3. Current practices in the Nordic countries

Image: iStock

In this chapter, we briefly outline current practices relating to offshore wind licensing in each of the Nordic countries. We also provide some preliminary assessments on key barriers to accelerated offshore wind deployment. Each of the subchapters 3.1–3.8 addresses the individual countries: Denmark, Norway, Sweden, Finland, Iceland, Åland, the Faroe Islands and Greenland. No offshore wind farms are currently in operation in the latter four countries.

Each subchapter is structured as follows:

- Background: Brief account of installed capacity and the latest developments

- Licensing process: Overview of the process for deploying offshore wind projects, including regulations, implementation in practice, subsidies and organisational considerations. “Licensing” is therefore understood broadly to encompass all aspects that influence deployment. The depiction is intended to be concise, yet specific regarding the policies that influence design and deployment timing.

- Barriers: Our identified main barriers to increased and accelerated offshore wind deployment. We also briefly summarise interviews and desktop studies that suggest adjustments are needed to overcome existing barriers.

Finally, we summarise selected similarities and differences between the Nordic countries (subchapter 3.9) and discuss and compare the most important barriers to accelerated deployment (subchapter 3.10).

3.1. Denmark

Background

Denmark was the first country in the world to install offshore wind, and since 1991, the country has constructed 2.7 GW of offshore wind capacity, with 1.4 GW under construction. Offshore wind now covers approximately 25 per cent of the country’s total electricity consumption. The country is committed to achieving its emission reduction targets (-70 per cent by 2030 vs. 1990) and aims to achieve climate neutrality by 2045. Offshore wind targets are decided by the Danish Parliament as part of its Energy Agreements, which, although binding, are not enacted in law. In addition, several informal offshore wind energy targets have been set in previous years through various agreements that act as drivers, including the signing of the Marienborg Declaration

Finance Act (2022): Tender for 2 GW by 2030. Klimaaftale om grøn strøm og varme [Climate Agreement on Green Electricity and Heat] (2022): Tender for at least 4 GW by 2030. Tillægsaftale om Energiø Bornholm (2022): Tender at least 3 GW by 2030. Marienborg-Declaration (2022): Aims to develop 6.3 GW in Denmark by 2030.

Esbjerg Declaration + Ostend Declaration: Aims to develop 35 GW in the Danish section of the North Sea by 2050.

While Denmark has spearheaded the development of offshore wind, the country has encountered significant challenges in its tendering process over the last few years. The Thor tender in 2021 marked the first instance where the successful bidder agreed to pay the state rather than receive a subsidy. The subsequent tender round in 2024, which offered no subsidies and included a requirement for state co-ownership, failed to attract any bids. The government is now preparing a new offshore wind tender for 3 GW of capacity, which includes a state subsidy.

Source: Danish Energy Agency, adapted by Brinckmann.

Procedural framework

The Danish Energy Agency (DEA) serves as the primary point of contact for developers in the permitting process, as it issues the three main permits required to establish offshore wind projects. In addition to the three permits issued by the DEA, developers must obtain approvals from other authorities, for example, from the Danish Maritime Authority for the temporary and permanent marking and buoying of the work areas and the wind farm itself, and from the Danish Civil Aviation and Railway Authority for turbine lighting, among others. The DEA functions as the central contact point for the permitting process, facilitating coordination between developers and the relevant authorities.

Today, offshore wind project development in Denmark is driven through a competitive tendering procedure. In the past, offshore sites were also allocated via an open-door system, where developers could apply to build an offshore wind farm with a specific capacity at a location of their choosing, rather than the national government specifying both the capacity and area. In June 2023, the Danish Energy Agency rejected 24 open-door projects and subsequently cancelled the scheme due to concerns about its compliance with European Union (EU) state aid rules.

Note that in May 2024, the Energy Appeals Board referred a number of previously rejected cases for re-evaluation. The outcome of this re-evaluation is still pending.

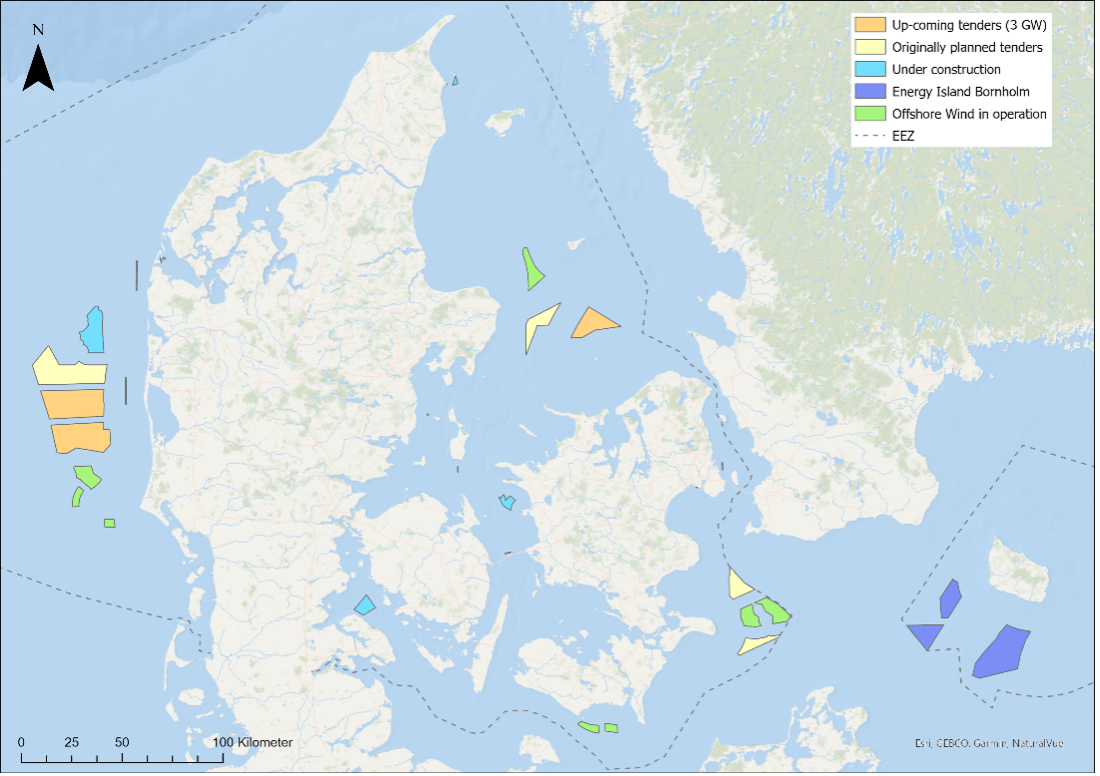

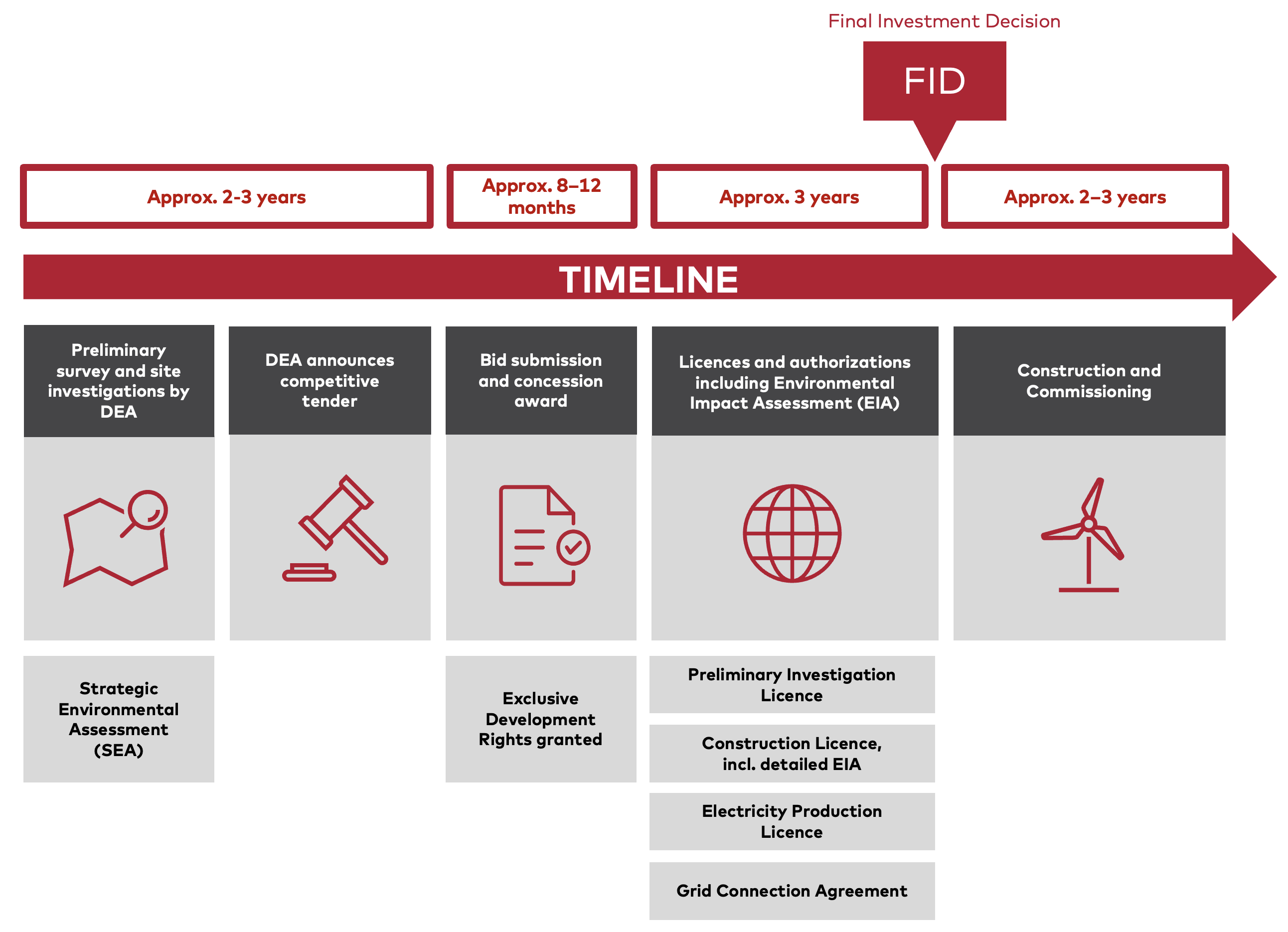

The Danish tender and permit process is illustrated in Figure 3.2. The figure shows the process for tenders prepared in 2024/25. It should be noted that several additional areas in Danish waters have been designated for offshore wind but have not yet been preliminarily assessed or included in development planning. The process is described in more detail below.

Before a tender is issued, the DEA, through the Danish TSO Energinet, undertakes preliminary site investigations, including assessments of wind resources, seabed conditions and environmental factors such as marine mammals, birds, fish and fisheries for inclusion in the subsequent Environmental Impact Assessment (EIA). In addition, a Strategic Environmental Assessment (SEA) is conducted, covering potential environmental impacts at planning level (e.g. effects on marine biodiversity, fisheries, bird migration and ecosystems). The results from both the SEA and preliminary site investigations are made available to potential bidders in the tender.

The Danish TSO, Energinet, also prepares a potential point of grid connection onshore to be ready in time for the future wind farm owner, should they choose to connect the wind farm to the grid. The early preparation of the grid connection is intended to enable the developer to commission the wind farm in time to meet the deadline for completion of the facility. As part of this process, Energinet conducts an EIA of the onshore project, of both the point of connections (PoCs) that Energinet will own and operate, and the future wind farm owner’s portion of the onshore transmissions facilities for exporting the electricity from the offshore wind farm to the national electricity grid.

Preliminary site investigations are generally launched as soon as possible after the political decision designating the site or sites to be included in a new tender. The investigations are then conducted simultaneously with the preparation of the tender, with data and results published continuously once available. While every effort is made to finalise and make these available before the bid deadline, due to the timeline of the tender process, some results from the preliminary site investigations may only be available after the bid deadline.

The 2024 tender consists of open procedures, where any interested economic operator who can comply with the minimum requirements may submit a tender, meaning that the tenderers’ financial and technical capabilities are assessed after the tender submission deadline. Before the tender is issued, the DEA conducts market dialogues with potential bidders and developers to collect feedback that may lead to adjustments in the final tender material.

After the final tender materials have been published, the potential bidders can still ask clarifying questions (Q&A) until relatively close to the bid deadline, but no major changes will be made after publication.

Once the tender submission deadline has passed, the DEA reviews and evaluates the bids. Before the concession is formally awarded and signed, regulatory screenings in accordance with the FSR and FDI frameworks are carried out. Once this has happened, the successful bidder is granted the exclusive right to develop the offshore wind farm at the specified site. Concessionaires who choose to connect the offshore wind farm to the grid must enter into a grid connection agreement with Energinet. The grid connection agreement is a standalone agreement and not an integral part of the concession, but is provided to the potential bidders to inform them of the terms of the grid connection. The concession includes obligations relating to areas such as completion milestones, guarantees and sustainability.

Following the concession award, the developer must obtain three main licences:

- Preliminary Investigation Licence: Facilitates detailed site investigations and starts the EIA process. If the project has to undergo an EIA assessment, the developer must submit an EIA report prior to applying for the construction licence. The EIA report will be subject to a public hearing.

- Construction Licence: Permits the actual construction of the wind farm.

- Electricity Production Licence: Authorises operation and electricity generation.

After obtaining the necessary licences and approvals, the developer makes the final investment decision (FID) and secures financing for the project. This step involves finalising contracts with suppliers and contractors. Lastly, the developer proceeds with the construction of the offshore wind farm, adhering to the approved project plan, the construction licence including any terms stemming from the EIA and other regulatory requirements. On completion, the wind farm undergoes testing and commissioning before commencing commercial operation.

Textbox 3.1: Recent tenders in Denmark

The tender round held in 2024 encompassed three offshore wind sites, each with 1 GW capacity (Nordsøen I A1, A2 and A3). No form of subsidy was involved. In addition, the design included a state co-ownership of 20 per cent. The tender round closed in December 2024, after failing to attract any bids. Subsequently, the tender for the areas Kattegat (1 GW), Hesselø (0.8 GW) and Kriegers Flak II (1 GW), which was planned for April 2025, was cancelled.

In addition to the preparation of the 6 GW tenders, Germany and Denmark have entered into an Intergovernmental Agreement regarding the joint project relating to Bornholm Energy Island, involving a minimum deployment of 3 GW in the Danish Baltic Sea. This was the first legally binding cooperation agreement in Europe regulating the sharing of renewable energy target amounts. Following the zero-bid outcome of the Nordsøen I tender, the Danish government advised the parties to the political agreement that the legal framework for implementing the next phase of the Bornholm Energy Island project was not yet in place.

Barriers

Auction design

In Denmark, rights to build an offshore wind farm are awarded through a competitive tendering procedure. Following an attractive 2021 tender round for the Thor area that resulted in negative pricing, the Danish Energy Agency (DEA) revised the tender design. Combined with challenging market conditions, this led to no bids being submitted in 2024. The tender design resulted in higher uncertainty and an overall high investment risk due to various elements, including:

- A market-based revenue model offering no guaranteed revenue

- Uncapped negative bidding, where the developer pays for the right to build the wind farm

- Developer responsibility for grid connection and the costs for such

- A mandatory 20 per cent state co-ownership in each project

- Developer management of permitting and project-specific studies

The DEA held separate meetings with 17 companies following the failure to attract any bids for the three offshore wind farms with a combined capacity of 3 GW in the North Sea

Danish Energy Agency (2025). Summary of market dialogue on 3 GW offshore wind in the North Sea.

Key proposals from market participants to increase the attractiveness and competitiveness of the tender process included:

- Adopt a two-sided Contract for Difference (CfD): Such a model would give developers financial support when market prices fall below the agreed benchmark, while paying the state when prices exceed it. This arrangement provides revenue stability and mitigates market price fluctuations.

- Reduce and reallocate preliminary investigation costs: High upfront costs relating to environmental surveys, military radar adjustments and grid connection are considered a significant burden. Proposals to tackle the cost challenges include government subsidies, spreading costs across the project period and granting developers the flexibility to conduct their own surveys to reduce costs.

- Revenue and risk considerations: Developers expressed concerns about low and volatile electricity prices in Denmark. Overplanting could lead to more instances of surplus energy production during low-demand periods, further depressing revenues and increasing financial risks for developers. However, without a supportive framework, overplanting might induce CAPEX/OPEX increases without assured returns.

- Simplify and reduce project costs through targeted support: In addition to CfDs, some developers highlighted that state funding of export cables or reductions in other costs (e.g. guarantees, penalties and radar-related expenses) would render projects more financially viable.

- Address market risks and improve price dynamics: Suggestions include boosting electricity demand in Denmark and enabling better integration with neighbouring markets to expand sales opportunities.

- Develop the hydrogen market: Addressing uncertainties in hydrogen market infrastructure and regulations (e.g. export opportunities to Germany) could improve project feasibility.

The DEA reworked the tender design to avoid a further no-bid scenario. Brinckmann’s assessment of the failed 2024 tender prior to the 19 May 2025 agreement looked into the following key factors that could be considered to ensure a successful tender process

Brinckmann Report (2025). Assessment Of The Failed Offshore Wind Auction In Denmark.

- Adopt Contracts for Difference (CfDs): Provide developers with price guarantees, reducing exposure to volatile energy markets, similar to in the UK.

- Guaranteed floor prices: Establish minimum prices to enable developers to cover costs during periods of low electricity prices.

- Government-funded grid infrastructure: Transfer the responsibility for grid connections to the state or a state-owned operator.

- Cost-sharing model: Reduce the financial burden by splitting grid connection expenses between the state and developers, similar to in Germany.

- Make co-ownership optional: Give developers the choice, rather than require them, to include 20 per cent state ownership in their projects.

The 19 May 2025 political agreement addressed several of the above points by:

- introducing a support model with state-backed risk-sharing (CfDs)

- removing the requirement for state co-ownership

- introducing a new penalty regime including lower penalties for delays in the first two years, and the abolishment of double penalties

- stipulating requirements for sustainability and social responsibility (recyclable turbine blades)

- facilitating overplanting opportunities within two years of commissioning minimum capacity

- providing state support for preliminary studies and defence-related adjustments

Limited electricity demand

Current electricity demand in Denmark, and its projected growth, remain relatively limited compared to larger nations. Renewable energy sources currently generate more than 80 per cent of the country’s electricity.

Challenging market conditions have also impacted proposed hydrogen infrastructure projects such as constructing a hydrogen pipeline from Esbjerg to the German border. Danish hydrogen exports have been a key driver of offshore wind developments as Germany could be established as a novel off-taker. However, hydrogen infrastructure construction has faced significant delays, due to factors such as regulatory and demand uncertainties, permitting processes and challenges in coordinating investments across the hydrogen value chain.

Overall, there is no definitive approach to promoting offshore wind development or to determining how segments of Denmark’s offshore waters should be allocated for potential collaboration with neighbouring countries.

Environmental impact assessment processes

For every new offshore wind project, a separate Environmental Impact Assessment (EIA) must be undertaken by the developer. The EIA assesses the current state of the environment to evaluate the projects’ potential environmental impacts. If required, mitigation strategies are developed to ensure the offshore wind farm is developed sustainably while minimising negative environmental impacts. The Danish Environmental Protection Agency (EPA) and the DEA oversee and enforce EIA requirements for onshore and offshore projects, respectively. The following key challenges relating to the EIA process could potentially be improved to enhance offshore wind development in Denmark:

- Knowledge-sharing: Each new offshore wind project requires a separate Environmental Impact Assessment (EIA), based on the latest collected environmental data at the designated sites. One way in which efficiency could be improved is by highlighting available up-to-date studies and utilising real-world impact data from existing wind farms in close proximity to the planned project. Although EIAs must be based on the latest data, improving access to reusable datasets could increase process efficiency. Broader knowledge-sharing would also be beneficial, although existing data often does not sufficiently cover the specific project area.

- Interface of the SEA and EIA: The SEA is implemented before the tender bid deadline, in coordination with the overall maritime spatial plan and the planning of offshore wind leasing zones, while the EIA is carried out for a specific project. While both assessments fulfil their specific roles, industry experts suggested that they could be better aligned in order to reduce uncertainty and risk for developers. In particular, the SEA could define environmental mitigation measures at an earlier stage, so that developers know earlier in the process what they need to comply with.

3.2 Norway

Background

The Norwegian offshore wind market is relatively immature, with an installed capacity just short of 100 MW. So far, development has been restricted to demonstration and pilot projects using floating substructures. Norway’s focus on floating offshore wind reflects the country’s relatively limited access to suitable shallow waters. This submarket is regarded as strategically important to the transition of the conventional oil and gas industry, which has decades of experience in designing and constructing floating substructures. The MET Centre has hosted several test turbines, and in 2023, Hywind Tampen, the world’s largest floating offshore wind farm (88 MW), entered operation.

While deployment has been limited, the Norwegian government has set itself an ambitious long-term target of awarding a capacity of 30 GW by 2040. The country’s first large-scale tender was completed in 2024 for Sørlige Nordsjø II, with Ventyr (Parkwind and Ingka group) emerging as the successful bidder. Sørlige Nordsjø II is a bottom-fixed project located in the North Sea with a capacity of 1,500 MW. The government also started the tendering process for three floating wind projects, each with capacity of 500 MW, at Utsira Nord. The tender was delayed due to challenges with the ESA approval process, which were clarified in April 2025. Completion of Utsira Nord is now scheduled for 2025. Although three sites will still be awarded, only one project (500 MW) will receive financial support in the initial auction, mainly due to escalating costs. (The initial plan was to award support for all three projects.)

Procedural framework

The licensing process for commercial offshore wind in Norway follows the same procedure whether projects are located within or outside the baseline. However, for installations outside the baseline, the authorities’ decisions are made in accordance with the Offshore Energy Act (Havenergilova) and the Offshore Energy Regulations (Havenergilovforskrifta).

The baseline is defined as the line that follows the low-water mark along the coast of a state. You can find a map of the Norwegian baseline and offshore wind areas here

Source: Menon Economics

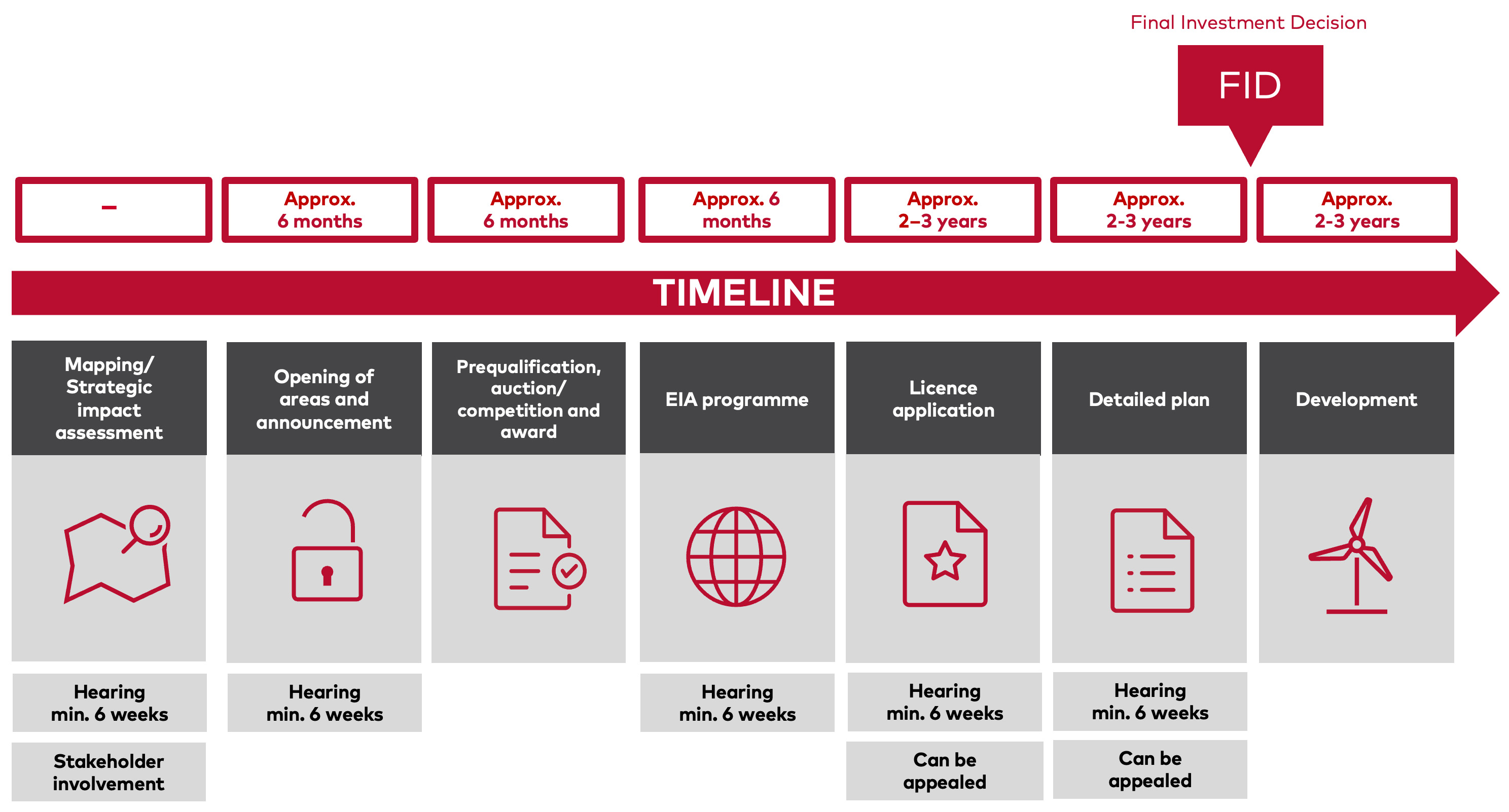

In the Norwegian system, the Norwegian Water Resources and Energy Directorate (NVE) first identifies areas suitable for offshore wind deployment. After that, NVE conducts a strategic impact assessment. This assessment includes a preliminary evaluation of the potential wind farms’ general and site-specific impacts. NVE also holds a dialogue with stakeholders. The goal of the strategic impact assessment is to provide a suitable basis for decision-making to determine whether it is acceptable to establish offshore wind in the relevant areas, considering environmental or other spatial and industry interests. The assessments also evaluate whether the areas are suitable for the establishment of offshore wind in light of prospects for profitable development, assessments of grid capacity and the need for any measures in the onshore grid. The assessment is conducted in cooperation with the Norwegian Offshore Directorate, the Directorate of Fisheries, the Norwegian Environment Agency, the Norwegian Coastal Administration, the Norwegian Defence Estates Agency, the Norwegian Water Resources and the Energy Directorate. Once the Ministry has decided which areas should be opened for development, the specific sites are then awarded through a competitive tender.

The Ministry can decide whether the tender should be awarded based on qualitative criteria or by auction, and whether participants need to prequalify to participate in the auction. Consequently, different types of competition may be used for different areas, as illustrated by Utsira Nord and Sørlige Nordsjø II, where the latter used prequalification before an auction was held.

The auction winner is awarded a time-limited exclusive right to carry out a project-specific impact assessment and apply for a licence. If the application is approved, developers can then make a final investment decision (FID)

However, developers prefer to make the FID with as much information as possible. Detailed planning therefore often takes place before the FID. The detailed plan includes developers finalising concepts and submitting a detailed plan, outlining construction, transport and design specifications. Once the detailed plan has been approved and any appeals settled, construction can begin. The process includes five rounds of public hearings, which allows stakeholders to provide input. Additionally, both the licence award and the decision on the detailed plan can be appealed. Appeals against the licence award can potentially stop the whole development, whereas appeals against the detailed plan cannot overturn project approval, but may cause delays should additional information be required.

The timing of the FID varies among developers. According to our interviewees, the investment decision should be made after the licence has been granted, but before submitting a proposal for the detailed plan. Typically, an offshore wind developer prefers to delay the FID as much as possible. However, because the detailed plan must contain information that only becomes available once the FID has been completed, the FID must therefore be finalised before the detailed plan is submitted.

However, developers prefer to make the FID with as much information as possible. Detailed planning therefore often takes place before the FID. The detailed plan includes developers finalising concepts and submitting a detailed plan, outlining construction, transport and design specifications. Once the detailed plan has been approved and any appeals settled, construction can begin. The process includes five rounds of public hearings, which allows stakeholders to provide input. Additionally, both the licence award and the decision on the detailed plan can be appealed. Appeals against the licence award can potentially stop the whole development, whereas appeals against the detailed plan cannot overturn project approval, but may cause delays should additional information be required.

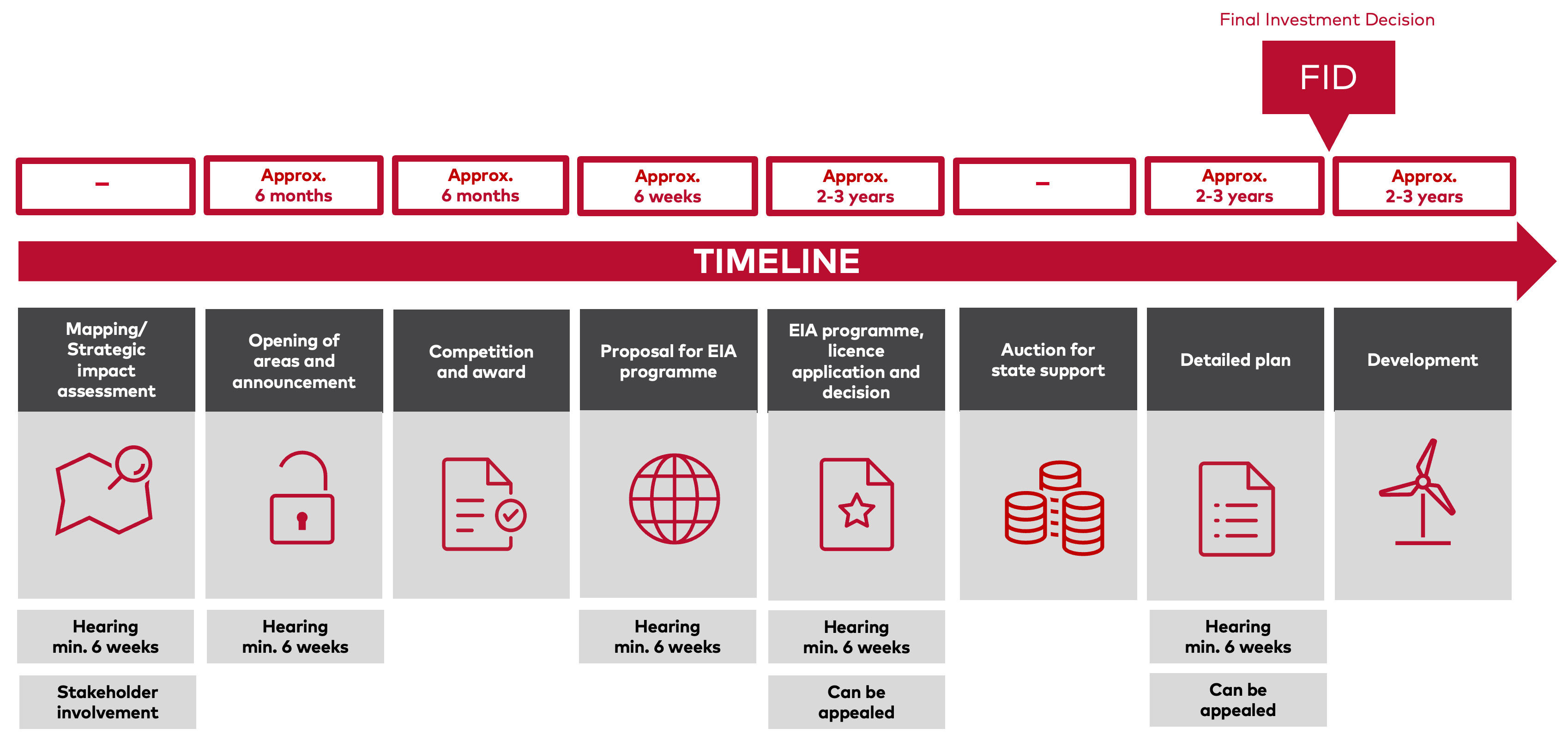

The proposed model for floating offshore wind in Utsira Nord is based on a two-stage model, where a competition for the right to develop specific sites is held first, based on qualitative criteria (see Figure 3.4). Up to three applicants will be awarded rights to one project area each: the highest-ranked “bidder” chooses first, the second-ranked chooses next, and the third is awarded the remaining area. Each winner must then propose and carry out an environmental impact assessment (EIA) for their project area and submit a concession application. Only projects with an approved concession application are eligible to compete in a subsequent auction for financial support, which is conducted as a sealed-bid process. In this auction, companies bid for the amount of state aid they require, and the project offering the lowest support per MW of installed capacity will be awarded the funding.

Source: Menon Economics, based on data from the Norwegian Ministry of Energy

With regard to support schemes for SN II, the government has decided to use Contracts-for-Difference

The Hywind Tampen offshore wind farm was developed to power offshore infrastructure with no cable to shore and was consequently developed in accordance with oil and gas legislation and attracted tax allowances of 78 per cent under the Norwegian oil and gas resource rent tax regime.

Exemptions from the overarching regulations

While the general rule of the Offshore Energy Act (OEA) is that areas must have been opened for offshore wind development before licence applications can be considered, some exemptions are permitted. In “special cases”, the Ministry can bypass the opening process, allowing projects to proceed directly to a project-specific impact assessment and licence application, in a kind of “open door” approach. This exemption is currently under consideration for GoliatVind, which has been characterised as a “fast-track” licensing project.

The decision on the exemption will be made together with the decision on the licence.

The Offshore Energy Act (OEA) also permits the detailed plan to be bypassed in “special cases”, for instance where the licence application contains sufficient details about the project.

Barriers

The main identified barriers to accelerating offshore wind development in Norway relate to the tender design and profitability under the current support scheme, long-term political uncertainty, procedural misalignment and inadequate data availability and sharing.

Tender and support design

Our interviewees highlighted the political uncertainty associated with offshore wind projects in Norway as a main barrier to accelerating the development of offshore wind. To counteract the lack of profitability, the Norwegian government has introduced a support scheme based on Contracts-for-Difference, which is intended to increase the projects’ profitability and mitigate the financial risks involved. However, the proposed support schemes for Sørlige Nordsjø II and Utsira Nord had to be approved by the ESA to ensure they complied with EU state aid rules. This process took longer for Sørlige Nordsjø II than initially anticipated, leading to development delays. Utsira Nord (FOW) initially planned to award areas in 2023 but did not receive ESA approval until April 2025. This led to several developers withdrawing early from the competition, as the prevailing uncertainty substantially increased project-specific risk.

Industry actors also point to the design of the support scheme itself. Norwegian CfDs include a cap on the total amount of government support available over the contract duration. Several industry stakeholders have noted that this limit creates uncertainty regarding revenue streams after the cap has been reached. This mirrors the findings in Menon Economics (2022) study on support design for offshore wind. Furthermore, as the CfD remains in force, concluding a Power Purchase Agreement (PPA) after contract signing becomes problematic, since prices above the strike price could require payments to both the government and the PPA buyer for the duration of the agreement.

It is important to note that the uncertainty surrounding the tender process should be mitigated for fixed-bottom installations and could be mitigated for floating offshore wind once the ESA process has been completed. This barrier should therefore be viewed as temporary.

Political uncertainty

The Norwegian offshore wind market is also exposed to political risk, in both the short and long term. Public sentiment towards offshore wind has taken a negative turn, increasing political risk. In early September 2024, the floating offshore wind project Green Volt off the coast of Scotland acquired a CfD from the British government at a strike price of around 27o øre/kWh.

This corresponds to a Levelised Cost of Energy (LCOE) of about 210–230 øre/kWh

This estimate is based on calculated expected revenue streams per kWh production. We assume an electricity price in the UK of 103 øre/kWh in 2030, 77 øre/kWh in 2040 and 70 øre/kWh in 2050. We also assume a discount rate of 6 per cent, a lifetime of 30 years, and 4,752 hours of full-capacity production per year. The capacity is 400 MW. Under these assumptions, the wind farm’s income is 220 øre/kWh. To reach break-even, the LCOE cannot be higher than the expected income per kWh. Given the uncertainty of several parameters (e.g. future electricity prices), a LCOE of around 210–230 øre/kWh seems reasonable.

The short-term consequence of the cost increase, and the dwindling political support, are reflected in the tender design itself. For Utsira Nord, the government initially wanted to award financial support for three projects. Initially, the number of projects was reduced to two, a modification that could be interpreted as a design adjustment intended to ensure sufficient competition in the auction process

If all three sites were to receive financial support, the support would have to be granted based on a bilateral negotiation.

Some developers have expressed concerns that they might not be able to reuse their applications if they lose a tender, as the terms and conditions for upcoming tenders have not yet been settled (irrespective of the ESA process). For instance, much of the work would need to be redone to submit a new application, which would be a costly process that adds uncertainty and risk. Moreover, both the timing and the amount of any potential award remain unclear. This uncertainty diminishes the value of the bidder’s exclusive, site-specific development right, even if the bidder does not win the auction. In this way, short-term risks extend into the long term.

Increased risk with regard to long-term deployment also reduces the profitability of investments in the value chain. This barrier is especially important for floating offshore wind (Menon 2022/2024).

Textbox 3.2: Market-related barriers to offshore wind in Norway

Several interviewees cite a potential scarcity of vessels, as well as bottlenecks in the supply chain of floating wind turbines, as important barriers to the deployment of offshore wind in Norway. The scarcity of vessels relates both to installation vessels for construction and vessels for conducting environmental impact assessments (EIA). Furthermore, there is a shortage of floating wind turbine suppliers in Europe. These turbines must withstand greater movement than bottom-fixed models and require R&D investment to be fully developed. However, uncertainty about the future market for floating offshore wind farms in Europe makes such investments in supply chain capacity unattractive for turbine manufacturers. Relying on suppliers outside Europe is risky for offshore wind developers due to geopolitical concerns.

Procedural barriers

The process of obtaining all the required licences for developing an offshore wind farm is considered somewhat cumbersome, involving problems relating to several of the steps shown in Figure 3.3, and in particular grid connection and stakeholder involvement. While the NVE has proposed several adjustments to address many of the barriers mentioned in this section, we feel it important to highlight the impact of these barriers.

Firstly, the processes for obtaining a licence for grid connection and a licence for operating the wind farm are somewhat misaligned. For example, the location of the grid connection is not determined at the time of the tender. Additionally, Statnett and the developers’ responsibilities are not clearly delineated. Statnett, as a transmission system operator, is not responsible for developing radial connections to offshore wind farms. As a result, developers must submit a separate licence application for grid connection when they submit a licence application for their wind farm. Finding the right route for the subsea cable and obtaining a licence for this is a time-consuming process, involving many uncertainties. The related risk is borne by the developer and many interviewees cited grid connection as the biggest uncertainty in the process.

Furthermore, our interviewees highlighted the chronological sequencing of different steps as a problem. This issue primarily concerns the detailed plan, which is expected to include information that becomes available only after the final investment decision (FID), for example, details about specific turbine models. From a company’s perspective, it would be ideal to take the FID after the detailed plan has been accepted and potential appeals have been reviewed. This entails a significantly higher level of risk at the FID stage, reducing investors’ willingness to proceed with wind farm construction and potentially slowing overall development.

Moreover, the project-specific EIA is conducted at a relatively late stage when limited data for the area is available. Several interviewees from different backgrounds pointed out that they would have liked more information to be collected and assessed as part of NVE’s strategic impact assessment. Having more information at an earlier stage would facilitate more detailed planning and reduce developer risk. With the lack of knowledge about local conditions, the risk of conducting the wrong type of assessments and encountering unexpected issues is higher. This could delay development and, in the worst case, discourage developers from submitting applications. Gaining more knowledge at an earlier stage would reduce the project’s risk profile during the competition, thereby lowering the level of support required to secure adequate funding. However, collecting more data at an earlier stage entails higher costs, which must either be borne by the government or shared with prospective developers.

Another element that could delay the process is the extensive involvement of the public through five rounds of public hearings with two possibilities to appeal decisions. In particular, the public hearing of the detailed plan, and the possibility of appeals, is expected to pose a barrier due to the associated risk of delays. By this stage, the project should have gained sufficient acceptance from all stakeholders to render this round redundant. In Norway, the involvement of different authorities in the licensing process can also lead to delays in the process. Streamlining this process is regarded by the EU (and in RED III) as important to accelerate the processes.

3.3 Sweden

Background

Sweden currently has four offshore wind power farms, comprising 79 fixed-bottom turbines with a total installed effect of 190 MW. This includes Lillgrund (110 MW), Kårehamn (48 MW) and Bockstigen (2.75 MW), as well as Vänern (30 MW), located in a lake. Four other offshore projects have received valid permits. The Swedish government has set a planning target for the national electricity system, aiming to meet a demand of at least 300 TWh by 2045.

The Swedish Agency for Marine and Water Management recently published new marine plans in Sweden. This work was carried out in collaboration with several directorates. The new marine plans identify areas suitable for offshore wind and indicate a potential for a total of 120 TWh in Sweden. However, this does not represent a national offshore wind target.

In late 2024 and early 2025, the Swedish government carried out a substantial amount of work relating to offshore wind power. SOU (2024:89) aims to propose a more efficient and transparent system for environmental assessment of offshore wind power. The report recommends that Sweden establish an auction system where the government designates feasible, exclusive areas for offshore wind power. The proposal has been referred for consultation, and further work is currently ongoing within the Government Offices of Sweden. The Swedish Agency for Marine and Water Management, together with other authorities, has developed proposals for new marine plans. These plans identify suitable areas with an additional electricity production potential of 90 TWh compared with the current marine plans. SOU (2024:98) proposes measures to simplify and shorten the licensing process under the Environmental Code by making assessments more flexible, efficient and predictable. The changes are expected to be implemented in 2027/2028.

The reports mentioned above are motivated by the need for more efficient planning processes to fuel the green transition and to implement new EU directives (see chapter 2). Handling will take time, and the outcome remains uncertain. In the following, we base our analysis on the current approval situation in Sweden.

Procedural framework

The overall licensing process for offshore wind power in Sweden is quite similar to the licensing process for onshore power. The process is initiated and led by the developer and as such differs from in the other Nordic countries. There are certain differences between the licensing process for projects in territorial waters (within 12 nautical miles, or approximately 22 km from the coast) and those in the Swedish Exclusive Economic Zone (12–200 nautical miles, or up to about 370 km offshore). The main aspects of the processes are summarised in Figure 3.5 and Figure 3.6. However, the greatest differences primarily concern which stakeholders hold decision-making authority at the various stages.

Territorial waters

The licensing process for wind farms within territorial waters is based on the same legislation as for onshore wind and is conducted according to the Environmental Code. However, several other pieces of legislation must be followed, and the developer must obtain several permits throughout the process.

The Environmental Code regulates environmental protection and the management of natural resources in Sweden. The law aims to promote sustainable development by protecting people and the environment from harm and preserving biological diversity, and covers areas such as nature conservation, water management, noise pollution and industry plans.

In an offshore wind project, the developer initiates the process by independently identifying suitable areas for development. This process takes place in close consultation with authorities, mainly the municipality. A central element of this process involves determining whether the project will have significant environmental impacts. The municipality holds the right of veto and therefore wields considerable influence over the project throughout the licensing process. This approach is similar to that used for onshore wind power.

If the seabed in the relevant area has not been previously explored, a separate permit for seabed exploration is required under the Continental Shelf Act

If the municipality supports the project, the developer can submit a licence application to the Land and Environment Court (Mark- och miljödomstolen). An application must include the consultation report and an environmental impact assessment. The Land and Environment Court processes the licence application and sends it for public hearing. The licensing process may lead to requirements for additional studies and can impose various conditions on the project. The decision can be appealed, initially to the Land and Environment Court of Appeal, and subsequently to the Supreme Court. If the project is granted a final licence, it must still go through a stage of detailed planning and a final investment decision before construction of the wind farm can begin. In connection with the licence application, the developer must secure access to the water area and obtain permission for water activities. In addition, a separate process is required to acquire an electricity grid licence and approval to install seabed cables. It is also important to note that Sweden currently has no subsidy scheme for offshore wind power. Whether and when such financial support will be made available is uncertain.

Swedish Exclusive Economic Zone (SEZ)

The licensing process for wind farms in the Swedish Exclusive Economic Zone is conducted according to the Act on Sweden’s Exclusive Economic Zone. The steps of the process align well with those for territorial waters; however, other key stakeholders and different actors are responsible for licence evaluation.

Compared with projects in territorial waters, municipalities have less influence and no power of veto. The Government Offices of Sweden are responsible for evaluating licence applications within the Swedish Exclusive Economic Zone. The County Administrative Board is typically asked to conduct the public hearing and prepare a draft decision, but the Government Offices make the final decision. In the event of an appeal, the Supreme Administrative Court is the appellate body. As with territorial waters, there is a separate process for grid connection.

Barriers

Developer-led processes

The developer-led process in Sweden facilitates market entry but also requires developers to invest significant time and resources during the early stages of a project. Close dialogue with the authorities in the early stages of the process is expected to guide developers toward the most suitable areas for deployment. However, developers bear considerable financial risk, an issue that is highlighted below in relation to municipal power of veto and potential conflicts with defence interests.

Municipal veto

Since 2019, 40 per cent of Swedish offshore wind projects have been stopped due to municipal vetoes.

The municipality’s stance on offshore wind is closely linked to the population’s attitudes. Our understanding is that there is significant opposition to offshore wind development among the Swedish population. The fishing industry, as a strong stakeholder, is clearly opposed to offshore wind development and effectively communicates its concerns. Offshore wind power imposes restrictions on industrial trawling in the affected areas. Impacts on biodiversity, with a focus on porpoises and certain migratory birds, are other important counter-interests against offshore wind that receive public attention. Although there are both benefits and drawbacks to offshore wind development and fishery activities, it appears reasonable to assume that the prevailing opposition to offshore wind is influencing the municipalities’ perspectives.

The municipalities’ limited incentives to approve offshore wind power deployment in coastal areas have reinforced the NIMBY effect.

Swedish defence interests

In November 2024, the Swedish Government announced its decisions for 14 offshore wind applications.

The Armed Forces take part in the initial consultation process when developers assess potential areas for offshore wind power within the Exclusive Economic Zone. In consideration of the security policy situation, and to avoid disclosing security information, the Armed Forces are cautious in their statements. The handling of cases within the Swedish Armed Forces can take considerable time, sometimes up to a year, and developers often find it difficult to anticipate the outcome. This causes risk for developers and represents a barrier to wind power development, but could be resolved through a more centralised site allocation system.

Grid connection

In an auction-based offshore wind system with pre-defined development areas, the strategic assessment often involves outlining where the power can be fed into the grid. In Sweden, offshore wind developers can apply to develop wind power anywhere, and there is no systematic plan with regard to allocation of grid capacity. Additionally, recent governments have emitted varying signals regarding who should bear the costs of the grid connection. The previous government had a policy in place requiring the state to finance the land connection, but the current government has repealed it. That was the main reason cited by Vattenfall for its decision to pause the Swedish Krieger Flak project at a very late stage in preparations due to a current lack of profitability. Developers therefore face significant uncertainty regarding the location and timing of potential connection points, and the share of the grid costs that the project will have to cover. It is estimated that grid costs can constitute about one-sixth to one-third of the total costs of an offshore wind project.

Political uncertainty

Different governments have shown different ambitions and degrees of willingness to invest in grid connections and offshore wind in general, albeit without making a clear commitment. As such, Sweden still lacks specific targets for offshore wind development.

Data availability and sharing

Under the developer-led, open-door process in Sweden, developers can plan projects where they want and different developers can investigate the same areas for offshore wind deployment. This means that seabed exploration and data collection are financed by the developer and data sharing between competitors is not rational. Additionally, collecting, storing and sharing of bathymetry data in the territorial waters are generally forbidden due to security aspects. The licence application must be made public, but the data submitted to the authorities does not have to be disclosed. This results in less cross-learning among companies and data costs being higher than they could be.

3.4 Finland

Background

Finland currently has one offshore wind farm in Pori, comprising 11 fixed-bottom turbines.

Renewables Finland. Offshore wind power. Available here.

The Ministry of Economic Affairs and Employment (2024). New coordination group to intensify national cooperation in promotion of offshore wind power. Available here.

An overview of the action plan and measures proposed by the working group can be found here.

Procedural framework

The licensing procedures differ between territorial waters and the EEZ. In the following sections we provide a brief overview of the process, before we discuss the main barriers to deploying offshore wind in Finland.

Territorial waters

There are two key stakeholders involved in the development in territorial waters: Metsähallitus and the municipalities. The municipalities are the spatial planning authorities, who play a similar role to in onshore land areas and facilitate wind power development in their regions through maritime spatial planning and building permits. Metsähallitus manages all government-owned sea (and land) areas, and is generally the landowner in the territorial waters, and leases state-owned areas to developers.

Initially, feasibility studies and exploration are conducted to identify suitable sites for wind power in territorial waters, taking into account wind and seabed conditions while avoiding conflicts with other interests. In areas it owns, Metsähallitus conducts the initial surveys and identifies suitable locations in collaboration with the municipalities.

Metsähallitus. Offshore wind power is a decade-long project. Available here.

Metsähallitus. Our offshore projects. Available here.

All wind turbines exceeding a total height of 50 metres require approval from the Finnish Defence Forces before the wind power project can proceed. In practice, this means that all industrial-sized wind farms always require such approval.

Metsähallitus. Offshore wind power is a decade-long project. Available here.

After suitable areas have been identified and a developer has been awarded the tender for the area by Metsähallitus (or other landowners), and received approval from the Finnish Defence Forces, they can begin work on the Environmental Impact Assessment (EIA) and Master Plan. These are often developed simultaneously. The developer must contact the ELY Centre to determine if the EIA procedure is required and, if necessary, initiate the EIA process.

Required for projects comprising more than ten turbines or 45 MW. The ELY Centre may also require EIA for smaller projects in sensitive environments or with similar impacts.

In the final phase of the licensing process, the developer must obtain several remaining permits.

An environmental permit is not usually required from the municipality’s environmental inspector, unless hydrogen production is being constructed in connection with the wind farm.

Renewables Finland. Permitting process. Available here.

In the same way as the power line permit for constructing the offshore substation, the submarine cable and the onshore connection cable.

Exclusive Economic Zone

The licensing process for offshore wind in Finland’s Exclusive Economic Zone has recently changed following the introduction of the new Act on Offshore Wind Power in the Exclusive Economic Zone from 1 January 2025.

The Ministry of Economic Affairs and Employment (2024). Act on Offshore Wind Power in the Exclusive Economic Zone enters into force – First tenders could be organised at the end of 2025. Available here.

Details regarding which areas will be opened up to tender and how they are identified are still being finalised, along with the criteria for selecting the tender winners. The government aims to select the first areas for tendering in the autumn of 2025.

The exploration and utilisation permit grants rights to utilise the area for a specified period. The duration of this period has not yet been determined, but this is crucial as it forces developers to proceed with projects. A time-limited permit ensures that developers do not sit on project rights while waiting for higher electricity prices or lower construction costs, a practice that could slow the pace of offshore wind development. Additionally, if the winner of the tendering process chooses to not apply for an exploitation and utilisation permit, the second-best tenderer will be allowed to apply immediately. This allows for quicker project development compared to restarting the tendering process from scratch, should the winner decide not to explore or develop the area.

In addition, the rule limiting a single bidder to winning only one area, even when multiple areas are tendered simultaneously, has been removed.

The new tendering process will not only accelerate development due to the limited duration of exclusive rights but will also reduce the financial risk for developers. With exclusive rights, they can invest in exploration without the risk of competitors pre-emptively developing the area if it proves economically viable. Under the previous system, the legislation allowed several exploration permits to be granted for the same area, without giving priority to the entity that carried out the investigations for project development. This could lead to complications if the area was suitable for offshore wind and the project was financially viable.

An exploitation permit alone does not guarantee that the project will be implemented, as this requires additional permits. This includes obtaining a water permit from the Regional State Administrative Agencies (AVI) for the use of the water. The developer is also required to carry out an Environmental Impact Assessment (EIA) for the wind power project, which must receive government approval. If the project has cross-border effects, it must follow the procedure set out in the Convention on Environmental Impact Assessment in a Transboundary Context. Under the Territorial Surveillance Act, a permit for exploration and surveys from the Finnish Defence Forces is generally not required for projects located in the Exclusive Economic Zone. However, a permit is required to run cables through territorial waters.

The Finnish Defence Forces also provide their assessment of the project’s suitability to the government when multiple areas are being considered for exploitation and utilisation permits.

Once all necessary permits have been obtained, the developer can start project development. See the figure below for an overview of the licensing process for offshore wind in Finland’s Exclusive Economic Zone. It is important to note that Finland has not established a financial support mechanism for offshore wind. As such, even projects that are regarded as mature with regard to the licensing process could face significant risk in terms of financial profitability. The latter is discussed in more detail below.

This figure is somewhat uncertain due to ongoing changes in the licensing procedure.

Barriers

Profitability

A primary barrier to expanding offshore wind energy in Finland is the lack of profitability. High development costs and low electricity prices make it difficult to secure profitable projects. Unlike some other markets, Finland has no government support schemes such as Contracts for Difference (CfDs), leaving developers to shoulder most of the risk in achieving profitability. Financing for such projects typically relies on securing Power Purchase Agreements (PPAs). However, securing these agreements can be challenging. Additionally, the long development timelines create significant uncertainty regarding electricity prices when the wind farm becomes operational.

Grid connection

A significant barrier cited by many stakeholders is grid connection, which often creates a bottleneck in projects and hinders their realisation. The grid connection process is not integrated into the licensing process for offshore wind, which can lead to several practical issues. Grid connection is not guaranteed, even if an operator wins a tendering process for an area, either within territorial waters or the EEZ. Grid connection is crucial for the project’s feasibility, and clarifications regarding grid connection should be made as early as possible to ensure that the project is viable in practice. In Finland, however, grid connection is resolved at the end of the process when all other elements are in place. This creates significant uncertainty for developers with regard to cost and project progress.

Fingrid

A Finnish limited company that operates the transmission network in Finland. The Finnish state is the majority owner of the company.

Finnish Defence interests

Wind turbines taller than 50 metres require approval from the Finnish Defence Forces and TUVE

Government Security Network.

Finish Defence Forces. Available here.

Renewables Finland. Available here.

The regulatory framework does not accommodate specific offshore wind needs

The current licensing process consists of a broad spectrum of laws and regulations that apply to offshore wind development, without a well-conceived process for the development. This can result in unnecessarily lengthy processes and increased risk for developers. This issue has been partially improved by the new tendering process in the EEZ; however, some parts of the process for offshore wind have still not been streamlined, such as obtaining a water permit. The Water Act was drafted before offshore wind development was feasible in Finland. Stakeholders believe that adapting and streamlining this permit would offer significant benefits in terms of accelerating offshore wind projects. Finland’s offshore wind working group has proposed aligning the water permit process with the rest of the permitting procedure.

Some stakeholders we have spoken to also point out that having different processes for territorial waters and the EEZ is unfortunate, especially given the somewhat limited offshore wind potential. This results in numerous governmental authorities working on the same challenges independently, leading to fragmented expertise and inefficient management.

Lack of data sharing

To identify areas best suited for offshore wind and develop projects that do not conflict with other interests, it is essential to map maritime wildlife, other business interests and seabed conditions. In Finland, authorities conduct limited surveys before areas are tendered in the EEZ but more extensive surveys in the territorial waters, which means the majority of exploration and surveys are carried out by the companies in the EEZ. Some stakeholders state that this leaves companies with limited knowledge of the areas they are bidding for, increasing their exposure to risk if the sites later prove unsuitable for offshore wind development. In territorial waters, Metsähallitus conducts more comprehensive assessments before auctioning areas. It also shares this data with all interested parties considering bidding for the area. This approach reduces risk for developers, as they have more information, and prevents duplication of effort in conducting assessments.

Under the previous process in the EEZ (prior to the new tendering process), multiple companies surveyed the same areas at the same time. The lack of exclusivity over areas results in less data sharing and duplicate exploration efforts. This increases financial risk for developers and reduces data sharing. The stakeholders report that the introduction of exclusivity over areas does not necessarily lead to increased data sharing. The reason is that companies have no incentive to share data.

Practical challenges

Some practical challenges pose barriers to deploying offshore wind energy in Finland. One issue is that Finnish sea areas often freeze during the winter months. This situation complicates the construction of offshore wind farms and renders floating wind solutions almost impossible to implement. The reliance on bottom-fixed installations presents a further challenge, as many areas, especially within the EEZ, are too deep. Nevertheless, there are several locations that are suitable for the development of bottom-fixed offshore wind farms.

Another practical challenge that could impede the pace of offshore wind development in Finland is the height of the Øresund Bridge, which connects Denmark and Sweden. All vessels heading to Finnish territorial waters and the EEZ must pass under this bridge. The problem arises because wind turbine installation vessels are typically very tall, as they require high cranes for turbine installation. Some of the vessels are too large to pass under the Øresund Bridge, which reduces their availability and may lead to increased waiting times. This situation could create a bottleneck, particularly since next-generation offshore wind turbines are generally taller, necessitating vessels with even higher cranes. Recent studies indicate that only 4 out of 44 installation vessels are too large to navigate under the bridge,

Wind Europe (2022). Offshore wind vessel availability until 2030: Baltic Sea and Polish perspective. Available here.

Textbox 3.3: Factors accelerating the development of offshore wind in Finland

While we identify a number of barriers to the development of offshore wind in Finland, we also recognise factors that help accelerate this development.

Municipal property tax: In Finland’s territorial waters, municipalities hold significant authority in the licensing process for offshore wind projects, as they are the planning authority and in charge of spatial planning in their areas. Wind power installations, both onshore and offshore, pay property taxes to the municipalities. Property tax revenue can be a substantial incentive to accelerate development within the territorial waters. Consequently, offshore wind projects encounter little local opposition, as some of the revenue from the power plants benefits the municipalities. However, there have been discussions about redistributing these funds among municipalities, which could diminish the local incentive to develop wind power.

New tendering process for exclusive rights in the EEZ: The new licensing system in the EEZ introduces a tendering process granting exclusive rights to apply for exploration permits and subsequent development, thereby speeding up project progress compared with the previous system. Firstly, exclusivity over areas reduces financial risk for developers during exploration and development. Secondly, allowing the second applicant to apply for an exploration permit if the first does not, enables another entity to immediately exploit the area without needing to restart the entire process. Thirdly, the time limitation on exclusive rights prevents developers from holding onto the rights while waiting for higher electricity prices and lower development costs, requiring them to proceed with construction once they have the rights. Fourthly, authorities will likely select areas where development is less likely to conflict with other interests, increasing the likelihood that developers will obtain other necessary permits, such as water permits or approval from the Defence Forces. It is, however, still unknown how the areas designated for tendering will be selected and to what extent the authorities will survey these areas, as well as the degree to which they will coordinate with other interests.rway.

3.5 Iceland

Background

Iceland currently has no deployed offshore wind farms. Historically, the abundance of geothermal and hydropower has been more than sufficient to meet the country’s energy needs. Hydropower generates approximately 70 per cent of the country’s electricity needs, with the remaining 30 per cent generated by geothermal power plants (IRENA, 2024). In the future, Iceland expects a significant increase in demand for electricity due to the decarbonisation of road transport, shipping and fishing vessels, as well as growth in power-intensive industries like data centres. The extra supply of electricity is expected to primarily come from wind and geothermal sources, and to a lesser extent from additional hydropower, given the smaller potential for further hydropower development (The National Regulatory Authority, 2024).

When it comes to offshore wind, there are currently no projects in the pipeline under review by the energy authorities. Iceland lacks a policy framework and specific legislation for offshore wind development, indicating that the country is still in a premature phase regarding this sector. However, the fact that several companies have expressed interest in developing offshore wind in Iceland suggests that such projects are likely to materialise in the country in the future. Iceland is currently developing an Energy Production strategy and roadmap which will presumably include all energy sources, including onshore and offshore wind.

Barriers

While laws and policies do not necessarily need to be established before the development of offshore wind, having them in place would greatly facilitate the process. Iceland’s experience with fish farming, which initially faced regulatory challenges similar to those expected for offshore wind, highlights the need for proactive planning. Strengthening preparedness for offshore wind development will help ensure that projects move forward responsibly, with fewer uncertainties, and may prevent time-consuming conflicts over environmental and resource management.

Electricity production licensing is covered by the Electricity Act. However, the legislation is not designed for offshore wind energy. If a developer wants to establish a project, the authorities would either have to use the existing legislation for onshore wind, with expanded scope to include offshore wind, or develop new legislation specifically applicable to offshore wind. It can be assumed that developers would have to complete an Environmental Impact Assessment (EIA). Based on experience from onshore wind development, this can be a lengthy process involving public consultation. Although some streamlining has been achieved, for instance by removing duplicate elements, there is still room to further speed up the process without compromising quality. Currently, the existing EIA process would likely also apply to offshore wind projects, while the licensing process requires further development.

Connecting offshore wind farms to the grid could also be a potential barrier. Challenges can arise because local authorities have their own construction and land-use plans for grid infrastructure, which historically required approval from each municipality affected by the grid. Efforts have been made to streamline this process with new planning laws to avoid the need for individual approvals from all municipalities. Despite working on simplifying the regulations to facilitate grid expansion, it is currently unclear if these challenges have been fully resolved.

3.5 Åland

Background

Åland does not yet have any offshore wind production but sees significant potential. The goal of the Sunnanvind project is to pave the way for offshore wind development through a series of preparatory measures. One of these is to spearhead efforts to develop regional development plans for sea areas on the northern side of Åland. In the first stages of the Sunnanvind project, the wind power areas south of Åland were highlighted as promising due to their high production potential. However, because of defence interests and security considerations, these areas were excluded from the Sunnanvind project pending changes in the geopolitical situation in the Baltic Sea. The area in the north currently covers 1,200 km², providing a potential production capacity of 3–4 GW, with estimated production in the range of 20 TWh. This represents roughly 65 times Åland’s current total electricity consumption, meaning that most of the output would need to find off-takers in neighbouring markets such as Finland or Sweden. One alternative could be supplying electricity to Åland itself if demand rises sharply, for example due to new hydrogen production facilities. During the current preparatory phase, the government is developing procedures for allocating sea areas for energy production and identifying sites suitable for offshore wind. The right to develop and build offshore wind farms will be awarded based on a market-based competitive auction process to be arranged by the government. The Sunnanvind project, with €2.7 million funding from the EU, will deliver its final report by 30 June 2026. The project is conducting an extensive environmental impact assessment of the regional plans, as required by legislation. Two private developers have investigated the seabed in areas identified in the Åland Maritime Spatial Plan.

Åland is an autonomous region of Finland with its own legislative powers in several areas relating to wind power and the associated licensing process. Of the authorities involved in the licensing process, some are local to Åland and some are national agencies. Åland follows a similar licensing process to the one used in Finnish territorial waters, but Åland has decision-making authority in areas where municipalities have jurisdiction in Finland, as well as in the legislative fields of environment and energy. Several municipalities in Åland have only a few hundred inhabitants, resulting in limited capacity and expertise to manage offshore wind issues. As part of the Sunnanvind project, the Åland government will prepare a comprehensive plan proposal, divided into six separate municipal plans to facilitate offshore wind development. While the Sunnavind project is developing the plan proposals for the municipalities, the municipalities will ultimately make the final decisions regarding adaptation of the plan for offshore wind in their jurisdictions.

Åland is subject to EU directives in the same way as Finland, as outlined in chapter 2. Finland has authority relating to areas such as maritime traffic, defence, aviation and seabed surveys. However, Åland is responsible for decisions concerning planning, administration, environmental assessments, construction law and maritime cultural heritage. Åland’s government has its own maritime plan that outlines the usage possibilities for the Åland public waters that are managed by the government. Private waters are excluded from the current maritime spatial plan. As part of the municipal plan proposal, initial overarching environmental assessments in the relevant areas are conducted by the government. More detailed environmental impact studies will be carried out by the offshore wind developer at a later stage, i.e. EIA assessment for projects to receive environmental permits and building permits.

The licensing process in Åland, which is illustrated in Figure 3.10, follows the Finnish model for territorial waters. However, although the procedural framework is in place, the initial environmental assessment and the identification of suitable areas have not yet been completed. An appeal in the master planning process could take up to three years to resolve in court.

Once the building application complies with the zoning regulations, the developer receives a building permit. A cable connection to shore is not included in the current plans. Cable permits require a separate environmental impact assessment, depending on whether the export cable is routed to Finland, Sweden or Åland. The Finnish TSO, Fingrid, has identified potential grid connection points for offshore wind from Åland, whereas no such points have yet been defined in Sweden. Consequently, the permitting timeline may vary depending on where the wind farm connects to the grid.

Barriers

We have identified two main barriers that increase risk with regard to progress, cost and local acceptance in Åland.

The first barrier relates to grid connection. Åland is an independent energy market, with grid connections to the mainland grid in Finland and to the SE3 price region in Sweden. Given the expected electricity production volume, the power will need to be exported either to Sweden or Finland. As several offshore wind projects in both countries also require grid connections, the availability of suitable connection capacity will need to be clarified. Åland has its own legislation for the electricity market and in addition to the technical solutions and availability, this legislation and that of mainland Finland may need to be adapted to handle the possible hybrid connection issues for the offshore wind farm(s).

Secondly, it is also worth noting that taxes generated from future wind farms go to Finland rather than Åland, which provides local incentives for acceptance. This approach is consistent with other forms of taxation on Åland; however, it may act as a barrier by offering limited incentives for offshore wind development in the region.

3.7 Faroe Islands

Background

The Faroe Islands currently do not have any offshore wind projects in operation. However, the country has gained relevant experience from building onshore wind farms that can also be applied to offshore wind development.

The Faroe Islands are a self-governing nation with extensive autonomous powers and responsibilities within the Kingdom of Denmark. The country has exclusive authority to legislate and govern independently in a wide range of areas. These include external trade relations, customs, taxation and financial policy, business regulation, management of fisheries and all other utilisation of natural resources, energy and the environment, the labour market, social security, emergency preparedness, education, research and culture.

Generally, offshore wind developers require three types of permits from the Environment Agency: a permit for the Environmental Impact Assessment (EIA), an environmental licence and an electricity production licence for the wind farm. These three permits are all obtained from the Faroese Environment Agency. The EIA and environmental licence are issued by the Department of Conservation, while the development licence is granted by the Department of Energy. The permitting process is coordinated between the two departments, with the Department of Energy acting as the primary point of contact.

The authorities have not yet designated specific areas for offshore wind deployment, unlike for onshore wind.

Barriers

We have identified a number of barriers that could potentially limit or slow down offshore wind development on the Faroe Islands: challenges include the timely completion of EIA studies (such as assessments of rare bird species), conflicting interests with fisheries, and potential appeals from the public, NGOs or other developers. The Parliamentary Act on Electricity and District Heating was amended in 2024, stipulating that a development licence cannot be tendered before the EIA has been approved. Previously, the licence could be tendered but not awarded prior to approval. These amendments ensure that assessments are carried out earlier in the process, thereby reducing the risk of conflicts at later stages.

3.8 Greenland

Greenland has no current wind projects, nor any in the pipeline. Some initiatives exist for land-based wind energy aimed at producing other green energy carriers (Galimova et al., 2024). However, no ambitions or initiatives have been identified for offshore wind energy. There are currently no government policies or designated areas supporting offshore wind development.

Textbox 3.4: The Net Zero Industry Act

Spatial data is essential for both optimising site selection and ensuring cost efficiency, technical feasibility and effective energy production, while minimising negative impacts in areas such as marine biodiversity. Nordic Energy Research (2023) highlights the importance of knowledge and data sharing (using reliable third parties) in order to accommodate other interests, in particular nature, but also fisheries, shipping, military activities, aquaculture and tourism. Data collection and analysis after deployment could also provide valuable insights for the industry and other stakeholders, e.g. with regard to turbine performance and bird observations (Kusiak 2016). With rapid advances in data processing and analysis, including the use of AI, the value of data is increasing as it provides a stronger foundation for informed decision-making.

Data collection is costly. Geophysical and geotechnical surveys require specialised vessels, dedicated equipment and skilled personnel. Resource and metocean assessments, in turn, depend on specialised sensors and extended data collection over time; while other environmental surveys and socioeconomic studies could require vessels, aircrafts and specialised personnel.

Sharing existing data across industry actors, government agencies and others could therefore potentially help reduce costs and accelerate projects. In interviews with industry actors and government agencies we have explored the extent of data sharing and to what degree lack of data sharing is a barrier to accelerated offshore wind deployment. In the following we summarise our findings, in general, and with regard to specific countries where relevant.

Several of our interviewees cite lack of data as a barrier to offshore wind deployment. There are platforms that gather and make data accessible, in particular Nordic Spatial and EMODnet, as well as country-specific data (e.g. Geonorge and the Offshore Directorate in Norway). Our understanding is that the data-sharing platforms themselves are adequate, but that there is insufficient underlying data. This may be due either to limited data collection or to restricted data sharing by industry or government actors. Examples of data sharing initiatives in Norway include:

- The hull-based surveys (MBES, backscatter and SBP) on Sørlige Nordsjø II and Utsira Nord have been made available via Kartverket in Norway.

- For the Sørlige Nordsjø II area, awarded to Ventyr Energi, all data has been made available via the Offshore Directorate’s Diskos database, except for magnetometer and water column data.

In Finland, the authorities conduct limited surveys before areas are tendered in the EEZ, but more extensive surveys in the territorial waters, which means the majority of exploration and surveys are carried out by the companies in the EEZ. Some stakeholders point out that this leads to companies having less knowledge about the areas they are bidding on, increasing their risk since the areas may turn out to be unsuitable for offshore wind for various reasons. In territorial waters, Metsähallitus conducts more comprehensive assessments before auctioning areas. It also shares this data with all parties interested in bidding for the area. This approach reduces risk for developers, as they have more information, and prevents duplication of effort in conducting assessments.

Under the previous process in the EEZ (prior to the new tendering process), multiple companies surveyed the same areas at the same time. The lack of exclusivity over areas results in less data sharing and duplicate exploration efforts. This increases financial risk for developers and reduces data sharing. The stakeholders report that the introduction of exclusivity over areas does not necessarily lead to increased data sharing due to the fact that companies have no incentive to share data.

To improve the information base and data in these areas, the Finnish working group for offshore wind proposes to extend maritime observation activities and the coverage of the Finnish Inventory Programme for Underwater Marine Diversity (Velmu) in deeper waters. It also proposes producing more detailed maritime information to support maritime spatial planning and land use planning, and launching studies on the impacts of offshore wind power on migratory fish, marine mammals, migratory birds and bats. It further proposes developing information systems to streamline assessment and administrative processes across administrative sectors and to enable anticipation of business project planning.

3.9 Similarities and differences between the Nordic countries