, CRU202469, published 12 July 2024. Available at: https://cruie-live-96ca64acab2247eca8a850a7e54b-5b34f62.divio-media.com/documents/CRU202469_DSO_Demand_Flexibility_Product_Procurement_Decision_Paper.pdf

The mechanism is designed to enhance the flexibility of the electricity distribution network by promoting (primarily) DSR. It is part of a strategy that aims for 15-20% flexible system demand by 2025 and 20-30% by 2030.

The scheme seeks to procure up to 500 MW of flexibility products to manage congestion within the DSO grid. Participation is open to a range of technologies capable of delivering the required technical and operational performance. This includes solutions that reduce or shift demand to off-peak periods, as well as those that can inject power at or near their full contracted capacity for a minimum of four hours per day over most business days, typically for a duration of 3-6 months per year.

The procurement process follows a competitive assessment based on a 'most economically advantageous' approach. Key evaluation criteria include value for money, operability, deliverability, and the ability to support multi-market participation. By introducing this framework, the regulator aims to facilitate more efficient use of the electricity network, reduce the need for costly grid reinforcements, and support Ireland’s broader decarbonisation goals.

Spain, Slovakia, Hungary: Investment support for BESSEuropean Commission (2023), State aid SA.106554 (2023/N) – Slovakia – Investment support for electricity storage, C(2023) 7563 final, 3 November 2023. Available at: https://ec.europa.eu/competition/state_aid/cases1/202403/SA_106554_F0E8168D-0000-CF9B-989F-10E7ABBD77C3_80_1.pdf;

European Commission (2023), State aid SA.102428 (2022/N) – Hungary – Aid for energy storage facilities for the integration of weather-variable renewable energy sources, C(2023) 4257 final, 21 June 2023. Available at: https://ec.europa.eu/competition/state_aid/cases1/202330/SA_102428_F09B8D89-0100-C81D-9E22-4DB74E82A2DE_73_1.pdf;

European Commission (2023), State aid SA.103068 – Spain – Support for innovative electricity storage projects, C(2023) 4721 final, 7 July 2023. Available at: https://ec.europa.eu/competition/state_aid/cases1/202402/SA_103068_C06FED8C-0100-CB2A-A2A3-D0CD056F25DD_156_1.pdf

European Commission (2023), State aid SA.106554 (2023/N) – Slovakia – Investment support for electricity storage, C(2023) 7563 final, 3 November 2023. Available at: https://ec.europa.eu/competition/state_aid/cases1/202403/SA_106554_F0E8168D-0000-CF9B-989F-10E7ABBD77C3_80_1.pdf;

European Commission (2023), State aid SA.102428 (2022/N) – Hungary – Aid for energy storage facilities for the integration of weather-variable renewable energy sources, C(2023) 4257 final, 21 June 2023. Available at: https://ec.europa.eu/competition/state_aid/cases1/202330/SA_102428_F09B8D89-0100-C81D-9E22-4DB74E82A2DE_73_1.pdf;

European Commission (2023), State aid SA.103068 – Spain – Support for innovative electricity storage projects, C(2023) 4721 final, 7 July 2023. Available at: https://ec.europa.eu/competition/state_aid/cases1/202402/SA_103068_C06FED8C-0100-CB2A-A2A3-D0CD056F25DD_156_1.pdf

European Commission (2023), State aid SA.102428 (2022/N) – Hungary – Aid for energy storage facilities for the integration of weather-variable renewable energy sources, C(2023) 4257 final, 21 June 2023. Available at: https://ec.europa.eu/competition/state_aid/cases1/202330/SA_102428_F09B8D89-0100-C81D-9E22-4DB74E82A2DE_73_1.pdf;

European Commission (2023), State aid SA.103068 – Spain – Support for innovative electricity storage projects, C(2023) 4721 final, 7 July 2023. Available at: https://ec.europa.eu/competition/state_aid/cases1/202402/SA_103068_C06FED8C-0100-CB2A-A2A3-D0CD056F25DD_156_1.pdf

Several EU member states have implemented state aid schemes supporting BESS (and hydro pump storage where available) under the Temporary Crisis and Transition Framework for State Aid, which allows for targeted aid to address the energy crisis. These schemes generally focus on providing investment support for energy storage solutions to enhance grid stability and flexibility. While each scheme is tailored to the specific needs of the country, they share the common goal of supporting the integration of renewable energy sources, improving energy security, and enabling a more resilient energy infrastructure.

In Slovakia, the state aid scheme is designed to support the construction and operation of energy storage systems, primarily for renewable energy integration and grid balancing. Similarly, Hungary has introduced a state aid measure that focuses on promoting the deployment of energy storage solutions, with an emphasis on enhancing the capacity for peak load shaving and frequency regulation.

In Spain, the scheme follows a similar model, targeting the expansion of energy storage capacities to support grid flexibility and renewable energy integration. The Spanish scheme not only focuses on investment support for BESS but also incorporates mechanisms to ensure that these systems can participates in balancing services.

Germany: Investment support for gas power plantBundesministerium für Wirtschaft und Klimaschutz (BMWK) (2024), Kraftwerkssicherheitsgesetz – Wasserstofffähige Gaskraftwerke, available at: bmwk.de

Bundesministerium für Wirtschaft und Klimaschutz (BMWK) (2024), Kraftwerkssicherheitsgesetz – Wasserstofffähige Gaskraftwerke, available at: bmwk.de

Similar to the schemes described above, Germany is planning to introduce a support for in total 12.5GW of new generation capacity (a mix of natural gas, hydrogen-ready and hydrogen-only power plants) as well as 500MW long-term energy storage under the new Power Plant Safety Act. The successful bidders must complete construction within 6 years and have no obligation to participate in any specific market (apart from the general REMIT requirements).

Primarily new, but also partly refurbished units, may participate. They are required to deliver 96 hours of continuous supply, and 2/3 are to be located in southern Germany. The latter is to be achieved by adding a component to the bid price to account for system cost savings. There are also some other technical requirements for the units, among them the possibility to deliver “grid-forming” – basically operate as a rotating mass to provide inertia.

The successful bidder will receive annual pay-outs over 15 years. The units will also be exposed to a clawback mechanism, where 70% of the income beyond a daily set trigger price. Using the concept of reliability options, there will also be a production-independent clawback to ensure availability when the system is under stress.

Italy: MACSE

MACSE is an electricity storage capacity procurement mechanism for new capacity. Successful providers are required to make the storage capacity, once built and operational, available to the TSO, which will offer the pooled storage capacity to third parties, in the form of standardised time-shifting products on a new centralised trading platform. The time-shifting products will give their buyers the possibility to use a virtual storage asset as if was theirs, to store and sell electricity at a later time when they wish to do so.

A single tender process will be organised at national level and at lower geographical level (i.e. bidding zone). This is done to ensure that Italy has sufficient storage capacity both on national level as well as in the bidding zones the reflect the regional resource situation.

Capacity providers enter into 15-year contracts with the TSO. These contracts offer a fixed annual premium, ensuring a stable revenue stream for the duration of the agreement. While the primary compensation is fixed, providers may have opportunities to earn additional revenue. For instance, they can participate in the balancing markets and retain a portion of the profits, potentially up to 20%.

5.3.4 Conceptual designs

The concepts outlined in this sub-chapter are designed to complement NFFSS design alternatives based on longlist of CRM designs.

FRR availability obligation

A potential type of flexibility support mechanism is to support technologies aimed at the balancing reserves. This approach may be implemented when a country identifies a structural need for additional balancing reserves but determines that the market alone is unable to deliver the required capacity. In such cases, a specific support mechanism can be introduced to incentivise the development of new flexible capacity, ensuring that sufficient balancing resources exists in the market to be able to maintain system stability.

Under this model, capacity providers would receive long-term contracts to develop and operate new flexible assets, such as BESS, DSR, or flexible generation. In return for this support, these assets would be required to participate in the balancing market, for example by being required to bid in the aFRR/mFRR CM or in the EAM. By supporting balancing capacity through long-term commitments, this mechanism provides investment certainty for developers while ensuring the power system has access to critical flexibility resources.

Dispatchable flexible reserves

The Dispatchable Flexible Reserve represents an alternative to the Strategic Reserve 2.0 design outlined in the CRM longlist but is implemented under the NFFSS regulation. As such, it is specifically targeted at new, non-fossil technologies and DSR, rather than extending the operation of existing capacity nearing phase-out. Dispatchable Flexible Reserves operate in a manner similar to strategic reserves by providing dedicated and restricted capacity, but with enhanced flexibility. The awarded capacity is excluded from competitive market participation and is activated exclusively during periods of critically high prices, preferably within the Single Intraday Coupling (SIDC), or alternatively within the Single Day-Ahead Coupling (SDAC). The solution does not require intervention by the TSO, as activation is triggered automatically by a predetermined market price threshold. Further detailed descriptions of this design can be found in the shortlist section (Chapter 6) of this report.