Nordic Economic Policy Review 2026

The Norwegian Tax Experiment – From Idea to Implementation

Simen Markussen and Marie Bjørneby

Abstract

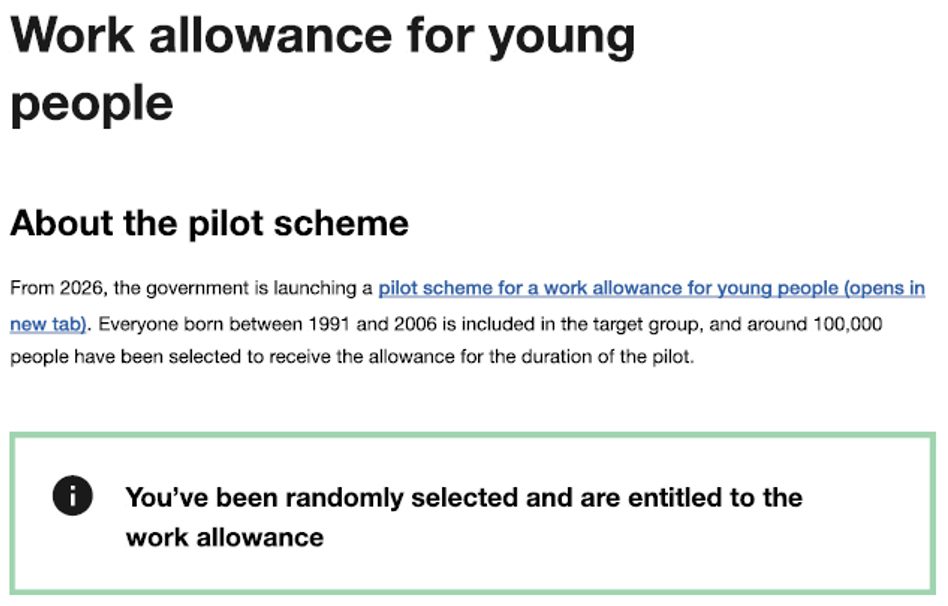

In December 2025, 106,469 young Norwegians received their annual tax card (skattekort), which adds a new feature to the tax system in Norway: an earned income tax credit. The recipients are all part of a large real-world experiment, in which 8% of all taxpayers between the ages of 20 and 35

were randomly assigned to a treatment group. For this group, the tax system includes an additional earned income tax credit.

They will continue to receive the allowance after turning 36, as it is granted by cohort, not age.

In this article, written before any results from the experiment have materialised, we present the experiment, how it came about, and how we worked on its implementation. We aim to present some of the challenges we encountered, as well as the insights we gained while working on the project.

This article is partly based on the early assessment by a joint research group at Norwegian Fiscal Studies, Department of Economics at the University of Oslo and the Ragnar Frisch Centre for Economic Research available [here] .The research group consists of Simon Bensnes, Øystein Hernæs, Morten Håvarstein, Simen Markussen, Magne Mogstad, Oddbjørn Raaum, Ragnhild Schreiner and Gaute Torsvik.

1 Introduction

From 1 January 2026, a randomly selected 8% of all taxpayers in Norway aged 20–35 have a different tax schedule than the rest of the population. The modification includes an earned income tax credit (EITC) targeting people on low and medium incomes. The goal, which is now being put to the test in a large-scale randomised experiment planned to last five years, is to increase labour market participation. In this article, written before any results from the experiment have materialised, we present the experiment, what we can learn from it, how it came about, and how we worked on its implementation. We aim to present some of the challenges we faced as well as the insights we gained while working on this project.

The article is structured as follows. In Section 2, we describe the background to the experiment as the intersection of three different developments. First, a negative development in labour market participation among young adults, at least relative to other countries. Second, an interest in EITC and whether it is a suitable way to increase labour market participation. Third, following the pandemic, there has been an increased awareness of the need for knowledge-based policy and a growing interest in randomised trials. In Section 3, we describe the feasibility study conducted by the research group and the Ministry of Finance, which assessed the expected fiscal and behavioural effects of different designs for EITCs, looked at the opportunities for learning about those effects by using different research designs, and discussed how these insights relate to the legislative requirements for experiments of this kind.

In Section 4, we briefly describe the public hearing and the reactions to the proposed experiment. In Section 5, we describe the practical planning and implementation of the experiment in summer and autumn 2025, in particular, the information sent from the tax administration to randomised groups of taxpayers, the stratified randomisation, a large complementary survey, research ethics, and more.

2 Background

The large-scale experiment can be seen as the result of three developments over the last few years. First, in Norway, as in many other countries, improving labour market participation remains a key challenge for public policy. Over the last 20–25 years, employment rates in Norway have not risen as much as in many comparable countries. As a result, employment rates in Norway are no longer among the highest in Europe, even though they remain relatively high.

The combination of the employment rate not rising and demographic changes is placing a growing fiscal strain on public budgets. As a response, the government has declared its ambition to raise the employment rate among people aged 20–64 from 80.5% in 2023 to 82% by 2030, with a further increase to 83% by 2035. It is considered particularly important to prevent young people from becoming detached from the labour market. Achieving these goals will require a range of policy measures designed both to improve underlying conditions for labour market attachment and to strengthen incentives to work.

One such approach is to use financial incentives to stimulate labour supply. An earned income tax credit (EITC) is a general tool to achieve this aim. It is widely used in OECD countries as an instrument to reduce the tax burden on labour and incentivise employment (e.g., the EITC programme in the US). It typically takes the form of deductions or credits applied to taxable income or directly to tax liability, and it is often, but not always, targeted at people on low and middle incomes.

Norway is one of the countries that has not introduced EITCs into the tax system. It has, however, been proposed several times in recent years, including in the budget proposal from the (outgoing) Conservative government in 2021 and in an expert commission on taxes in 2022 (NOU 2022:20). These proposals constitute the second development that has made the experiment possible.

Despite its use in many countries, there is limited knowledge on the effectiveness of EITCs as a tax instrument. Previous Nordic and international experiences, e.g., Sweden’s broad jobbskatteavdraget, typically lack clear counterfactuals when implemented at full scale.

Several studies have examined how financial incentives, more generally, affect labour supply among marginal workers. A notable example is Canada’s Self-Sufficiency Project, which offered financial bonuses to single mothers working over 30 hours per week. The programme increased employment and income, and reduced poverty (Michalopoulos et al., 2005).

In the US and UK, programmes like Earned Income Tax Credit (EITC) and Working Tax Credit (WTC) provide income support to low-wage workers meeting minimum work requirements. Although not experimental, research using policy variation suggests these programmes have increased labour force participation, especially among single mothers (Eissa & Liebman, 1996; Blundell & Hoynes, 2004; Meyer & Rosenbaum, 2001). However, these findings have recently been questioned by Kleven (2024).

In Norway, reforms to disability benefit rules in 2005 and 2011 showed that stronger work incentives can move people from welfare to work, particularly younger recipients (Kostøl & Mogstad, 2014; Alne, 2018). However, a Finnish experiment with a basic income for long-term unemployed people found no significant increase in employment (Verho et al., 2022).

The existing literature on EITCs suggests they can increase labour supply, but estimating their effects is challenging due to the lack of clear comparison groups (Laun, 2019). One key issue is distinguishing between income effects and substitution effects, both of which influence how individuals respond to changes in taxation. Recent Norwegian research (Graber et al., 2025) finds both income and substitution effects to be strong, with uncompensated elasticities of 0.15 for middle-income individuals and steadily increasing with income up to around 0.5 for high earners, which has significant implications for tax policy.

This uncertainty underscores the need for greater empirical knowledge about behavioural responses to taxation. In the case of earned income tax allowances, both income and substitution effects often point in the same direction (if the allowance is phased out at higher income levels), making it crucial to understand the magnitude of the effects to avoid unintended reductions in labour supply.

The third, and comparatively unrelated, development started with the pandemic, during which the need for knowledge about policy design became acute. A number of attempts were made at the time to conduct randomised trials to learn about the effects of policies such as school closures, labour market interventions, the use of masks, and so forth. After the pandemic, the Norwegian government set up a specialist interministerial core group to strengthen the knowledge system for crisis management (“Knowledge in Crises”) and address the shortcomings in evidence-based decision-making revealed by the COVID-19 pandemic. The group commissioned reports from two expert groups highlighting the need for secure and efficient data infrastructure, rapid access to real-time and raw data, and clearer legislation and ethical frameworks for data use and experimental approaches. Following this, the government has stated that it will seek to facilitate greater use of experiments in the public administration.

Although randomised controlled trials can be effective tools for generating reliable knowledge on policy effectiveness, their use has been limited due to methodological, legal, and ethical challenges, as well as insufficient expertise within government agencies (Gopinathan et al., 2025). To address these barriers, and following recommendations from the expert group, a national guidance service for policy experiments was established in November 2025. Hosted by Statistics Norway, its goal is to create a competence environment to help public-sector agencies identify information needs, assess existing knowledge, select appropriate methods, design and implement experiments, and conduct evaluations.

Setting up this service marks a tangible step toward increasing the use of experimental methods in Norwegian public administration and ensuring that new policy measures are tested more systematically before they are implemented at scale.

3 Feasibility study: researchers and officials working together

In the 2024 budget proposal, the Norwegian government announced that it intended to explore the possibility of implementing a limited pilot scheme for an earned income tax credit for young people:

“The government believes there is a need for greater knowledge about the effects of a work tax credit before considering whether it might be an appropriate measure.”

“The ministry will, with the assistance of relevant research environments, investigate (…) whether the trial scheme can and should be implemented.”

It was clear that the Ministry of Finance would need to work closely with researchers over a prolonged period to achieve this. In January 2024, the ministry invited relevant research communities to an open dialogue meeting to discuss the way forward and what would be required for any potential pilot to deliver the intended learning outcomes. In June 2024, the ministry entered into a research and development (R&D) agreement with a team of researchers from the Ragnar Frisch Centre for Economic Research and Norwegian Fiscal Studies at the University of Oslo, formalising a long-term collaboration to support the development and evaluation of the initiative.

Three questions were central to this assessment:

- Was there a need for greater knowledge about how EITCs affect labour supply?

- Could an experiment contribute to new insights – and how?

- Would such an experiment be feasible given the legal and ethical frameworks, administrative considerations, and the need to safeguard the legitimacy of the tax system?

Based on existing evidence, it is hard to assess whether an EITC is an appropriate policy measure to boost labour supply. Theory predicts that labour supply can be affected through three channels: (a) extensive margin effect—by lowering participation tax rates, the EITC makes taking a job more attractive; (b) income effect—higher disposable income may reduce the hours worked by those who already have jobs; (c) substitution effect—changes in marginal tax rates change the payoff from an extra hour of work. If the EITC is to target low and middle incomes, it needs to be phased out for higher earners. This increases the effective marginal tax rate in the phase-out segment, and both income and substitution effects are expected to reduce labour supply.

EITCs can be designed in a number of ways, varying in size, phase-in, and phase-out. To quantify the expected effects of different designs, the research group started by developing a quantitative labour supply model to predict labour supply responses, both on the extensive and intensive margins, to changes in the tax schedule. The model was applied to microdata for the full population of taxpayers in the relevant age range and combines register-based income and benefit data with parameterised behavioural responses (participation and intensive-margin elasticities), explicit treatment of means-tested benefit tapering, and stochastic participation decisions. Potential earnings for non-participants are imputed as 80% of observed employed peers with the same sex, age, and education.

In the process, the behavioural and fiscal consequences of a number of designs were simulated, before one was recommended. It should come as no surprise that researchers designing an EITC must address certain unavoidable properties:

- The larger the deduction, the larger the effect on labour market participation.

- The larger the deduction, the larger the reduction in tax revenue.

- An EITC that targets the low- and middle-income segment will involve a phase-out. This lessens the reduction in tax revenue but has a negative labour supply effect on the intensive margin.

In order to predict the quantitative importance of these factors, researchers need both a model and data for the income distribution. Needless to say, such predictions involve a high degree of uncertainty.

Table 1 shows the key behavioural parameters that were set exogenously: In the baseline scenario, the participation elasticity was set to 0.5, the compensated elasticity to 0.1, and the income effect to −0.05.

Table 1. Key behavioural parameters used in the simulations

Participation elasticity | Income effect | Compensated elasticity | |

Baseline scenario | 0.5 | -0.05 | 0.1 |

Low participation response | 0.2 | -0.05 | 0.1 |

Strong intensive margin response | 0.5 | -0.2 | 0.3 |

Low participation response and strong intensive margin response | 0.2 | -0.2 | 0.3 |

Source: Bensnes et al. (2025)

For a given budget, the government faces a choice: A large deduction combined with a phase-out for higher incomes, or a small deduction without a phase-out. The former should have stronger positive effects on the extensive margin and a stronger negative effect on the intensive margin. Hence, this can be seen as a high-risk strategy, since both the potential gains and costs may be greater than in the alternative that does not involve a phase-out.

This is also illustrated in Figures 1 and 2, which display the self-financing ratio and the change in labour supply relative to the loss in tax revenue under different phase-out alternatives (no phase-out, slow, steep, and extra steep), and different alternatives regarding the strength of the behavioural parameters in the model.

Figure 1. Estimated self-financing ratios with different designs and under different assumptions regarding labour supply responses

Source: Bensnes et al. (2025)

Figure 2. Estimated change in total labour supply with different designs and under different assumptions regarding labour supply responses

Source: Bensnes et al. (2025)

For three main reasons, the alternative with the steepest phase-out was the one recommended by the research group. First, under the baseline modelling scenario, its expected implications were preferred as a (unspecified) weighted combination of outcomes, including expected changes in labour supply, reductions in net taxes and labour market participation, as well as income inequality. Second, the “risk” of potentially weaker responses on the extensive margin and stronger (negative) responses on the intensive margin was accorded little weight, since the experiment only covers a fraction of the population for a limited time. Third, the “riskiness” in terms of stronger expected responses on both margins is actually a strength, given that the purpose is to gain knowledge about these behavioural changes, as larger responses are easier to separate from “noise” in the data.

Table 2 below summarises the predicted effects from the main parameterisation of the model, using the baseline parameters (cf. Table 1).

Table 2. Simulated behavioural and fiscal consequences of an EITC (extra steep phase-out alternative) for all taxpayers aged 20–35 using baseline behavioural parameters

Expected change in… | |

Participation rate | 0.8p.p. |

No. of people participating in the labour market | 9,364 (out of 1.1 million) |

No. of people shifting from a minor to a major job (the “super extensive” margin) | 5,691 (out of 1.1 million) |

Average labour earnings | NOK 1,776 |

…conditional on earnings < NOK 300k | NOK 10,553 |

…conditional on earnings > NOK 300k | NOK -4,478 |

…among disability insurance recipients | NOK 7,841 |

…among students | NOK 4,305 |

…social assistant recipients | NOK 22,442 |

Inequality (Gini after tax) | -0.0098 |

Fiscal effect | NOK -5,169 mill. |

…excluding behavioural responses | NOK -6,015 mill. |

Source: Bensnes et al. (2025)

Needless to say, the conclusions from such a simulation exercise depend on both the data and the model parameterisation. We do not know the income distribution in 2026 and later, and we have used 2022 as a proxy. We believe the uncertainty generated by this aspect will be minor. More important is the assumed strength of the responses, the labour supply elasticities, as illustrated in Figures 1 and 2.

The most important lesson from this is that, if the motivation for introducing the tax credit is to increase labour supply, EITCs can easily be counterproductive, i.e., based on existing knowledge, we cannot rule out them reducing the labour supply instead of increasing it.

The simulation model also allows us to describe the expected labour supply responses in detail. It is instructive to divide the population into six different groups, based on how they are expected to change their behaviour because of the tax allowance:

- Non-participants: Approximately 10% of the population in this age range has no labour income. The EITC reduces their participation tax rate by increasing the net income gain from participating in the labour market. The effect is unambiguously to increase labour supply. With the baseline parameterisation, we predict the tax allowance will increase the participation rate by 0.8 percentage points.

- “Super-extensive” margin movements among very low earners: A proportion of the population participates in the labour market, but to a very low degree. As such, they are unaffected by the EITC on the intensive margin (their income is below the basic deductions in the tax system). When offered the tax allowance, we predict that some of these individuals will increase their labour supply on the extensive margin in the same way as non-participants.

- Low earners: For workers with incomes between the basic deductions and the tax allowance for earned income (200k – 320k), the marginal tax rate will decrease substantially, by 22 percentage points. This indicates substantial positive labour supply effects. This group will also have a lower average tax rate and a corresponding reduction in labour supply due to the income effect. In theory, the net labour supply response is thus ambiguous. In our parameterisation, however, the model predicts labour supply will increase.

- Maximum gainers: For people earning between 320,000 and 335,000, the EITC is maximised, and the marginal tax is unaffected. For this relatively small group, there is no substitution effect, only an income effect. They will gain NOK 27,500, and the model thus predicts a small reduction in labour supply.

- Medium earners: From 335,000 to 647,000, the allowance is phased out. This is done quite rapidly, such that they will lose NOK 0.4 in allowance per extra 1 NOK in earnings. This 0.4 NOK is taxed at 22%, such that their effective marginal tax will increase by 8.8 percentage points. Hence, for these workers, the theoretical predictions are an unambiguously decreased labour supply, since they have both negative income and substitution effects.

- High earners: Many in this group earn more than NOK 647,000. These workers are unaffected on the intensive margin. In theory, they could, however, be affected on the extensive margin if, without the tax allowance, they are on the margin between full-time earnings, e.g., 800,000 and part-time earnings, e.g., 400,000. In the simulation model, we have ignored this effect, but an evaluation will show whether this margin is relevant or not.

3.1 Choice of experimental design, and how it relates to legal requirements

Randomised allocation of different tax schedules is at odds with general legal principles of equal treatment. Norway does have legislation specifically for pilot schemes and experiments, but it is mainly for situations in which a municipality or other public-sector body wants to try out new ways of organising parts of their services.

From a legal perspective, the starting point is the Constitution, which states that everybody is equal in the eyes of the law. The key questions are whether differential treatment is objectively justified and proportionate. In this case, the reason for it is the “need for knowledge”. A better understanding of behavioural responses to such a tax change is considered important. The latter requirement (proportionality) implied that we needed to investigate whether the same knowledge could be obtained in a less intrusive way, without randomisation or with a lesser degree of unequal treatment.

To address this, two different potential research designs and evaluation strategies were considered that did not involve randomisation:

- Providing the treatment to everyone aged 20–35 in rural municipalities with low employment rates: As the expected effects are relatively small at the individual level, these effects will be dwarfed by the lack of parallel trends and expected fluctuations when comparing these municipalities with other ones.

- Providing the treatment to everyone in a narrow age range, e.g., age 25–30: This avoids randomisation but provides opportunities to use quasi-experimental methods. However, this type of evaluation requires additional assumptions, such as common time- or age-effects across cohorts/years. To assess this approach, the research group constructed a panel dataset with annual earnings for a number of years and birth cohorts (77 combinations). Within this dataset, we estimated a number of potential placebo models, assuming treatment was given at different years and different age thresholds. For each combination, we estimated a simple DiD model and saved the coefficients. The standard deviation of these coefficients informs us about what we have chosen to term “design uncertainty”, which is a form of uncertainty not captured by the standard error (which captures sampling uncertainty). The design uncertainty arises from the fact that any deviation from the additional assumptions in the DiD model will lead directly to bias in the estimated treatment. It turns out that, in this case, the design uncertainty is about the same size as the expected effects, so we concluded that this would not be a satisfying strategy for achieving the desired knowledge. Note that this assessment is not one of principle, but pragmatic, and related to the case in hand.

The general conclusion from this assessment was that we could only fulfil the knowledge needs if the research design was based on some kind of randomisation. This was again crucial for the legal assessment conducted by the Ministry of Finance, which concluded that the requirements for unequal treatment were satisfied.

A randomised experiment can be designed in many ways. In the first assessment, two alternatives were considered: Randomisation of municipalities and randomisation of individuals. The first has some advantages as it also captures equilibrium effects, at least in theory. However, this is only true if the unit of randomisation is aligned with the entities in which the general equilibrium is reached, e.g., independent labour markets. Norway has 358 municipalities, many of which are very small. The number of local labour markets depends on the definition used, but commonly used categorisations vary between 40 and 130 local labour markets.

To compare the two alternatives involving randomisation, we conducted power calculations for stratified randomisation. The strata are based on year of birth, gender and previous earnings, which substantially increases precision. We find that with individual randomisation, the minimum detectable effect for labour market participation is 0.4 percentage points. By contrast, even if the experiment involves 50% of all municipalities (approx. 550,000 treated), the minimum detectable effect in a municipality-based randomisation design is no less than 0.65 percentage points. Hence, in order to obtain the necessary precision using this approach, the study would have to involve a large number of treated subjects and increase the fiscal costs by an order of magnitude. The combination of statistical precision and fiscal cost made the research group recommend the alternative using individual randomisation.

At a later stage, the research group also considered a mix of approaches, with varying treatment intensities between municipalities. This is a design used by, among others, Crépon et al. (2013) and Cheung et al. (2024), and which, in many respects, captures the best of both worlds with individual randomization and an opportunity to learn about spillovers and equilibrium effects. However, the research group decided in the end that the potential for useful insights about such effects within a realistic budget was too limited to recommend such a design.

The research group also had to provide a recommendation about the size of the treatment group, as well as the number of treatment arms. As mentioned above, the minimum detectable effect for the participation rate is actually quite small, even with, e.g., 35,000 in the treatment group. However, to assess responses along the intensive margin and participation effects in various subgroups, the research group recommended a treatment group of 100,000.

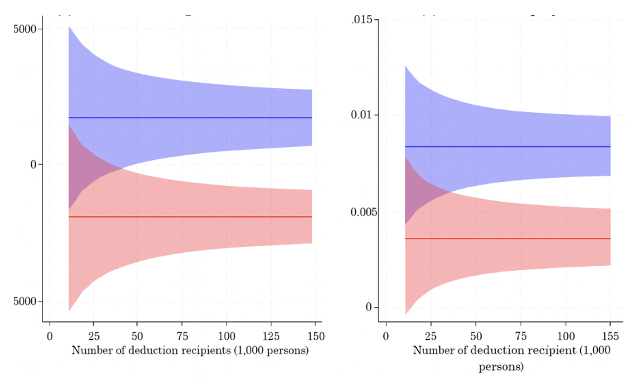

Figure 3 illustrates the expected effects on a) average labour income (left) and b) employment (right) according to various assumptions about the magnitude of the responses, as discussed above. The shaded areas (95% confidence intervals) show how precision increases with the number of recipients. With 100,000 people receiving the deduction, it is expected that the responses can be estimated quite precisely.

Figure 3. Expected effects on average labour income (left) and employment (right) according to different assumptions regarding labour supply responses (cf. Table 1) and 95% confidence intervals

Behind this recommendation also lies a degree of caution. Many things can go wrong, and the researchers wanted to avoid an outcome with a number of underpowered experiments offering limited learning opportunities. On the number of treatment arms, the research group recommended three – one with a different-sized tax credit, and another with a different phase-out.

The final recommendations from the research group can be summarised as follows. The expected effects of introducing an EITC are highly uncertain. Unless the EITC is introduced experimentally, the effects cannot be credibly estimated. In order to gain sufficiently precise estimates, the experiment should be based on individual randomisation and be large, with around 100,000 recipients per treatment arm. The experiment should ideally include several treatment arms, e.g., with and without a phase-out. However, the research group also presented a preferred alternative for one treatment arm.

4 Public hearing and debate

The proposed experiment required specific legislative changes and a public hearing. It was also clear that the experiment would be extraordinary in scale, and that the use of randomisation and experimental research methods deserved to be the subject of public debate.

The experiment was first presented at a press conference on 27 May 2025 by the Minister of Finance, Jens Stoltenberg, the Minister of Labour and Social Inclusion, Tonje Brenna, and the research group. Our impression is that the experiment came as a surprise to the media, and not all news outlets even bothered to turn up. This changed rapidly, and what has been termed “Stoltenberg’s Tax Lottery” became a big news story. It quickly also became controversial and was criticised – and praised - by key media commentators and several political parties. Initially, the discussion went along two lines: First, that the use of randomisation in combination with taxes was unfair and could undermine trust in the tax authorities and system. Second, that it was unnecessary, either because critics expected the EITC not to work or were certain it would.

During the public hearing, which was due on 1 August, the Ministry of Finance received a large number of consultative comments. A summary can be found in the Proposal to the Parliament (in Norwegian) here: Prop. 1 LS (2025–2026) - regjeringen.no.

5 From idea to reality: The practical implementation and the research design used

The budget for 2026 was not passed in the Parliament until December 2025. Hence, in order to start the experiment on 1 January 2026, the practical implementation needed to be undertaken without knowing whether the experiment would be approved. Below, we will present the different elements of the experiment, which is now up and running.

5.1 The tax scheme

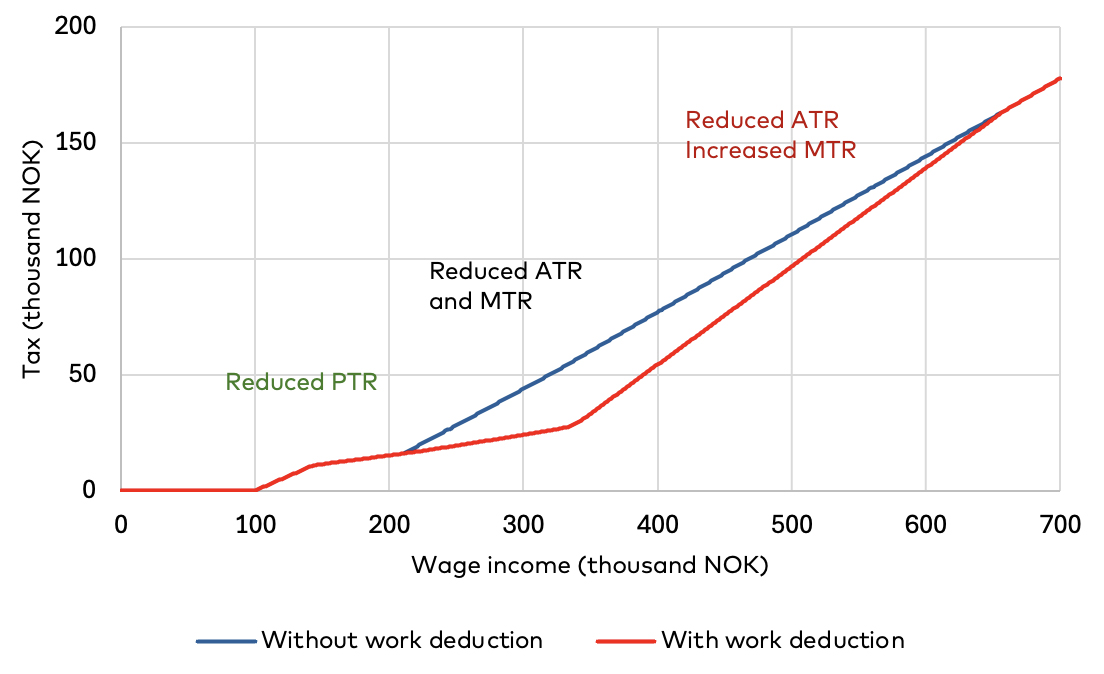

The EITC in the experiment is similar to the research group’s main alternative. Compared to previously proposed tax deductions of this type in Norway, it is relatively sizeable, with a maximum value of NOK 125,000. It raises the threshold for paying the 22% tax on ordinary income from around NOK 210,000 to 335,000.

It also targets low and middle incomes. For every NOK earned exceeding NOK 345,000, the allowance is reduced by NOK 0.40. This increases the effective marginal tax rate (MTR) by 8.8 percentage points in the phase-out region. The ordinary scheme and the test scheme with this deduction are illustrated in Figure 4.

The EITC is fully phased out when labour income exceeds NOK 657,500, which is somewhat below the average income in Norway. Within the target group for the experiment (20–35 years), around 31% of taxpayers are expected to have income above this threshold. For another 28%, earned income is zero or net income is expected to be below the threshold for paying the 22% “tax on ordinary income”. Hence, this group will not benefit from the allowance unless they earn more. However, their participation tax rate (PTR) will be lowered, increasing their incentives to start work or to increase their labour supply.

For the remaining 42% of the target group, the allowance will reduce their average tax rate (ATR). For those with earnings below NOK 335,000, the marginal tax rate will also be reduced, while for those with earnings exceeding NOK 345,000 in the phase-out region, it will increase their marginal tax rate. See Figure 4.

Figure 4. The tax schedule with and without the EITC. Wage earner with standard deductions and only wage income. 2026-rules

5.2 The “lottery” draw

The random distribution of deductions was carried out by computer code. This code was made public along with the budget proposal. For practical reasons, related to the survey (see below) and to the planning of individual tax cards, the random draw into treatment and control groups needed to be carried out before Parliament passed the budget. We ended up with this process:

- The computer code was made public on the Ministry of Finance website (here). The code specified the draw conditional on two “keys”. The first key was a code constructed as a function of the dataset (“hash”), which ensures that the dataset used is unchanged. The second key was the (at the time, not yet realised) opening value of the Oslo Stock Exchange (OSEBX) on 3 November 2025.

- The dataset used for the draw was constructed by the tax administration on 31 October, before the second key was available. This guarantees that those constructing the dataset in the tax administration were unable to manipulate the outcome of the draw by “fiddling” with the data.

- On 3 November, the opening value of OSEBX was added as the second key and the draw was made.

The relevant population contains approximately 1.3 million taxpayers, and 8% were randomised into the treatment group. The randomisation was “stratified,” with the population divided into small and homogeneous groups before the draw. The groups were constructed by first grouping the population based on:

- Year of birth

- Gender

- Whether or not they received social security benefits in 2025 (January to September)

- Whether or not they had labour earnings in 2024

- Whether or not they had self-employment/business income in 2024

- Residency status and tax liability status in Norway.

Within each of these groups, the population was sorted by their labour earnings in 2025 (January to September) and divided into groups of 100. From each stratum, eight individuals were randomly drawn to be in the part of the tax system with the deduction. This group is denoted group A. The remaining 92 individuals were randomly split into two equally sized groups, groups B and C, one that will receive an information treatment (B) and one that will not (C).

5.3 The information given

Everyone involved received information about the experiment at the same time as the annual tax cards were made available. The tax authorities sent text messages or emails saying that “Your tax card for 2026 is ready. This year, the government is starting a trial with work deductions for young people. Log in to our website to see if you are eligible for a work deduction.”

After logging in, a “banner” appears about the experiment. When you click on it, you receive the information treatment described below. The system registers whether or not you visit the information page, and this information is used to separate “compliers” from “non-compliers” in the evaluation.

Behavioural responses to a tax change require that people also change their perception or belief of what their taxes are. Following a regular tax reform, we believe such changes take time. However, the experiment has a limited duration, and we do not have time to let the new tax system influence perceptions in a natural way. Also, since the reformed tax system only applies to a minority of taxpayers, the change in perceptions will be different from changes in a normal situation.

When designing the experiment, we aimed to simulate changes to perceptions in the long term following a reform. However, we need to achieve this almost instantly, or at least within a short time frame.

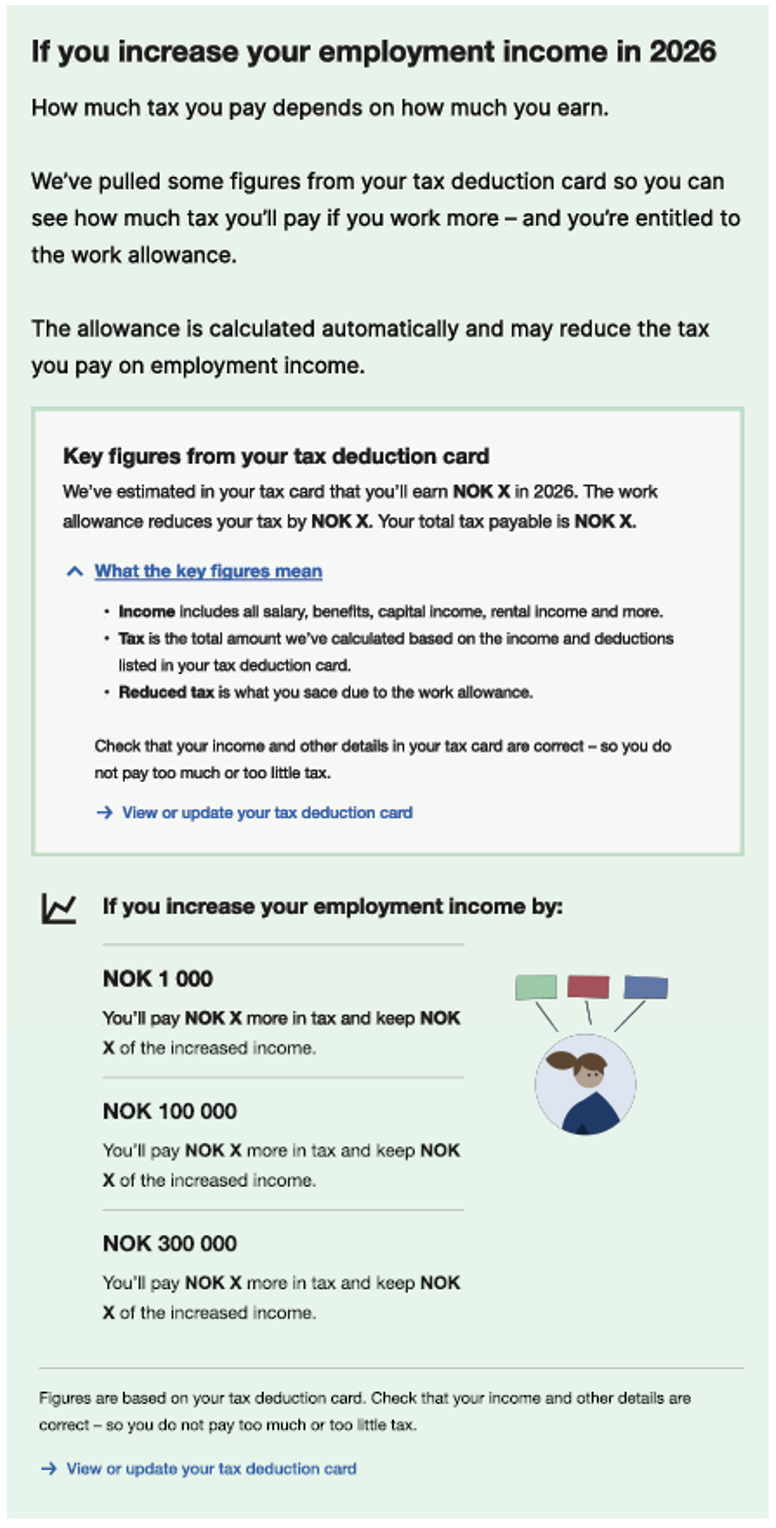

To obtain this, the treatment group is provided with the following five pieces of information (see also Figure 5):

- Predicted income for the next year (used to calculate each person’s tax schedule for advance tax).

- Predicted tax, including the expected tax reduction from the EITC.

- Individual specific examples on the amount of additional tax – and resulting increase in net income – stemming from:

- an increase in labour earnings of NOK 1,000. We think of this as informing recipients of the marginal tax rate without using the term.

- an increase in labour earnings of NOK 100,000. We think of this as the “participation tax rate” for a medium-sized income change.

- an increase in labour earnings of NOK 300,000. We think of this as the “participation tax rate” for individuals outside the labour force.

The extraordinary information given to the treatment group presents us with a second challenge: That the information regarding marginal and participation tax rates could in itself affect labour supply.

To disentangle the effect of information from the effect of the deduction, we split the control group randomly into two parts. Half of them (Group B) receive the same information but with numbers calculated for the ordinary tax scheme, see Figure 6. The others (Group C) received just a minimum of information, see Figure 7.

Figure 5. Information given to group A

Figure 6. Information given to group B

Figure 7. Information given to group C

5.4 The survey

In parallel with the experiment, we are also conducting a large survey in two waves. The first wave was in November 2025, when 30,000 participants were invited to take part. The second wave will be in 2026 and include all respondents from the first wave. In addition, 50,000 new participants will be invited to take part. In the evaluation, the survey data will be linked to administrative data.

Among other things, the survey is designed to inform us about respondents’ perceptions of their tax rate, both before and after the experiment has started. Perhaps most importantly, it will inform us on whether their perceptions of their tax rates differ, after treatment, between groups A, B and C.

The participants are also asked questions about trust in the tax authorities and others, facilitating at least some investigation of some of the critical concerns raised in the public debate and hearing.

5.5 Consent and research ethics

Both the Ministry of Finance and the research group have a responsibility to assess ethical concerns arising from the research and abide by established research ethical norms. Several such concerns have been raised, both by the research group and the public. We will limit the discussion here to the arguably three most important concerns

:

The research groups full ethical assessment is available online: https://frischsenteret.no/publication-details/?skrift_id=1790

- Negative effects on those who gain nothing: Research is not supposed to harm anybody. This experiment will do so indirectly by providing extra resources to some at the expense of others. It is our assessment that this negative effect will be so small as to be negligible. In principle, this is the case for all experiments paid for out of the public purse.

- Harmful disappointment: Will the control group be disappointed, and might this have a negative effect on them? Again, we believe the effect will be negligible. We also believe the disappointment of losing in a lottery with a small probability of winning is much less than in one with a high probability of winning, say 75%.

- Active or passive consent: The main rule in the Norwegian ethical guidelines for social science research is that participants should provide active consent.

Another option is passive consent, where individuals can reserve themselves from taking part in the experiment. This is the approach preferred by the research group. However, the Ministry of Finance concluded that asking the full target group to take part (or not) in a project not yet approved by Parliament would be disrespectful to the legislature. Given this, the research group and the Ministry of Finance agree that the experiment entails no negative risk to anyone (participants can only gain), and that it is acceptable to conduct the experiment without consent.

6 The way forward

The experiment with an earned income tax credit for young adults represents a major investment in evidence-based labour market policy that aims to fill critical knowledge gaps about how tax incentives influence labour supply in a Nordic welfare state. The tax experiment has just started, and no results are available yet, neither to the researchers nor the public. We believe this experiment will provide important insights and hopefully also expand the possibility frontier for future experiments.

References

Bensnes, S., et al. (2025). Utredning om forsøksordning med arbeidsfradrag. Retrieved from: https://…/Utredning-om-forsoksordning-med-arbeidsfradrag.pdf

Cheung, M., Egebark, J., Forslund, A., Laun, L., Rödin, M., & Vikström, J. (2024). Does job search assistance reduce unemployment? Evidence on displacement effects and mechanisms. Journal of Labor Economics, 43(1), 47–81.

Crépon, B., Duflo, E., Gurgand, M., Rathelot, R., & Zamora, P. (2013). Do labor market policies have displacement effects? Evidence from a clustered randomized experiment. The Quarterly Journal of Economics, 128(2), 531–580. Retrieved from: https://doi.org/10.1093/qje/qjt001

Gopinathan, U., Elgersma, J., Dalsbø, T., Bjørbæk, M., & Fretheim, A. (2025). Strengthening research preparedness for crises: Lessons from Norwegian government agencies in using randomized trials and quasi-experimental methods to evaluate public policy interventions. Health Research Policy and Systems, 23(1), 8.

Graber, M., Mogstad, M., Torsvik, G., & Vestad, O. L. (2022). Behavioural responses to income taxation in Norway. Memorandum No. 04/2022.

Kleven, H. (2024). The EITC and the extensive margin: A reappraisal. Journal of Public Economics, 236, 105135.

Kostøl, A. R., & Mogstad, M. (2014). How financial incentives induce disability insurance recipients to return to work. American Economic Review, 104(2), 624–655.

Laun, L. (2019). Ett effektivare jobbskatteavdrag? Rapport till Finanspolitiska rådet 2019/2.

Meyer, B. D., & Rosenbaum, D. T. (2001). Welfare, the earned income tax credit, and the labor supply of single mothers. The Quarterly Journal of Economics, 116(3), 1063–1114.

Michalopoulos, C., Robins, P. K., & Card, D. (2005). When financial work incentives pay for themselves: Evidence from a randomized social experiment for welfare recipients. Journal of Public Economics, 89(1), 5–29.

Verho, J., Hämäläinen, K., & Kanninen, O. (2022). Removing welfare traps: Employment responses in the Finnish basic income experiment. American Economic Journal: Economic Policy, 14(1), 501–522.