Too slow progress

The Nordic industry is struggling with decarbonisation, as the Nordic GHG emissions from industry have remained almost unchanged over the past decade.

Reducing industrial emissions is challenging, and there has not been a sufficient decoupling between production levels and emissions. Consequently, industrial emissions increase with rising production. Breaking this connection requires substantial updates to industrial processes, which have not yet occurred on a large scale.

The Nordic industry has been growing with increasing speed since the 1990s, increasing the overall industrial energy consumption. However, this is countered by a decrease in the carbon intensity of industrial consumption. Additionally, the heat consumption in in the industrial sectors is drastically increase since 1990’s.

It is crucial to switch to less carbon-intensive solutions while maintaining growth. While there are emerging hydrogen projects in the Nordics, recent delays and cancellations of several green investments, including power-to-X projects, hinder progress.

Industry energy consumption

Since 1990, industrial energy consumption has seen varied trends. Finland and Norway experienced increases of 19% and 11%, respectively, while Iceland's industry consumption skyrocketed by 250%. In contrast, Denmark and Sweden managed to reduce their industrial energy consumption by 11% and 5% in 2021.

All Nordic countries, except Norway, have reduced their fossil fuel usage in the industry sector. Norway's fossil fuel consumption has remained relatively stable, with an overall increase of 7% since 1990. Electricity consumption in industry has risen in all countries except Sweden, which achieved a 13% reduction. Notably, electricity accounts for 97% of Iceland's total industrial energy consumption.

Heat consumption has surged in Finland, Norway, and Sweden since 1990, while Denmark saw a more modest increase of about 18%. Unfortunately, there is no data available for Iceland's industrial heat consumption. Biofuel consumption has increased significantly across all Nordic countries, ranging from 30% to 70% since 1990, with Finland and Sweden being the largest consumers at 174 PJ and 200 PJ in 2021, respectively.

Source:World Energy Balances IEA

Carbon intensity of industry energy consumption

Carbon intensity in industry consumption has decreased across all Nordic countries since 1990 except Norway, where it has seen a slight increase.

Iceland has made a remarkable reduction, bringing its carbon intensity down to 1 tCO2/TJ in 2022. This is a significant achievement compared to Denmark, which has the highest carbon intensity among the Nordic nations at 40 tCO2/TJ in 2022.

GHG emissions development in industry

Since 1990, Norway has consistently had the highest greenhouse gas (GHG) emissions from industry among the Nordic countries, despite a significant reduction of 37% by 2022. This is largely due to its substantial oil and gas sector. In contrast, other Nordic countries have seen a slight decrease in industrial emissions since 1990, with the exception of Iceland.

Iceland's industrial emissions have surged, primarily due to the addition of new aluminum smelters, which are major sources of greenhouse gases. Specifically, Denmark's industrial emissions decreased by 21% in 2022, Sweden's by 7%, and Finland's by 5%, while Iceland's emissions have increased by more than 120% since 1990.

Over the past decade, Denmark’s emissions have decreased by 19%, Finland’s by 15%, and Sweden’s by 6%, continuing the downward trend observed since 1990. In contrast, Iceland’s emissions have continued to rise, increasing just by 6%, while Norway’s emissions have reversed their long-term downward trend, increasing by 4% in the past decade.

Source: Nordic Statistics

In the spotlight:

Stegra’s plant in Boden, Sweden

Stegra, formerly H2GS Boden AB, is set to build the world’s first large-scale, low-carbon, hydrogen-based steel manufacturing plant in Boden, northern Sweden. This groundbreaking project, powered by renewable sources, aims to produce 5 million tonnes of high-quality steel annually by 2030, with production starting in 2025. The plant will utilise a hydrogen-based direct reduction process combined with electrified downstream facilities, significantly reducing CO₂ emissions by up to 95% compared to traditional steelmaking methods.

The innovative approach replaces coal with hydrogen, produced on-site using Europe’s largest electrolyser powered by renewable energy. This process will primarily emit water and heat instead of CO₂, marking a significant environmental breakthrough. The project also emphasises circularity, ensuring minimal waste and maximum resource efficiency. This positions the plant as a pioneer in low-carbon steelmaking in Europe and globally.

From a productivity standpoint, the project leverages established technologies on a large scale, enhancing Sweden and Finland’s research and development capabilities in green steel manufacturing. It supports the Swedish steel industry’s transition to more sustainable methods, contributing to the post-fossil fuel era.

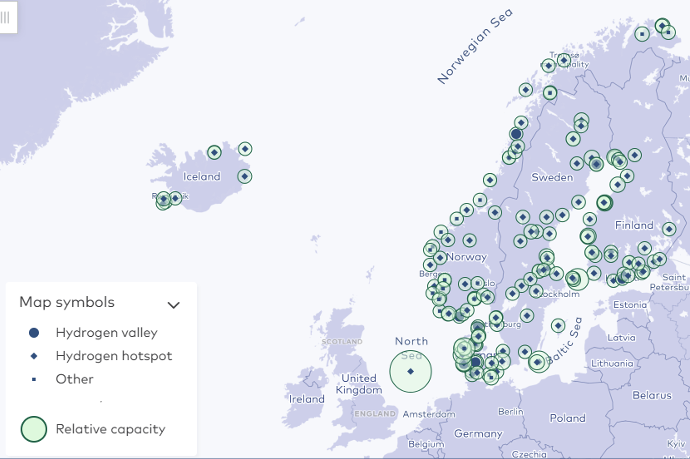

Insight into “Nordic Hydrogen Valleys - value chain mapping across the region”

The Nordic Hydrogen Valleys project by NER focused on fostering the growth of Nordic hydrogen valleys, facilitating the exchange of knowledge among Nordic stakeholders, and highlighting Nordic strengths in hydrogen value chains. This was accomplished by establishing definitions for hydrogen valleys and hotspots, mapping hydrogen projects throughout the Nordic region, and categorising them based on specific criteria.

The criteria for hydrogen valleys include:

- covering a specific geography in at least one Nordic country,

- covering at least two steps of the hydrogen value chain (production, distribution, use),

- having a hydrogen production capacity exceeding 500 tonnes per annum (tpa),

- supplying hydrogen to at least two different end-use sectors, and

- having at least reached the feasibility phase (feasibility study).

Nordic hydrogen hotspots are projects that do not qualify as hydrogen valleys but fulfill criterion 1 and at least two of criteria 2–5.

Denmark, Finland , Iceland, Norway and Sweden* has 162 hydrogen projects. Together, these projects aim for a total planned hydrogen production capacity of 7,221 kilotonnes per annum (ktpa). Among these projects, 123 are classified as hydrogen hotspots. Hydrogen hotspots encompass both direct and indirect uses of hydrogen, such as producing fuels or chemicals. These hotspots alone account for 5,986 ktpa of the planned hydrogen production capacity.

Country | Total number of H2 projects | Total planned H2 production capacity (ktpa) | Number of hotspots |

29 | 3 748 | 18 | |

36 | 1 126 | 39 | |

9 | 112 | 9 | |

50 | 711 | 24 | |

38 | 1 524 | 37 |

Source: Nordic Hydrogen Valleys-value chain mapping across the region, NER

Plans for an extensive H2 grid

The European Hydrogen Backbone initiative consists of over 30 infrastructure operators who aim to accelerate the European decarbonisation by defining the critical role of the hydrogen. Their current plan is based on a range of production facilities, storages, consumers, and hydrogen grid.

The European Investment Bank estimates that the total investment needs could be up to 500 billion euros by 2050. However, the recent economic uncertainty and a period with higher interest rates, have delayed and halted several projects significantly delaying the overall progress.