Cross-national policy recommendations

Photo: Pexels

According to basic economic theory, politicians and authorities should abstain from direct interventions in well-functioning markets. For a market to be well-functioning, though, a set of basic conditions must be met. Some of these conditions apply to flexibility markets and market-based utilisation of demand-side flexibility in particular:

- Markets may be missing, or market access may be limited

- Product definitions may not be sufficiently standardised

- Technologies/solutions may be immature

- Information may not be adequately available

In addition to such market failures, there may be regulatory failures, i.e., other regulations that effectively constitute barriers. An example of the latter is the economic regulation of DSOs that incentivise grid investments even if the use of flexibility is the more economical solution.

Another important basic economic principle is that, once a market or regulatory failure (barrier) has been properly identified and described, targeted policy measures should be specifically designed to address the nature of that market failure. Should several market failures be identified, each should be targeted individually, and measures should be implemented that ensure that the goal is reached in a cost-effective way. Administrative costs and transaction costs associated with the measure should be considered, and the measure should only be implemented if the benefits are larger than the costs.

In this chapter, we first summarise and assess the barriers identified in the case studies as a basis for the policy recommendation (4.1). The development of flexibility solutions, both in terms of smart appliances’ flexibility potentials, communication protocols, and market and product design, is still ongoing. In Section 4.2, we lay out how this may affect the regulatory approach. Finally, in section 4.3, before we present our recommendations to the Nordic regulators in section 4.4, we provide an overview of existing EU regulation and ongoing policy developments with ramifications for the development of efficient flexibility markets in the Nordic markets.

Assessment and summary of identified barriers

Various barriers can hinder the provision and use of economically profitable demand-side flexibility sources in helping solve grid challenges. The result would be grid customers paying too much for their grid connections and for their use of the grid. It is crucial to remember that the aim is not necessarily to realise the full flexibility potential of all the different flexibility sources, but to exploit the economically profitable flexibility. This implies identifying and removing barriers related to market and regulatory failures along the value chain that hinder the economically efficient provision and/or procurement of DSF services.

The main barriers are summarised in this section. In the majority of the case studies, the actors report that it is difficult to make demand-side flexibility from smart appliances profitable. Aggregators need to make various investments and other efforts to be able to aggregate and offer a portfolio of loads to the marketplace. The payment from the markets is usually not very high. Thus, a main challenge is the lack of profitability due to a combination of barriers that make costs too high and compensation too low.

Barriers related to smart appliances and barriers related to market design are intertwined and should be considered collectively. We see that identified issues can be solved by improving the flexibility abilities of smart appliances or by changing the requirements to participate in the market.

Table 12 gives an overview of the most important barriers we have identified from each of the case studies. We have selected the barriers that are reported from several case studies. The barriers are described in more detail below the table.

Table 28: Overview of main barriers and where they were identified*

1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | |

Low market liquidity | ||||||||||

Low level of economic compensation | ||||||||||

Value stacking | ||||||||||

Differences between local DSF markets | ||||||||||

Rebound effects | ||||||||||

Lack of standardized communication protocols | ||||||||||

Non-smart appliances | ||||||||||

Consumption measurement and verification of activation | ||||||||||

Baseline issues | ||||||||||

Incentives in economic regulation | ||||||||||

Reliability and stability in framework conditions | ||||||||||

Information and knowledge |

*Numbers in columns refer to: 1. Byggflex, 2. Battflex, 3. Norflex, 4. Sthlmflex, 5. Effekthandel väst, 6. E.ON’s flexibility markets, 7. FUSE, 8. EcoGrid, 9. Helen, 10. Elenia.

Low market liquidity in local flexibility markets

Market liquidity was a reported barrier in Sthlmflex, Effekthandel väst, and in the first of E.ON’s flexibility markets. Low market liquidity is a problem for the DSO procuring flexibility, as it can lead to high prices and even the absence of bids. This can result in a vicious circle, where the DSO lowers its demand even more because they do not trust that the market can deliver flexibility at the right time and in sufficient volumes. DSOs will then use other measures to fix their grid issues. However, low demand from the DSO can also occur from grid issues being smaller than expected. This happened in Sthlmflex, where mild winters and high power prices led to the forecasted grid issues being smaller than expected.

In some use-cases, e.g., Helen Electricity Network’s and Fingrid’s marketplace, a bid can only include resources from one BRP, limiting the opportunities to combine different loads. In this way, the market design (bid requirements) can prevent sufficient market liquidity. However, setting requirements like this might also be necessary if the flexibility is needed to solve grid issues in a specific area, e.g., solving a local bottleneck.

Achieving sufficient market liquidity can also be difficult when actors in practice have to choose between participating in the TSO reserve markets or the DSO local flexibility markets (more about this in the section on Value stacking below).

No or too low economic compensation for flexible loads

In several of the case studies, the economic compensation for flexibility was considered too low and/or uncertain. In some of the technical demos, no economic compensation was offered for the loads involved (e.g., Byggflex). In other cases, the offered compensation was seen as too small to incentivise participation (e.g., FUSE and EcoGrid). It was also stated that it is difficult for actors who are considering joining the market because they do not have insight into the market dynamics and potential earnings, making it difficult for them to develop business models.

Limited opportunities for value stacking

Profitability of flexibility provision, making flexibility provision more attractive, would be easier to achieve if providers could participate in both the TSO reserve market and the DSO local DSF markets with the same load. This is generally not possible today due to:

- There is no setup ready to coordinate between the markets. Finland is an exception, as participation in the new local DSF market and reserve markets of the TSO with the same flexible resource is possible. However, even in Finland, the same capacity of a resource cannot be bid to the congestion management market and to the reserve markets (mFRR, aFRR, FCR-N, FCR-D, or FFR) for the same hour. Resources can, e.g., participate in the hourly FCR market at 2-5 PM and the local DSF market at 7-9 PM. In Euroflex, which is the follow-up project of Norflex, a possible solution for this lack of coordination is being developed and tested. The suggested solution is a flexibility register, where all prequalified FSPs and flexibility resources are registered.

- The minimum bid size in reserve markets (FFR) is too large for FSPs of small household appliances. FSPs can participate through a larger aggregator/BRP, but this would require agreements with each owner of the specific loads and the BRP. Requirements on how fast a bid should be activated are also a barrier for smaller loads from smart appliances.

- The trading deadlines between the different markets are not aligned. This is important if bids from the local markets shall be forwarded to a TSO reserve market, or vice versa.

Added value can also be achieved by delivering implicit flexibility, i.e., varying power consumption depending on the spot price. Generally, there is more money to be saved by adjusting your electricity consumption to the spot price rather than participating in flexibility markets. In theory, you can do both, but there are issues related to timing. Spot prices are announced the day ahead, which may result in actors not wanting to make bids in local DSF markets before they know the spot prices of the specific day.

Different requirements and designs of local DSF markets

Aggregators/FSPs that want to participate in different local DSF markets (with different loads) face different rules and market platforms for each market. This constitutes an entry barrier as they must go through integration of communication protocols for each market, while with a common, standard approach, they could have realised economies of scale. This is identified as a barrier in the case study of Effekthandel väst. Another example of such different rules is verification requirements related to the accuracy in electricity consumption measurement, identified in the Helen & Fingrid case study. The Norflex case study identified different financial support schemes in different countries as a barrier, making it more difficult for flexibility service providers to scale their business model.

Rebound effects causing voltage issues

Rebound effects are seen in mechanisms using only price optimisation, where fast upregulation after downregulation can result in voltage issues (this can also occur after implicit load shifting based on spot prices), which must be handled by the DSO. This implies a cost for the DSO. DSOs can give economic incentives to prevent such rebound effects through the grid tariff structure. Capacity-based grid tariffs promote a flatter power consumption curve and may encourage slower upregulation after downregulation. A barrier to enable consumption following both activation/price signals and the grid tariff today is the variation in capacity-based tariff structures among DSOs. Without an easily automatised way to import data on the different tariffs, it will be hard to keep the optimisation algorithms up to date.

Another possible risk is that other appliances are being turned on when the appliance offering flexibility is activated, e.g., floor heating vs heat pump heating. This makes it necessary to activate a larger volume because consumer adjustment counteracts the activation.

Lack of standardised communication protocols

Communication protocols and API solutions are not yet standardised across appliances. This means that FSPs have to integrate each appliance individually into their platforms. How difficult and time-consuming this is depends on the level of complexity in the API, but this setup cost represents an entry barrier. However, many FSPs see their integration solution as part of their business proposition. As an analogy, this can be seen as their “patent”, or reward for being innovative. We grant actors patents for their innovations to ensure they have incentives to develop such solutions. According to interviewees, standardisation at this point risks limiting innovation as the markets, integration solutions, and business models are still immature. Following the same analogy, patents are only given for a certain amount of time. Having these entry barriers is not the desired end-situation but may be a necessary step to incentivise the development of innovative solutions necessary to realise the future where flexibility can be cheaply offered from smart appliances with easy “plug-n-play” features.

This is not to say that there are no issues today regarding the lack of harmonisation of manufacturers’ API interfaces for load control and minimum requirements for control and monitoring capabilities. As stated above, developing solutions enabling demand-side flexibility can be time-consuming for the FSPs. Building managers with lacking knowledge and/or competence may also find it hard to operate and optimise intricate and/or multiple control system installations and interfaces. Heterogeneity of communication systems in different loads is also a barrier if loads have to be aggregated, e.g., to fulfil minimum bid sizes in the reserve markets.

In FUSE, challenges were identified related to ensuring real-time interoperability between chargers, aggregators, and grid operators due to a lack of standardised communication protocols. Variations in data formatting across different platforms made integration more complex, suggesting a need for standardisation. If interoperability between chargers (EV users), aggregators, and grid operators is not ensured, then the message might not be interpreted correctly (e.g., kWh could be read as Wh).

Some appliances, e.g., electric radiators, are connected to the FSP service with a variety of connectivities and protocols (Bluetooth, USB-C, Wifi). This is seen as a barrier because it makes it more complicated for the FSP to connect radiators to their service.

Non-smart appliances

Older appliances have a limited ability to integrate and communicate with top control systems due to proprietary protocols and/or missing load control units. Requirements for individual measurement per unit lead to a high participation cost per unit for loads without measurement hardware. In Norway, there are no requirements to install load controls on appliances in new buildings. The Helen and Fingrid case study found that internet connectivity is often an additional module for cheaper heat pumps, even if they are brand new. Installing communication modules later is possible, but likely to be significantly more expensive.

Lacking harmonisation of electricity consumption measurement and verification accuracy

The accuracy of electricity consumption measurement varies, and this is a barrier to verification. There is no harmonised method to measure consumption nor harmonised requirements for minimum accuracy.

Sub-metering at the specific appliance provides more accurate verification than aggregated household consumption data (via the smart meter), but the costs for high-resolution metering are higher. Sub-metering can be more beneficial for loads like space heating, consisting of several heating sources, as it is then more complicated to estimate how electricity consumption behaves.

As explained above, the smart meter (AMS) reaction time is too slow for loads to participate in TSO markets (this is even true in Finland, with a 5-minute resolution of AMS). Many meters can be programmed to send data with a higher resolution, but the amount of data could then lead to limitations in reaction time due to the capacity of the mobile network.

Lack of information about resources and their current electricity consumption makes it hard to know which resources are actually available for activation (consumption increase or decrease). In the Elenia case study, it was stated that only the customer knows if a load is connected to the relay suitable for the DSF service, causing uncertainty for the FSPs in estimating the DSF potential of their resources. In the Helen Electricity Network’s case study, the FSP had difficulties obtaining customer information (electricity supply point, electricity supplier, BRP). Such information could be obtained from a data hub through customers’ authorisation. FSPs neither have real-time information about the ESWHs’ temperature nor their electricity consumption, which they need to estimate DR capacity and verify fulfilled flexibility. The same problems were present for air-to-air heat pumps, as they lack a two-way communication interface. The Modbus communication module, enabling two-way communication, can cost up to 300 EUR for one heat pump. Communication protocols in air-to-air heat pumps are manufacturer-specific, and harmonisation of these would help. The same problem applies to electric radiators.

Baselining issues

Five of the case studies reported baseline issues as a barrier. One example is Norflex, where there were significant deviations between estimated and actual consumption. The deviations were primarily due to two issues: i) consumption data was collected from the main metering device, rather than from dedicated submeters, and ii) the behaviour of the tested loads was hard to predict. However, several of the other case studies have tested possible solutions to the issue of unpredictable behaviour. In the Ecogrid case, machine learning based forecasting was used to predict power consumption more accurately based on parameters like historical consumption data, weather conditions, and time-of-day factors.

Counteracting incentives in the economic regulation of DSOs

In Norway, the economic regulation of the DSOs favours solutions involving (grid) investments relative to operational expenses. Similar issues are reported from Sweden, where interviewees hold that the economic regulation of DSOs makes investments in physical grids more economically appealing than investing in flexibility measures. This perception prevails, although the Swedish Electricity Act states that flexibility measures should be reflected in determining DSOs’ revenue cap. Another issue in Sweden is that the DSOs subscribe to a specific grid capacity from the TSO. If they need to temporarily exceed this capacity, they can apply for a temporary increase in the subscribed capacity. The price of this temporary subscription is generally lower than the cost of using local DSF to stay within their normal capacity limit. Generally, the regulation should incentivise DSOs to choose the cheapest way to solve grid issues, taking into account the total socio-economic costs.

Uncertainty about future market conditions and reliability

Actors need to know that they invest according to a market design that is going to last, and that the procurer (TSO/DSO) will use the market actively to solve grid issues, in order to trust that their investment will be profitable. The demand response network code says that member states are to assign the responsibility of setting up and organising local DSF markets, but this is not expected to be implemented until 2027 at the earliest. The pending decision may delay the establishment of local flexibility markets, which in turn can delay the development of solutions by FSPs and the procurement and use of smart appliances by customers.

A local DSF market with low liquidity might not be adequate for the DSOs, as they need to be certain that a sufficient power and energy volume will be available to solve their grid issues. It is therefore important to put enough emphasis on building the market in the beginning, to avoid low liquidity being an issue for a long time. Information to owners of suitable loads is an important part of this.

In some cases, the DSO does not yet trust local DSF markets to solve their grid issues and therefore uses bilateral contracts. EU directives state that market solutions should be chosen before, e.g., conditional contracts, but this is not always implemented in national legislation.

Lacking information and knowledge

Owners of loads, e.g., the supermarkets in Effekthandel väst, are often unaware of their own ability to participate in local DSF markets. Lack of technical competence might also be a barrier, e.g., owners of smart appliances who need help to connect their devices to the internet. Both the lack of information that they can profit from their smart appliances and how to do it are seen as barriers to achieving sufficient liquidity in local DSF markets.

Level of maturity affects the choice of policy measures

The choice of policy measures or market intervention should be adjusted according to the technological and commercial maturity of the technology/solution at hand.

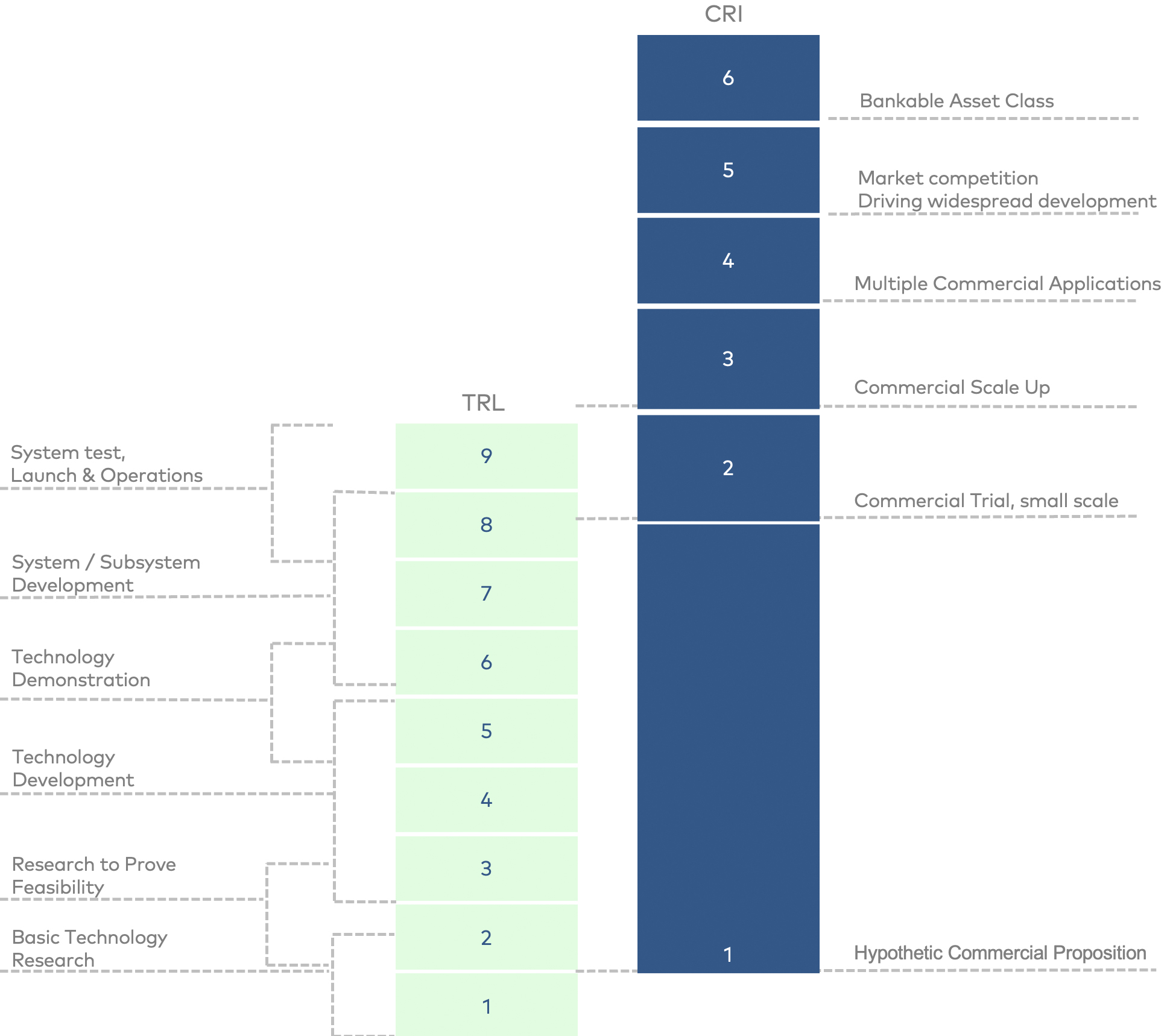

Policy measures should be based on the level of maturity, technologically and commercially. Technology development is measured by the Technology Readiness Level (TRL), while market change is measured by the Commercial Readiness Index (CRI). The connection between the TRL and CRI is shown in the figure below.

Figure 3: Technology Readiness Level and Commercial Readiness Index

Source: Commonwealth of Australia/ARENA (2014): Commercial Readiness Index for Renewable Energy Sectors

The illustration is developed by ARENA (2014): https://arena.gov.au/assets/2014/02/Commercial-Readiness-Index.pdf

A range of indicators should be analysed when assessing the step on the commercial readiness index. These indicators include regulatory environment, stakeholder acceptance, technical performance, financial proposition (costs and revenue), industry supply chain and skills, market opportunities, and company maturity. In step 3, public support is given to technology development, while in step 4, the goal of the public support is to increase demand.

Our maturity assessment is based on information on flexibility use described in chapter two, and the 10 use-cases. We see some variation in maturity across the different countries. Even though the technology level should not differ between countries, different framework conditions can lead to different stages in commercial readiness. For instance, there are only permanent DSF solutions in Sweden. Even though we view the permanent solutions in Sweden as more mature, they have not reached CRI level 6.

We assess the commercial readiness of local DSF markets to be between stages 3 and 4. Although we see some permanent markets, most initiatives are still either technology demonstrations or pilots.

Existing relevant policy and industry standards

The extent to which end-user appliances can provide flexibility and the costs related to such supply are affected by technological developments, product design, and a host of EU regulations, initiatives, and industry standards. The incentives to provide such flexibility, on the other hand, depend on the demand for flexibility services and the value of flexibility that can be realised in the market. Hence, the regulation of grid companies and network codes affects the TSO and DSOs’ incentives to use demand-side flexibility, and the requirements in the revised renewables directive (RED III) and even the electricity market directive may facilitate or work as barriers for the exploitation of DSF. To provide recommendations for the improvement of policies to promote DSF, it is important to understand and assess relevant framework conditions that already are or are expected to be implemented. In this section, we describe and discuss relevant elements of Ecodesign and Energy Labelling regulations, the Code of Conduct, the Network code on Demand Response, the Revised Renewables Directive (RED III), and the Electricity Market Directive.

Ecodesign for Sustainable Products Regulation and Energy Labelling

The Ecodesign for Sustainable Products Regulation (ESPR) entered into force in 2024

Replacing the Ecodesign Directive 2009/125.

“The ESPR aims to significantly improve the sustainability of products placed on the EU market by improving their circularity, energy performance, recyclability and durability» (https://commission.europa.eu/energy-climate-change-environment/standards-tools-and-labels/products-labelling-rules-and-requirements/ecodesign-sustainable-products-regulation_en).

While the ESPR sets minimum energy efficiency and sustainability standards, the Energy Label informs consumers about products’ energy performance and other environmental characteristics. The standards and requirements are set individually for each product. Requirements include information about the appliance’s energy use, its energy efficiency relative to a product-specific energy efficiency index (EEI), in addition to other information relevant to its energy use and environmental footprint throughout the product’s life cycle. The appliances’ ability for smart operation is not included in the sustainability criteria. While the ESPR sets the minimum requirements, the Energy Labelling requirements range the allowed product characteristics.

Increasing the energy efficiency of an electrical appliance that may provide DSF is likely to affect the flexibility potential of the appliance. If the appliance needs less energy or capacity, it can also deliver less down- or upregulation (peak shaving). Better insulation that reduces losses may, however, make the appliance more flexible in terms of load shifting. In some cases, EE regulations may also reduce the appliance's ability to provide demand flexibility. For example, the Ecodesign regulation for water heaters sets maximum storage volumes for electrical storage water heaters (ESWHs) and limits to heat loss in storage, implying a stronger preference for directly gas-heated water heaters. In some countries, such as Finland, France, and Norway, however, where electricity generation is mainly based on hydro and nuclear power, households have traditionally installed relatively large ESWHs, rather than heating directly by natural gas. In these countries, ESWHs represent an important DSF potential that may be reduced by Ecodesign regulation. From an energy system perspective, the flexibility value of ESWHs should be included in the impact assessment of stricter energy efficiency requirements, limiting the storage volumes of ESWHs.

Code of Conduct

The Code of Conduct (CoC) for smart appliances was launched in April 2024 (EC, 2024). The CoC initiative develops an industry standard on “energy management related operability of Energy Smart Appliances”. Work on the development of the CoC was initiated and is led by the EU (DG Energy and the Joint Research Center, JRC) based on a preparatory study, see text box 2. The CoC defines common standards for the smartness of energy appliances, with an aim to increase the number of interoperable energy smart appliances (ESAs). This means that appliances capable of flexible operation are to be designed with functionality capable of reacting automatically to machine-to-machine communication, enabling them to respond to external signals subject to user permission. The CoC includes electrical appliances that are subject to Energy Label requirements (see the previous section).

Moreover, the CoC specifies a number of use cases in terms of abilities and flexibility characteristics that the appliances should be able to provide:

- Flexible start

- Monitoring of power consumption

- Limitation of power consumption

- Incentive-table-based power consumption management

- Manual operation (providing users with the necessary information in case of user-driven manual operation)

The list of use cases is expected to be developed further. The second phase of the CoC was kicked off by a workshop in September 2024. Two of the agenda items were a discussion of the expansion of the CoC to cover energy management systems, photovoltaic inverters, and electric vehicle chargers, and to update the first version of the CoC to include new solutions and protocols.

Use-cases may be mandatory or optional, and this differs between different categories of ESAs (EU, 2022). For heat pumps, for example, monitoring of power consumption is mandatory, while for heating, cooling, and ventilation appliances, monitoring of power consumption and limitation of power consumption are mandatory. The monitoring of power consumption use-case implies that information from the ESA is applied in an overall energy management concept.

Importantly, the CoC defines a common language for technical specifications (features, functions, devices, etc.) of ESAs, the Smart Application Reference ontology (SAREF). This is a necessary step towards a future in which appliances can be made plug-and-play, reducing the need for additional APIs to integrate appliances in smart management systems and enabling communication across relevant protocols.

The CoC also sets Active Power Limits for the maximum active (real) power consumption of an ESA. As with the Ecodesign requirements, this may limit the flexibility potential of the load, but is justifiable if the value of the energy saving is higher than the value of the (lost) flexibility potential.

According to press releases from some of the industry parties in the CoC, manufacturers who have signed the code are to prepare the performance of their products accordingly within a year, i.e., by April 2025. Thereafter, the CoC is to be reviewed once a year. Currently, 11 manufacturers have signed the CoC, including Miele, Mitsubishi, Panasonic, and Electrolux (EC, 2024).

According to the initiative’s web page

Prior to reaching the ultimate goal of the CoC, which is “regulation ensuring interoperability across the board”, “technological readiness for manufacturing energy-smart appliances”, and “natural market convergence towards interoperable products” must be promoted and achieved. While the first stage points to the development of mature technologies, the second stage points to the commercial readiness of the solutions (cf. Section 4.3).

Network Code on Demand Response

The Network Code on Demand Response (NC DR) includes provisions related to the grid companies’ use of and facilitation of DSF, in particular the facilitation of DSF supply from smaller customers, “... including load, energy storage and distributed generation, individually or aggregated, …” through market-based procurement of flexibility services by DSOs and TSOs. The revised draft has been subject to public consultation, and ACER submitted its proposal to the Commission in March 2025.

The regulation focuses on

According to ACERs presentation of the draft NC DR on October 1st, 2024: ACER webinar: draft network code on demand response | www.acer.europa.eu

- effective participation of small system users in all markets, by setting clearer requirements for the implementation of aggregation models and establishing a European registry for baselining methodologies,

- easier access to balancing and local markets, by rules for product verification and by simpler and shorter prequalification, and by establishing a flexibility information system,

- a transparent process to ensure the establishment of local markets, by making market-based procurement the default and requiring justification of deviations, and setting clearer requirements for the interaction between markets, and

- ensuring overall efficient operation, through TSO-DSO and DSO-DSO coordination.

Provisions relevant for the use of DSF include, inter alia:

- Baselining. The national system operators are to define, calculate, and validate terms and conditions for baselining methods according to a process commonly proposed by all TSOs, according to minimum requirements. ENTSO-E and EU DSO are to publish and update annually a baselining method register.

- Aggregation models. According to the Electricity regulation, all market participants are responsible for their own imbalances, either directly, as BRPs, or by contractually delegating their responsibility to another BRP. The regulation sets clear rules for the correct allocation of balance responsibility.

- Lower minimum bid sizes and bid granularity of balancing products. To facilitate the participation of smaller resources in balancing services, including by means of aggregation, the minimum bid size, defined in the TCMs of the NC DR, is set at 1 MW for standard energy and capacity products for balancing, frequency restoration, and replacement reserves (as defined by other EU regulations, including Regulation (EU) 2017/2195).

- Product prequalification. To lower entry barriers, while ensuing system security and safe grid operation, the regulation establishes EU-wide methodologies for the technical requirements for service providing units (SPUs) or service providing groups (SPGs) providing balancing or local services. The specific product attributes shall be defined in a table of equivalence, determining, among other things, availability window, preparation period, ramping period, validity period, mode of activation, and location. A proposal shall be developed by each member state.

- Obligations of market-based procurement of local services. All service procurements should be made in a process where either the selection or activation of the service provider is based on a bidding process.

- Criteria for application of flexible connection. Any activation of flexible connection agreements shall not lead to market distortions, for example, through agreements that limit the system users’ (with such an agreement) provision of balancing and local services in the relevant markets.

- Ownership of energy storage facilities by system operators. As all energy storage services shall be market-based and competitive, the NC DR sets out under which criteria system operators may own, develop, or operate such a facility.

- Requirements for Distribution Network Development Plans (DNDP). In pursuit of art. 32(3) of Directive (EU) 2019/944, DSOs shall publish transparent DNDPs at least every two years. The NC DR sets out the content and requirements of the plans. The plans should, inter alia, include an overview of local services and local energy strategies.

- TSO-DSO and DSO-DSO coordination. Member states shall develop a proposal for national terms and conditions for TSO-DSO and DSO-DSO coordination. These shall ensure that, e.g., actions to solve balancing, congestion, or voltage issues are coordinated.

- Reporting and monitoring. At least every two years, ENTSO-E and the EU DSO entity are to publish a report on demand response.

According to the draft, the grid companies will be obliged to regularly consider whether system services can be procured more efficiently through market mechanisms, and to implement such mechanisms if they are deemed more efficient.

The Commission will review the ACER proposal and initiate a process to get the Demand Response (DR) Regulation established and the three related regulations amended. Once adopted by member states, the policies will become legally binding across the EU.

RED III art. 20(a)

The objective of the Renewable Energy Directive is to facilitate efficient integration of increased shares of renewable electricity in the power system. Access to flexibility sources is seen as crucial to achieving this.

Significantly, Article 20a of the revised Renewable Energy Directive (RED III) is about measures to facilitate system integration of renewable electricity, and hence, about ensuring efficient development, procurement, and use of flexibility sources. Its five paragraphs cover:

- Customers' access to information

- Interoperability and harmonised approach for access to the data from paragraph 1

- Access to basic battery information

- Smart and bi-directional charging

- Non-discriminatory access for small and mobile storage assets to electricity markets, including capacity markets and local flexibility markets

Article 20a is an amendment to the previous version of the Renewable Energy Directive. Member states are to implement their provisions by 21 May 2025. The Commission has published a guidance document (C(2024) 5041 final) to help member states in the implementation of Article 20a. This document explains and details the paragraphs, including their interlinkages and overlaps with other EU legislation.

The provisions imply requirements regarding data and market access for different actors:

- TSOs and (if possible) DSOs to increase transparency of and access to relevant data to electricity market players, aggregators, consumers, and end-users, including EV users. Specifically, information about RES share and GHG emissions is to be made available in real-time and with a maximum granularity of one hour in each bidding zone.

- In addition, DSOs are to provide anonymised and aggregated data on the demand response potential and injected generation from self-consumers and renewable energy communities.

- Battery and EV manufacturers must enable access to information on battery owners and users, including access to such data for third parties acting on their behalf.

- Member states are to

- ensure that DSOs are fully informed about flexible load assets in their systems, e.g., through a permitting or notification procedure if necessary,

- ensure smart recharging, and, where appropriate, interface with smart metering systems, if deployed by MS, and bidirectional recharging functionalities for non-publicly accessible normal power recharging points, and

- non-discriminatory access for small and mobile storage assets to the balancing and flexibility services markets.

Appliances explicitly mentioned in Article 20a are PVs, Heat pumps, EV charging, small storage assets, and Building management systems, but the provisions cover most relevant appliances as they are not technology specific.

Regarding interoperability, the guidance advises Member states to use specific existing, commonly agreed data exchange formats and standards for standardised data exchange between system operators. Advice is also offered on how member states can achieve the required interoperability and a harmonised approach for access to data.

The Electricity market directive and the Electricity market regulation

The Electricity market directive and Electricity market regulation, whose general objective is to ensure a well-functioning electricity market, also contain provisions relevant to the utilisation of demand-side flexibility. Significantly, the Regulation sets out that DSOs should be incentivised to procure flexibility services and gives the EU DSO entity the task of “facilitating demand side flexibility and response, and distribution grid users' access to markets”. Article 3 sets basic rules on non-discriminatory access to flexibility markets, Article 13 is about possibilities for (independent) aggregation, and Articles 15-17 are about the role of active customers (that own an energy storage facility) participating in the market.

The Regulation says that consumers should have the possibility of participating in all forms of demand response and sets out incentives for the use of flexibility in the distribution networks (Article 32) and the integration of electromobility into the electricity network (Article 33). The provisions imply that DSO regulations that incentivise the DSOs to procure flexibility services should be put in place, and that procurement should be market-based, transparent, and non-discriminatory. Similarly, EV charging points should be regulated with a view to facilitating connection to the distribution networks. DSOs are not allowed to own, develop, manage, or operate charging points (unless they are strictly for their own use).

Assessment and implications for the Nordic regulators

The EU regulations and processes approach the challenge of unleashing demand-side flexibility from several angles – from the market angle by facilitating market access (and reducing transaction costs) for flexibility providers and strengthening the incentives (or requirements) on TSOs and DSOs demand for DSF, and from the flexibility product design angle by developing technical requirements or industry standards on potentially smart appliances. These provisions and processes should indeed create stronger incentives for the use of flexibility and the development of innovative solutions, improved information, and lower transaction costs that are undoubtedly important enablers for the development of liquid flexibility markets.

However, the necessary comprehensive set of EU rules and regulations for efficient utilisation of DSF in the IEM is (still) on the drawing board. When it comes to EU policy development, it is quite common that early provisions are quite general and subsequently tightened and followed up by more detailed provisions over time, as experience is gained and technologies, solutions, and methodologies are developed. It is also quite common that some regulations and rules apply at the EU level, while others still give the member states significant freedom when it comes to implementation nationally. Notably, the NC DR contains several national TCMs applying to, e.g., baselining methodologies and rules for TSO-DSO and DSO-DSO coordination. Sometimes, such national leeway is provided due to system differences that imply that uniform rules across the EU are not deemed efficient, and sometimes, in cases where new solutions are developed, one wants to stimulate continued innovation until the solutions are sufficiently mature to tighten the regulation and decide on uniform rules and standards. Such an approach is also in accordance with the development of regulation in contango with the CRI level described in section 4.3.

As noted on the website of the CoC initiative, “policy support for a wide-scale deployment of Energy Smart Appliances is a complex matter”. One of the difficulties is the baselining issue that has haunted the flexibility discussion for years. Unable to find the perfect, or generally well-working, solution, the NC DR still leaves the question to national authorities, while requiring that the chosen solutions be reported to a common directory. Presumably, this directory will serve as a basis for future assessments of the various models and, hopefully, for further common rules and regulations based on the best practices that emerge. A timeline for such developments has, however, to our knowledge, not been set.

Apart from an understandable impatience with a seemingly slow-working EU rule-making process, there is little evidence that the EU regulations directly hamper the development of flexibility markets for member states that wish to go further in their efforts. Based on the comparably advanced experience from numerous pilots and demos, the regulations leave room for the Nordic countries to continue to be front-runners in the development and utilisation of DSF in both market and system operation.

On the supply side, the development of regulations to ensure the smartness and interoperability of appliances is, however, less advanced. The lack of such industry standards and regulations does come with the risk of hampering the advancement of flexibility solutions and provision in the Nordic market, thus indirectly also hampering the DSOs' demand for DSF and the development of liquid flexibility markets.

The process towards future common “plug and play” standards and requirements for appliances is left open-ended, which is unfortunate. The EU's justification for not setting common standards for appliances is explicitly that setting common standards at an early development stage risks being counterproductive when it comes to developing optimal requirements for the smartness of electric appliances (cf. the CRI approach described in section 4.3). The CoC process and the application of its results in EU regulation are an important step towards ensuring “interoperability across the board”, and its progress is vital. The CoC process should result in technical and commercial maturity of flexible and smart appliances and provide a basis for standardisation of product requirements and inclusion of corresponding minimum requirements integrated into the ESPR sustainability regulation, according to specified criteria and depending on available technology. However, to our knowledge, there is no set timeline for the CoC process, nor is there any plan for the inclusion of its findings in EU regulations. In addition, participation in the CoC process is voluntary for industry actors. In order to step up and speed up the process to remove this crucial barrier, it is necessary to develop a road map with an action plan, stricter timeline, and clearer milestones for the advancement of these crucial elements for the development of the supply side, i.e., standards for the flexibility of appliances and their interoperability. In this respect, the vital steps are to determine the flexibility criteria and set appropriate minimum requirements for the relevant appliances.

Policy Recommendations

The objective of this report is to inform regulatory approaches that can facilitate and promote the adoption of beneficial demand-side flexibility solutions in the Nordic power system. Increasing the provision of flexibility by engaging and enabling demand side flexibility requires investments by providers as well as users and includes the provision of explicit as well as implicit flexibility. Such investments will only happen if there is a positive “business case” for flexibility provision.

The profitability of investing in flexible solutions can be enhanced by reducing costs and increasing revenues. Regulations can promote cost reductions and increased revenues. On the cost side, making appliances smart and accessible via automatic signals is necessary to make it technically feasible, easier, and cheaper to react to market signals. Reducing the costs of flexibility provision should also, ceteris paribus, cater for increased interest and demand for DSF from TSOs and DSOs. Regulatory measures could also promote more efficient use and increased revenues from flexibility provision by strengthening the grid companies’ incentives to use flexibility in grid operation and planning. This includes expanding the opportunities to supply flexibility across platforms and uses, i.e., removing unnecessary barriers to value stacking, taking into account that explicit TSO and DSO flexibility markets will not be the only revenue stream for flexibility providers. Other revenue sources include adapting to spot prices and grid tariffs.

Combining the insights from the 10 case studies with knowledge of how Nordic DSOs and TSOs are using demand side flexibility today, we discuss possible policy measures to address the barriers summarised in Table 27. We have organised the policy discussion on the basis of six overarching messages that may guide the Nordic regulators’ further work on framework conditions in this field.

Six messages guiding the future regulation of DSF in the Nordics

The case studies reveal an array of both specific barriers and enablers for flexibility provision, thus providing an up-to-date knowledge basis for the continuation of regulatory efforts to enhance the provision and use of DSF in the Nordic markets. However, the mapping of pilots and initiatives shows that the knowledge base is fragmented, and a host of issues still need to be resolved. Our general assessment is that it is premature to recommend a specific set of measures that could be readily implemented. We do, however, think that the insights from the studies provide valuable guidance on the way ahead for the Nordic regulators.

The detailed case studies focus on the provision of DSF in explicit market contexts or pilots that are limited in scope, space, and time. Recommendations on policy frameworks need to take into account the larger picture, including market signals and grid tariffs incentivising the provision of implicit flexibility and the multiple uses of explicit and implicit flexibility. Notably, the lack of standardised requirements for flexibility and interoperability of smart appliances acts as a barrier for the provision and use of both explicit and implicit flexibility. Similarly, the possibility to earn revenues from the provision of flexibility depends on access to all procurement platforms where the flexibility bears value for the system (where the opportunity cost is – or may be – higher). Limiting access to products, platforms, and markets reduces the potential revenues for providers and increases the cost of using flexibility for DSOs and TSOs. Notably, such limitations also increase the uncertainty of investing in flexibility for both suppliers and grid companies.

In section 4.3.6, we provide recommendations that mainly regard the establishment of standards and requirements for the smartness and interoperability of appliances in the EU. Such standards and requirements should indeed be developed on an EU level, both because the appliances are traded in a European market and because the standards and requirements are integrated in other EU regulations that apply to the Nordic markets as well. Hence, we recommend that the Nordic regulators take initiatives to speed up the processes by developing a road map and work plan for the inclusion of such standards in EU regulation.

A similar comprehensive road map and work plan, covering the development of other elements that are necessary to advance the use and provision of flexibility, should be developed for the continued efforts to develop flexibility solutions for the Nordic market. Below, we present our recommendations for what such a road map should focus on and for the principles or factors that should guide the development of such a plan.

Message 1 – Using demand-side flexibility to solve grid issues represents a fundamental change in how DSOs operate their grids, increasing the importance of technology-neutral economic regulation of DSOs

Well-functioning markets where DSF can participate and be adequately remunerated require that the demand is there. Explicit demand for DSF depends on the demand for the relevant flexibility services from DSOs and TSOs. This demand depends heavily on the incentives embedded in the economic regulation of grid companies.

DSOs are responsible for providing grid capacity to all customers with satisfactory quality of supply according to current regulations. This objective may be achieved through grid investments and operational measures. Until recently, access to adequate operational measures has been limited for DSOs. Technology development has changed this for the better. At the same time, operating the grid has become more complex. Along with the energy transition, we have seen an extraordinary increase in demand for grid capacity in addition to an ever-growing proportion of power production that is not continuously available. Transitioning from reliance on grid investments alone to also trusting market measures to deliver the necessary flexibility at the right time and place requires the right incentives for DSOs to adopt new solutions and change their “culture”. This requires adaptation in the economic regulation of DSOs that was developed according to traditional grid operation.

The authorities should adapt the economic regulation of DSOs to make it technology-neutral in terms of how they choose to comply with their responsibilities, cf. the approach of E.ON Energidistribution. Changing the economic regulation of DSOs is a complex matter that needs to be well thought through to achieve the desired effects, and the details need to be analysed beyond the scope of this project.

This first message addresses one of the barriers described in Chapter 4.1., “Counteractive incentives in the economic regulation of DSOs. In both Norway and Sweden, we have identified through the case studies that the economic regulation of DSOs makes investments in physical grids more economically appealing than investing in flexibility measures. Making sure that the economic regulation is technology-neutral will remove such counteractive incentives, which may prevent DSOs from choosing the overall most economically efficient solutions when providing grid capacity.

Message 2 – When establishing a local DSF market, the DSO should commit to and invest in it, building market liquidity for the longer term

A barrier that is recurrently reported from the case studies is the lack of market liquidity, in particular in terms of the supply of flexibility sources. Linked to this challenge is low or lacking economic compensation, uncertainty of its future value, and a lack of information and knowledge among potential flexibility providers.

From the DSOs' standpoint, they need to trust that sufficient demand-side flexibility capacity can be delivered at the right time and place. However, demand-side flexibility providers will only deliver what the DSOs need if the investment and/or effort is worthwhile, i.e., expected to pay off. This chicken-and-egg dilemma needs to be resolved.

From the mapping of flexibility initiatives and case studies conducted in this project, we observe that most of the pilots are limited in both scope and time, and as such, likely to yield limited information about the full potential of DSF provision in a future, mature market. In general, the pilots test solutions, but to reveal the full scope of the demand and potential for provisions needs to be seen in a wider context and over a longer time period where both the demand and the supply side have time to mature. To bring about such necessary changes, regulatory action is likely to be necessary.

The only Nordic country with semi-permanent local DSF-markets is Sweden, where E.ON Energidistribution has established DSF markets in nine grid areas. This case study clearly shows what they do differently to make it work: After having established through thorough analyses for each grid area that a DSF market is the better solution, they invest in the market by ensuring that it will be operational for a set number of years and guarantee the providers a minimum reservation (availability) fee.

Correspondingly, regulators can enhance such behaviour by requiring that the DSOs integrate analyses of the long-term potentials and benefits of exploiting DSF in their long-term grid planning, and that, if the analyses show that the use of DSF is a promising avenue to take – in combination with other measures – that the DSOs take steps to develop the supply of flexibility in their grid area. Moreover, the regulator should provide guidance on how the DSOs can take action to reduce the uncertainty for potential providers in order to enhance market liquidity (provision). Building on the experience from the E.ON markets, reducing uncertainty by guaranteeing minimum compensation for a set time period and informing on how and when they are planning to use the market the most, based on which grid issues the market will be used to fix, and educating and informing their grid customers, are steps likely to increase flexibility provision.

Making the general DSO regulation technology-neutral in the choice between grid investments and operational measures (cf. message 1) would reinforce the attractiveness of increased use of DSF for DSOs and should thus increase the explicit demand for local DSF further.

Establishing a local flexibility market is, however, not always the right procurement method for DSOs who want to use demand side flexibility to solve grid issues. We discuss this in message 6.

This second message addresses four of the identified barriers. When grid companies ensure that the flexibility market will be operational for a set number of years and guarantee the providers a minimum reservation (availability) fee, this will both help increase the market liquidity and address issues of no or too low economic compensation. It will furthermore reduce the uncertainty about future market conditions and reliability. Finally, an important finding from the use cases is that many potential flexibility providers are unaware of their own ability to participate in and profit from flexibility markets. Clear communication from the grid companies on how and when they are planning to use the market the most should help increase the knowledge of possible flexibility suppliers.

Message 3 – New initiatives should continue to build on experience from previous studies and address identified barriers, but focus on TSO-DSO and DSO-DSO coordination

Ongoing initiatives are developing solutions to identified barriers and building on experience from earlier pilots and initiatives. However, as the pilots are fragmented and often limited in scope, there is a clear need for a strengthening of the DSO-DSO and TSO-DSO coordination dimension to further leverage the learnings and increase the attractiveness of flexibility provision as an integral part of grid operation and planning. Lacking opportunities for value stacking or prohibitively high costs of participating in more than one market with the same loads are important barriers for the development of liquid markets for local flexibility. Related to this is the need for further technological development and standardisation of the appliances and their interoperability, which is necessary to make DSF attractive for DSOs and aggregators to bring down the cost for the provision of flexibility from smart appliances. While the conducted studies and pilots have increased the understanding of the issues and developed solutions to some of them, several barriers related to coordination and value stacking opportunities are yet to be solved, in addition to a lack of standardized communication protocols, including rebound effects causing voltage issues in the local grids, baselining issues, and different participation requirements and designs in local markets.

Examples of important barriers experienced in early pilots that are addressed in subsequent and ongoing flexibility initiatives are:

The development of a flexibility register in Euroflex. Flexibility registers will ease the ability to participate in multiple markets and thus achieve value stacking, which is stated as a barrier in many of the case studies.

Introduction of the new product, MaxUsage, introduced in the NODES platform. The new product eliminated baseline issues by only requiring a pool of loads to stay within a certain capacity level.

- Preventing rebound effects due to pure price optimisation, causing voltage issues by “Grid-friendly activation”, may be solved through better coordination. In Battflex, the issue of potential rebound effects was mitigated through implementing an automatic and autonomous voltage control algorithm in the smart control unit of each appliance. Combining this with price optimisation, grid-friendly activation was achieved, and rebound effects were prevented.

- Most initiatives only involve one or a few DSOs. Solutions and coordination necessary to enable participation in multiple markets should be developed through pilots where both TSOs and DSOs participate. The only case study where a marketplace for both a TSO and a DSO is established is Helen Electricity Network’s and Fingrid’s marketplace for congestion management. The goal of this pilot is to establish a common national marketplace. An important benefit of developing such a common marketplace is that it prevents different requirements and designs of local DSF markets.

This third message addresses five of the identified barriers. Baselining issues and value stacking are important barriers that are addressed in subsequent flexibility initiatives, showing a healthy innovation process. At the same time, the initiatives are not sufficiently focused on coordination between the actors. Strengthening the DSO-DSO and TSO-DSO coordination is crucial to enable value stacking. Enabling participation in more than one market with the same load will increase profitability and, by that, contribute to the development of liquid markets for local flexibility. We have also seen that coordination between actors is crucial for solutions to prevent voltage issues due to rebound effects. Coordination may also prevent different requirements and designs in the different local DSF markets, which can cause entry barriers and reduce economies of scale.

Message 4 – Verification requirements for smaller loads should be simplified, and the focus should be on incentivising the ability to react to market signals

The loads from smart appliances are generally small, and using them as flexibility resources can easily be dismissed as not being worth the hassle. Our estimates of the overall flexibility potentials of smart appliances show, however, that on an aggregated level, they can offer substantial amounts of flexibility to the power system. In view of the prospects for a growing need for flexible resources in the power system, their significance should not be dismissed. Being able to react to variations in spot prices (implicit flexibility) is currently the main motivation for demand-side investments in flexible solutions. This could be interpreted as implicit flexibility outcompeting explicit flexibility. In other words, it is more money to be made by simply following the spot price than participating in flexibility markets. While the latter might be true, it is not necessarily a problem. On the contrary, without the profits one can gain by adjusting electricity consumption according to the spot price, it could very well be too costly for providers to make the investments or changes in behaviour necessary to be able to participate in (explicit) flexibility markets. Beyond what is required for implicit flexibility, additional requirements to enable explicit flexibility are related to the aggregation and verification of delivery. Simplifying requirements to offer explicit flexibility beyond what is necessary to react to spot prices will make the provision of explicit flexibility easier and more profitable for many loads.

As stated, the value of flexibility from each appliance is small. For smaller loads to deliver flexibility, the necessary investment must also be small. Thus, we cannot require the same accuracy of data and verification as for big industrial loads participating in TSO reserve markets. An important question is what the most important feature is – that they react exactly like what they are paid to do, or that they act according to what is beneficial for the power grid in the situation. The overarching goal is to ensure the availability of resources that are able to be flexible. Several examples show that implicit flexibility has solved prognosticated grid issues that would otherwise have had to be solved by explicit flexibility. For example, in Sthlmflex, projected grid issues did not occur to the expected extent due to increased electricity prices after the Russian invasion of Ukraine, in addition to reduced electricity demand due to a mild winter. Another example is the Swedish activation strategic reserve, which, according to Svenska Kraftnät, has not been used to support the Swedish power system for the last 10 years

The strategic reserve was activated one time during the winter of 2021/2022, but this was related to offering help to Poland: https://www.svk.se/press-och-nyheter/nyheter/allmanna-nyheter/2023/om-inte-elen-racker-till-finns-effektreserven/

THEMA (2015): Capacity Adequacy in the Nordic Electricity Market. https://library.oapen.org/bitstream/handle/20.500.12657/32905/594223.pdf?sequence=1

For many small loads, like smart appliances often are, the most valuable approach might be to only incentivise the loads to be able to react to market signals. This could imply paying resources to be able to react to relevant activation signals, leaving verification and payment of activation out of the equation. One way to do this could be compensating all resources that are registered in the flexibility register, provided that they qualify according to a given set of requirements. Over time and with the employment of forecasting models, it will be easier to estimate the share of resources that are actually available for activation. Hence, DSOs and TSOs should consider simplifying verification requirements for smaller loads like smart appliances in buildings, where complex requirements related to baselining, individual measurement, and verification requirements would make participation in flexibility markets too costly.

This fourth message addresses three of the identified barriers. Simplifying verification requirements for smaller loads directly addresses the barrier regarding electricity consumption measurement and verification accuracy. Removing verification requirements for smaller loads will also remove the baselining issues for these loads. Finally, making provision of flexibility easier and more profitable for small loads can increase market liquidity.

Message 5 – We need to rethink risk in the power grid

Technology developments have enabled increased grid capacity utilisation without increasing the risk of outages. This is, for instance, achieved by relying on actual measurement of grid capacity, rather than on theoretical limits with substantial margins. At the same time, the cost of maintaining the delivery quality we are used to has increased. Operating the power grid has become more complex with a new generation mix. In many of the Nordic countries, long grid connection queues are waiting for grid investments, which also come with a high cost for society. When achieving the same level of outage risk (loss of load probability) becomes more costly, it should be considered whether a slight increase in the loss of load risk is acceptable. In the 2023 strategy of Norwegian TSO Statnett, one of the main points was that digitalisation would make it possible to increase the utilisation of today's power grid through grater calculated risk taking.

Taking calculated risks is enabled by digitalisation, which provides more and better data that can be used in grid operation and planning

Statnett (2024): Økt utnyttelse av anlegg i det grønne skiftet - håndtering av risiko. Presentation at "NVEs kraftberedskapskonferanse", 16th of January 2024

This fifth message addresses calculated risk-taking in general and is illustrated by an example where the identified barriers of baselining issues and lacking harmonisation of electricity consumption measurement and verification accuracy are addressed.

Message 6 – Complex markets are not necessarily always the best way to utilise demand-side flexibility

As shown in Chapter 2, local flexibility markets are not the only way to make use of demand side flexibility to solve grid issues. Conditional connection, bilateral agreements, and grid tariffs are examples of other means that can also be used and are generally a lot easier to handle for both parties. These measures do not generally involve bidding and activation, eliminating many important barriers like baselining issues, non-standardised communication protocols, and verification. For instance, as we have previously discussed, it can be difficult to acquire sufficient market liquidity in local flexibility markets aimed at solving local bottlenecks. In Sthlmflex, they decided to discontinue the market mainly due to lower-than-expected demand for flexibility. The DSOs see the need for flexibility as present and growing, but in the near term, they see other flexibility measures, such as bilateral contracts or conditional connections, as more promising. In general, the benefits of more advanced and accurate measures should be weighed against the costs. This also underscores the importance of technology- or solution-neutral economic regulation of DSOs to incentivise their finding of the best combination of solutions to comply with their responsibilities.

This final message is a reminder that there are other efficient procurement methods of demand side flexibility that do not face many of the issues markets bring with them. This includes three of the identified barriers regarding lack of standardised communication protocols, lack of harmonisation of electricity consumption measurement and verification accuracy, and baselining issues.