- Front page

- Contents

- Executive summary

- 1. Industry specific drivers

- 2. Vision for the future

- 3. Consisting gaps

- 4. Transformation & Scale

- Appendix 1: Value chain of the industries

- Appendix 2: Current state analysis and circular opportunities

- Appendix 3: Additional details on sources

- About this publication

MENU

Contents

Executive summary

This playbook builds on the Nordic Circular Economy Playbook, and is tailored to companies in the Nordic manufacturing industries. It provides examples on the following five sub-sectors:

- machinery & equipment,

- maritime,

- energy,

- transportation,

- construction

- Companies need to transform and scale their business as a response to increased pressure from industry drivers, as well as unlocking new business opportunities in order to face climate change related challenges

- Circular economy and circular business models are about turning inefficiencies in linear value chains into business value. This playbook identifies key circular business models for the industry sub-sectors as well as key ecosystem actors to enable transformation across the value chain

- There are three stages a company typically needs to undergo on their transformation journey; explore & shape, attract & win, and scale and keep growing. This playbook focuses on the third stage and outlining the main challenges when scaling, which are related to people & culture, new collaborations, lack of transparency, and the sustainability organisation ownership

- The playbook is also describing the key enablers to fully transform and become a circular business; (a) focus on making one part of the business fully circular before scaling, (b) integrate data & technology in the entire transformation journey, (c) invest in the people and the organisation, and (d) have a dedicated transformation team

1

Industry specific drivers

CHAPTER SUMMARY: Industry specific drivers

Governments and regulators need to deliver on their circular economy and climate commitments, forced through policies and regulations at record speed as well as companies setting their own circular targets The increased pressure from regulators, B2B customers, and investors push businesses to change their way of working by adopting new business models Businesses should embrace opportunities stemming from resource and climate change related challenges, thus giving them a first-mover advantage and unlocking growth opportunities

This chapter will help you:

- Understand the increased requirements from stakeholders on circular economy and sustainability transparency across the value chain

- Learn why transformation to a circular economy is needed

Additional material that can be found in the Nordic Circular Economy Playbook:

- Understand why the circular economy offers an advantage compared to the linear value chain in terms of addressing inefficiencies and untapped value potential

- Learn why now is a good time to shift from linear to circular business

- Supporting tools: Value case tool to calculate high-level business case for circular business models

Increased pressure from stakeholders push manufacturing companies to transform their business, entering untapped circular opportunities

Introduction of drivers

|  |  |

| REGULATORS | B2B CUSTOMERS | INVESTORS |

| New circular and sustainability regulations are proposed and entered into force at a record speed The scope of regulation is expanding – regulations cover the entire value chain (incl. material, design, production processes, and waste handling) The enforcement starts with prioritized industries, incl. energy, construction, transportation etc. | Companies are facing increased pressure from buyers’ supply chain sustainability targets There are accelerating requirements for upstream suppliers to report on ESG, and to showcase concrete actions towards circularity and carbon reduction B2B customers require greener products and services from their value chain partners to meet customer requirements and keep competitive position | Investors are adjusting their portfolios towards sustainability, encouraging portfolio companies to develop their ESG reporting and carbon data disclosure Investors are placing greater emphasis on companies’ ESG performance when making investment decisions Companies that are acting have priority to access financial resources |

Being both resource and carbon intensive, the manufacturing industry is at the forefront facing the challenges, as well as the massive business opportunities ahead when emerging on a circular transformation journey | ||

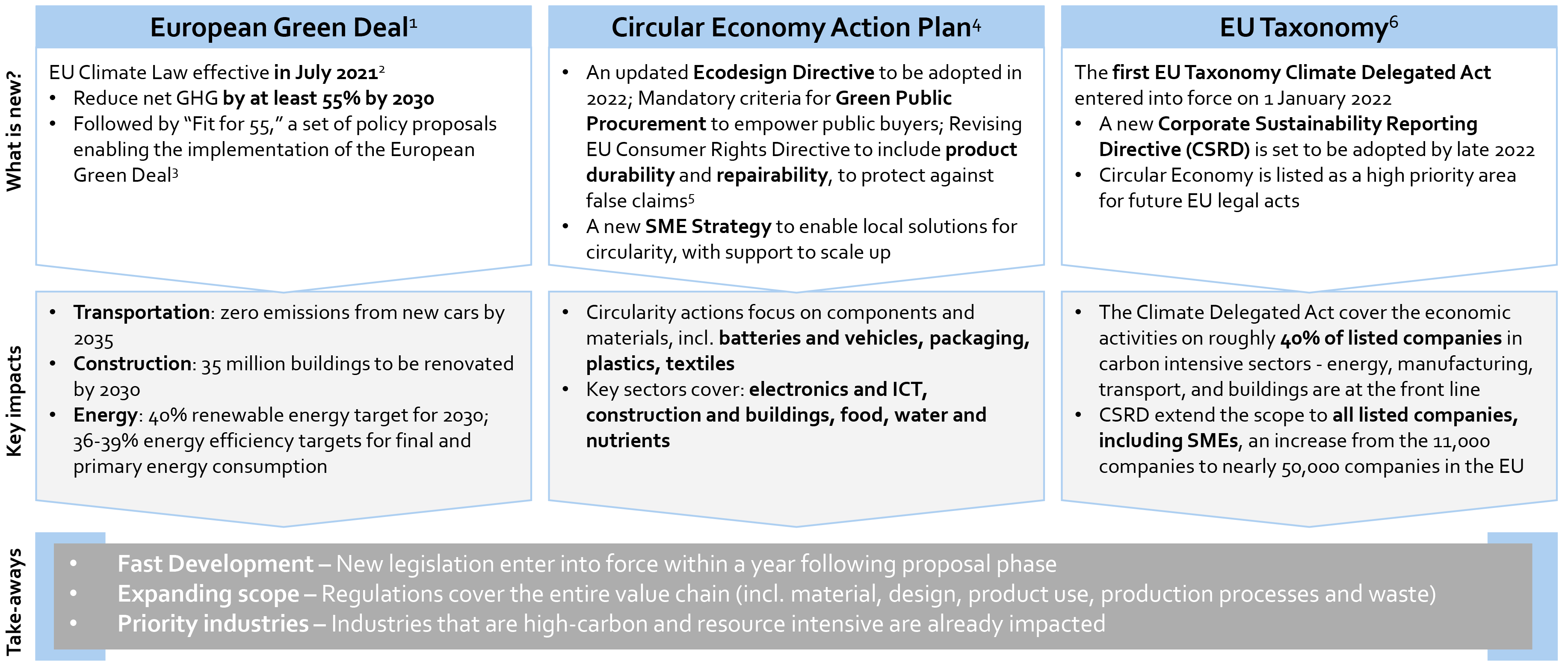

EU regulations are updated at a record speed with increased ambitions to drive transformation towards circular economy

Regulators

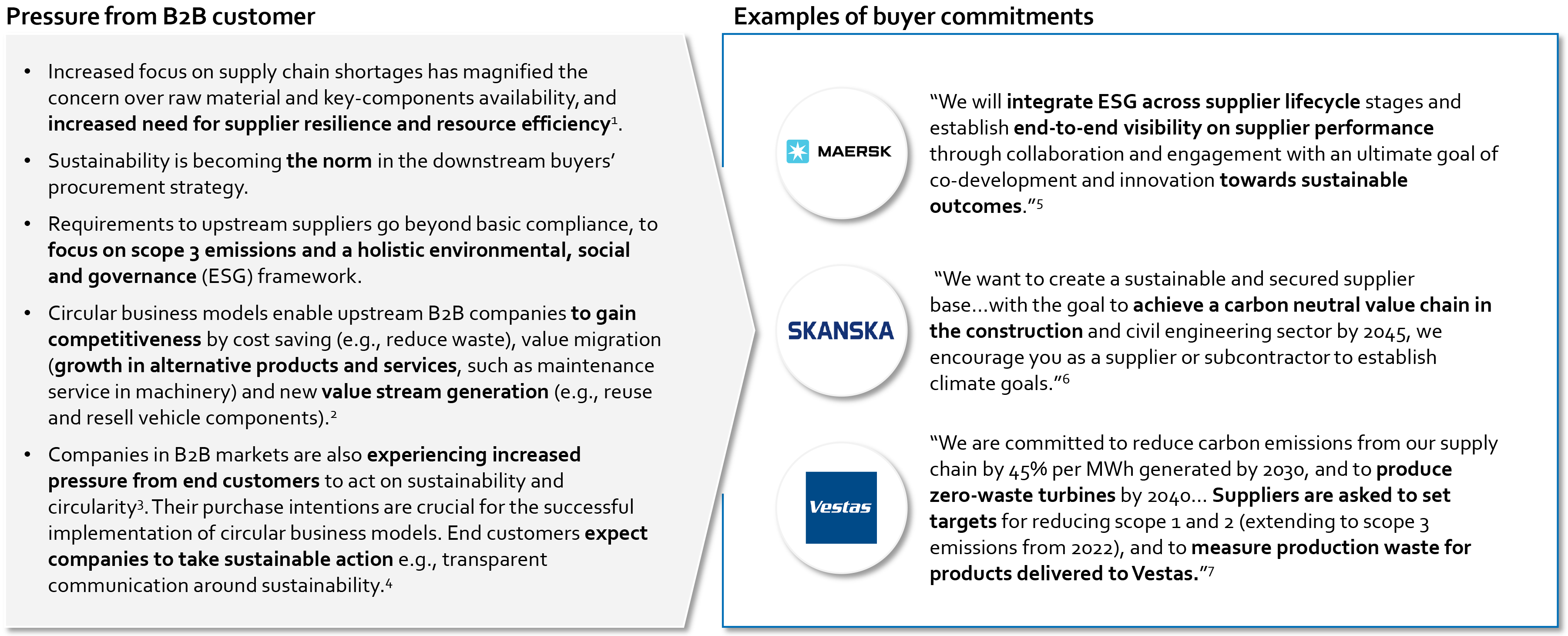

Companies in B2B markets are facing increasing pressures from buyers’ supply chain sustainability targets

B2B Customers

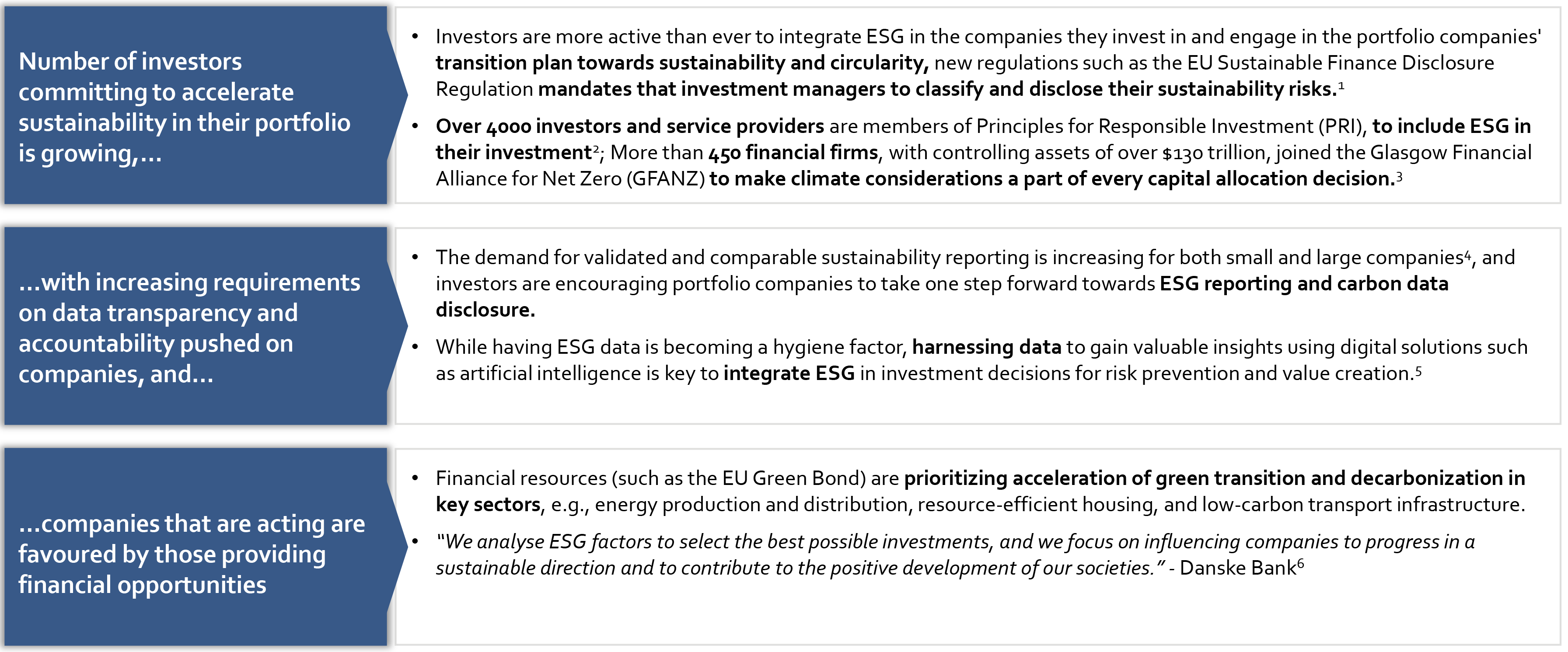

Investors are holding companies under increased scrutiny and accountability for their sustainability actions

Investors

2

Vision for the future

CHAPTER SUMMARY: Vision for the future

The circular economy offers companies the opportunity to turn inefficiencies in linear value chains into business value Based on the inefficiencies that occur across the value chain as well as the external drivers for each industry sub-sector, three key circular business models have been identified for each sub-sector To unlock the circular business value, ecosystem collaboration is important. Therefore, key actors in the ecosystem have been outlined for the key opportunities in each sub-sector Circular business model examples from leading Nordic and global manufacturing companies demonstrates a strong case for circularity

This chapter will help you to:

- Understand how the future ecosystem can look like for manufacturing industries and that circularity only can be achieved together; it requires building an ecosystem of partners in order to achieve scale and economic viability

- Learn which circular business models are the most promising in your industry and what role you can play in the ecosystem

Additional material that can be found in the Nordic Circular Economy Playbook:

- Assess the major inefficiencies and waste driver in your linear value chains as a lens for untapped circular opportunities

- Explore technologies that can enable your selected circular business model(s)

- Supporting tools: Business model development toolkit, Ecosystem partner identification tool

The circular economy is about turning inefficiencies in linear value chains into business value

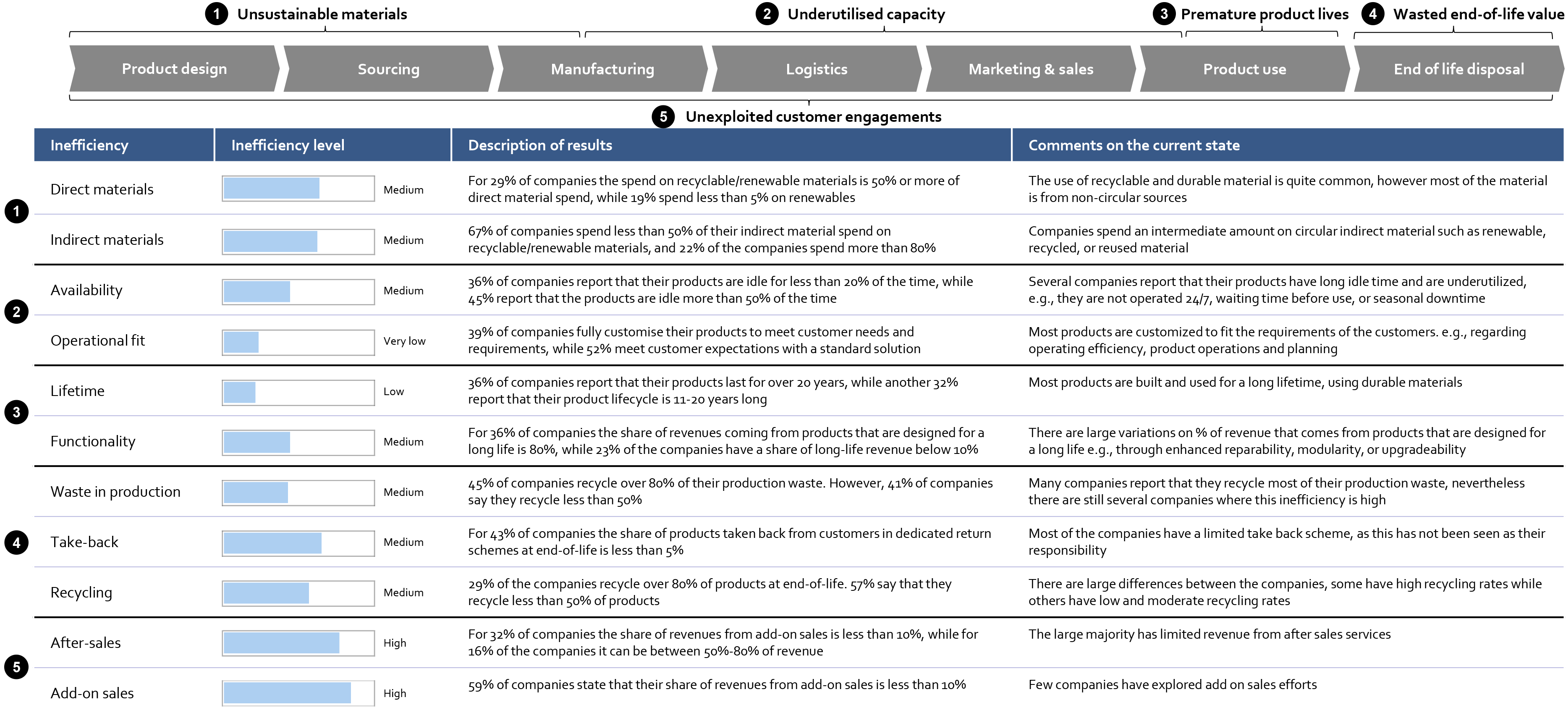

Inefficiencies in linear value chains

Inefficiencies are largest at the start and end of the manufacturing value chain – add on and after sales services have unexploited potential

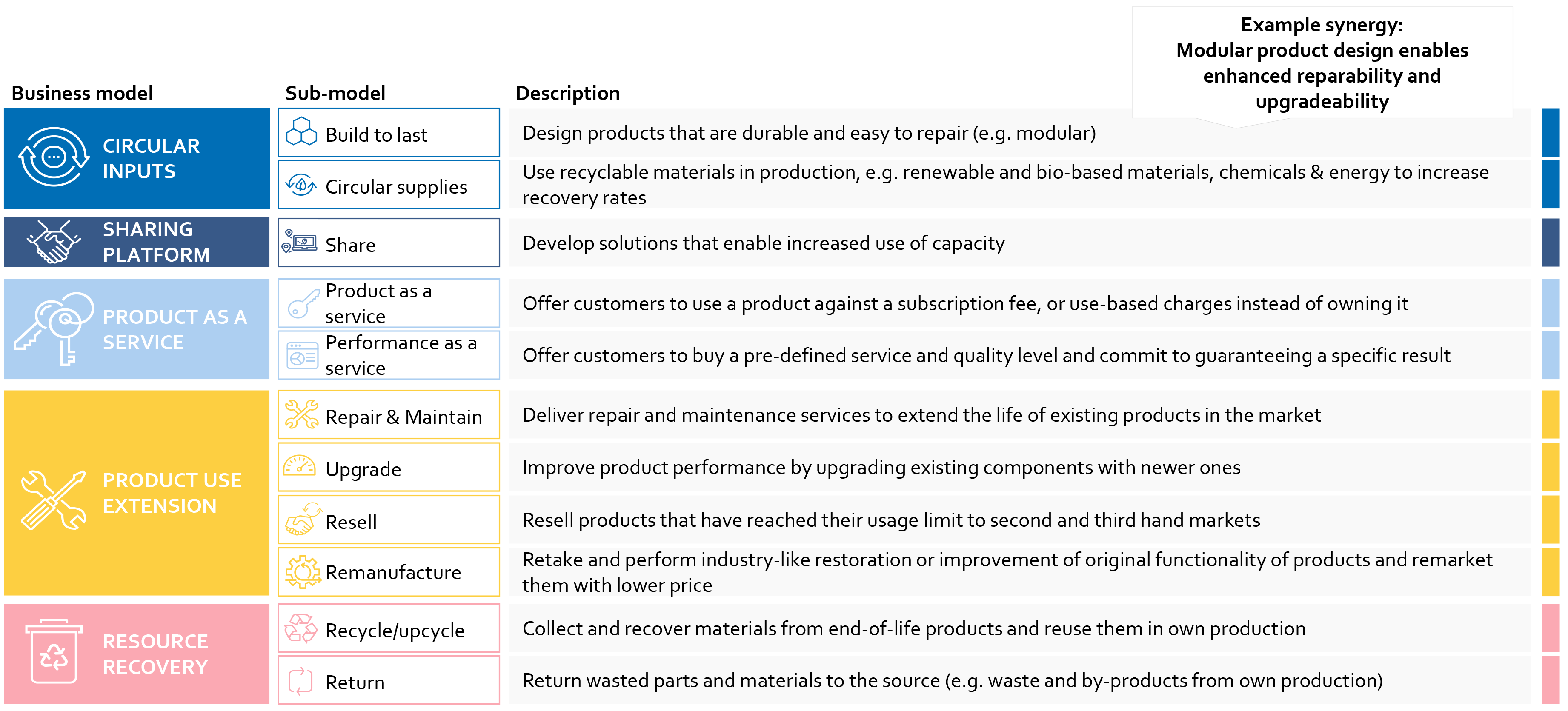

Five business models reduce the inefficiencies and create value for companies

Circular business models

Companies can explore the sub-models individually or as powerful combinations

Circular business models

Key opportunities have been identified for industries to reduce inefficiencies and create value as companies scale and transform

Key circularity opportunities

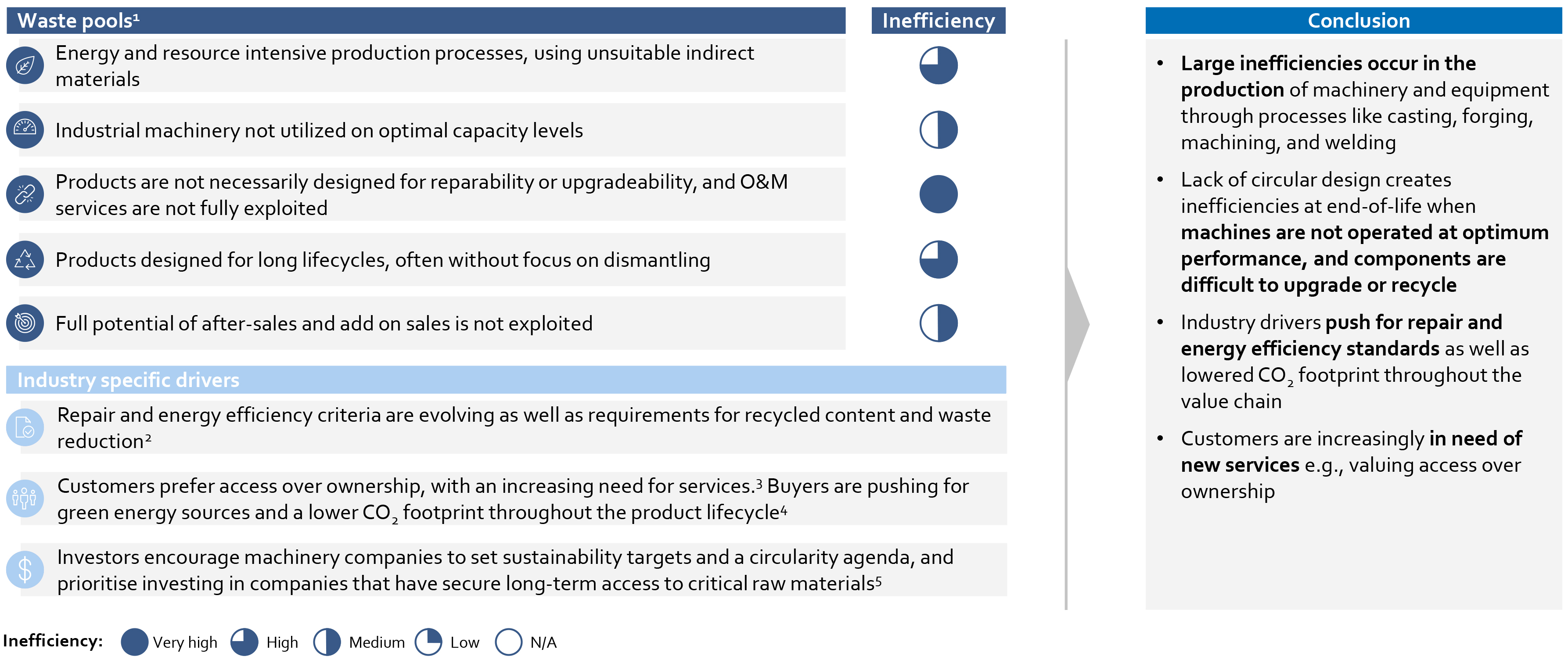

Inefficiencies occur across the value chain, especially in production from underutilized capacities, and at the end-of-life

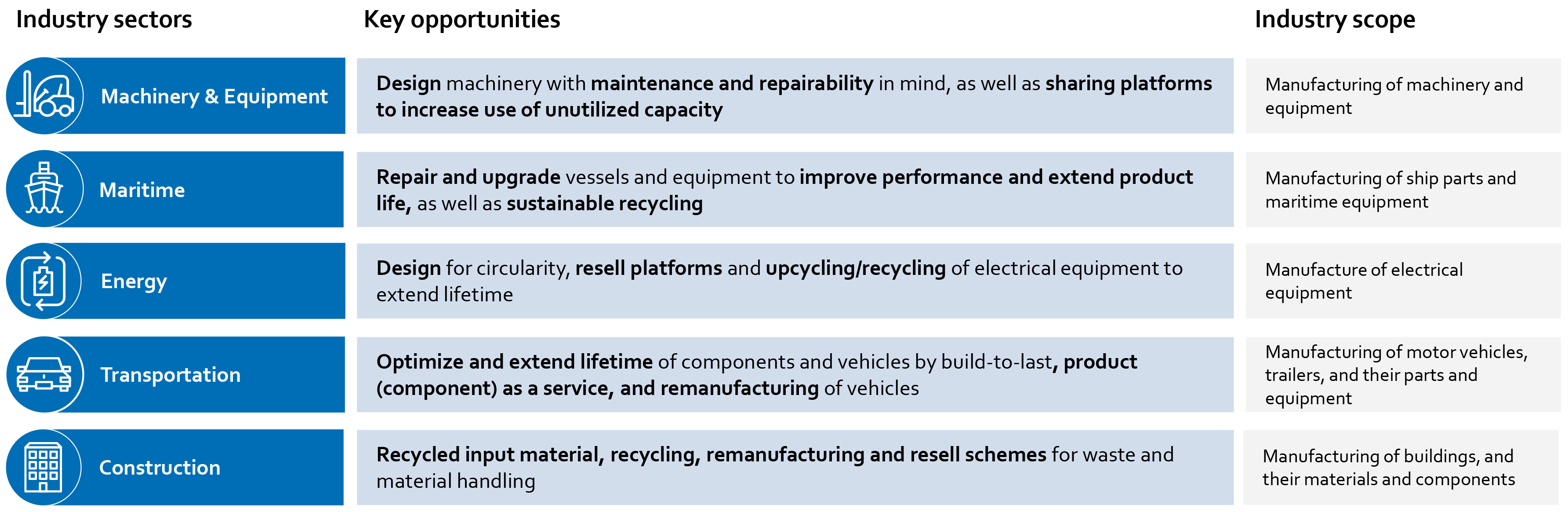

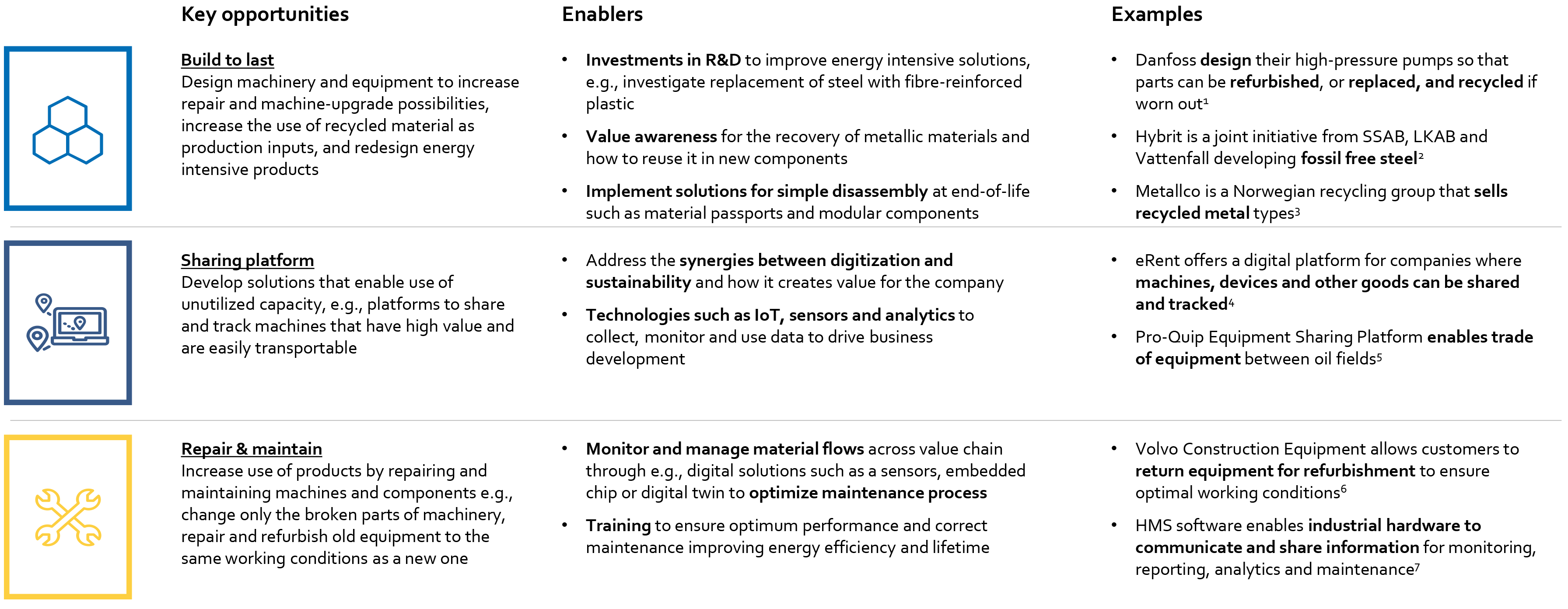

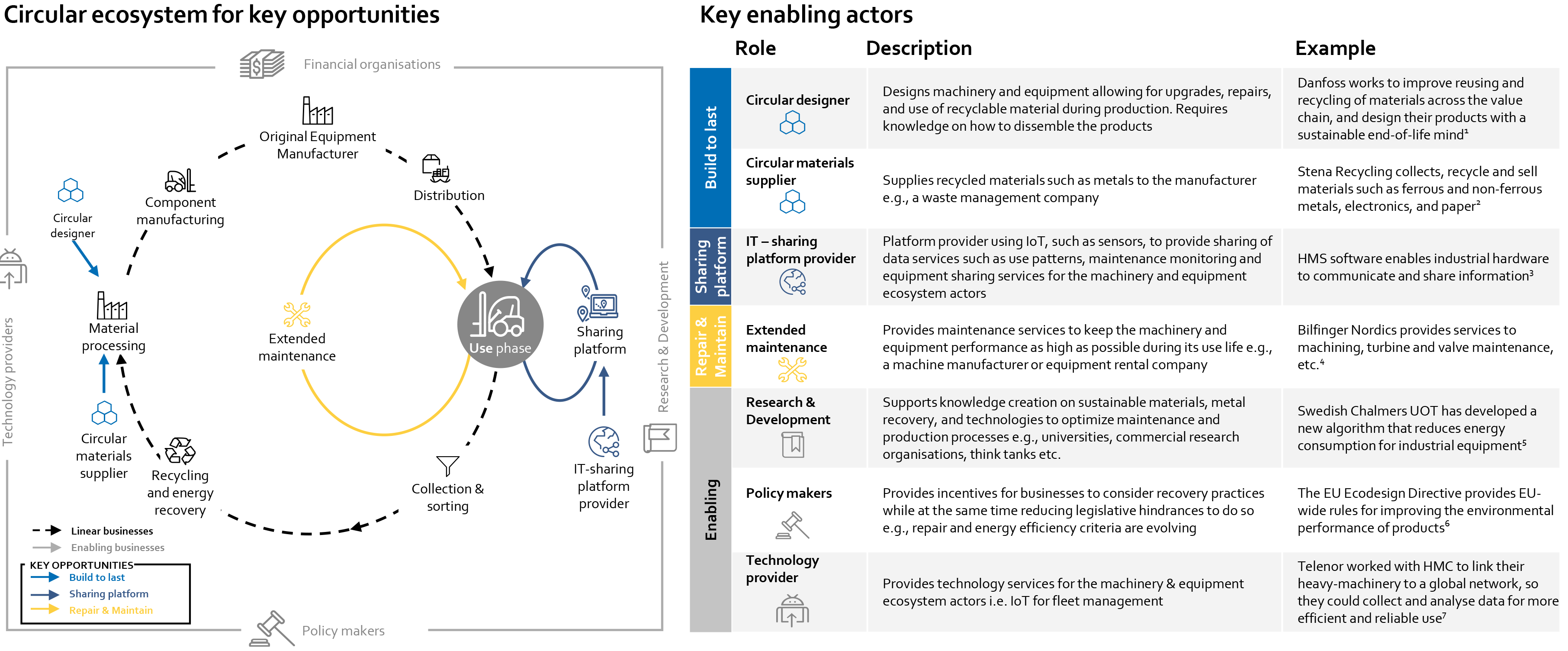

Key opportunities: Machinery & Equipment (1/3)

Design machinery to increase repairability and product maintenance as well as sharing platforms to increase use of unutilized capacity

Key opportunities: Machinery & Equipment (2/3)

To unlock key opportunities in the industry, ecosystem actors need to know their role and together collaborate across the value chain

Key opportunities: Machinery & Equipment (3/3)

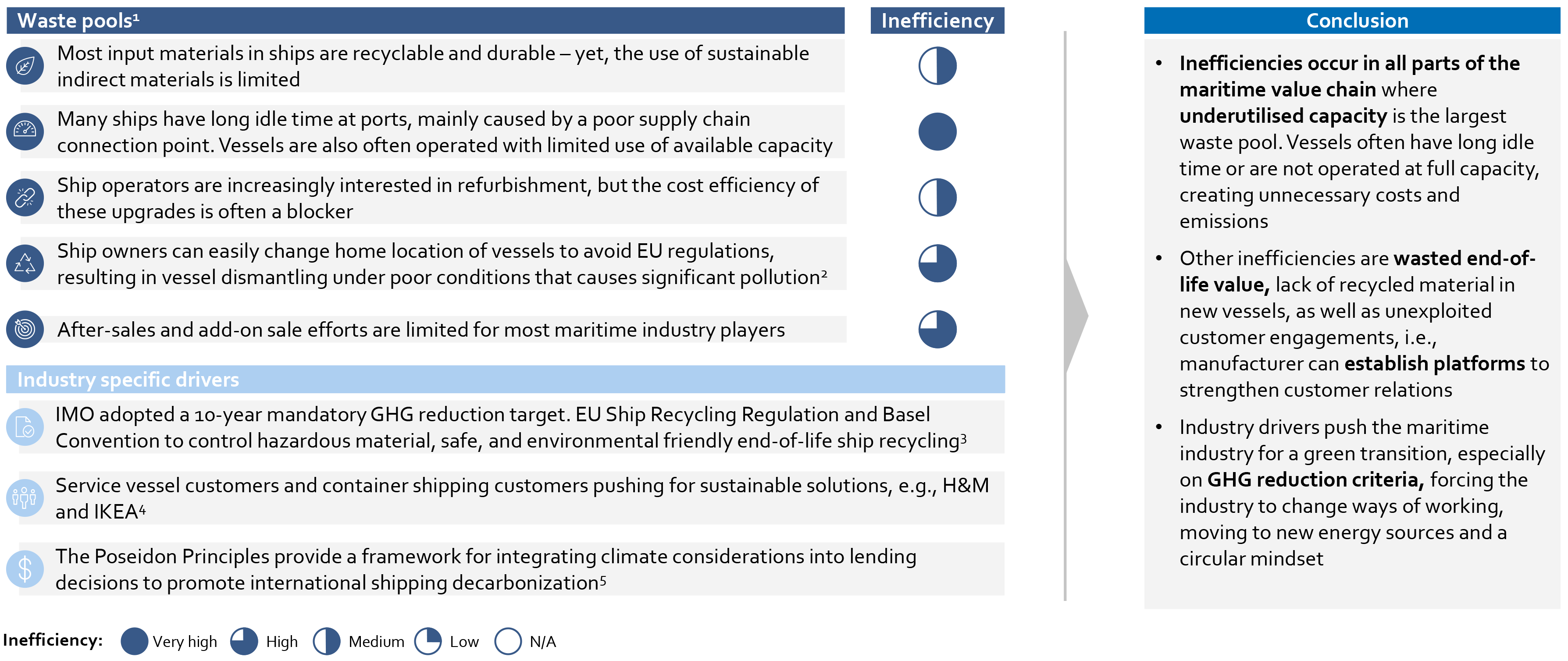

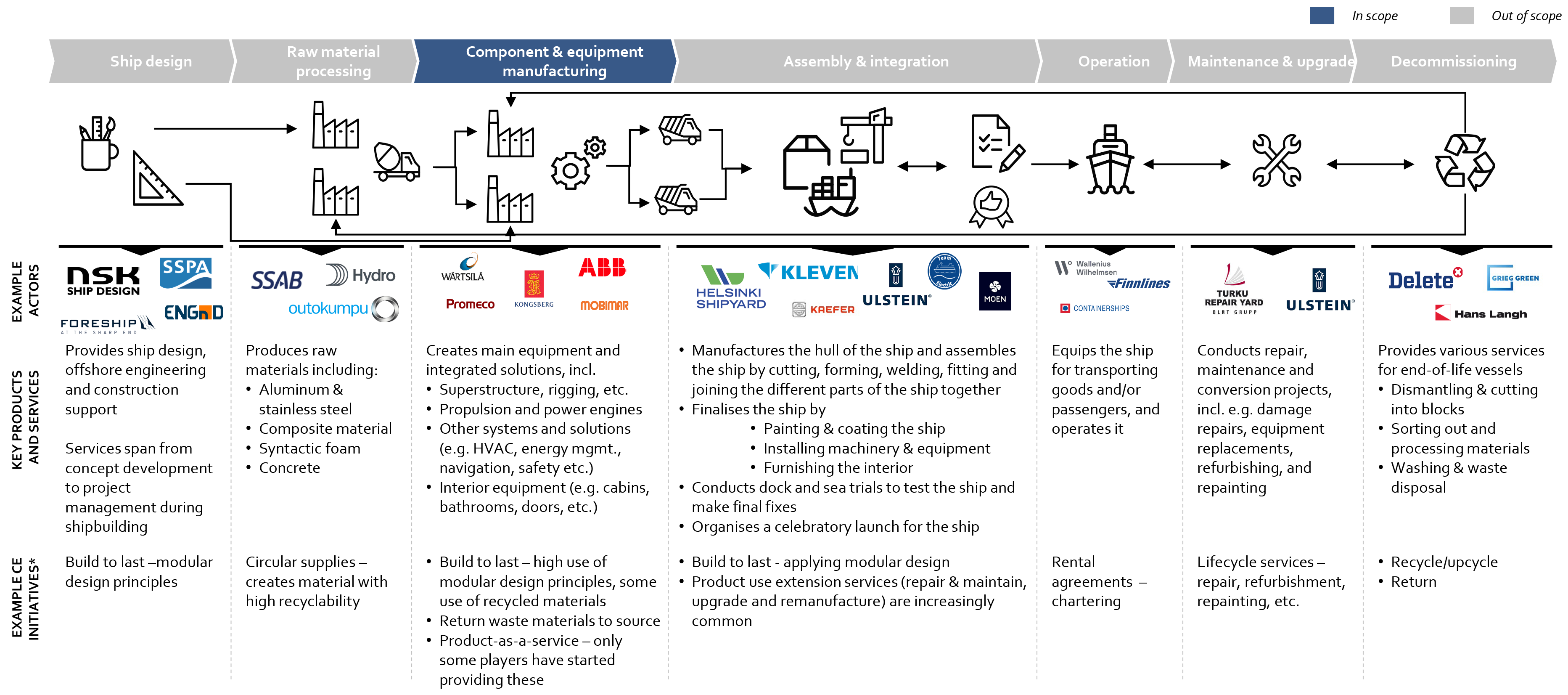

Inefficiencies occur in all parts of the maritime value chain and industry drivers push for greener solutions during the lifecycle

Key opportunities: Maritime (1/3)

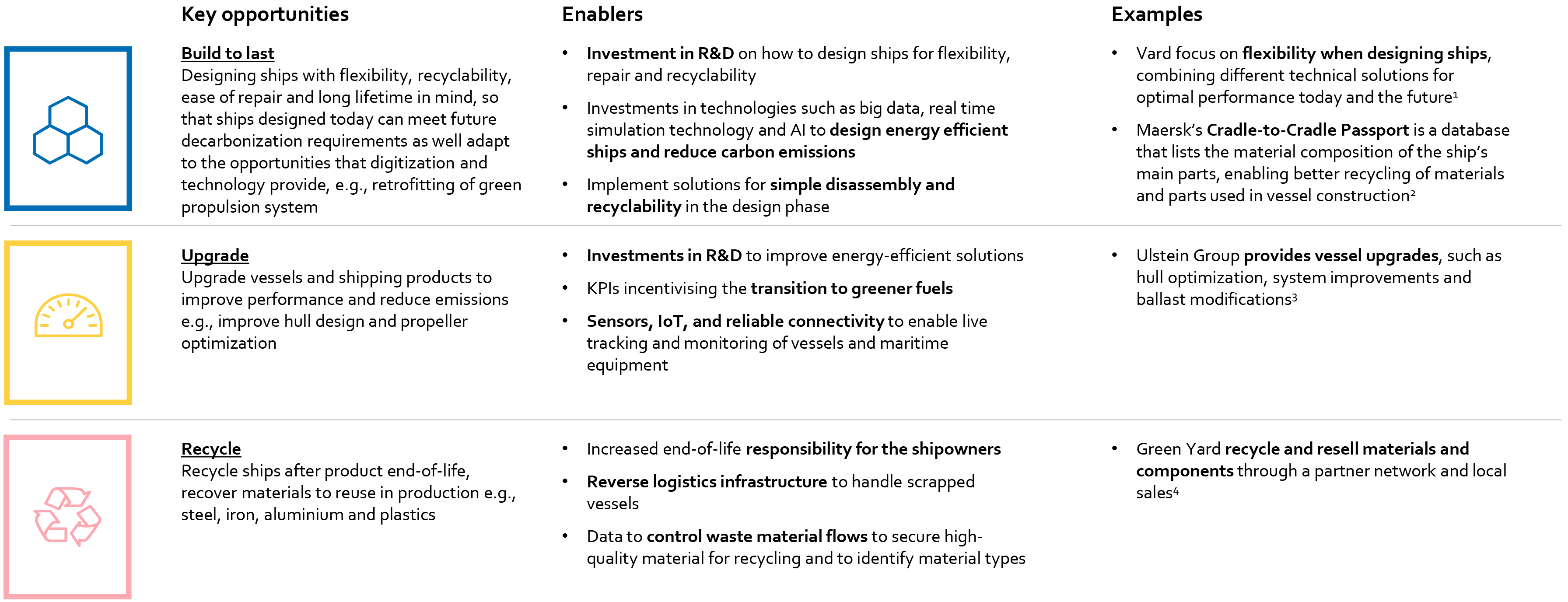

Repair and upgrade vessels and equipment to improve performance and extend product usage are big industry opportunities

Key opportunities: Maritime (2/3)

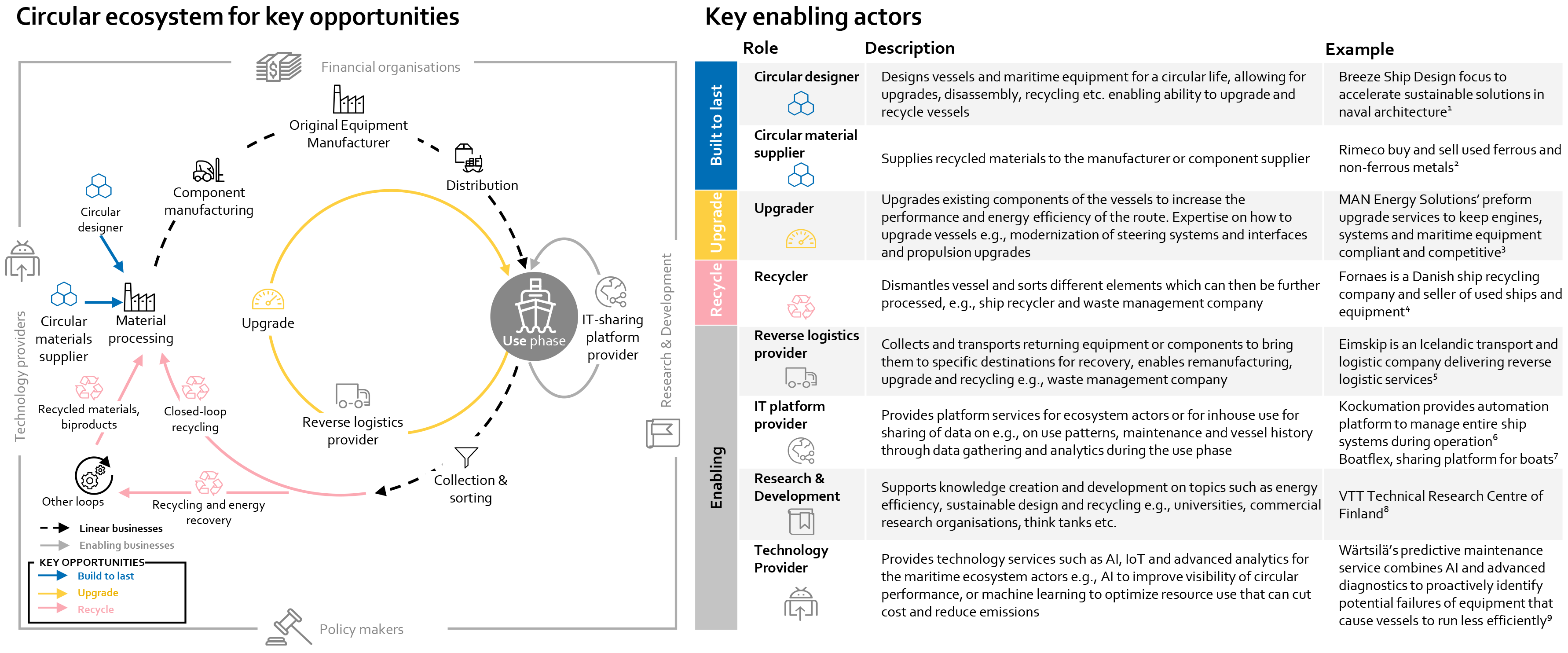

To unlock key opportunities in the industry, ecosystem actors need to know their role and together collaborate across the value chain

Key opportunities: Maritime (3/3)

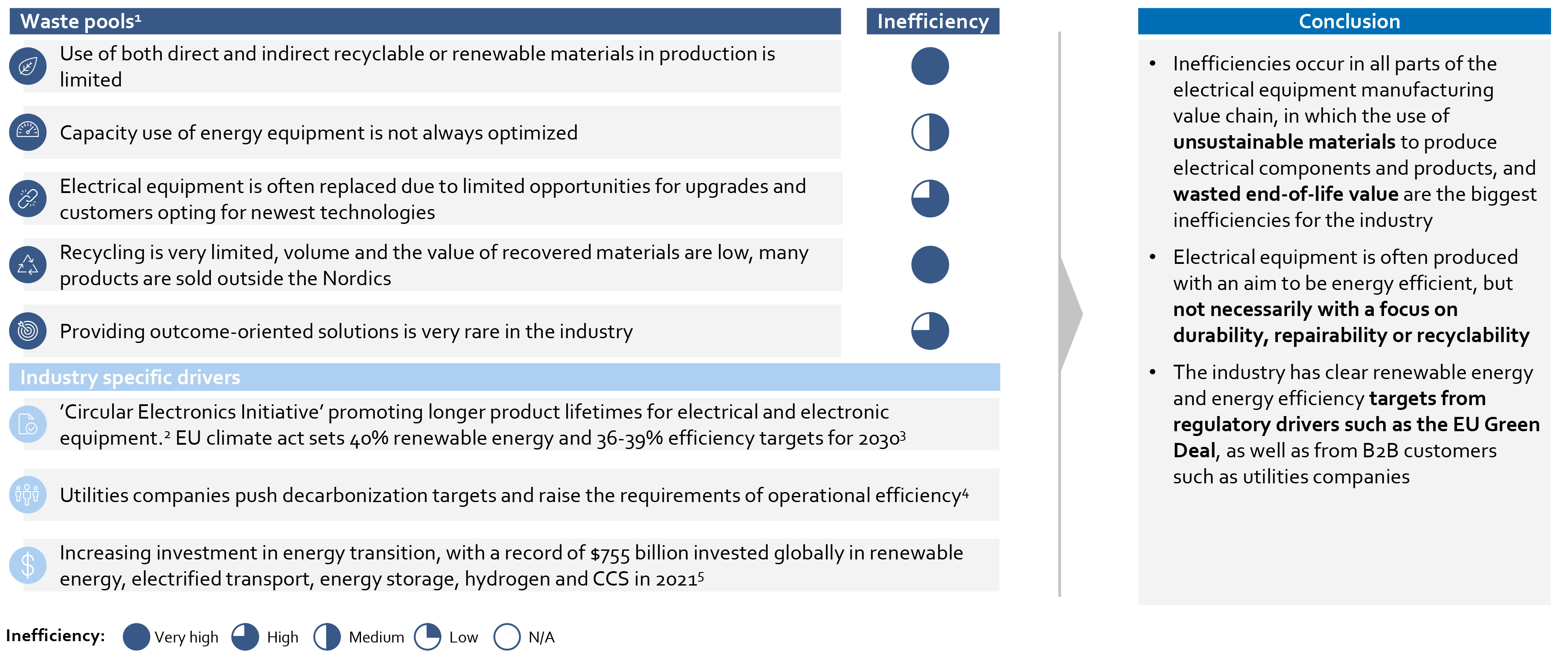

Unsustainable materials used in production and wasted end-of-life value are large inefficiencies in the industry

Key opportunities: Energy (1/3)

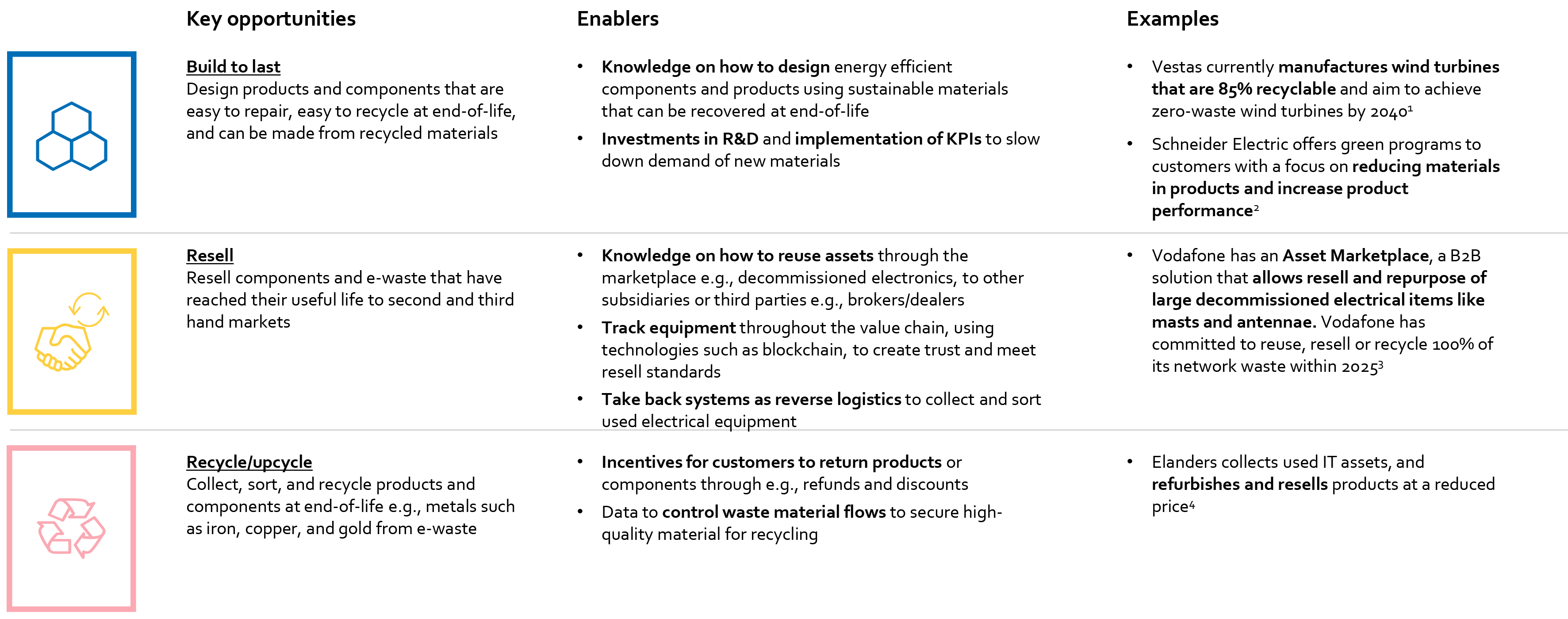

Design for easier disassembly, platform to resell, and recycling of equipment are key opportunities

Key opportunities: Energy (2/3)

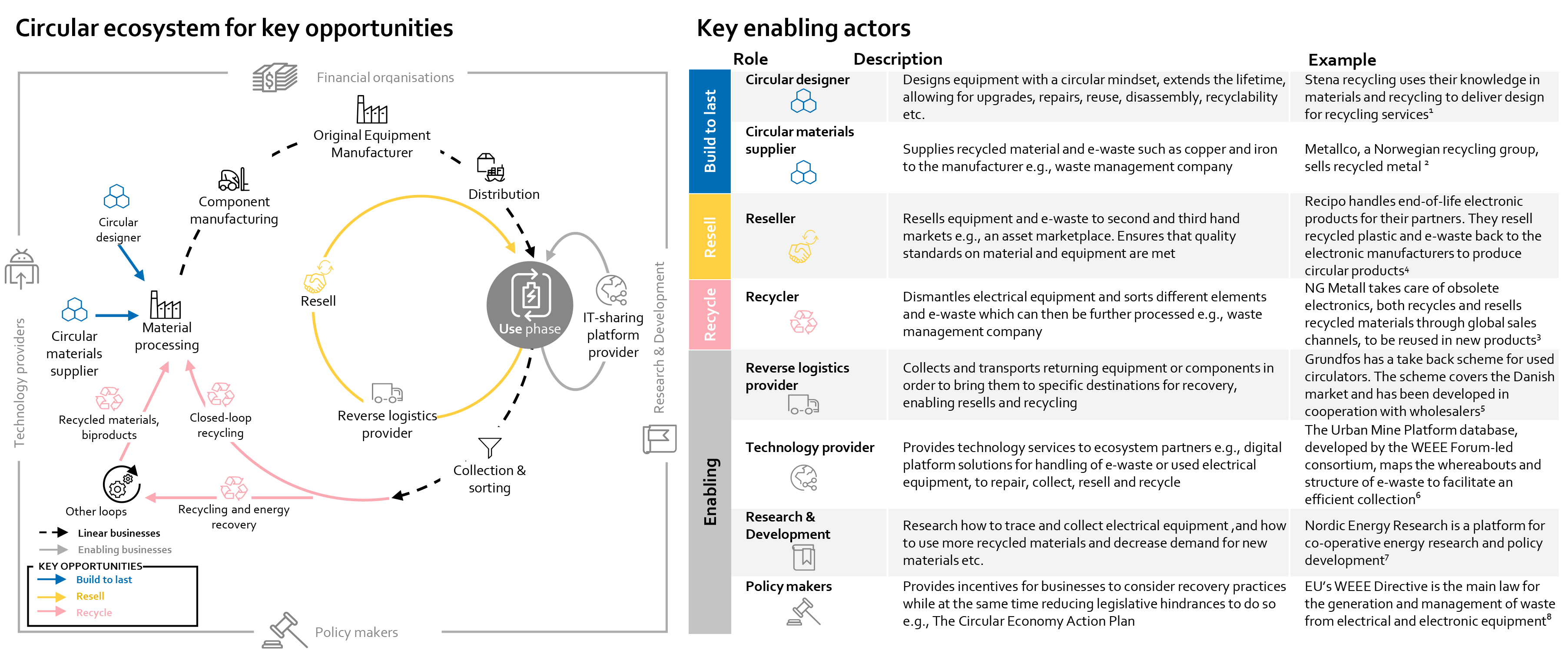

To unlock key opportunities in the industry, ecosystem actors need to know their role and together collaborate across the value chain

Key opportunities: Energy (3/3)

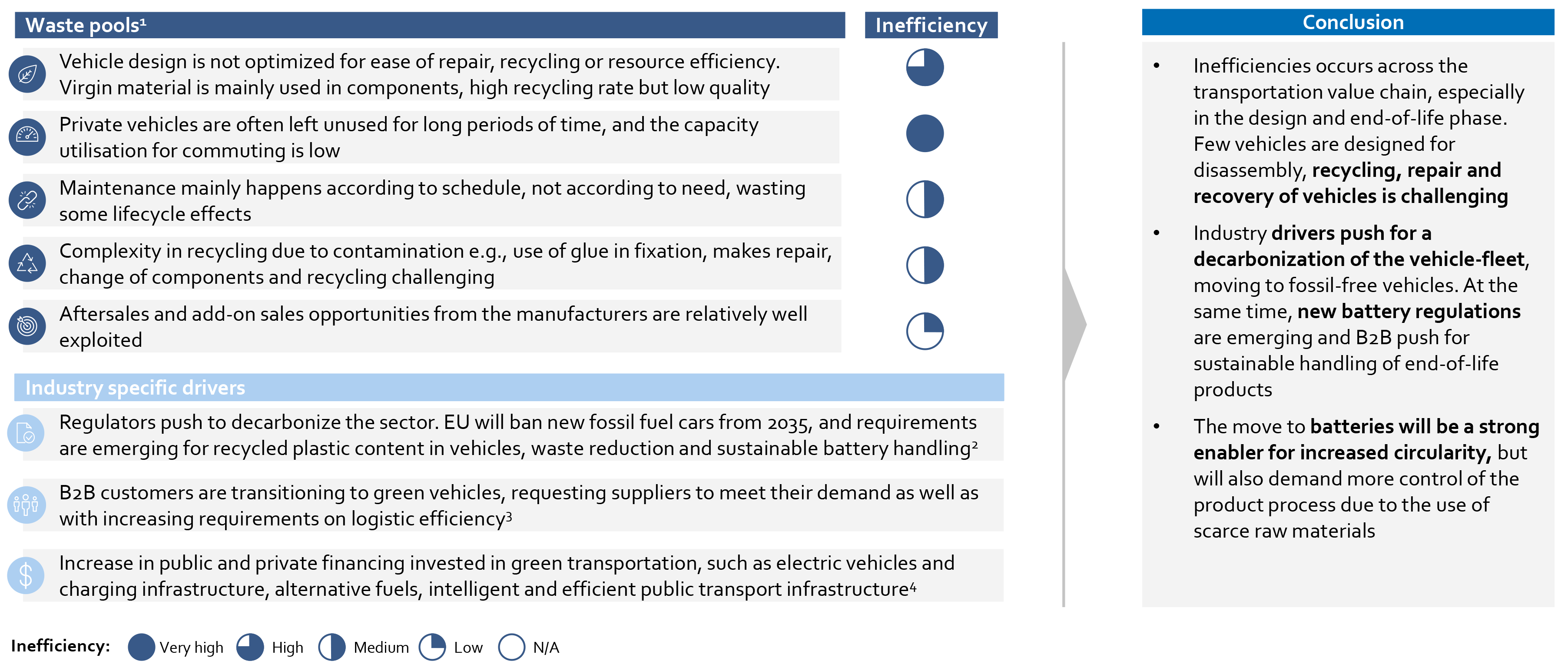

Inefficiencies occur especially in the design and end-of-life phase, drivers push for greener solutions and for phase out of fossil fuels

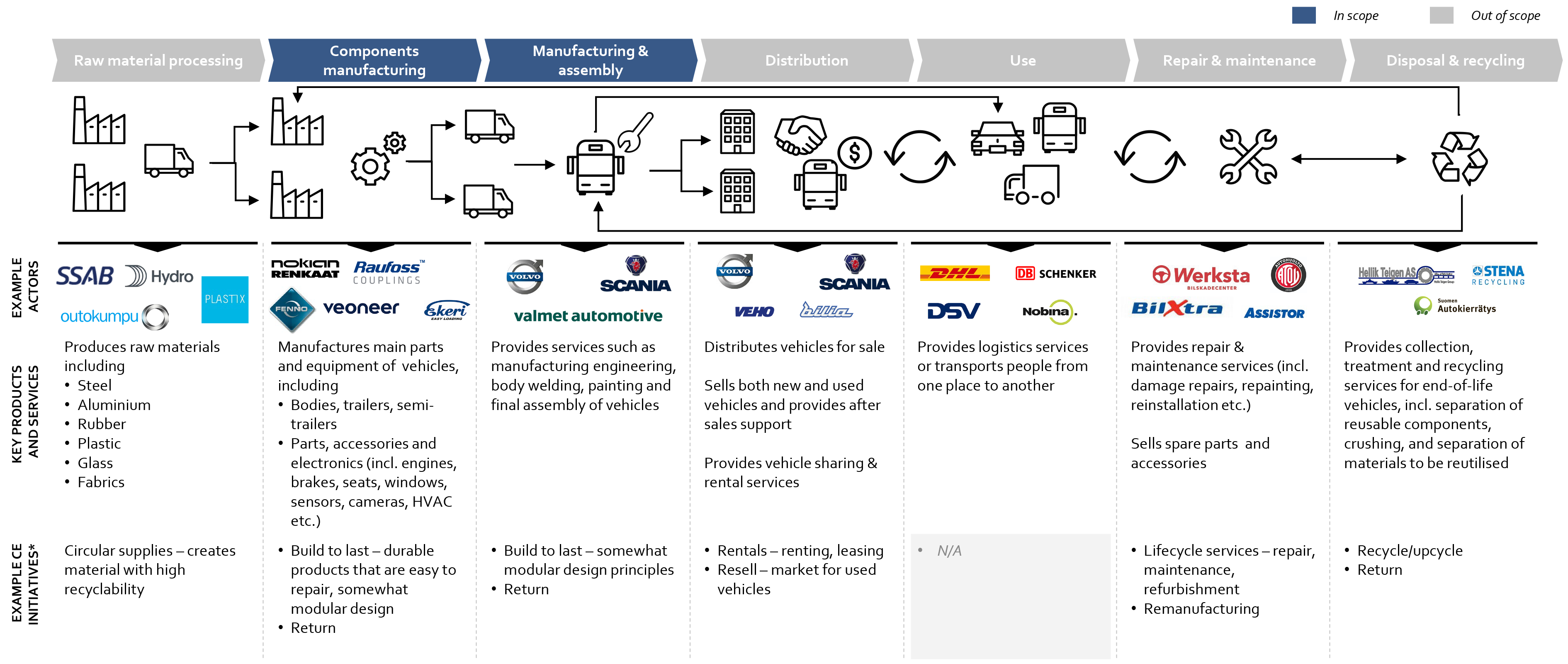

Key opportunities: Transportation (1/3)

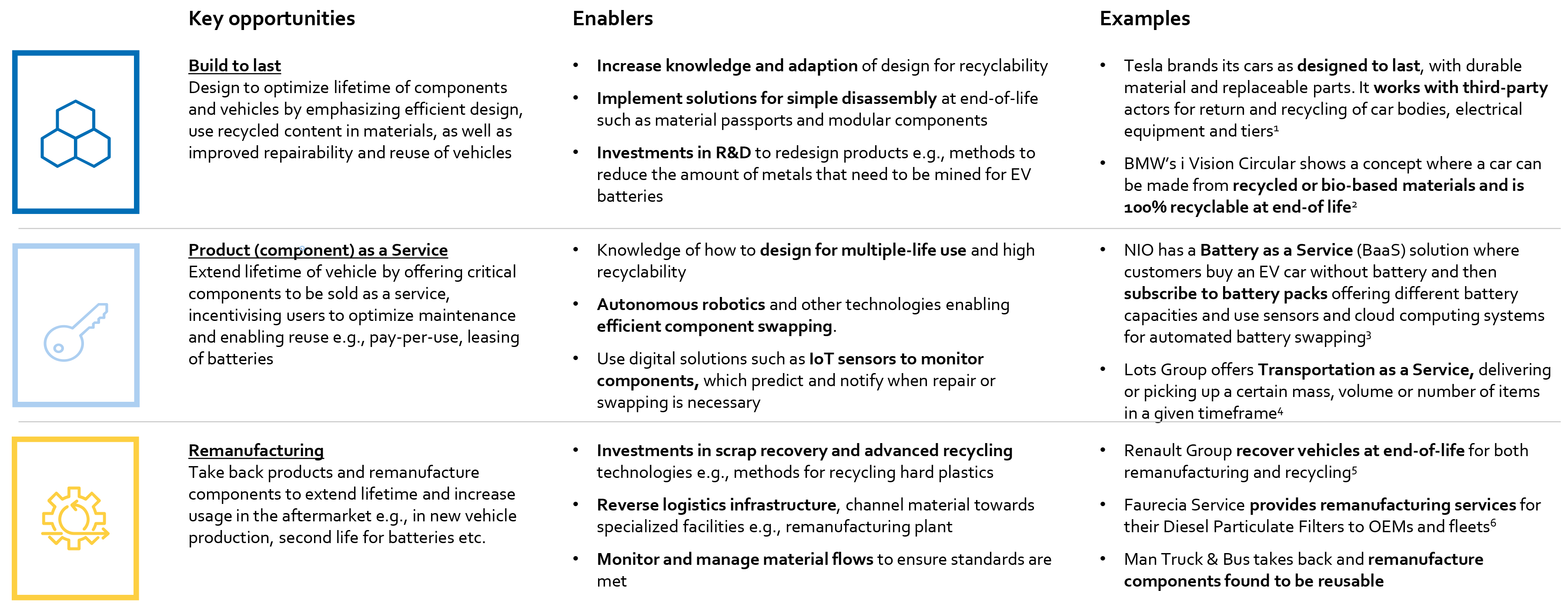

Build to last, repair and maintain, and remanufacturing of vehicles are key opportunities for the industry

Key opportunities: Transportation (2/3)

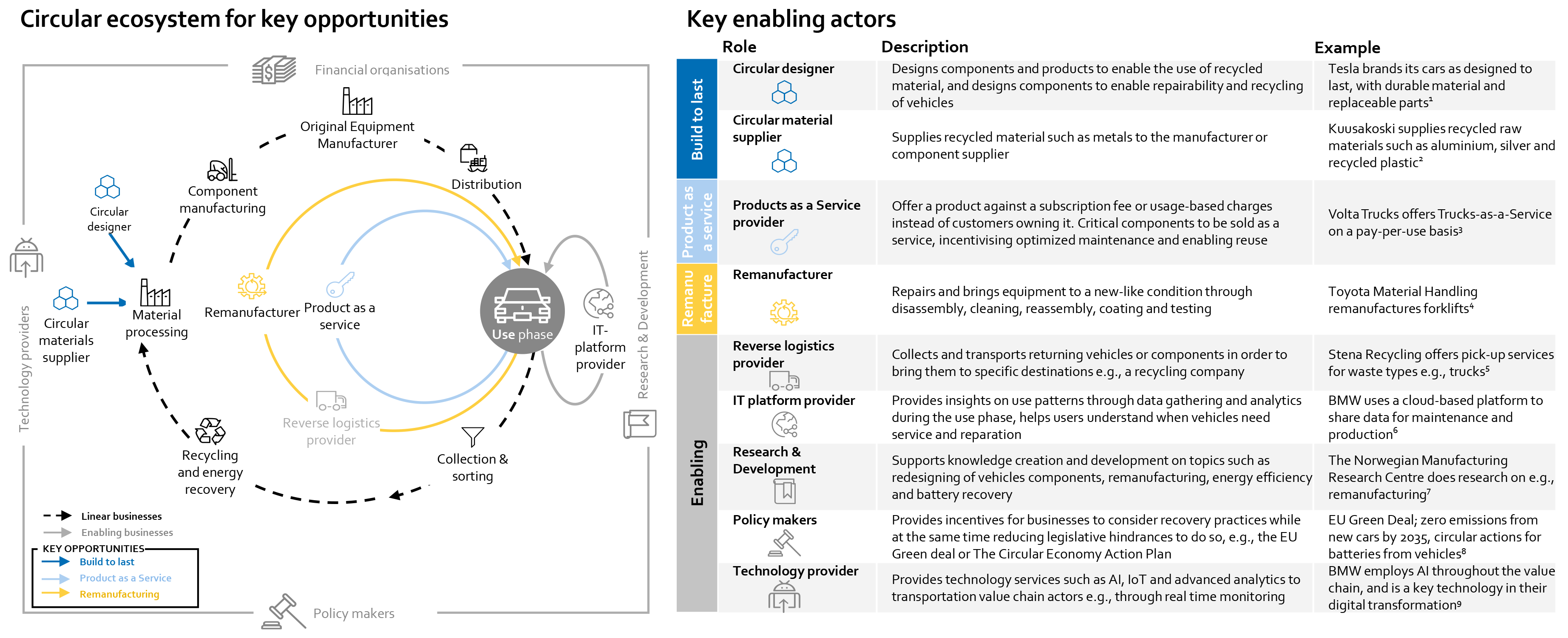

To unlock key opportunities in the industry, ecosystem actors need to know their role and together collaborate across the value chain

Key opportunities: Transportation (3/3)

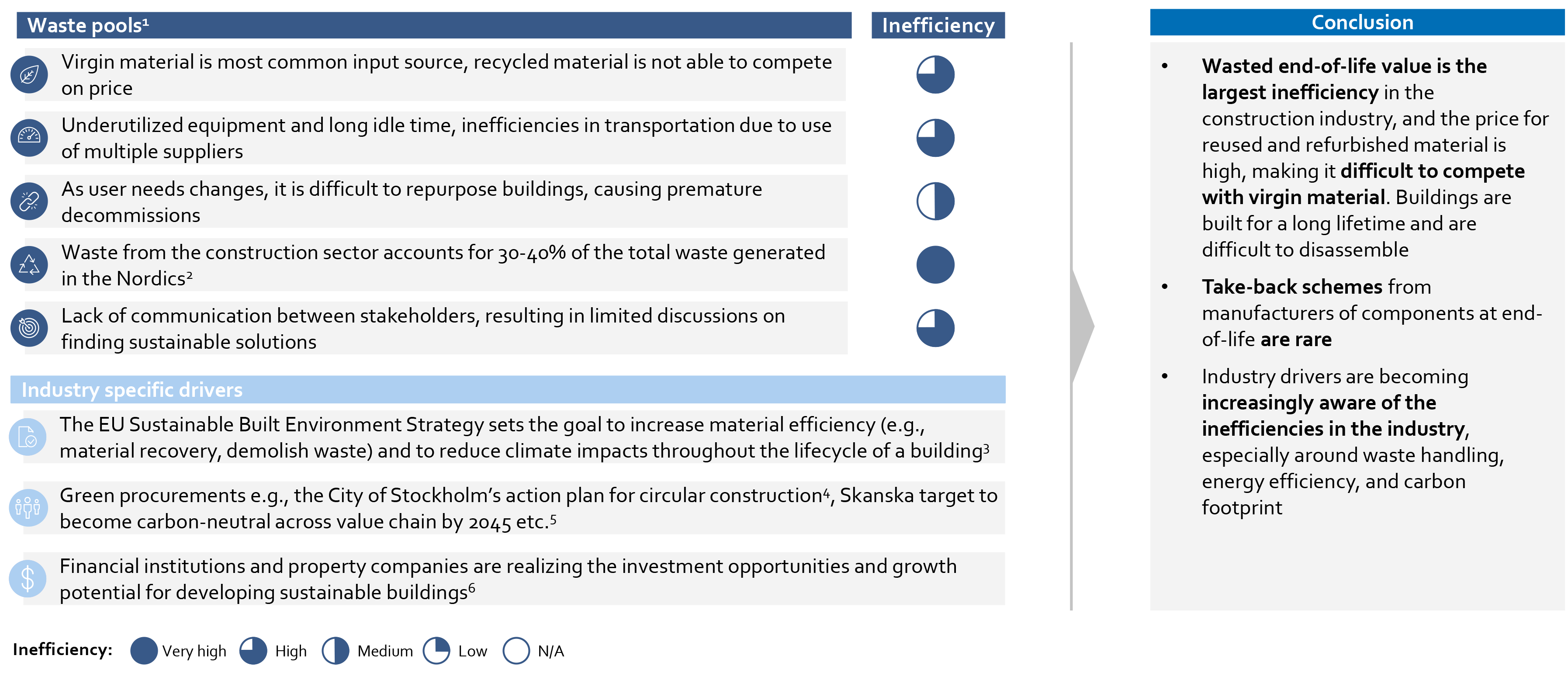

Wasted end-of-life value is the largest waste pool, drivers pressure the industry for better waste handling and energy efficiency

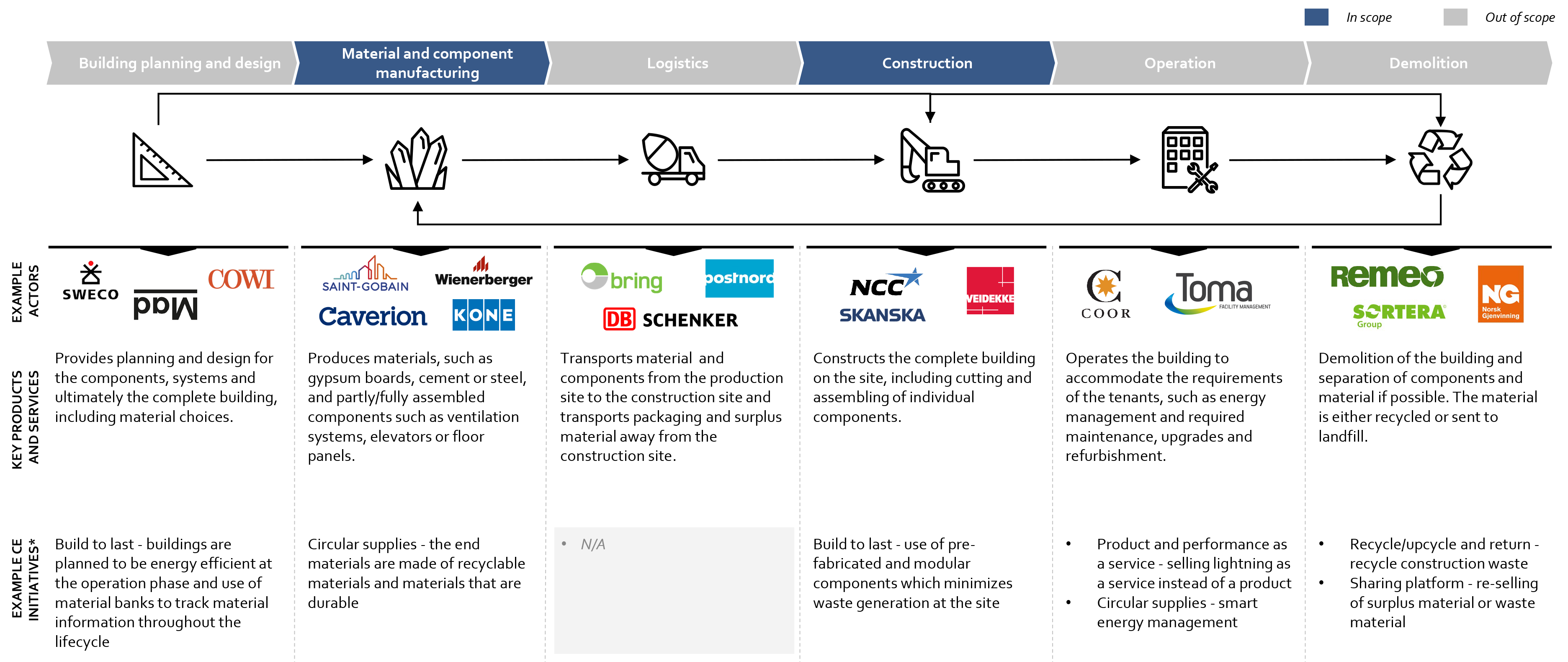

Key opportunities: Construction (1/3)

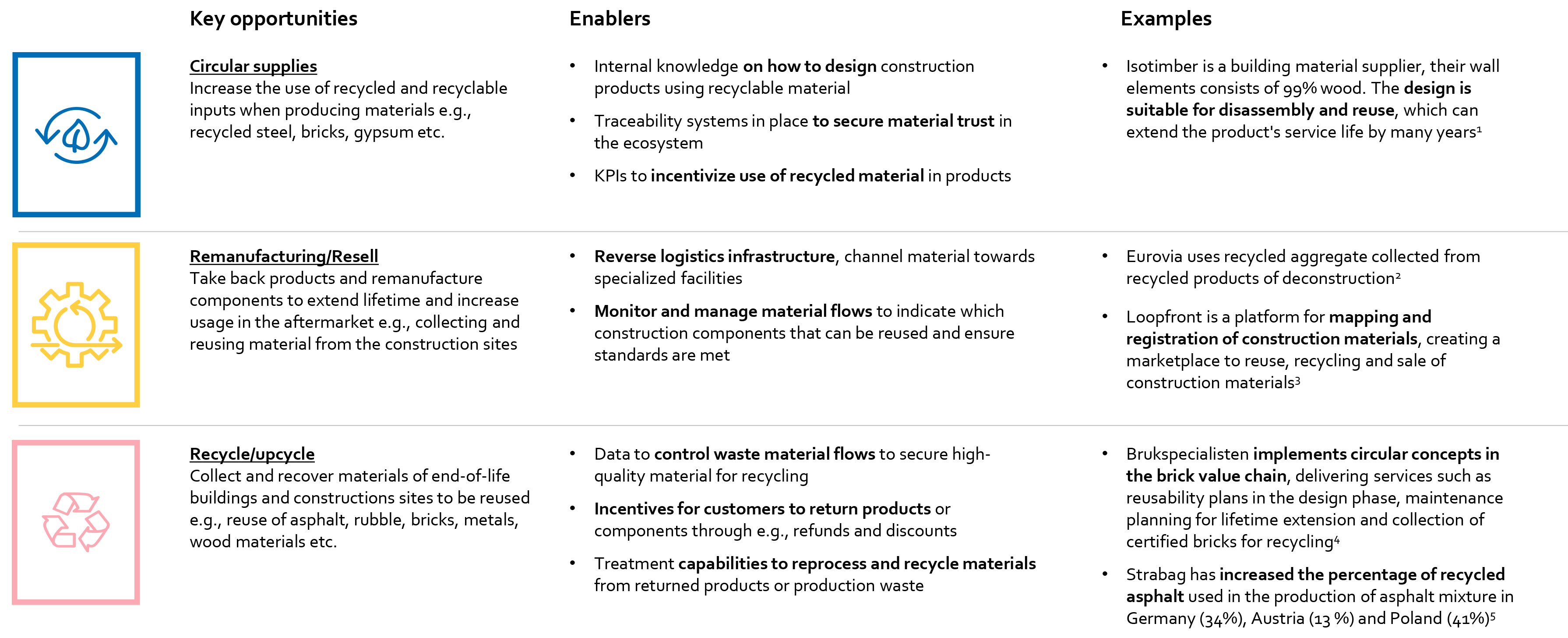

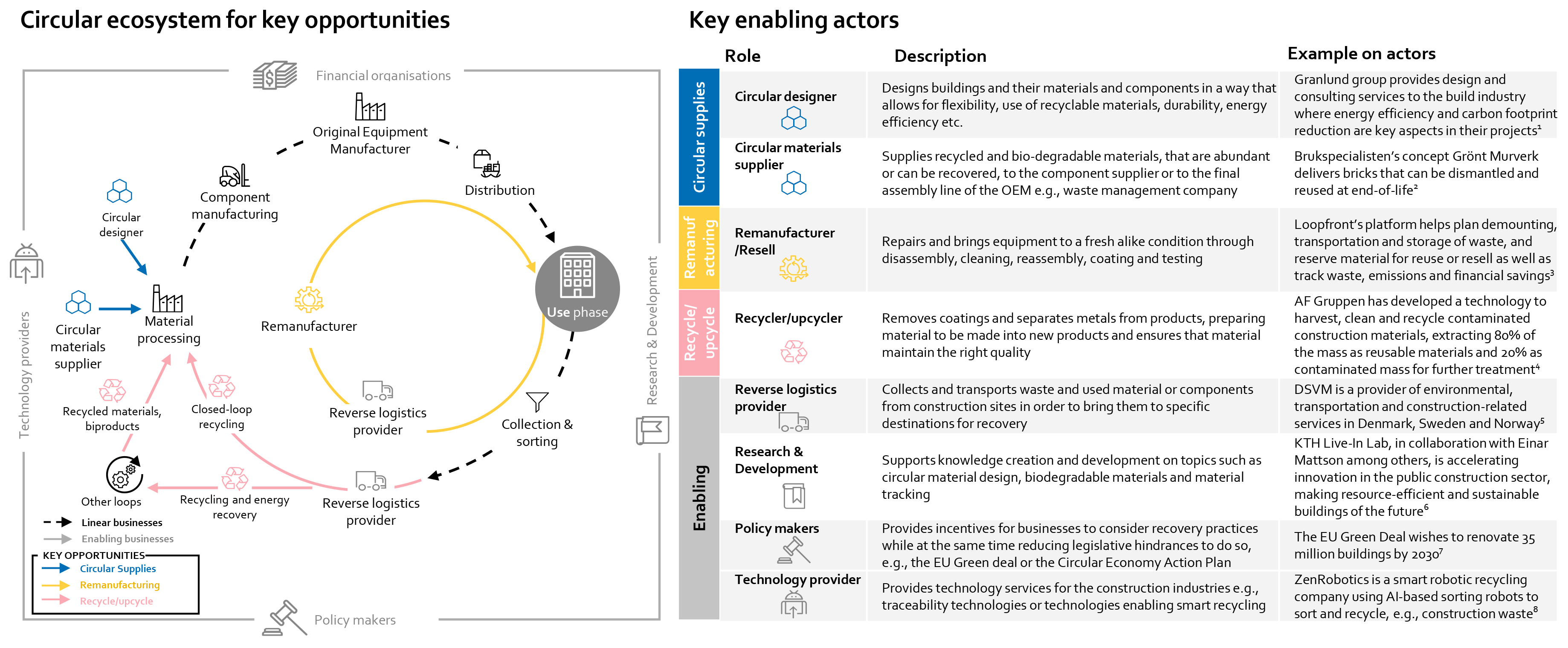

Recycled input material, reuse and resell schemes for waste, and material handling are circular opportunities for the industry

Key opportunities: Construction (2/3)

To unlock key opportunities in the industry, ecosystem actors need to know their role and collaborate across the value chain

Key opportunities: Construction (3/3)

3

Consisting gaps

CHAPTER SUMMARY: Consisting gaps

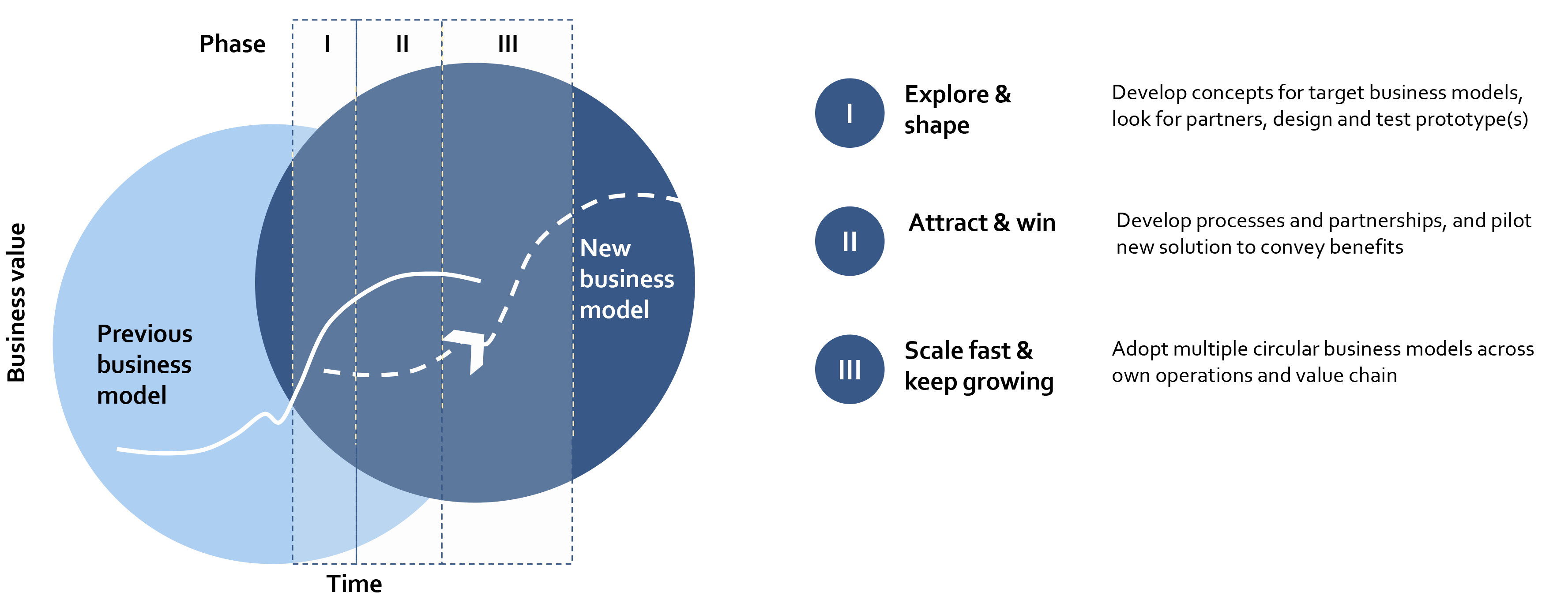

The transformation journey required to leverage the circular advantage typically takes companies through three different stages

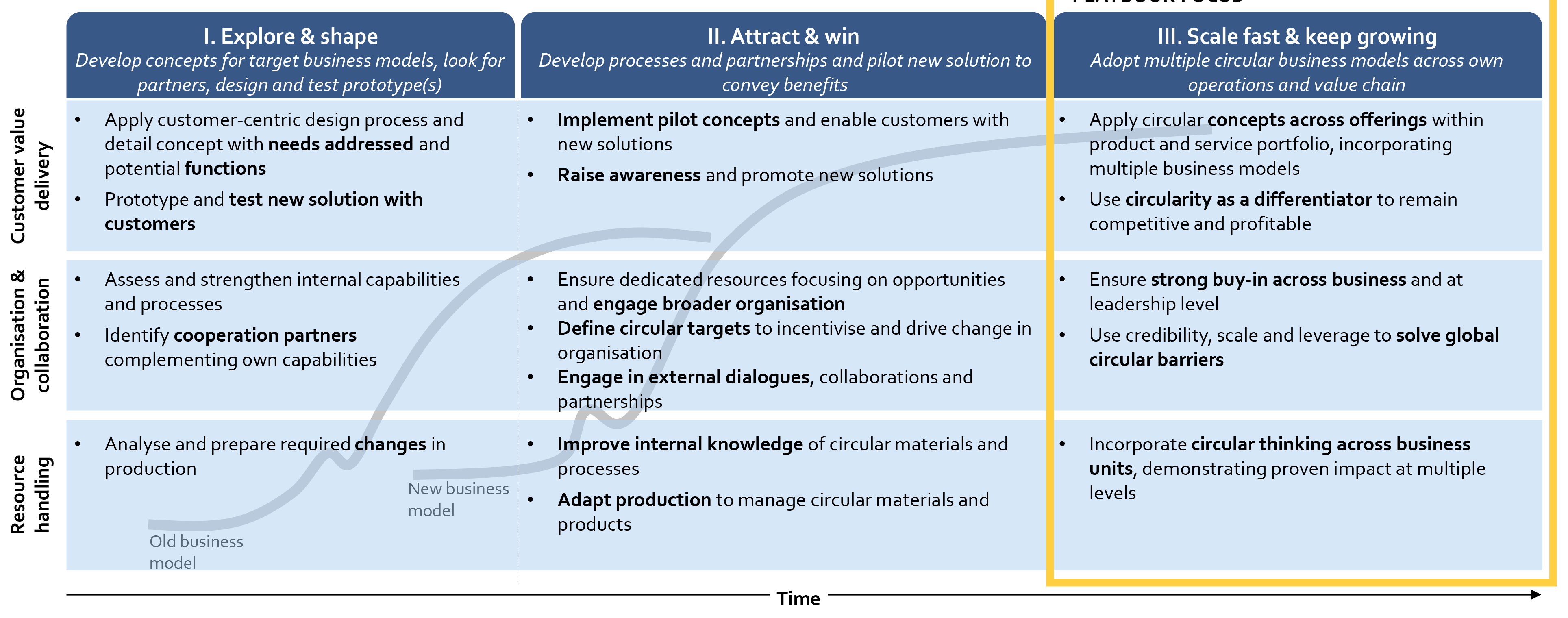

They first “Explore & shape” to develop concepts for target business models, look for partners, design and test prototypes. They then “Attract & win”, as they develop required processes and partnerships and pilot new solutions. Finally, they “Scale fast & keep growing” by adopting multiple circular business models across their operation

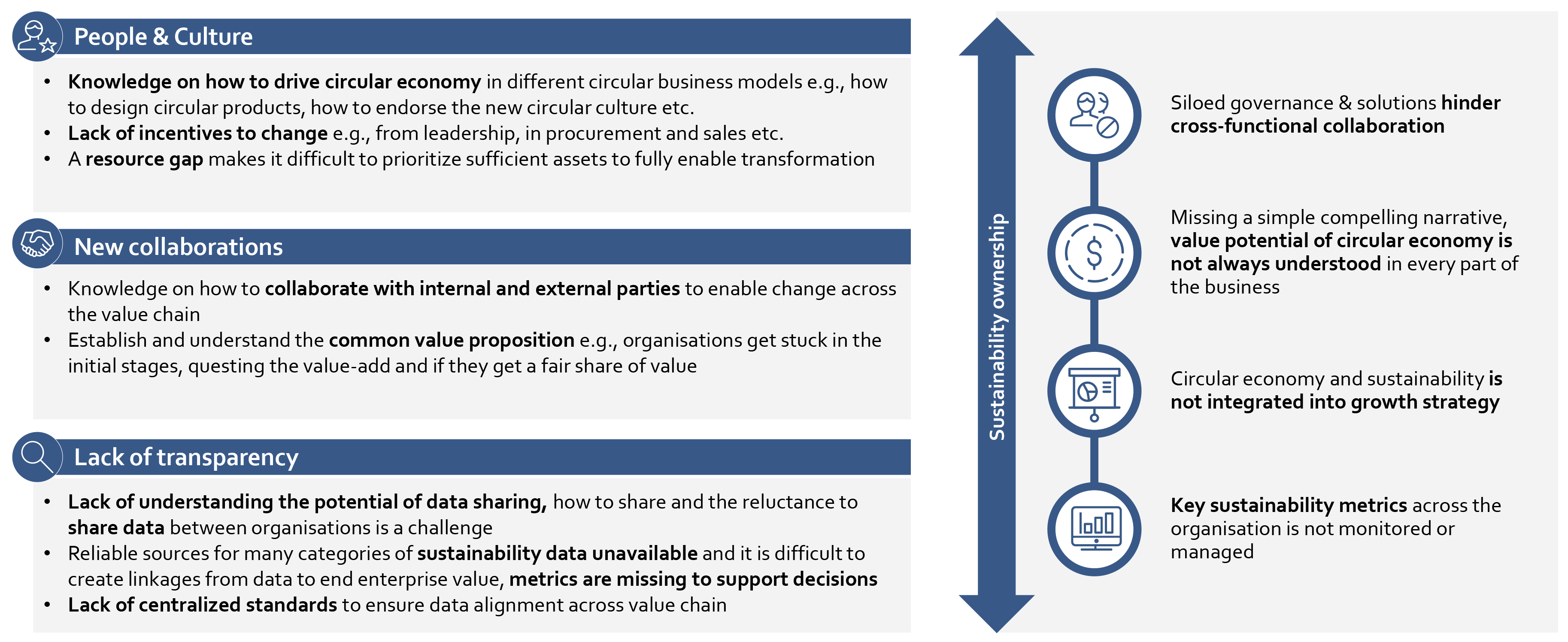

Most companies struggle to transform and scale and have not made it through pilot stage. Main challenges are typically related to (a) people & culture, (b) new collaborations, (c) lack of transparency and (d) sustainability organisation ownership

This chapter will help you to:

- Learn the importance of shifting to a customer-value delivery focus in the organisation, to adopt circular business models across own operations and value chain

- Understand the challenges that companies are facing when transforming and scaling new business models related to organisation, ecosystemand data

Additional material that can be found in the Nordic Circular Economy Playbook:

- Nine capabilities that can enable companies to increase circularity in the organisation

- Assess capability gaps and identify actions to bridge them as well as identify potential technology partners and suppliers

- Understand the key steps, common barriers and success factors for the stages “Explore & shape” and “Attract & win”

- Supporting tools: Culture gap analysis and funding requirements analysis

The transition from the previous to the new business model is gradual and has three phases

Three phase transformation

In each phase, customer value delivery, collaboration and resource handling follow circular business logic

Scale fast and keep growing

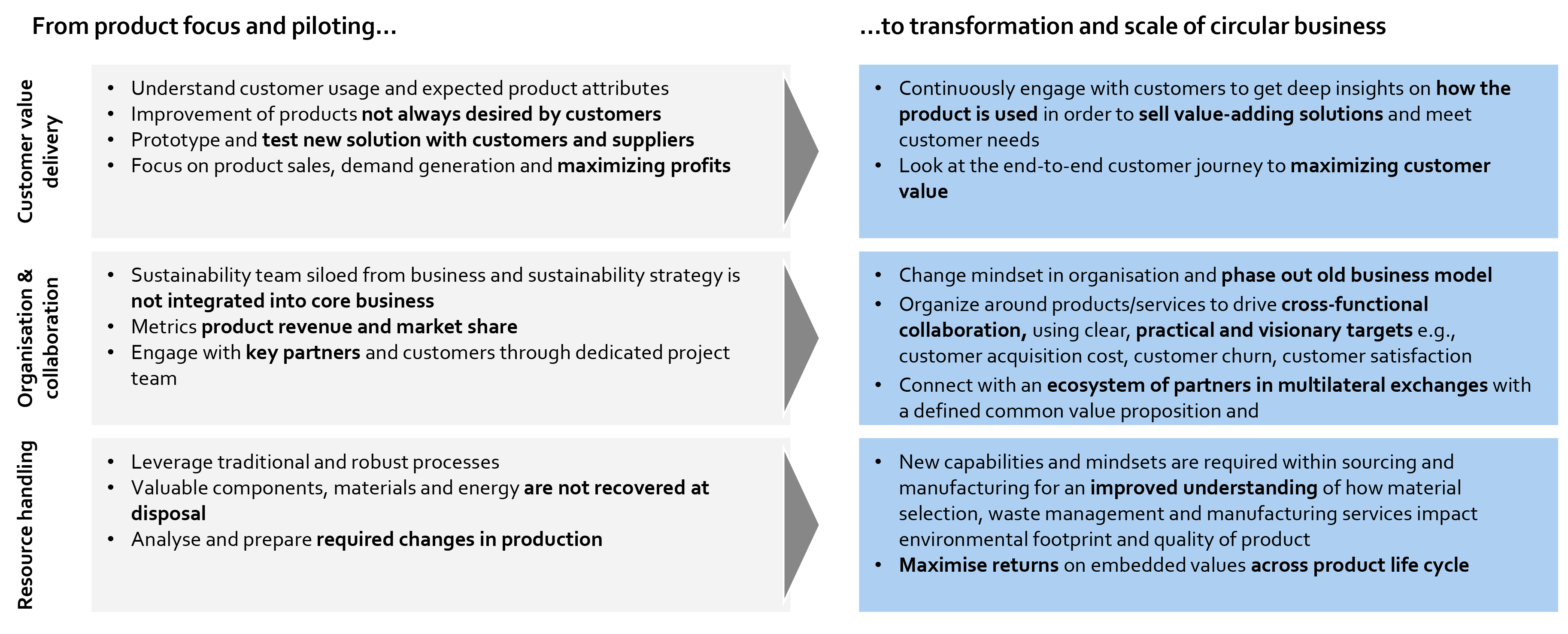

Transforming to a circular business requires different capabilities and a focus on the end-to-end customer journey

Organisational change

Understanding the importance of people & culture, new collaborations and transparency are key to achieve full transformation and scale

Main challenges

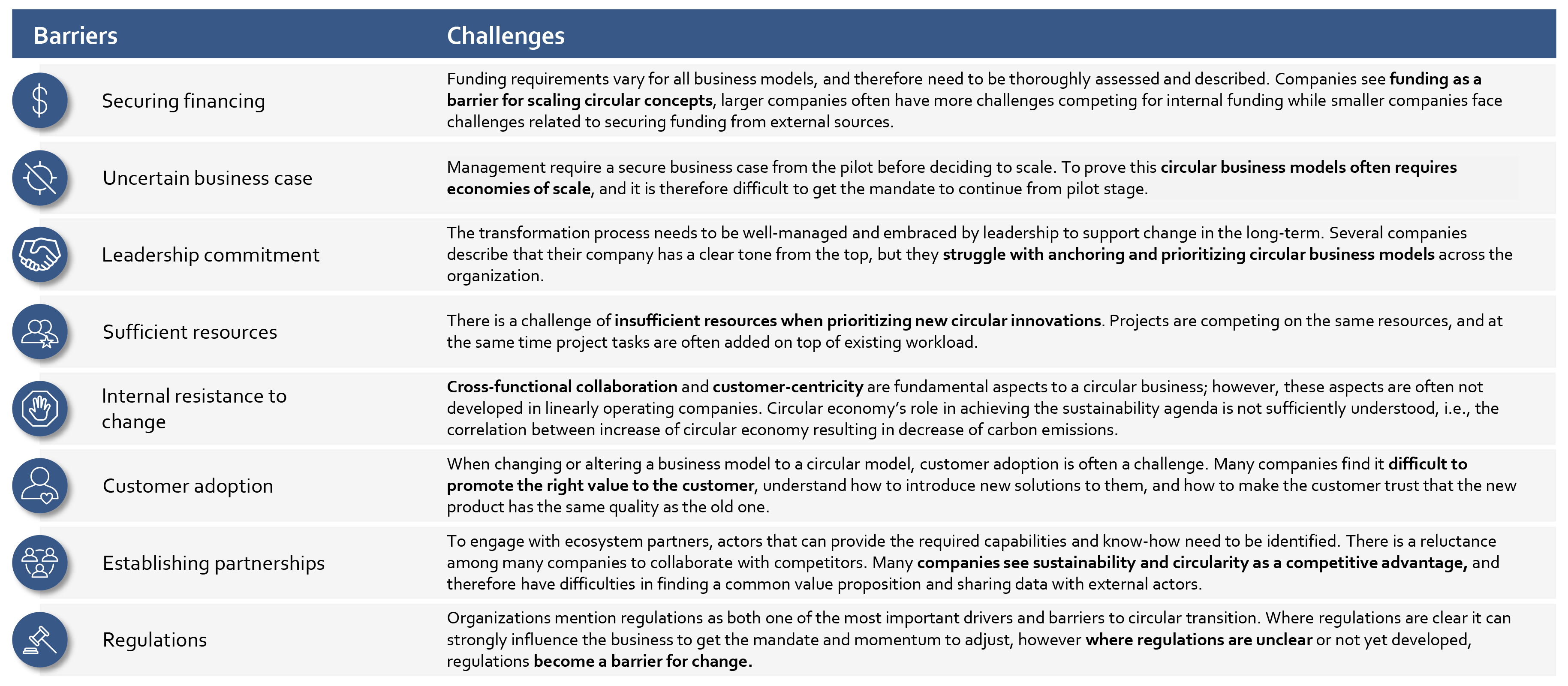

Companies face several barriers during their circular transformation journey

Output from Nordic Circular Industries workshops

4

Transformation & Scale

CHAPTER SUMMARY: Transformation & Scale

-

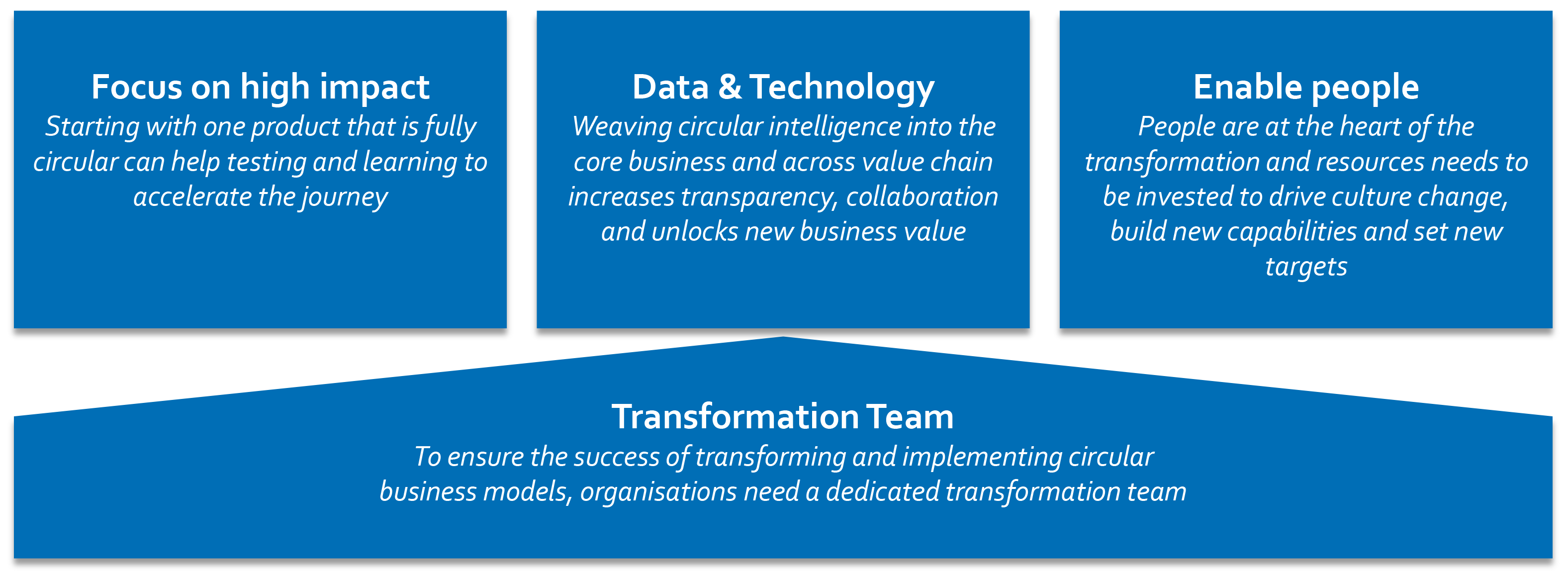

For companies to fully transform and become circular businesses, enablers are typically related to four elements:

(a) focus on high impact, starting with making one product fully circular to test and learn, (b) use data & technology to lever and unlock business value, (c) enable people to drive culture change and build capabilities, and (d) ensure the success of implementing circular business models by having a dedicated transformation team

This chapter will help you to:

- Understand enablers that can help companies successfully overcome barriers, transform and become circular businesses

Additional material that can be found in the Nordic Circular Economy Playbook:

- Identify actions to be implemented in terms of culture, ecosystem partners and financing, to avoid typical pitfalls

- Learn how to design a transformation roadmap with concrete next steps, responsibilities and milestones

- Supporting tools: Roadmap development tool

To overcome barriers, four enablers can help companies successfully transform

Investors

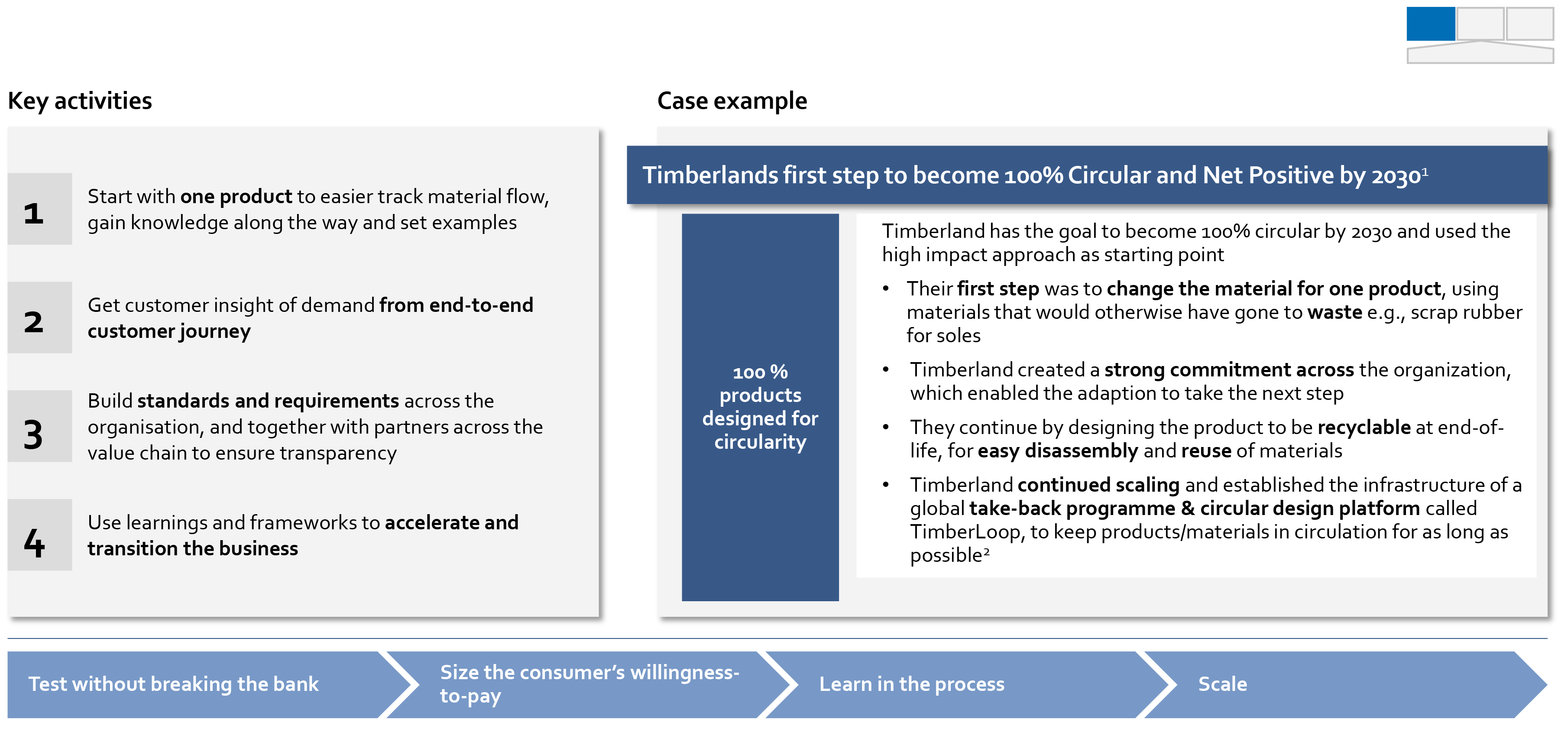

Starting with making one product fully circular can help test, learn and secure commitment to accelerate the transformation journey

Focus on high impact

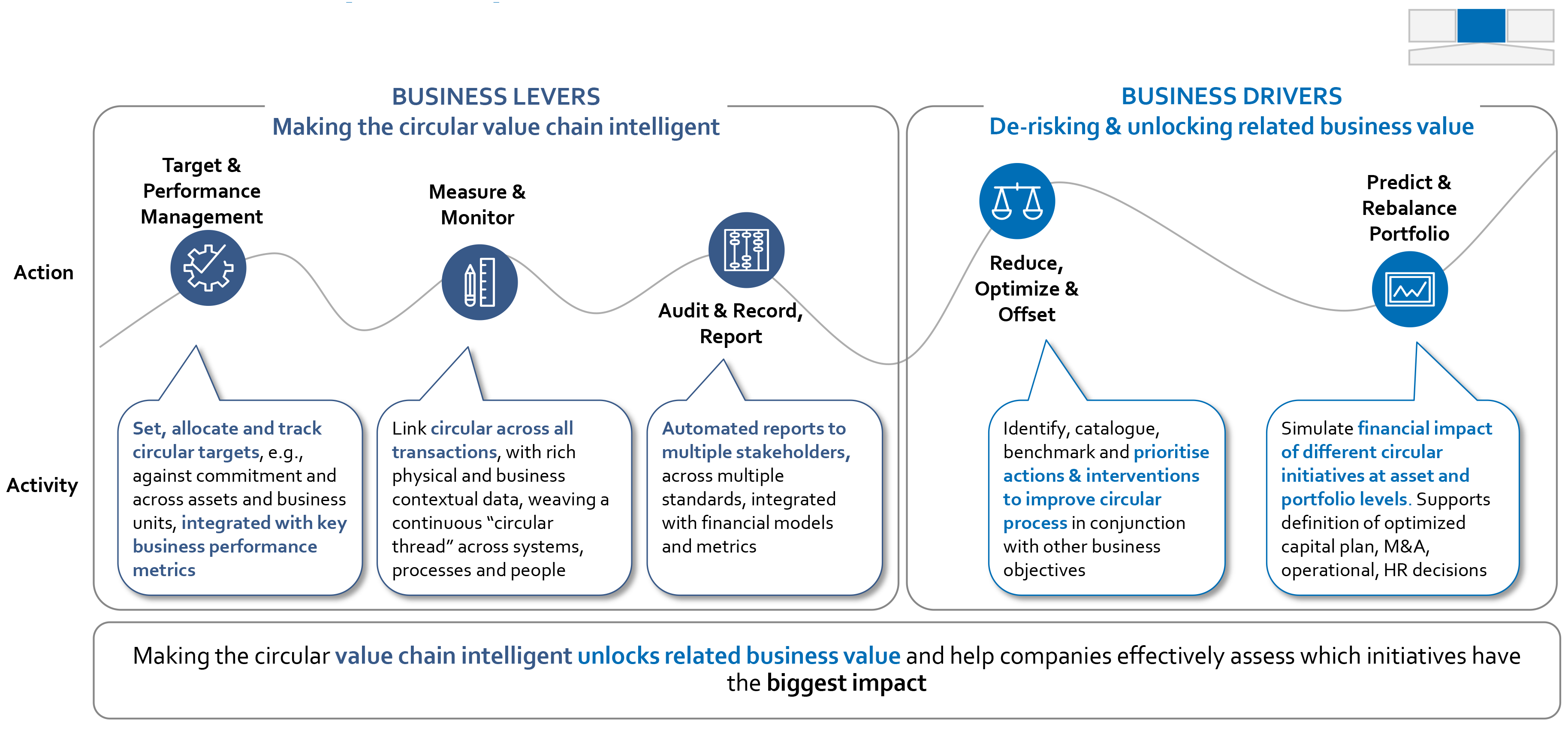

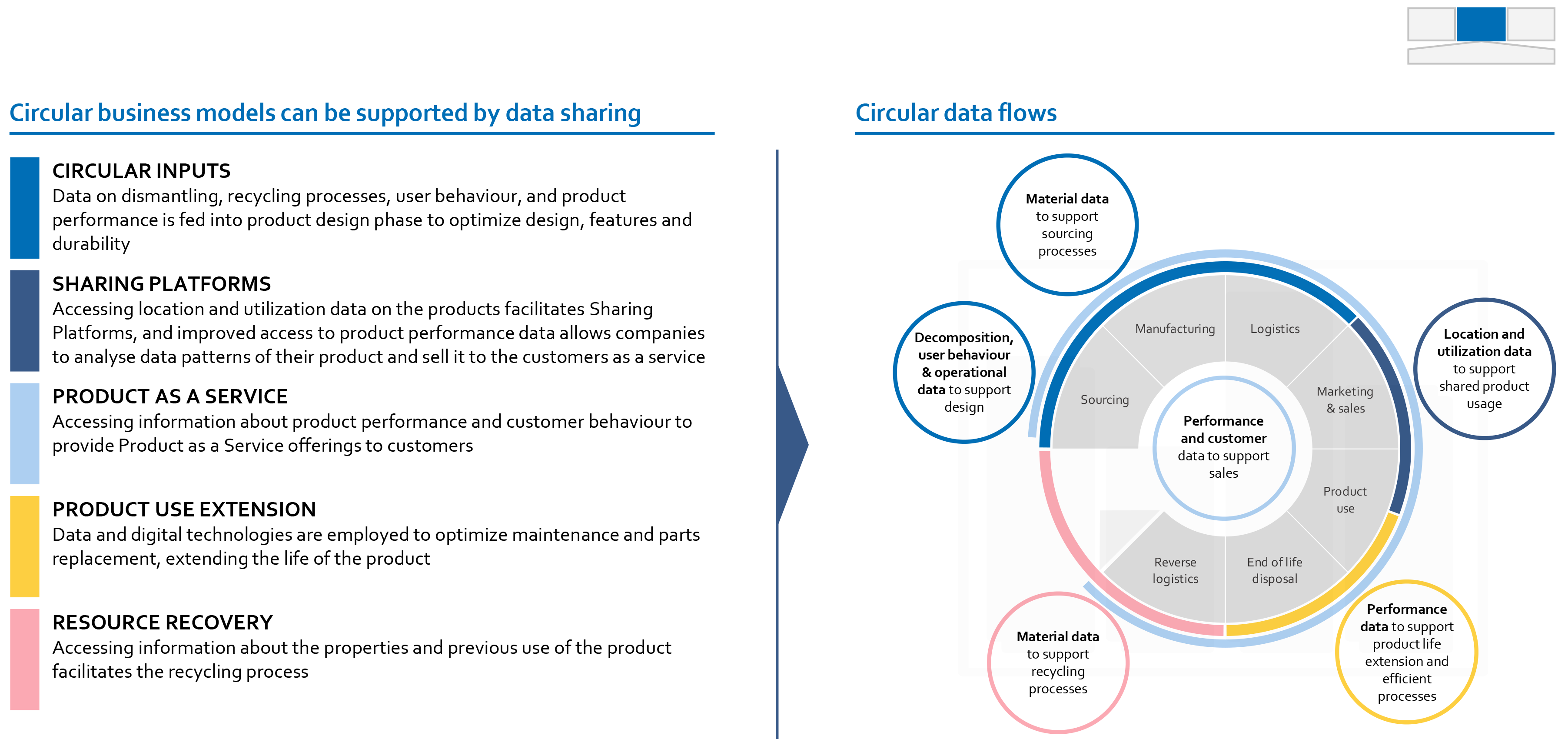

Weaving circular intelligence into core business and across value chain increases transparency, collaboration and unlocks new business value

Data & Technology

An increased flow of data across the value chain will accelerate the development of circular business models

Circular data flow

Enablers

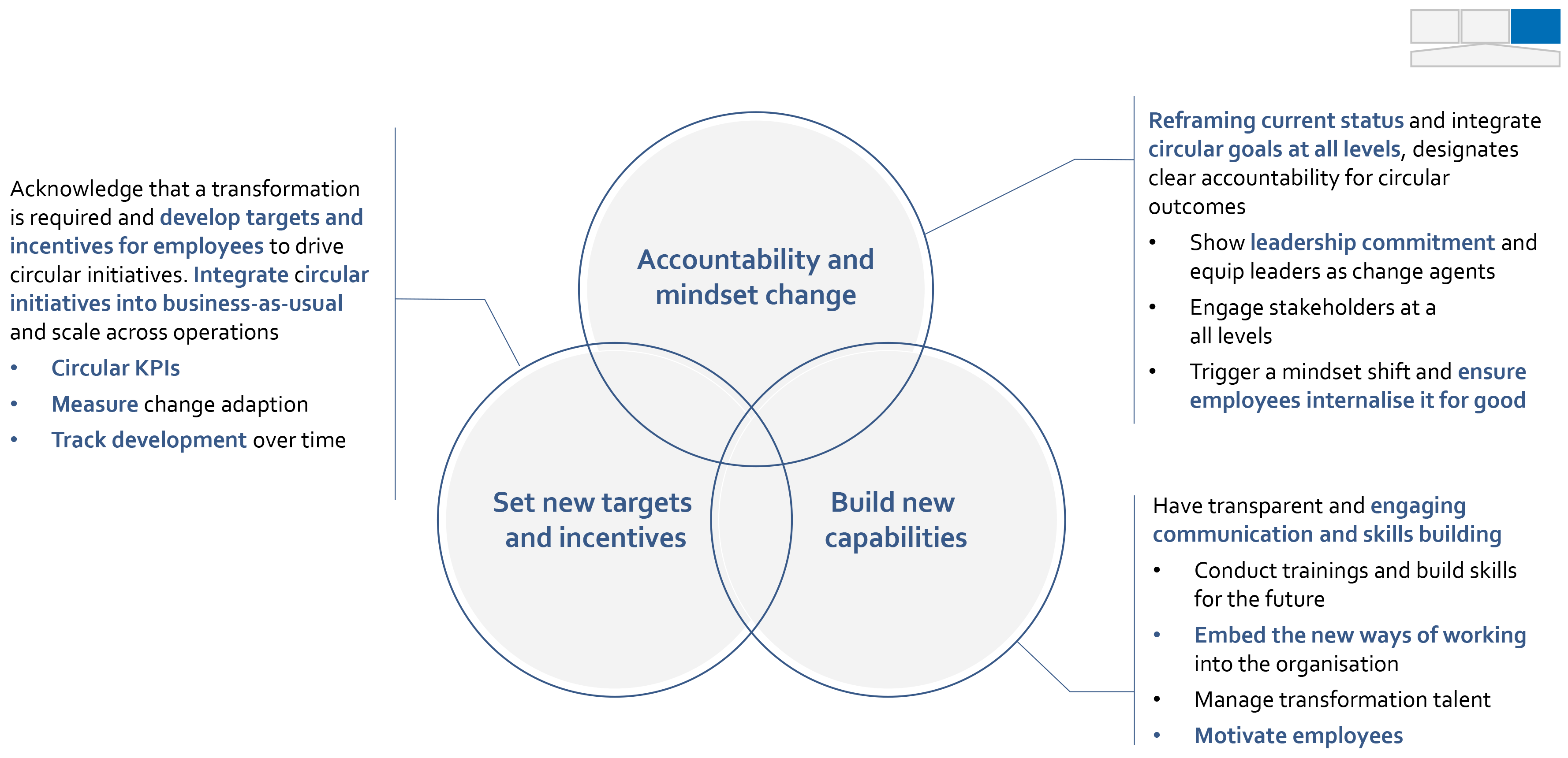

People are at the heart of the transformation and resources need to be invested to drive culture change, build new capabilities and set new targets

Enable people

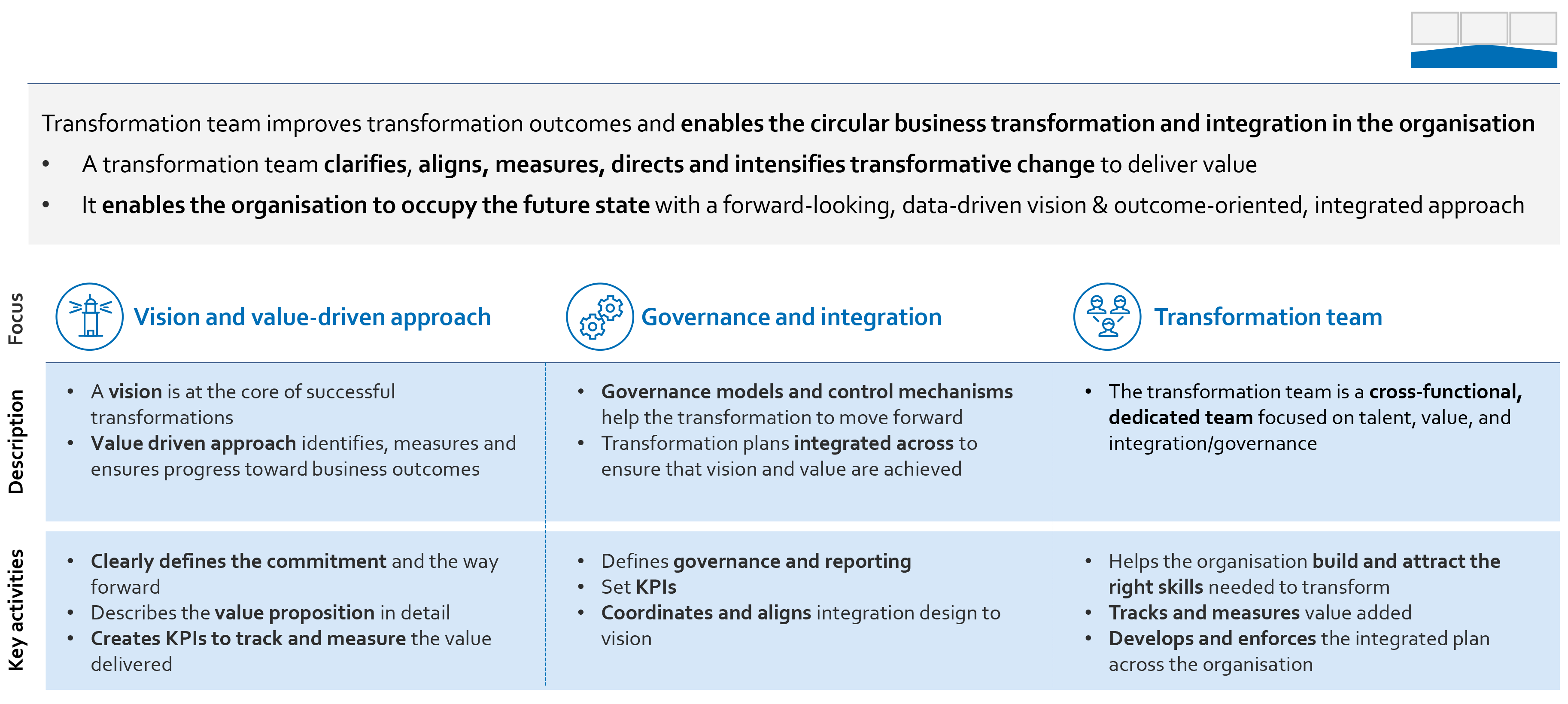

To ensure the success of transforming and implementing circular business models, organisations need a transformation team

Transformation Team

Appendix

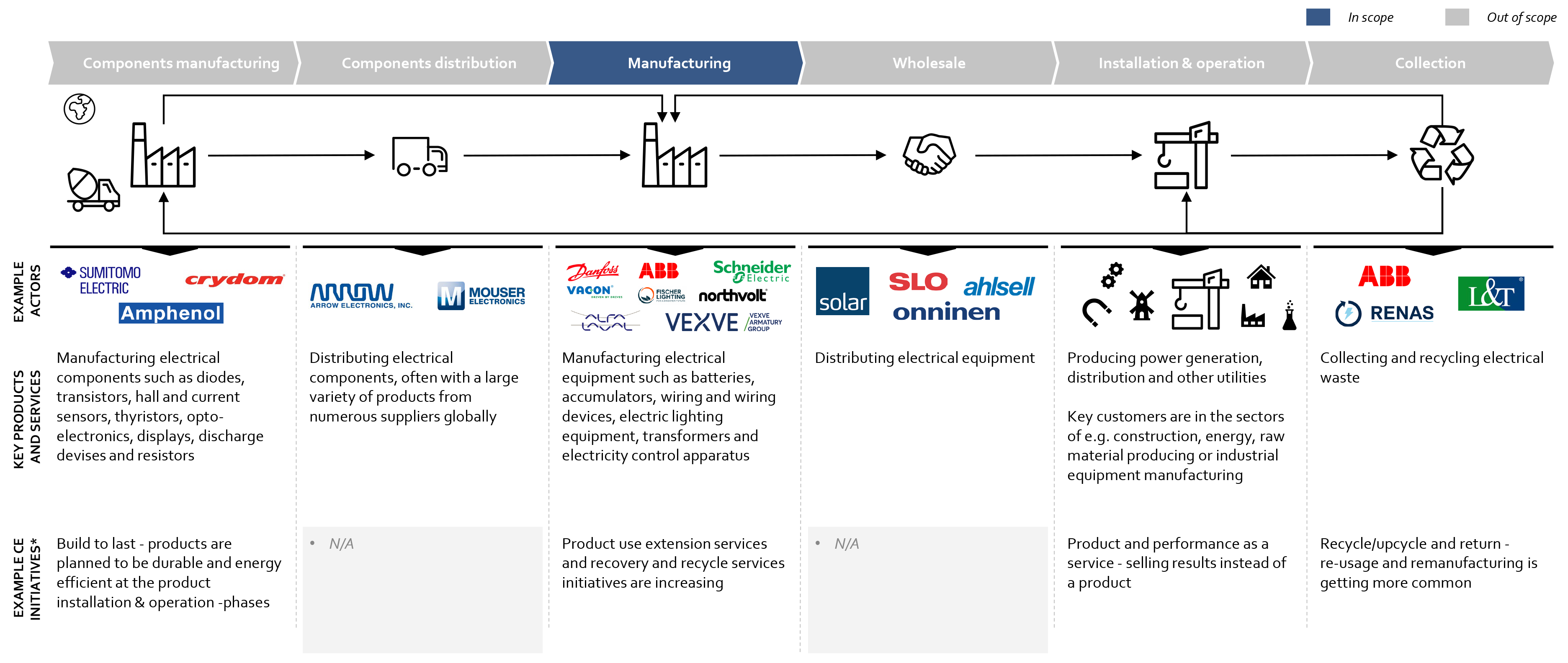

Value chain of the industries

1

Machinery & equipment

Maritime

Energy

Transportation

Construction

Appendix

Current state analysis and circular opportunities

2

INTRODUCTION: CIRCULAR MATURITY SURVEY

| Content | The circular maturity survey was conducted to understand the starting point of Nordic manufacturing companies in adopting the circular economy principles. |

| Outcome | The survey included reflection of current inefficiency assessment focused on understanding the occurrence and level of the five inefficiencies of the linear model: - Unsustainable materials - Underutilised capacities - Premature product lives - Wasted end-of-life value - Unexploited customer engagements |

| Outcome | In total, 24 Nordic manufacturing companies replied to the survey. The responses were collected in workshops in August – October 2022. Detailed results of the survey are presented in the following pages. |

RESULTS – CIRCULAR MATURITY SURVEY

Inefficiency assessment (1/5)

1) Unsustainable materials

Material and energy that cannot be continually regenerated (e.g., direct and indirect material is not renewable or bio-based)

RESULTS – CIRCULAR MATURITY SURVEY

Inefficiency assessment (2/5)

2) Underutilised capacity

Underutilised or unused products and assets (e.g., products are not operating full hours or full functionality is not used)

RESULTS – CIRCULAR MATURITY SURVEY

Inefficiency assessment (3/5)

3) Premature product lives

Products are not used to the fullest possible working life (e.g., due to new models and features or lack of repair and maintenance)

RESULTS – CIRCULAR MATURITY SURVEY

Inefficiency assessment (4/5)

4) Wasted end-of-life value

Valuable components, materials and energy is not recovered at disposal (e.g., not recycled or recovered at end of life)

RESULTS – CIRCULAR MATURITY SURVEY

Inefficiency assessment (5/5)

5) Unexploited customer engagements

Material and energy that cannot be continually regenerated (e.g., direct and indirect material is not renewable or bio-based)

Appendix

Additional details on sources

3

| Content | Playbook pages | Source |

| 5 Circular business models | 14 | Accenture – Lacy, P. & Rutqvist, J. (2015). Waste to Wealth: The Circular Economy Advantage. 1st ed. English: Palgrave Macmillan. Accenture – Lacy, P., Long, J. & Spindler, W. (2020). The Circular Economy Handbook: Realizing the Circular Advantage. 1st ed. English: Palgrave Macmillian. |

| 4 types of inefficiencies in the linear value chain | 12 | Accenture – Lacy, P. & Rutqvist, J. (2015). Waste to Wealth: The Circular Economy Advantage. 1st ed. English: Palgrave Macmillan Accenture presentation, Circular Materials Conference (2018) Accenture – 3D Printing vs 3D-TV: https://www.accenture.com/no-en/insight-3d-printing-vs-3d-tv |

| Development of resource demand | 24 | Accenture – Lacy, P. & Rutqvist, J. (2015). Waste to Wealth: The Circular Economy Advantage. 1st ed. English: Palgrave Macmillan |

| Circular technology descriptions | 93 - 101 | Adapted from Accenture – Lacy, P., Long, J. & Spindler, W. (2020). The Circular Economy Handbook: Realizing the Circular Advantage. 1st ed. English: Palgrave Macmillian. World Economic Forum, in collaboration with Accenture – Driving the Sustainability of Production Systems with Fourth Industrial Revolution Innovation (2018): http://www3.weforum.org/docs/WEF_39558_White_Paper_Driving_the_Sustainability_of_Production_Systems_4IR.pdf |

| Circular sub-models | 15, 18, 21, 24,27, 30 | Adapted from Accenture – Lacy, P., Long, J. & Spindler, W. (2020). The Circular Economy Handbook: Realizing the Circular Advantage. 1st ed. English: Palgrave Macmillian. Accenture presentation, Circular Materials Conference (2018) |

| The wise pivot | 34, 35 | Accenture Point of View – Leading in the NEW: Harness the Power of Disruption (2017): https://www.accenture.com/t00010101T000000Z__w__/jp-ja/_acnmedia/PDF-62/Accenture-Leading-in-the-New-POV.pdf |

| Circular data flow | 44 | Nordic Innovation, Data Sharing for a Circular Economy in the Nordics (2021): https://www.nordicinnovation.org/CEdatasharing |

About this publication

Nordic Circular Economy Playbook 2.0

Transform & Scale

© Nordic Innovation, 2022

Disclaimer: This playbook is part of the program Nordic Sustainable Business Transformation by Nordic Innovation. Accenture is responsible for all its content.

This Nordic Circular Economy Playbook 2.0 is a manual for change. It gives you the tools to build your sustainable business models and design the transformation journey from industrial value-chains to cross sectoral ecosystems. By taking a step towards a circular business, you take a step ahead of your competitors. The Nordic Circular Economy Playbook builds on the Circular economy business models for the manufacturing industry playbook by the Finnish Innovation Fund Sitra.

One of the three main pillars in the Nordic Vision 2030 is a green Nordic region. This can be achieved through a sustainable circular and bio-based economy, and this playbook will give Nordic companies the tools to start the journey and involve their entire value chain.

For a more accessible version of this publication download the powerpoint here: https://pub.norden.org/us2022-468/us2022-468.pdf