2 Economic instruments to promote circular economy in the textile sector

In this chapter, we move from the general overview of the use of economic instruments into discussing the possible role of economic instruments in the textile sector to promote circular transition. First, the current developments of the sector in the Nordic region are investigated, and then options for economic instruments targeted to the textile sector are discussed.

2.1 The role of the sector in the circular transition

The textile value chain is estimated to account for approximately 10% of the global greenhouse gas emissions (European Parliament, 2020). The textile sector is a major user of fossil-based virgin materials and there is a lot of potential for circularity, and hence reducing the environmental impact of the sector.

Currently, the trend of consuming textiles is going upwards and since year 2000, the amount of used textiles from the EU has tripled from 550,000 tonnes to approximately 1.7 million tonnes in 2019. To add to the effects of overly produced amounts of textiles, textile waste creates environmental and social issues. Textiles used in 2019, were mainly exported from the EU region to Africa (46%) and Asia (41%). Annual export of used textiles from the EU region to non-EU European countries has been constant at a level of 10% throughout the past two decades. Textiles that are not reused or recycled are likely to end up in open landfills (European Environmental Agency, 2023a).

To address the challenges from the increased export of textile waste, the EU Member States agreed in March 2022 on a new strategy on sustainable and circular textiles. The strategy intends to increase sustainability patterns across the global trade of textile waste, thus promoting a circular economy (European Commission, 2022a).

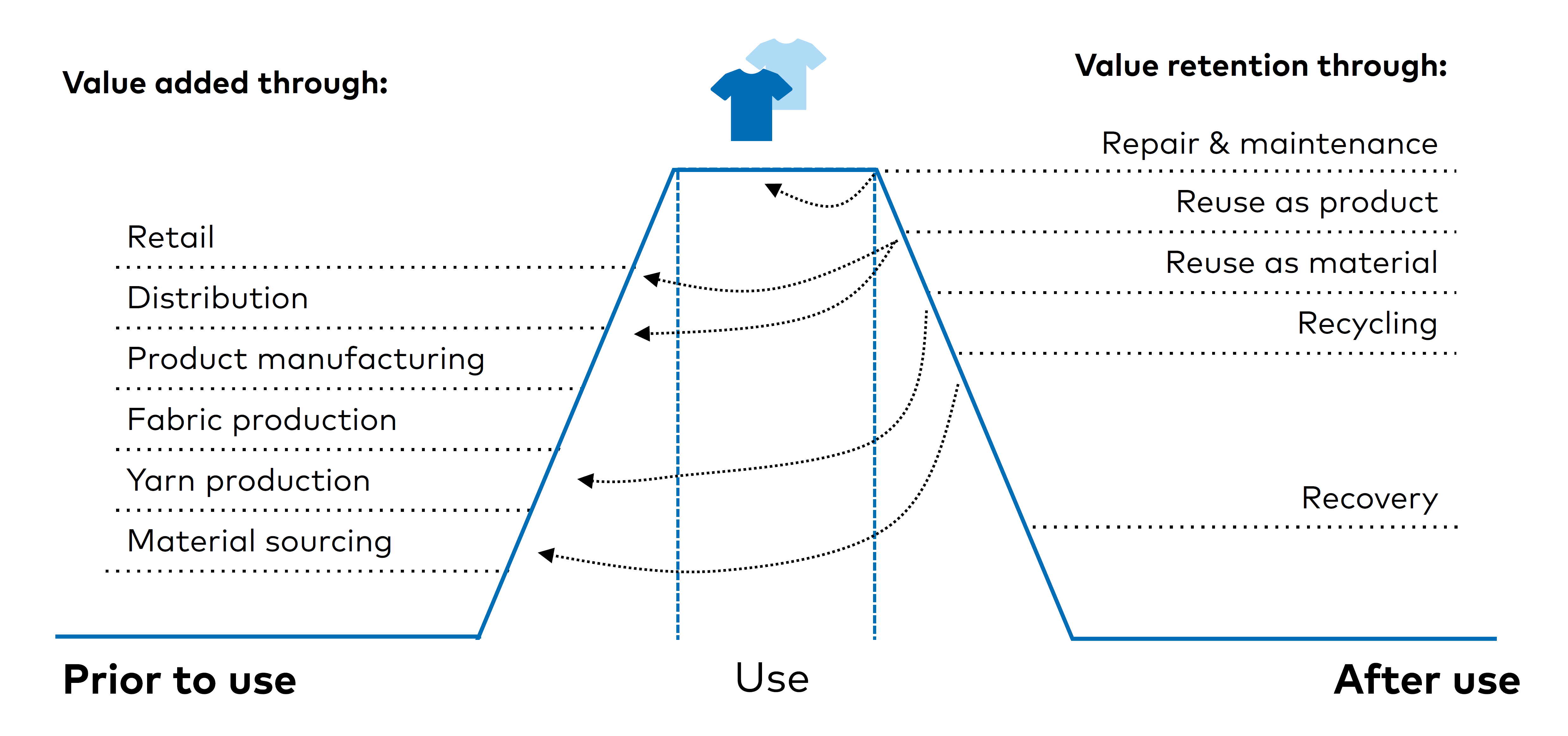

Traditionally, when manufacturing a textile product, value is added throughout the value chain, where the highest value is gained from the finished product (Figure 5). Prolonging the lifespan of textiles and improving reuse and recycling activities across the value chain are key actions in moving towards circularity. Moreover, in the textile industry, key aspects in the circular transition relate to traceability of raw materials, design for longevity, sustainable production (e.g., resource efficiency, production on-demand and local production), renting and leasing services, repair and maintenance services, take-back and resale of the product (second hand), collection, reuse and recycling of material (e.g., chemical and mechanical recycling).

Figure 5: Value addition and retention in the circular value chain of textiles.

Source: Originally adapted from Achterberg, Hinfelaar, & Bocken (2016)

2.2 The textile sector in the Nordics

The textile sector is important in the economy of many European countries, including the Nordics. In 2021, the European textile and clothing industry turnover was 147 billion Euro, which is an increase with 11 percent since the year before. The sector has 1.3 million employees in Europe (EURATEX, 2022).

The selected Nordic countries in this study and their respective turnover within the textile and clothes industry for the year 2020 is shown in table 2 below.

Unit: billion Euro | Finland | Sweden | Norway |

Textile industry turnover | 0.44 | 0.86 | 0.71 |

Clothing industry turnover | 0.58 | 1.24 | 0.28 |

Table 2: Overview of textile and clothes turnover, (year 2020), billion Euro.

Source: Finnish Textile and Fashion Association, 2020; Statistics Sweden, 2020

In 2019, around 62 kt of new textiles were imported to Finland and the total consumption of new textile products was 11,3 kilos per capita, household consumption having the largest share (83%) (Dahlbo et al. 2020). The Swedish total consumption of new textiles was 13,7 kilos per capita during 2019. A large share of used clothes and textiles, approximately 7,5 kilo per capita end up as waste and are sent directly to incineration. Thus, a large portion of textiles are not being reused or recycled (Naturvårdsverket, 2021). Norway’s total consumption of new textiles and clothes was 15 kilos per capita during 2020. Approximately 50 percent of the used clothes and textiles end up as waste and then sent directly to incineration (Klima- og miljødepartementet, 2021).

Figure 6: Number of companies in the textile and clothing industry in Finland, Sweden, and Norway (year 2020)

Source: Finnish Textile Fashion, 2022

The textile and clothing industry provides many employment opportunities and represents one of many gateways for young people access to the labour market. The number of companies in the textile and clothes industry in Finland, Sweden and Norway can be seen in figure 6.

The numbers of employees in the textile and clothing industry in Finland, Sweden and Norway related to year 2020 can be seen in figure 7 below.

Figure 7: Overview of number of employees in the textile and clothing industry in Finland, Sweden and Norway (year 2020)

Source: Finnish Textile Fashion, 2022

In the light of the data in table 2, and figures 6 and 7, it is obvious that the value chain of textiles was one of the prioritised areas identified in the Nordic Council of Ministers’ large study on circular transition potential, 2020–22 (Luoma et al., 2021) and subsequently also chosen as scope for the present work. Textiles are explicitly mentioned as focus areas of national priorities for Sweden, Finland, Denmark, Åland as well as for the European Union (See e.g., European Environmental Agency, 2023b). Joint Nordic processes have also been launched which aims to turn the textile industry towards more sustainability. It is also internationally acknowledged that the Nordics (in particular Finland and Sweden) host cutting-edge RDI activity on new biobased and circular textile solutions, such as man-made cellulose fibres. At the same time, the fashion industry in the Nordics has become increasingly aware of more sustainable consumer trends, forming a counterforce to disposable fast fashion.

The textile sector in the Nordics has shown notable development in promoting sustainability and circularity. There are several initiatives developing more sustainable production methods, design principles, material choices, collection, sorting and recycling methods, as well as consumption related initiatives (See e.g., the Nordic Council of Ministers, 2023). There are also some initiatives taken regarding economic instruments to promote circular economy in the textile sector. These initiatives are primarily targeted at implementing EPR for textiles.

A study commissioned by the Swedish Government in 2017, had the main task of analysing and proposing economic instruments to promote a resource efficient and circular economy. The study proposed introducing a tax reduction of 50% of the labour cost for consumption of goods and services in connection to repairing textiles, maintenance of furniture, second-hand sales, or repair of consumer products (SOU, 2017).

The Royal Swedish Academy of Engineering Sciences (2020) studied how current policies need to shift to establishing a national movement towards resource efficiency and a circular economy. Within the textile sector, the study suggests promoting increased use of regenerated fibres from residual flows by promoting economic instruments that favour recycling of textiles. As an incentive, manufactures of new products based on recycled materials should be rewarded by a tax break, which in turn could potentially create new jobs, build a more competitive manufacturing industry, thus contributing to the national economy. Finally, the study suggests reviewing which kind of customer barriers that create obstacles to the trading of used clothes as well as difficulties for trading used materials between countries (IVA, 2020).

IVL Swedish Environmental Research Institute (2022) studied policy measures on behalf of Circular Sweden

Circular Sweden is a business forum that focuses on driving the development of circular product and material flows forward. https://www.circularsweden.se/

In 2020, the Swedish Government initiated an investigation with a focus to examine the EPR for textiles, to ensure separate collection of textiles for reuse and textiles for waste and recycling (SOU, 2020). The study showed that less than 1 percent of textiles are recycled, and fibre to fibre recycling occurs approximately at a rate of 2–3 percent on a global scale.

During September 2022, the Norwegian government decided to appoint a working group to investigate the possibilities of implementing EPR for textiles, with the aim to reduce their environmental impact. The working group will focus on mapping quantities, the portion of imports and how textiles are managed after use. Digital product passports will also be examined to evaluate if they can be designed for usage in the textile sector. National objectives thought to boost a circular economy, will also be presented by the working group in September 2023 (Klima- og miljødepartementet, 2022).

In Finland, there are currently ongoing discussions on how EPR will affect already established schemes for collecting waste textiles (Saarinen, 2023). It should also be noted that the European Union is proposing an EPR for textiles as part of the renewal of the Waste Framework Directive (EU Commission, 2023b).

2.3 Options for economic instruments in the textile sector

In the textile sector, economic instruments can play a crucial role in promoting a circular economy, as well as unlocking various opportunities. By implementing economic instruments, the market for more sustainable textiles can be boosted, creating a level playing field for environmentally friendly products. This, in turn, could encourage innovation in the sector, leading to the development of new technologies and practices that enhance the circular economy.

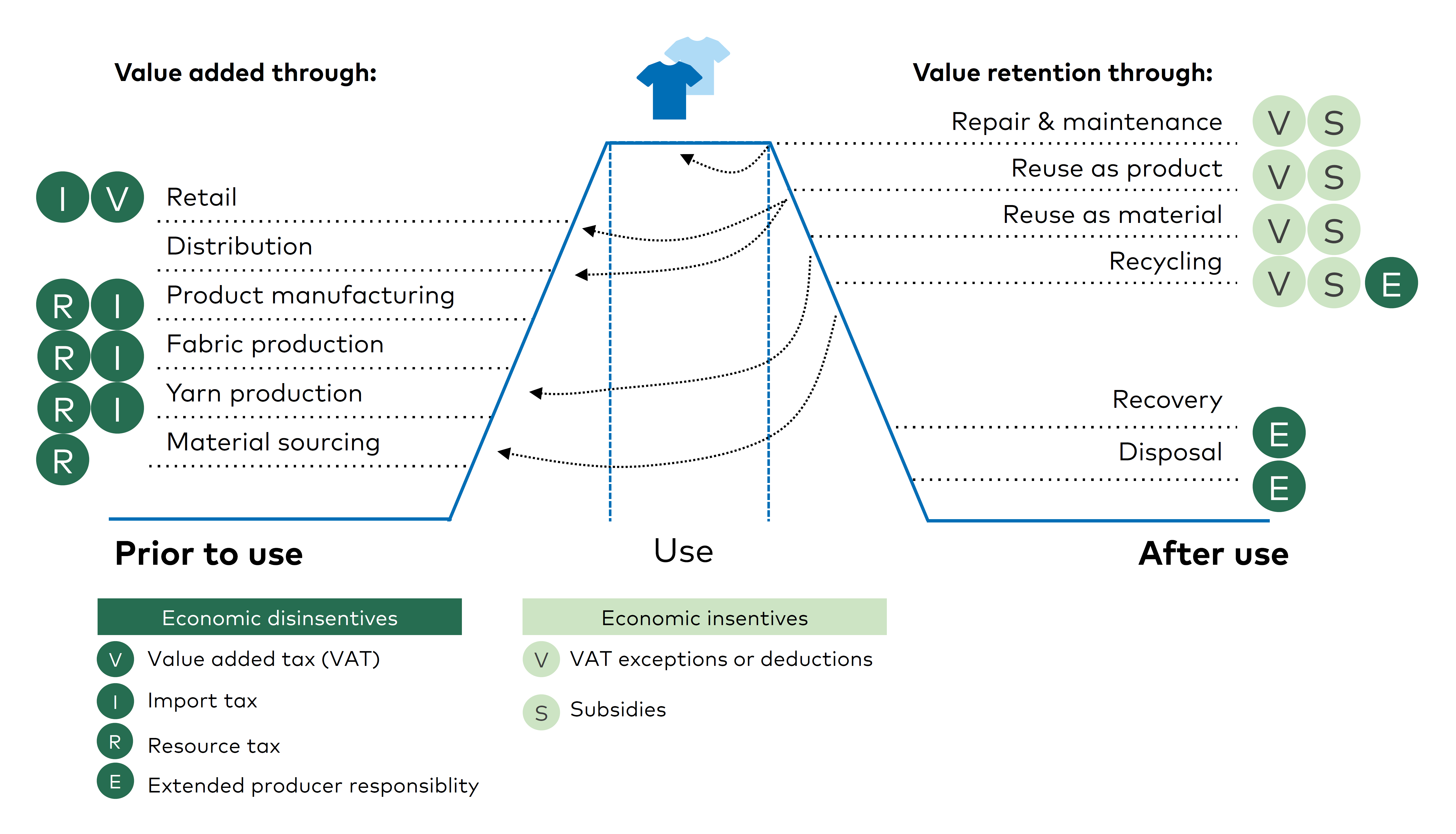

As discussed in the previous chapters, several economic instruments to support a circular textile sector have been attempted or studied in the Nordics. Figure 8 shows how different economic instruments could be placed into the value chain of textiles. Chosen economic instruments for further discussion are divided into resources taxes, import taxes, EPR schemes and increasing of VAT.

Figure 8: Outlook for possible economic instruments to promote the circular economy in the textile sector

Source: Originally adapted from Achterberg, Hinfelaar, & Bocken, 2016

For textiles, natural resource taxes, such as raw material tax could be targeted to the first stages of the value chain, where raw materials are purchased. Although a natural resource tax is already in use in certain sectors, the key challenge in the textile sector is linked to the fact that such a tax requires careful targeting to the early stages of the value chain in order to be effective. Whereas most textiles used in the Nordics are manufactured outside the region, natural resource tax would essentially target raw materials that are produced in the Nordic countries. Thus, the volumes, types and sustainability performance of textiles produced locally would need to be assessed firstly. In general, the tax should be targeted towards non-sustainable textile fibres, steering towards the use of sustainable ones. However, there is a notable risk that introducing tax to local textile production in the Nordics might only harm domestic textile production sector and steer the acquiring of fibre towards cheaper countries.

Import taxes, i.e. customs duty could be used to guide towards more sustainable material usage in the textile products and encourage local production and sourcing. A research study by Hennlock et al. (2021) indicate possibilities for the Nordic countries to let the textile importer of a specific good bear the environmental charges, fees or taxes corresponding to the external effects caused by the design and production. This is further discussed in chapter 4.4.6. However, effective implementation and enforcement across international supply chains poses challenges that need to be solved. Firstly, from an EU member state perspective, import tax is only targeted for non-EU imports. Additionally, such as WTO-rules would have to be taken account which might create challenges. Also, current global commodity codes that are used for import and export declarations isn’t built to segregate sustainable and non-sustainable textiles from each other. The lack of alternative sustainable raw materials poses challenges also, similarly as with resource tax.

By implementing EPR schemes, the textile sector could steer producers to design products with recyclability in mind and establish effective recycling systems. Leading to reduced waste, resource conservation, and increased circularity in the industry.

By raising the VAT on textiles, consumers’ purchasing decisions can be guided towards opting for durable and environmentally friendly products. In addition, the playing field between unsustainable and sustainable textiles could be levelled by targeting the prices of less sustainable textiles. Such an increase in the VAT could create a price differential that would incentivise the adoption of circular business models, such as product repair and reuse, while discouraging fast fashion and disposable consumption patterns. While increasing the VAT on textiles can promote sustainable consumption, it is crucial to find the right balance in order to not hamper the affordability and creating resistance from industry stakeholders. In addition, policy makers tend to be somewhat hesitant to create a complex sector-specific VAT system.

One potential possibility for economic instruments in the textile sector is the implementation of VAT exceptions or deductions for activities like reselling, or mending and repairing services, rather than imposing taxes on raw materials. Such measures could incentivize and support the growth of second-hand markets, prolonging the lifespan of textiles. Furthermore, a reduction of the VAT for repair services can be a powerful tool, incentivising consumers to make sustainable choices and prolonging the life of textiles. On the other hand, reducing the VAT requires careful consideration of the impacts on revenues and market dynamics. As highlighted in section 1.4, policymakers in Sweden reduced the exactly this VAT during 2022.

Subsidies can play a role in promoting a circular economy in the textile sector. One potential form of subsidy is investment support, which can help businesses in the sector to acquire and implement technologies that enable more sustainable practices. This could include financial assistance for the purchase of machinery and equipment for mechanical or chemical recycling, as well as support research and development activities aimed at advancing circular economy solutions. In addition to providing financial assistance, subsidies can also encourage collaboration and knowledge sharing among businesses, research institutions, and technology providers.

The implementation of economic instruments promoting a circular economy in the textile sector faces several challenges. In addition to the challenge of defining what constitutes a "sustainable fibre" (considering different perspectives and criteria), there is, to date, a limited availability of affordable substitutes for popular virgin materials like cotton or polyester. In the Nordic countries, most companies operating in the textile sector are SMEs. Companies that struggle to afford novel recycled and sustainable materials, as their availability is scarce, and mostly out of reach. New innovations are brought to the attention of the industry each year, (e.g. Spinnova and Infinited Fiber Company both from Finland), but most of the solutions are still in their scaling phase and the startups only have capacity to cooperate with larger companies in the industry, as the demand for their raw materials is significant.

As pointed out in the Low-Carbon Circular Transition in the Nordics study (Part II), promoting the use of recycled content for textiles is dependent on technologies to be scaled up, especially when it comes to novel materials. For example, the development of chemical recycling, a promising solution for textile waste, is still in its early stages and largely limited to pilot-scale initiatives. Scaling up this technology poses challenges in terms of infrastructure, investment, and technological advancements. There is a lack of incentives among brand-owners and investors to further drive the development of chemical recycling. Recycled fibres are more expensive than virgin fibres, and the infrastructure for chemical recycling plants is underdeveloped. For the future, chemical recycling can be promising especially because it can for instance separate blended cotton and polyester fibres without decreasing the value of the fibres (Hjelt et al. 2022).