2. Is more cross-border M&A desirable in the Nordics?

Exhibit 47

Research question in this chapter

Research question in this chapter

Chapter 2

Is more cross-border M&A activity desirable in sectors important for the green and digital transition from an economic Nordic perspective? What is preventing more cross-border mergers from taking place?

Is more cross-border M&A activity desirable in sectors important for the green and digital transition from an economic Nordic perspective? What is preventing more cross-border mergers from taking place?

In the previous chapter we argued that there’s a positive relationship between M&A and positive firm outcomes in many cases, while there are also several sector specific examples of insignificant effects and potential harmful effects (innovation/investment). This chapter highlights some of the negative spillovers (like price-effects/consumer harm) and the role of the EU competition authorities as well as barriers to cross-border M&A.

2.1 Spillover effects and consumer harm

Q 2.1: What does the empirical evidence say about the spillover effects on consumer prices and competitive pressure?

Several empirical studies have examined the price effects of mergers across different industries. In retail food and home appliances, mergers were found to raise prices by 3–5 pct. (Allain et al. 2017; Ashenfelter 2013). In banking, the loss of a competitor increased average interest rates by around 6 basis points (Allen et al. 2013). Similarly, in health insurance, Dafny et al. (2012) found that a merger was associated with a premium increase of about 7 percentage points.

Other studies highlight more sector-specific dynamics. In beer markets, a rise in concentration raised prices by 2 pct., though most of this effect was offset by efficiency gains (Ashenfelter et al. 2015). Telecommunications appear particularly sensitive, with Genakos et al. (2018) showing that a 10 percentage-point rise in market concentration increased prices by 20 percent. Petrol markets, by contrast, showed only modest effects, with vertical mergers linked to small price increases of 0.15–0.45 cents per litre (Houde 2012).

The results on consumer price changes are presented in table 8.

- Supermarket industry: A merger analysed led to a significant post-merger price increase of 1.8 pct. to 2.4 pct. at rival stores in affected areas, and a 4% to 5% increase in the prices of the merging firms Allain et Al. (2017).

- Mobile Telecommunications Industry (OECD countries): Genakos et al. (2018) determined that, on average, a 10-percentage point increase in the Herfindahl-Hirschman Index (HHI) leads to a 20% price increase.

- Various industries (rival markups): Stiebale and Szuecs (2022) suggested that higher concentration, resulting from mergers, can enable higher markups for non-merging rival firms, which generally indicates higher prices relative to marginal costs.

Table 8 Results on price-effects by industries (Lear et al. 2024)

Overview of results from different papers

Overview of results from different papers

Paper | AREA | Results |

Allain et al. (2017) | Retail food | Prices increased between 4% and 5% after a merger. |

Allen et al. (2013) | Banks | The loss of a competitor led to an increase in the average interest rate of 6 basis points. |

Ashenfelter (2013) | Home appliances | Prices increased between 3% and 4% after merger. |

Ashenfelter et al. (2015) | Beer | The increase in concentration (average increase of 358 HHI points) led to a price increase of 2%, which was offset by efficiencies (1.8%). |

Dafny et al. (2012) | Health insurance | The merger was associated with a premium increase of approximately 7-percantage points. |

Genakos et al. (2018) | Telecommunications | 10-percentage point increase in HHI leads to a price increase of 20%. |

Houde (2012) | Petrol | Prices increased between 0.15 and 0.45 cents pr. litre after vertical mergers, or at most a 0.7% price increase. |

Hovhannisyan et al. (2019) | Retail food | 5% increase in HHI would lead to an 18% increase in prices. |

Lopez et al. (2002) | Food-processing industries | 1% increase in HHI can lead to a price increase between 1%–6%. |

Matsa (2011) | Retail food | Inventory shortfalls decreased by up to 24% after Wal-Mart entry |

Russell (2021) | Education | Tuitions and fees increased by at least 7% after merger. |

Stiebale and Szuecs | 132 different 4-digit NACE industries | Mergers and acquisitions (M&A) can increase the markups of rival firms between 2% and 4%. |

Exhibit

Take-aways: On sector-specific spill-over effects

Take-aways: On sector-specific spill-over effects

Overall, the evidence suggests that mergers tend to raise prices across many industries, though the magnitude varies considerably by sector. While some markets, such as telecommunications and health insurance, show large and persistent price effects, others, like petrol or beer, display more limited impacts due to efficiency gains or modest concentration changes. This underlines the importance of sector-specific assessments in merger control.

2.2 Is EU merger policy too strict?

European Union merger policy lies at the intersection between market facilitation and regulatory oversight, shaping the landscape for cross-border transactions. While harmonized rules and liberalization efforts can spur mergers and acquisitions, strict antitrust enforcement and foreign investment barriers act as counterweights. As we consider whether the EU's approach is too strict or too lenient, it is essential to weigh both the regulatory intent and the practical outcomes observed.

Q 2.2: Is EU merger policy too strict or too lenient?

The European Union provides a unified framework for merger control through the EU Merger Regulation (EUMR), which applies when mergers meet specific EU-wide turnover thresholds and are deemed to have a "Community dimension." When a merger qualifies under these thresholds, it falls under the exclusive jurisdiction of the European Commission (EC), which has the authority to review, approve, or prohibit the transaction before it can be completed.

While all Nordic NCAs follow broadly similar procedural steps – notification, investigation, decision, and enforcement – their legal powers and tools differ significantly. Denmark, Iceland, and Norway can prohibit mergers directly through administrative decisions, while Sweden and Finland must pursue such actions through the courts, which may slow or complicate interventions.

Exhibit 48

When does the EU review mergers?

When does the EU review mergers?

In principle, the Commission only examines larger mergers with an EU dimension that reach certain turnover thresholds:

Option 1: Simple big deal test

A merger is reviewed if:

A merger is reviewed if:

- Combined global turnover of all merging firms is over €5,000 million, and

- Each of at least two firms has EU turnover of over 250 million.

Option 2: Complex EU-wide test

A merger is reviewed if:

A merger is reviewed if:

- Combined global turnover of all merging firms is over €2,500 million, and

- Together, they make over €100 million in each of at least 3 EU countries, and

- In each of those 3 countries, at least two firms each make over €25 million, and

- At least two firms each make over €100 million in the EU overall.

Exception:

Even if the thresholds are met, the merger won’t be reviewed by the EU if each firm earns more than two-thirds of its EU turnover in the same country.

Even if the thresholds are met, the merger won’t be reviewed by the EU if each firm earns more than two-thirds of its EU turnover in the same country.

Source: EU Commission’s Factsheet on Merger Control Procedures

Exhibit 49

In 2021 EU blocked the acquisition of a below threshold company

In 2021 EU blocked the acquisition of a below threshold company

The European Commission has updated how it interprets Article 22 of Regulation No 139/2004 for merger control. Now, national competition authorities can refer cases that might harm competition, even if these cases do not meet their usual size requirements (the thresholds mentioned above). This means deals involving valuable, innovative companies can be checked sooner, even if those companies are new and don't have much turnover.

In 2021, France used this new rule for the first time by referring Illumina’s plan to buy Grail – a company that works on early cancer detection using genomic sequencing – to the European Commission.

After reviewing the deal, the Commission decided that buying Grail could hurt other companies in the field. On September 6th, 2022, they blocked the acquisition. This case shows how the new referral process helps keep competition fair by catching risky deals that would not have been reviewed before (OECD, link).

Source: OECD

2.3 Competition policy and enforcement

Understanding the distinction between the creation of competition policy – shaped by lawmakers – and its enforcement is essential for grasping how the EU and its member states uphold fair markets. At both the European and national levels, legislative authorities set the framework for competition rules, while enforcement bodies interpret and apply those rules in practice. The table below highlights major differences in legal foundations, procedural steps, and the consequences of merger reviews, underscoring why a clear separation between policy-making and enforcement is crucial for effective and consistent competition oversight.

EU Level | National Level (Nordic countries) | ||

Legal | Legislative authority |

|

|

Key legal basis |

|

| |

Primary enforcement body | European Commission – DG COMP (Directorate-General for Competition) | National Competition Authorities (NCAs) | |

Scope of enforcement |

|

| |

Procedure | Notification requirement |

|

|

Simplified procedure |

|

| |

Phase I review |

|

| |

Phase II investigation |

|

| |

Outcomes | Possible outcomes |

|

|

Example |

|

|

Exhibit 50

Toolbox of the EU competition authorities (DG COMP)

Toolbox of the EU competition authorities (DG COMP)

The following information on the EU level procedures is based on the description in a report by The Danish Competition and Consumer Authority (2021):

Mixed-methods assessment: Quantitative economic analysis is a valuable component in EU merger reviews, but it does not solely determine whether a merger will significantly impede effective competition. Every merger investigation involves an overall assessment and balancing of all qualitative and quantitative evidence.

Market definition: This is a crucial initial step, often based on a tentative market definition in Phase I, evolving into a more elaborate assessment in Phase II through extensive market surveys.

Concentration measures (HHI): Assessments are established in evaluating the merger's impact on market shares and the Herfindahl-Hirschman Index (HHI)

Critical loss analysis (CLA): Used to support qualitative evidence, sometimes in two-sided market versions

Indicators for unilateral effects:

- Upward pricing pressure (UPP): Measures the incentive for the merged firm to raise prices.

- Compensating marginal cost requirements (CMCR): Calculates the critical level of efficiency gains needed to prevent a merger from harming consumers by keeping post-merger prices and aggregate production the same as pre-merger.

- Illustrative price rise (IPR): Extended from UPP/CMCR, accounting for more complex interactions.

Full simulation of mergers: This is the most advanced method, effectively an IPR extended to the whole market, incorporating competitor responses and the merged firm's reactions. Simulation results depend on calibrated or econometrically estimated parameters like price elasticities and diversion ratios.

In conclusion, the tools and review process applied by DG COMP are generally appropriate and incorporate several beneficial and flexible elements. At the same time, we note that long-term effects on innovation could play a more prominent role in merger assessment as these aspects are not systematically considered today. We also note that event studies (assessments of pre/post stock price changes as we analysed in section 1.3) are not currently used in merger reviews by the EU. This type of analysis should perhaps play a larger role in the reviews themselves and the evaluation of previously approved cases.

It is important to note that only a very small share of mergers are either blocked or cleared subject to remedies. In recent years, remedies have applied to around 2–3 pct. of notified EU cases, while outright prohibitions have affected fewer than 0.5 pct. Since 2004, only about 0.7 pct. of all notified mergers have been blocked or withdrawn following an investigation. This should not be interpreted as weak enforcement. Merger control also has a deterrent effect, influencing firms’ behaviour before a transaction is even notified, as we highlight in the following chapter.

2.4 Deterrence effects of competition policy

The primary method for estimating the deterrent effects of cartel, antitrust, and merger control policies is through surveys of companies and legal advisors. These surveys ask how many anticompetitive mergers or agreements were abandoned or changed due to competition law. However, past surveys have often suffered from small sample sizes (grey bars) and are not very recent, covering only a few European countries since 2010–2011. Despite these limitations, survey results provide a rough estimate of the wider impact. Exhibit 51 indicates that each blocked or remedied merger deters 3 to 7 additional mergers (5 on average).

Exhibit 51 Survey studies indicate that 5 mergers are deterred for every merger blocked

Number of mergers abandoned or modified for every merger blocked/remedied

Number of mergers abandoned or modified for every merger blocked/remedied

Source: Dierx et al. (2022). Green bars indicate the highest-quality survey studies on deterrence based on the sample size.

Unlike in the EU, where several survey-based studies estimate how many mergers are deterred for each blocked or remedied merger, no comparable survey evidence was found for the United States.

Instead, U.S. evidence is based on empirical analyses. Clougherty and Seldeslachts (2013) find that merger enforcement leads to a 21% reduction in subsequent merger attempts within the affected industries. In a broader cross-country study including the U.S., Seldeslachts, Clougherty and Barros (2009) estimate that each prohibition may deter up to 34 future merger filings.

Yet it is important to recognize that the true deterrence effect of competition policy may be considerably greater than survey figures suggest. Interviews with national experts highlighted a widespread reluctance to disclose information about abandoned or altered transactions among those tasked with managing complex mergers (typically law firms). This stems from concerns over confidentiality, reputational risk, and potential regulatory scrutiny. As a result, many cases where merger plans are quietly shelved or substantially revised in anticipation of competition authority intervention remain undocumented and unreported in survey responses. Consequently, the estimates based on available survey data are likely to understate the actual scale of deterrence, capturing only a fraction of the potential mergers affected by enforcement.

In conclusion, while the evidence is based on different methods, the overall picture is broadly similar: merger enforcement has a measurable deterrent effect in both the EU and the U.S. However, methodological differences make direct comparisons difficult, and the amount of deterrence is likely to be underestimated in surveys more generally.

EU level barriers

Regulatory scrutiny and deal timelines:

When firms engage in a merger, regulators may interfere with a review process of the merge. The duration and complexity of regulatory reviews significantly influence M&A activities as lengthy review periods can introduce uncertainty and increase transaction costs, potentially deterring companies from pursuing M&A. For example, the European Commission's merger control procedures, while thorough, can be time-consuming, affecting deal timelines (EU merger control procedures, 2021; Bain, 2024).

Un-intended distortion of regulation:

Regulatory frameworks can unintentionally distort market dynamics by affecting firms differently based on their size and resources. Larger firms are often better equipped to handle complex compliance requirements, while smaller firms may find such obligations disproportionately burdensome (Fich, Griffen, & Kalmenovitz, 2023). This asymmetry can influence competitive conditions and create unintended incentives for which type of firms are involved in cross-border M&A. A relevant example is the Corporate Sustainability Reporting Directive (CSRD), an EU regulation designed to standardize and enhance corporate sustainability reporting. It mandates detailed disclosures on environmental, social, and governance (ESG) matters to improve transparency for stakeholders. CSRD exemplifies this trend, with national laws similarly adding complexity that could discourage scaling.

Assessments of long-term innovation effects in merger policy:

We have argued that EU merger reviews could benefit from integrating long-term effects on innovation in merger assessments. As of now innovation can be part of merging parties’ efficiency defence, but only to the extent that the merging parties can demonstrate how the merger will have immediate positive effects on innovation. Authorities’ reviews of mergers are thus somewhat “static” which could introduce a status quo bias in a rapidly changing technological landscape. In this sense it might be useful to be able to consider relatively probable (likely) technological breakthroughs using e.g., technology readiness levels (TRL) in important areas. Another way to approach this would be to consider different scenarios for technology in the relevant market (or competing markets) on a 5–10 year horizon. For example, the effects of a merger between two traditional car manufacturing firms (gas) might have fewer adverse effects if electric vehicles is just about to “break through”.

Exhibit 52

Take-aways: Is EU merger policy too strict?

Take-aways: Is EU merger policy too strict?

Our analysis suggests that, at the EU level, the policy stance seems well balanced overall – both in terms of enforcement and policy.

We briefly describe the tools and merger review process in the case of the DG COMP. We argue that these tools are appropriate and has a many beneficial flexible elements built in. We highlight that long-term effects on innovation could perhaps play a larger role in the review process (i.e., as part of efficiency defence) – these are currently not considered.

We find that very few cases are subject to remedies in EU merger cases - however, around five mergers are deterred for every case rejected. This leads to the conclusion that enforcement is not overly tight. In fact, evidence shown in the report highlights how approved mergers have in some cases reduced innovation. We therefore emphasize other policy measures to increase productivity and competitiveness as well as barriers to M&A outside of competition policy to be of primary interest to Nordic policymakers (see below).

EU merger policy is currently under review, e.g., due to the Draghi report and secular trends/changes in market structures (digital) as well as geopolitical risk. These trends do warrant a review possibly with extended notions of surplus outside of consumer harm and efficiency gains (e.g., geopolitical, and transitionary) as suggested in the beginning of the report. However, we also show that market concentration and markups have been rising in advanced economies which is an important counter argument to the industrial policy agenda. Competition should remain the core concern of competition policy as opposed to concerns about increasing investment levels or driving economic transitions.

Nordic countries

In the vast majority of mergers in the Nordic countries do not meet the EU thresholds and are therefore handled by national competition authorities (NCAs). Between 2014 and 2019, for example, only 26 mergers involving at least one Nordic party were notified to the European Commission, while thousands of mergers were reviewed at the national level. This highlights that less than 1 pct. of Nordic mergers are typically subject to EU-level scrutiny – underscoring the central role of national authorities in the region.

The scope of the project is, however, mainly concerned with larger incumbent firms (i.e., established firms already active in an international market). Since we are mainly concerned with cross-border M&A these would typically adhere to EU competition policy.

All of the five Nordic countries align their competition policies closely with the EU level, including Norway.

While the EU’s harmonized approach reduces cross-border barriers within the Union, it may not always reflect the specific needs or economic priorities of individual countries, which can create tensions between the need for uniformity in regulatory standards and the desire for greater flexibility to account for local conditions.

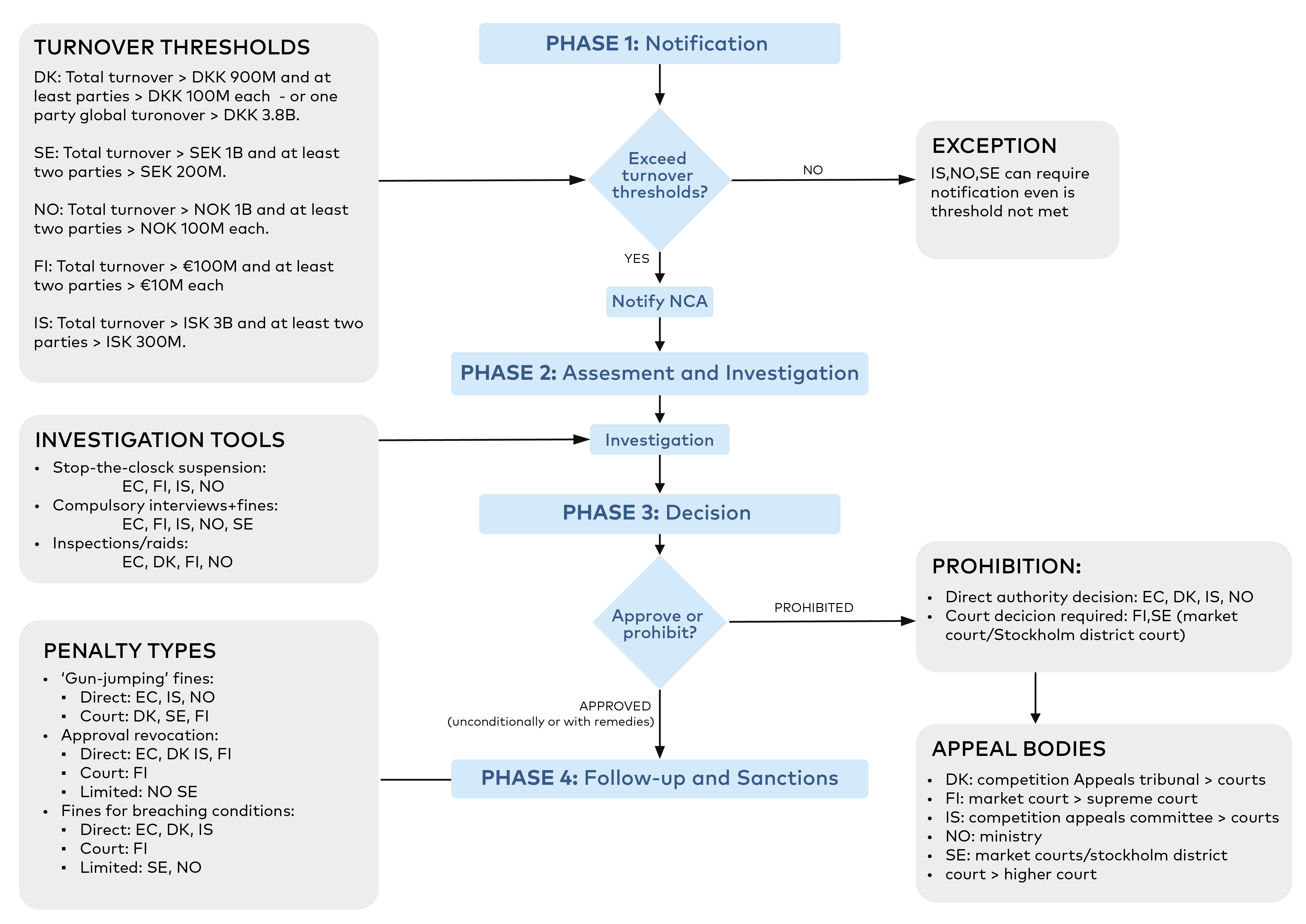

All Nordic NCAs follow a common procedural framework; notification, assessment, decision, follow-up, and appeal, see exhibit 54. Yet, the degree of legal authority and institutional independence varies significantly:

- Denmark, Iceland, and Norway can prohibit mergers directly through administrative decisions. Sweden and Finland, by contrast, must go through the courts to block a merger.

- Only the EC, Iceland, and Norway can impose direct fines for "gun jumping" (i.e., implementing a merger without approval).

- The ability to revoke a merger clearance or enforce conditions also varies, with Sweden and Norway having more limited tools than Denmark or the EC.

Moreover, investigative tools differ across jurisdictions. For example:

- Compulsory interviews and suspension of review timelines are used by some (e.g., EC, Finland, Norway) but not all (e.g., Denmark and Sweden).

- Inspection powers are not uniformly available; Iceland and Sweden have more limited authority in this area.

These differences mean that while the Nordic countries operate within a harmonized EU competition framework, national authorities exercise different degrees of discretion and face varied institutional constraints. This affects not only how M&A cases are reviewed but also how firms plan cross-border transactions.

Exhibit 53 Merger control powers and procedures across Nordic competition authorities

Legal and procedural differences in how national competition authorities (NCA) handle M&A.

Legal and procedural differences in how national competition authorities (NCA) handle M&A.

Note: HBS Economics own illustration.

Source: Based on the report “A Vision for Competition – Competition Policy towards 2020” from the Nordic competition authorities.

The Nordic countries all apply turnover-based thresholds to determine whether a merger must be notified for review. While the overall principles are aligned with the EU Merger Regulation, there are notable differences in the level of thresholds. As shown in table 9, Iceland applies by far the lowest notification threshold among the Nordic countries. This means that transactions of a relatively modest size may be subject to a full merger review in Iceland, whereas the same transaction would fall below the thresholds in Denmark, Sweden, Norway, or Finland.

Such divergence can be interpreted as an example of over-implementation of EU rules, where national legislation goes beyond what is strictly required under the EU framework. From a business perspective, lower thresholds can create additional administrative burdens and compliance costs, particularly for smaller or purely domestic transactions that are unlikely to raise competition concerns. At the same time, stricter thresholds may reflect a policy choice to ensure close scrutiny of market developments in a small and concentrated economy.

Table 9 Thresholds for M&A

Thresholds for M&As in the Nordic countries

Thresholds for M&As in the Nordic countries

Country | Threshold for combined turnover in the country | Minimum turnover per party in the country | Notes |

Denmark | EUR 120 million | EUR 13.4 million each | “Call-in” option: the Danish Competition and Consumer Authority can require notification from 6.7 million EUR. |

Finland | EUR 100 million | EUR 10 million each | Focus on national turnover, not global turnover. |

Iceland | EUR 20 million | EUR 2.1 million each | The Competition Authority can request notification below the threshold. |

Norway | EUR 85 million | EUR 8.9 million each | The Competition Authority can request notification below the threshold. |

Sweden | EUR 90 million | EUR 17.9 million | Notification can also be requested voluntarily or under special circumstances |

Sources: DK; Konkurrenceloven (§12). FI; Kilpailulaki (§ 22). IS: Samkeppnislög (44/2005, §17/18). NO; Konkurranseloven (§18). SE: Konkurrenslagen (4/§6). The table is based on our own conversion of currencies.

Exhibit 54

Case: Low notification thresholds in Iceland

Case: Low notification thresholds in Iceland

- During the interviews one of the national experts from Iceland highlighted that Iceland has a relatively large number of agencies (including sectoral agencies) protecting consumers. Coordinating with different branches may discourage smaller firms form acquiring or merging with Icelandic firms. Combined with the fact that notification thresholds are comparatively low in Iceland this might be a drag on business dynamics and foreign investment.

2.5 Barriers to cross-border M&A

Q 2.3: What barriers prevent nordic Cross-border M&A?

While the Nordic region is generally recognized for its open economies, stable institutions, and high ease of doing business, several barriers may constrain mergers and acquisitions (M&A) activity – particularly cross-border transactions within the region and with external markets.

A central challenge is the limited supply of venture capital relative to market potential, both in the Nordic countries and in the EU more broadly. This restricts early-stage scaling and reduces the pipeline of attractive acquisition targets. Although substantial savings are held in pension funds, insurance companies, and other institutional investment vehicles, these resources are only mobilised for M&A when investors identify profitable opportunities. Delays or the lack of harmonised frameworks for cross-border transactions could mean that many otherwise viable acquisitions do not meet investors’ return expectations.

Policy reforms aimed at reducing frictions in cross-border deals – such as the streamlining of compliance requirements, mutual recognition of regulatory approvals, and alignment of corporate governance rules – would make a greater share of potential transactions profitable. Such measures should therefore be a priority for both policymakers and market participants seeking to strengthen the Nordic capital market’s integration and competitiveness.

Exhibit 55

Cross-border M&A in the Nordics (interview highlights)

Cross-border M&A in the Nordics (interview highlights)

Interviews during the project indicate that national exports highlight that Nordic countries perform strongly relative to their size in innovation and competitiveness. However, cross-border M&A may be constrained by fragmented regulatory frameworks, goldplating of EU rules, and inconsistent enforcement across countries. While the region is attractive for start-ups these regulatory barriers prevent the Nordics from functioning as a unified market in practice.

Fragmentation across the region: Despite frequent external references to “the Nordics” as one block, national markets are in practice highly fragmented. Differences in regulation, enforcement structures, and market thresholds mean that firms do not perceive the Nordics as a single integrated market. This creates frictions for cross-border deals and can reduce potential synergies.

Goldplating as a structural barrier: A recurring challenge is the over-implementation of EU legislation (“goldplating”), which can be more restrictive than EU requirements and varies across countries. This issue appears particularly pronounced in Iceland where, according to one expert, multiple authorities regulate overlapping areas. Goldplating is considered more problematic than simply having stricter formal rules, as it is less transparent and harder to anticipate.

Differences in legislation vs. enforcement: Stakeholders distinguish clearly between the formal rules (legislation) and the way they are applied (enforcement). In some cases, enforcement practices (e.g., moving cases into lengthy phase-2 merger reviews) create significant delays and uncertainty, effectively freezing smaller firms for extended periods. This drag on transaction timelines directly undermines deal value.

Competition policy challenges: Competition measures, such as market concentration indices (e.g., HHI), do not always reflect the international exposure of Nordic firms as we have previously highlighted. For example, one expert from Iceland noted how salmon producers operate in global markets, yet enforcement is based on national revenue considerations, which may distort assessments of market power and concentration.

Implications for cross-border M&A: Structural fragmentation, goldplating, and varying enforcement practices limit the effectiveness of cross-border M&A in creating a more integrated Nordic market. For firms and investors, the Nordics remain attractive for innovation and start-ups, but regulatory complexity reduces the region’s comparative advantage in terms of scaling.

Examples of barriers particularly relevant in the Nordic might include regulatory differences in competition law enforcement (e.g., thresholds above), taxation discrepancies, labour market regulations, such as varying rules on employee representation in corporate boards and collective bargaining agreements.

Addressing these barriers would not only increase M&A flows within the Nordic region but also enhance the attractiveness of Nordic companies as acquisition targets for investors from outside the region.

Exhibit 56

The role of international standards

The role of international standards

Global standards in fields such as M&As and competition regulations are designed to create uniformity across markets, which can significantly streamline cross-border transactions. These standards reduce the complexity of navigating multiple regulatory frameworks, lowering transaction costs, and facilitating business operations across borders. By ensuring that similar rules apply across various regions, harmonized regulations help firms avoid regulatory discrepancies and inconsistencies, thereby fostering more efficient international business practices.

- Even though national competition regimes in Denmark, Finland, and Sweden align closely with the EU Merger Regulation, the procedural demands vary. For instance, Denmark’s competition authority recently extended the pre-notification phase and typically requires more extensive information than other Nordic authorities (Bird & Bird, 2023)

- Since December 2023, Sweden’s implementation of the EU FDI screening regulation has introduced new stand-alone notification requirements for foreign investments, adding a separate approval layer for certain M&A transactions (CMS, 2024)

- The ECB has warned that fragmented financial systems – with differences in insolvency frameworks, collateral rules, and governance structures complicate cross-border bank mergers in the EU, including the Nordic region.

- National authorities possess expanded investigative powers. Since 2024 the Danish Competition and Consumer Authority (DCCA) can “call in” M&A transactions that fall below normal thresholds -potentially increasing unpredictability and raising costs for deals that would otherwise proceed unchallenged (DLA Piper, 2023).

- While the Nordic countries have an agreement on cooperation in competition cases, procedural differences – such as handling below-threshold mergers and divergent enforcement styles – can delay or deter cross-border transactions (EBR, 2024).

Exhibit 57

Nordic agreement on cooperation between competition authorities

Nordic agreement on cooperation between competition authorities

The Nordic Competition Authorities of Denmark, Finland, Iceland, Norway, and Sweden have enhanced their longstanding cooperation through the Agreement on Cooperation in Competition Cases (2018). This agreement builds upon previous arrangements from 2001 and 2004, enabling a higher level of regional coordination than is available under the European Competition Network.

Notably, it facilitates the exchange of both confidential and non-confidential information in merger and antitrust matters and permits member authorities to carry out inspections on each other’s behalf. These measures promote consistent enforcement of competition laws throughout the region, minimize duplication of efforts, and strengthen mutual trust among the authorities.

These examples illustrate that even within the harmonised economic landscape of the Nordics, barriers remain – from procedural complexity and regulatory discretion to cross-border tax mismatches and digital identity constraints. Addressing such frictions would unlock greater capital deployment, enhance investor confidence, and improve integration across the region.

Exhibit 58

Take-aways on barriers to Nordic cross-border M&A

Take-aways on barriers to Nordic cross-border M&A

Large size cross-border M&A will typically abide by EU rules and EU competition enforcement. However, the potential challengers (new market entrants) are subject to national rules and enforcement policies which typically closely align with the EU. Harmonizing standards (reviews thresholds and processes) in Nordic countries could reduce frictions for firms engaged in M&A with multiple Nordic countries at the same time. Such harmonisation could be a desirable extension of the already well-developed framework of corporation between Nordic countries. Harmonising the merger control rules across the Nordic countries would contribute to a more integrated regional market and make the regulatory environment easier to navigate for foreign investors. Similar thresholds and regulatory standards can potentially make the Nordic region more appealing to foreign investors because it requires less institutional knowledge for individual countries.

We argue however, that these barriers directly linked to competition policy are limited and can be adopted within the existing framework of EU and national competition policy. While addressing this problem it is important that Nordic countries continue to promote investment, growth, and innovation outside of competition policy.