Nordic Economic Policy Review 2024

Comment on Torben M. Andersen:

Fiscal Stabilisers in Denmark

Paul Lassenius Kramp

Torben M. Andersen provides an excellent overview of fiscal policy stabilisation in Denmark. This review of his article provides a few supplementary comments.

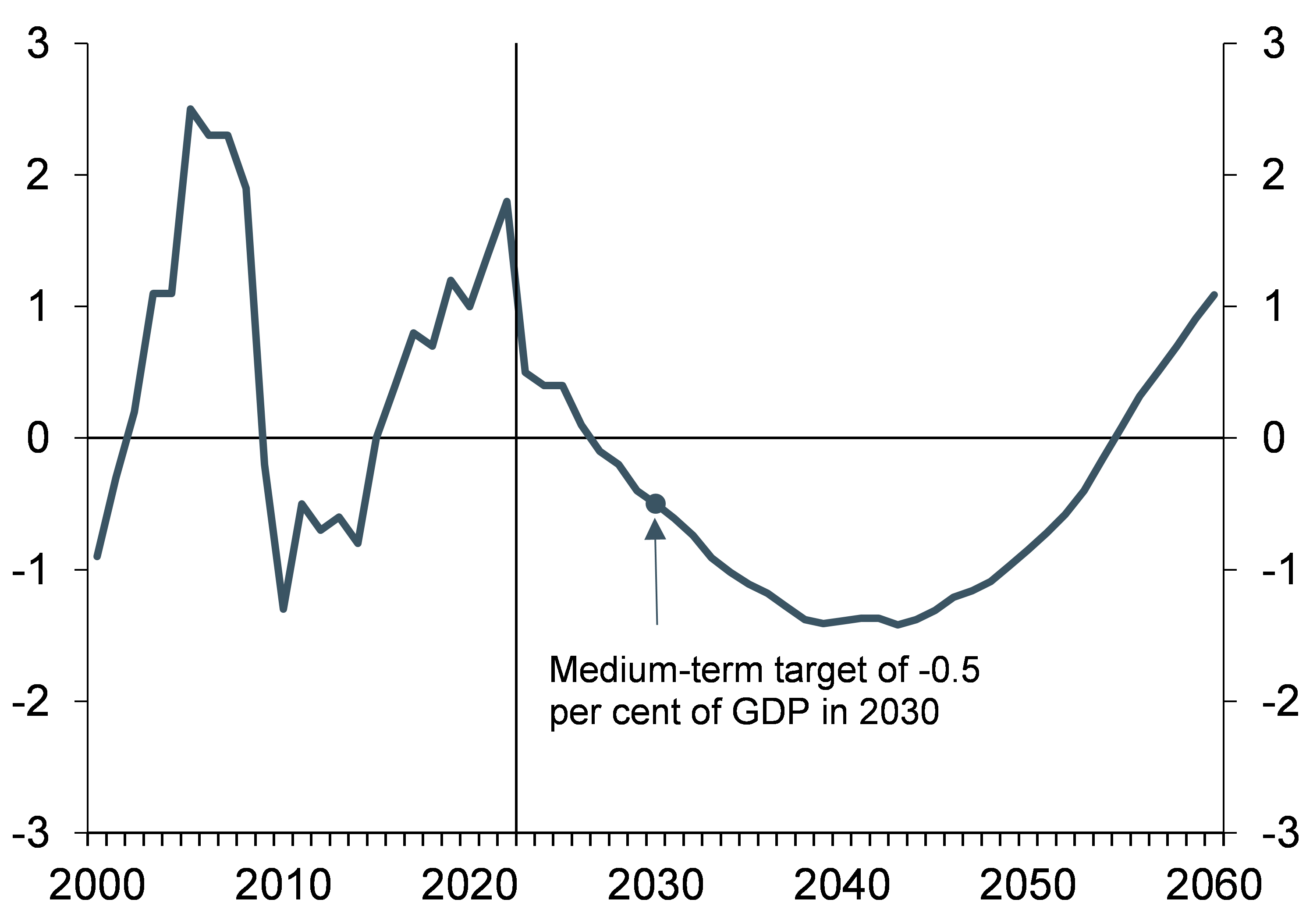

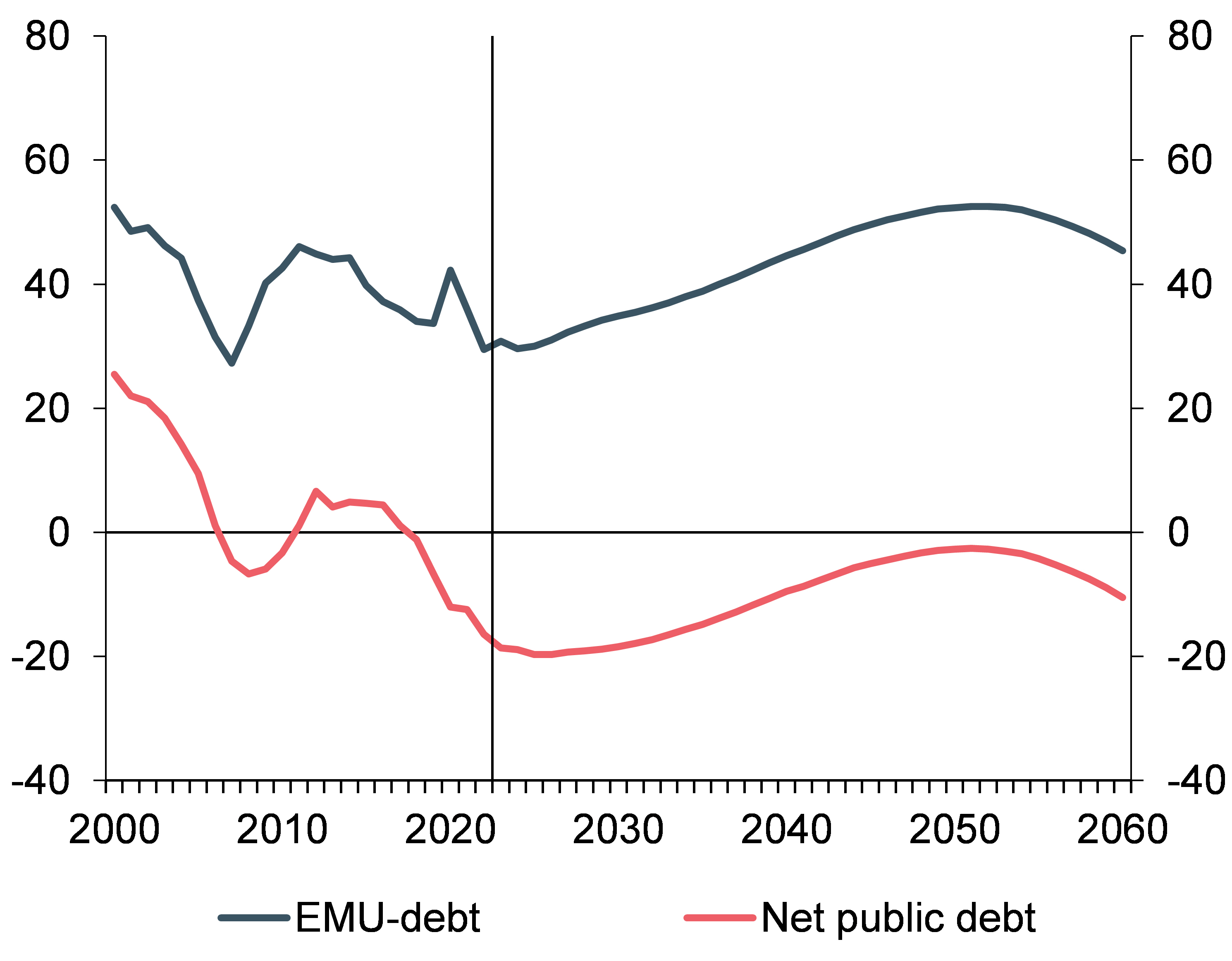

In Denmark, the medium-term target for fiscal policy is a structural budget balance of -0.5% of GDP in 2030, cf. Figure 1. This is consistent with fiscal sustainability (the sustainability indicator is estimated to be positive) and low public debt as a share of GDP, cf. Figure 2. The 2030 target implies a fiscal space for political prioritisation, including covering the expense of demographic changes, higher defence spending, the green transition, etc. It also provides room for discretionary stabilisation in the event of an economic downturn, within the structural deficit limit of -1% of GDP stipulated in the Danish Budget Act.

In case of exceptional circumstances, it is possible to deviate from the deficit limit.

The structural deficit limit of -1% of GDP laid out in the Budget Act allows the automatic stabilisers to operate freely in a normal economic downturn while complying with the deficit limit on the actual budget balance of -3% of GDP in the Stability and Growth Pact, cf. Erfaringer med budgetloven 2014-2020, Ministry of Finance, April 2022. In addition, expenditure ceilings in the Budget Act have a stabilising effect as they help e.g. prevent procyclical expenditure slippages during economic upturns.

Figure 1. Structural budget balance

Percent of GDP

Source: Danish Ministry of Finance, August 2023 projection

Figure 2. Public debt

Percent of GDP

Source: Danish Ministry of Finance, August 2023 projection

The automatic stabilisers are large in Denmark compared to many other countries, which in itself reduces the need for discretionary stabilisation. Active stabilisation is primarily used to counter large economic shocks (such as the COVID-19 pandemic and high inflation of recent years), while it is generally considered unrealistic to finetune the business cycle. This is in part due to the uncertainties of the current and future business cycle, the lags in fiscal policy between recognising issues, making decisions and implementing them, and the adverse effects if frequent adjustments are made to tax rates, the quality of public services, etc.

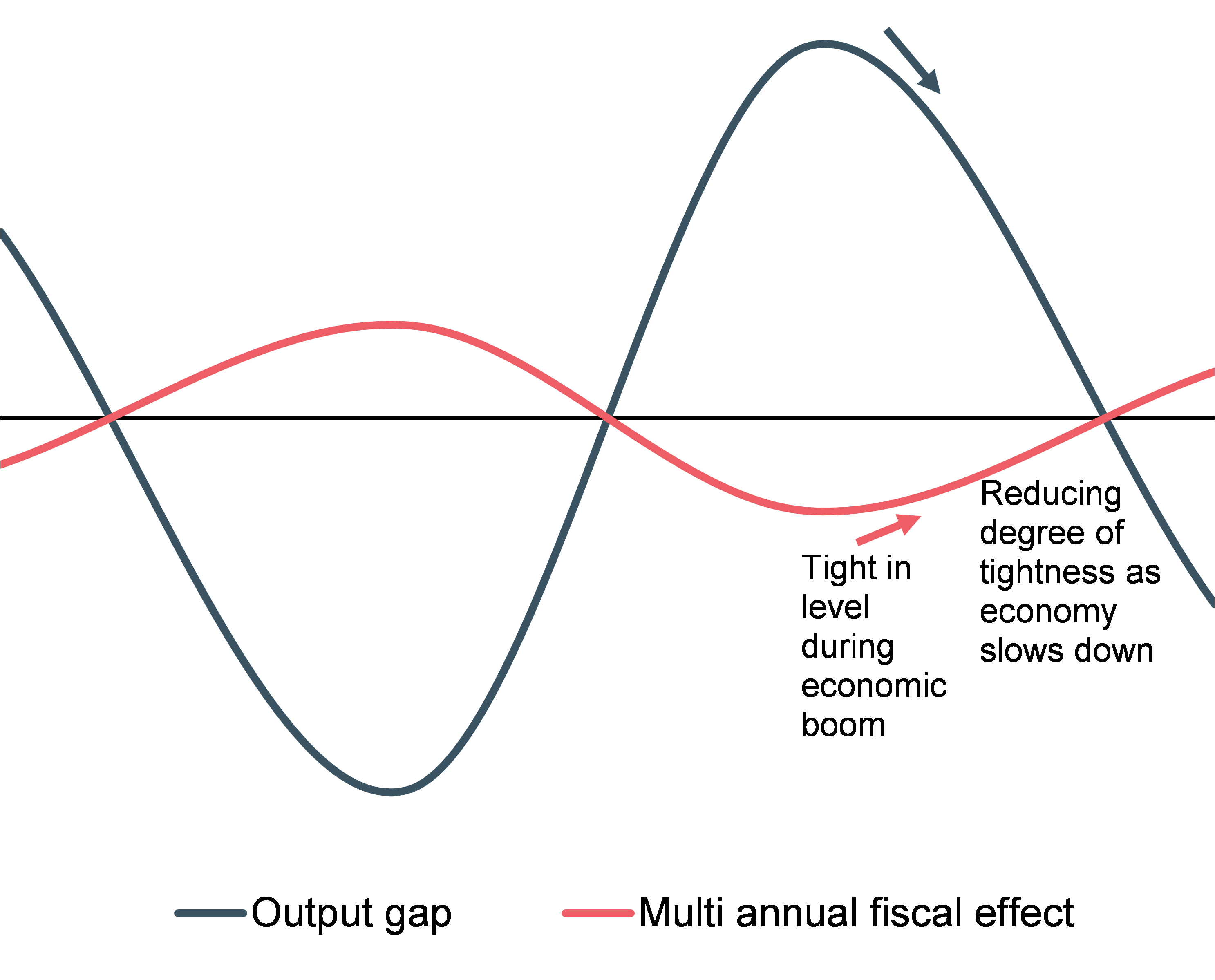

The Danish Economic Council (2007) described a mechanical rule implying that discretionary fiscal policy can aim to close ¼ of the output gap that would exist in the absence of discretionary measures. The ¼ assumption reflects the uncertainties related to discretionary fiscal policy. According to the rule, fiscal policy must be tight in an economic boom – measured in level, not annual tightening – and expansionary in a downturn. This implies that fiscal policy should not be tightened further from year to year when the economy slows down while the output gap remains positive. Instead, it may be appropriate to reduce the degree of tightness to support a soft landing, cf. the red and blue arrows in Figure 3. This is given the assumption that fiscal policy in the previous years was appropriate.

Figure 3. Illustration of fiscal stabilisation according to a mechanical rule

Source: Economic Survey, August 2023

Figure 4. Fiscal effects compared with benchmarks from a mechanical rule

Note: The multi-annual fiscal effect measures the impact of the discretionary fiscal and structural policy since 2019 on the output gap in a given year

Source: Economic Survey, August 2023

Source: Economic Survey, August 2023

In practice, discretionary fiscal policy does not follow a mechanical rule, but it can be used as a benchmark for comparison with the fiscal stance. The Danish Ministry of Finance measures the impact of discretionary fiscal and structural policy on the output and employment gaps by means of the so-called “fiscal effects”, which are based on calculations on the new macroeconomic model, MAKRO. Note that this is not equivalent to the changes in the structural budget balance; see, e.g., Economic Survey, December 2023.

In the forecast Economic Survey, August 2023, the multi-annual fiscal effect – which measures the impact of fiscal policy in the given year and the preceding years relative to the base year in 2019 – is estimated at -0.4 percentage points in 2024. Thus, fiscal policy helps dampen capacity pressure (output gap), which is in line with the implication of the illustrative mechanical rule, cf. Figure 4.

During the COVID-19 pandemic, the expansionary fiscal policy response in 2020 and 2021 was larger than the illustrative mechanical rule would suggest. This reflects the special nature of the crisis, including the extraordinary need to support businesses and employees and, at the same time, send a clear signal that great efforts were being made to support the economy which in turn contributed to reduce uncertainty.

The fiscal easing in 2020 and 2021 was offset by greater tightening in 2022 and 2023 than the rule would imply. Overall, this means that the level of fiscal policy, i.e. the multi-year fiscal effect in 2024, is broadly in line with the mechanical level rule.