Mapping the Nordic tourism startup landscape

To move from early-stage ideas to meaningful and relevant industry solutions, you need to understand the broader ecosystem in which you are working. It’s intuitive: Innovation doesn’t happen in isolation, and in the Nordics, it seems almost obvious that there is potential for innovation to travel the borders – also in terms of tourism solutions.

Across the Nordics, we share common values, such as a high level of trust, which makes it easier to scale products across the region. We’ve actually viewed scaling across the Nordics more as an extension of the home market than as an international expansion.

… in conversation with Anders Mogensen, Founder of Founderment. Read the full interview here.

From the start, XNTC has focused on identifying cross-Nordic innovation potential. However, it quickly became clear that a comprehensive, connected cross-Nordic overview of the tourism-related startup landscape was missing.

To bridge this gap, the XNTC programme created a mapping of the Nordic tourism startup landscape, as a tool to search for existing solutions, connecting findings from problem workshops, hackathons, and design sprints with the wider trends.

The mapping now allows us to zoom out across the Nordic landscape, identify patterns and blind spots, and uncover where new solutions and innovation can add the most value to the industry.

A Mapping with Challenges

Mapping the Nordic tourism startup landscape hasn’t been without its challenges. The landscape is scattered, largely unclustered, and mostly unmapped — particularly across borders.

The difficulty also lies with definitions: Unlike sectors such as fintech, proptech, or health tech, where startups are neatly categorised under clear labels, 'travel tech' remains somewhat loosely defined and fragmented across the Nordic region. Furthermore, tourism itself is not a standalone industry but overlaps with multiple other sectors, altogether making it harder to pinpoint and search for startups using standard labels or keywords.

Finally, the startup landscapes change constantly. With most data points collected in the late 2023, this mapping is a snapshot overview with some of the included companies likely already out of the market, and with new ones entered.

As such, the XNTC startup mapping cannot be considered exhaustive, however with data collected on approximately 450 startups across the Nordic tourism eco-system, it provides a good, comprehensive and useful overview of a landscape that has hitherto been underexplored. Perhaps this will be the start of more mappings to come…

In this chapter, you will find:

- A snapshot overview of the Nordic tourism startup ecosystem.

- Insights revealed by the mapping in terms of trends shaping the Nordic tourism startup landscape, and potential opportunity gaps.

- Investor insights from the Nordic tourism landscape.

XNTC MAPPING APPROACH

In line with this Guidebook, this mapping is not a scientific nor statistically exhaustive analysis, but instead a practical, data-driven overview designed to guide firstly, the XNTC search for solutions within the prioritised problem fields of the programme, and hopefully also as a resource to a wider circle of tourism industry stakeholders and policymakers seeking to understand the landscape and identify opportunities across the Nordic tourism ecosystem.

Definitions and Criteria

Defining startups in the travel and tourism landscape proved complex, as many companies do not identify explicitly as part of the "visitor economy" or “tourism industry”. Instead, they position themselves within sectors like circular economy, personal mobility, energy efficiency, or sharing economy – though with relevance to and customers within the tourism sector.

For this mapping, we applied the following definition:

- A startup is a growth-focused company offering technology-based solutions or services relevant to travel and tourism.

- Startups need not officially belong to the tourism sector by industry codes but must demonstrate solutions applicable to the visitor economy and tourism industry.

- Growth focus, not age, is key. Startups may be 10+ years old if they are actively scaling through partnerships, investment, and innovation.

When categorising startups, we adopted an approach of referencing a sector and sub-sectors, inspired by Investopedia, where a sector is a distinct part of an economy characterised by specific types of businesses or activities.

Following this definition, the Nordic travel and tourism landscape can be considered as a sector, while the startups analysed in this report fall under a series of subsectors, e.g. technology, sustainability, education, mobility, experience design, etc.

Sources and Data Collection

The mapping relied on publicly available sources and manual screening to ensure data relevance and accuracy. Key sources & steps included:

- Publicly available databases & startup hubs: Data was gathered from the databases of startup hubs and lists like The Hub by Danske Growth Hub, EU-Startups, and Dealroom, and more.

- Manual screening: Startups often come and go, making lists and overviews dynamic and, at times, unreliable. Most startups from databases were therefore manually screened, to the extent possible, and enriched by other sources.

- Merging data: The XNTC desk research was merged with data from Nordic Traveltech Lab (Norway), adding 70 companies to the sample after screening for doubles, actuality, and relevance according to the criteria.

- Local Scouting: XNTC reached out to several Nordic destination organisations (DMOs), who contributed with lists of startups in their destinations – again screened and entered manually into the mapping.

Given the dynamic nature of startups — many appearing and disappearing quickly — all entries were manually screened to reflect their current status. But as this was mostly done in last half of 2023 (and early 2024), by the time of you reading this Guidebook, the landscape will most likely already have changed somewhat again.

LOOKING ACROSS THE LANDSCAPE

Tourism is a highly diverse industry, encompassing a wide range of sub-sectors — a diversity also reflected in the mapped startup landscape.

Key sub-sectors within this tourism landscape include technology, experiences, mobility, and sustainability, with 46% of startups falling partly or fully into these categories.

Globally, hospitality and online booking platforms are often dominant within the travel tech landscape. However, in the Nordic region, the highest concentration of startups is found in the tour & experience and technology provider sub-sectors.

The sustainability and mobility sub-sectors also take some space in the overall landscape of Nordic tourism startups.

Smaller but notable sub-sectors also emerge, including startups offering organisational solutions like Legal & Admin, Finance, and Job & HR Management.

THE DIFFERENT SUBSECTORS IN THE NORDIC TRAVEL & TOURISM STARTUP LANDSCAPE

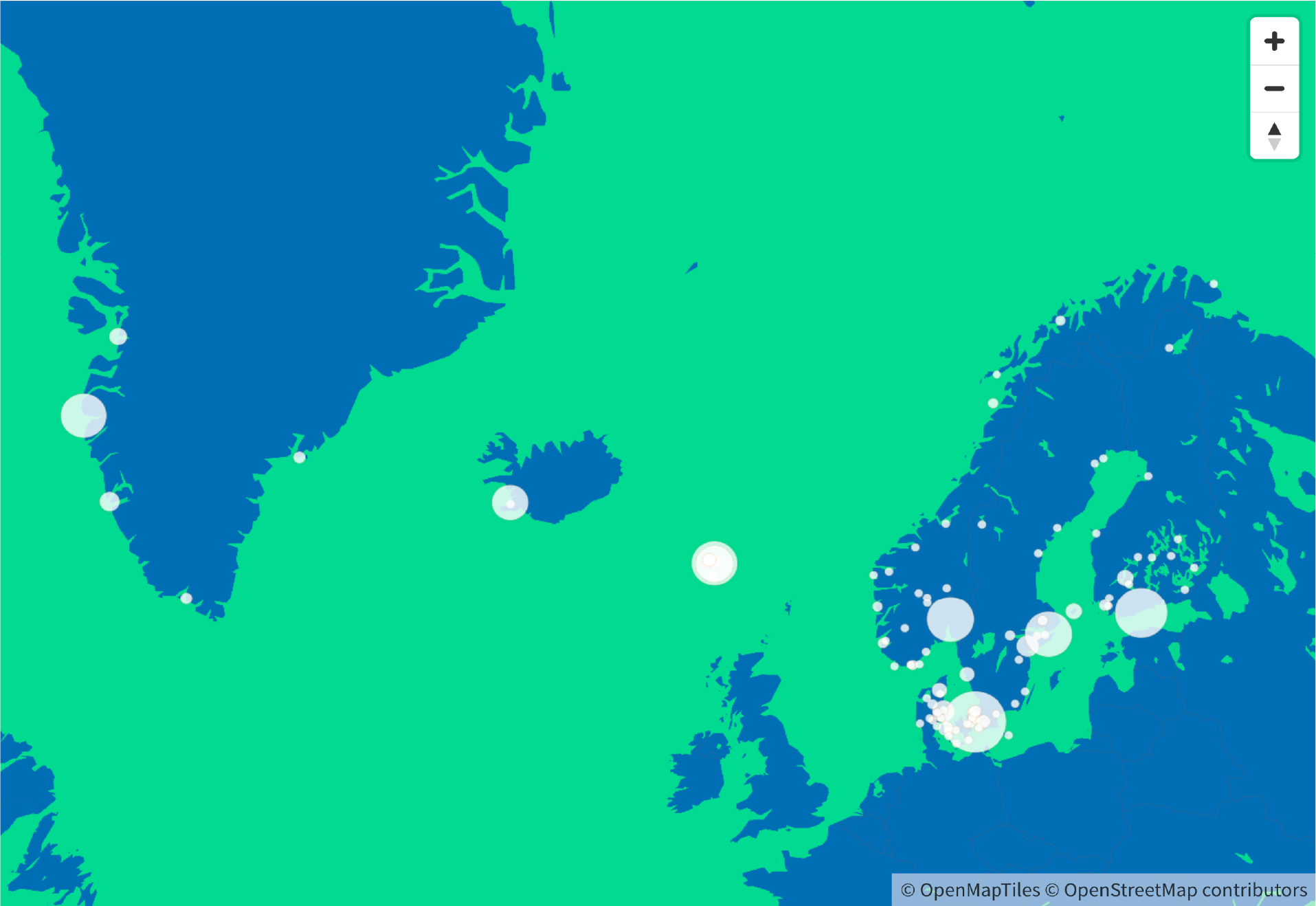

Nordic Capital Cities as Startup Hubs

The XNTC mapping reveals a trend: Most Nordic tourism startups are concentrated in and around capital cities, mirroring patterns seen across other sectors outside tourism (Faster Capital, 2024).

This concentration is no surprise. Bigger cities offer startups access to essential resources: advanced technological infrastructure, knowledge hubs, investment opportunities, support networks, and a strong talent pool – all critical factors for growth and innovation, regardless of industry.

That said, startups – and perhaps especially tourism startups – are not limited to urban centers. The location of startups often depends on the nature of a business and the product or service it delivers – and hence with tourism as the common red thread, there are also many tourism startups outside of the major and capital cities.

CLUSTERS OF THE NORDIC TOURISM & TRAVEL STARTUP LANDSCAPE

Diverse Sector Strengths

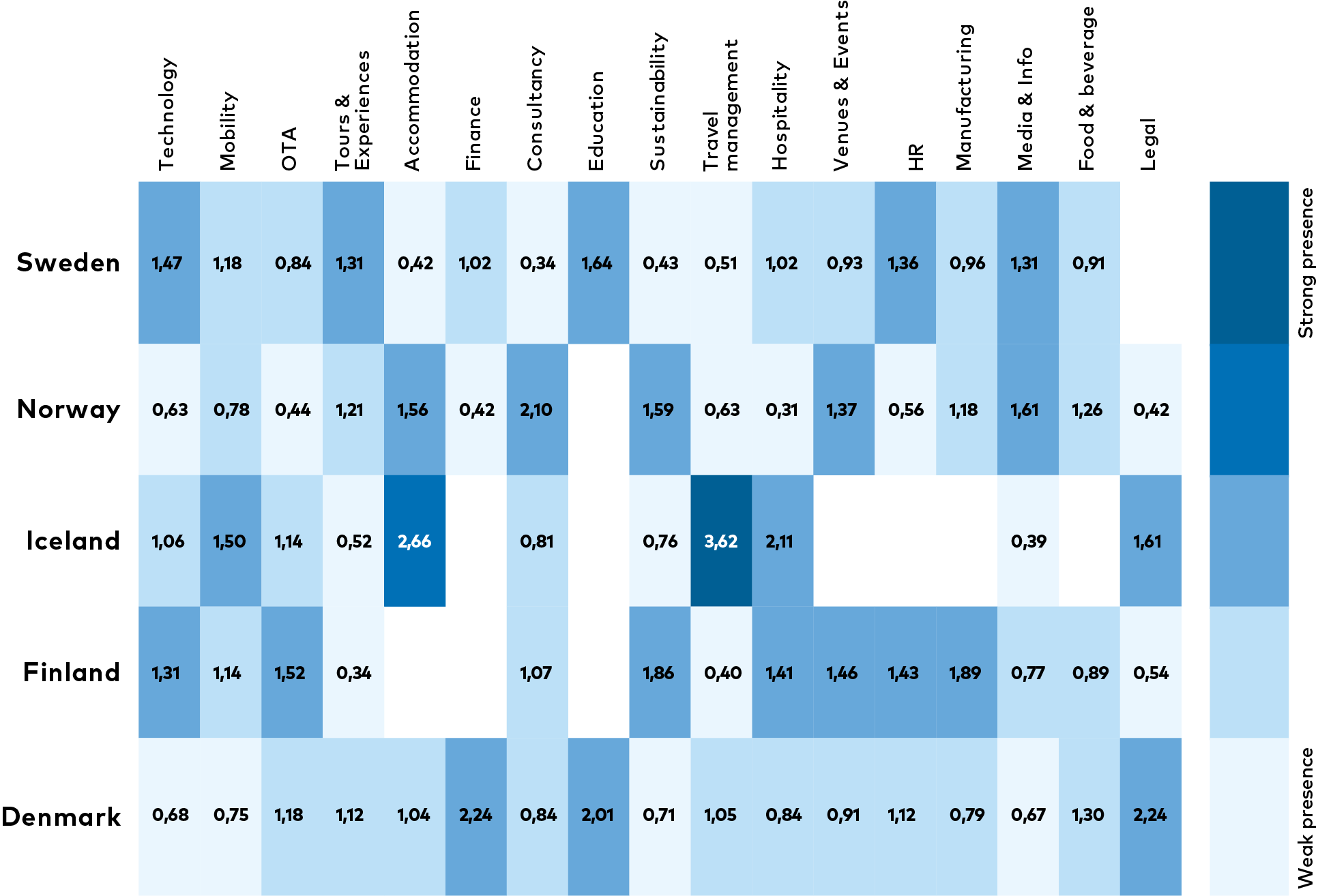

The Nordic tourism startup landscape reveals distinct strengths across countries and regions. Using the Balassa Index – where 1 represents the average or expected value, and higher values indicate specialisation – a heatmap highlights relative concentrations within different sub-sectors across the Nordic countries. So, if a region can show a value 2 in “Finance”, it means that there are double as many start-ups in finance as you would expect to find in an average Nordic region.

Although based on a limited dataset, the heatmap indicates that Iceland has notable specialisation in Accommodation and Travel Management, while other Nordic countries display a broader, less concentrated spread across various sectors, though still with indications of regional differences.

By leveraging each Nordic country’s different strengths, the region holds potential to attract different types of investment, talent, and partnerships with potential to strengthen the Nordic tourism startup ecosystem.

HEAT MAP DISTRIBUTION OF NORDIC TRAVEL & TOURISM STARTUPS ACROSS SECTORS BASED ON THE BALASSA INDEX

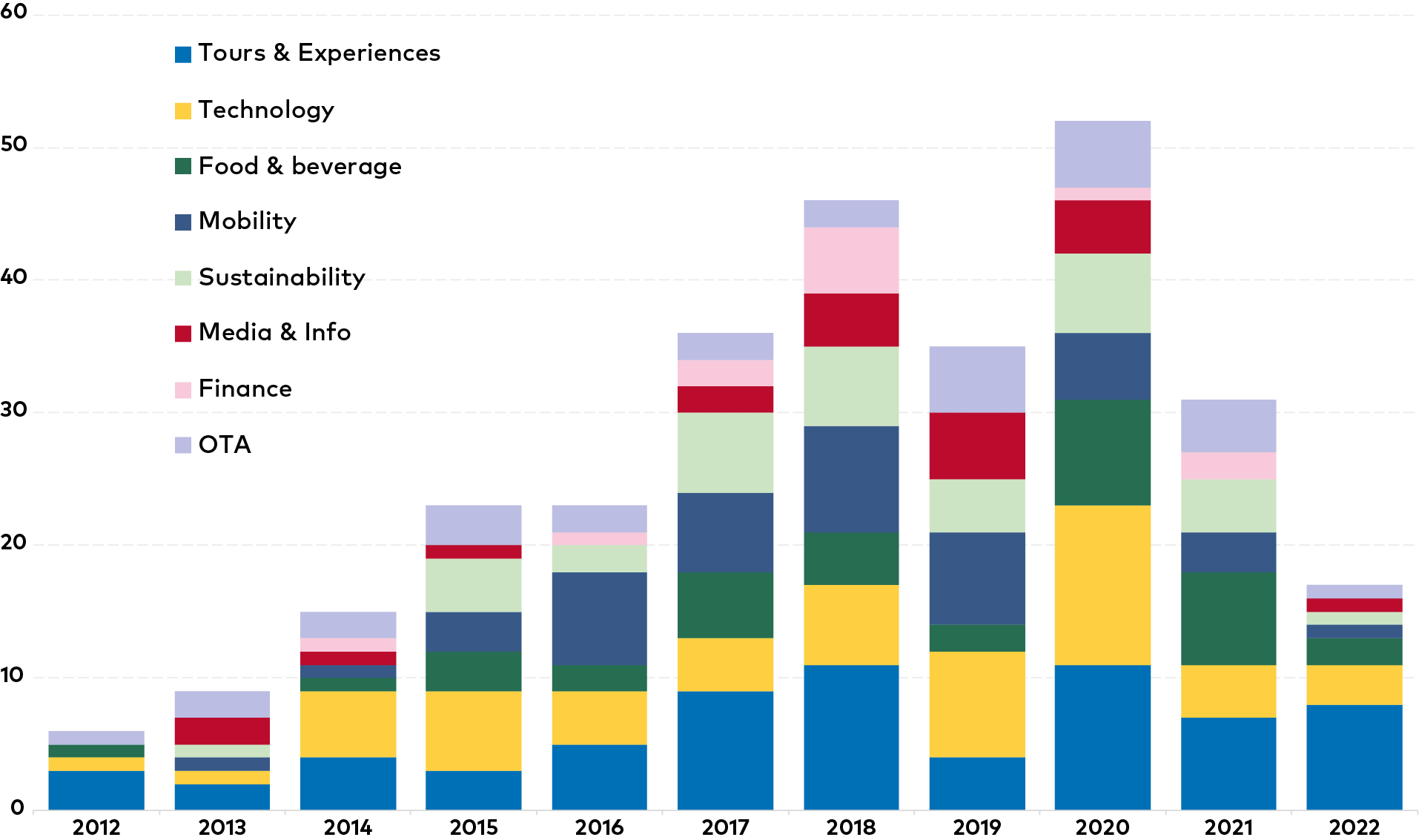

Big Sectoral Shifts Following the Pandemic

The number of Nordic tourism startups founded across sub-sectors reveals clear trends before, during, and after the COVID-19 pandemic.

Tours & Experiences and Food & Beverage startups saw a sharp rise in new ventures before the pandemic, followed by a steep decline when travel restrictions hit. In contrast, Technology-providing startups peaked during the pandemic as demand for digital solutions surged to address operational challenges.

Sub-sectors like Sustainability, Media & Information, and Finance experienced steady growth leading up to the pandemic but saw a slowdown during its peak. These shifts highlight how external disruptions can accelerate, stall, or reshape entrepreneurial activity across the tourism and travel startup landscape.

NUMBER OF NORDIC TOURISM & TRAVEL STARTUPS FOUNDED ACROSS SUBSECTORS

A Sector of Smaller Companies

The Nordic tourism startup landscape is predominantly made up of smaller companies. A significant 69% of mapped startups have fewer than 10 employees, suggesting a high concentration of early-stage businesses or a reflection of broader challenges in scaling tourism businesses, possibly driven by economic, social, or structural factors specific to the Nordic tourism market.

In the mid-range, 26% of startups have fewer than 50 employees, representing those who have begun to scale but remain relatively small. At the top end, 5% of startups in the mapping employ more than 250 people, likely reflecting successful scale-ups that have managed to innovate, address market gaps, and grow significantly.

The large proportion of micro-sized startups (fewer than 10 employees) raises questions about a potential growth ceiling within the tourism sector. Whether due to market size, funding limitations, or other barriers, this trend may constrain expansion opportunities for Nordic travel and tourism startups.

Further comparative research with other regions could provide valuable insights into the factors influencing growth and scalability, shedding light on opportunities to better support startup development and long-term success in the cross-Nordic market.

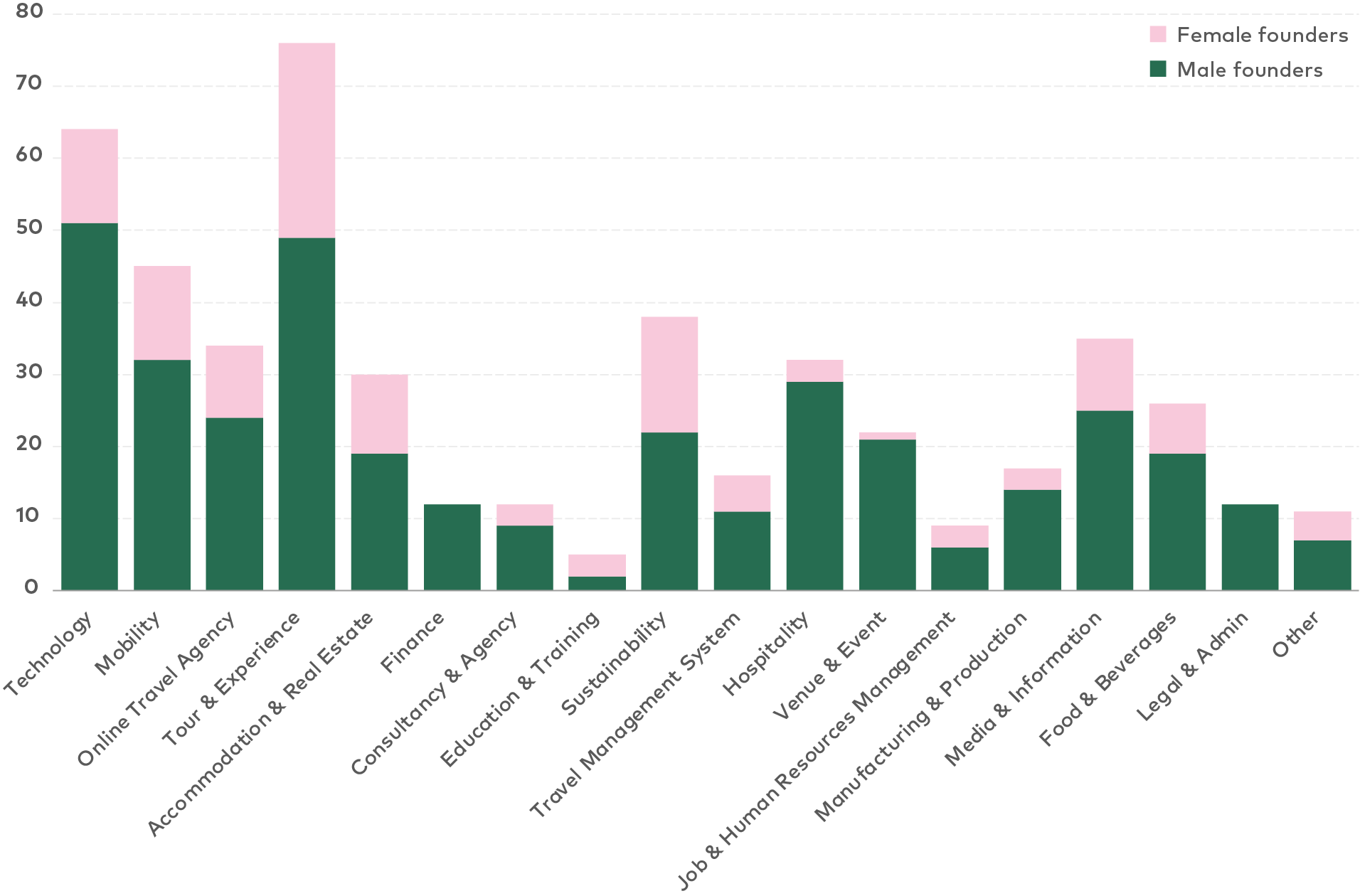

Female Founders in Tourism

In 2023, nearly 25% of all startups in Finland, Norway, and Denmark had female founders, highlighting a gender gap as approximately three-quarters of mapped travel and tourism startups are founded by men.

Interestingly, Iceland, despite being consistently ranked the world’s most gender-equal country (World Economic Forum, 2023), appears in this mapping with the lowest share of female-founded tourism startups at just 17%.

Across sub-sectors, male founders dominate in all categories, though the size of the gender gap varies. Sub-sectors such as Technology Providers, Venue & Event, Hospitality, Finance, and Legal & Administration show the widest disparities. In contrast, sectors like Education & Training, Sustainability, and Tour & Experience have the highest percentages of female founders.

The findings indicate a gender imbalance within the Nordic tourism startup landscape. Greater focus on gender diversity, particularly in sub-sectors with significant gaps, is needed to foster a more inclusive, competitive, and innovative startup ecosystem.

FEMALE AND MALE TRAVEL STARTUP FOUNDERS ACROSS CATEGORIES IN THE NORDICS,1991-2023

INVESTING IN NORDIC TOURISM STARTUPS: A NICHE?

To complement the cross-Nordic startup mapping, this section explores the investor landscape in Nordic tourism. This involves firstly an overall scan of the landscape, as well as an interview with one of the highlighted investors.

Scanning VC trends in Nordic Tourism

The findings of the investor scan reveal a key challenge: Only a small handful of venture capital (VC) funds focus directly on travel and tourism. A notable exception is the Danish fund Founderment, which, as of December 2023, had made five investments in the tourism industry.

Interestingly, tourism and travel tech startups are often categorised under broader and more established labels like SaaS, Fintech, or Mobility in fund portfolios. While this approach increases their chances of securing funding, it also makes tourism-focused investments less visible, potentially distorting perceptions of investor interest in the sector.

When looking at specific investments, a clear trend emerges: Investors gravitate toward technology-driven startups with strong scalability and global market potential (see table XX). This preference reflects the growth expectations of VC funding and highlights the challenges faced by more traditional tourism business models in attracting investment.

NORDIC STARTUPS AND THEIR INVESTORS

Start-up name | Investors | Country | Round type | Source |

Landfolk | Founderment, Seed Capital | DK | Seed | |

BeCause | Ugly Duckling | DK | Preseed | |

Holdbar | Firstminute capital | DK | Seed | |

Campanyon | start-uplab and angels | NO | Pressed | |

Asistobe | DSD, Valinor | NO | Pressed | |

Chooose.Today | Genzero | NO | A-round | |

Acamp | Spintop | SW | Preseed | |

Fast Travel Games | Brightly Ventures | SW | Seed | |

Allihop | Rockstart | SW | Preseed | |

Stayify | Angel investors | FI | Angel round | |

Reveel | Inventure and Angels | FI | Preseed | |

Bob W | Evli Growth Partners | FI | Growth | |

Travelshift | General Electric | IS | Growth | |

PaxFlow | Brunnur | IS | Seed |

LEADING ACTIVE INVESTORS IN NORDIC TOURISM & TRAVEL

Investor | Country | Tourism Investment | Website |

Founderment | DK | Landfolk, Holdbar, Raus, Plumguide, Pere | |

Seed Capital | DK | Landfolk, Holdbar | |

Ugly Duckling | DK | BeCause | |

start-upLab | NO | Campanyon, Favrit | |

Shibsted Growth | NO | Campanyon | |

Katapult | NO | Brim Explorer | |

Almi Invest | SW | Handiscover | |

Backing Minds | SW | Campcation, Mylla | |

Spintop Ventures | SW | Acamp | |

Icebreaker.vc | FI | Valpas | |

Inventure | FI | Reveel | |

Vendep | FI | Hostaway | |

Brunnur | IS | PaxFlow | |

Frumtak Ventures | IS | Kaptio | |

Crowberry | IS | Greenbytes |

Scaling Tourism Innovation: A Nordic Dilemma?

In conversation with Anders Mogensen, Founder of Founderment

The Nordic region holds potential to become a leader in sustainable and tech-driven tourism innovation. Anders Mogensen, Founder of Founderment — an early-stage VC fund — shares his insights on where the opportunities lie, what makes tourism startups investable, and how technology is shaping the next chapter of the industry.

For you as an investor, why does tourism stand out as a promising area for investment?

The industry has become more open to digital transformation in recent years. Historically, the digital offerings in the industry were controlled by a few large players, but digitalisation has recently opened the market to new entrants.

In our case, we’ve invested in a company called Holdbar, which offers tourism companies a much more customised digital solution. It handles both the digital and practical needs of companies like hotels, tour operators, and travel experience providers.

What makes Nordic tourism and travel tech startups interesting to invest in?

Well, the Nordics aren’t inherently interesting to us as a venture capital company ... Everything we invest in must have the potential to scale beyond the Nordic countries – even ideally also outside the European market. The Nordics are, however, a great market to launch a company, especially for consumer-facing solutions.

We’ve seen a momentum for applications that attract new tourists to the region when it highlights special hospitality opportunities. In our portfolio, for example, we have Landfolk, which provides access to high-quality and unique vacation rentals that weren’t even available on the market before! For these kinds of solutions, the Nordics serve as a great launchpad. Saying that, it’s crucial to take the next steps beyond the Nordic market soon after achieving product-market fit in the region.

In your view, what unique characteristics define the Nordic market, and how do they impact scaling strategies for startups?

Across the Nordics, we share common values, such as a high level of trust, which makes it easier to scale products across the region. We’ve actually viewed scaling across the Nordics more as an extension of the home market than as an international expansion.

However, this homogeneity can also be a weakness. You might end up building something that is hard to scale outside the Nordics.Sometimes we see this limitation reflected in founders' mindsets. They might think, "If we’ve nailed our home market and launched in other Nordic countries, we’ve made it." But that’s rarely enough to make a startup interesting for us as a venture capital firm.

What challenges do startups face when raising funds for international growth after proving their potential in the Nordic region? And is it hard for you as a venture fund to help your portfolio raise funding?

Yes, definitely! Tourism isn’t the most attractive industry for investors, and this holds us back from doubling down on it. I think this is largely because many startups in the space lack the grandiosity, we see in other B2B SaaS products. It’s rare to find Nordic travel tech startups with a mindset to conquer the global market. More often, they focus on incremental improvements, like making trip searches easier. That vision is too limited for a venture journey today.

Has the tourism industry reached a plateau in innovation, or are there untapped opportunities for startups to disrupt the market?

The tourism industry tends to be industry-first and tech-second — but maybe it should be the other way around. What I mean is that we shouldn’t be limited by the normal boundaries of the tourism industry. There is a glass ceiling in the industry, and it’s mainly created by the industry itself. Overcoming this requires building grander visions that go beyond current limitations. Sometimes, scaling may even involve tapping into adjacent industries to build something big enough for the long term. I fear the Nordic tourism industry could become its own limitation.

.. Many startups in the space lack the grandiosity, we see in other B2B SaaS products. It’s rare to find Nordic travel tech startups.

Anders Mogensen, Founder of Founderment

How can the Nordic tourism industry overcome its limitations to attract more substantial venture capital investment?

We need a higher degree of innovation and for industry players to focus more on this. Moving beyond local and industry-specific thinking is crucial to creating new startup category leaders. For example, in Understory, we invested in them becasue we see the potential for them to become the Shopify of the tourism industry - a central hub that allows others to tap into the market. That is a grand vision and something that excites venture capitalists. Startups need to break out of traditional trajectories, and travel tech cases have struggled to prove this to us and other investors.

It will be interesting to see how travel tech evolves with the latest advancements in technology, like AI. With AI we see a lot of innovation in other industries, but in the tourism industry it’s, well, not substantial innovation - but merely small incremental improvements - rarely something that would really excite a venture capital fund. Looking ahead to technologies such as quantum computing, which show promise in other industries, it’s also hard to predict how they might move the needle here in the tourism industry. Nonetheless, we’re eager to follow and support this development if it comes with greater visions to strengthen not just the Nordic, but the global market.

SO, WHAT DID WE LEARN FROM MAPPING THE LANDSCAPE?

The startup mapping and investor scan shed light on opportunities and challenges within the Nordic tourism startup ecosystem.

On the one hand, the region is rich with diversity and innovation across different industry-related sub-sectors. Technology-driven solutions are gaining ground, and the Nordics can serve as a larger extended home-market and hence a strong launchpad of new solutions.

On the other hand, significant barriers remain. The ecosystem is fragmented, and many startups struggle to scale — both within the Nordics and beyond.

Investors tend to prioritise solutions that fit broader, established categories like SaaS or fintech, leaving tourism-specific innovations less visible.

For innovation programme leaders and Nordic ecosystem builders, these findings could point to three critical questions to ask yourselves:

How can you support Nordic startups in testing and scaling across the Nordic region? And later beyond the Nordics?

How can you help bridge the fragmented Nordic tourism startup ecosystem?

How can you better showcase tourism startups to investors?

What can we learn from global tourism innovation ecosystems?

How do Nordic startups compare in technology adoption, scaling speed, and investment traction?

How do Nordic startups compare in technology adoption, scaling speed, and investment traction?

Sources for data analysis

AVERAGE TIME TO REACH PROFITABILITY AT A STARTUP – Zippia (https://www.zippia.com/advice/start-up-profitability-statistics/)

Carta 2024: A sector-by-sector guide to the gender gap among startup founders (https://carta.com/data/gender-gap-by-sector-2023/)

Choose the right location for your startup – Faster Capital (https://fastercapital.com/content/Choose-the-Right-Location-for-Your-Startup.html)

Global Gender Gap 2023 - World Economic Forum (https://www3.weforum.org/docs/WEF_GGGR_2023.pdf)

Global startup Ecosystem Index 2023 - startup Blink (https://techbbq.dk/wp-content/uploads/2023/09/Startup-Blink-GSEI-2023.pdf)

Gender parity: Here’s what leading countries are getting right – World Economic Forum, 2023 (https://www.weforum.org/stories/2023/06/global-gender-gap-parity/)

Innovation Lab Asia - A Guide to Nordic Innovation (https://innovationlabasia.dk/wp-content/uploads/ILA-report_Nordic-ecosystem_FINAL.pdf)

Nordic Impact startups 2023 - Dealroom, Danske Bank Growth, and Stockholm (https://danskebankgrowth.com/-/media/danske-bank-com/pdf/growth/nordic-impact-startups-2023.pdf)

Nordic startup Employment 2023 - Dealroom & Danske Growth (https://dealroom.co/uploaded/2023/09/Nordic-Startup-Jobs-2023-4.pdf?x67760)

Startup Surge: Pandemic Causes New Businesses To Double – Forbes (https://www.forbes.com/councils/theyec/2021/01/20/startup-surge-pandemic-causes-new-businesses-to-double/)

Travel and Tourism Tech Startup Ecosystem and Investment Landscape - UNWTO (https://www.unwto.org/travel-and-tourism-tech-startup-ecosystem-and-investment-landscape)

What Is an Economic Sector and How Do the 4 Main Types Work? Investopedia (https://www.investopedia.com/terms/s/sector.asp)

What is the average lifespan of a startup? Faster Capital (https://fastercapital.com/questions/what-is-the-average-lifespan-of-a-startup.html)

What is a startup? the Hub definition - The Hub (https://insights.thehub.io/insight/what-is-a-startup-the-hub-definition/)