Photo: Unsplash

2. Nordic criteria for hydrogen valleys and hydrogen hotspots

2.1 EU criteria for hydrogen valleys

The Mission Innovation Hydrogen Valleys Platform was commissioned by the European Union and launched in 2021 to “[present] comprehensive insights into the most advanced and ambitious Hydrogen Valleys around the globe”.

Clean Hydrogen Partnership – Mission Innovation Hydrogen Valleys Platform. Available: https://www.clean-hydrogen.europa.eu/get-involved/mission-innovation-hydrogen-valleys-platform_en

Both Mission Innovation reports are available here: https://h2v.eu/analysis/reports

Clean Hydrogen Partnership – Mission Innovation Hydrogen Valleys Platform. Available: https://www.clean-hydrogen.europa.eu/get-involved/mission-innovation-hydrogen-valleys-platform_en

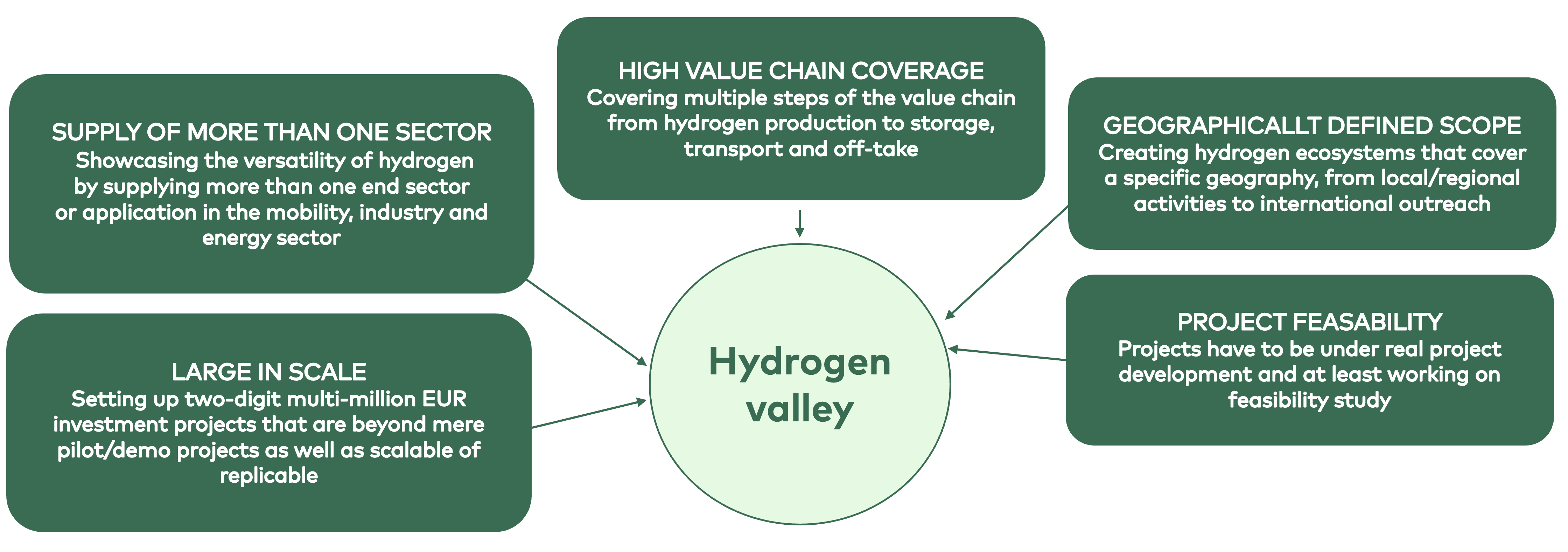

Figure 2. Key characteristics of hydrogen valleys, as identified by the Mission Innovation Hydrogen Valleys Platform (adapted illustration, based on publication from the Mission Innovation report).

Going Global – An update on Hydrogen Valleys and their role in the new hydrogen economy. Available: Hydrogen_Valleys_online_2022.pdf

With reference to the Mission Innovation report, the 2024 Horizon Europe call for hydrogen valley projects summarised the concept as follows (emphasis added in bold):

“Hydrogen Valleys are hydrogen ecosystems that cover a specific geography ranging from local or regional focus (e.g. industrial cluster, ports, airports etc.) to specific national or international regions (e.g. cross border hydrogen corridors). Hydrogen Valleys showcase the versatility of hydrogen by supplying several sectors in their geography such as mobility, industry and energy end uses. They are ecosystems or clusters where various final applications share a common hydrogen supply infrastructure. Across their geographic scope, Hydrogen Valleys cover multiple steps in the hydrogen value chain, ranging from hydrogen production (and often even dedicated renewables production) to the subsequent storage of hydrogen and distribution to off-takers via various modes of transport.”

The definition given by Horizon Europe uses three of the five criteria from the Mission Innovation report (emphasised) but excludes the scale and feasibility criteria. The call does, however, set a different scale criterion (production of at least 500 tpa of hydrogen) and adds the requirement that hydrogen must be produced from renewable sources

As defined by the Renewable Energy Directive, 2018/2001/EU

2.2 Nordic criteria for hydrogen valleys and hydrogen hotspots

Summarising the different criteria and definitions used by the EU and described above, the following possible criteria for a definition of “hydrogen valley” can be identified:

- Hydrogen valleys have a defined geographic scope/coverage.

- Hydrogen valleys supply several end-use sectors.

- Hydrogen valleys cover multiple steps of the hydrogen value chain.

- Hydrogen valleys are large in scale

a. At least a two-digit MEUR investment (Mission Innovation), or

b. >500 tpa production (Horizon Europe). - Hydrogen valleys are projects that have at least reached the feasibility phase (Mission Innovation).

- Hydrogen valleys use hydrogen from renewable energy sources (Horizon Europe).

In the present mapping of Nordic hydrogen valleys, the possible criteria listed above were used as a starting point to define Nordic hydrogen valleys. The first three criteria in the list above are used both by Mission Innovation and by Horizon Europe. They are also used in the Nordic hydrogen valley definition proposed by the present project, with only minor adjustments and clarifications. “Several” and “multiple” in criteria 2–3 have been replaced by “at least two” and the “steps of the hydrogen value chain” referred to in criterion 3 are explicitly defined as production, distribution and use.

Regarding the criterion to supply several end-use sectors, a similar level of integration may be achieved if one end-user has several suppliers. However, because most projects are production-oriented, the number of such projects (end-users with multiple suppliers) is expected to be very low, and they were not included in the proposed definition.

The first criterion does not have strict sub-criteria that must be fulfilled (e.g. aligning with rules for geographically confined hydrogen networks set out in Article 52 of the EU’s Directive on common rules for the internal markets for renewable gas, natural gas and hydrogen (EU 2024/1788)). More detailed criteria would make the task of mapping extremely challenging due to the limited public access to project-specific data. Having a specified site of hydrogen production supplying specific end-users is sufficient is sufficient to fulfil criterion 1. The interplay between the first criterion and the second criterion (end-use sectors) is further discussed in Section 3.1.

Regarding the fourth criterion (scale), we find the capacity metric used by Horizon Europe (production capacity) more suitable than the investment metric used by Mission Innovation (investment volume) for the following reasons:

- Investment estimates are uncertain and change as a project matures.

- Investment estimates are often communicated as lump sums without details on the scope and methodology of the estimate, making it very difficult to compare projects. An investment estimate may include costs that are not directly related to the hydrogen value chain.

- For most projects, information on production volumes is more readily available than information on investments, which facilitates mapping.

It should be noted that the Mission Innovation platform considers not only scale, but also project replicability and scalability in its scale criterion. Replicability and scalability are difficult to assess in a definitive way for early-stage projects with very limited information publicly available. Therefore, the mapping only considered production capacity (which is an easily evaluated metric) for the scale criterion. However, we consider all the identified valleys to be either replicable or scalable, although modifications would of course be necessary to allow implementation at other locations.

We consider the fifth criterion suitable since it avoids the inclusion of highly uncertain projects in the “concept stage”.

The sixth criterion was not formally included in the proposed definition since it would require an assessment of the electricity used for electrolysis in all mapped projects, which may prove difficult for early-stage projects. However, it can be expected that virtually all included projects use renewable energy.

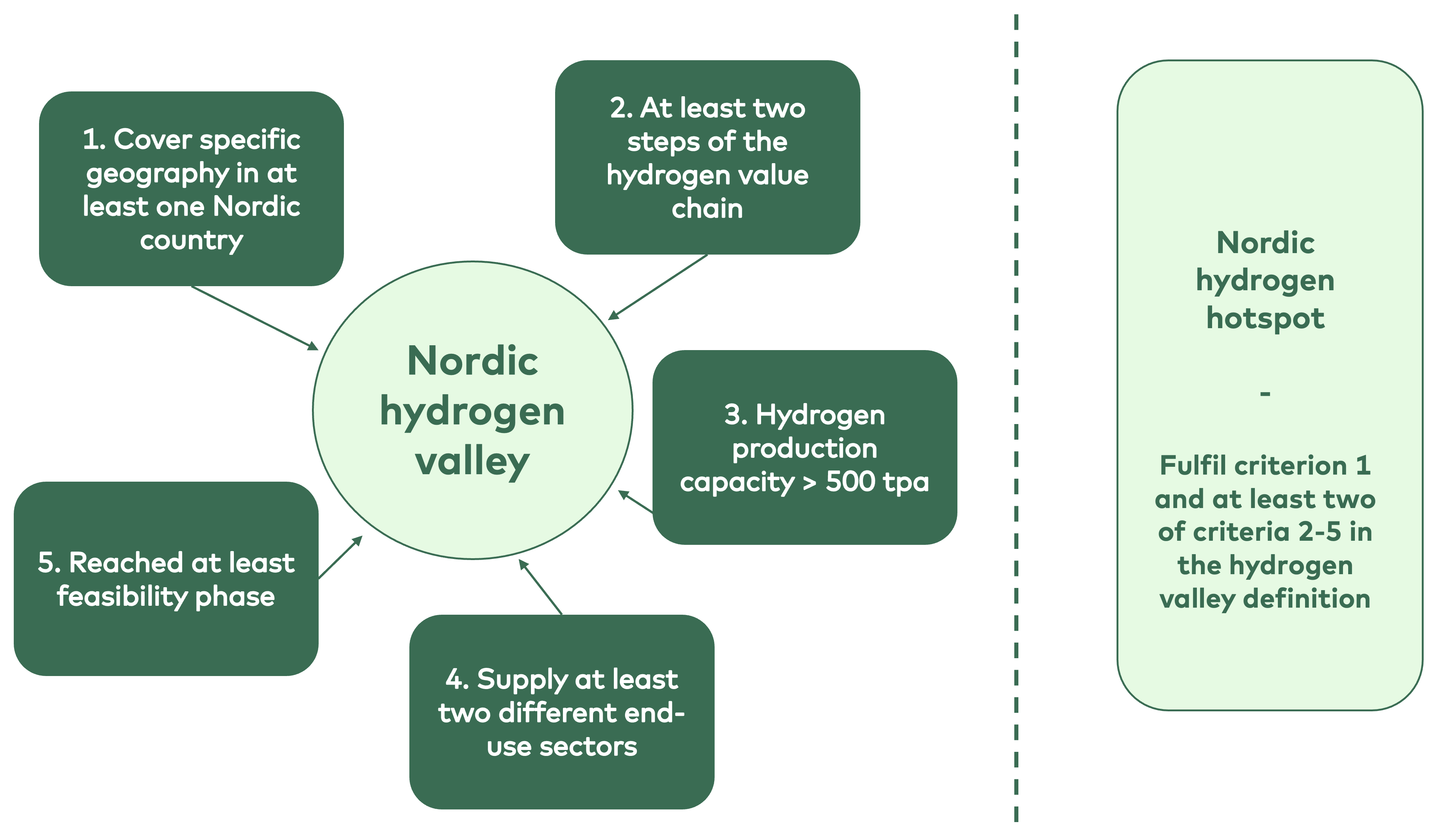

With the adjustments discussed above, a Nordic definition of a “hydrogen valley” can be given:

Nordic hydrogen valleys are projects that:

- cover a specific geography in at least one Nordic country,

- cover at least two steps of the hydrogen value chain

(production → distribution → use), - have a hydrogen production capacity exceeding 500 tonnes per annum (tpa),

- supply hydrogen to at least two different end-use sectors,

- have at least reached the feasibility phase (i.e. are working on a feasibility study).

There are many projects that do not fulfil the requirements to be designated as a hydrogen valley but may develop into a hydrogen valley in the future. Such projects are called Nordic hydrogen hotspots in the present report and are defined as:

Projects that fulfil criterion 1 and at least 2 of criteria 2–5 in the hydrogen valley definition.

Figure 3. Key characteristics of Nordic hydrogen valleys, as defined in this study.

2.3 Input from workshops and expert interviews

The proposed definition was discussed during the project workshop and in expert interviews, see Appendices A–C.

The proposed definition was generally approved by workshop participants and interviewed experts. The more frequent comments and suggestions are discussed below:

- “It will be challenging to identify projects that fulfil criterion 4 (at least two end-use sectors).”

This concern was raised both in the workshop and in the expert interviews. Indeed, this is the criterion that most of the potential hydrogen valleys in our mapping fail to meet. Nonetheless, showing the versatility of hydrogen is a core aspect of the hydrogen valley concept and the criterion was not removed from the proposed hydrogen valley definition. Moreover, projects that fail only this criterion are still included in the mapping as “hydrogen hotspots”. - “The colour of hydrogen is important.”

The issue of hydrogen colour was raised by several workshop participants and experts, but there was no clear consensus regarding which colours to include/exclude. To address this issue, the hydrogen production technology has been specified for all projects included in the database developed by the present project. - “The lower capacity limit (500 tpa) is too low.”

This concern was raised by a few of the interviewed experts. The stated minimum capacity is indeed low and was exceeded by most of the potential hydrogen valleys mapped in this project. Nonetheless, this limit was used throughout the mapping process. The developed database can, however, easily be adjusted to a higher capacity limit as the hydrogen market evolves.