Nordic Strengths and Challenges in Critical Raw Materials Mining

The Nordic’s geological wealth, robust innovation ecosystem, and access to clean, affordable energy create a solid foundation for the Nordics to become a reliable source of responsibly sourced minerals essential for the European market.

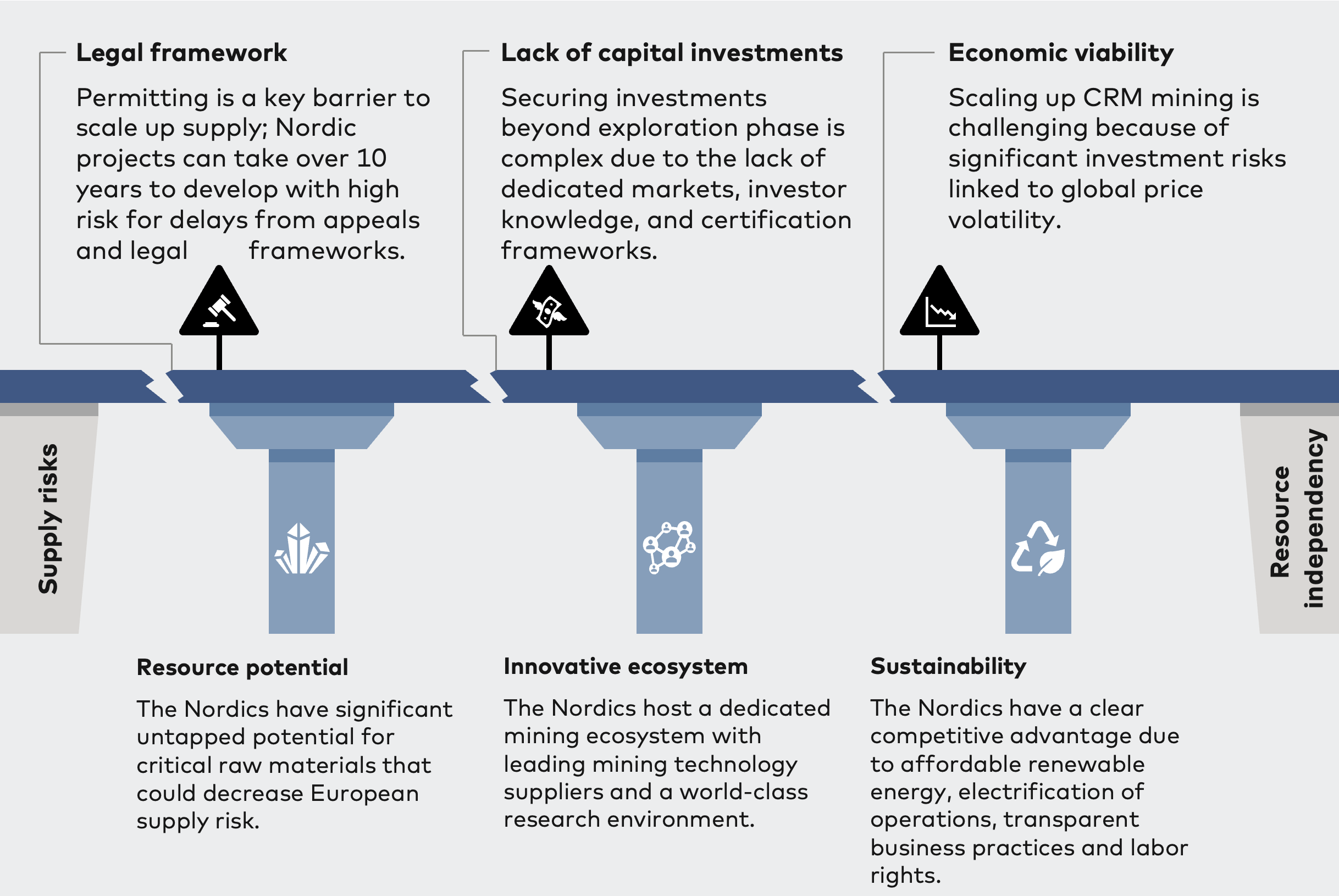

Despite these advantages, several major obstacles currently impede further development and investment in mining within the Nordics, especially concerning CRMs. These challenges create uncertainty around the returns on investment, classifying mining projects as high-risk and diminishing investor confidence.

Strengths

The Nordics hold considerable untapped potential for CRMs, which could significantly reduce Europe’s supply risk. The region’s rich geology shares similarities with other resource-rich nations like Australia and Canada. A 2021 study by the Nordic geological surveys found that the region contains deposits of all 25 CRMs then listed by the EU. An updated study is underway based on the latest EU CRM list. Of these, 11 materials were identified as holding significant importance and potential from a Nordic perspective, due to both resource availability and their relevance to Europe. There is notable overlap across the countries: Sweden has deposits of all 25 materials, Finland and Greenland have 24, and Norway has 23, while Iceland and Denmark have limited potential due to their geology.

Cobalt 100% of European mine production | Graphite 90% of European mine production | Hafnium 100% of European resources | Lithium Battery-grade production under development | Niobium 8% of global and 99% of European resources | PGMs 100% mine production and 99% of resources in Europe |

|---|---|---|---|---|---|

REEs 9% of global resources | Silicon metal 6% of global and 50% of European production | Tantalum 99% of European resources | Titanium 100% mine production and 90% of resources in Europe | Vanadium 10% of global resources | |

Antimony | Baryte | Beryllium | Bismuth | Copper | Fluorspar |

Gallium | Manganese | Nickel | Phosphorus | Scandium | Tungsten |

Germanium | Indium | AppleGoogleOffice 365OutlookOutlook.comYahoo | |||

The Nordics boast a dedicated mining ecosystem, supported by leading mining technology suppliers and world-class research institutions. The region is home to a dense network of technology suppliers who lead in automation, electrification, and digitalisation of mining operations and export advanced technologies globally. Top universities and research institutes contribute to advancements in mineral processing, mining automation, and environmental technologies, often working closely with industry partners. Geological surveys provide crucial geoscientific data to help de-risk investments and guide sustainable development. Industry associations promote responsible mining, foster collaboration, and drive innovation through shared research initiatives. The mining ecosystem is especially concentrated in Finland and Sweden, reflecting their longer mining traditions. In contrast, Norway, Iceland, Denmark, and Greenland have less developed ecosystems owing to different industrial focuses or limited mining potential.

Nordic mining and metal production demonstrates significantly lower CO₂ intensity compared to the global average, primarily due to access to low-carbon power grids and electrification of operations. The region benefits from affordable renewable energy sources such as hydropower and wind in Norway and Sweden, complemented by substantial nuclear capacity in Sweden and Finland, creating a low-emission energy supply. Given that metal processing is extremely energy-intensive, grid emission factors play a critical role in determining production footprints. Abundant natural resources and strong grid connectivity provide Nordic producers with a strategic advantage in delivering low-carbon metals to the manufacturing industry, positioning the region as a preferred supplier under increasingly stringent ESG requirements. However, this competitive edge may diminish if energy capacity expansion slows down or if market integration drives up electricity prices.

Challenges

Permitting remains a complex aspect of scaling up supply in the Nordics. Mining projects often require long lead times, with approvals for new mines typically taking several years due to environmental considerations and multi-level regulatory requirements. Differences in national legislation and administrative procedures can complicate cross-border projects, while overlapping EU, national, and local rules add layers of complexity – particularly for SMEs. Streamlining and harmonising permitting processes across the region would help reduce administrative burdens and create a more predictable environment for investors.

Data only available for countries with 5 or more mines opened during the researched period, of which no European country had opened 5 or more

Voices from the industry | ||||

“Permitting can take decades, even for known deposits; starting from scratch can take 20 years” – Mine Developer | “Lengthy permitting processes and EU regulations are still the greatest challenges.” – Industry Association | “If the permitting could be solved, everything else would be peanuts in comparison.” – Mine Developer | “Even after permits are secured, NGOs can initiate court cases that threaten project viability for years” – Industry Expert | “Mining projects in the Nordics face significant social and environmental opposition, leading to long and unpredictable permitting processes.” – Industry Expert |

Lack of Capital Investments

Investment flows into Nordic mining are still developing. Globally, the sector will require significant capital – estimated at USD 5.4 trillion by 2035 – to meet growing demand for raw materials. While Nordic projects benefit from strong ESG credentials and political support, challenges such as limited investor familiarity with mining projects, absence of specialised capital markets, and long project timelines can limit investment. Clearer certification frameworks and greater regulatory predictability could help attract both domestic and international capital.

Note 1: Accounting for sustaining, project and exploration-phases.

Source: McKinsey Global Materials Perspective 2024 & 2025.

Source: McKinsey Global Materials Perspective 2024 & 2025.

USD billion, total need between 2024–2035

Voices from the industry | ||||

“Capital and financing is a bottleneck for the mining industry in general in the Nordic countries” – Mine Developer | “If you want to make something happen, the states need to get more involved and take the risk off” – International Financial Institution | “We are not so attractive for risk capital, and that is a bit of a shame” – Industry Association | “We have the minerals, the money, and the institutions to make this happen – if we act together” – International Financial Institution | “The main barrier for junior mining companies is access to capital (…) Financing is a critical bottleneck for project advancement” – Mine & Refinery Developer |

Economic Viability

Market volatility remains a key consideration for investors. Prices for some critical minerals have fluctuated sharply in recent years, influencing project economics and investment decisions. Geopolitical factors and concentrated supply chains add further uncertainty. Despite these dynamics, strong downstream demand and supportive policy frameworks provide a foundation for long-term growth, particularly for projects that can demonstrate resilience and cost competitiveness.

Gold is often considered a more secure investment, underpinned by recent price developments and its demonstrated resilience amid volatility in broader mineral markets. This dynamic is further evidenced by recent foreign direct investment trends, which indicate a marked preference for precious metals over other mineral categories.

Other challenges

Other challenges highlighted by stakeholders include social acceptance, energy access, talent shortages and technology adoption.

Public acceptance of mining varies across the Nordic countries. While mining is widely recognised as essential for the green transition, engagement with local communities and respect for indigenous rights remain critical. Transparent dialogue and benefit-sharing can help strengthen trust and ensure projects contribute positively to regional development.

Mining and processing are energy-intensive, and access to reliable, affordable, and preferably renewable energy is vital. Nordic power prices are competitive within Europe, but continued investment in capacity will be important to maintain this advantage as demand grows.

Securing skilled talent is an ongoing challenge and priority. Interest in mining careers has declined among younger generations, and competition from other sectors, such as oil and gas, adds pressure. Building attractive career pathways and fostering international recruitment will be key to meeting future workforce needs.

Innovative technologies, including AI and electrified machinery, offer opportunities to improve efficiency and sustainability. While adoption has been gradual, growing interest in digital solutions and automation signals a positive trend toward modernisation across the sector.

SOCIAL LICENCE | ENERGY ACCESS | TALENT SHORTAGES | TECHNOLOGY ADOPTION |

|---|---|---|---|

|  |  |  |

While mining is seen as vital for the green transition in Sweden and Norway, public support in Finland is rather mixed. Local communities often support projects for jobs and regional development. Indigenous rights (e.g., Sámi land use) remain a major source of conflict especially in Norway and Sweden. | The industry is energy-intensive and heavily reliant on access to abundant affordable (green) energy. Nordic power prices are highly competitive on a European level but integration into the EU’s power market, global competition and lack of capacity additions threaten competitiveness. Mining and metals could account for 3% of renewables demand 2035. | Attracting and retaining skilled workers is difficult, with declining interest among youth in mining careers and challenges for international talent integration – threatening future workforce pipelines. – Especially challenging in Norway as oil and gas sector attracts many geologists. Globally, metals and mining industry will need 340,000 new jobs by 2035 to scale supply. | New technologies such as AI, electrified machinery and other innovations present opportunities to combat operational inefficiencies and declining ore grade but suffer from slow adoption rates. •Many operators remain risk averse and are not willing to jeopardise billion-dollar assets with unproven technologies. |

“Public acceptance remains a challenge, with ‘not in my backyard’ attitudes and outdated perceptions of mining practices.” – Mining & Refining Company | “Energy costs can be up to 50% of smelter expenses – policy changes have a major impact” – Refining Company | “Persistent difficulty attracting young professionals to mining programmes and industry roles across the Nordics.” – Industry Expert | “Mining operators are often hesitant to use new technology because the risks to large, long-term assets are too high.” – Industry Expert |

Note: Quotes are paraphrased

Source: Business Sweden interviews and analysis