Executive summary

The objective of the project presented in this report was to support the development of Nordic hydrogen valleys, contribute to the exchange of experience among Nordic stakeholders and to promote and enhance Nordic strengths within Nordic hydrogen value chains.

The project reached this objective by providing:

- A Nordic definition of hydrogen valleys and hydrogen hotspots.

- A mapping of hydrogen projects in the Nordic region, including Denmark, Greenland, the Faroe Islands, Finland, Iceland, Norway, Sweden and Åland.

- A categorisation – based on the proposed definitions – of the mapped projects into the categories “hydrogen valleys”, “hydrogen hotspots” and “other”.

- A user-friendly and versatile prototype digital tool for visualising the results of the mapping work, based on which a more comprehensive digital tool can be developed at a later stage.

- A deeper understanding of the challenges and opportunities for the use of hydrogen and clean fuels in Arctic maritime transport.

- An overview of drivers and barriers for hydrogen valley development in the Nordics, as well as policy recommendations.

Information was gathered through literature reviews, expert interviews and an open project workshop. All data was collected in the spring of 2024, and changes in, for instance, stakeholders’ investment plans after May 2024 have not been incorporated. The interviews and the workshop also gave stakeholders an opportunity to provide feedback on draft work and to give suggestions on ways to move forward.

Hydrogen valley mapping and tool development

This project proposed the following definition of Nordic hydrogen valleys and hydrogen hotspots, based on findings by the Mission Innovation Hydrogen Valley Platform and definitions used in relevant EU calls.

Hydrogen valleys are projects that:

- cover a specific geography in at least one Nordic country,

- cover at least two steps of the hydrogen value chain (production → distribution → use),

- have a hydrogen production capacity exceeding 500 tonnes per annum (tpa),

- supply hydrogen to at least two different end-use sectors,

- have at least reached the feasibility phase (feasibility study).

Nordic hydrogen hotspots are projects that do not qualify as hydrogen valleys but fulfil criterion 1 and at least two of criteria 2–5 in the hydrogen valley definition. Use includes both direct and indirect use of hydrogen (e.g. to produce fuels or chemicals).

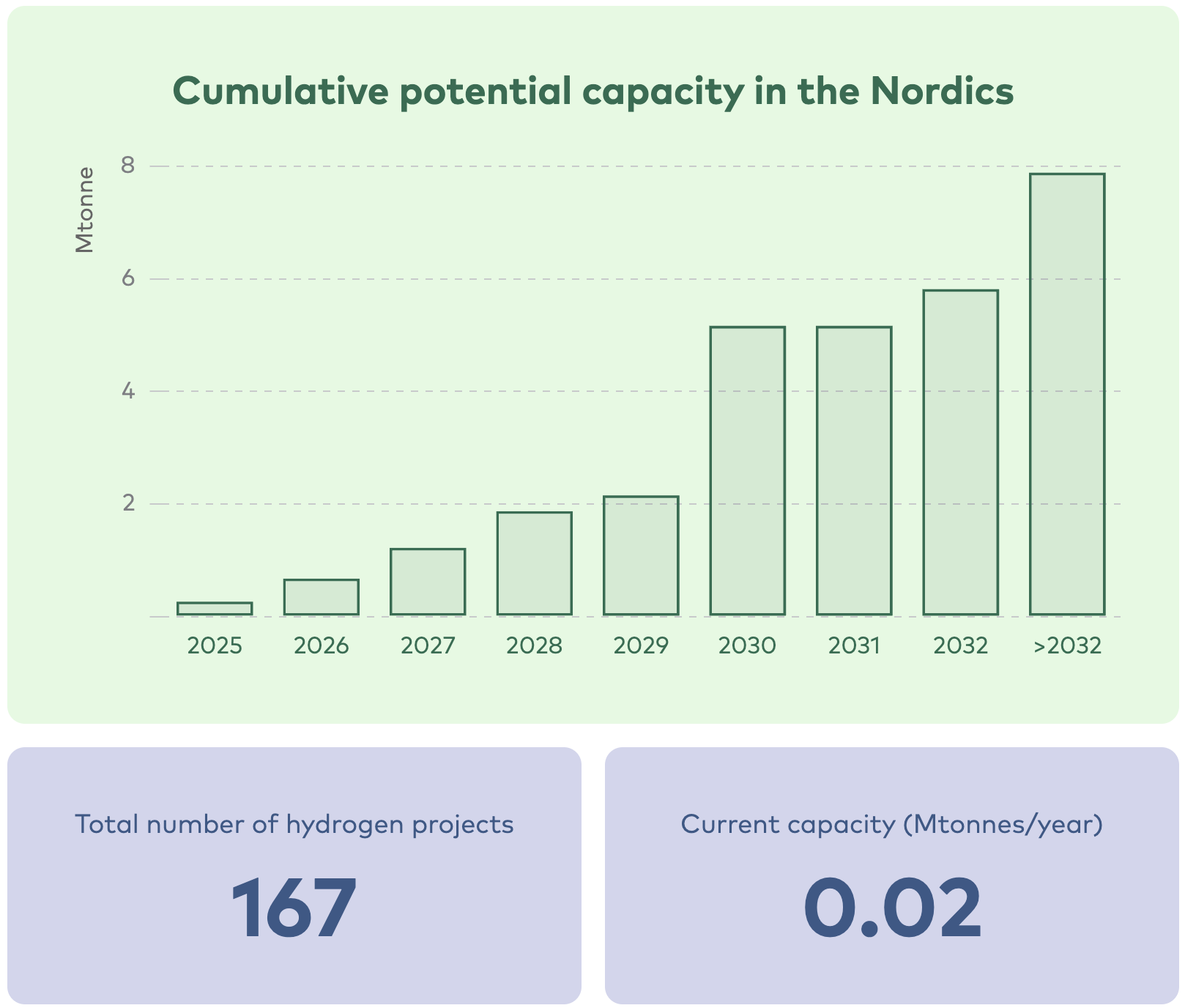

The project mapped 167 Nordic hydrogen projects and gathered key information in a database, which was subsequently visualised using a digital tool developed within the project. Nine of the mapped projects fulfilled the hydrogen valley definition at the time of the mapping (spring 2024). The mapping results are available at nordich2valleys.org , and a summary is given below.

The digital tool is a publicly available interactive web application that allows users to view and analyse data gathered during the mapping. The tool is managed by Nordic Energy Research and is a prototype from which a more comprehensive tool may be developed at a later stage.

Mapped hydrogen projects, hotspots and valleys per Nordic country. Production capacity refers to the total planned capacity of the mapped projects and includes capacity that is already operational. About 0.2% of the total planned capacity in the Nordics is operational; none of the identified valley projects are operational. Hydrogen projects that cannot be categorised as hotspots or valleys are categorised as “other”. Thus, totals do not equal the sum of hotspots and valleys (the difference is especially notable for Norway).

Country | Total number of hydrogen projects | Total planned hydrogen production capacity (ktpa) | Number of hotspots | Planned hydrogen production capacity of hotspots (ktpa) | Number of valleys | Planned hydrogen production capacity of valleys (ktpa) |

Denmark | 29 | 3,748 | 18 | 2,822 | 5 | 237 |

Faroe Islands | 0 | 0 | 0 | 0 | 0 | 0 |

Finland | 36 | 1 126 | 35 | 1 126 | 1 | 0.5 |

Greenland | 1 | 153–255 | 1 | 153–255 | 0 | 0 |

Iceland | 9 | 112 | 9 | 112 | 0 | 0 |

Norway | 50 | 711 | 24 | 414 | 2 | 10 |

Sweden | 38 | 1,524 | 37 | 1,512 | 1 | 12 |

Åland Islands | 4 | 513 | 4 | 513 | 0 | 0 |

The fourth hydrogen valley criterion was identified as challenging in expert interviews and the open project workshop. This sentiment was confirmed by the mapping; only 25 of the mapped projects supply hydrogen to specific off-takers in multiple sectors, meaning that 142 mapped projects failed to meet this criterion. Of the 25 projects that do supply more than one end-use sector, 16 failed to meet the hydrogen valley definition, mainly because of insufficient project maturity.

Although the total capacity of the mapped projects is significant – about 8 Mt or 270 TWh of hydrogen per year – only about 0.2% of this capacity is operational, with an additional approx. 1% under construction. Most projects – especially those very large in scale (hundreds of MW or more) – are in the very early stages of development, meaning that project scope, scale and timeline are still subject to change. Realistically, most of the mapped projects will never materialise. This means that the developed project database and digital tool will require frequent updates to stay relevant.

Common characteristics among the mapped projects (regardless of their status) are summarised below.

Projects in Sweden and Finland often aim to use hydrogen for the on-site production of e-fuel/chemicals or to decarbonise existing industrial processes. While Danish projects also commonly use hydrogen for the on-site production of e-fuel/chemicals, Denmark also hosts several large-scale, export-oriented projects aiming to sell hydrogen in potential future European or Global markets. To export hydrogen, Danish projects often plan to use (prospective) hydrogen gas grids. Norwegian projects also cover a variety of end-uses but are distinguished by a focus on utilising hydrogen for ammonia production or as a maritime fuel. The two aspects are sometimes combined, with hydrogen being used to produce ammonia for use as maritime fuel. However, there are also projects producing hydrogen for direct use as maritime fuel or projects producing ammonia for industrial use (e.g. to decarbonise fertiliser production).

It should also be noted that the mapping often failed to identify intended end-users for the Norwegian projects, indicating that the planned hydrogen capacity will be available “on the market” for interested off-takers. In comparison with the previously discussed countries, the majority of Norwegian projects produce hydrogen for use on-site (instead of exporting hydrogen to e.g. the transport sector), meaning they are not in control of the entire value chain. Consequently, final off-takers are sometimes not identified even in advanced stages of project development. One explanation for the difference between Norwegian projects and especially Finnish and Swedish projects may be that the latter focus on the decarbonisation of their own processes, while Norwegian projects have great opportunities for export due to low power prices.

The number of mapped projects in Iceland, Åland, the Faroe Islands and Greenland is too low to draw general conclusions. Most of the mapped Icelandic projects target e-fuel/chemicals production or direct use in transport. This is in line with the Hydrogen and E-fuels Roadmap for Iceland, which identifies hydrogen and e-fuels as key elements in decarbonising Iceland’s transport and maritime sectors. Identified projects in Åland are export-oriented, aiming to export hydrogen via prospective Baltic Sea hydrogen infrastructure.

The most common hydrogen derivatives produced by the mapped projects are methanol, ammonia and methane, with the production of e-SAF being less common. Common direct uses of hydrogen include road transport and industrial heating, as well as the decarbonisation of industrial processes by replacing a fossil input (e.g. coal in steel making or fossil hydrogen in refinery processes or ammonia production).

This project has not assessed Nordic strengths and weaknesses in relation to other EU countries. However, the presence of large-scale export projects targeting the European market (especially in Denmark) indicate a position of strength.

Since most of the mapped projects – especially the larger projects – are in the very early stages of development, the scope and timeline of many projects are still very uncertain and subject to change. Consequently, the developed database and the tool will require regular updates, maintenance and development to stay relevant. Given that the tool continues to be developed and updated, it will contribute to knowledge development among Nordic stakeholders and promote and enhance Nordic strengths within Nordic hydrogen value chains.

The potential role of hydrogen in Arctic maritime transport

The potential future role of hydrogen and hydrogen-based fuels for Arctic maritime transport in the Nordic countries was assessed by a review of existing literature and knowledge about relevant projects (including projects covered by the mapping).

In context of this project, “Arctic” is defined as Greenland, Iceland, the Faroe Islands and Northern Norway.

Since 1 July 2024, there has been a ban on the use and carriage of HFO in Arctic waters, although waivers and exemptions could allow continued use and carriage for a few years longer. Nonetheless, this ban can be expected to incentivise the use of alternative fuels in Arctic maritime transport.

The literature and outcomes of projects find hydrogen and hydrogen-based fuels to be among the most promising alternatives to facilitate the decarbonisation of shipping. In addition to their environmental benefits, the isolated power infrastructure in the Arctic makes green hydrogen and hydrogen-based fuels particularly interesting. Wind and PV have huge untapped potential in the region and can be put in use in areas with no grid or low grid capacity. In addition to supplying marine fuel, the scattered communities in the Arctic would benefit from the harnessed power, which would in turn contribute to job and value creation in the region.

The current use of hydrogen in Arctic maritime transport is negligible compared to the use of fossil fuels. Projects producing hydrogen or hydrogen-based e-fuels such as ammonia and methanol are under development in the region, especially in Northern Norway where about 600 thousand tonnes of hydrogen capacity (including natural gas reforming with CCS) is under development, mostly for ammonia production and often aimed at maritime off-takers. Several large-scale e-fuel projects are also under development in Iceland, where maritime activities are an important part of the economy. Because ammonia and methanol are likely future fuels for decarbonised shipping, these projects may pave the way for increased hydrogen use in Arctic shipping, although most projects are still in the early stages of development.

To enable the use of hydrogen and hydrogen-based fuels in Arctic shipping, some barriers need to be addressed. The advancement of regulatory frameworks, bunkering facilities and technical and operational know-how on using these fuels onboard ships would facilitate their adoption.

Drivers, barriers and policy measures for Nordic hydrogen valley development

This project reviewed relevant literature to map the drivers and barriers for hydrogen valley development in the Nordics (and for hydrogen development in general). Expert interviews and a workshop were conducted to complement and rank a list of drivers and barriers developed during the literature review.

Of the identified drivers, the three most important are current and future access to renewable energy production, policy support on a Nordic/EU level and industries’ ambitions to use hydrogen for the decarbonisation of their own activities.

In most of the Nordic countries, an important driver for the development of a hydrogen economy is the potential of untapped national resources (e.g. wind power) to create additional value.

The most important barriers that need to be addressed include the overall business case for hydrogen projects, regulatory frameworks, which are not optimal for developing hydrogen projects, and a lack of local energy supply and infrastructure.

The literature review, expert interviews and workshop were also used to identify policy suggestions. One key finding from this work is that stakeholder priorities can differ significantly regarding which policy measures are deemed most important. However, the most prioritised policy measures identified include:

- Defining long-term strategies and targets for the development of hydrogen production and use on the national level, with a view to supporting investments.

- Promoting the development of a cost-effective hydrogen value chain by improving the support schemes for both the demand and supply side. This could support initial development to reduce the cost difference in relation to less sustainable options.

- Supporting the development of hydrogen infrastructure (pipeline and refuelling infrastructure, hydrogen storage) through the creation of partnerships to reduce risk.

- Supporting the promptest possible implementation of more general climate policies at the EU level (such as CBAM, EU ETS, RED III etc.), as a general driver for fossil-free alternatives, including hydrogen.

- Providing support to reduce unnecessary lead times in permitting processes for electricity and hydrogen infrastructure, while establishing suitable regulations to streamline these processes.

- Creating standards to define the origin, quality and life cycle of hydrogen GHG emissions. This should be aligned with the EU’s Renewable Energy Directive (RED III) and other relevant regulations.

The respondents of the interviews, who represented national hydrogen associations and project managers involved in the “Nordic Hydrogen Valleys as Energy Hubs” programme, stressed the need for financial support for the entire value chain of early-stage hydrogen projects. This value chain includes energy supply and hydrogen production, as well as hydrogen distribution, infrastructure and utilisation.