1. The relationship between M&A, productivity, and investment

Exhibit 35

Research question in this chapter

Research question in this chapter

Chapter 1

Do large cross-border merger and acquisition deals in internationally competitive sectors enhance firms’ ability to compete and are they associated with positive firm outcomes (e.g., investment, innovation, and productivity)?

Do large cross-border merger and acquisition deals in internationally competitive sectors enhance firms’ ability to compete and are they associated with positive firm outcomes (e.g., investment, innovation, and productivity)?

This chapter pursues three primary objectives related to firm-level impacts. First, it conducts a comprehensive review of the economic literature on cross-border M&A and examines how it affects the competitive capabilities of firms. Second, it evaluates existing research regarding cross-border M&A’s relevance to key outcomes, such as productivity, investment, and innovation, while highlighting both the advantages and disadvantages of increased market concentration from a corporate/firm perspective. Finally, the chapter analyses academic studies on Nordic mergers, with particular attention to event study methodologies.

1.1 Cross-border M&A and the ability to compete

Q 1.1: Does theory and empirical evidence support that cross-border M&A increase firms’ ability to compete internationally?

While theoretical frameworks suggest that cross-border M&A can enhance international competitiveness through various mechanisms like efficiency gains, knowledge transfer, and market access, empirical evidence presents a mixed picture. The success of cross-border M&A in boosting competitiveness is highly contingent on the specific characteristics of the firms involved (e.g., sector and horizontal/vertical mergers), the nature of the industry, and the broader economic, regulatory, and cultural environments of the countries implicated in the transaction. Table 2 shows highlights from the literature.

Exhibit 36

Definition of horizontal and vertical mergers

Definition of horizontal and vertical mergers

Horizontal M&As occur between competitors in the same industry. These deals often raise competition concerns, as they can reduce market rivalry and enable price increases or output restrictions. Although they may offer efficiency gains, these are sometimes outweighed by anti-competitive risks, making horizontal M&As a key focus for regulators.

Vertical M&As involve firms at different stages of the supply chain. They are typically associated with efficiency improvements – such as lower transaction costs, better coordination, and elimination of double marginalization (Williamson, 1971). Empirical studies (Chipty, 2001; Hortacsu & Syver-son, 2007) generally find that vertical M&As enhance efficiency, though risks like foreclosure - where rivals lose access to critical inputs - remain.

Table 2 Review of literature (cross-border M&A vs. competition)

Theory | Efficiency gains and synergies Mergers can create economies of scale, foster knowledge sharing, and enable patent-pooling, which may increase efficiency and ultimately benefit consumers. While they may potentially reduce consumer-welfare due to reduced competition, these efficiencies are critical to compensate for any increased market power. These gains can manifest as reduced marginal costs, allowing firms to expand (Affeldt, 2021; IMF 2019; Bajgar 2024). |

Market access Cross-border M&A can provide or ease access to new product markets by leveraging the target firm's existing customer base, marketing expertise, or local market-specific knowledge. This is considered a more important feature for cross-border M&A than for domestic M&A. The ability to scale intangible assets, like innovation and management practices, across borders can be amplified by access to larger global markets (Stiebale, 2025; Bajgar, 2021). | |

Empirical results | Productivity improvement: Numerous studies find that foreign ownership leads to increased total factor productivity of acquired plants over time, often linked to increased investment, employment, and integration into global trade. European establishments acquired by U.S. firms show productivity improvements, consistent with managerial practice spillovers (Ahern, 2025). |

M&A is consistently associated with higher prices in some sectors (indicating lesser competition): The results reviewed indicate consistent results for sectors such as mobile telecommunications, pharmaceuticals (Lear et al. 2024). The adverse effects are most common in the case of horizontal mergers. Market power has increased particularly sharply in the tech sector (IMF, 2021) | |

National champion debate: While some argue for policies to create "national export champions" through less domestic competition to achieve scale for international competitiveness, a survey of EU exporting firms largely contradicts this. Most respondents (85% for quality, 84% for efficiency, 78% for innovation) reported a positive impact of domestic competition on their export performance, and 66% stated domestic competition does not curb their size in a damaging way. This suggests that domestic rivalry spurs efficiency and innovation, better equipping firms for international markets (Lear et al., 2024). |

Source: HBS Economics

Exhibit 37

Take-aways

Take-aways

Numerous studies find that foreign ownership leads to increased total factor productivity of acquired manufacturing plants over time, often linked to increased investment, employment, and integration into global trade. European firms acquired by U.S. firms show productivity improvements, consistent with managerial practice spillovers.

For sectors such as digital-intensive (tech) and pharmaceuticals empirical studies indicate that the effects of cross-border M&A on competitiveness are complex and vary by sector. For instance, in sectors such as mobile telecommunications, increased concentration resulting from M&A is associated with higher prices in markets characterized by limited competition. It is also reported that horizontal mergers are likely to more severely impact competition.

Survey results contradict the idea of creating national champion (a leading domestic firm) by shielding it from domestic competition (e.g., respondents say domestic competition positively impact export performance).

1.2 Cross-border M&A and economic outcomes

Q 1.2: Does theory and empirical evidence support that cross-border M&A increase firms’ investments, productivity, and innovative ability?

Innovation

Economic theory has long debated how market competition affects firms’ incentives to innovate. Two classic perspectives dominate this discussion. Joseph Schumpeter argued that firms with market power – such as monopolies – are motivated to innovate to maintain and strengthen their position and to deter potential entrants. In concentrated markets, high profits can be reinvested into R&D, giving incumbents (i.e., established firms) the resources to innovate.

By contrast, Kenneth Arrow emphasized that in competitive markets, firms innovate to “escape” competition – e.g., by introducing new products or processes, a firm can gain a temporary advantage over rivals. In this view, a monopoly not threatened by competitors has less incentive to innovate.

These two perspectives imply that the relationship between competition and innovation is not straightforward. Competition policy plays a key role in shaping it, primarily by removing barriers to entry and opening access to markets and preventing anticompetitive behaviour.

Greater market access increases the size of the addressable market for firms, allowing fixed R&D costs to be spread over more units, which strengthens the incentive to innovate (Griffith, 2021). Opening markets also allows new players to enter with alternative or more efficient business models, forcing incumbents to respond. In this way, competition can act as a lever for forward-looking, risk-taking firms, paving the way for new ideas, formats, and production processes that foster growth. By contrast, protectionist measures tend to limit market size, reduce competitive pressure, and slow the pace of innovation.

A well-functioning market should therefore aim not only for static efficiency – an optimal allocation of resources at a given point in time – but also for dynamic efficiency, which involves sustaining innovation, enabling the entry of new firms, and creating entirely new markets (Aghion, Cohen, and Pisani-Ferry, 2006).

The precise effect of competition on innovation also depends on a firm’s position relative to the technological frontier. In sectors dominated by a leading innovator, firms far behind the frontier may not be encouraged to innovate, as the investment required to catch up is high relative to the potential reward. By contrast, when firms are technologically similar, stronger competition reduces profits and increases the “escape competition” effect, prompting them to innovate in order to differentiate themselves, gain market share, and potentially become the leader.

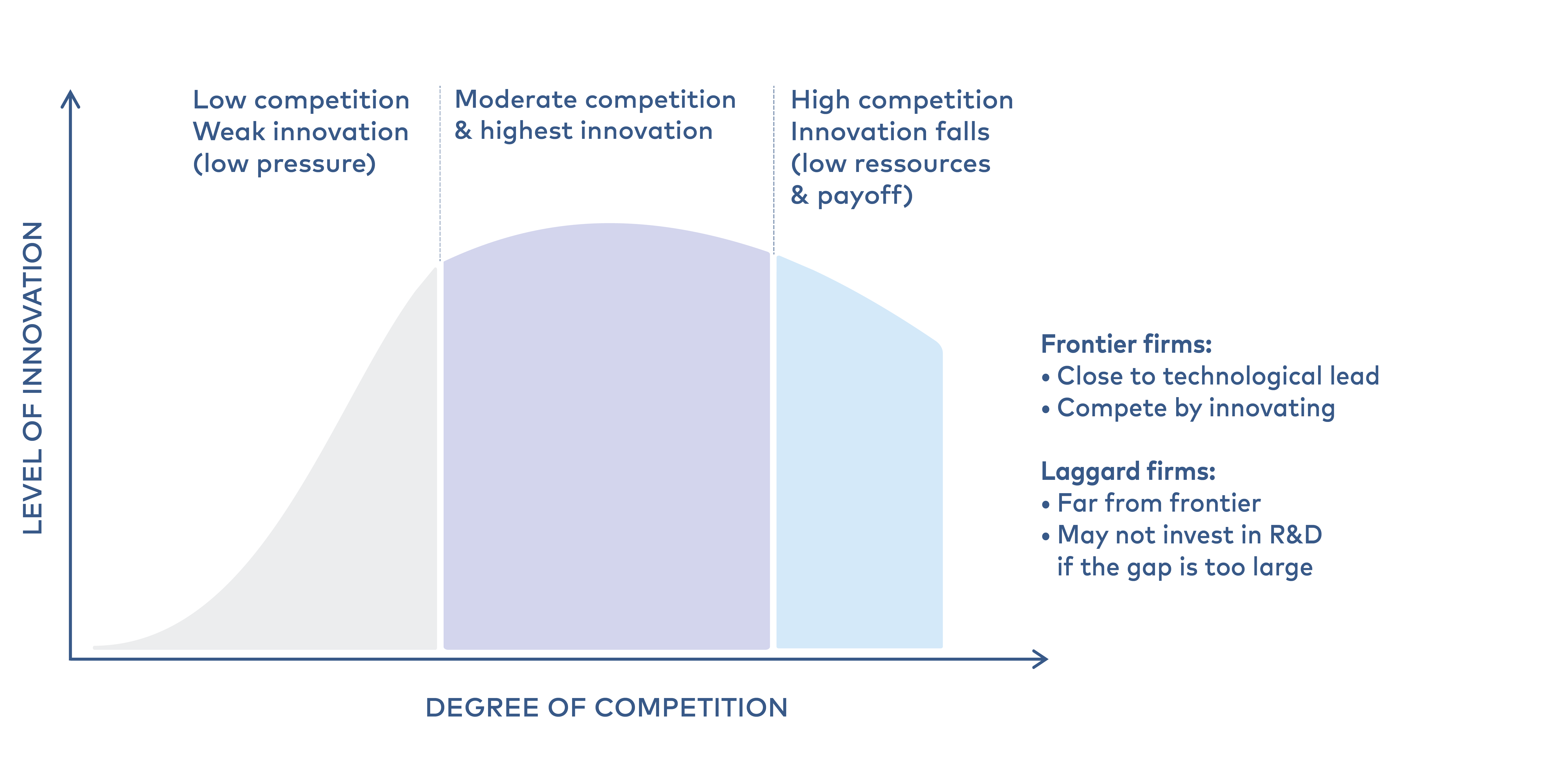

Philippe Aghion (2005) integrated these into a single framework, demonstrating an inverted U-shaped relationship between competition and innovation. Innovation activity and competition intensity rise together up to a certain threshold, after which stronger competition begins to reduce innovation. In simple terms: with little competition, firms feel no urgency to improve; with moderate competition, innovation peaks as firms race to get ahead; and with very high competition, shrinking profits limit resources and incentives for R&D.

Exhibit 38 Inverted U-shape of competition and innovation

Illustration Aghion et al (2005) – dark green zone maximize innovation by the “escape competition effect”

Illustration Aghion et al (2005) – dark green zone maximize innovation by the “escape competition effect”

Source: HBS Economics own illustrations based on Aghion et al. (2005).

Is competition good or bad for innovation and growth?

A timeline of economic ideas

The relationship between innovation and competition have major implications for competition policy, especially in how regulators balance market power and innovation incentives:

Rethinking the role of market power - Traditional view: Market power is bad—monopolies reduce output, raise prices, and harm consumers.

- Modern view (Aghion et al.): Some degree of market power can encourage innovation, especially when firms are trying to “escape competition” by innovating.

- Policy implication: Strict enforcement of antitrust policies might undermine innovation if it reduces the incentives for firms to invest in R&D.

Optimal competition is not maximum competition - The inverted U-shape suggests that:

- Too little competition → firms are complacent.

- Too much competition → firms fear they won’t recoup R&D costs.

- Policy implication: Regulators should aim for a “Goldilocks zone” of competition – not too little, not too much – to maximize innovation.

Sector-specific competition policy - The relationship between competition and innovation varies by industry:

- In pharmaceuticals, strong IP rights and some market power may be necessary.

- In tech, rapid innovation may occur even under intense competition.

- Policy implication: Competition policy should be tailored to industry dynamics, not one-size-fits-all.

Dynamic vs. static efficiency - Traditional antitrust focuses on static efficiency (prices, output). Whereas newer empirical work emphasizes dynamic efficiency – how competition affects long-term innovation and growth.

- Policy implication: Regulators should consider long-run innovation effects, not just short-run consumer prices.

Timeline (paradigms): | |||

1940s | 1960s | 1990s | 2005– |

Innovation is enhanced by monopoly power. Competition may actually reduce innovation by undercutting profits needed for R&D. | Competition fosters innovation by creating incentives for firms to outperform rivals and capture rents and market shares. | Growth is endogenous, and innovation is an economic engine, not an exogenous shock. | Moderate competition is optimal for innovation. Both too little and too much competition can stifle innovation. |

Joseph Schumpeter | Kenneth Arrow | Paul Romer | Philippe Aghion |

Key work: Capitalism, Socialism and Democracy (1942) | Key work: Economic Welfare and the Allocation of Resources for Invention (1962) | Key work: Endogenous Technological Change (1990) | Key work: Competition and Innovation: An Inverted-U Relationship (2005) |

Contribution: Introduced “creative destruction” – innovation by entrepreneurs destroys old industries and creates new ones. | Contribution: Explained why competitive markets may underinvest in innovation – knowledge spreads too easily to capture full profits. | Contribution: Built models where innovation drives long-run economic growth through investment in knowledge. | Contribution: Found that too little or too much competition can hurt innovation – the best results come with moderate rivalry. |

In the European Union, cross-border M&A correlates with diminished innovation output (e.g., fewer patent applications) in target countries but enhances innovation in acquirer countries (Stiebale, 2025). Studies on M&A and innovation remain mixed, though most indicate adverse effects (Lear et al. 2024).

One example is Haucap et al. (2019) who examines 65 mergers between pharmaceutical firms reviewed by the European Commission between 1991 and 2007. They find that, overall, mergers reduced innovation among the merging firms compared to non-merging peers. Using a difference-in-differences approach, the authors estimate the average impact of mergers on patent applications and show that, consistent with their theoretical predictions, horizontal mergers negatively affect innovative activity three years after the merger, with the effect becoming even larger after four years.

Table 3 Review of literature (cross-border M&A vs. innovation)

Theory | Knowledge and technology transfer: Firms can acquire the target firm's knowledge-based resources, including non-replicable and invisible tacit knowledge, to expand their knowledge base and achieve secondary innovations. This can lead to R&D synergies and reduced R&D costs. Highly mobile knowledge capital from the acquirer can be complemented by local immobile knowledge of the foreign target (Ahern, 2025; Yu Zhang, 2018). |

Effects on consumer surplus: Horizontal mergers typically leads to a decrease in consumer surplus if i) firms compete in a single market, ii) costs of additional R&D is not increasing too rapidly and iii) there are no spillovers to R&D. | |

Empirical results | Mixed effects: The relationship between M&A and corporate innovation is a prominent topic but lacks unanimous agreement on a consistently favourable impact (Wang, 2025). |

Positive for acquirers, negative for targets (innovation): Cross-border M&A is, on average, associated with an increase in innovation (patents) in the acquirer's country (around 9% increase) but a decline in innovation in the target's country (around 4% decrease). This suggests that R&D activities may be relocated to the technologically more advanced firm (often the acquirer), (Stiebale, 2025). | |

Negative for targets (specific contexts): Some studies, particularly focusing on horizontal mergers or the pharmaceutical industry, report negative effects of mergers on innovation for the merged entity and non-merging competitors (Aleztra, 2024, Haucap, 2019). Non-horizontal mergers may be more beneficial for scale and investment than horizontal ones, which tend to reduce innovation (Stiebale, 2025) | |

Innovation intensity: In research-intensive industries, mergers are more likely to be profitable, but they can also lead to negative effects on innovation for both the merged entity and rivals (Stiebale, 2016) | |

Productivity and knowledge capital: More productive firms, and those with higher intangible knowledge capital (e.g., in technology-intensive industries), are more likely to successfully engage in international expansion and integrate foreign affiliates (Ahern, 2025). The positive relationship between intangible investment (which aids scaling) and concentration is amplified in more globalized and digitally intensive industries, indicating that access to larger markets complements the scale-up potential of intangible capital (Bajgar, 2024). |

Source: HBS Economics

Exhibit 39

Take-aways

Take-aways

We highlight the work of Aghion which implies the existence of a sweet-spot (i.e., a degree of competition to maximize innovation). Innovation could play a larger role in TFP growth going forward as a result of the trends mentioned in Q.2.2.

Empirical results on innovation are mixed; while certain M&A activities enable knowledge transfer, concerns about "killer acquisitions" in e.g., pharmaceuticals highlight potential negative impacts on competition. Recent studies also show that cross-border M&A tends to negatively affect innovation (measured as patents) in the acquired (target) firm and country. This could be used as a myopic argument in favour of protecting Nordic and European research-intensive sectors from foreign acquisition.

Investment

In this section, we turn our attention from innovation to the ways in which cross-border M&A shapes investment behaviour. Drawing on empirical research and theoretical perspectives, we explore how these transactions influence both the allocation and composition of capital – shedding light on when M&A stimulates investment, and when it may restrain it.

Increased market concentration can affect investment through several channels. One is that dominant firms may restrict output and raise prices rather than invest in expanding capacity, particularly when competitive pressure is limited (Gutiérrez and Philippon, 2017).

Another mechanism is that only large ‘superstar’ firms have the financial resources, managerial capability, and know-how to make large-scale investments with uncertain payback periods, effectively crowding out investment by smaller, less productive, or new firms (Crouzet and Eberly, 2019). Firm-level data suggests that large firms account for a higher share of investment relative to their output, although the gap has not increased over time (Hanappi, Millot and Turban, 2023).

In reality, the relationship between market power and investment is likely to be nuanced, and firm specific. For example, firms may first achieve market power through innovation and efficiency, gaining scale through network effects and intangible synergies. Over time, however, some may shift their focus from innovation and fixed capital investment toward rent-seeking strategies, such as regulatory capture and lobbying, to preserve their dominant position (Akcigit and Ates, 2021)

Table 4 Review of literature (cross-border M&A vs. investment)

Theory | Larger firms typically invest more: Greater market access increases the size of the addressable market for firms, allowing fixed R&D costs to be spread over more units, which strengthens the incentive to invest and innovate (Griffith, 2021). |

Increased market concentration may decrease incentives to invest based on the theoretical ideas of Arrow (previous section). | |

Shorter geographic distance and higher trade flows increase the likelihood of cross-border mergers, consistent with easier monitoring and cultural familiarity, which can facilitate investment (Ahern, 2025). Larger cultural differences can impede post-merger integration and reduce the likelihood of cross-border M&A. | |

Empirical results | Negative relationship with concentration: Empirical analysis suggests a negative relationship between market concentration and investment, particularly in sectors like mobile telecommunications. A rise in the number of mobile network operators (MNOs) is positively associated with country-level investment (e.g., a 10% increase in CAPEX). This implies that mergers reducing the number of operators (increasing concentration) may reduce investment (Lear et al. 2024; Stiebale, 2025). |

Impact of markups: Higher markups, often resulting from M&As and increased market power, are associated with somewhat lower physical capital investment. For instance, a 10-percentage point increase in a firm's markup is linked to a 0.6 percentage point decrease in its physical capital investment rate, with a larger effect (2 percentage points) for top decile firms (IMF, 2019). | |

Shorter geographic distance and higher trade flows increase the likelihood of cross-border mergers, consistent with easier monitoring and cultural familiarity, which can facilitate investment (Ahern, 2025). |

Source: HBS Economics

Exhibit 40

Take-aways

Take-aways

Greater market access theoretically allows firms to spread fixed costs (e.g., R&D), which strengthens incentives to invest. Based on existing literature, however, we mainly find a negative relationship between market concentration and investment (e.g., in ICT). According to IMF higher firm-level markups are associated with lower investment (increasingly for larger firms). In sectors with high levels of international competition however, increasing concentration is less likely to translate into elevated markups. In these cases, impacts on innovation is of high importance.

Productivity

More productive firms frequently seek to expand internationally through M&A, leveraging their competitive advantages and transferring key capabilities – including managerial expertise and intangible knowledge capital – to foreign affiliates. At the same time, firms with less established competitive strengths may pursue acquisitions to access new markets, technologies, or management practices. This section investigates the possible productivity effects of M&A, considering how these transactions can drive efficiency gains, knowledge transfers, and broader changes within target and acquiring firms alike. By examining empirical evidence and theoretical insights, we aim to clarify under what circumstances cross-border M&A can enhance or hinder productivity growth.

Table 5 Review of literature (cross-border M&A vs. productivity)

Theory | Knowledge transfer and efficiency gains: M&A can facilitate the transfer of intangible knowledge capital, such as management practices, technology, and R&D capabilities, from more productive acquirers to less productive target firms. This transfer can lead to improved efficiency, expanded knowledge bases, R&D synergies, and a reduction in R&D costs, fostering secondary innovations and potentially enhancing the target firm's productivity. Firms with high mobile knowledge may acquire foreign firms to complement their mobile knowledge with local immobile knowledge (Zu Zhang, 2024; Ahern, 2025). |

Alleviation of financial constraints: Foreign acquirers from countries with stronger investor protection can improve the governance practices of target firms, which can lead to greater investor confidence and improved access to financing, thereby alleviating financial constraints in the host country and potentially boosting productivity (Ahern, 2025) | |

Empirical results | Productivity boost for target firms: Studies have found that foreign ownership leads to a significant increase in the total factor productivity (TFP) of acquired manufacturing plants (e.g., a 13.5% increase in Indonesian plants over three years, linked to increased investment, employment, and trade integration). Acquired European establishments by U.S. firms also show productivity improvements, consistent with the spillover of managerial practices (Javorcik, 2009). |

Relocation of R&D and innovation: Cross-border M&A is associated with an increase in innovation in the acquirer's country (around 9%) but a decline in innovation in the target's country (around 4%). This suggests that R&D activities may be relocated to the technologically more advanced firm, which is often the acquirer. This relocation can lead to substantial declines exceeding 10% for target firms five years after M&A. Some studies even estimate negative productivity effects for EU acquisition targets. |

Source: HBS Economics

Exhibit 41

Take-aways

Take-aways

Evidence is scarce but consistent with productivity boosts in target firms in manufacturing plants possibly owing to managerial spillover effects. Results also indicate adverse effect on R&D in target firms possibly slowing productivity in some sectors (e.g., technology and pharmaceuticals).

1.3 Evidence from Nordic market consolidation

Micro-level evidence from Denmark

A study by Bandick and Koch (2023) investigates the causal treatment effects of domestic and foreign acquisitions on plant survival, employment (growth), and the skill composition within acquired plants in Danish manufacturing and service sectors during 2002–2015. This research provides micro-level evidence within a Nordic context. The study reveals distinct impacts depending on whether the acquisition is domestic or foreign (cross-border):

- For domestic targets, the results indicate positive effects on plant survival, employment (growth), and the skill intensity within plants following an acquisition.

- For foreign targets, the study finds no robust evidence of any significant change in employment (growth) or the survival probability.

- These findings are confirmed to be robust across different methods and various sub-samples.

Exhibit 42

Context and methodology (Bandick and Koch, 2023)

Context and methodology (Bandick and Koch, 2023)

The research focuses on Danish manufacturing and service sectors during the period 2002–2015. This provides micro-level evidence within a Nordic context. To establish causal effects, the authors employ a detailed and unique dataset that combines plant-, firm-, and industry-level information.

- A key aspect of their methodology is controlling for the non-random selection of acquisition targets, which is differentiated for domestic and foreign acquirers

- They achieve this by combining a difference-in-differences approach with a propensity score weighting estimator

- The study also uses a matching approach, linking foreign-acquired firms to similar domestic-acquired firms, to help isolate the "foreign" component of acquisitions

Broader European evidence including Nordic countries

- Acquiring firms tend to increase markups after mergers and acquisitions (IMF, 2019). However, it remains unclear whether consumer losses from higher prices are offset by cost savings or other efficiencies, and this question needs further study.

- Lear et al. (2024) found that in the EU mobile telecommunications sector, higher market concentration leads to higher prices. Specifically, a 1,000-point rise in the Herfindahl-Hirschman Index increases prices by 11–18% across countries with three or four major network operators.

- Pharmaceuticals: In this sector, market power is associated with intellectual property protections. There are ongoing discussions about "patent thickets" and "killer acquisitions," where companies acquire patents or firms and choose not to commercialize them, leading to reduced competition.

Q 1.3: Is there evidence from market consolidation in Nordic sectors important for technology? (consumer harm and innovation etc.)

For the question regarding experiences from Nordic merger cases evidence is scarcer (see above). The following section uses event studies from specific merger cases in which one or more Nordic firms were involved. In general, the event-studies measure returns using stock price changes before and after the mergers to assess their success. The analysis is based on 14 event studies each investigating many different mergers.

Exhibit 43

Literature search in this section (selection of event studies)

Literature search in this section (selection of event studies)

The following search-query was used in Google Scholar:

"event study" AND (merger OR acquisition OR "M&A" OR takeover) AND (Denmark OR Sweden OR Norway OR Finland OR Iceland OR Nordic OR Scandinavia) AND ("abnormal returns" OR "announcement returns" OR CAR)

The query produced 4,630 results of which the top 20 studies were selected based on their relevance (recency and citations). 14 studies were selected for the review. Each source can be seen from the appendix table in this chapter.

Take-aways from the review of event studies

M&As involving companies in the same industry and at the same stage of the value chain (horizontal mergers) are common strategies to strengthen market position, increase optimization, and enhance efficiency. Generally, horizontal deals are considered "wealth-building" and are more likely to create positive abnormal returns (potentially harming consumers).

While M&A activity is prevalent in both highly competitive and digital sectors across the Nordics, the underlying motivations and the precise nature of shareholder value creation can vary. Digital and tech-intensive sectors emphasize innovation, patents, and new capabilities, often showing positive returns. Highly competitive sectors like banking drive consolidation and scale, with targets consistently benefiting, but acquirer returns can be more ambiguous depending on the specific market conditions and deal characteristics. The studies reviewed in this section are therefore mainly focused on acquirers returns.

Acquirers frequently originate from nations with appreciating currencies and better-performing stock markets relative to targets, suggesting that valuation changes drive economically rational mergers. Geographic proximity and superior accounting disclosure standards in acquirer countries further increase the likelihood of cross-border M&As.

Sector level insights

- The

information technology sector (ICT) is identified as one of the most active sectors for M&A activity in the Nordic region (Andersen, 2018). A Swedish study show that ICT outperformed the Finance, Insurance and Real Estate sector in terms of acquirer return (Bergman, 2018). - M&A in

Healthcare and ICT sectors in the Nordics have historically created the most return to shareholders (of target firms), see exhibit 44. This is in line with evidence from the IMF showing that those sectors have seen the largest increase in markups. - The

telecommunications sector is identified as one of the highly patent-intensive sectors in Scandinavia, where studies have found a positive relationship between patents and abnormal M&A announcement returns for both acquirer and target shareholders (Hisdal, 2021). - Studies indicate that M&As within the

renewable energy and cleantech industries are generally value-adding for acquirers in the short term. - In the Nordic

banking sector , target banks consistently experience significantly positive abnormal returns following M&A announcements

Exhibit 44 High returns on target firms in technology and healthcare (Nordics)

Returns to shareholders of acquired firms

Returns to shareholders of acquired firms

Source: Opsahl (2022). Return is measured as the cumulative abnormal return (CAR) for target firms. Data from 2001–2019.

Exhibit 45

Supported by IMF calculations of global markups

Returns on healthcare and tech is echoed by IMF

Returns on healthcare and tech is echoed by IMF

- Across all ten (one-digit) sectors, the Technology and Healthcare sectors experienced the largest increases in markups between 1995 and 2016.

- Technology and Healthcare saw increased markups of 30–40 percent (cumulative percentage change) compared to 10 percent in consumer goods and industrials.

Source: IMF (2021). Rising corporate market power (IMF staff calculations).

The table below highlights the results from all 14 sources in different dimensions:

The first section of the table shows that general/overall evidence for M&A activities (domestic and cross-border) favours that M&A typically yield statistically significant results in term of acquirer returns in a Nordic context – the literature generally finds consistent results indicating that target returns are positive – which is why we focus primarily on studies about acquirer returns. The second section of the table shows that results indicate higher returns in the case of horizontal deals. The third section highlights some sector-specific results indicating positive returns in most sectors with a few notable exceptions (e.g., banking, insurance, and real estate). The last section indicates that cross-border M&A shows mixed results compared to domestic M&A (using the event study methodology) with some studies indicating a lower return whilst other indicate higher returns in the case of cross-border M&A.

Table 6 Estimates in recent event studies in Nordic countries

Plus/minus show the direction of estimates and (?) indicate insignificant estimates

Plus/minus show the direction of estimates and (?) indicate insignificant estimates

Study | Category/Characteristic | Target return | Acquirer return |

Holmberg 2023 | General/Overall (Nordic) | Not estimated | + |

Andersen 2018 | General/Overall (Nordic) | Not estimated | + |

Furuholm 2022 | General/Overall (Nordic) | Not estimated | + |

Kinnunen 2022 | General/Overall (Nordic) | Not estimated | + |

Lindholm 2020 | General/Overall (Nordic) | Not estimated | + |

Roitto 2017 | General/Overall (Nordic) | Not estimated | +? |

Hisdal 2021 | General/Overall (Scandinavian, incl. patent effect) | + | + |

Kantola 2024 | General/Overall (Nordic, Longer-term +/-10 years) | Not estimated | – |

Kantola 2024 | General/Overall (Nordic, Short-term) | Not estimated | + |

Andersson Edlin 2025 | General/Overall (Swedish acquirers) | Not estimated | + |

Bergman 2018 | General/Overall (Swedish) | Not estimated | + |

Vasko 2023 | General/Overall (Swedish) | Not estimated | + |

Kantola 2024 | Industry Relatedness: Vertical Deals | Not estimated | –? |

Vasko 2023 | Industry Relatedness: Horizontal Deals | Not estimated | + |

Nordbø 2024 | Industry: Banking Sector (Overall) | + | +? |

Bergman 2018 | Industry: Finance, Insurance, Real Estate | Not estimated | +? |

Bergman 2018 | Industry: Manufacturing | Not estimated | + |

Johansson et al 2020 | Industry: Renewable Energy | Not estimated | +? |

Bergman 2018 | Industry: Service | Not estimated | + |

Bergman 2018 | Industry: Transportation, Comm., Electric, Gas, Sanitary | Not estimated | + |

Bergman 2018 | Industry: Wholesale Trade and Retail Trade | Not estimated | + |

Nordbø 2024 | Internationality: Cross-Border (Banking Sector) | Not estimated | – |

Holmberg 2023 | Internationality: Cross-Border Acquisitions | Not estimated | –? |

Kantola 2024 | Internationality: Cross-Border Deals | Not estimated | – |

Andersson Edlin 2025 | Internationality: Cross-Border M&As (Swedish) | Not estimated | + |

Johansson et al 2020 | Internationality: Cross-Border vs Domestic (in Renewable Energy) | Not estimated | +? |

Kantola 2024 | Internationality: Domestic Deals | Not estimated | +? |

Andersson Edlin 2025 | Internationality: Domestic M&As (Swedish) | Not estimated | + |

Bergman 2018 | Internationality: Domestic vs Cross-border | Not estimated | -? |

Andersson Edlin 2025 | Internationality: Cross-Border vs Domestic M&As (Swedish) | Not estimated | + |

Lindholm 2020 | Internationality: Domestic vs Cross-border | Not estimated | + |

Opsahl 2022 | Internationality: Cross-Border vs Local | +? | –? |

Andersen 2018 (Value creation through M&As in a Nordic context), Andersson & Edlin 2025 (Domestic vs. cross-border M&A bidder returns in Sweden), Bergman 2018 (Announcement effect of M&As on short-term performance), Furuholm 2022 (Abnormal acquirer returns in Nordic markets), Hisdal 2021 (Role of patents in Scandinavian M&As), Holmberg 2023 (Merger waves and long-term value for Nordic acquirers), Johansson et al. 2020 (M&As and shareholder value in renewable energy/cleantech), Kantola 2024 (M&A wealth effects in the Nordics), Kinnunen 2022 (Abnormal returns and trading volume in M&As), Lindholm 2020 (Impact of M&As on Nordic acquirers’ financial performance), Nordbø 2024 (M&A announcements in Nordic banking), Opsahl 2022 (Cross-border M&A and shareholder wealth in Europe), Roitto 2017 (Abnormal acquirer returns in Nordic takeovers), Vasko 2023 (Short-term impact of M&A announcements in Sweden).

Exhibit 46

Take-aways: Nordic experiences

Take-aways: Nordic experiences

Results are mixed; however, the literature suggests that horizontal mergers in sectors such as Healthcare, Technology, ICT and Pharmaceuticals are typically profitable for investors and might damage innovation in target countries and potentially increase consumers prices.

Conversely, micro-level evidence from the manufacturing sector in Denmark show that domestic target firms show increased probability of survival and higher employment growth.

A European study (including Nordics) in the Mobile telecom sector show that higher market concentration (mergers) is highly associated with higher consumer prices (Lear et al 2024).

Evidence specific to Nordic countries is limited and we primarily rely on 14 event studies. We show that M&A (domestic and cross border) is typically associated with relatively high returns on target firm (the return for shareholder with shares in the target firm). For acquiring firms, evidence is more mixed with studies indicating both positive and negative effects of cross-border M&A compared to domestic transactions. Gains are typically larger for horizontal mergers and in the healthcare and technology sectors. What this implies is that these deals increase profitability, potentially as a result of less competition.