Introduction

The report addresses conflicting competition/industrial-policy views and recent increases in market concentration in advanced economies, presenting evidence to inform Nordic policymakers about welfare impacts of rising market concentration.

The project is motivated by the need to understand how cross-border mergers and acquisitions (M&A) can potentially strengthen productivity, competitiveness, and capacity for investment in the Nordic economies. As Europe faces mounting challenges—ranging from technological lag to geopolitical uncertainty, there is growing interest in whether strategic consolidation in key sectors can help unlock economic potential.

The Nordic Council of Ministers has commissioned this analysis to explore the conditions under which M&A can deliver broad societal benefits, while also identifying the risks to competition and consumer welfare. While advanced economies have experienced steadily increasing concentration and profitability, the underlying drivers are contested. Part of the explanation lies in structural changes such as globalisation and the rise of intangible assets, while only a modest share can be directly attributed to M&A. This distinction matters for policy: concentration itself is not necessarily harmful, but it may become problematic when high profits are combined with persistent barriers to entry.

For the Nordic region, these issues are particularly relevant. The Nordics are small, open economies that perform strongly compared to most EU peers, yet they remain vulnerable to structural challenges. They face a widening digital investment gap vis-à-vis the US, a limited presence among the world’s largest technology firms, and less developed capital markets. At the same time, the region hosts globally competitive pharmaceutical companies and highly digitalized SMEs, underscoring both strengths and weaknesses. The central policy challenge is therefore not only how to safeguard competition at home, but also how to ensure that Nordic firms remain able to scale and compete internationally.

The project aims to provide a structured framework and evidence base to inform policy decisions that balance economic efficiency with strategic resilience in a rapidly evolving European industrial landscape. A recurring theme throughout the analysis is the dual nature of mergers. On the one hand, they can deliver efficiency gains, knowledge transfer, and stronger international competitiveness. On the other hand, in concentrated sectors they risk entrenching market power, raising consumer prices, and reducing innovation. The balance between these outcomes—the so-called Williamson trade-off—is at the heart of current debates on competition and industrial policy.

The aim of this report is therefore to provide Nordic policymakers with:

- Evidence on the relationship between M&A, competition, innovation, and productivity.

- Analytical tools to distinguish between cases where M&A may benefit society as a whole, and cases where the risks to competition and consumer welfare are more significant.

- Policy recommendations on how Nordic governments can support growth, productivity, and resilience without undermining competition.

The findings presented here build on a combination of literature review, quantitative analysis, and expert interviews across the Nordic countries. This approach provides both empirical robustness and sector-specific insights. The results are summarised below in an extended analysis box, structured according to the report’s three research questions. Each set of findings highlights not only the state of evidence, but also the implications for policymakers in the Nordic countries and in the wider EU.

The report is structured around a set of guiding questions that frame the analysis across chapters. These questions capture both the drivers of cross-border M&A, their economic effects, and the broader policy implications for the Nordic region.

Chapter 1 revisits the literature on cross-border M&A to assess the correlation between increased market concentration (fewer and larger firms) and the ability of these firms to compete in international markets. The chapter also explores the relationship between market concentration and economic outcomes such as investment, innovation, and productivity.

Chapter 2 explores the desirability of enabling more mergers in EU and the Nordic region based on the conclusions drawn from chapter 1. It discusses how the EU competition authority (DG COMP) currently reviews mergers, and we analyse the rejected merger proposals by the commission. The chapter further explores what economic and structural barriers might prevent more M&A deals within EU and the Nordic region.

Exhibit 1

Main analysis questions

Main analysis questions

Chapter 1: Do large cross-border merger and acquisition deals in internationally competitive sectors enhance firms’ ability to com-pete and are they associated with positive firm outcomes (e.g., investment, innovation, and productivity)?

Chapter 2: Is more cross-border M&A activity desirable in sectors important for the green and digital transition from an economic and/or Nordic perspective? What is preventing more cross-border mergers from taking place?

Chapter 3: How can the Nordic governments promote productivity, competition, and investment in technologically advanced sec-tors.

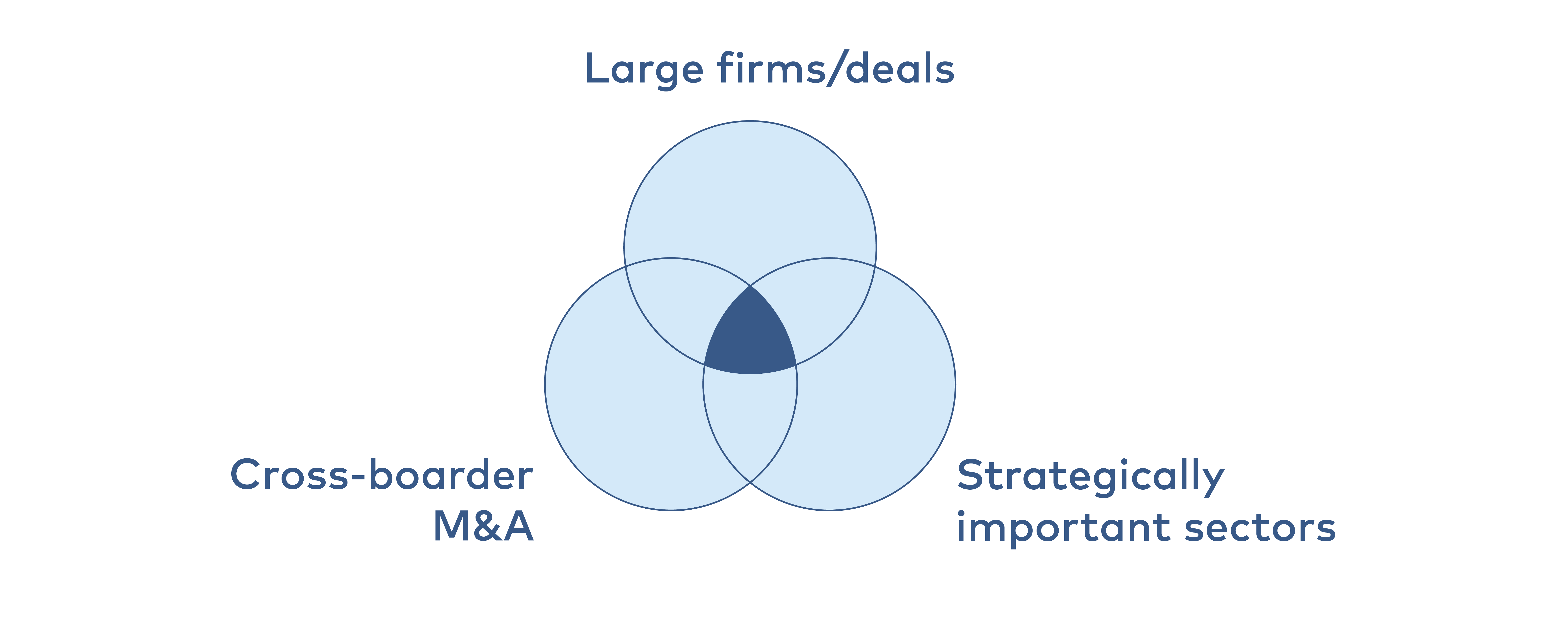

The analysis concentrates on the types of transactions and sectors that are most relevant to current policy debates in the Nordics and the EU. This focus reflects the fact that industrial policy discussions are primarily concerned with large, internationally active firms operating in sectors that are central to Europe’s technological capabilities and strategic resilience. The scope of our analysis is illustrated in exhibit 2 and focused along three key dimensions:

Exhibit 2

Illustration of overall scope of the report

Illustration of overall scope of the report

Source: HBS Economics

Focus on large-scale M&A transactions

The report concentrates on large M&A deals involving major corporate actors. While numerous smaller mergers take place across the EU and Nordic countries—typically handled by national competition authorities, these are of secondary interest to this analysis. This focus reflects the fact that current policy debates centre on industrial policy considerations that are primarily relevant for large, internationally active corporations.Emphasis on cross-border M&A

Cross-border M&A transactions are of main interest and domestic M&A activity is mainly included in the analysis as a baseline comparison. Cross-border deals are defined as deals where the merging firms are headquartered in different countries.Strategically important sectors

The analysis is limited to sectors considered strategically important in a European and Nordic context. Based on the framing presented in the introduction, we define strategically important sectors as those that meet one or more of the following criteria:- They are technologically advanced

- They function in internationally competitive markets

- They are critical to the green transition, or

- They are essential to digital transformation.

To guide the analysis, the report applies several key concepts and definitions that clarify what is meant by cross-border mergers and acquisitions and how they are assessed in competition policy debates. These concepts are presented in exhibit 3.

Exhibit 3

Key concepts

Key concepts

Cross-border mergers and acquisitions

A cross-border merger and acquisition (M&A) refers to a transaction in which the acquiring firm and the target firm are headquartered in different countries. This type of M&A involves the transfer of ownership or control of assets across national borders and can take various forms, including:

A cross-border merger and acquisition (M&A) refers to a transaction in which the acquiring firm and the target firm are headquartered in different countries. This type of M&A involves the transfer of ownership or control of assets across national borders and can take various forms, including:

- Mergers, where two companies combine to form a new legal entity

- Acquisitions, where one company purchases a controlling stake in another.

Types of M&A

- Horizontal mergers occur between competitors in the same industry. These often raise competition concerns, as they may reduce rivalry and enable price increases or reduced output.

- Vertical mergers involve firms at different stages of the supply chain. They are typically associated with efficiency gains such as lower transaction costs and better coordination, though risks such as foreclosure of rivals may arise.

The Williamson trade-off

- A classic framework highlighting the tension between efficiency gains (e.g., economies of scale, lower costs, improved coordination) and increased market power (e.g., higher prices, reduced output). This trade-off remains central to the assessment of whether mergers deliver overall welfare benefits.

Tangible vs. intangible assets

- Intangible assets (such as patents, data, know-how, and brands) are highly mobile and strategically sensitive. They are particularly relevant in technology- and knowledge-intensive sectors, where their transfer can reshape competitive dynamics across borders.

- Tangible assets (such as factories, infrastructure, or land) are location-bound and generally less sensitive from a competition or sovereignty perspective since they cannot be relocated.

The findings further rest on a structured methodology that combines literature review, data analysis, expert interviews, and case-based evidence, ensuring both breadth and depth in the assessment. An overview of the methodological approach is presented in exhibit 4.

Exhibit 4

Methodology

Methodology

The analysis presented in this report builds on a combination of complementary methods designed to ensure both breadth and depth:

- Literature review

A systematic review of existing international and European research on cross-border mergers and acquisitions was conducted. The review covered empirical studies on the effects of M&A on competition, investment, innovation, and productivity, as well as theoretical frameworks such as the Williamson trade-off and the inverted U-curve relationship between competition and innovation. This step provided the conceptual foundation for the report and ensured that the analysis was grounded in the most relevant academic and policy debates. - Quantitative analysis of market trends

The report draws on data from international sources such as the IMF, OECD, Eurostat, and Mergermarket. These data are used to track long-term developments in market concentration, markups, and productivity across the EU, the US, and the Nordic region. Special attention is given to sectors of strategic importance for the green and digital transitions. Exhibits on markups, investment gaps, and cross-border M&A deal flows illustrate these dynamics. - Expert interviews

To complement desk research, a series of semi-structured interviews was conducted with national experts across all Nordic countries. Interviewees were selected based on their industry knowledge and broad experience with M&A regulation and practice. Each interview lasted 45–60 minutes and was conducted virtually. To ensure openness and confidentiality, no individual names, affiliations, or roles are disclosed. Instead, insights have been anonymised and synthesised at an aggregated level. The interviews provided valuable context on barriers to M&A, enforcement practices, and the broader industrial-policy debate. - Event studies and case-based evidence

The report reviews 14 recent event studies covering Nordic merger cases, as well as sector-specific analyses of healthcare, technology, ICT, and manufacturing. Event studies provide evidence on shareholder value effects of mergers by analysing abnormal stock market returns before and after M&A announcements. These are supplemented by case evidence from sectors such as telecommunications and pharmaceuticals, where M&A has been linked to price effects, innovation impacts, and competition outcomes.