9. Recommendations and conclusions

9.1 Leveraging Existing Infrastructure and Framework

9.1.1 Existing infrastructure and building blocks:

To address the challenges identified in the AS-IS scenario, it is recommended to leverage existing digital setups, infrastructures, and building blocks, such as the CEF eDelivery infrastructure, for cross-border electronic document (eDocument) exchange (e.g. of eInvoices, eCatalogues, eOrders, eReceipts and Dispatch advice). Additionally, the TO-BE scenario envisions that platforms are supplied with the necessary access points to enable companies to send and receive eDocuments through centralized infrastructures. This approach enables efficient, secure, and reliable sharing of product and climate data for reporting and future data needs.

9.1.2 Organized by public institutions:

In relation to this, it is recommended to leverage (extend) on solututions and platforms managed and hosted by public institutions, but in collaboration with private organizations. The rationale includes:

- The digital setup will be available to all stakeholders in the market, including SME’s who most likely would face barriers in private-led setups, hence public authorities support inclusivity.

- Public authorities support all types of companies by providing a neutral framework that considers businesses, regardless of size, thereby enhancing trust and reducing biases or conflicts of interest.

The Danish Bookkeeping Act

The Danish Bookkeeping Act is a regulation launched to regulate fundamental responsibilities for companies’ storage and bookkeeping of accounting material. The material stored and recorded often forms the basis for other mandatory duties for companies, such a preparation of the annual financial report etc. (Danish Business Authorities, Bogføringsloven, 2024)

In contrast, Sweden currently lacks a central eInvoicing solution or platform for (c.f. figure 8). The current digital setup is organized by private service providers who offer services accommodating both the private and public sectors. This is considered an inhibitor to scaled adoption, and therefore it is recommended that Swedish authorities aim to take greater ownership of the processes.

In relation to the reasons listed above, it is recommended to identify the appropriate public authority in each country and define their roles and responsibilities concerning the organization of the relevant digital setup.

9.1.3 Standardization and Interoperability

It is also recommended to leverage established, open, and free standards like the Peppol Framework and data exchange and interoperability frameworks such as CEF eDelivery to help organizations comply with the regulatory requirements introduced by CSRD. Peppol offers a standardized approach to sharing specific datapoints, thereby reducing the need for data conversion and reformatting upon receiving the data and enabling greater automation of current sharing practices. However, standards other than the Peppol Framework should also be considered, to accommodate the current needs and solutions of a broader range of stakeholders.

Utilizing existing setups and frameworks, reduces the costs and complexity of integration and implementation efforts and ensures interoperability and long-term resilliance. In addition, standards can help further accelerate the adoption and implementation in an inexpensive manner.

9.2 eDocuments, Standards and Classification

9.2.1 eDocuments and datapoints

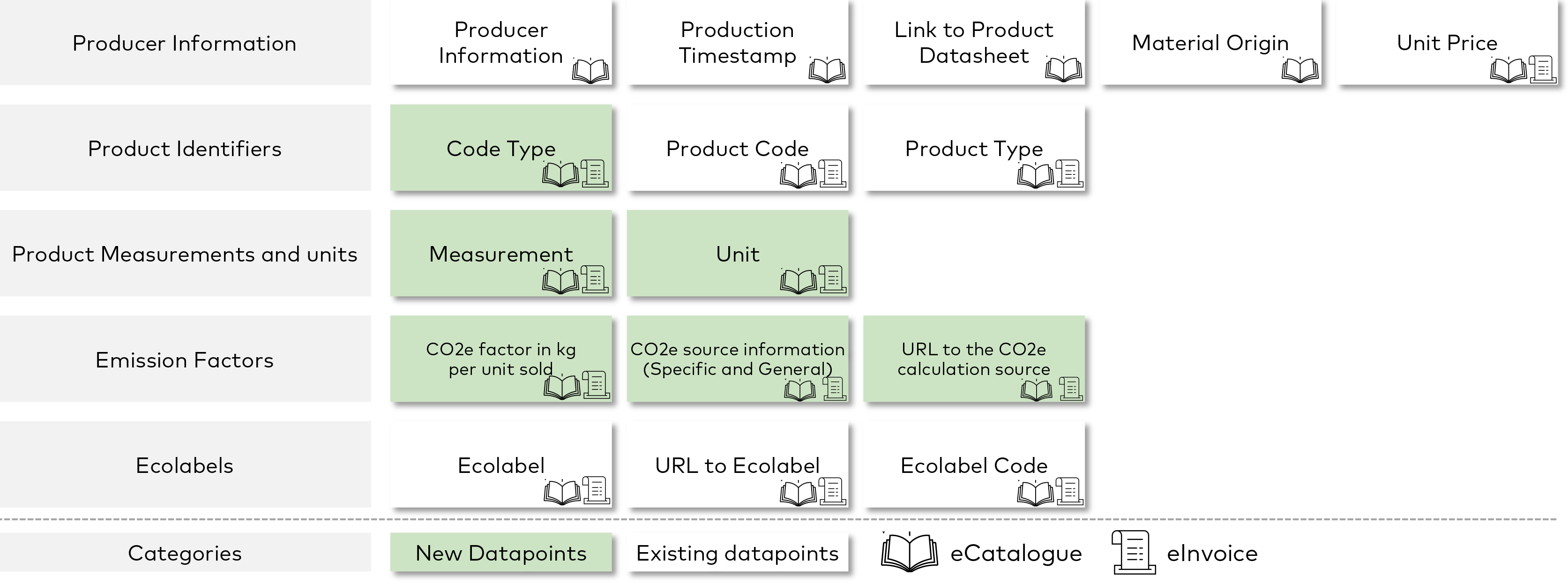

Since eDocuments are the recommended carriers of climate data, adding new fields will help to accomodate and support climate data needs and reduce the administrative burdens of data sharing. In figure 13, the recommended fields to support the reporting needs are outlined. These consist of both existing and new datapoints. The grey boxes indicate datapoint groups, while the blue highlights new datapoints not currently present in eDocuments or the Peppol Framework.

Figure 13 illustrates that the eCatalogue can accommodate more datapoints, including detailed producer information. In contrast, the eInvoice should remain simple, containing only essential datapoints. Figure 13’s eCatalogue and eInvoice symbols denote the recommended eDocument type(s) for implementation.

9.2.2 Catalogue as a repository

Businesses should ideally store relevant datapoints in eCatalogues to enable automatic availability in other eDocuments, such as eInvoices. This allows the eCatalogue to serve as a central repository for all datapoints. The eCatalogue should store the most detailed datapoints, while the eInvoice should remain simple (cf. the section “eDocuments and Green data (Mockups)). However, it is essential that all eDocuments, not just eCatalogues, include some or all significant and material datapoints, such as the "CO2e factor per unit sold”. Using open and free standards (see section 9.1.3), organizations and even countries can tailor datapoints and values to their needs in each relevant eDocument. This will permit a seamless flow of product and climate data throughout supply chains, supporting the objective of the project.

9.2.3 Classification systems:

To enhance data consistency and usability, adopting the UNSPSC code standard is recommended. Its stable structure supports accurate classification of products across multiple sectors. The UNSPSC code standard allows for easy and seamless addition of new products. Furthermore, it provides a hierarchical classification structure that enhances search functionality and enables data to be structured, categorized, and stored for easy access and retrieval in all systems.

The Nordic countries should consider aligning on the same UNSPSC version. Currently, there are 26 versions, with the latest being UNv26.0801. Denmark has implemented and translated version 19, Norway uses version 18, and Sweden, Finland, and Iceland rely on older versions. To streamline efforts, it is recommended that the Nordic countries collaborate to adopt, translate, and implement the latest version (or at least the same version). Leveraging Artificial Intelligence (AI) might help minimize translation costs and reduce the time required. This alignment would streamline and improve both climate reporting and general reporting across the Nordic countries.

9.2.4 Linking of UoM to a Product Code list:

To improve product and climate data exchange in eDocuments and simplify processes for suppliers, linking the ”Unit of Measurement” datapoint to a product code list like UNSPSC is recommended. This enables the automation of the “Measurement of Units” field for each product. This means that, each time a product has been defined with an UNSPSC code, the field for “Units of Measurement” will automatically be populated.

Since "Unit of Measurement" is stable, it simplifies identifying a product's emission factor, to find average emission factors, which can be used with GHG Protocol's average data method.

Since "Unit of Measurement" is stable, it simplifies identifying a product's emission factor, to find average emission factors, which can be used with GHG Protocol's average data method.

In this regard, it is recommended to draw inspiration from Norway’s successful project of linking UoM to a product code list. This approach can result in significant cost and time savings.

9.2.5 Additional Item Properties (AdditionalItemProperty)

Since approving new datapoints in communities like the Peppol community takes about a year and it is on a cross-country level acceptance, using the “AdditionalItemProperty” group is recommended as a temporary solution. This simplifes implementation while maintaining compatibility with existing standards. Denmark has already integrated the Additional Item Property in both the eInvoice and eCatalogue. It aligns with the ISO/IEC 19845 standards, which defines the “Universal Business Language” (UBL), which the EU-Norm also is based on, making it possible to facilitate this under the EU-norm. This ensures immediate usability. Furthermore, it should be considered to use the Additional Item Property group for data fields such as the Unit of Measurement, which is typically a fixed value. In Norway, only the fixed value "Kilogram" is used. Additionally, by utilizing the Additional Item Property group for the "Unit of Measurement" data field, it would allow for more flexibility, enabling additional measurement values to be included.

In this context, it is recommended that the other Nordic countries follow Denmark's example by adopting the same structure and approach for implementing the Additional Item Property group. This simplifies emission data sharing for suppliers. It is recommended for the EU commission to implement this approach as well in the EU-norm as soon as possible.

9.3 Reliability and Process Management

9.3.1 Creating guidelines for Updating Datapoints:

It is recommended to guide service providers in how to update datapoints in companies’ IT core systems (e.g. ERP-systems), as they need to ensure reliability, availability and security of each datapoint. In addition, this will also help to ensure that the correct datapoints are used for the right purpose.

9.3.2 Creating guidelines for Identifying Dependency Risks:

When updating datapoints, it is further recommended for the service providers to identify if there are any potential risks of dependencies on specific datapoints or systems that could lead to inconsistencies or overwriting of critical information, to ensure data integrity. This is important when considering fields which are automatically populated

An example of a dependency risk: If a supplier changes the “Unit of Measure” for a specific product from kilograms to pieces, this can cause errors between the supplier's and the customer's systems. If the customer's system is configured to interpret the product's UoM as kilograms in an invoice based on previous transactions but then receives an invoice with the UoM updated to pieces, the system may reject the invoice because it cannot map "pieces" to the expected format.

The recommendations of guiding service providers in how to update and evaluate datapoints will support the trustworthiness of exchanging and utilizing product and climate data for the recipients and generally throughout the supply chain.

9.4 Calculation Methods and Guidelines

9.4.1 Support of Accurate Calculations:

It is recommended to provide businesses with guidelines on how and when to use similar but distinct datapoints. For instance, if a supplier has both the following datapoints:

- “CO2e factor in kg per unit sold”

- “CO2e factor in kg per base unit”.

Guidelines should help the supplier and users prevent errors and ensure accurate “net emissions” calculations in the systems and eDocuments. This should also include necessary guidance on converting datapoints.

9.4.2 Calculation Methods:

Moreover, it is recommended not to include the “calculation methods” datapoint, as no common standard or method exists yet. At the time of this report, there exists several hundred approaches to calculate emission factors or conduct Lifecycle Assessments (LCA). However, it is recommended to further explore the potential value in including the most commonly used methods for LCAs and calculating emission factors, namely Attributional Life Cycle Assssment (ALCA) and Consequencuel Life Cycle Assessment (CLCA). For example, the Product Environmental Footprint (PEF) and Organization Environmental Footprint (OEF) methods could be relevant to consider, as they provide common guidelines for modeling and calculating LCAs and emission factors. It is recommended to establish an on-going system to monitor and assess the maturity and potential of calculation methods deemed appropriate, and when relevant, conduct trials to see if a specific initiative can provide long-term value.

9.4.3 Alignment with standards:

Any guidelines developed to assist businesses in calculating, estimating or collecting datapoints should align with the recommended accounting standards of ESRS and CSRD, such as the GHG protocol. This ensures accuracy, reliability and industry relevance.

9.5 Enabling the recommendations to ease the Administrative Burdens

The 13 recommendations outlined aim to streamline administrative processes for businesses by leveraging international standards and integrating new datapoints into existing documents, datasets, systems, and process flows. Achieving this requires sustained collaboration across the Nordic countries.

What: There is a need for a standardized and digital data exchanged across the Nordic and EU level. This will simplify ESG data collection and sharing, reducing redundancies, and improving efficiencies. Harmonizing processes across borders will also enhance the value of this initiative and create synergies with other digitalization programs.

A strong cross-border Nordic collaboration is recommended to explore how digitalisation and automation can improve sustainability documentation and reporting. The Initial focus should be on climate-related reporting, with the expectation to expand into broader ESG topics.

Initial key areas of focus include:

- Ensuring that any data and digital initiatives are supported by clear guidance for users to understand technical changes (incl. the cross-disciplinary standards) and their impact.

- Supporting the implementation of an international, open, and free standard to enable standardized, secure, and efficient exchange of data relevant to climate reporting.

- Introducing new ESG-related data fields within existing eDocuments in alignment with the GHG Protocol and CSRD requirements.

- Alligning new datafields with recognized open and free standards, such as Peppol, to facilitate interoperability and accellerate the adoption across countries and industries.

- Building upon relevant Nordic, EU, and global initiatives, such as NSG&B, the European strategy for data, Product Environmental Footprint (PEF), and the Digital Product Passport (DPP).

- Strengthening collaboration with standardization bodies and service providers to ensure consitent implementation.

Why: The increasing regulatory requirements for sustainability reporting, have prompted various governmental initiatives to simplify compliance. However, these efforts often operate in isolation, leading to inconsistencies that can increase the reporting burdens on businesses rather than reduce it. Without coordination, companies must navigate multiple reporting frameworks and repeatedly adjust their systems, creating inefficiencies and unnecessary costs.

Coordinated alignment across the Nordic region is essential to prevent redundant efforts and ensure a streamlined approach. Even if all Nordic countries agree on relevant datapoints and electronic documents, differences in adoption timeline and methodologies can create inconsistencies. A harmonized approach will mitigate these risks, ensuring regulatory compliance while reducing administrative complexity.

Who: The Nordic collaboration should contain multiple workstreams with individual, but internally aligned, working groups. The working groups should include representatives from public authorities, businesses across industries, service providers, and NGOs. Generally, there is a need for a cross-functional collaboration which involves:

- Public authorities specializing in areas such as sustainability regulation, digitalization, business policy etc.

- Businesses across industries, representing both upstream and downstream activities, to ensure a comprehensive understanding of value chain requirements - the movement of materials, products, services, etc., in relation to the end customer – to get an overview of existing processes, digital landscape and practices.

- Standardization bodies and key industry initiatives to ensure alignment with best practices and international frameworks.

How: The cross-Nordic collaboration should, as stated, draw on existing groups of specialists and ideally, to the extent possible, be anchored within the existing domains where digitalization and climate responsibilities reside. For this reason, a suggested first step would be to map the relevant stakeholders within the countries, and involve them in the creation of a committed plan to deliver on (or to adjust and deliver on) the above recommendations.

Potential impact: By implementing these recommendations through a coordinated Nordic collaboration, businesses, particularly SME’s, will benefit from reduced reporting burdens, improved data quality, and enhanced transparency. A unified approach will also ensure that companies are better prepared for future ESG regulations, minimizing compliance disruptions and administrative overhead. In addition, this will establish a foundation for digital standardization, fostering a more efficient and interconnected sustainability reporting landscape across the Nordic region.

Potential impact: By implementing these recommendations through a coordinated Nordic collaboration, businesses, particularly SME’s, will benefit from reduced reporting burdens, improved data quality, and enhanced transparency. A unified approach will also ensure that companies are better prepared for future ESG regulations, minimizing compliance disruptions and administrative overhead. In addition, this will establish a foundation for digital standardization, fostering a more efficient and interconnected sustainability reporting landscape across the Nordic region.