- Full page image w/ text

- Table of contents

- Foreword

- Preface – Covid measures

- Summary

- Sammendrag

- 1 Introduction

- 1.1 Definitions and limitations

- 2 Review on green stimulus measures

- 2.1 The understanding of green stimulus

- 2.2 Assessments of stimulus measures

- 3 Nordic stimulus measures in response to covid-19

- 3.1 Overview of Nordic financial stimulus measures

- 3.2 Comparison of total stimulus measures granted

- 4 Identification of sectors with green stimulus potential

- 4.1 Step 1: Identify impact of Covid-19 pandemic on Nordic economic sectors

- 4.2 Step 2: Identify impact of economic sectors on CO2 emissions

- 4.3 Step 3: Identify impact of economic sectors on the environment

- 4.4 Step 4: Identify economic sectors with the largest green stimulus potential

- 5 The impact of the Nordic financial stimulus measures on the climate and environment

- 5.1 Method for analysing impact of financial stimulus measures

- 5.2 Stimulus measures with potential impact on climate/environment

- 5.3 Climate impact of stimulus measures with direct budgetary impact

- 5.4 Environmental impact of Covid-19 stimulus measures with direct budgetary impact

- 5.5 Impact of guarantees and loans

- 6 Summary and discussion

- Main findings

- Discussion

- Policy implications

- References

- Appendix A – NACE sectors

- Appendix B – Stimulus measures by country

- Appendix C – Sectors with largest negative economic impact per country

- Appendix D - Contribution to total CO2 emissions by sector

- Appendix E – Emission intensive sectors

- Appendix F – Method for analysing effect on climate and environment

- Appendix G – Environmental effect of Covid-19 stimulus per country

- About this publication

MENU

Contents

Foreword

Since the winter of 2020, the spread of covid-19 has affected economic activity in the Nordic region. All the Nordic countries introduced fiscal policy measures to counteract the economic downturn and the negative effects the lockdown has on economic output and employment. At the same time, the Nordic countries are concerned with the more long-term crisis related to global warming, and the national targets for reducing greenhouse gas emissions and environmental degradation. The financial stimulus measures may exacerbate or positively impact challenges related to the environment and to greenhouse gas emissions.

In this project we have assessed the economic stimulus measures that have been introduced in the Nordic region, and their impact on climate and the environment.

The project is a cooperation between Menon Economics, Friðrik Már Baldursson, Professor of Economics at Reykjavik University and Erik Dahlberg at HBS Economics. We are grateful for all comments from the members of The Nordic Group on Environment and Economy (NME).

March 2022

Annegrete Bruvoll

Project responsible

Menon Economics

Nina Bruvik Westberg

Erika Karttinen

Operative project leaders

Menon Economics

Preface – Covid measures

During the coronavirus disease 2019 (COVID-19) the Nordic governments have all launched powerful economic stimulus packages to protect businesses and households from losses of production and employment, and to avoid a deep recession. In the spring 2020 the climate and environment ministers issued a joint statement where they emphasized the need to exploit synergies between economic recovery and green transition.

The purpose of this project has been to map and analyze the stimulus measures in our countries that have impacts on climate and the environment. How “green” or “brown” have these measures been? Part of the task has been to identify the sectors of greatest relevance, i.e. the sectors significantly affected by the economic disruptions resulting from COVID-19, and at the same time relevant because they have substantial impact on climate or the environment. One interesting finding is that stimulus measures having a positive or negative climate and environmental impact seem to constitute a relatively small part of the overall economic stimulus. Overall, this could indicate that the synergies mentioned by the climate and environment ministers are either not so large or have not been utilized. This is one issue that the consultants have commented on in the study.

The report has been prepared by Menon Economics, in cooperation with Fridrik Már Baldursson, Professor of Economics at Reykjavik University and Erik Dahlberg at HBS Economics. Members of the Nordic group for Environment and Economy (NME) have provided comments on draft reports during the project. But the authors of the report are responsible for the content, and any views and recommendations presented in the report do not necessarily reflect the views and positions of the Nordic governments or of NME.

April 2022

Bent Arne Sæther

the Nordic working group for Environment and Economy

Summary

This report assesses the “green stimulus” relevance of the covid-19 stimulus measures in the Nordic region. By green stimulus we mean measures that can achieve economic stimulus while also reducing greenhouse gas emissions and enhancing environmental and natural resource quality.

All Nordic countries implemented comprehensive covid-19 stimulus packages after the outbreak of the pandemic, amounting to between 2000 euro per capita in Finland to 4400 euro per capita in Denmark. We have identified that at least 6–21 percent of the measures suit the definition as green stimulus in terms of decreasing greenhouse gas emissions. A lower share, at least 2–13 percent, contributes to increase greenhouse gas emissions. The picture is almost the same for the environment. This is in line with a similar study covering the G20 economies.[1]Nahm, Miller and Urpelainen (2022) Hence, we do not find strong evidence of green stimulus in the covid-19 packages. However, neither do we find evidence that the net effects of the Nordic covid-19 packages on climate gas emissions and the environment were negative; the remaining measures are either assessed as not having any significant impact on emissions or the environment, i.e., schemes directed at sectors with low emission intensity or low environmental impact, or they are not possible to evaluate.

Most measures target several sectors or the economy in general, such as business cost support. For these support schemes, more comprehensive analyses for each measure are needed to conclude on the climate and environmental effects.

The main argument for green stimulus programs is that they can achieve economic stimulus targets while also improving the environment. This does, however, not agree with economic theory on policy design, which states that to achieve two separate policy targets efficiently, one separate instrument for each goal is needed. Our literature review supports this. For example, Chen et al. (2020) states that to put limited government funds to the best use, most of the pandemic-related stimulus should initially focus on investments that get people back to work quickly. This may be said to correspond to most of the Nordic stimulus measures.

Any public project of a certain size should undergo a cost-benefit analysis, where climate and environmental effects are considered in line with the positive benefits to employment and economic growth. In this approach, both elements in green stimulus - stimulating the economy while reducing greenhouse gas emissions and enhancing environmental and natural resource quality - are balanced. Direct instruments counteracting climate and environmental costs are generally more efficient than scaling down the measure to stimulate the economy.

For most of the covid-19 support measures undertaken by the Nordic governments, there is a lack of information enabling analysis of green effects. This reflects the urgency of getting the economic support schemes in place, where pre-evaluations based on full cost-benefit analyses were probably not prioritized. Our impression is that the short-term measures supporting companies and households were mostly appropriate in that they prevented a catastrophic downturn in the economy and household incomes.

Some green stimulus measures can also reduce market failures, such as support for technology development, R&D and market introduction. Detailed, ex-post evaluations of the largest support schemes could bring insight into which instruments provide the most efficient green stimulus. This could be valuable information in future economic crises with little time to analyse the effects of the measures before implementation.

Footnotes

- ^ Nahm, Miller and Urpelainen (2022)

Sammendrag

Denne rapporten vurderer i hvilken grad de økonomiske støtteordningene i Norden i forbindelse med covid-19 har vært grønne støtteordninger. Med grønne støtteordninger mener vi tiltak som stimulerer økonomisk aktivitet og samtidig bidrar til reduserte klimagassutslipp og bedret miljø.

Alle nordiske land implementerte omfattende stimuleringspakker etter utbruddet av pandemien, som beløper seg til mellom 2000 euro per innbygger i Finland til 4400 euro per innbygger i Danmark. Vi har identifisert at minst 10–20 prosent av tiltakene virker til reduserte klimagassutslipp, mens en lavere ande, minst 2–13 prosent, stimulerer til økte utslipp. Bildet er nesten det samme for miljøet (henholdsvis 2–13 og 2–13 prosent). Disse funnene er i samsvar med en lignende studie av G20-landene.[1]Nahm, Miller and Urpelainen (2022) Selv om vi ikke finner sterke indikasjoner på grønn stimulans i de nordiske covid-19-pakkene, finner vi heller ikke at tiltakene samlet sett har hatt negativ innvirkning på klimagassutslipp og miljø; de resterende tiltakene vurderes enten å ikke ha noen vesentlig påvirkning på utslipp eller miljø, eller de er ikke mulig å vurdere.

De fleste tiltak retter seg mot flere sektorer eller økonomien generelt, for eksempel støtte til bedrifter for å opprettholde sysselsettingen. Det vil være nødvendig med mer detaljerte analyser for å anslå klima- og miljøeffekter av slike tiltak.

Hovedargumentet for grønne stimuleringsprogrammer er at de både kan støtte økonomisk vekst og ha positive klima- og miljøeffekter. Å oppnå flere mål med ett virkemiddel samstemmer imidlertid ikke med økonomisk teori, som sier at effektiv måloppnåelse krever ett virkemiddel per mål. Vår litteraturgjennomgang av covid-19-analyser støtter dette, der for eksempel Chen et al. (2020) påpeker at mesteparten av støtteordningene i pandemien bør fokusere på investeringer som får folk raskt tilbake i arbeid. Vi finner at dette også er i samsvar med de fleste av de nordiske stimuleringstiltakene.

Ethvert offentlig prosjekt av en viss størrelse bør gjennomgå en nytte-kostnadsanalyse, hvor klima- og miljøeffekter vurderes i tråd med de positive virkningene for sysselsetting og økonomisk vekst. Denne tilnærmingen balanserer begge elementene i grønn stimulans, både økonomisk stimulans og klimagassutslipp/miljø. Direkte virkemidler som motvirker klima- og miljøkostnader er generelt mer effektive enn å trappe ned tiltaket som skal stimulere økonomien for å nå alt med ett instrument.

For de fleste covid-19-støttetiltakene mangler informasjon som muliggjør analyser av grønne effekter. Dette viser at det har hastet å få på plass den økonomiske støtten, og forhåndsevalueringer basert på fulle nyttekostnadsanalyser kunne ikke prioriteres. Vårt inntrykk er at de kortsiktige tiltakene til støtte for bedrifter og husholdninger stort sett har nådd sine mål ved bygge unngå en vedvarende nedgang i økonomien og husholdningenes inntekter.

Støtteordninger som bygger ned markedssvikt, som støtte til teknologiutvikling, FoU og markedsintroduksjon vil både kunne representere grønne støtteordninger og være kostnadseffektive. Etter-evalueringer av de største støtteordningene kan gi innsikt i hvilke virkemidler som mest effektivt kan stimulere både økonomien og klima/miljø positivt. Dette kan være verdifull informasjon i fremtidige økonomiske kriser, med knapp tid til å analysere tiltakseffekter før implementering.

Footnotes

- ^ Nahm, Miller and Urpelainen (2022)

1 Introduction

Since the winter of 2020, the spread of covid-19 has affected economic activity in the Nordic region.[1]All Nordic countries have introduced national measures to limit the spread of infection. In addition, changes in other countries' economic activity have affected the Nordic countries. All Nordic countries have introduced fiscal policy measures to counteract the economic downturn and the negative effects the lockdown has on economic output and employment. At the same time, the Nordic countries are concerned with the more long-term crisis related to global warming, and the national targets for reducing greenhouse gas emissions and environmental degradation. Lockdown measures and the economic downturn led to reductions in greenhouse gas emissions during 2020. The Nordic countries’ ability to reduce their emissions will depend on the type and strength of the financial stimulus measures, which may exacerbate or positively impact challenges related to the environment and to greenhouse gas emissions.

The first fiscal policy measures that were introduced were mainly aimed at limiting the number of bankruptcies and securing jobs, as well as providing financial security for the laid-off and the unemployed. In the changing pandemic situation after the spring of 2020, the countries have continuously adjusted the measures to counteract the negative economic effects of lockdowns. In the beginning of 2022, we may face the end of the pandemic, but are still in an uncertain stage. It is likely that there will be long-term needs for financial support to bring the economy back to a more stable path. Most measures are designed independently of climate and environmental goals, but some are labelled as causing double positive effects: both stimulating GDP growth and the transition to low-emission economies.

Facing the multiple challenges, it is of great importance to identify fiscal instruments that at the same time contribute to the achievement of climate targets and reduce the pressure on the environment. The variation in the implemented instruments in the pandemic offers a broad set of measures to be analysed for this purpose. The question of interest is to identify which measures have the favourable property of serving both policy goals, and which stimulus measures should be less used if they undermine the environment and contribute to increased global warming.

The Nordic Working Group for Environment and Economy (NME) at the Nordic Council of Ministers (NCM) has requested a survey and an assessment of stimulus measures that have been introduced or are considered in the Nordic region, and their impact on climate and the environment. The target groups for the results are Nordic and international decision-makers, civil servants and politicians who prepare and execute the stimulus measures and coordinate fiscal and climate and environmental policy.

Footnotes

- ^ All Nordic countries have introduced national measures to limit the spread of infection. In addition, changes in other countries' economic activity have affected the Nordic countries.

In the announcement, the NME outlines four main questions:

Question 1: Identify and briefly summarize the knowledge base, including theory, about measures that have both a stimulus effect and that in the short and long term have a positive impact on the environment and climate.

Question 2: Identify sectors where stimulus measures are most relevant in light of the current economic crisis and which can lead to particularly large and positive environmental and climate impacts.

Question 3: Describe which measures the Nordic countries have implemented or plan to implement, which can be classified as environmental and climatic measures, or which counteract this development.

Question 4: Analyse whether there are any measures that can be effective in terms of economic activity, but which risk making it difficult for the Nordic countries to achieve their climate goals, and whether they can be designed in a different way so that they have so little negative impact on the environment as possible and contribute to the fulfilment of climate goals.

1.1 Definitions and limitations

The Nordic countries have introduced a wide range of measures and policies, including financial stimulus measures, mandates, bans and regulations. In this project we focus on the financial stimulus measures. When relevant, we refer to other policies that may impact economic growth and/or the climate/environment. In line with the tender requirements, we do not focus on EU’s financial stimulus measures under the EU Green Deal.

We assume that all implemented covid-19 stimulus measures have the anticipated short-term positive effects on the economy. Hence, we do not focus further on the effects on employment and economic growth.

The measures are based on information in the respective country’s state budget for 2020 and 2021 and cover the central government’s stimulus measures only. We do not capture local stimulus measures unless the state transfers funds to this purpose.

We define positive climate impacts as impacts that reduce greenhouse gas emissions or adapts to climate change, compared to a scenario with the economic consequences of the pandemic but without the stimulus measures.

Positive environmental impacts are impacts that enhance environmental and natural resource quality, such as reduced pollution and preservation of biodiversity and ecosystem services, compared to a scenario with the economic consequences of the pandemic but without the stimulus measures.

The analysis is based on observations and data available up to the fall of 2021.

2 Review on green stimulus measures

2.1 The understanding of green stimulus

Even though there are several definitions of green stimulus in the literature, the definitions seem to be conceptually similar. The formulation by Strand and Toman (2010), in a working paper for the World Bank, represents a standard definition of green stimulus:

"the application of policies and measures to stimulate short run economic activity while at the same time preserving, protecting and enhancing environmental and natural resource quality both near-term and long-term”.

Agrawala et al. (2020) argues that what separates green stimulus from green policies in general is that it is aimed at buffering an economic shock in addition to having environmental benefits. The literature includes several other terms used to describe similar concepts to green stimulus, e.g., green recovery[1](OECD, 2021) or sustainable recovery[2]Hepburn et al. (2020).

The definition of green varies, as exemplified in the definition from Strand and Toman (2010), and is often context specific. The greenness of a measure can for instance be connected to carbon emission targets, environmental clean-up targets, biodiversity, air pollution, material usage efficiency, water usage, or investments in environmental R&D.[3](OECD, 2020) When we use the term green in this report, we mean any type of effect that can be said to preserve, protect, or reach targets related to the environment or climate.

The short-term or long-term economic benefit of stimulus measures is often measured as a change in employment[4]Popp et al. (2020), or change in gross domestic product (GDP)[5](IEA, 2020).

The main argument for green stimulus programs is that they can achieve economic stimulus targets while also reducing climate gas emissions and improving the environment. Hence, these measures are argued to have a double effect compared to non-green stimulus measures, as they can both assist with recovery from the covid-19 crisis and steer society onto a more sustainable path. While this sounds like a compelling argument, it does not coincide with economic theory on policy design, which states that to achieve two separate policy targets efficiently, one separate instrument for each goal is needed. Policies aiming to achieve two targets at once, in this case short- or long-term environmental benefits and economic gains, are difficult to design efficiently. Hence, we cannot take as a given that the first argument for green stimulus holds.

Another argument is that green stimulus can increase long-term competitiveness, as the global demand of green goods, services, and processes are believed to increase in coming years.[6]Strand and Toman (2010) An economic crisis can result in less focus on environmental questions and climate change, and thus offset needed structural change. For instance, recovery measures in support of carbon intensive technologies risk creating lock-in effects which holds back the green transition.[7]Strand and Toman (2010), Hepburn et al. (2020) Green stimulus may be an opposing force. An example of stimulus based on this argument is the European Green Deal[8](European Commission , 2021b), which combines covid-19 recovery with long-term greenhouse gas emission and resource-efficiency goals.

Both economic and environmental effects can be short- and long-term. Pollution clean-up is an example of a measure with primarily short-term effects, while infrastructure investments have more of a long-run impact.

2.2 Assessments of stimulus measures

In our search for empirical studies of efficient green stimulus measures, we find that the literature is scant in this field.[1]This is in contrast to the literature on double dividend effects of environmental taxes. This refers to the notion that taxes can both reduce pollution and reduce the overall economic costs associated with the tax system. If using the revenue generated from the environmental taxes to displace more distortionary taxes, economic growth may also be stimulated. The same is reflected in Agrawala et al. (2020), who evaluates green stimulus packages in response to the global financial crisis 2007–08 and draws lessons for the covid-19. They conclude that evaluations of macroeconomic, labour market and environmental effects of the green stimulus measures are relatively scarce, and point to the difficult task of defining a suitable counterfactual to compare the impacts against.

We do, however, find some qualitative evaluations of green stimulus measures, and studies of economic stimulus on the environment and the economy.

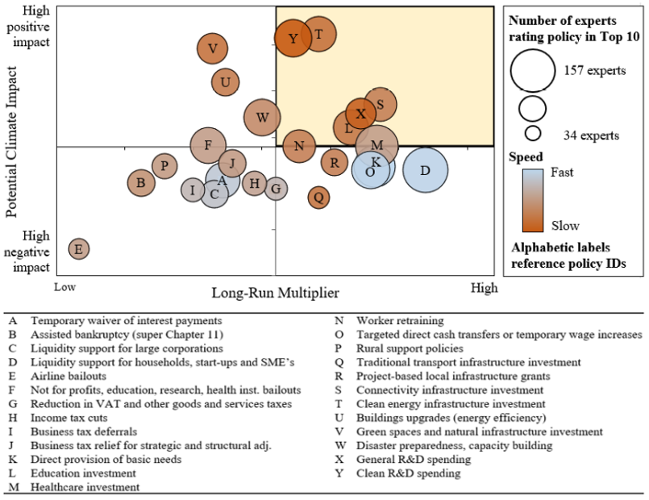

Based on survey answers from 231 experts, including central bank officials, finance ministry officials, and other economic experts from G20 countries, Hepburn et al. (2020) identified policies with large potential for both economic recovery and positive climate impact. The experts were asked to assess recovery-policy types based on speed of implementation, long-run economic multipliers, and positive or negative climate impact potential. The results are shown in Figure 2.1. The authors identified five policies that can have both a positive climate impact as well as an impact on long-run economic multipliers:

- clean physical infrastructure investment in the form of renewable energy assets, storage (including hydrogen), grid modernisation and CCS technology

- building efficiency spending for renovations and retrofits including improved insulation, heating, and domestic energy storage systems

- investment in education and training to address immediate unemployment from COVID-19 and structural shifts from decarbonisation

- natural capital investment for ecosystem resilience and regeneration including restoration of carbon-rich habitats and climate-friendly agriculture

- clean R&D

Footnotes

- ^ This is in contrast to the literature on double dividend effects of environmental taxes. This refers to the notion that taxes can both reduce pollution and reduce the overall economic costs associated with the tax system. If using the revenue generated from the environmental taxes to displace more distortionary taxes, economic growth may also be stimulated.

All the above-mentioned policies are assessed to be relatively slow to implement, implying that they are not suitable as rapid responses to economic crises. The paper does not identify any quickly implementable policy measures with a positive climate impact.

Figure 2.1 Categorization of policy measures based on potential climate impact, long-run multiplier, and speed of implementation.

Source: Hepburn et al. (2020)

Strand and Toman (2010) gives a qualitative assessment of expected economic and environmental effects from a variety of stimulus measures, see Table 2.1. Many of these policies align with the policies suggested by Hepburn et al. (2020). The column “short-term stimulus” considers short-term economic effects, whereas the three other columns consider longer term effects.[1]Strand and Toman (2010) present effects both for developed and developing countries. We present here the effects for developed countries. Overall, the more labour-intensive a measure is, the higher is the expected economic effect (in terms of increased employment). Short- or long-term depend on how quickly different types of projects can be launched and the first- and second order effects. The effects on greenhouse gas emissions or other environmental factors vary between policies.

Footnotes

- ^ Strand and Toman (2010) present effects both for developed and developing countries. We present here the effects for developed countries.

Table 2.1 Policies categorized based on short- and long-term stimulus effect, in addition to greenhouse gas (GHG) and environment and resource “co-benefits”[1]The co-benefits comprise, e.g., of internalization of otherwise non-corrected external effects. These can be environmental but can also include effects such as reduced accident rates and congestion from road traffic following increased fuel prices..

Source: Adapted based on Strand and Toman (2010)

Footnotes

- ^ The co-benefits comprise, e.g., of internalization of otherwise non-corrected external effects. These can be environmental but can also include effects such as reduced accident rates and congestion from road traffic following increased fuel prices.

| Policy category | Short-term stimulus | Long-term growth | GHG emission reductions | Environment and resource “co-benefits” |

| Quickly implemented, labour intensive, activities | ||||

| Non-hazardous environmental clean-up | High | Low | Low | High |

| Natural resource maintenance, monitoring and policing | Medium | Low | Variable | High |

| Energy efficiency retrofits | High | Medium | Medium | Medium |

| Expansion of currently cultivated bio-energy | Medium | Low | Variable | Variable |

| Expanded biological carbon sequestration | Medium | Low | Medium | Variable |

| Capital investments in environmental and natural resources | ||||

| Conventional pollution control/prevention | Low | Medium | Variable | High |

| Increased renewable electricity production | Low | Variable | High | Medium |

| Introduction of new forms of bio-energy | Low | Variable | Medium | Variable |

| Energy efficiency improvements in new capital | Low | Low | High | Medium |

| Green transport infrastructure | Low | Low | Medium | Medium |

| Investment to strengthen resilience of natural resources to climate change | Medium | Medium | Variable | High |

| Other specific programs with “green” characteristics | ||||

| “Cash for clunkers”* | Medium | Low | Low | Low |

| Development and expansion of recycling systems | Low | Low | Low | Variable |

| Congestion reduction measures | Low | Medium | High | Medium |

| Altered urban forms for greater density and mixed use | Low | Medium | Medium | Low |

| Power grid expansion | Low | Medium | Low | Variable |

| *Incentive programs to trade in old, less fuel-efficient cars for new, more fuel-efficient ones. | ||||

Strand and Toman (2010) argue that infrastructure investments in sectors like transport, energy, supply, and water could be compatible with long-term growth and environmental targets. While they conclude that these investments are important for long-term economic activity, they also note that measures categorised as green within these sectors are often large projects with long time horizons, making them less suitable for short-term stimuli. This is especially true for investments in the transport sector. The authors argue that investments in the energy sector could instead provide shorter-term economic gains.

Pollitt (2011) assessed the green elements of the fiscal stimulus packages in response to the financial crisis in 2008 in nine EU and four other countries. According to their evaluation, optimal recovery packages must include a balance between policies that provide short and long-term benefits (both economic and environmental). They also underline that the short-term economic benefits of green stimulus can be limited. They find that the short-term benefits are largely economic and could hence be equally met by non-green policies. Further, green R&D and innovation measures also bring long-term economic benefits from greater energy efficiency, reduced imports of fossil fuels and reduced exposure to volatile global energy prices.

2.2.1 Economic effects

Based on the empirical literature, green stimulus measures appear to have mostly long-term rather than short-term effects on the economy, even if there are some studies contradicting this conclusion. Even if the short-term effect of green stimulus is limited, the stimulus could still play an important role in economic recovery through its effects on long-term growth and employment.

Strand and Toman (2010) argue that green stimulus measures may have a limited effect economically, at least in the short run, compared to other available alternatives. Especially, they argue that government support for renewable energy is not an efficient way to increase employment in the short-term, since stimulating other sectors would create more employment. The conclusion is based on a literature review of papers studying economic effects of green stimulus in the EU overall in addition to country-specific studies on Denmark and Spain as well as the US. The effects of renewable energy investments could be different today, as unit costs for renewable energy have decreased and the investments required today are proportionately lower. Nevertheless, Agrawala et al. (2020) also conclude that the evidence of job creation from renewable energy policies is still mixed.

Popp et al. (2020) also conclude that “while a green stimulus can help reshape the economy, it is less likely to help restart the economy”. They study the US American Recovery and Reinvestment act of 2009 (ARRA) and find that each 1 mill. dollars of green stimulus created 15 new jobs. However, these job gains are found in years 2013–2017, and they find little evidence of employment gains before this. Green stimulus, based on this study, does increase employment, but works more slowly than non-green stimulus. This is in line with the efficiency argument that two policy targets require two separate instruments. To put limited government funds to the best use, the authors argue that most of the pandemic-related stimulus should initially focus on investments that get people back to work quickly.[1]This argument is presented in a published paper in 2020, Chen et al. (2020)

Similar to other scholars, Brahmbatt (2021) states, based on a literature review of theoretical and empirical studies on green recovery, that the win-win situation that green stimulus is argued to represent is unlikely to work in practise: “Green recovery would yield more environmental benefits, especially in the medium and long term, but would generate a relatively slower and smaller recovery from the COVID crisis”.

On the other hand, a study by Pollitt (2011) for the European Commission finds that the green stimulus after the 2008–09 crisis did have a positive short-run impact on the EU economy.[2]See Pollitt (2011) The impact on short-term economic multipliers from green investments ranged from around 0.6 percent to 1.1 percent of GDP at the national level, and up to 1.5 percent of GDP at the European level. An important finding in this study is that co-ordinated green stimulus measures delivered greater short-term economic impact than green measures implemented by individual countries. The study also finds that the effects from green investments are similar to those from other investments.[3]Estimate is based on the short-term multiplier effect, the ratio of the boost to GDP. See Pollitt (2011).

Further, Chen et al. (2020) argue that there is a place for green stimulus in a pandemic recovery even if it would not have significant short-run effects, as the long-run benefits of green stimulus on the economy are clear. The authors argue that green recovery measures should be seen as assisting in the inevitable transition to a greener economy, but that these may need to be combined with other policies that are better at tackling the pressing economic realities of the crisis. This is also supported by the findings from the expert interviews in Hepburn et al. (2020).

In their study for the European Commission, Pollitt (2011) claims that an optimal recovery package should include a balance between long- and short-term policies. They also argue that short-term benefits of green policies could be enhanced. They believe this could be done by using already prepared business plans that are quick to implement, or by increasing the use of “co-financing” from the private sector. An example of co-financing projects is vehicle scrappage schemes, where consumers are incentivized to exchange old cars for newer, more fuel-efficient ones. In this scheme, consumers are incentivized to purchase a new car and spend money they most likely would have saved otherwise, creating a larger short-term economic boost than would have been possible with public spending alone.

Additionally, combining green stimulus with training programmes could improve the stimulating effect. Popp et al. (2020) find that skill availability, that workers have the skills needed for the green economy, is crucial for the success of green stimuli. Hence, countries where the workers already have the skills needed will benefit more from green stimulus than countries that do not.[4]This is consistent with the theories on the cost of job reallocation in labour economics. The larger the green skill gap in the community and the more non-green jobs that will be lost, the higher the cost of transitioning to a green economy will be. See Chen et al. (2020) for more. Building on these findings in another study, later in 2020, the authors provide suggestive evidence that combining green stimulus with training programmes improves the effectiveness of green subsidies on economic recovery.[5]Chen et al. (2020). The green stimulus programs assessed were a part of the ARRA green package. The ARRA package, amongst other things, provided funding for energy efficiency retrofits and the renewable energy industry. The training programmes were also directed at these activities.

Footnotes

- ^ This argument is presented in a published paper in 2020, Chen et al. (2020)

- ^ See Pollitt (2011)

- ^ Estimate is based on the short-term multiplier effect, the ratio of the boost to GDP. See Pollitt (2011).

- ^ This is consistent with the theories on the cost of job reallocation in labour economics. The larger the green skill gap in the community and the more non-green jobs that will be lost, the higher the cost of transitioning to a green economy will be. See Chen et al. (2020) for more.

- ^ Chen et al. (2020). The green stimulus programs assessed were a part of the ARRA green package. The ARRA package, amongst other things, provided funding for energy efficiency retrofits and the renewable energy industry. The training programmes were also directed at these activities.

2.2.2 Environmental effects

In the following, we summarize the effects of green stimulus measures on different green outcomes, specifically reduced greenhouse gas emissions through:

- investments in or subsidies for renewable energy,

- tax incentives and grants aimed at increasing building energy efficiency and/or reducing household energy consumption, and

- scrappage schemes incentivizing consumers to swap old vehicles for newer less fuel-intensive vehicles.

The reason for a focus on reduced greenhouse gas emissions is that the green measures after the 2008–2009 financial crisis, which most empirical studies within this topic are based on, were mainly targeted towards energy efficiency and climate change mitigation, both in Europe and the US.[1]Pollitt (2011) and Chen et al. (2020)

In general, there is evidence that green stimulus and green policy measures achieve environmental targets to some extent. However, the evidence is mixed, and green incentives, e.g., for vehicle scrappage or increased energy efficiency in buildings, can have unintended consequences that make them less efficient.

Green stimulus has been successful in accelerating the shift to renewable energy. A study by the US Council of Economic Advisors in 2016 shows that stimulus programmes in response to the 2008 financial crises increased renewable energy generation: solar electricity in the US increased 30 times from 2008 to 2015, and wind generation increased more than threefold. This development is to a large extent attributed to the deployments made possible by the US American Recovery and Reinvestment act of 2009 (ARRA). The ARRA program allocated $90 bill. of the stimulus to renewable energy projects, which funded a variety of different projects through differing funding mechanisms.[2]Around 30 percent of the stimulus package was in the form of tax incentives, while 70 percent was in the form of spending. The funding was directed towards the following categories: renewable generation, energy efficiency, grid modernization, advanced vehicles and fuels, transit, carbon capture and storage, green innovation and job training, and clean energy manufacturing. Additionally, ARRA contributed to dramatic cost reductions, increasing the viability of renewable energy as an alternative to fossil fuels.[3]Council of Economic Advisors (2016)

Stimulus measures have also been directed to increasing building energy efficiency and reducing energy consumption. Energy efficiency stimulus includes tax incentives and grants for investing in insulation, installation of energy efficient lights, and retrofitting buildings. Installing smart meters, that inform consumers of their energy consumption, has been shown to stimulate reduced energy consumption.[4]See Agrawala et al. (2020) for a more detailed discussion of the literature

Incentives may also have unintended consequences as shown in Alberini et al. (2016). In the study, the effect on energy consumption from a new heat pump is measured on two groups, one which received an incentive to install it and one which did not. On average, household energy consumption is reduced by eight percent when a new, more energy-efficient pump is installed. However, among the incentive receivers (households) the effect is small, and the larger the incentive, the smaller the reduction in energy usage. Hence, environmental benefits might not increase in proportion to the size of the investment or could even be offset by behavioural rebound effects. Based on this, Agrawala et al. (2020) conclude with that energy-efficiency programmes might need to be combined with measures that account for behavioural responses to improve policy design.

The environmental impact of scrappage schemes, which provide financial incentives to trade in vehicles with low fuel efficiency, are mixed.[5]Agrawala et al. (2020) In the US, the CARS programme introduced in 2009 is estimated to have reduced CO2 emissions,[6]Li et al. (2013) and a European study found that the scrappage schemes increased fuel efficiency of new cars during the financial crisis.[7]Grigolon et al. (2016) On the other hand, a German scrappage scheme resulted in people trading in smaller vehicles for medium-sized ones. Even though the new vehicles were more fuel-efficient, larger cars use more fuel than smaller cars, cancelling out some of the benefits from the scheme.[8]OECD/ITF (2011) Additionally, based on a Pollitt (2011), the post financial crises scrappage schemes had limited environmental benefits as many vehicles would have been replaced soon with or without the schemes.

The effects from investing in green R&D are also mixed. Agrawala et al. (2020) have primarily looked at studies on investments in carbon capture technology. They conclude that projects in recovery packages in both Europe and the US had a low success rate, even though several other carbon capture projects have been successful in the same period. Agrawala et al. (2020) conclude that direct public R&D can create problems as governments need to try and pick winners for the investment to pay off, and that governments instead should try and encourage competitive selection to direct the investments better.

The mixed experiences do not disqualify green stimulus packages but point to the classical argument that separate instruments are needed to achieve separate policy targets efficiently.

Footnotes

- ^ Pollitt (2011) and Chen et al. (2020)

- ^ Around 30 percent of the stimulus package was in the form of tax incentives, while 70 percent was in the form of spending. The funding was directed towards the following categories: renewable generation, energy efficiency, grid modernization, advanced vehicles and fuels, transit, carbon capture and storage, green innovation and job training, and clean energy manufacturing.

- ^ Council of Economic Advisors (2016)

- ^ See Agrawala et al. (2020) for a more detailed discussion of the literature

- ^ Agrawala et al. (2020)

- ^ Li et al. (2013)

- ^ Grigolon et al. (2016)

- ^ OECD/ITF (2011)

3 Nordic stimulus measures in response to covid-19

3.1 Overview of Nordic financial stimulus measures

The Nordic countries have introduced a wide range of measures and policies, including financial stimulus measures, mandates, bans and regulations. The stimulus can be roughly categorized into the following groups of instruments:

- Tax deferrals

- Permanent tax reduction or exemption

- Loan guarantees

- Grants and subsidies

- Investments

The instruments have different aims, and target either specific sector(s) or the general economy.

Tax deferrals and tax reductions/exemptions are given to increase companies and households’ liquidity, at the expense of forgone or postponed revenue to the government. Most of the tax deferrals or tax reductions/exemptions target companies, yet there are also examples of tax exemption given to households, e.g., Iceland’s VAT refunds covering leisure housing, design and supervision of construction, car repairs, etc.

Loan guarantees are given in order relieve credit constraints in the financial market. The loan guarantees are given to companies regardless of sector or target specific companies, such as airlines.

Grants or subsidies either 1) compensate for loss of income for companies or households or 2) target specific sectors to stimulate activity. In the first case, the grants/subsidies either compensate for proven income loss or expected future income loss, for example through purchase of transportation services. In the second case, the receiving party is not necessarily experiencing an income loss. The aim is instead to increase activity and thus raise current or future employment. Examples of this are grants to the construction sector or grants to research projects/funds.

3.2 Comparison of total stimulus measures granted

By stimulus measures, we mean all measures that the national governments have labelled a response to the economic consequences of the pandemic. Further, we have included all measures with a direct budgetary impact and excluded support to activities related directly to handling the pandemic, like support to hospitals and testing stations.

The Covid-19 stimulus packages differ both in composition and in total stimulus, amounting to between 1 bill. euros (Iceland) and 26 bill. euros (Denmark). All countries have agreed on large stimulus packages, and in all countries a significant share of this has been directed as immediate support to all companies and households affected by the pandemic. Figure 3.1 shows the total stimulus per capita in all Nordic countries during 2020–2021.[1]We have only included stimulus measures that, to the best of our knowledge, were planned for 2020 and 2021. We have based our analyses on planned implementation of measures, and the actual implementation might differ. We collected data during the fall of 2021, and hence we have not included any of the stimulus implemented due to new restrictions in December 2021 in several Nordic countries.

Footnotes

- ^ We have only included stimulus measures that, to the best of our knowledge, were planned for 2020 and 2021. We have based our analyses on planned implementation of measures, and the actual implementation might differ. We collected data during the fall of 2021, and hence we have not included any of the stimulus implemented due to new restrictions in December 2021 in several Nordic countries.

Figure 3.1 Total covid-19 stimulus measures during 2020–2021 per country, specified and unspecified stimulus.[1]Danish stimulus had not yet been specified in terms of which initiative and sector the money should be directed to in October 2021 In euro per capita.

Footnotes

- ^ Danish stimulus had not yet been specified in terms of which initiative and sector the money should be directed to in October 2021

Based on our mapping, Denmark and Iceland have agreed upon the most generous stimulus packages measured per capita. Both countries have chosen to introduce large infrastructure projects running over several years as a response to the economic repercussions. Given that projects like these undergo long time investigation and processing before they are launched, it is likely that the infrastructure projects were planned, before the pandemic. There is a good chance that some of these packages would have been realized even without the pandemic. Still, we do not surmise on this matter, as they have been labelled corona stimulus by the respective national governments. Further, it is possible that the adoption of some of these measures were speeded up, and/or increased in size, because of the pandemic. To compare, Finland in late 2019 agreed upon a program called One-off future-oriented investments which runs from 2020–22 and totals 3 bill. euro. As this was agreed upon before the pandemic, it is not included as stimulus measures, even though it in practise could have had a stimulating effect.

The total amount of covid-19 stimulus granted is reported differently in all Nordic countries, and a direct comparison is therefore difficult. The total amounts per capita presented in Figure 3.1 hence be viewed with care. For example, even though Denmark has agreed upon the largest amount of stimulus of all the Nordic countries, over two thirds of this was, to the best of our knowledge, not yet specified when we conducted this analysis[1]Danish stimulus had not yet been specified in terms of which initiative and sector the money should be directed to in October 2021 in terms of which initiative and sector the money should be directed to. Whether the stimulus will eventually be paid out or not, it most likely has not be distributed within 2020–2021, which is our period of observation. If we exclude the stimulus that is yet to be specified, Denmark goes from highest to lowest stimulus per capita in the Nordic countries.

For a more detailed description of the financial stimulus packages that have been implemented in response to the covid-19 pandemic in all Nordic countries, see Appendix B.

Footnotes

- ^ Danish stimulus had not yet been specified in terms of which initiative and sector the money should be directed to in October 2021

4 Identification of sectors with green stimulus potential

The purpose of this chapter is to identify economic sectors in the Nordic economies in need of stimulus following the Covid-19 pandemic, and where stimulus has green potential, e.g., a positive impact on the climate/environment (Question 2).[1]As described in section 2.1, the term green in this report refers to any type of effect that can be said to preserve, protect, or reach targets related to the climate and the environment, the latter including biodiversity, pollution, waste, land use, water use and ecosystem services.

This is done stepwise:[2]This framework is based on a method developed for categorizing the state budget items by greenhouse gas emissions. (Menon and CICERO, 2020).

- Step 1: Identify impact of Covid-19 pandemic on the Nordic economic sectors (section 4.1)

- Step 2: Identify impact of the economic sectors on the climate in terms of CO2 emissions (section 4.2)

- Step 3: Identify impact of the economic sectors on the environment (section 4.3)

- Step 4: Identify economic sectors with the largest green stimulus potential (section 4.4)

In Step 1, we present and analyse how the various sectors[3]The identification of sectors follows NACE Rev. 2, the European standard classification of productive economic activities. of the Nordic economies have been impacted by the pandemic in terms of gross value added (GVA), employment and the total number of hours worked. This provides an intuition of which sectors that have been/are in most need of stimulus measures, to mitigate the negative impacts of the pandemic. We primarily use data from Eurostat, which has comparable data for all Nordic countries.[4]However, one should note that it is the respective national statistical offices that provide Eurostat with data. We use data for the latest year available for all the Nordic countries. The national statistical offices of the Nordic countries provide more detailed data, which complement the analysis when needed.

In Step 2, we present and analyse the total greenhouse gas (GHG) emissions from the activity in each sector, as well as their emission intensities. This provides an intuition of the expected climate impacts of the stimulus measures directed for each sector.

In Step 3, we categorize the impact of different sectors on the environment. In contrast to greenhouse gas emissions (Step 2) there is no common unit for measuring environmental outcomes. Hence, we follow a more qualitative approach to identify sectors that may impact the environment.

In Step 4 we combine information from the three previous steps. Sectors in need of stimulus (from Step 1) that negatively impact either the climate (from Step 2) and/or the environment (from Step 3) are most relevant in a stimulus perspective.

Footnotes

- ^ As described in section 2.1, the term green in this report refers to any type of effect that can be said to preserve, protect, or reach targets related to the climate and the environment, the latter including biodiversity, pollution, waste, land use, water use and ecosystem services.

- ^ This framework is based on a method developed for categorizing the state budget items by greenhouse gas emissions. (Menon and CICERO, 2020).

- ^ The identification of sectors follows NACE Rev. 2, the European standard classification of productive economic activities.

- ^ However, one should note that it is the respective national statistical offices that provide Eurostat with data.

4.1 Step 1: Identify impact of Covid-19 pandemic on Nordic economic sectors

The pandemic and the restrictive measures have impacted most, if not all, sectors of the Nordic economies. However, some sectors have clearly been more severely impacted than others. In principle, one can expect that the stimulus measures to sup|port economic activity would primarily target the sectors that have seen the largest negative impact during the pandemic, while sectors that have been more mildly impacted should be in less need of stimulus measures. The sectoral economic growth from pre Covid-19 up to the end of 2021 also reflect the support measures made available for struggling companies (in all sectors) relatively early during the pandemic.[1]For example, the Swedish government proposed measures for tax deferment and financial support for furloughing employees in March 2019. (Finansdepartementet, 2020). These measures have reduced the negative impacts on companies and employees, e.g., by enabling companies to furlough, instead of laying off, their workforce.

The impact on GVA, employment and hours worked differed substantially across sectors and, perhaps more surprisingly, across the Nordic countries. The impact on the total economy and eleven broad sectors in 2020 is presented in Table 4.1. The table also includes the average annual growth rate during 2017–2019 in parentheses, for comparison. To help visualise the magnitude of the impacts for the different sectors and countries, a growth rate of –5 percentage points or lower in 2020 compared to the average annual growth rate in 2017–2019 is coloured red, a growth rate of 0 percent to –4.9 percentage points is coloured yellow, and a growth rate of 0.1 percentage points or higher is coloured green.

Each Nordic country experienced negative growth in total gross value added (GVA) during 2020 compared to 2019, although the magnitude of the impacts varied substantially. While Icelandic GVA decreased by 6.3 percent, Norwegian GVA decreased by a more limited 0.6 percent. For Denmark, Finland and Sweden, the decrease was between 2.4 percent and 3.1 percent. However, Iceland also experienced a higher average annual growth rate during the three years preceding 2020 (4 percent) than the other Nordic countries (1.4–2.3 percent).

For the EU27, GVA decreased by 5.9 percent from 2019 to 2020. Hence, except for Iceland, the Nordic countries had a clearly lower economic recession compared to the EU27.

Iceland was also the hardest hit Nordic country in terms of employment, with a decrease of 4.6 percent in employment and a decrease of 7.2 percent in total hours worked. Denmark was the Nordic country with the lowest decrease in employment (-0.7 percent), while Norway experienced the lowest decrease in total hours worked (-2.2 percent). For all Nordic countries, the number of hours worked decreased more than the number of employed persons. This suggests that a large portion of the furloughs were used by companies to avoid having to lay off employees. For example, at one point during 2020, the three largest vehicle manufacturers in Sweden (AB Volvo, Volvo Cars and Scania) had fully stopped their production and more than 60,000 employees were furloughed. By October 2020, all employees had returned to work.[2](Sveriges Radio, 2020)

For the EU27, employment decreased by 1.4 percent, similar to the Nordic countries, except for Iceland. The total number of hours worked decreased by 6.4 percent, which is a larger decrease than in the Nordic countries, except for Iceland.

Table 4.1 Economic impact per sector and country in 2020. Percentage change in Gross Value Added (GVA), persons employed (PE), and hours worked (HW) in 2020 compared to 2019, fixed index values. (Average annual change during 2017–2019 for comparison).

Source: Eurostat.[1]Gross value added and income by A*10 industry breakdowns and Employment by A*10 industry breakdowns

Footnotes

- ^ Gross value added and income by A*10 industry breakdowns and Employment by A*10 industry breakdowns

| The colors indicate the difference in growth in 2020 and average growth 2017–2019: | > 0.1 percentage points | -4.9 – 0 percentage points | -5 < percentage points |

| Sector | Denmark | Finland | Iceland | Norway | Sweden |

| TOTAL – all sectors of the economy | GVA: -2.4 (2.3) | GVA: -3.0 (2.0) | GVA: -6.3 (4.0) | GVA: -0.6 (1.4) | GVA: -3.1 (2.3) |

| PE: -0.7 (1.4) | PE: -2.1 (1.8) | PE: -4.6 (2.4) | PE: -1.2 (1.5) | PE: -1.3 (1.5) | |

| HW: -2.8 (0.5) | HW: -3.0 (1.4) | HW: -7.2 (1.5) | HW: -2.2 (1.2) | HW: -3.2 (1.0) | |

| A - Agriculture, forestry and fishing | GVA: 6.1 (10.9) | GVA: -2.8 (3.4) | GVA: -0.5 (4.2) | GVA: 0.2 (2.6) | GVA: 1.1 (0.2) |

| PE: 3.0 (-1.3) | PE: -1.4 (-2.3) | PE: -2.8 (-1.3) | PE: -1.5 (0.5) | PE:3.4 (-0.7) | |

| HW: 2.8 (-3.0) | HW: -1.1 (-2.0) | HW: -1.7 (-2.2) | HW: -1.0 (0.3) | HW: 1.3 (-1.4) | |

| B-E - Industry (except construction) | GVA: -1.2 (4.0) | GVA: -0.4 (2.1) | GVA: -5.8 (2.0) | GVA: 5.5 (-0.9) | GVA: -5.2 (1.3) |

| PE: -2.4 (1.5) | PE: -0.4 (0.7) | PE: -4.1 (-0.3) | PE: -0.3 (0.7) | PE: -1.8 (1.5) | |

| HW: -4.0 (0.3) | HW: -1.4 (0.8) | HW: -4.7 (-1.2) | HW: -0.4 (0.5) | HW: -6.1 (0.5) | |

| C – Manufacturing | GVA: -0.3 (6.5) | GVA: -0.9 (2.1) | GVA: -5.0 (0.8) | GVA: -2.5 (1.6) | GVA: -6.3 (1.4) |

| PE: -2.6 (1.5) | PE: -0.7 (0.6) | PE: -5.0 (-0.6) | PE: -1.8 (0.5) | PE: -2.4 (1.4) | |

| HW: -4.5 (0.3) | HW: -1.8 (0.7) | HW: -5.5 (-1.7) | HW: -2.2 (0.1) | HW: -7.4 (0.5) | |

| F – Construction | GVA: 1.2 (1.9) | GVA: 4.1 (-0.4) | GVA: -6.8 (7.6) | GVA: -3.1 (2.9) | GVA: 1.0 (3.7) |

| PE: 1.6 (2.9) | PE: -2.4 (2.1) | PE: -7.3 (8.8) | PE: 0.0 (3.8) | PE: -0.8 (3.6) | |

| HW: 1.7 (1.8) | HW: -2.5 (1.4) | HW: -8.3 (7.6) | HW: -0.5 (2.7) | HW: -4.4 (2.3) | |

| G-I - Wholesale and retail trade, transport, accommodation and food service activities | GVA: -7.6 (3.0) | GVA: -10.1 (2.1) | GVA: -23.8 (2.5) | GVA: -6.3 (1.8) | GVA: -7.6 (1.8) |

| PE: -2.1 (1.7) | PE: -7.5 (1.0) | PE: -14.8 (1.7) | PE: -3.9 (0.4) | PE: -3.9 (1.2) | |

| HW: -6.1 (0.3) | HW: -10.0 (0.8) | HW: -20.2 (1.0) | HW: -6.3 (-0.2) | HW: -6.2 (0.8) | |

| J - Information and communication | GVA: 3.1 (2.7) | GVA: 4.6 (3.8) | GVA: -2.0 (8.4) | GVA: -1.0 (5.4) | GVA: 2.3 (8.6) |

| PE: 1.6 (2.1) | PE: 2.1 (3.8) | PE: -1.2 (0.0) | PE: -2.0 (3.2) | PE: 5.0 (3.1) | |

| HW: 0.6 (1.1) | HW: 1.7 (3.1) | HW: -2.1 (0.2) | HW: -0.6 (2.7) | HW: 4.0 (3.4) | |

| K - Financial and insurance activities | GVA: 3.2 (2.3) | GVA: -1.3 (-0.5) | GVA: 5.8 (4.8) | GVA: 3.4 (2.6) | GVA: 3.2 (2.2) |

| PE: -1.4 (2.3) | PE: -4.0 (0.1) | PE: -3.6 (-1.7) | PE: 2.1 (0.0) | PE: 2.3 (1.6) | |

| HW: -2.3 (1.8) | HW: -3.8 (-0.6) | HW: -3.6 (-2.7) | HW: 2.6 (-0.4) | HW: 1.7 (-0.7) | |

| L - Real estate activities | GVA: 1.5 (2.0) | GVA: 0.7 (2.4) | GVA: 1.7 (3.4) | GVA: 1.2 (1.3) | GVA: 0.6 (4.3) |

| PE: 0.8 (1.3) | PE: 7.5 (1.7) | PE: -6.2 (7.4) | PE: 0.0 (1.1) | PE: 1.6 (2.6) | |

| HW: -0.3 (-0.7) | HW: 5.8 (1.3) | HW: -4.5 (6.5) | HW: 0.0 (0.0) | HW: 0.9 (3.1) | |

| M-N - Professional, scientific and technical activities; administrative and support service activities | GVA: 1.5 (1.0) | GVA: -3.7 (5.7) | GVA: -20.8 (6.0) | GVA: -7.6 (4.8) | GVA: -5.0 (3.0) |

| PE: -1.5 (2.3) | PE: -2.4 (4.4) | PE: -15.5 (4.6) | PE: -3.8 (3.9) | PE: -1.5 (3.1) | |

| HW: -2.5 (1.2) | HW: -3.3 (3.9) | HW: -18.3 (3.3) | HW: -5.7 (3.3) | HW: -3.2 (2.6) | |

| O-Q - Public administration, defence, education, human health and social work activities | GVA: -3.8 (0.7) | GVA: -3.5 (0.6) | GVA: 4.5 (3.9) | GVA: -1.0 (1.4) | GVA: -2.5 (0.1) |

| PE: 0.6 (0.7) | PE: 0.6 (2.1) | PE: 6.2 (3.0) | PE: 0.8 (1.0) | PE: -0.8 (0.8) | |

| HW: -1.5 (0.3) | HW: 0.8 (1.9) | HW: 4.0 (2.2) | HW: 0.0 (1.0) | HW: -1.0 (0.4) | |

| R-U - Arts, entertainment, recreation; oth. service activities; household activ., extra-territorial organizations/bodies | GVA: -18.3 (1.2) | GVA: -8.1 (1.4) | GVA: 0.2 (5.0) | GVA: -25.7 (1.5) | GVA: -5.0 (1.7) |

| PE: -2.0 (1.1) | PE: -4.3 (0.9) | PE: 3.1 (4.0) | PE: -4.5 (3.9) | PE: -3.1 (1.5) | |

| HW: -5.6 (-0.2) | HW: -6.0 (0.1) | HW: -0.7 (2.9) | HW: -6.5 (3.7) | HW: -6.8 (1.1) |

Three broad sectors stand out by being severely negatively impacted in almost all Nordic countries:

- The aggregated sector of Wholesale and retail trade, transport, accommodation and food service activities,

- The aggregated sector of Arts, entertainment and recreation; other service activities; activities of households and extra-territorial organizations and bodies,

- The aggregated sector of Professional, scientific and technical activities; administrative and support service activities - hereunder Travel agency, tour operators and other reservation service and related activities.

All these sectors, and especially the first two, are characterised by being highly dependent on human contact and interaction. For example, lockdown measures had a large impact on the day-to-day operations of retail stores, hotels, restaurants and cafes, as well as on the cultural sectors. While the specific types and levels of restrictions differed across the Nordic countries, such business activities were wholly or partially shut down for periods of time, due to the restrictions.

4.1.1 Sectors with largest negative impacts per country

The national statistical offices provide more detailed information of how the pandemic impacted the various sectors of the Nordic economies. Table 4.2 provides an overview of the three sectors in each Nordic country that experienced the largest negative impact in 2020 compared to 2019.

Accommodation and food service activities were among the most negatively impacted in all Nordic countries. As above these activities are characterised by being highly dependent on human interaction. Similarly, Arts, entertainment and recreation were among the most negatively impacted.

Transportation and storage was also generally negatively affected in all countries. In Norway, this sector was not among the three most affected. Unlike the other Nordic countries, manufacturing was also among the hardest hit sectors in Sweden. For a more detailed description per country, see Appendix C.

Table 4.2 The three sectors in each country with the largest negative impact in 2020 compared to 2019, in terms of Gross Value Added (GVA), Persons employed (PE) and Hours worked (HW).

Source: Statistics Denmark, Statistics Finland, Statistics Iceland, Statistics Norway, and Statistics Sweden.

| Denmark | Arts, entertainment and recreation | Accommodation and food service activities | Transportation and storage |

| GVA | -36.4 | -35.4 | -21.2 |

| Persons employed | -4.6 | -8.7 | -3.5 |

| Hours worked | -11.2 | -19.3 | -7.0 |

| Finland | Accommodation and food service activities | Transportation and storage | Arts, entertainment and recreation |

| GVA | -33.5 | -25.8 | -12.6 |

| Persons employed | -22.2 | -8.7 | -9.4 |

| Hours worked | -25.1 | -11.8 | -9.8 |

| Iceland | Accommodation and food service activities | Administrative and support service activities | Transportation and storage |

| GVA | -50.8 | -38.5 | -35.7 |

| Persons employed | -27.6 | -27.5 | -19.3 |

| Hours worked | -37.3 | -31.3 | -23.7 |

| Norway | Accommodation and food service activities | Arts, entertainment and recreation | Administrative and support service activities |

| GVA | -29.8 | -25.7 | -19.3 |

| Persons employed | -10.9 | -4.5 | -7.9 |

| Hours worked | -21.0 | -6.4 | -11.1 |

| Sweden | Accommodation and food service activities | Manufacturing of motor vehicles | Manufacture of other transport equipment |

| GVA | -29.0 | -17.7 | -14.4 |

| Persons employed | -15.4 | -5.1 | 0.0 |

| Hours worked | -18.5 | -12.3 | -3.4 |

| *Manufacture of motor vehicles, trailers and semi-trailers ** Manufacture of other transport equipment | |||

4.1.2 Åland, Greenland, and the Faroe Islands

For the autonomous region Åland and the autonomous territories Greenland and the Faroe Islands, we do not have access to as detailed data. The number of hotel nights serves as an indicator to the impact on inbound tourism, which is an important industry in these areas. The data reveals significant negative consequences to this sector from 2019 to 2020, and varying degree of recovery in 2021, see Figure 4.1.

Figure 4.1 Number of hotel nights in Åland, Greenland and the Faroe Islands, YTD 2018–2021.

Source: Ålands Statistik- och Utredningsbyrå, Grønlands Statistik, Hagstova Føroya.[1]Based on latest available data for each respective geography.

Footnotes

- ^ Based on latest available data for each respective geography.

The general picture is that the economies of Åland, Greenland and the Faroe Islands faced a significant recession after the outbreak of the pandemic in 2020. However, the recovery in terms of tourism indicators was obvious during the first part of 2021.

Åland experienced the largest decrease in number of hotel nights of the three geographies. In 2020, the number of hotel nights in Åland were 56 percent lower than in 2019. In April 2020, the registered hotel nights in Åland were 94 percent lower than in April 2019. During the most popular tourist month of the year, July, the decrease was 40 percent compared to the year before. The total year-to-date (January-October, latest data available) number of hotel nights in 2021 was 18 percent lower than in 2019. While the number of hotel nights in Åland decreased for almost all nationalities, the decrease was much larger for Swedish visitors. In 2019, Swedish nationals made up 41 percent of the hotel nights in Åland, while in 2020 they only made-up 11 percent. In contrast, visitors from Finland made up 49 percent of the hotel nights in 2019, but 83 percent in 2020. Still, the total number of hotel nights from Finnish nationals decreased by 27 percent in 2020 compared to 2019.

In Greenland, the number of hotel nights decreased by 34 percent in 2020 compared to 2019. As in Åland, April was the month with the largest relative decrease of 83 percent from April 2019. As in Åland, the Greenlandic tourism is still far from its pre-pandemic levels, with the year-to-date (January-September, latest data available) number of hotel nights being 20 percent lower in 2021 than in 2019.

In the Faroe Islands, the number of hotel nights decreased by 43 percent in 2020 compared to 2019. The largest decrease, 90 percent, was in April. Unlike Åland and Greenland, the year-to-date (January-October, latest data available) number of hotel nights in 2021 surpasses that of 2019 by 3 percent. Thus, it appears that the Faroese tourism sector has managed to recover more swiftly than its counterparts in Åland and Greenland.

4.2 Step 2: Identify impact of economic sectors on CO2 emissions

To identify the impact of the economic sectors on CO2 emissions we focus on two measures:

- Sectors’ contribution to total CO2-equivalent emissions

- Sectors’ greenhouse gas emission intensities, e.g., CO2 equivalents per euro of gross value added (GVA)

By combining information on these measures, we find that the following sectors have the largest negative impact on CO2 emissions:

- A - Agriculture, forestry and fishing

- B - Mining and quarrying / D – Electricity, gas, steam and air conditioning supply / E – Water supply, sewerage, waste management and remediation activities

- C - Manufacturing

- F - Construction

- G-I - Wholesale and retail trade, transport, accommodation and food service activities

In the following, we describe in detail the sectors’ contribution to total CO2-equivalent emissions in each country, and the sectors’ greenhouse gas emission intensities.

4.2.1 Sectors’ contribution to total CO2 emissions

The country profiles of greenhouse gas (GHG) emissions, measured in CO2 equivalents, differ across the countries, due to varying size and sectoral composition of the Nordic economies. Furthermore, while there are international standards and instructions for national statistical offices’ reports on CO2 emissions, there are nonetheless differences in how the data is collected and classified.

In 2018 (the latest year where Eurostat presents data on GHG emissions for all Nordic countries[1]Eurostat, Air emissions accounts by NACE Rev. 2 activity [env_ac_ainah_r2].) Denmark reported the highest total emissions of GHG, at 81 mill. tonnes[2]More than half (56 percent) of total Danish GHG emissions emanate from the transport sector. 90 percent of those emissions originate from international transport by Danish ships, airplanes, and vehicles (e.g., international shipping with Danish flagged ships).. Iceland was the Nordic country with lowest total GHG emissions, at 7 mill. tonnes. Emissions from Norway amounted to 69 mill. tonnes, from Finland 54 mill. tonnes, and from Sweden 48 mill. tonnes.

Figure 4.2 presents the relative distribution of GHG emissions per sector in each country, measured as GHG emissions per sector as share of total GHG emissions, excluding GHG emissions from households. We have only included the four most emitting sectors for each country in the figure, the rest are summed into the category “other sectors”.

As the figure shows, there are some relatively marked differences in the sectoral composition of the GHG emissions across the countries. The transportation and storage sector (H) is a large source of emissions in all Nordic countries, but especially so in Denmark. The agricultural sector (A) is also amongst the 4 most emitting sectors in all Nordic countries. So is manufacturing, but to a varying degree. Not surprisingly mining and quarrying (B) is the second most emitting sector after transport in Norway, due to petroleum production. For more details by country, see Appendix D.

Footnotes

- ^ Eurostat, Air emissions accounts by NACE Rev. 2 activity [env_ac_ainah_r2].

- ^ More than half (56 percent) of total Danish GHG emissions emanate from the transport sector. 90 percent of those emissions originate from international transport by Danish ships, airplanes, and vehicles (e.g., international shipping with Danish flagged ships).

Figure 4.2 Share of total emissions of greenhouse gases from economic activity, CO2 equivalents, by sector and country, 2018. Four largest emitting sectors specified per country. The rest are under “Other sectors”.[1]For a more detailed description of emissions per sector, see Appendix C.

Footnotes

- ^ For a more detailed description of emissions per sector, see Appendix C.

4.2.2 Sectors’ greenhouse gas emission intensities

Sectoral emission intensities measure the sector’s emissions with respect to its economic size. This allows for comparison of GHG emissions across sectors and countries, see Table 4.3. We measure emission intensities by emissions of greenhouse gas (GHG) measured in CO2 equivalents per euro of gross value added (GVA).

The weighted average emission intensity of the Nordic economies is 212 grams of GHG emissions per euro of GVA, in 2017.[1]The latest year with available Eurostat data on emission intensity across sectors for all Nordic countries Iceland has the highest average emission intensity, with 353 grams of GHG emissions per euro of GVA, i.e., almost two thirds higher than the Nordic average. Sweden has the lowest average emission intensity, with 114 grams of GHG emissions per euro of GVA, i.e., almost half of the average Nordic emission intensity.

Footnotes

- ^ The latest year with available Eurostat data on emission intensity across sectors for all Nordic countries

Table 4.3. GHG emission intensity, grams of GHG emissions (CO2 equivalents) per euro of GVA, by sector and country, 2017.[1]Note: J-U: All other sectors, such as information and communication, finance and insurance, professional services, arts and entertainment, etc. The emission intensity for sector J-U is calculated as the simple average for all these sectors, per country. All these sectors have very low emission intensities: the highest emission intensity is 43 percent lower than the national average (the Norwegian “Other service activities” sector).

Source: Eurostat, Air emissions intensities by NACE Rev. 2 activity

Footnotes

- ^ Note: J-U: All other sectors, such as information and communication, finance and insurance, professional services, arts and entertainment, etc. The emission intensity for sector J-U is calculated as the simple average for all these sectors, per country. All these sectors have very low emission intensities: the highest emission intensity is 43 percent lower than the national average (the Norwegian “Other service activities” sector).

| Lower emission intensity than the national average | Average emission intensity for each country | 0 to 99 percent higher emission intensity than the national average | 100 percent or higher emission intensity than the national average |

| NACE | Denmark | Finland | Iceland | Norway | Sweden |

| TOTAL - Total - all NACE activities | 308 | 270 | 353 | 221 | 114 |

| A - Agriculture, forestry and fishing | 3.265 | 1.572 | 1.377 | 765 | 1.318 |

| B - Mining and quarrying | 618 | 469 | 65 | 301 | 430 |

| C – Manufacturing | 156 | 347 | 1.040 | 548 | 239 |

| D - Electricity, gas, steam and air conditioning supply | 2.390 | 3.861 | 222 | 272 | 711 |

| E - Water supply; sewerage, waste management and remediation activities | 1.251 | 1.338 | 1.459 | 913 | 611 |

| F – Construction | 110 | 95 | 137 | 101 | 64 |

| G - Wholesale and retail trade; repair of motor vehicles and motorcycles | 34 | 28 | 47 | 42 | 35 |

| H - Transportation and storage | 3.110 | 1.131 | 2.262 | 1.775 | 414 |

| I - Accommodation and food service activities | 34 | 59 | 7 | 29 | 10 |

| J - U (see table note) | 14 | 19 | 14 | 14 | 12 |

In all Nordic countries, three sectors stand out by being more than twice (i.e., more than 100 percent) as emission intensive compared to the national average: 1) agriculture, forestry and fishing, 2) transportation and storage, and 3) water supply, sewerage, waste management and remediation activities. More details per country can be found in Appendix E.

For three other sectors, there are at least two Nordic countries where the sectors’ emission intensities are more than twice as high as the national average: 1) mining and quarrying, 2) manufacturing, and 3) electricity, gas, steam, and air conditioning supply.

Emission intensity in transport

The aggregated sectoral analysis conceals important variation within the sector. This is especially relevant in the transport sector. A study from the European Environment Agency (EEA)[1](European Environment Agency, 2021b) shows a clear hierarchy of passenger and freight transport modes based on historical averages for the EU-27. Based on this study, passenger flights and passenger cars have clearly higher CO2 emissions per passenger kilometre than busses, ferries, and trains. The same hierarchy applies for freight transport, with air cargo and heavy goods vehicles having the highest emissions per tonne kilometre.

Footnotes

- ^ (European Environment Agency, 2021b)

4.3 Step 3: Identify impact of economic sectors on the environment

There is no common unit for environmental outcomes, and we need to use other indicators to identify sectors that positively or negatively impact the environment.

The environmental state is closely linked to land and water use. Economic sectors that require land or water are thus expected to have a more negative impact on the environment compared to other sectors. To identify which sectors are relevant it is useful to consider the main factors of production in each sector. The production factors are broadly defined as land, labour, capital or entrepreneurship, where land includes water and other natural resources. Further, it is relevant to identify pollution intensive sectors.

Our assessment of the environmental impact by sector is presented in Table 4.4. The assessment of land and/or capital intensity is based on a qualitative assessment, while statistics are used to assess the impact on local air pollution[1]We have looked primarily at impact on nitrogen oxides, particulates < 2.5µm, and particulates < 10µm..

Footnotes

- ^ We have looked primarily at impact on nitrogen oxides, particulates < 2.5µm, and particulates < 10µm.

Table 4.4. Economic sectors (Nace Rev. 2) that are land- and/ capital-intensive.

Source: Qualitative assessment and Eurostat air emissions accounts by NACE Rev. 2 activity

| Sector (Nace Rev. 2) | Land- and/or -capital intensive | Source of local air pollution |

| A - Agriculture, forestry and fishing | Yes | Yes |

| B-E - Industry (except construction and manufacturing)* | Yes | Yes |

| C – Manufacturing | Yes | Yes |

| F – Construction | Yes | Yes |

| G-I - Wholesale and retail trade, transport, accommodation and food service activities | Partly | Partly |

| J - Information and communication | No | No |

| K - Financial and insurance activities | No | No |

| L - Real estate activities | No | No |

| M-N - Professional, scientific and technical activities; administrative and support service activities | No | No |

| O-Q - Public administration, defence, education, human health and social work activities | No | No |

| R-U - Arts, entertainment and recreation; other service activities; activities of household and extra-territorial organizations and bodies | No | No |

| *The B-E - Industry (except construction and manufacturing) includes B- Mining and quarrying, D – Electricity, gas, steam and air conditioning supply and E - Water supply, sewerage, waste management and remediation activities. | ||

The sector A- Agriculture, forestry and fishing requires considerable land and water resources, thus impacting the environment negatively. Negative impacts may include soil degradation and water depletion, which further impact biodiversity. The sector is also a major source of air pollution, even though the air pollution levels vary within the Nordic countries. This is most likely explained by differences in both the size of sector and type of produce.