1. Introduction

In the past decades, the world has seen substantial changes in policy practices and multilateral agreements shifting towards building resilient, sustainable societies. This has led to an increased global understanding of the impact and importance of utilising policy instruments for the environment in taxation practices.

European Environment Agency (2020). The sustainability transition in Europe in an age of demographic and technological change - An exploration of implications for fiscal and financial strategies

OECD (n.d). Tax and the environment

United Nations, Department of Economic and Social affairs (n.d). Environmental Taxation

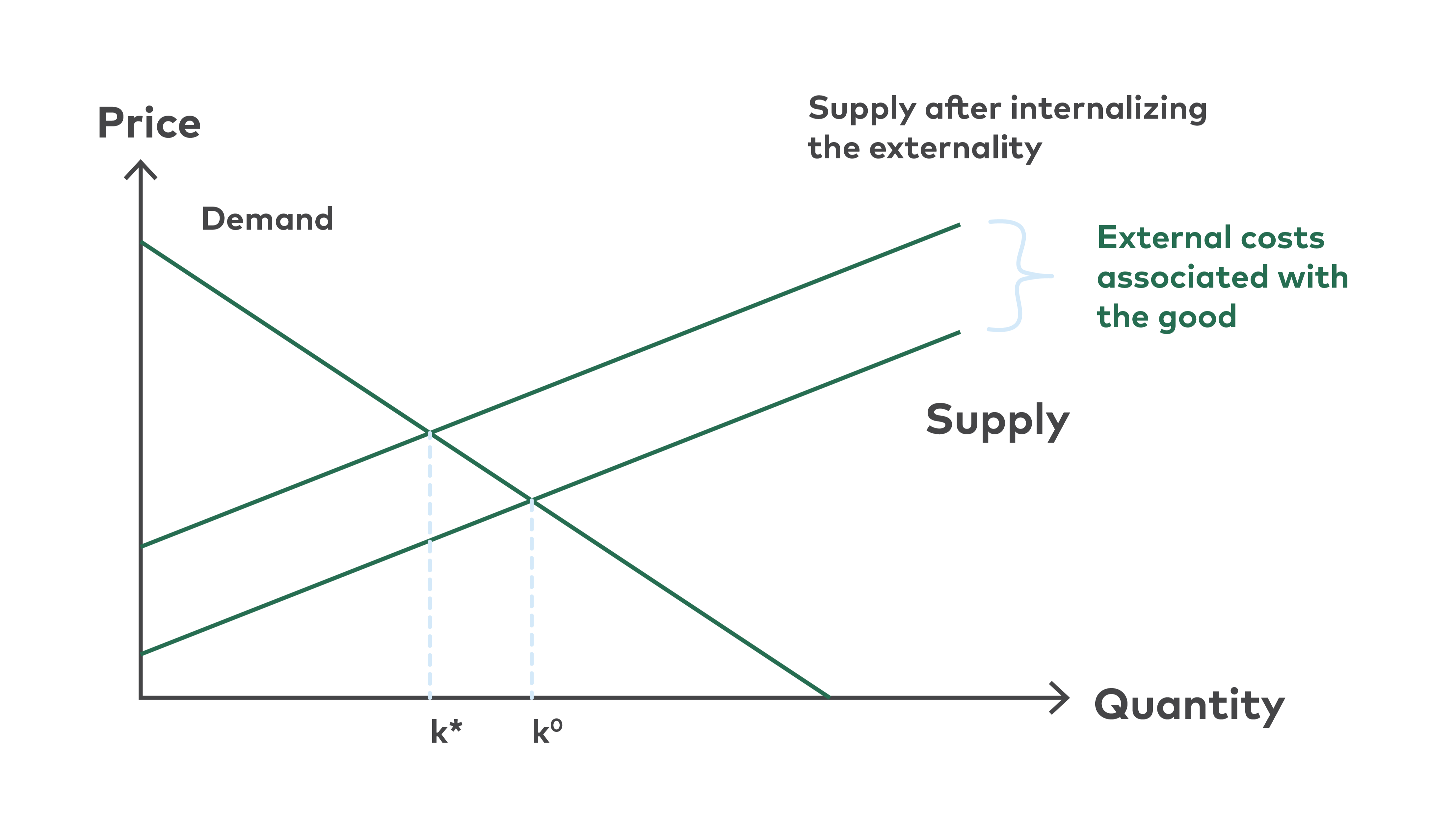

No market is perfect, as economic activities create externalities that are not reflected in the market price (shadow prices). These externalities are considered market failures. Governments use economic instruments, such as fees and charges, to correct for negative externalities and to change market actors' behaviour.k^0\rightarrow k * to achieve a social optimum, thus internalising the externality of the good.

Perman et al (2011). Natural Resource and Environmental Economics

Figure 1: Effect on price and quantity when internalising externalities.

Examples of green charges are energy taxes, waste taxes, and taxes on polluting substances, such as chemicals and particle matter. These taxes aim to internalise negative externalities, e.g., by integrating the polluters-pay principle, incentivising consumers to buy other products, and shifting consumer and/or producer behaviour. Collectively, green taxation aids in integrating economic practices and environmental protection.

The polluters-pay-principle and green charges have been an integral part of global environmental policy for decades as a part of the UNEP

UNEP (1994). Economic instruments for Environmental Management and Sustainable Development

Khan (2015). Polluters-Pays-Principle: The Cardinal Instrument for Addressing Climate Change

Mottershead et al (2021), Green Taxation and other economic instruments – internalising environmental costs to make the polluters pay.

TFEU Article 191(2) of the 2007 Treaty of the Functioning of the European Union

European Environment Agency (2022). The role of (environmental) taxation in supporting sustainability transitions

European Court of Auditors (2021). The Polluters Pays Principle: Inconsistent application across EU envrionmental policies and actions

Despite the popularity of the principle within the EU, a study conducted by the European Commission shows that the external, societal costs of pollution within the EU are still, to a large extent, not being paid by polluters.

Mottershead et al (2021), Green Taxation and other economic instruments – internalising environmental costs to make the polluters pay

European Environment Agency (2024b). Share of environmental taxes in total tax revenues in Europe

Implementing environmental taxes can be complicated, especially in the integration of other policies and coordination across policies.

Milne & Andersen (2012). Handbook of Research on Environmental taxation

Why use green charges in environmental policy?

Green charges can be effective governance tools in achieving environmental goals. Green charges often require less administration than prescriptive regulations, and therefore more economically effective. Since governments cannot know the cost of pollution units of every firm, green charges encourage each polluter to abate in the most cost-efficient way. Green charges also generate government revenue that can be earmarked towards environmental policy measures or towards subsidies and compensation, thereby aiding in the progression of environmental policies. They can also inspire technological innovation by means of encouraging cost-effective practices and thus creating a demand for green technology. The European Environment Agency summarises the reasons for using environmental taxes in five categories: internalisation of externalities, incentivising behavioural change, minimisation of pollution control costs, incentivising innovation and raising revenue.

European Environment Agency (1996). Environmental taxes: Implementation and environmental effectiveness

- Bringing externalities into prices: When a cost, such as pollution, is not reflected in the price of said good, it’s an externality. Environmental taxes can incorporate the cost of the environmental damage in the price of the good, thus internalising the externality and reinforcing the Polluter Pays Principle.

- Incentive structure: environmental taxes incentivise both producer and consumer to generate or use less of the taxed good or service.

- Minimising pollution control costs: Because pollution abatement cost varies across producers, policy tools such as prescriptive regulations cannot differentiate between differences in pollution abatement costs. Economic tools do not have to, however, since they will encourage the polluters with the lowest cost of pollution reduction to abate, while for those producers with higher abatement costs, it will be cheaper to pay the tax. This ensures that the cost of archiving a given pollution reduction is lower than with regulation.

- Encourages ongoing innovation: while regulatory policies leave no incentive for companies to reduce their pollution below the given threshold, economic tools such as green charges encourage ongoing innovation because the companies will be continuously incentivised to reduce pollution.

- Raising revenue: economic tools such as taxes, tradable permits or quotas raise government revenue that can be earmarked towards environmental policy measures or subsidies and compensation measures, also called the double dividend effect.

The impact of an environmental fee depends on the price elasticities of both demand and supply. The price elasticity of demand refers to how much consumers (or producers acquiring inputs) will change their demand following a price increase or decrease. In contrast, the price elasticity of supply refers to how much producers are willing to supply at different price levels. Together, they determine the combined effect of an environmental fee. The amount of the fee transmitted to consumers is the tax incidence, which is only, in special cases, the full amount of the fee. Environmental fees often concern “necessity goods”, characterised by a low degree of elasticity of demand, as these types of goods will be consumed on the market even with substantial changes in product prices. Examples include water, petrol and electricity. If the goods have a low degree of price elasticity, the effect of taxation is less than that of regular goods and should, in theory, be higher to be impactful.

Ramsey (1927), A contribution to the theory of taxation

An example is the tax on petrol – as petrol is considered a fairly inelastic good, because the price change has little effect on short-term consumption levels. Yet, the long-term elasticity is still more elastic, as consumers and the market adopt over time. This can for example be seen from the market shift to electric vehicles, which offers an equivalent substitute to the gasoline engine. However, setting the tax “as high as possible” has shown to have regressive social effects and therefore distortive market outcomes, posing a heavy burden on low-income groups.

Høst et al. (2020), A socially sustainable green transition in the Nordic region

Part of the explanation of why price elasticities vary among product types lies in the type of product, whether they are considered necessity goods, luxury goods, or inferior goods (demand drops with higher income). However, the consumer responses (and resulting price elasticities) are also influenced by various biases or cognitive processes that limit (or enhance) the possible effects of taxes. For example, many individuals inhibit cumulative cost neglect, which results in low behavioural impact from incremental price changes, even though they may have a significant budget impact over time. Charges may also interact with other motivations, particularly for consumers, potentially resulting in “crowding-in” or “crowding-out” effects.

1.1 Economic instruments in Nordic environmental policy

The Nordic countries have a long history of implementing economic policy instruments to protect the environment.

Pedersen & Dengsøe (2000), Vurderinger af de grønne afgifters effekter i de nordiske lande

Svenningsen et al. (2018), Policy Brief: The use of economic instruments in Nordic environmental policy 1990-2017

European Environment Agency (1996). Environmental Taxes: Implementation and Environmental Effectiveness

Dengsøe & Pedersen (2000), Vurderinger af de grønne afgifters effekter i de nordiske lande

Dansk Retur System (2022), 20 år med producentansvar på tværs af Brancher

European Commission (2021), Deposit Refund Schemes

Sveriges Riksdag (1990), Lag (1990:613) om miljöavgift på utsläpp av kväveoxider vid energiproduktion

Effective environmental policies are key to achieving the climate goals and the Nordic 2030 vision of becoming the world's most sustainable and integrated region.

Nordic Council of Ministers (2020), The Nordic Region – towards being the most sustainable and integrated region in the world – Action Plan for 2021 to 2024.