7. CBAM system expansion

The discussion around the scope of CBAM centres on two main approaches: narrow, feasible implementation and a broader, more efficient one. (Kuusi et al.. 2020) One of the principal strengths of the narrow design is its administrative practicality: by targeting a limited number of sectors, the EU has aimed to streamline data collection, regulatory enforcement, and compliance, reducing the complexity for customs officials, regulators, and businesses. Legally and politically, the focused nature of the mechanism helps demonstrate fairness in international trade, lowering the risks of World Trade Organization disputes and minimizing potential trade retaliation. Economically and environmentally, the impact of the EU CBAM remains contained, as it affects only a fraction of total imports.

However, a narrow CBAM has its drawbacks. Its limited coverage means it cannot fully resolve the problem of carbon leakage, and there remains the risk that emissions could shift into products not covered by the mechanism. This loophole could undermine the effectiveness of the EU’s climate policy.

In contrast, a broader CBAM would encompass a much wider range of emission-intensive products, potentially covering up to all manufacturing sectors. It would involve more detailed and country-specific emissions data and might include all direct and indirect emissions. The broader scope would allow the mechanism to address carbon leakage much more effectively, as more imported emissions would be covered and there would be fewer opportunities for emissions to shift into unregulated products. This would send a strong price signal to foreign producers, encouraging decarbonization across more sectors, and would help ensure a level playing field between EU and non-EU producers. In the long run, a broader CBAM would align with more ambitious climate targets and could prepare the ground for broader international cooperation on carbon pricing. The broader approach, however, brings significant challenges. The complexity and administrative burden increase sharply, as collecting, verifying, and monitoring emissions data across many sectors and countries is difficult and costly.

The risk of legal challenges also rises, since a broad CBAM is more likely to be viewed as arbitrary or discriminatory under international trade rules. Political risks are higher, too, as the chances of retaliation from trading partners—especially large economies like China—increase. There are also potential negative effects on EU industries that rely on global value chains, as more expensive imported inputs could make these industries less competitive internationally.

The current situation is that the CBAM system is set to expand its scope to include either more downstream products, more emissions per product category, or new product categories also covered by the ETS. Expansion of the CBAM system will increase the current costs for importers and can potentially include more importers in the system.

Many questions about the expansion have not yet been clarified by the EU. According to article 30 of the CBAM regulation, a report on potential expansion of the regulation should be published by the end of the transitional period (late 2025), but had not been so by the finalisation of this report.

This section will investigate the potential impacts of different types of expansion. Listed in article 30, are four possible avenues of expansion for the CBAM scope:

- Embedded indirect emissions in the goods listed in annex II

- Embedded emissions in the transport of the goods listed in annex I

- Goods at risk of carbon leakage other than those listed in annex I, and specifically organic chemicals and polymers

- Other input materials (precursors) for the goods listed in annex I.

Further, in recital (38) and (65) the future expansion to cover downstream products is mentioned, to avoid carbon leakage.

Expansions 2 and 4 extend past the scope of the report, and as such the following section will focus on extending CBAM to cover indirect emissions, and which sectors CBAM potentially could expand into.

7.1 Impact of CBAM expansion on Nordic competitiveness

Previous sections have described the current state of the CBAM regulation, and the opportunities and risks it presents for Nordic industry. This section builds on the previous conclusions, by investigating what would happen if the scope of CBAM was expanded to include indirect emissions.

7.1.1 National elasticity to increased costs

Expanding CBAM to require importers to purchase CBAM certificates for both direct and indirect emissions for all covered sectors will increase the economic burden on importers and will improve conditions for the protected sectors. In the following, the increased expected cost is modelled.

Evaluating the increased costs from both direct and indirect emissions can be done using emission data from the EEMRIO database EXIOBase. The datasets in EXIOBase allow a division of CO2-emissions into categories. It is possible to distinguish how much CO2e is emitted from direct sources (e.g. coke or coal), indirect sources (e.g. electricity), and other sources (precursor products, transport, waste treatment, etc). CO2-emissions from indirect and other sources might possibly be tariffed with an expansion of CBAM. Using an average ETS-rate it is possible to calculate the annual increased cost for importers, for all four sectors, nationalized to exporting countries (Figure 4)

The emission factors (EF) are calculated as a weighted average between the largest countries by imported mass, covering minimum 80% of imports. The EFs are calculated per sector per country, weighted by the imported amount from each country.

Figure 10. Calculation of total cost increase in % for both direct and indirect emissions, compared to average existing cost. An average ETS price of 72.8€/T CO2e is used.

Based on the percentual price increases, as well as a list of European tariff elasticities (Kuusi et al, 2020) it is possible to calculate the predicted percentual change in imports. No tariff elasticity is available for fertilizers, so this sector has been excluded.

Figure 11. Predicted decrease in import due to increased CBAM costs from direct and indirect emissions

Note: The graph’s y-axis starts at 95% and stops at 101% to enable a better visualisation.

The predicted decrease in imports, corresponds to an economic value that is displaced from the current exporting countries to either EU or non-EU producers, or results from reduced demand due to higher prices. The estimated annual economic values of displaced imports are seen in Table 2. and vary significantly across sectors. In particular, sectors such as iron and steel and aluminium account for a substantial share of the displaced value, reflecting both their trade exposure and sensitivity to carbon-related cost increases. In contrast, sectors with lower import volumes or more limited CBAM coverage show smaller absolute impacts.

These sectoral differences suggest that the observed effects reflect a combination of trade diversion and demand reduction, with the relative importance depending on product characteristics and market structure. As discussed previously, Nordic suppliers may have a potential competitive advantage in some CBAM-covered sectors where domestic production has lower emission intensity, although the extent to which displaced imports are replaced by Nordic production rather than by other EU or non-EU suppliers remains uncertain.

Country | Product | Value displaced from direct costs (€) | Value displaced from indirect costs (€) | Sum of displaced value (€) |

DK | Aluminium | 323,866 | 1,290,118 | 1,613,984 |

DK | Cement | 430,446 | 23,706 | 454,152 |

DK | Iron and steel | 6,375,868 | 33,439 | 6,409,306 |

FI | Aluminium | 197,610 | 1,176,905 | 1,374,515 |

FI | Cement | 9,302 | 512 | 9,814 |

FI | Iron and steel | 3,563,105 | 17,735 | 3,580,840 |

SE | Aluminium | 9,883 | 1,965,290 | 1,975,173 |

SE | Cement | 114,308 | 1,678 | 115,986 |

SE | Iron and steel | 180,621 | 13,661 | 194,282 |

Table 2. The annual economic value that is predicted to be displaced from existing exporters, as the cost increases.

In sum, expanding CBAM to cover indirect emissions is likely to reinforce its protective function for EU producers while increasing cost pressures on importers in the covered sectors. By combining EXIOBase emissions data with ETS price assumptions and tariff elasticities, the modelling illustrates how the inclusion of indirect emissions could significantly alter trade flows—both through reduced demand for high-emission imports and through the displacement of economic value toward lower-emission suppliers. While this may create opportunities for Nordic actors, it also highlights the importance of strategic positioning, technological readiness and policy coordination to benefit from these shifts. Ultimately, the results underscore that an expanded CBAM would not only reshape sectoral trade dynamics but also influence industrial competitiveness and the geography of emissions across global value chains.

7.2 Incentives for third countries to introduce emissions pricing

From 2026, EU importers of goods that fall under CBAM must buy CBAM certificates. Number of certificates will correspond to the amount of emissions embedded in the goods imported. The price per certificate will be calculated based on a weekly average auction price of EU ETS allowances, €/tonne CO2. However, if a carbon price already has been paid in the country of origin during production, the amount paid can according to Article 9 of the CBAM Regulation be deducted in accordance with the price paid in the country of origin during production (European Commission, n.d.a). Hence, importing companies are allowed to account for costs incurred under a third-country carbon pricing instrument (CPI) covering the embedded emissions of CBAM products. However, evidence is needed of the carbon price paid in the country of origin (third country), to declare the price that has been paid for the embedded emissions in the imported CBAM goods. In August 2025, the European Commission set out an initiative to provide feedback for the methodology of converting CBAM certificates to the carbon price paid in a third country(European Commission 2025). The commission is planning to adopt a methodology by the first quarter of 2026. The price paid can either be interpreted as the average price for a certain period of time (e.g. quarterly if prices fluctuate) or the actual price paid (Wildgrube et al., 2024). By allowing carbon pricing mechanisms in third countries to be deducted from the CBAM certificates also avoids double counting, which would strengthen the defence for CBAM under international trade law and reduce opposition. This could, in turn, incentivise third countries to adopt carbon pricing mechanisms (Stockholm Environment Institute, 2022).

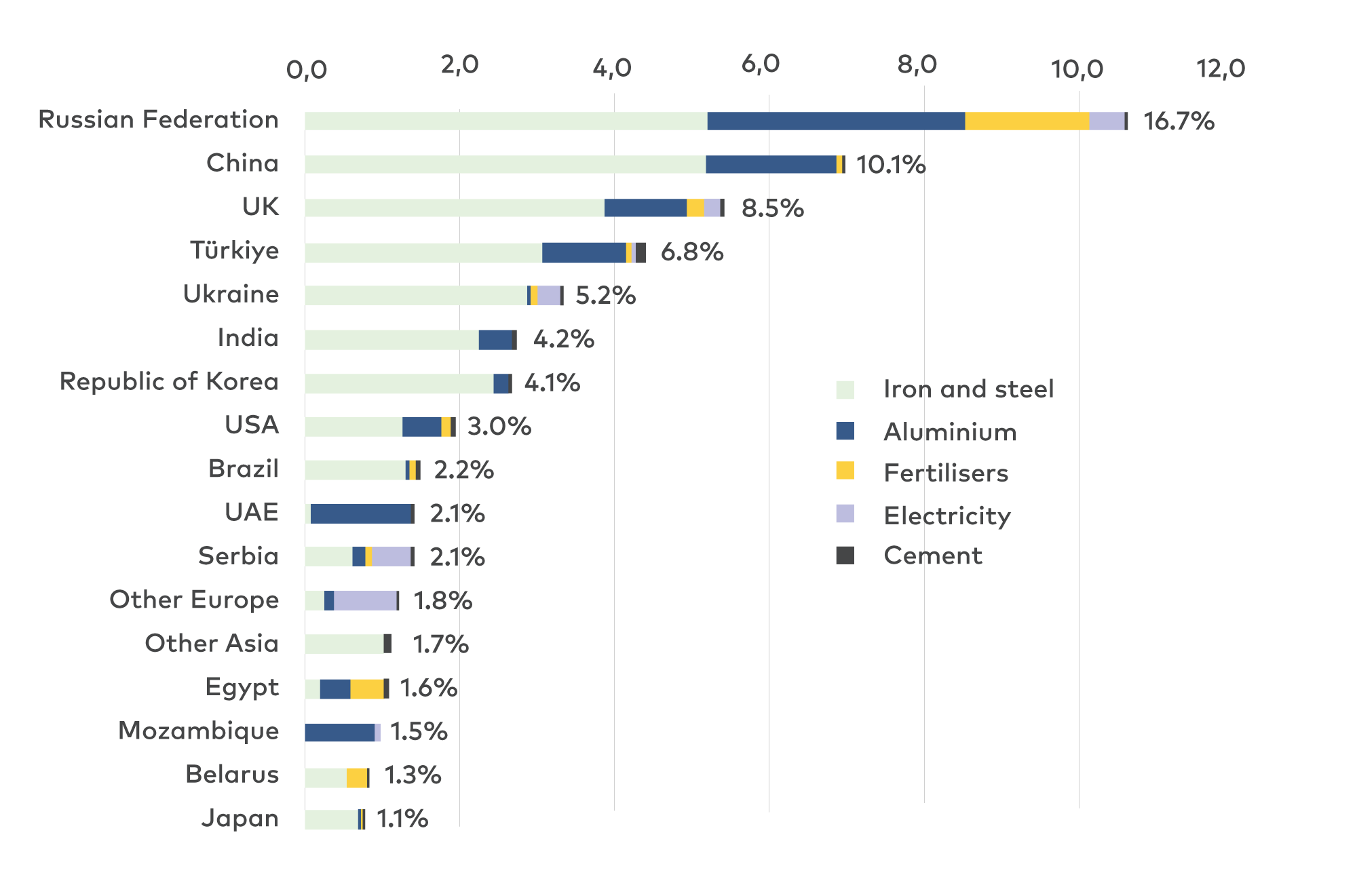

Figure 12. Top 10 exporters of CBAM goods to EU27. Numbers are presented in annual average billion USD, 2015–2019 (Wildgrube et al., 2024). It should be noted that exports from Russia may have changed since the invasion of Ukraine, as several sanctions have been put on Russian products entering the EU.

The figure above gives an interesting picture of the countries that constitute the biggest share of imports to the EU across the different sectors. It shows that iron and steel by far, constitute the largest share of imports to the EU, followed by aluminium and fertilisers.

Carbon pricing is already a widespread policy in third countries. According to CO2-IQ, there is 18 non-EU countries with relevant CBAM carbon pricing implemented at national level (Sirressi, 2024). Of CBAM relevant sectors, 16 of the countries have implemented, or scheduled, carbon pricing for the Iron & Steel sector, 13 of the countries have carbon pricing for aluminium, 12 for fertilizers and 16 for cement. All 18 countries have CBAM-relevant carbon pricing for electricity (Sirressi, 2024).

Countries (out of 18) that have implemented or scheduled implementation for CBAM-relevant carbon prices | Total embedded emissions in CBAM-sector | |

Iron & Steel | 16 | 54% |

Aluminium | 13 | 35% |

Fertilizers | 12 | 13% |

Cement | 16 | 37% |

Table 3. Numbers adopted from CO2-IQ article (Sirressi, 2024), originating from CO2-IQ database for CO2 Price Radar as well as trade data from Eurostat COMEXT 2023.

The incentive for third countries to implement a carbon-pricing mechanism in CBAM sectors is primarily founded in the benefit of the revenue of the policy. If a third-country implements a carbon-pricing mechanism, the levy is paid in the home country, ultimately increasing welfare in the country where the production is happening instead of paying the EU. This is also referred to as carbon revenue leakage. According to a global carbon price forecast of Wood Mackenzie (2023b), in the long term, the coverage of carbon pricing will increase substantially with the financial obligations of the CBAM. However, in the short term, implementing carbon pricing is only incentivized if the country exports a substantial part of its CBAM covered goods to the EU.

Of the top exporting countries of CBAM goods (see figure 12), as of writing this report all countries, but Russia and the United Arab Emirates have implemented or is developing a CBAM relevant carbon pricing mechanism. Most recent are Turkey, Brazil and Ukraine, where these are still in its developing and implementing phase. However, other economic instruments might still be in place, that has an indirect effect on less carbon intensive alternatives, without pricing the direct emissions. This could for example be subsidies, taxes or feed-in tariffs. A feed-in tariff incentivises renewable energy by guaranteeing a specific price from electricity produced by renewable sources, fed into the grid. Furthermore, other voluntary measures like offsets or carbon credits are not recognised either. Hence, many types of domestic carbon pricing mechanisms must be defined and specified to which ones are eligible for deduction under CBAM (Wildgrube et al., 2024). Of all the top exporters, only the UK has a carbon price that is equivalent to the current EU ETS yearly average price level.

According to an OECD report on CBAM effects along the supply chain, country-level results indicate that CBAM imposes a shift in demand towards countries that either has a carbon pricing mechanism in place or has low-emission intensity production in place. Results show that emission intensity (kgCO2/€) has a positive impact, even though modest, on the value added for the exporting country. For example, production that relies on electricity rather than fossil fuels, is positively affected by CBAM. This indicates that CBAM potentially could have a positive effect on third countries to introduce a carbon pricing instrument and change towards lower emission production alternatives (Dechezleprêtre et al., 2025).

In an analysis from the Swedish Environmental Protection Agency (2022), the effect on third countries is also evaluated. The report discusses countries like China, who is an important exporter of e.g. steel and iron to the EU, but the EU market only constitutes a small share of total steel export for China (4% in 2023(Eurostat, 2025a)). It can therefore be assumed, that since the EU constitutes such a small share of total steel and iron export, China is unlikely to change its climate policy regulations because of a price increase due to CBAM. Other countries on the other hand, where the EU market constitute a larger share of the third country´s total exports, will likely be more affected by the introduction of CBAM and hence more willing to change internal climate regulations, e.g. by introducing a carbon pricing mechanism equivalent to CBAM. Example of more affected countries are Ukraine, Belarus and Moldova who are more dependent on exports to the EU, and where the carbon pricing under CBAM will have bigger impact on the national economy (Naturvårdsverket, 2020).

Third countries exporting to the EU have also expressed concern about CBAM. Especially developing countries in Africa have expressed worry that CBAM will apply an extra economic burden on them, undermining their competitiveness and industrialisation development. Most of these countries do not have a carbon pricing mechanism in place, nor low-emission technology in place (Pauw et al., 2022). In a joint statement from NGO´s as a response to the adoption of the CBAM proposal by the EU Parliament and Commission in 2021, five stakeholders

argue for increased financial support from the EU to African countries, to support climate finance investments in these countries. It is pointed out though, that the least developed countries, among them being many of the African countries, account for a small share of carbon emissions from imported goods to the EU. Only exception is Mozambique, which accounts for almost 8% of EU´s imports of aluminium. Therefore, the stakeholders argue that by giving an exemption to these countries, would not have major impact on carbon leakage, but rather ease administrative burdens and costs, which tend to be higher in developing countries. However, this is argued to be a less favourable solution in the long run, as it could cause a major delay in technology investments in these countries, leaving them even further behind in renewable technology development and production processes. Therefore, supportive measures from the EU, both in know-how and financial measures, is argued to be a more sustainable solution in the long run. This is suggested to be done by channelling revenues from CBAM towards climate action policies in third countries. Other third countries like the BRICS

countries state that CBAM is causing discriminatory trade barriers and opposes international trade rules. However, an important incentive to third countries to implement some sort of carbon pricing instrument, is that countries rather want their businesses to pay taxes or tariffs in their home country instead of paying to the EU (Pauw et al., 2022).

Carbon Market Watch, E3G, European Environmental Bureau, World Wide Fund, Climate Action Network Europe

Brazil, Russia, India, China, South Africa

7.2.1 Implementation challenges and considerations

A part of the CBAM definitive regime (from 2026 onwards) is to provide an incentive for third countries to implement a carbon pricing scheme by offering deduction of carbon prices, that has been effectively paid for (European Parliament & Council of the European Union, 2023), avoiding double counting. However, designing a successful deduction system of third-country carbon pricing in terms of CBAM goods encompass a few challenges.

First of all, converting third country pricing (monetary) values to CBAM certification-quantity values can prove to be challenging (see Wildgrube et al., 2024). Second, calculating these values depend on the approach and methodology to do so. Currently, the approach to this is not specified by the Commission, but following the amendments made to the regulation due to the Omnibus package, it is noted in Article 9(4) that a methodology for third countries default carbon prices will be developed and published in the CBAM registry by 2027. How well these calculations are able to capture cases such as multi-product installations are discussed in depth in Wildgrube et al (2024). The main challenge here is based on cases where facilities produce several primary products where some fall under CBAM and some does not. The case of ammonia is highlighted, as ammonia is both a part of the production of fertilizer (part of CBAM) and explosives (not part of CBAM). When a producer pays a carbon cost affiliated with both CBAM and non-CBAM products, it’s important to distinguish between the production to make sure that producers are only being deducted for CBAM goods and not their overall carbon price paid in their home country (Wildgrube et al., 2024).

In an impact assessment from the EU Commission on potential effects from a CBAM implementation, various policy mix options are compared and assessed, where views from stakeholders from the CBAM public consultation has been considered as well. Stakeholders that participated in the public consultation believe that CBAM can encourage more ambitious climate policies in third countries, because it incentivises revenue generation from carbon pricing on the domestic market, rather than the EU. The highest level of agreement was among citizens and civil society organisations, whereas business organisations were somewhat more sceptical about the positive effect on third country incentives to abate emissions. Lastly the assessment suggests what indicator and data input can be used to monitor the impact from CBAM on third country production processes. The indicator suggested is Evolution of actual emissions for CBAM sectors in third countries, where the level of emissions demonstrated by third country producers subject to the CBAM can be used to measure the impact (European Commission, 2021).

The case of subnational carbon pricing systems also needs to be considered in the reimbursement framework. Several nations have emissions trading systems, crediting mechanisms or carbon tariffs at state or regional level, such as the US, China, Mexico and Canada (World Bank Group, n.d). For instance, in the US the state of California has implemented carbon prices at the state border but does not count as a national carbon price. This means, that goods imported from the state of California will not have their carbon pricing deducted unless the framework allows for subnational carbon pricing mechanisms. If these are not met, it is plausible that the competitiveness of Californian goods may be affected poorly relative to states without carbon pricing. According to the World Bank Group, there is, as of 2025, a total of 44 subnational jurisdictions using carbon pricing which is not a negligible amount.

7.3 Sectoral considerations for CBAM expansion

Since CBAM was originally passed, it has been the intention to extend its scope. Extending CBAM to new sectors will pose new trade-offs for the affected sectors, benefitting some companies and adversely affecting others. In this section the potential sectors for expansion will be mapped, based on the available sources.

7.3.1 Sectors explicitly identified for possible CBAM expansion

In both the CBAM Regulation and the subsequent Omnibus amendment, several sectors were highlighted as candidates for a future extension of the CBAM scope. These sectors are characterised by high emissions intensity, significant trade volumes with third countries, or a high risk of carbon leakage—factors that make them likely candidates for future inclusion.

Organic chemicals

Organic chemicals—used widely in the production of pharmaceuticals, plastics, coatings, and industrial intermediates—are associated with substantial process emissions. The sector also has extensive global supply chains, and many EU producers compete directly with imports from regions with lower carbon constraints. Because of this combination of high emissions intensity and strong international competition, organic chemicals have been singled out as a potential next wave of CBAM-covered products.

Polymers

Polymers, particularly plastic polymers such as PE, PP, PET or PS, have high embodied emissions linked to energy-intensive production and fossil feedstocks. The EU imports significant volumes of polymers from countries with varying carbon regulations. Extending CBAM to polymers could therefore address competitive distortions while supporting EU objectives on circularity and decarbonisation in plastics value chains.

Downstream products

Downstream products refer to more processed goods that incorporate inputs already covered by CBAM sectors. At present, only iron and steel products fall under this definition. Including further downstream products would reduce the incentive for importers to circumvent CBAM by shifting to more processed goods outside the current scope. Such an expansion could be particularly relevant for mechanical components, machinery, and assembled products where iron, steel, or aluminium constitute a significant share of the embedded emissions.

7.3.2 ETS-covered sectors

The EU ETS already regulates a large share of industrial emissions. The sectors listed below are currently covered under the ETS, and several of them are also included in CBAM. Understanding the overlap between ETS- and CBAM-covered sectors is important, as it determines how the phase-out of free allowances will affect different industries and how CBAM may interact with existing regulatory frameworks.

Industry / Sector | |

Electricity and heat generation | Production of glass |

Oil refineries | Production of ceramics |

Steel works | Production of pulp, paper and cardboard |

Production of iron | Production of acids (general), and production of nitric, adipic and glyoxylic acids and glyoxal |

Production of aluminium | Production of bulk organic chemicals |

Production of metals (other than iron and aluminium) | Aviation (EEA internal flights and flights departing to Switzerland and the UK) |

Production of cement | Maritime transport (50% of emissions for voyages starting/ending outside EU, 100% between EU ports and within ports) |

Production of lime | |

Table 4. Overlap between EU ETS-covered sectors and CBAM-covered products

The sectors subject to both ETS and CBAM will face the strongest regulatory pressures going forward, as they are exposed to rising carbon prices domestically and increased scrutiny at the EU border. This dual exposure may accelerate investments in low-emission technologies but also increases the risk of competitiveness loss, particularly for trade-exposed sectors with limited substitution possibilities. For sectors covered only by the ETS, the gradual phase-out of free allowances will still impose higher costs, though without the protective effect of CBAM.

7.3.3 Other sectors

Economic analyses have shown that expanding CBAM to cover both imports and exports could more effectively prevent carbon leakage by ensuring that European producers are not disadvantaged in global markets. Since CBAM increases production costs within the EU, export-oriented companies may require compensation or partial refunds of carbon costs to maintain competitiveness when selling to countries without equivalent carbon pricing. Such an export adjustment mechanism could help preserve market access while supporting the transition to low-emission production.

However, extending CBAM to exports introduces legal and practical challenges, particularly with respect to World Trade Organization (WTO) rules and the risk of being perceived as a protectionist measure (Kuusi et al., 2020). It would also require clear criteria for eligibility, robust monitoring systems and careful alignment with existing ETS rules.

Importantly, the development of carbon tariffs is closely linked to the gradual phase-out of free emission allowances under the EU ETS. This is a necessary step to maintain the environmental integrity of CBAM and align with EU climate targets. Yet it may also temporarily reduce the competitiveness of energy-intensive exporting sectors. As a result, some products may see a decline in exports despite the introduction of CBAM, especially in sectors where low-carbon alternatives are not yet scalable or commercially viable.