2. Background

2.1. The need for integrated biodiversity considerations in the finance sector

Economic growth relies on natural capital. Despite this fact, there is a discrepancy between this dependency and the activities of the financial sector, contributing to threats towards biodiversity and the natural environment. The financial sector must turn this trend around by aligning their activities with biodiversity objectives and play a positive role in preserving and restoring functional ecosystems

OECD (2021)

According to IPBES, five major factors are the main drivers of biodiversity loss

IPBES (2019)

- Land-use and sea-use change

- Direct overexploitation of natural resources

- Climate change

- Pollution of soil, water, and air

- Spread of invasive species

All business activities contribute to these five factors, whether it is through resource extraction, manufacturing, transportation, consumption, or end-of-life treatment. Certain sectors have considerably higher negative impact on biodiversity than others, due to their large contribution to biodiversity loss drivers. The main value chains that are responsible for most of the biodiversity loss are the food system, the infrastructure and mobility sector, the energy sector and the textile sector

Benton et al. (2021)

Campbell et al. (2017)

Finance institutions have facilitated the expansion of business activities detrimental to biological diversity. By investing in sectors such as agriculture, fisheries, fossil fuels, and energy, and providing funding to polluting industries, the finance sector has supported activities that have led to biodiversity loss

IPBES (2019)

Consideration of nature has been absent in the finance sector and in economic models in general, and issues related to the biosphere have been dismissed as externalities. However, with increasing demonstration of environmental crises, consideration for the natural environment in the financial sector has gradually become necessary or in many cases even a business opportunity. This is seen, for example, in the inclusion of climate change in economic models and in shifting energy investments from fossil fuels to renewable sources. Until recently, the financial sector has primarily focused on climate aspects of their investments, monitoring GHG emissions. It has been expressed that this scope needs to be broadened to address the interconnected climate and biodiversity crises we are facing.

Biodiversity loss from financial activities is one of the branches of environmental concerns that has grown in the later years, and an issue that has been thoroughly described in the Dasgupta

Dasgupta (2021)

TNFD (2022)

Dasgupta (2021)

Dasgupta (2021)

Deutz et. Al. (2020)

UNEP & ELD (2022)

2.2. The potential for the financial sector to increase nature-positive investments and Nature Based Solutions

The demand for investing in activities with positive impact on nature is rapidly rising, and the financial sector is increasingly urged to align their portfolios with biodiversity positive outcomes. Many nature positive investment activities are already in place, and new initiatives are surfacing.

Overall, strategies can be divided into two categories: Increasing investments that are positive for nature and reducing investments that have negative impacts on nature. The first category can be termed financing green, representing the efforts to invest more in activities that are positive for nature, while the second category can be termed greening finance, encompassing divestment from harmful activities.

2.2.1. Financial approaches to nature-positive investments

Many nature-positive investments have indirect beneficial effects on biodiversity conservation, while some are directly aimed at biodiversity conservation (Table 1).

Indirect potential nature positive activities | Direct nature positive activities |

|

|

Table 1. Overview of indirect and direct nature positive activities. Adapted from WWF and The Biodiversity Consultancy.

WWF & The Biodiversity Consultancy (2021)

Until now, most sustainable investment activities have climate adaptation or mitigation as their primary focus, with indirect benefits for nature. Investment in Nature-based Solutions which can promote synergies between climate goals and biodiversity conservation are key to make finance nature positive. Scaling up investments in these solutions are a significant opportunity.

There are several financial approaches that can support investment in nature-positive activities: Many of which are already being used by public development banks. Examples are:

- Grants

- Pay for success structures

- Sustainability bonds or green bonds

- Public loans linked to environmental programs

- Investments integrating Natural Capital Accounting

- First loss or other concessional capital

- Financial guarantees or risk insurance

- Leveraging debt conversion for nature conservation

- Private loans and/or equity linked to positive environmental outcomes

- Targeted investment in conservation businesses

- Technical assistance funds or project preparation grants.

This section has presented the potential for financial institutions to contribute positively to biodiversity conservation through overall strategies and investment activities. Ongoing initiatives have pinpointed the need for specific tools in order to implement well-functioning criteria, standards, and safeguards. Several analytical tools have already been developed globally to support the uptake of nature-positive investments in the financial sector. Examples of such analytical tools will be presented in the next chapter.

2.3. Analytical tools to ensure positive biodiversity strategies

Integrating biodiversity into finance and investments is complex, but there already exist numerous tools and frameworks to help better account for biodiversity and/or enable nature positive investments. Furthermore, multiple different forums and initiatives have been established in recent years with the purpose of establishing ways to share knowledge of best practices future developments and/or to send a message on the willingness to address the topic and act on the biodiversity crisis. But there are still numerous difficulties and little data that enable properly connecting biodiversity and finance activities in a meaningful way that allows to better support the integration of biodiversity into decision-making processes. But the finance-biodiversity nexus is currently drawing more and more attention, and in addition to already existing tools there are several initiatives in development, including in the Nordic countries. Two projects have recently received funding from the Swedish research institution MISTRA. The first project, FinBio, which is led by the Stockholm Resilience Centre, will develop methods and metrics to identify business models that protect biodiversity

MISTRA (2022)

MISTRA FinBio (2023)

The list below (Table 2) provides an overview of Key initiatives & Forums and Tools & Frameworks. A list with further details can be found in Appendix B.

Key Initiatives & Forums |

Biodiversity/Nature Specific Focus |

|

Sustainability Focus |

|

Table 2: Overview of Key initiatives & Forums and Tools & Frameworks

Frameworks & Standards |

|

Tools |

Biodiversity Focus |

|

Sustainability Focus |

|

2.4. Commonly used biodiversity safeguards

Biodiversity safeguards play a crucial role in protecting and preserving biodiversity and are employed to mitigate the negative impacts and promote sustainable practices. The safeguards encompass a wide range of approaches and tools.

2.4.1. Risk-based approach

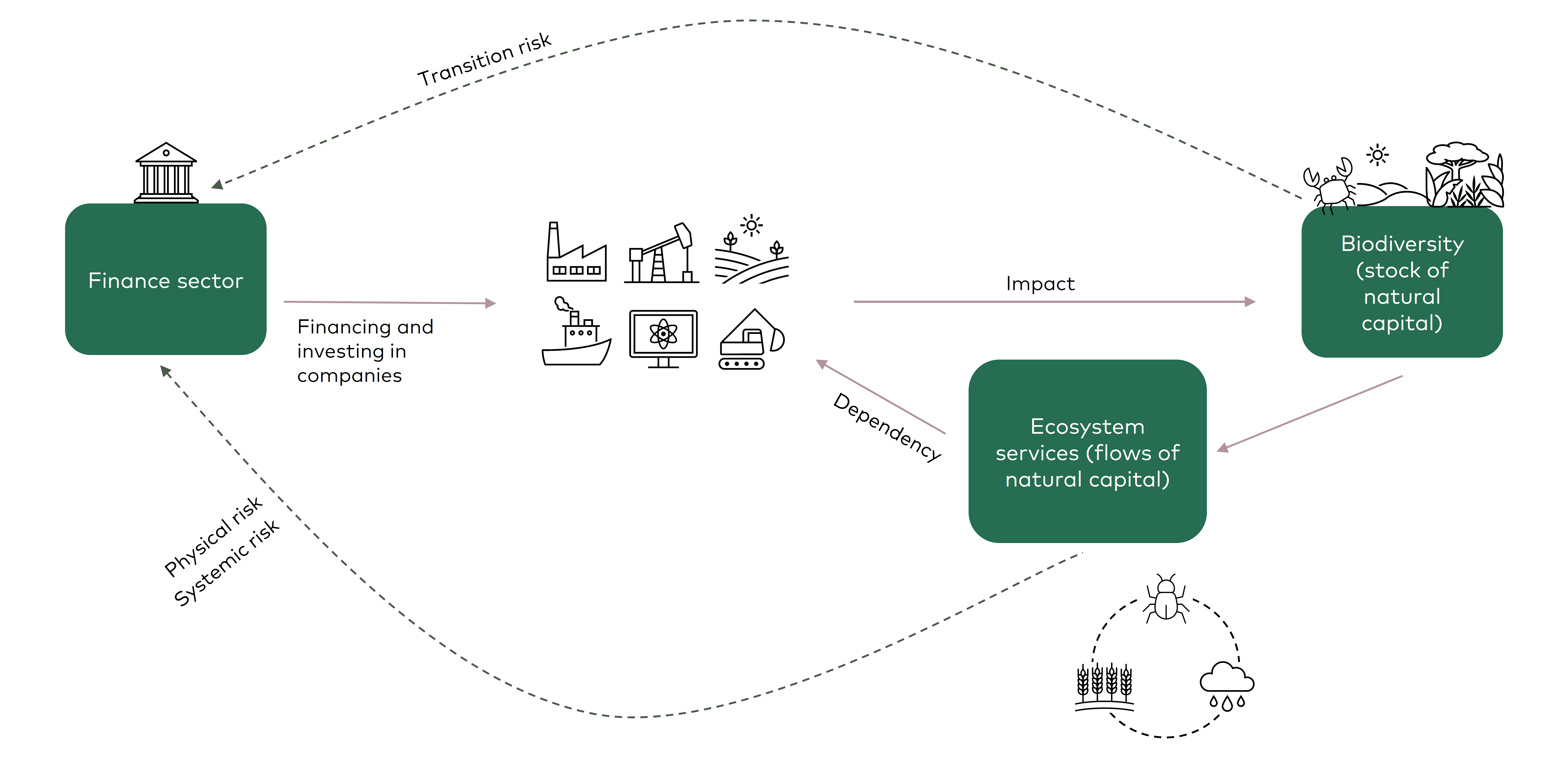

Investing in activities that cause harm on nature and biodiversity brings several types of risks for financial institutions, as illustrated in Figure 1.

Figure 1. Overview of risks for financial institutions. Relationship between financial sector, economy, biodiversity and ecosystem services, and resulting risks. Adapted from WWF and The Biodiversity Consultancy.

WWF & The Biodiversity Consultancy (2021)

A risk-based approach requires that financial institutions consider the physical, systemic, and transition risk of biodiversity of their investments, as these translate into market and credit risks. Risk-screening of potential projects serves as an opportunity to identify projects with potentially high biodiversity risk, that are not eligible for funding or whose funding should be withdrawn.

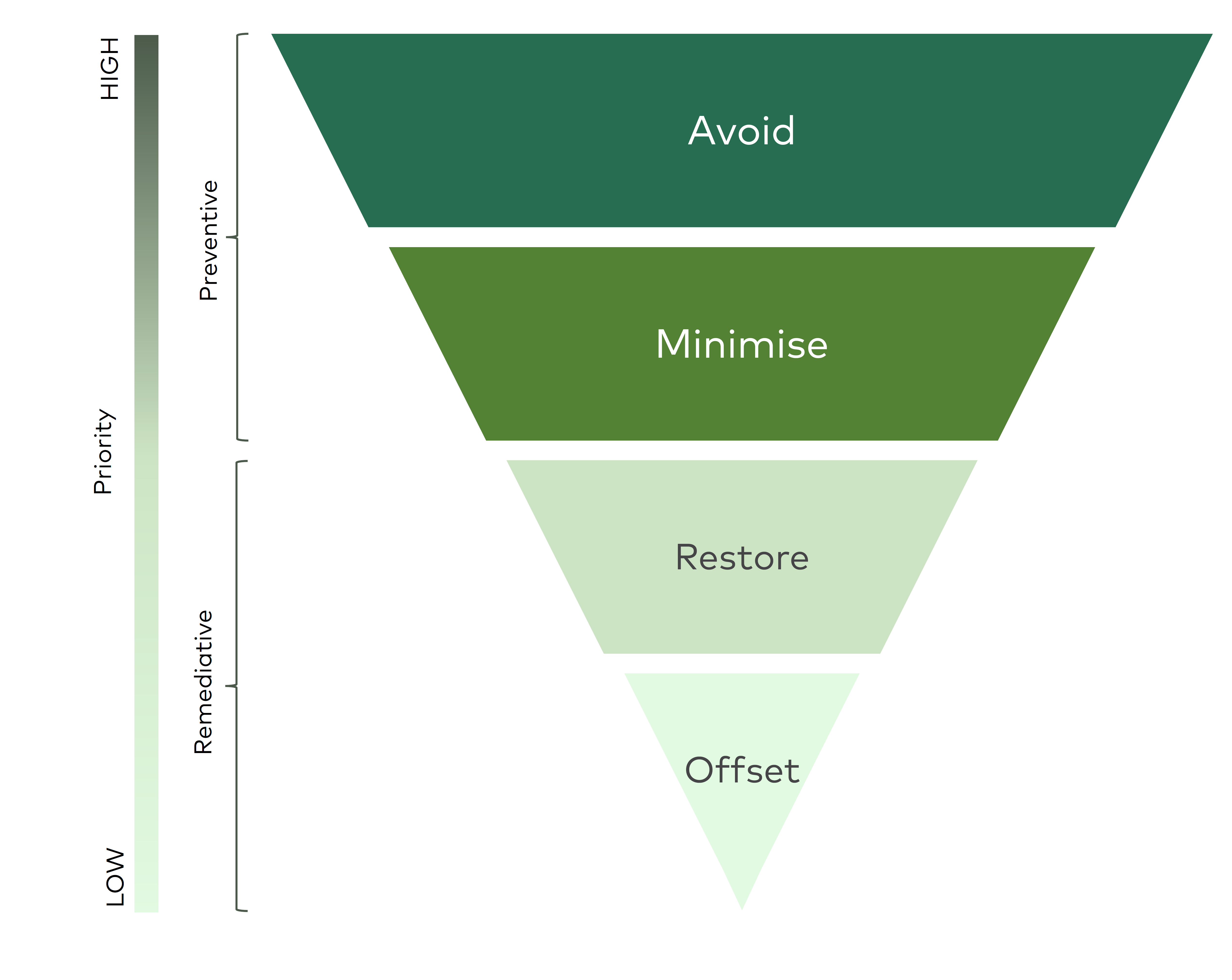

2.4.2. Mitigation hierarchy

The mitigation hierarchy is an acknowledged tool to manage potential risks and impacts to biodiversity, often used by financial institutions

IFC (2012)

Avoid negative impacts by considering alternative locations, technologies, layout, phasing or scope of the project. Avoidance is often the least costly mitigation step and, in many cases, the only option to protect pristine biodiversity.

Where complete avoidance is not possible minimisation of impacts is the next step. Minimising efforts should contribute to reduction of the intensity, significance, and duration of impacts.

Restoration entails repair of any degradation or damage on biodiversity or ecosystems. This can for example be done by re-establishment of the ecosystem function, structure and composition.

Offsetting negative impacts is the last resort in case all other options are unsuccessful, or there are residual impacts after taking all other measures. It thereby works as compensation for any residual negative impacts. Offsets should be designed to achieve measurable positive biodiversity outcomes that fulfil the no net loss criteria or contribute to net gain.

Figure 2. The mitigation hierarchy

Cross Sector Biodiversity Initiative (2015)

2.4.3. Criteria to identify biodiversity features of high concern.

In order to evaluate whether projects can be considered a threat to biodiversity features of high concern, financial institutions apply certain criteria to identify relevant areas or traits. Criteria are often built around for example the Integrated Biodiversity Assessment Tool

IBAT (2023)

IUCN Red List (2023)

2.5. International Agreements and Regulatory requirements

This following section will outline international agreements and regulatory requirements for sustainable financing.

2.5.1. The Kunming-Montreal Biodiversity Framework

One of the most significant milestones in tackling the biodiversity crisis is the adoption of the Kunming-Montreal Global framework, which is considered to be to the nature agenda what the Paris Agreement is to climate change. The framework was adopted by 196 parties to the Convention on Biological Diversity in December 2022 at COP 15 in Montreal Canada

CBD (2022A)

UNEP FI (2022)

The framework has four long-term goals for 2050 and presents 23 targets for urgent action in the current decade to ensure that by 2030 several targets are reached such as the protection of 30 % of nature, and that we are on the right trajectory for achieving the 2050 goals. Some of the targets suggest measures directly aimed at the financial sector and outline several actions needing to be taken by the financial sector. The third section of the targets describes tools and solutions for mainstreaming and implementation. Target 14 describes the need for biodiversity to become an integral part of decision-making processes across levels of government and sectors and ensure proper alignment of fiscal and financial flows with the framework goals. Target 15 states the need to implement adequate measures, including legal measures to ensure that financial institutions regularly monitor and assess their risks, dependencies, and impacts on biodiversity and that they are transparently disclosed, thereby contributing to reducing negative impacts, reducing biodiversity-related risks and increasing positive impacts and ensure sustainable production patterns. To address the nature-related funding gap, Target 19 calls for an increase in financial resources from both public and private sources, an increase in domestic resource mobilisation, and a reallocation of funds from the global north to the global south. Some of the measures suggested in Target 19 include PES (Payments for Ecosystem Services) schemes, green bonds, biodiversity offsets and credits, and to optimise co-benefits and synergies with measures that target both biodiversity and climate change

CBD (2022A)

Besides the global biodiversity framework, other supporting documents were adopted, including a monitoring framework with indicators for tracking progress towards reaching the goals. The monitoring framework will be continuously updated and further developed in the coming years

CBD (2022B)

CBD (2022C)

CBD (2022D)

Many parties will soon update their biodiversity strategies and action plans to ensure alignment with the new global framework by adopting new policies and/or legislation. This provides new risks as well as new opportunities for businesses and financial institutions. As a response to the global biodiversity framework, UNEP FI will update their guidance for setting biodiversity targets in order to align it with the new global framework, especially relevant to the signatories to the Principles for Responsible Banking and calls for alignment with other initiatives

UNEP FI (2023)

2.5.2. EU Policies

The overarching EU Policies on sustainable finance are the Action Plan on Financing Sustainable Growth from 2018 and the Strategy for financing the transition to a sustainable economy published in 2021

EU (2021A)

2.5.3. EU taxonomy

The Taxonomy Regulation entered into force in July 2020 and has since been delegated in 2021 and 2022

EU (2020A)

EU (2023)

The EU taxonomy has a guiding purpose and does not entail any types of obligations on companies or prohibition against certain types of investments. Rather, it is expected to provide benefits though increased transparency, classification, and communication regarding which economic activities that can be considered environmentally sustainable.

The taxonomy includes economic activities in several sectors, which are held against six environmental objectives

EU (2023)

- Climate change mitigation

- Climate change adaptation

- The sustainable use and protection of water and marine resources

- The transition to a circular economy

- Pollution prevention and control

- The protection and restoration of biodiversity and ecosystems

The sixth objective regarding biodiversity is most relevant for this study. However, the other environmental objectives also have relevance based on their indirect impact on biodiversity and ecosystems. Economic activities will be assigned technical screening criteria tied to each of the environmental objectives. These technical screening criteria are defined through delegated acts to the taxonomy regulation. Currently (Q1 2023), only the first delegated act on sustainable activities for climate change adaptation and mitigation objectives has been published

EU (2021C)

- Conservation including restoration, of habitats, ecosystems and species and

- Hotels, holiday, camping grounds and similar accommodation

Once the final version of technical screening criteria for the protection and restoration of biodiversity and ecosystems are published, this will provide a clearer framework for finance activities contributing positively to biodiversity.

For an activity to be classified as sustainable it is not sufficient to contribute to one of the of the six objectives. The activity must not violate any of the other objectives either. There are four criteria for classifying an economic activity as sustainable:

- The economic activity contributes to one of the six environmental objectives

- The economic activity does ‘no significant harm’ (DNSH) to any of the six environmental objectives

- The economic activity meets ‘minimum safeguards’ such as the UN Guiding Principles on Business and Human Rights to not have negative social impact

- The economic activity complies with the technical screening criteria developed by the EU Technical Expert Group

If these four criteria are fulfilled, the activity can be classified as sustainable according to the Taxonomy.

While the Taxonomy does not entail any obligations on its own, it has ties to other EU legislation that require companies to disclose the share of taxonomy-aligned activities. This is part of the Sustainable Finance Disclosure Regulation and the Corporate Sustainability Reporting Directive.

2.5.4. EU Corporate Sustainability Reporting Directive

The Corporate Sustainability Reporting Directive entered into force in January 2023

EU (2022A)

EFRAG (2023)

2.5.5. EU Sustainable Finance Disclosure Regulation

The EU Sustainable Finance Disclosure Regulation (SFDR) has been effective since March 2021 with the purpose to harmonise sustainability related transparency and disclosure requirements for financial market participants and financial advisers. The regulation requires financial market participants to assess and publicly disclose sustainability and environmental, social and governance (ESG) factors in their investments. Sustainability-related information should be disclosed at entity level as well as at product level, entity being the level of a for example a bank, and product being the level of for example a portfolio or pension scheme.

At entity level, financial market participants are required to disclose information about their policies on the integration of sustainability risks in their investment decision-making process. Moreover, they need to disclose information on where they consider investment decisions to have adverse impacts on sustainability factors and a statement of due diligence regarding these impacts. If they do not consider adverse impacts on sustainability factors of investment decisions, they should state clear reasons for why they do not do so. In remuneration policies, financial market participants shall include information on how these policies are consistent with the integration of sustainability risks.

Definition of ’sustainable investment’ in the SFDR

(Sustainable Finance Disclosure Regulation)

(Sustainable Finance Disclosure Regulation)

‘Sustainable investment’ means an investment in an economic activity that contributes to an environmental objective, as measured, for example, by key resource efficiency indicators on the use of energy, renewable energy, raw materials, water and land, on the production of waste, and greenhouse gas emissions, or on its impact on biodiversity and the circular economy, or an investment in an economic activity that contributes to a social objective, in particular an investment that contributes to tackling inequality or that fosters social cohesion, social integration and labour relations, or an investment in human capital or economically or socially disadvantaged communities, provided that such investments do not significantly harm any of those objectives and that the investee companies follow good governance practices, in particular with respect to sound management structures, employee relations, remuneration of staff and tax compliance.

EU (2020B)

At product level, financial market participants must disclose principal adverse impacts on sustainability factors.

The SFDR classifies financial products into three types

EU (2020B)

- Products that have sustainable investments as their primary objective (Article 9)

- Products that promote environmental and social characteristics, among other characteristics (Article 8)

- Products without integrated ESG considerations (Article 6)

Products that fit under Article 8 and 9 need to fulfil additional disclosure requirements

EU (2020B)

The specific regulatory technical standards that financial market participants should use for SFDR disclosure were adopted by the European Commission in April 2022. These standards outline the methodology, content and presentation of the disclosed content

EU (2022B)

2.5.6. Proposed or forthcoming regulatory requirements

In addition to the regulations described above, there are forthcoming legislative initiatives from the EU that will influence financial institutions with regards to sustainable investments. A European Green Bond standard was proposed in 2021. Currently, there is no existing EU regulation for Green Bonds, and Green bonds standards have not yet been legislated at national level by EU Member States, making the European Green Bond Standard the first on the EU market. The Green Bond Standard must support the upscale of green bonds on the European market and strengthening of the sustainability requirements for existing green bonds

EU (2021B)

The proposed framework includes four key requirements

European Commission (2021)

- Green bond funds should be fully allocated to EU taxonomy aligned projects

- There should be full transparency on the allocation of bond proceeds, regulated by reporting requirements

- External reviewers should check all green bonds for compliance and taxonomy alignment

- External reviewers must be supervised by the European Securities Markets Authority

Requirements will be voluntary and aim to make it possible to differentiate between EU Green Bonds, which will serve as a form of “gold standard”, and other green bonds. The standard will apply to bonds that are designated “European green bonds”, but also bonds that are earmarked as “green” without making use of the term “European green bonds”. The standard will provide opportunities for issuers of green bonds, such as the Nordic financial institutions, to demonstrate that their investments are aligned with the EU taxonomy.