- Full page image w/ text

- Table of contents

- The project

- Preface

- Summary

- Sammenfatning

- 1. Introduction

- 2. Background

- 2.1 What is ecosystem accounting

- 2.2 The role of ecosystems and their services

- 2.3 Uses of ecosystem accounts

- 2.4 Aims of report

- 2.5 Methodology

- 3. Ecosystem accounting at the international level

- 3.1 State-of-the art

- 3.2 Ecosystem accounting at the UN level

- 3.3 Ecosystem accounting at the EU level

- 3.4 Monetary valuation of ecosystem services

- 4. Ecosystem accounting in the Nordic countries

- 4.1 State-of-the art

- 4.2 Use and understanding of ecosystem accounting

- 4.3 Current and future use of models for the valuation of ecosystem services

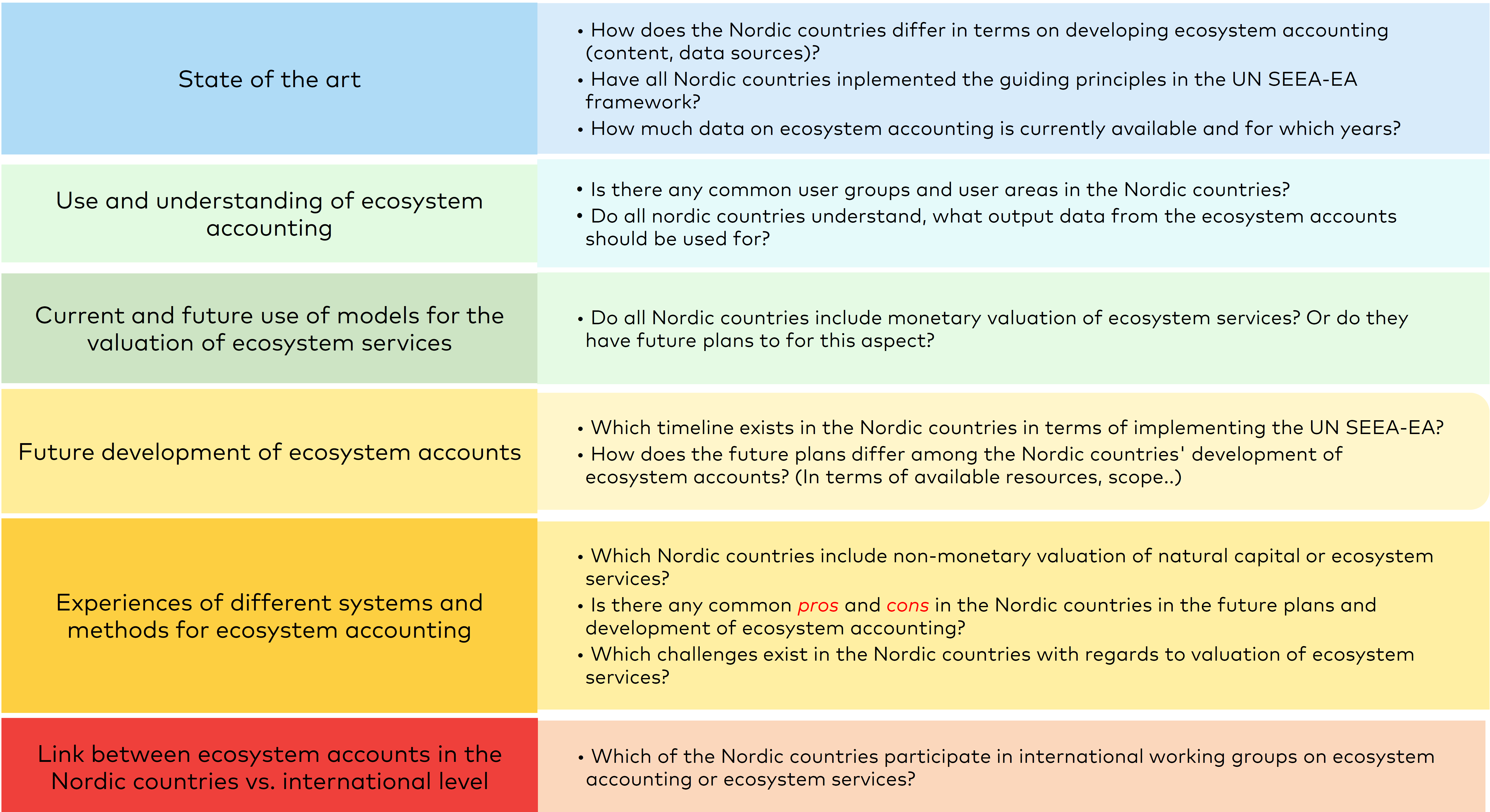

- 4.4 Future development of ecosystem accounts

- 4.5 Experiences of different systems and methods for ecosystem accounting

- 4.6 Link between ecosystem accounts in the Nordic countries vs. international level

- 5. Recommendations

- References

- Appendix 1

- About this publication

MENU

Contents

This publication is also available online in a web-accessible version at https://pub.norden.org/temanord2022-554.

Ecosystem accounting in the Nordic countries

Eskil Mattsson, Flintull Annica Eriksson, Mikael Malmaeus, Mark Sanctuary

IVL Swedish Environmental Research Institute

This project is funded by the Nordic Working Group for Environment and Economy (NME) and the Nordic Working Group on Biodiversity (NBM) under the Nordic Council of Ministers. The project has been carried out by IVL Swedish Environmental Research Institute (Sweden) in the period February 2022 to August 2022.

A reference group with representatives from the Nordics has been established, who provided valuable input to the study.

Preface

The loss of nature - ecosystems and biodiversity - is recognized as a major threat to global welfare and sustainability. Yet policymakers know far from enough about the status of our ecosystems and the development in the extent and the conditions, and how ecosystems and ecosystem services are linked to the economy. In 2021, the UN Statistical Commission adopted the System of Environmental-Economic Accounting Ecosystem Accounting (SEEA EA) which provides detailed guidance for such an accounting system. The EU Commission is currently preparing a legal proposal which includes the ecosystem accounting as a mandatory data collection.

This report gives an overview of the international work in this area, and of the status for ecosystems accounting efforts in our Nordic countries. This status includes former work in the area, as well as how far our countries have come in implementing new international standards. The report shows that Denmark, Finland, Norway, and Sweden to some extent are on the same timeline, due to the new EU legislation requirements. Iceland has not decided to go down this road, because the SEEA EA framework does not fit well with the structure of nature on a volcanic island. Ecosystem accounting is not a priority statistical area for the Faroe Islands

The report has been prepared by IVL Swedish Environmental Research Institute. Members of the Nordic group for Environment and Economy (NME) and the Nordic working group for Biodiversity (NBM) have provided comments on draft versions of the report during the project. The authors of the report are responsible for the content, and any views and recommendations presented in the report do not necessarily reflect the views and positions of the Nordic governments or of NME.

September 2022

Bent Arne Sæther

Chair of the Nordic working group for Environment and Economy

Hákon Ásgeirsson

Chair of the Nordic Working Group on Biodiversity

Summary

In this report, IVL Swedish Environmental Research Institute has mapped the current work on and use of ecosystem accounting in the Nordic countries. Specifically, the report provides an overview of the recent work on ecosystem accounting in each of the five Nordic countries including the Faroe Islands, illustrating advantages and disadvantages within the different countries regarding the use of existing ecosystem accounts, thus to which extent these accounts coincide with new international standards on ecosystem accounting. The report also provides an overview of the ongoing work on ecosystem accounting at an international level, including the development of international standards for ecosystem accounting.

During the last decade major developments have been made in analyzing and evaluating ecosystems in terms of their economic value value for the society and human wellbeing. This development has created a need to quantify and assess systematically the status of current ecosystems, thus their ability to provide ecosystem services. This framework is called ecosystem accounting. More specifically, ecosystem accounting is a statistical framework for organizing data, tracking changes in the extent and the condition of ecosystems, measuring ecosystem services and linking this information to economic and other human activity. Ecosystem accounting provides an internationally agreed guidance to integrate nature into decision-making in consistent and comparable by measuring and recording changes in ecosystems and ecosystem services.

Initially a literature review was conducted focusing on recent and ongoing work on ecosystem accounting at the Nordic and international level. As a second step survey interviews were conducted with experts in ecosystem accounting and related fields in the Nordic countries. The third step entailed analyzing the responses from the survey interviews, thus connecting them to a set of analytical thematic areas.

On an international level, the UN Statistical Commission adopted the System of Environmental-Economic Accounting Ecosystem Accounting in 2021 (SEEA EA) which provides detailed guidance measuring the extent and condition of ecosystems, and how to quantify ecosystem services. The SEEA EA is flexible and can be implemented in parts. For example, a country may choose to implement only a selection of the accounts, considering the specific environmental and economic context. Countries are also encouraged to contribute to the further methodological development of ecosystem accounts for use in policy and decision-making processes in both public and private sector. The SEEA EA consists of five core accounts using spatially explicit data and information about the functions of ecosystem assets and the ecosystem services they produce. At the international working group and task force level there are several ongoing initiatives on ecosystem accounts and ecosystem services. Once a year, the OECD and UNECE jointly organise an annual seminar on implementation of SEEA. All the Nordic countries participate actively in this meeting.

At the European level, The EU Commission is currently preparing a legal proposal which includes the ecosystem accounting as a mandatory data collection across all EU Member States. The proposal needs to pass through the European Parliament, and it can take more than four years before it will come into legal force. Basically, the Nordic countries are following the EU legal typology and modeling which has been developed by the Eurostat task force which are aligned with the UN SEEA EA. All the Nordic countries are to some extent on the same timeline, due to the new EU legislation requirements. The first reporting year for all Member States in the EU is proposed to be year 2026. This new legal act is the main legal document which guides the Nordic countries timelines in terms of implementing the SEEA-EA framework. At the Eurostat director’s level, there are regular meetings which relates to the development of environmental accounts in general, including ecosystem accounts. Denmark, Norway, Finland, Iceland and Sweden are participating in these meetings. Concurrent to the Eurostat directors’ levels group meeting there is a working group on environmental accounts in general, including ecosystem accounts. Here the same Nordic countries are represented. Below these groups there is a specific Eurostat task force group on ecosystem accounting. Only Norway and Finland are active in this task force.

The interviews with experts in ecosystem accounting and related fields in six Nordic countries show that there are some differences between the countries in terms of developing ecosystem accounting frameworks.

In Norway there is a longstanding established cooperation between the Statistics Norway and several research institutes in terms of data exchange and developing methods and ideas for the development of ecosystem accounting. Statistics Norway has started the plans of how to integrate the UN SEEA EA framework into its regular statistical production from year 2024. Norway has established a good foundation for implementing the SEEA EA framework as a large amount of research, methodology development and pilot testing has taken place between different organisations in Norway over the last couple of years.

In Finland, there is a growing interest for ecosystem accounting and environmental economic accounting and Statistics Finland and the Finnish Environmental Institute (SYKE) have been working jointly for many years on developing ecosystem accounts. In Finland, it has not yet been decided who will be the responsible organisation for developing ecosystem accounting. Statistics Finland and SYKE both have experts and data who cover statistics, national accounts, ecosystem and biodiversity topics. Finland has mapped different alternatives for ecosystem extent accounts and has long time series data on land cover data and forestry. Some pilot studies on mapping ecosystem services have also been made.

In Denmark, ongoing cooperation between Statistics Denmark, University of Copenhagen and Aarhus University is taking place in terms of data production and data exchange for ecosystem accounting. First steps have been processed via the national development of a Danish land use database. Denmark is following the legal process at the EU level, in terms of requirements and how it will affect the country’s reporting demands. Statistics Denmark has defined a schedule for drafting an internal roadmap within the organization. Denmark has consistent data on land use and forestry data and has in several studies mapped, quantified and valued ecosystem services.

In Sweden, limited cooperation has taken place in terms of developing ecosystem accounts. Independently, some pilot studies have been made in the area, but extended cooperation needs to be setup. Statistics Sweden will establish a road map for how Sweden will manage and implement the ecosystem accounting framework. Statistics Sweden is closely following the ongoing legal discussion at the EU level, in terms of how the requirements will affect the country’s reporting demands. In Sweden, high quality data on ecosystem extent accounts is available where the data is connected to private and public ownership.

Iceland is currently at an early stage and the country still needs to understand the whole concept of the ecosystem accounting, in terms of setting-up the framework, to understand and map which data sources to make use of. The current design of the SEEA EA framework does not fit well with Iceland’s conditions as the country is a volcanic island, with low forest cover and low amount of land area under arable cultivation.

Ecosystem accounting is not a priority statistical area for the Faroe Islands. The fact that the Faroe Islands is not part of the European Union implies the country is not part of the European statistical cooperation, thus it does not have any legal reporting requirements in this regard.

The interviews further revealed that there were several common user areas for the ecosystem accounts across Finland, Sweden, Denmark and Norway. It was highlighted that user areas such policies for land use and water resource planning, infrastructure development is of great importance when these countries will commence developing ecosystem accounts in a national level. These four countries have a common understanding of the need for creating a harmonised statistical framework for its national ecosystem service data. Most Nordic countries consider output data to be a very useful tool in terms of policy planning at a national and regional level and for different policy purposes in a harmonized statistical framework.

Many of the Nordic countries mentioned that they see it as useful to develop a common statistical framework for national ecosystem data, which is harmonized across countries. Also, many of the Nordic countries see the possibility of developing longer time-series with ecosystem accounting data as beneficial, with the aim to investigate and follow the development of the country's different ecosystems and make targeted policy decisions. Another common benefit is that all the Nordic countries see the opportunity of establishing new partnerships and networks as a great benefit when developing ecosystem accounts, as input data come from various institutes and agencies.

Moreover, four Nordic countries (Norway, Denmark, Sweden and Finland) mentioned that they view trade-offs between ecosystem services aspects of great importance, but they have not yet considered trade-offs from an accounting perspective. Monetary valuation is currently part of the development process of ecosystem accounts and was mentioned as highly important work in Finland and Norway. The other Nordic countries have no current plans to include monetary valuation into their ecosystem accounting framework at this stage.

All the Nordic countries lack additional resources for implementing the new ecosystem accounting framework and all the Nordic countries find it resource intensive and comprehensive to compile. Several Nordic countries see the development of ecosystem accounting as a major national coordination task, as input data in different formats and units comes from a wide range of data sources, from different national organisations. All countries need additional funding to be able to cope with the new EU legislation requirements, in terms of reporting mandatory data to Eurostat.

Moreover, several countries mentioned that a big challenge relates to finding appropriate data which fits the purposes of ecosystem accounts. Nationally there exists much spatial data, but this data it is not set up for accounting use as required for ecosystem accounts.

Based on the outcome of our analysis on the current work and use of ecosystem accounting in the Nordic countries, we provide the following six recommendations:

- Allocate additional resources for the development of ecosystem accounts in all five Nordic countries and the Faroe Islands

- Appoint national coordinators for ecosystem accounting

- Establish a base for knowledge sharing in terms of skills development of utilizing existing and potentially new data sources

- Launch information campaigns to increase public and private sector awareness relating to the importance of ecosystems and ecosystem accounting

- Development of ecosystem accounts is a technical challenge – more country case studies are needed

- Use monetary valuation methods with care

Sammanfattning

IVL Svenska Miljöinstitutet har på uppdrag av Nordiska Ministerrådet kartlagt arbetet med ekosystemräkenskaper i Norden. I denna rapport redovisas översiktligt status för arbetet med ekosystemräkenskaper i de fem nordiska länderna både vad gäller planer och konkret användning i de olika länderna. För- och nackdelar som har upplevts i de olika länderna vad gäller tillämpningen av deras existerande räkenskapssystem redovisas också, och till vilken grad existerande system sammanfaller med nya internationella standarder. Rapporten beskriver även nuvarande status i det internationella arbetet med utveckling av standarder för ekosystemräkenskaper.

Under det decenniet har betydelsen av att kunna utvärdera och analysera effekten av olika åtgärder på ekosystemens status och därmed deras ekonomiska värde för både samhället i stort och för den enskilda människan diskuterats. Detta har skapat ett behov för en systematisk översikt över ekosystem, deras status och förmåga att leverera ekosystemtjänster. Sådana system går ofta under benämningen ekosystemräkenskap. Ekosystemräkenskaper är ett statistiskt ramverk för att organisera data och att mäta förändringar i ekosystemens utbredning och tillstånd samt flödet av tjänster som ekosystemen tillhandahåller samhället och ekonomin. Ekosystemräkenskaper tillhandahåller en internationellt överenskommen vägledning som integrerar värdet av naturens tjänster i beslutsfattande på ett sätt som är konsistent och jämförbart genom att mäta förändringar i ekosystemens funktion och de tjänster som ekosystemen tillhandahåller.

Inledningsvis så genomfördes en litteraturstudie baserat på en genomgång av publicerade rapporter och vetenskapliga artiklar för att beskriva arbetet med ekosystemräkenskaper i Norden och i en internationell kontext. I ett andra steg genomfördes intervjuer med experter inom området ekosystemräkenskaper och angränsade ämnesområden i de fem nordiska länderna och Färöarna. I ett tredje steg analyserades svaren från intervjuerna och kopplades till ett analytiskt ramverk.

Under 2021 antog FN:s statistikkommission en ny statistisk standard för ekosystemräkenskaper (SEEA EA). Denna standard ger detaljerade riktlinjer hur ekosystemens utbredning och tillstånd kan mätas liksom hur ekosystemtjänster kan mätas och värderas. FN:s nya standard för ekosystemräkenskaper är flexibelt utformad och kan implementeras stegvis. Ett land kan till exempel välja att implementera en del av räkenskaperna utifrån miljömässiga och ekonomiska förutsättningar och omständigheter. Inom standarden uppmuntras länder att bidra till den metodologiska utvecklingen av ekosystemräkenskapena för ökad användning och tillämpning inom beslutsfattande både vad gäller offentlig och privat sektor. Den nya FN standarden för ekosystemräkenskaper består av fem delar innehållande rumsligt explicita data och information om funktion och betydelsen av ekosystemens tillgångar och ekosystemtjänster. På internationell nivå finns det flera pågående initiativ som bidrar till den metodologiska utvecklingen av ekosystemräkenskaper. Till exempel, anordnar Organisationen för ekonomiskt samarbete och utveckling (OECD) och FN:s ekonomiska kommission för Europa (UNECE) tillsammans ett årligt seminarium om utvecklingen av ekosystemräkenskaper där samtliga nordiska länder aktivt deltar.

På europeisk nivå arbetar EU kommissionen med att utveckla ett lagförslag som inkluderar ekosystemräkenskaper som ett obligatoriskt ramverk för datainsamling av utbredning och status av ekosystem i alla Europeiska unionens medlemsstater. Lagförslaget behöver godkännas av Europaparlamentet och det bedöms i nuläget ta mer än fyra år innan lagförslaget godkänns. De nordiska länderna följer ramverket för ekosystemräkenskaper som arbetats fram av EU:s statistikkontor, Eurostat som är anpassat enligt FN:s nya standard för ekosystemräkenskaper. Alla nordiska länder är därför på samma tidsnivå vad gäller implementeringen av ekosystemräkenskaper där det första rapporteringsåret enligt lagförslaget har föreslagits till 2026. Inom ramen för Eurostat-arbetet genomförs det regelbundna möten kring utvecklingen av ekosystemräkenskaper på europeisk nivå. Danmark, Norge, Finland, Island och Sverige deltar aktivt på dessa möten. Det finns även en samverkande arbetsgrupp om miljöräkenskaper där ekosystemräkenskaper ingår och där ovanstående länder deltar. Dessutom finns det en specifik arbetsgrupp om ekosystemräkenskaper som är underordnad arbetsgruppen om miljöräkenskaper där endast Norge och Finland deltar.

Intervjuer med experter inom området ekosystemräkenskaper i de fem nordiska länderna och Färöarna visar att det finns vissa skillnader mellan länderna i utvecklingen av ramverk för ekosystemräkenskaper.

I Norge finns det ett etablerat samarbete mellan den statistiska centralbyrån i Norge och flera forskningsinstitut och universitet i landet med avseende på utbyte av data och metodutveckling av ekosystemräkenskaper. Den statistiska centralbyrån i Norge har påbörjat arbetet med att integrera FN:s nya standard för ekosystemräkenskaper i befintlig statistikutveckling från 2024 och framåt. Norge har också goda förutsättningar att implementera FN:s nya standard för ekosystemräkenskaper eftersom det finns mycket forskning, metodutveckling och pilotstudier att tillgå inom området de senaste åren.

I Finland finns det ett ökande intresse för ekosystem- och miljöräkenskaper och dess användning. Statistikcentralen och Finlands miljöcentral (SYKE) har under flera år arbetat tillsammans med att utveckla system för ekosystemräkenskaper även om det ännu inte är bestämt vilken aktör som ska vara ansvarig för att utveckla arbetet med ekosystemräkenskaper. Både Statistikcentralen och SYKE har expertis och dataunderlag såsom inkluderar till exempel utbredning och tillstånd av ekosystem och biologisk mångfald. Finland har också kartlagt olika alternativ och datakällor för olika ekosystems utbredning och har långa tidsserier av data för marktäckning och skog. Det finns även pilotstudier som har kartlagt ekosystemtjänster från olika ekosystem.

I Danmark pågår samarbete mellan Danmarks statistik, Köpenhamns universitet och Århus universitet kring datautveckling och utbyte av data för ekosystemräkenskaper. Till exempel har en nationell databas för markanvändning utvecklats. Det finns även långa tidsserier av skogliga data liksom flera studier som har kartlagt och värderat ekosystemtjänster. Danmark följer även utvecklingen av de krav som utvecklas på europeisk nivå kring rapportering av ekosystemräkenskaper. Danmarks statistik har också tagit fram en intern färdplan för utvecklingen inom området.

I Sverige är samverkan mellan statistiska centralbyrån, SCB och andra myndigheter, universitet och forskningsinstitut än så länge begränsad vad gäller utvecklingen av dataunderlag för ekosystemräkenskaper, även om vissa pilotstudier har genomförts. Statistiska centralbyrån kommer att utveckla en färdplan inom området och SCB följer noga utvecklingen kring de lagförslag som diskuteras och är under utveckling på europeisk nivå och hur dessa krav påverkar nuvarande rapporteringskrav. I Sverige finns till exempel utvecklade dataunderlag kring arealer och utbredning av olika ekosystem kopplat till markräkenskaper för ekosystemtjänster.

Island befinner sig i ett tidigt skede i utvecklingen av ekosystemsystemräkenskaper och behöver mer förståelse kring uppbygganden av dess ramverk och vilka datakällor som krävs för dess användning och rapportering. Designen av ramverket på internationell nivå överensstämmer inte med de naturliga förutsättningarna på Island eftersom Island är en vulkanisk ö och ekosystemen på Island har delvis en annan karaktär än övriga nordiska länder med liten areal av till exempel skog och jordbruksmark.

Ekossystemräkenskaper är statistiskt sätt inte en prioriterad fråga i Färöarna. Eftersom Färöarna inte är medlemsland i Europeiska unionen ställs det inga krav att Färöarna behöver rapportera ekosystems utbredning och status.

Intervjuerna visade också att finns flera gemensamma användningsområden för ekosystemräkenskaper i Finland, Sverige, Danmark and Norge. Det betonandes att användningsområden för policyer kopplade till markanvändning, vattenresurshantering och infrastrukturutveckling är av stor betydelse i utvecklingen av ekosystemräkenskaper på nationell nivå. Dessa fyra länder har också en gemensam förståelse av behovet att utveckla ett enhetligt statistiskt ramverk för hanteringen av data kopplade till ekosystemen. De flesta nordiska länder anser även att utgående data och statistik är mycket användbar i politik och planering på både nationell och regional nivå.

Flera av de nordiska länderna nämnde nyttan av utvecklingen av ett nationellt statistiskt ramverk för mätning och uppföljning ekosystemens status som är jämförbar mellan länder. Flera länder ser också möjligheten att utveckla längre tidsserier med data för ekosystemräkenskaper som positivt och möjliggör att mäta och följa upp utvecklingen av länders olika ekosystemen som underlag till beslutsfattande. Alla nordiska länder ser också arbetet med att utveckla en statistisk standard för ekosystemräkenskaper som en möjlighet att utveckla nya nätverk och partnerskap eftersom indata kommer från olika institut och organisationer.

Fyra länder (Norge, Danmark, Sverige och Finland) nämnde också att de ser möjliga målkonflikter som kan uppstå mellan ekosystemtjänster som viktiga även om dessa fyra länder ännu inte tagit hänsyn till detta med i sitt arbete med utveckling av standard för ekosystemräkenskaper. Monetär värdering av ekosystemtjänster är en del av utvecklingen av standarden för ekosystemräkenskaper och Finland och Norge betonande betydelsen av detta som viktigt. De andra nordiska länderna har inga nuvarande planer att inkludera monetär värdering som en del av utvecklingen av sina ramverk för ekosystemräkenskaper.

Samtliga nordiska länder saknar resurser för att implementera nationella ramverk för ekosystemräkenskaper och alla länder anser att arbetet är resursintensivt och omfattande att sammanställa. Flera nordiska länder anser också att detta arbete kräver stor nationell samordning eftersom ingående data är sammanställt i olika format och enheter och kommer ifrån olika datakällor fördelat över flera olika organisationer. Alla länder behöver ytterligare finansiering för att kunna hantera kraven som ställs på EU-nivå att rapportera in obligatoriska data för ekosystemräkenskaper. Dessutom lyfte flera länder fram att det är en stor utmaning att hitta lämpliga data som passar de rapporteringskrav som ställs inom ramen för ekosystemräkenskaper. Ofta finns det mycket rumslig data tillgänglig i länderna men befintliga data är ofta inte utformad på det sätt som krävs för redovisning av ländernas status och utbredning av ekosystem och ekosystemtjänster.

Baserat på vår analys av översiktlig status för arbetet med ekosystemräkenskaper i de fem nordiska länderna rekommenderar vi följande sex åtgärder:

- Tilldela ytterligare resurser för utvecklingen av arbetet av ekosystemräkenskaper i samtliga nordiska länder och Färöarna

- Utse nationella samordnare för utveckling av ekosystemräkenskaper

- Utveckla former för kunskapsspridning till stöd för utveckling av ekosystemräkenskaper och användning av befintliga och nya datakällor

- Öka medvetenheten om behovet av ekosystemens och ekosystemräkenskapernas betydelse genom informationskampanjer

- Utveckling av ekosystemräkenskaper är tekniskt utmanande – nya pilotstudier behövs som underlag

- Monetära metoder för värdering av ekosystemtjänster behöver användas med försiktighet.

1. Introduction

Over the past 20 years, there has been a growing public interest in the role and value of natural ecosystems and how they contribute to our quality of life and to human wellbeing. Ecosystems provide a range of ecosystem goods and services (provisioning, regulating, supporting and cultural) that are that are central to human well-being, health and livelihoods (e.g., Costanza et al., 1997; MA, 2005; Fisher et al. 2009). These services include for example the provision of food, fibre, filtration of air and water, protection against extreme weather events such as flooding and heat waves and climate regulation. The degradation and loss of ecosystem assets (such as forests, grasslands, wetlands, biodiversity) has raised widespread concern about the sustainability and resilience of ecosystem services (Rockström, 2009; Diaz et al. 2028; IPBES, 2019). The ability of ecosystems to supply these ecosystem services depends on their extent and condition (INCA, 2021). Despite the critical role of ecosystems and their benefits for society, there is still no established way of measuring the extent and condition of ecosystem, and their change over time, as well as the quantity of services these ecosystems supply (Vysna et al. 2021).

In recent years, the United Nations (UN) has developed international standards for environmental accounting. In March 2021, the UN Statistical Commission adopted the System of Environmental-Economic Accounting Ecosystem Accounting which provides detailed guidance measuring the extent and condition of ecosystems, and how to quantify ecosystem services. International economic monitoring systems that collect policy relevant economic information such as the System of National Accounts (SNA) do not include adequate environmental information required to monitor changes in ecosystems (Vargas et al. 2019) Therefore, indicators such as gross domestic product (GDP) could be supplemented with complementary accounts for the extent and development of ecosystems, and indicators for possible overuse and negative environmental impacts (Obst et al., 2016; Lai et al. 2018). To achieve the goal to develop a monitoring system that integrates economic and environmental information two statistical frameworks have been developed to supplement the SNA: 1) the System of Environmental-Economic Accounting – Central Framework (SEEA CF) and 2) the System of Environmental-Economic Accounting –Ecosystem Accounting (SEEA EA) (UN et al., 2014ab).

The System of Environmental-Economic Accounting—Ecosystem Accounting (SEEA EA) is an integrated statistical framework to address stocks and flows that support or depend on ecosystems. It organizes biophysical information about ecosystems, measuring ecosystem services, tracking changes in ecosystem extent and condition, valuing ecosystem services and assets, and linking this information to measures of economic and human activity (United Nations et al. 2021). The SEEA EA has a spatial approach to accounting, since the benefits a society receives from ecosystems depend on where those assets are located in the landscape in relation to the beneficiaries. The SEEA EA complements the measurement of the relationship between the environment and the economy described in the SEEA Central Framework. On the other hand, the SEEA Central Framework focuses on individual environmental assets, i.e., resources, such as timber, water and energy (United Nations, 2022, 2014b).

2. Background

In this chapter some background knowledge is presented on what ecosystem accounting is, its role and what benefits society receives from ecosystems and their services. Later on, the uses of ecosystem accounts are elaborated and finally the methodology used throughout the report is described.

2.1 What is ecosystem accounting

Ecosystem accounts measure how nature, and its various ecosystems contribute to human well-being and the society economy and how this evolves over time (Maes et al. 2020). Ecosystem accounting (SEEA EA) is a rapidly developing field, which is seen as an extension of the environmental economic accounts (SEEA CF) that provides a structured approach to assessing the dependence and impacts of economic and human activity on the environment. According to UN (2021), the System of Environmental-Economic Accounting—Ecosystem Accounting (SEEA EA) is a spatially-based, integrated statistical framework for organizing biophysical information about ecosystems, measuring ecosystem services, tracking changes in ecosystem extent and condition, valuing ecosystem services and assets and linking this information to measures of economic and human activity. Furthermore, ecosystem accounting includes a broader range of benefits to people than captured in standard economic accounts. It offers a structured approach to assessing the dependence and impacts of economic and human activity on the environment (ibid.)

2.2 The role of ecosystems and their services

The concept of Ecosystem Services was created to address the interactions between nature and society. During the 1990s much of the current understanding of ecosystem services was developed and mainly after the Millennium Assessment report in 2005, research into ecosystem services has exploded with many attempts to identify, quantify, evaluate, and economically price ecosystem services.

The British Ministry of Finance, Dasgupta (2021) explains the importance biodiversity has on ecosystem functioning and its productivity. The report shed light to the fact that the global demand for different ecosystem services has increased immensely over several decades. The large demand of provisioning services in combination with the loss of the biosphere productivity in terms of lack of regulating, maintenance and cultural services have had a large negative impact on the global ecosystems over time. The report further illustrates the important relationships which exists between different ecosystems and communities of plants and animals, thus the importance of making use of the existing CICES classification for ecosystem services (see e.g., Haines-Young and Potschin, 2012). Dasgupta further argues throughout the report that decision-making at a national level can greatly improve through natural capital accounting and ecosystem accounting, as it illustrates the development on a national level. Henceforth, it could improve efficiency of extraction from nature, thus produce less waste and stop biodiversity losses. It could further enable changes into the supply chains, towards more fair and sustainable consumption.

2.3 Uses of ecosystem accounts

Ecosystem accounts can provide information that supports economic and environmental policy and decision-making, for example by highlighting the importance of ecosystems and ecosystem services to policymakers, or by impacting the design of policy responses, instruments and management of ecosystems. This can also entail monitoring the effectiveness of various policies through various indicators and supporting biodiversity assessments. It can also support mainstreaming environmental data in economic and financial decision-making (United Nations et al. 2021).

The SEEA EA can support national level policy decision making by connecting information about multiple ecosystem types and multiple ecosystem services to macro-level economic information. Nevertheless, ecosystem accounting is also applicable at subnational scales. For example, ecosystem accounts can be used to support decision making for individual administrative areas such as provinces and urban areas, and for environmentally defined areas such as water catchments, protected areas, biodiversity priority areas and coastal zones.

More specifically, fully developed ecosystem accounts can (in principle) answer questions such as:

- What is the extent of agricultural land at country or at EU-level? How has the extent and condition changed over time?

- How is the the extent and condition of forest soil changing? How much carbon does it retain?

- What is the value of marine ecosystems in the EU? How has it changed over time?

The information provided from the questions above is useful information to show ecosystems contributions to the economy, informing natural resource management decisions and for crafting policies that have an impact on natural capital, such as forestry, agriculture and transport (Hein et al 2020). Ecosystem accounts also allow for monitoring the status of ecosystem assets over time and thus give an indication of the change of their status (Eurostat, 2022).

2.4 Aims of report

This project maps the Nordic countries work on ecosystem accounts, as well as create an understanding of the interest in, and usage of ecosystem accounting.

This report is intended to serve as support in the development of ecosystem accounting in the Nordic countries, for decision and policy makers, and anyone else who might have use of the results and the need to evaluate and tracking changes in ecosystem extent, condition and ecosystem services.

Specifically, the report aims to provide an overview of the recent and ongoing work on ecosystem accounting in each of the five Nordic countries including the Faroe Islands, by illustrating advantages and disadvantages within the different countries regarding the use of existing ecosystem accounts. This study also analyses to which extent these accounts coincide with new international standards on ecosystem accounting. In addition, the report provides an overview of the ongoing work on ecosystem accounting at an international level, including the development of international standards for ecosystem accounting.

2.5 Methodology

The work of the report was conducted in several steps. Initially a literature review was conducted focusing on recent and ongoing work on ecosystem accounting at the Nordic and international level. As a second step survey interviews were conducted with experts in ecosystem accounting and related fields in six Nordic countries. The third step entailed analyzing the responses from the survey interviews, thus connecting them to the analytical thematic areas presented in chapter four of the report. Finally, this report concludes with a discussion and suggestions for further work.

The main results with recommended policy options are also presented in a separate policy brief.

2.5.1 Literature review

Existing research through reports, journal articles and statistics were acquired, screened and reviewed to understand the recent and ongoing work on ecosystem accounting in the Nordic countries as well as at the UN and EU-level. The literature review was meant to be an informative, rather than all encompassing, review of the literature on the topic of ecosystem accounting.

2.5.2 Interviews

Concurrent with the literature review, survey interviews were conducted with experts in ecosystem accounting and related fields in six Nordic countries; Finland, Norway, Sweden, Denmark, Iceland and the Faeroe Islands. The interviews were conducted in a semi-structured approach. The survey interviews are the foundation of the analysis in chapter 4. The interviews were conducted by utilizing Microsoft Teams. An interview guide (see Appendix 1) was drafted jointly with the Ministry of Nordic Council of Ministries.

The following eight interviews were conducted:

- One interview with Norway, with two experts from Statistics Norway

- One interview with Finland, with one expert from SYKE and one expert from Statistics Finland

- Two interviews with Sweden, with two experts, one from Statistics Sweden and one from the Swedish Environmental Protection Agency

- One interview with Iceland, with one expert from Statistics Iceland

- Two interviews with Denmark, with one expert from the IFRO Department at the University of Copenhagen, and one expert from Statistics Denmark.

- One interview with the Faeroe Islands, with one expert from Statistics Faroe Islands

An interview technique was built upon the following steps:

- Explain your background, relation to the ecosystem accounts in your country.

- Explain the use and understanding of ecosystem accounts in your country.

- Explain your country’s current use and future use of valuation models for ecosystem services

- Explain about your country’s development plans for the ecosystem accounts

- Discuss about the challenges your country is facing in measuring ecosystem accounts.

- Explain your country’s involvement at the international level in regard to ecosystem accounting.

3. Ecosystem accounting at the international level

In this chapter, the recent and ongoing work on ecosystem accounting at the UN- and EU-level is presented. Additionally, the structure of the ecosystem accounting framework is presented. Also, the new mandatory EU requirements is also highlighted in this section. Later on, key initiatives from the European Union are presented. Finally, the chapter contains a section which covers monetary valuation of ecosystem services.

3.1 State-of-the art

Currently, there is much ongoing work on developing and defining ecosystem accounts and their use at the international level (SCB, 2021). In 2021, a new UN ecosystem manual was published and there are ongoing discussions on extending the legal basis of the European environmental accounts to include ecosystem accounts (UN, 2021; EU Commission, 2022a). Currently, several documents of technical guidance are available to support implementation, application and interpretation of the ecosystem accounts which will be expanded as knowledge and experience on the use of ecosystem accounts advances.

3.2 Ecosystem accounting at the UN level

United Nations System of Environmental-Economic Accounting Central Framework (SEEA CF) is a framework to compile statistics linking environmental statistics to economic statistics. SEEA CF is described as a satellite system to the System of National Accounts (SNA). This means that the definitions, guidelines, and practical approaches of the SNA are applied to the SEEA CF.

In 2012, the UN published a manual on Experimental Ecosystem Accounting (UN, 2012) which formed the basis for continued work and development on ecosystem accounting (Statistics Sweden, 2021). This manual covers several areas, such as biodiversity, carbon sequestration and the extent and quality of land, which have been used by different statistical agencies, researchers, and international organizations. In 2015 a subsequent technical guide on experimental ecosystem accounts was published including more developed methods (UN, 2015).

In March 2021 the UN Statistical Commission adopted a new statistical standard - the ‘System of Environmental-Economic Accounting– Ecosystem Accounting’ (SEEA EA). The adoption of the adjacent handbook is a result of more than three years of work and discussions of more than 100 experts from a broad range of disciplines directly involved in writing the handbook, and many more who reviewed its drafts (Eurostat, 2021).

Prior to the adoption of the SEEA EA, several issues were discussed in the global consultation such as if the title of the handbook still should include the word “experimental”. Furthermore, there were disagreements regarding if the manual should contain monetary values on ecosystem services flows and ecosystem assets, or if this should be included as an appendix. These disagreements show that due to the complexity of ecosystem accounting, there might still be some time until a fully developed, internationally harmonized statistical system on ecosystem accounting is in place.

During the beginning of 2021, the United Nations Statistical Division (UNSD) made a global assessment of the SEEA EA implementation. On a global scale 34 countries indicated that they compile SEEA EA. Most countries (54%) who mentioned they compile SEEA EA are developed countries, while 47% are developing countries. The trend is the same for both types of countries, most countries have until now focused on developing extent accounts, followed by ecosystem services with supply and use tables. Condition, land and species accounts are currently being developed by a small number of countries. However, the results show that 82% of the currently implementing countries, have plans of expanding environmental-economic accounting in general (United Nations, Statistical Commission, 2021).

Following the adoption of the SEEA EA, the Artificial Intelligence for Environment & Sustainability (ARIES) for SEEA Explorer was released in 2021. ARIES is an integrated, open-source modelling platform for environmental sustainability, where researchers from across the globe can add their own data and models on ecosystem accounts to web-based repositories (UN, 2022). Tests are also being done to explore how ecosystem extent, condition, and regulating services can be modeled using high resolution data from remote sensing and global datasets (Hein et al. 2020).

The SEEA EA is flexible and can be implemented in parts. For example, a country may choose to implement only a selection of the accounts or to compile accounts for selected regions within their country, considering the specific environmental and economic context. Also, a country may decide to only produce accounts in physical terms and not in monetary terms (United Nations et al. 2021). There are opportunities for countries to compile ecosystem accounts using collaborative approaches by combining information from National Statistical Offices in combination with the expertise of other agencies and research organizations. Countries are encouraged to contribute to the further methodological development of ecosystem accounts for use in policy and decision-making processes in both public and private sector (Edens et al. 2022).

3.2.1 Structure of the SEEA EA framework

SEEA EA includes a wide variety of ecological and biophysical data, including data on their extent and condition and flows of ecosystem services. This requires data from biophysical models such as hydrological models. The SEEA EA consists of five core accounts using spatially explicit data and information about the functions of ecosystem assets and the ecosystem services they produce (UN, 2022). The SEEA EA is a geospatial approach where existing data on ecosystem stocks and flows, at different scales are collected, as the benefits a society receives from ecosystems depend on where those assets are in the landscape in relation to the beneficiaries (Farrell, 2021; UN, 2021).

The following ecosystem accounts are part of the SEEA EA framework:

ECOSYSTEM EXTENT accounts record the total area of each ecosystem (e.g., forests, wetlands, agricultural areas, marine areas), classified by type within a specified area (ecosystem accounting area). This account is a common starting point for ecosystem accounting, and they are the basis for condition and ecosystem services accounting. Ecosystem extent accounts are measured over time in ecosystem accounting areas (e.g., nation, province, river basin, protected area, etc.) by ecosystem type, thus illustrating the changes in extent from one ecosystem type to another over the accounting period.

ECOSYSTEM CONDITION accounts record the condition of ecosystem assets in terms of selected characteristics at specific points in time and the distance from a reference condition. Over time, they record the changes to their condition and provide valuable information on the health of ecosystems.

ECOSYSTEM SERVICES FLOW accounts (physical and monetary) record the supply of ecosystem services by ecosystem assets and the use of those services by economic units, including households. Ecosystem extent and condition typically influence the physical supply of ecosystem services.

MONETARY ECOSYSTEM ASSET accounts record information on stocks and changes in stocks (additions and reductions) of ecosystem assets. This includes accounting for ecosystem degradation and enhancement. Monetary valuation can be performed as a final part of a compilation process, but it is not a mandatory component.

Figure 1. Connections between the ecosystem accounts. Reference: Adapted from United Nations et al. (2021).

In addition, there are several related accounts that may be appropriate for monitoring and analysis in different circumstances, including “thematic accounts”. Thematic accounts organize data on themes of specific policy relevance. Examples of relevant themes include climate change, biodiversity, oceans and urban areas.

Figure 2. Water purification ecosystem services provided by forests to beneficiaries downstream. Reference: Adapted from United Nations et al. (2021).

Figure 1 shows the connection between the ecosystem accounts. The SEEA EA is a complement to the SEEA-CF as it includes the spatial approach to ecosystems, thus the services provided by forests, marine, recreation and water, the ecosystem services provided, and the location of beneficiaries. Figure 2 is showing an example of how ecosystem assets provide water filtration ecosystem services downstream, to beneficiaries. Furthermore, the SEEA EA can be compiled at different spatial scales, for example national level and across terrestrial, freshwater, and marine areas but also subnational scale taking into account state, river basin, protected area, urban, etc.

3.3 Ecosystem accounting at the EU level

Ecosystem accounts has been suggested as a new environmental account module in the European environmental accounts, which would make it mandatory for all European countries to collect this data on a regular basis. However, due to the complexity of ecosystem accounting there might still be some time until a fully developed, internationally harmonized statistical system on ecosystem accounting is in place. (SCB, 2021).

Until now several pilot studies have been made within the EU regarding the determination of the coverage of ecosystem services, how the ecosystems provide benefits for the economy and relevant policy use. Since 2017, Eurostat has co-financed SEEA EA projects in EU Member States including Bulgaria, Denmark, Estonia, Finland, Hungary, Italy, the Netherlands, Sweden, and the United Kingdom. Most of these projects focused on extent and condition accounts and provisioning and regulating services (Bagstad et al. 2021). The EU Commission has one ongoing task force on ecosystem accounting via Eurostat, where Norway and Finland are represented from the Nordic countries. This task force aims to find solutions to some of the challenges the implementation of SEEA- EA faces in EU Member States.

The survey interviews revealed that Norway and Finland would like to see participation from the other Nordic countries during these task force meetings, as they see many synergies across the Nordic neighboring countries, thus it would be beneficial to align common interests and viewpoints with the aim to influence the outcome at EU level.

The EU Commission is currently preparing a legal proposal which includes the ecosystem accounting as a mandatory data collection across all EU Member States. The proposal needs to pass through the European Parliament, and it can take more than four years before it will come into legal force (EU Commission, 2021a). However, the EU Commission has in this proposal set December 2026 as the first data transmission on ecosystem extent account, which a reporting requirement of reference data for year 2024.

According to the most recent legislative proposal from Eurostat, the mandatory ecosystem accounts to be reported by all EU Member States are:

- Extent account

- Condition account

- Services flow account (physical units)

The European framework on ecosystem accounting typology contains three levels of details, where level 1 is an overview of each ecosystem type and level 2 is a further breakdown of level 1 and finally level 3 is an additional breakdown of level 2. All data must be reported in the unit hectare (ha). By consensus it has been agreed to only include ecosystem typology at level 1 within the EU Member States, as a mandatory requirement, which follows the structure in Table 1 below.

Table 1: EU ecosystem typology, level 1. Reference: EU Commission, 2022a.

It was recently decided at the directors’ level meetings on environmental accounts, that monetary valuation should not be included in the EU legal proposal at this stage, focus should be on developing ecosystem accounts in physical units. Additional work on the monetary valuation methodology needs to be done and agreed upon in a wider audience across Europe (EU Commission, 2022a).

The extent and condition accounts are to be reported by all Member States every third year, as there are not large changes in-between each year to justify an annual reporting. However, the physical services flow accounts have an annual reporting requirement (EU Commission, 2022a).

3.3.1 Key initiatives at the EU level

There are two key initiatives on the European level on ecosystem accounting: The Mapping and Assessment of the Ecosystems and their Services (MAES) and the Knowledge Implementation Project on the Integrated system for Natural Capital and ecosystem services Accounting (KIP-INCA). These initiatives play a central role in developing ecosystem accounting (Maes et al. 2021; Vysna et al. 2021).

The KIP-INCA project aims to produce a pilot study for an integrated system of ecosystem accounting in the EU, based upon the principles develop in the guideline System of Environmental Economic Accounting – Experimental Ecosystem Accounting (SEEA EEA) published in 2014 by the United Nations (Vysna, 2021).

The final EU INCA report from 2021 illustrates:

- ecosystem extent accounts across nine different types of ecosystems namely forests and woodlands – cropland – grassland – urban – heathland and shrub - rivers and lakes – inland and wetlands – sparsely vegetated land – marine

- ecosystem condition accounts (forests, agro-ecosystems and rivers and lakes)

- ecosystem services accounts (for a subset of ecosystem services)

The ecosystem extent accounts for the EU INCA report were built upon Corine Land Cover data. The ecosystem condition accounts were built upon utilizing data from the common forest bird index and the EU ecosystem assessment which included number of bird species at a site, tree or vegetation coverage, the amount of soil organic carbon.

The ecosystem services accounts measure the connection between a specific set ecosystem and the production and consumption of activities of households, busines|ses and governments by making use of the supply and use concept. The method used in the INCA project is based upon measuring the two main drivers that affect the use of ecosystem services: the ecosystem service potential and ecosystem service demand. A combination of different economic statistics such as forestry, fishery, and harvested biomass from agriculture was used to define the demand for ecosystem services, thus for other types of ecosystem services modelling techniques was used.

The INCA project also connected monetary values to the ecosystem services for EU 28 countries for year 2012, by making use of non-market valuation methods to estimate the economic worth of non-marketed ecosystem services. The results show that forests supply the largest share of the seven ecosystem services with 47,5% (mostly nature-based recreation, water purification and timber provision), followed by croplands with 36% (mostly water purification and crop provision), followed by grasslands with 9% (mostly nature-based recreation, water purification flood control) and urban areas with less than 1%. Agriculture used 38% of the total supply of ecosystem services (Vysna, 2021).

The European Union has also launched a project which has built an online portal which aims to gather information on natural capital accounting in the EU Member States. The project is named MAIA (Mapping and Assessment of Integrated Ecosystem Accounting). At the MAIA portal factsheets for ten European countries are represented namely, Belgium, Bulgaria, Czech Republic, Germany, Greece, Finland, France, Netherlands, Norway and Spain (European Union, 2022). The other Nordic countries have not been involved in this project, thus does not have a fact sheet available.

3.4 Monetary valuation of ecosystem services

The EU Commission/Eurostat argues that monetary valuation adds value to the traditional System of Environmental Economic Accounting approach. When ecosystem accounts include valuation, it becomes easier to make national trade-offs for decision-makers as well as allocate public spending to protect and restore different ecosystems (EU Commission, 2021b). To make environmental information more compatible with SNA data there is an ambition in the Nordic countries to provide monetary valuation of ecosystem services, although there are different views on to what extent and how monetary valuation should be used. The ecosystem services approach implies that the importance of ecosystem services should be visible to anyone who makes decisions that can affect the environment. Benefits of monetary valuation may occur in connection with socio-economic analyzes, but also to justify inclusion of ecosystem services in national accounts and national wealth calculations (NOU 2013:10; Lai et al., 2018).

The general principle in economic valuation is to estimate changes in overall welfare, and the value of a change in an ecosystem service is thus the change in welfare associated with the change of the service. According to Barton et al. (2019), to be compatible with economic values in the SNA and SEEA, monetary values represented in ecosystem accounting will need to be anthropocentric, instrumental, quantifiable, and monetised. To compile monetary ecosystem asset accounts, Lai et al. (2018) suggests the following three steps:

Step 1: estimate the physical term of expected ecosystem services flows

Step 2: estimate the monetary term of expected ecosystem services flows

Step 3: estimate the monetary value of an ecosystem asset by discounting the monetary value of expected ecosystem services flows

This underlines the fact that the physical accounting of ecosystem services (Step 1) is the basis for all monetary valuation. In order to translate physical quantities into monetary values a range of methods are available, including

- Market prices

- Capital costs

- Avoided costs

- Time value (direct use values of experience services)

- Simulated prices / transaction values

- Hedonic methods

- Willingness to pay

- Travel expenses

For provisioning services and some cultural services market prices exist and can be used directly in ecosystem accounts. For example, the market value of food production, timber production and Christmas trees are already registered in economic accounts. For most regulation services and some cultural services that do not have markets, other methods are needed for monetary valuation. For example, when ecosystems provide water retention or erosion control, the corresponding investment and running costs of providing these services by other means may be used to estimate the value of these regulating ecosystem services. Carbon prices exist in different contexts, such as the EU Emissions Trading System (EU ETS), and may be used to impute monetary values on carbon sequestration and carbon storage by natural systems. And the monetary value of recreation services may be based on the revealed willingness of consumers to take on travel expenses for visits in nature (Vihervaara et al., 2018).

In December 2021, Eurostat provided a paper which illustrated the concepts and methodologies for monetary valuation of ecosystem services by using simulated exchange values (EU Commission, 2021c). This methodology simulates hypothetical exchange values, which could be fees for different ecosystem services that some people would be willing to pay, usually derived through contingent valuation or choice experiments. Then supply and demand of ecosystem services are simulated to arrive at prices at equilibrium (EU Commission, 2022b).

It should be noted that provisioning services, such as crops, timber or fish, will already be included in the SNA measurement although not attributed to ecosystems (Barton et al., 2019).

There are a number of challenges associated with monetary valuation of ecosystem services, and there has been controversy on the implications of providing economic values to nature which may open up the door for new markets for ecosystem services at the expense of legal instruments (NOU 2013). In addition to moral discussions there are more technical reservations that also must be made.

In many cases the biophysical accounting is the main challenge rather than monetary valuation, but the latter cannot be better than the understanding of the underlying biophysical linkages (Barton et al., 2019), at least if the process of valuation follows the three steps suggested by Lai et al. (2018) (above). Since one of the main purposes of ecosystem accounting is to compare how ecosystems change over time it may to some extent be sufficient to monitor changes in biophysical accounts. Comparing monetary values of different kinds of ecosystem services is also risky since valuation is typically carried out with different methods for different services and may therefore not be readily comparable. It is not evident, for example, that estimated costs for replacing ecosystem services (such as water retention or erosion control) should be compared with the willingness to pay for other ecosystem services.

More work is needed to establish practices for extrapolation of monetary valuation, and for scaling up biophysical ecosystem functions from research sites to whole ecosystem assets (Barton et al., 2019). Economic valuation is typically performed using micro-economic perspectives, and even market prices are established in situations characterized by market equilibrium. Hence estimated values may only be valid assuming marginal variations in market conditions, which limits the applicability of valuation in ecosystems where rapid loss of biodiversity and ecosystem functions occur.

4. Ecosystem accounting in the Nordic countries

In this chapter, the analysis of the survey interviews is presented. To present the responses in a structured way, the interview questions were connected to six thematic areas, illustrated below in figure 3. The questions and answers in each thematic area will be reviewed chronologically.

Figure 3: Overview of thematic areas of the analysis.

4.1 State-of-the art

How do the Nordic countries differ in terms on developing ecosystem accounting?

In Norway there is a longstanding established cooperation between the Statistics Norway, NINA (the Norwegian Institute for Nature Research), NIVA (Norwegian Institute for Water Research), NORAD (Norwegian Development Aid) and NIBIO (Norwegian Institute for Bioeconomy Reassert) in terms of data exchange and developing methods and ideas for the development of ecosystem accounting. These organisations have been working jointly on multiple projects in the past on ecosystem services. Recently, a trend shift has occurred in Norway where the ecosystem accounts have been moved into Statistics Norway as a new statistical area to be further developed. Until recently, ecosystem accounts have to a large extent been viewed as a research topic. Norway has recently started the process of integrating this new statistical area of ecosystem accounts into the traditional national accounting department of Statistics Norway, together with the other environmental accounting modules of the SEEA CF. Due to the longstanding work of ecosystem and biodiversity issues, Norway has established a wide knowledge base of ecosystem services. However, this information is scattered in many different organisations or agencies.

After conducting all interviews across the Nordic countries, we can conclude that in Finland there is a mutual understanding and solid partnership between the Finnish Environmental Institute (SYKE) & Statistics Finland on ecosystem accounts. These organisations have been working jointly for many years on developing ecosystem accounts. A new recent trend can be seen across Finland, launched by businesses in the private sector, where they are joining the ongoing discussions on the importance of protecting biodiversity and coping with the ongoing climate crisis. Focus is on how the private sector can align their business goals with ecosystem targets etc. Overall, in Finland there is a growing interest for ecosystem accounting and environmental economic accounting.

According to the interviews conducted with Danish experts, some cooperation has taken place between University of Copenhagen, Arhus University and Statistics Denmark in terms of data production and data exchange for ecosystem accounting. The first steps have been processed via the national development of a Danish land use database. This land use database is planned to be used as a basis for mapping ecosystem services and ecosystem accounts. Currently, this database is being used by Statistics Denmark in its statistical data production of land accounts. It contains a consistent way of tracking and monitoring land use change for Denmark with a high spatial resolution. Additionally, and independently, some pilot studies have been conducted both from Aarhus University and University of Copenhagen with an environmental economic point of view. In these pilot studies researchers mapped ecosystem services, modelling and valuation of ecosystem services. It was mentioned during the interviews that, going forward, these partnerships between the national statistical office and the Danish universities need to be further enhanced and developed.

The organisations in Sweden indicated that until today, limited cooperation has taken place in terms of developing ecosystem accounts. Independently, some pilot studies have been made in the area, (see for example Statistics Sweden 2017; 2021). To develop ecosystem accounts for use in policy and decision-making processes, more extended cooperation needs to be set up among relevant actors in Sweden.

The interviews revealed that Iceland is currently at an early stage, the country still needs to understand the whole concept of the ecosystem accounting, in terms of setting-up the framework, to understand and map which data sources to make use of. Iceland has recently paused the development process, until they have completely understood how the output data is supposed to be utilized. As of today, it is unclear for Iceland what questions the ecosystem accounts will be answering, as the country is a volcanic island, with low forest cover and low amount of land area under arable cultivation.

Ecosystem accounting is not a priority statistical area for the Faroe Islands. The fact that the Faroe Islands is not part of the European Union implies the country is not part of the European statistical cooperation, thus it does not have any legal reporting requirements in this regard.

Have all the Nordic countries implemented the international principles from the UN SEEA EA framework?

The level of development is quite different among the Nordic countries, as mentioned in the previous section. In Norway, Statistics Norway has started the plans of how to integrate the UN SEEA EA framework into its regular statistical production from year 2024. In recent years a large amount of research, methodology development and pilot testing has taken place between different organisations in Norway, thus the country has established a good foundation for implementing the SEEA EA framework. Norway mentioned during the interview that they see close collaboration between researchers, municipalities, and governmental agencies as a prerequisite for a successful establishment of ecosystem accounts in their country.

Finland mentioned during the interviews that it has not yet been decided who will be the responsible organisation for developing ecosystem accounting according to the UN SEEA EA standards. Currently, negotiations are taking place between Statistics Finland and SYKE in this regard. These two organisations both have experts who cover statistics, national accounts, ecosystem, and biodiversity topics. SYKE is currently drafting an internal road map which is intended to be used as a basis for the ongoing decision process on the responsible institute for developing ecosystem accounts in Finland. This internal road map is planned to be finished by SYKE during the summer of 2022.

Denmark is following the legal process at the EU level, in terms of requirements and how it will affect the country’s reporting demands. Statistics Denmark has defined a schedule for drafting an internal roadmap within the organization.

During the spring of 2022, Statistics Sweden has started working on a Eurostat grant project on SEEA EA, where the aim is to establish a road map for how Sweden will manage and implement this new framework. This road map is planned to be ready by December 2022. Once this road map is ready, a more detailed plan will be drafted. Statistics Sweden is closely following the ongoing legal discussion at the EU level, in terms of how the requirements will affect the country’s reporting demands. It was mentioned during the interviews that Sweden most likely will need to make use of land cover data from the Copernicus Corine Land Cover inventory (CORINE Land Cover, 2022) database to fulfil the legal obligations.

As stated under the previous section both Iceland and the Faroes Islands are not at a stage where they have started the planning of integrating the SEEA EA framework. Both islands need to better understand the usefulness to them of implementing ecosystem accounts. On the other hand, Iceland is an EEA (European Economic Area) and EFTA (European Free Trade Association) member state and collects data and compiles statistics for national and EU purposes.

How much data on ecosystem accounting is currently available and for which years?

In Denmark, two main studies were carried out before the UN SEEA EA principles were agreed upon. The first study focused on mapping of ecosystem services (Termansen et al. 2015) and the second study focused on modelling, quantification and valuation of ecosystem services and biodiversity indicators (Termansen et al 2017). Denmark also has consistent land use/land cover data since 2012 and long time series of forest data.

Norway has long before the UN principles for EA were set, developed various overviews of ecosystems with help from different Norwegian research institutes and universities. SSB has conducted assessments of extent accounts and resources through maps and statistics, but other research institutes are also mapping various data from ecosystems. NINA is responsible for monitoring the development of the state of ecological resources and develop indicators for forest and mountain ecosystems while NIBIO is responsible for the data on coastal ecosystems and recreational aspects and carbon sequestration in different ecosystems. The Norwegian Environment Agency gathers data on the status of biodiversity.

Finland has previously mapped different alternatives for ecosystem extent accounts. Finland also has long time series data on forestry. Some pilot studies on mapping ecosystem services have also been made. Plenty of historical data is available in Finland including long time series available for land cover data from 2000–2018. A technical challenge is that old datasets are causing conflicts with existing data as resolution and details are different. These are causing uncertainties in interpreting the data as well as different results for ecosystem accounts.

In Sweden, high quality data on ecosystem extent accounts is available where the data is connected to private and public ownership. Less data is available on ecosystem condition and ecosystem services. Two pilot studies on ecosystem accounting from 2015 and 2018 are also available.

Examples of data on ecosystem extent accounts, ecosystem condition accounts and ecosystem services accounts available in the Nordic countries are listed in Figure 4.

Figure 4. Data on ecosystem accounts (extent, condition, ecosystem services) available for the Nordic countries.

4.2 Use and understanding of ecosystem accounting

Can there be seen any common user groups and user areas in the Nordic countries?

The interviews revealed that there were several common user areas for the ecosystem accounts across Finland, Sweden, Denmark and Norway. It was highlighted that user areas such as policies for land use and water resource planning, and infrastructure development is of great importance when these countries will commence developing ecosystem accounts on a national level. These four countries have a common understanding of the need for creating a harmonised statistical framework for its national ecosystem service data.

The same countries mentioned some common user groups, which include local governments, regions, environmental protection agencies, NGOs, line ministries mainly Ministry of Environment, but also other ones such as the Ministry of Finance. For instance, in Denmark, the Ministry of Finance is currently building a Green Economic Model, which is planning to integrate the data from both SEEA CF and SEEA EA into the modelling framework. Therefore, Denmark sees this as a priority area to develop further. It was also mentioned in these countries that they see researchers as an important user group. Researchers have the capability of seeing new connections and possibilities between the SEEA CF, SEEA EA and SNA, thus they can develop new research questions to address and potentially use the output data for additional analysis purposes from a researcher’s point of view.

These mutual understandings and user areas across Finland, Sweden, Denmark and Norway could also be related to the natural features of these countries, as they all have forests, cropland, grassland, urban areas, rivers and lakes to different extent whereas Iceland’s and the Faroe Islands’ natural features and agricultural practices are different partly due to their geological island features.

Iceland was the only Nordic country which highlighted that they see it as a major challenge to get ecosystem account information into Iceland’s policymaking. This understanding could also be linked to the statement in the previous question under ‘4.1 state of the art’, where Iceland has taken a step back to get a better understanding of how the outputs from the Icelandic ecosystem accounts should be used in a national setting.

Do all Nordic countries understand, what output data from the ecosystem accounts should be used for?

No, all Nordic countries do not understand the use of SEEA EA. The current design of the SEEA EA framework does not fit well with Iceland’s conditions as a volcanic island. It was mentioned during the interview that they see the classification as too broad. Iceland has little vegetation, forest or cropland, but has extensive amounts of wetlands and lakes. Iceland considers the output data from the ecosystem accounts to not give any valuable information from their country’s point of view. They see the use of ecosystem accounts for the other Nordic countries, as these countries have large areas of forests and agricultural lands, and so forth. Norway, Finland, Sweden and Denmark’s have similar characteristics of natural environments; on the contrary Iceland’s is different.

The Faroe Islands believe that in relation to the major environmental challenges the world faces today, all nations have a responsibility to create the basis for a better understanding of the relationship between environmental and economic factors. A common international framework like System of Environmental Economic Accounts, which follows a structure and is consistent with the System of National Accounts is an essential statistical tool in doing so. However, the Faroe Islands have not yet been able to prioritise resources for developing environmental economic accounts.

Denmark considers a national system of ecosystem accounting to be an important tool. They see it as a good tool for analysing trade-offs or obtaining an understanding of where in Denmark the most valuable nature areas are located. Denmark see a great value in bridging all the different ecosystem dimensions together in a harmonized statistical framework. Today all this information is scattered across various organisations in Denmark. The interviews indicated that the ecosystem accounts are not likely to provide any additional knowledge, as Denmark already has data and information about for example, forest cover, timber supplies or forest carbon stocks.

Ecosystem accounting is mainly a new tool to organize national data on ecosystem services with different spatial resolutions that can highlight different ecosystem services and their interdependencies.

Norway considers output data to be a very useful tool in terms of policy planning at local or regional level, climate planning, and other policy purposes. They also see the output data of importance for measuring and monitoring different Sustainable Development Goal indicators. Additionally, Norway views output data from the ecosystem accounts to be of importance for evaluating various policy decisions on both a local, regional and national level.

Today in Sweden, there is a lack of a statistical framework which collects of all the ecosystem data in a coherent way. Sweden considers the development and output data from the ecosystem accounts as an important tool for policy use. The country sees a need for ecosystem accounts to fulfil environmental targets at a regional and local government level. In Sweden, the focus has been on considering land use and ownership, as a necessary basis for ecosystem accounts.

The survey interview with Finland indicated that they consider output data from the ecosystem accounts as a very important tool for the entire statistical world and for the decision-making sphere, not only due to the European Union legal act. Today there is a clear consensus between SYKE and Statistics Finland of the importance of ecosystem accounting. These organisations have an aim to raise the awareness on the importance of the ecosystem accounting, both to the broader public and to different line ministries. Finland has plans to soon launch a communication campaign in this regard, with the aim to give user groups information about the importance and use of the data developed from the SEEA EA.

4.3 Current and future use of models for the valuation of ecosystem services

Ecosystem services often support each other, but there can also be trade-offs between ecosystem services. We asked all the Nordic countries if they had considered these relationships between these ecosystem services during their previous pilot studies.

Within the sphere of different ecosystems such as forests, wetlands, agricultural land and marine areas the Nordic countries are supporting each other to maintain a diversity of plants and animals. There can also be trade-offs between ecosystem services. During the interviews the Nordic countries were asked if they had considered these relationships when conducting their previous pilot studies on ecosystem services.