- Frontpage

- Table of contents

- Executive summary – English

- Introduction

- Legal framework and relevant initiatives

- Today’s practive regarding lithium-ion batteries

- Sustainability of batteries

- Key barriers towards increased circularity today

- Best practice and design for increased circularity

- Policy recommendations

- Executive summary – Danish

- Introduktion

- Lovmæssige rammer og relevante initiativer

- Nuværende praksis vedrørende lithium-ion batterier

- Bæredygtighed af batterier

- Vigtigste barrierer mod øget cirkularitet

- Best practice og design for øget cirkularitet

- Anbefalede politik-muligheder

- 1 Introduction

- 1.1 Introduction to the study

- 1.2 Background

- 1.3 This report

- 2 Legal framework and relevant initiatives

- 2.1 EU legislation and initiatives

- 2.2 National legislation

- 2.3 Other initiatives

- 2.4 Standardisation

- 2.5 Discussion on the legal framework

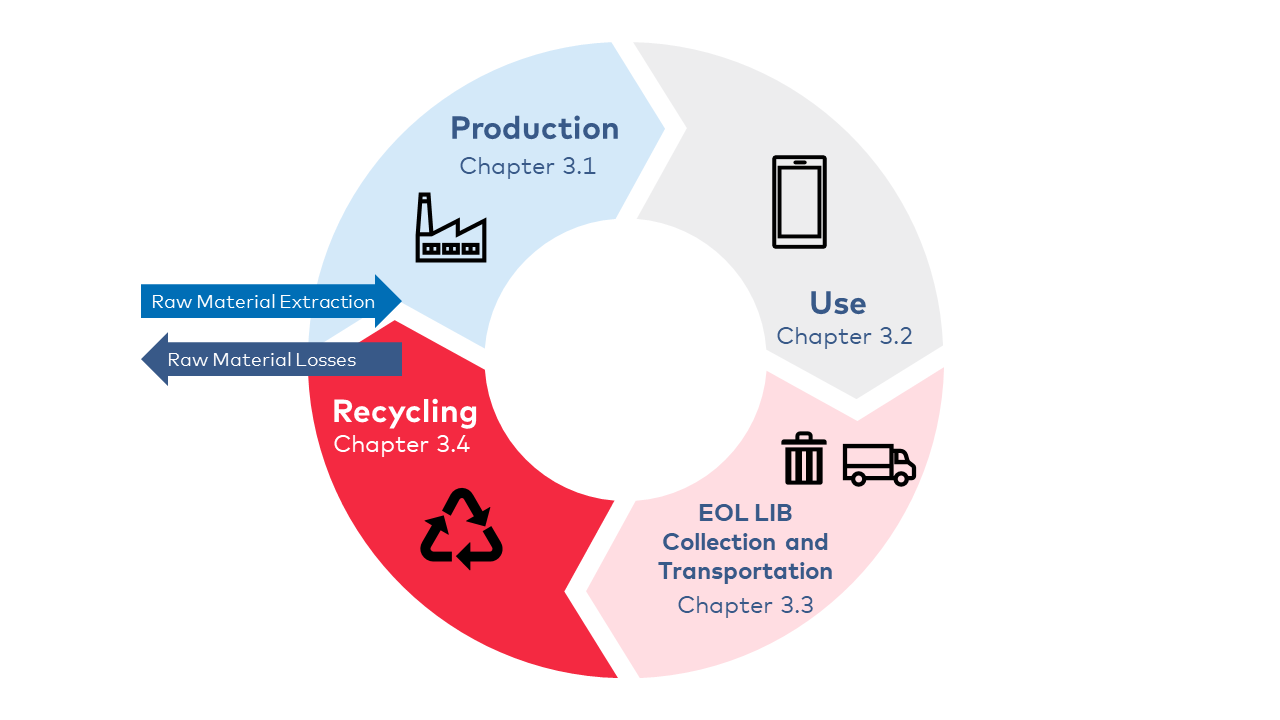

- 3 Today's practice regarding lithium-ion batteries

- 3.1 Production

- 3.2 Use

- 3.3 End of life LIB collection and transportation

- 3.4 Recycling

- 4 Sustainability of batteries

- 4.1 People

- 4.2 Planet

- 4.3 Prosperity

- 5 Key barriers towards increased circularity today

- 5.1 Company culture

- 5.2 Lack of circular design

- 5.3 Legislation

- 5.4 Lack of consumer awareness

- 5.5 Virgin vs recycled materials

- 5.6 The black battery markets and illegal exports

- 6 Best practice and design for increased circularity – handbooks

- 6..1 Introduction

- 6.2 Handbook of best practice for business

- 6.3 Handbook of best practice for consumers

- 7 Recommended policy options – policy brief

- 7.1 Policy recommendations for the Nordic countries to improve circularity of batteries and equipment

- 7.2 Policy recommendations for the Nordic countries to contribute to creating needed framework conditions

- ANNEX A: Interviewees and organisations referenced

- Manufacturing industry

- Recycling industry

- Miscellaneous

- ANNEX B: Prefered options IA

- About this publication

MENU

Contents

This publication is also available online in a web-accessible version at https://pub.norden.org/temanord2022-523.

Executive summary – English

Introduction

The overall aim of this project is to promote the Nordic countries as a forerunner region in demanding and using sustainable design of consumer electronics, and to identify key opportunities, barriers and challenges in the transition towards a more sustainable use of battery technologies, including the transport sector. The aesthetics of the design should meet with the overall sustainability: high quality, durability and smart assembly for refurbishing.

The project is funded by the Nordic Working Group for Circular Economy (NCE) un-der the Nordic Council of Ministers. The project has been carried out by Viegand Maagøe A/S (Denmark) and IVL Swedish Environmental Research Institute (Sweden) in the period 20 October 2020 to 31 December 2021.

A reference group with representatives from the Nordics has been established, who provided valuable input to the study.

Legal framework and relevant initiatives

EU legislation and initiatives have a direct or indirect influence in the Nordics on batteries and the products containing batteries.

The proposed new battery regulation to replace the Battery Directive is expected to become an important driver for the circularity of batteries and for minimising the negative environmental impact of batteries. The current Battery Directive applies to all batteries placed on the market within the European Union and establishes objectives and targets (e.g. on collection and recycling); specifies measures (such as phasing out mercury or establishing national schemes for collection) and enables actions (e.g. reporting or labelling) to achieve them.

The directive has been the EU’s best tool in ensuring recycling and beneficial environmental handling of batteries on the European market and have therefore also impacted the Nordic Member States’ handling of batteries. Still, the directive does not ensure that all batteries are properly collected and recycled at the end of their life, increasing the risk of releasing hazardous substances and wasting valuable and critical resources. Also, the existing directive does not fully grasp the intentions of the circular economy. Therefore, a new battery regulation was proposed repealing the existing directive to better reflect circularity, improve sustainability, and keep pace with technological developments.

The proposed Battery Regulation (published on 10 December 2020) includes:

- introduction of a new category of electric vehicle batteries, alongside the existing portable, automotive and industrial battery classes;

- progressive requirements to minimise the carbon footprint of EV batteries and rechargeable industrial batteries: a carbon footprint declaration requirement, applying as of 1 July 2024, complemented by classification in a carbon footprint performance category and related labelling (as of 1 January 2026); and a requirement to comply with maximum lifecycle carbon footprint thresholds (as of 1 July 2027);

- a recycled content declaration requirement, which would apply from 1 January 2027 to industrial batteries, EV batteries and automotive batteries containing cobalt, lead, lithium or nickel in active materials. Mandatory minimum levels of recycled content would be set for 2030 and 2035 (i.e. 12% cobalt; 85% lead, 4% lithium and 4% nickel as of 1 January 2030, increasing to 20% cobalt, 10% lithium and 12% nickel from 1 January 2035, the share for lead being unchanged);

- minimum electrochemical performance and durability requirements for portable batteries of general use (applying from 1 January 2027), as well as for rechargeable industrial batteries (from 1 January 2026). The Commission would assess the feasibility of phasing out non-rechargeable portable batteries of general use by the end of 2030;

- a new obligation of battery replaceability for portable batteries; safety requirements for stationary battery energy storage systems;

- supply chain due diligence obligations for economic operators that place rechargeable industrial batteries and EV batteries on the market. For this requirement on responsible raw material sourcing (as well as for those related to the carbon footprint and the recycled content levels), the Commission proposal envisages mandatory third-party verification through notified bodies;

- increased collection rate targets for waste portable batteries, excluding waste batteries from light means of transport (65% by the end of 2025, rising to 70% by the end of 2030);

- as regards recycling efficiencies, increased targets for lead-acid batteries (recycling of 75% by average weight of the lead-acid batteries by 2025, rising to 80% by 2030) and new targets for lithium-based batteries (65% by 2025, 70% by 2030). The proposed regulation also envisages specific material recovery targets, namely 90% for cobalt, copper, lead and nickel, and 35% for lithium, to be achieved by the end of 2025. By 2030, the recovery levels should reach 95% for cobalt, copper, lead and nickel, and 70% for lithium;

- requirements relating to the operations of repurposing and remanufacturing for a second life of industrial and EV batteries;

- labelling and information requirements. From 1 January 2027, batteries should be marked with a label with information necessary for the identification of batteries and of their main characteristics. Various labels on the battery or the battery packaging would also provide information on lifetime, charging capacity, separate collection requirements, the presence of hazardous substances and safety risks. Rechargeable industrial batteries and EV batteries should contain a battery management system storing the information and data needed to determine the state of health and expected lifetime of batteries. This system should be accessible to battery owners and independent operators acting on their behalf (e.g. to facilitate the reuse, repurposing or remanufacturing of the battery);

- the setting up, by 1 January 2026, of an electronic exchange system for battery information, with the creation of a battery passport (i.e. electronic record) for each industrial battery and EV battery placed on the market or put into service;

- envisaging of the development of minimum mandatory green public procurement criteria or targets.

The Ecodesign Directive establishes a framework for setting ecodesign requirements on energy-related products such as household appliances, consumer electronics and information and communication technologies. In recent years, a set of resource efficiency requirements have been implemented in the Ecodesign product regulations including requirements on disassembly for repair and reuse and for products’ built-in batteries. These include the regulations on computers and on enterprise and data centre servers and storage products and proposed requirements in the working documents for smartphones and tablets. These requirements can be highly relevant for circularity of the batteries themselves and also for extending the lifetime of the products using built-in batteries due to longer battery lifetime and possibility for easy replacement of the batteries.

Green Public Procurement (GPP) criteria for computers, monitors, tablets and smartphones include requirements for built-in batteries related to product lifetime extension, energy consumption, hazardous substances, end-of-life management and refurbished/remanufactured products. Setting such requirements to batteries should create an economic incentive to produce and sell batteries with a longer lifetime. GPP also provides incentives to produce batteries with a high endurance and quality by making sure they are tested according to international standard i.e. EN 61960-3:2017.

Other relevant legislations include:

- The Waste Electrical and Electronic Equipment (WEEE) Directive

- EU List of Waste

- The Regulation on shipments of waste

- The Regulation on CE marking

- The Restriction of Hazardous Substances (RoHS) Directive

- The Regulation on Registration, Evaluation, Authorisation and Restriction of Chemicals (REACH)

- The EU Conflict Minerals Regulation

Additional to the legislative initiatives, important other initiatives include the 2021 Industrial Strategy Update, where one strategic area is lithium-ion batteries (LIBs); and the Strategic Action Plan to develop a European battery value chain embracing raw materials extraction, sourcing and processing, battery materials, cell production, battery systems, as well as re-use and recycling. Furthermore, the European Com|mission supported the establishment of the The European Battery Alliance (EBA).

Finally, EU has funding schemes for research, pilots, demonstrators, scale-up and roll-out in batteries, such as Horizon 2020, Horizon Europe, the Innovation Fund and Important Projects of Common European Interest (IPCEI).

Today’s practive regarding lithium-ion batteries

Production

LIB production is very complex and involves several steps, from mining to battery pack production. Extraction of metals occurs in different parts of the world; however, China is currently dominating cell production including cathode and anode production. Some raw materials are critical (high supply risks and very economic important) for EU including cobalt, graphite and lithium.

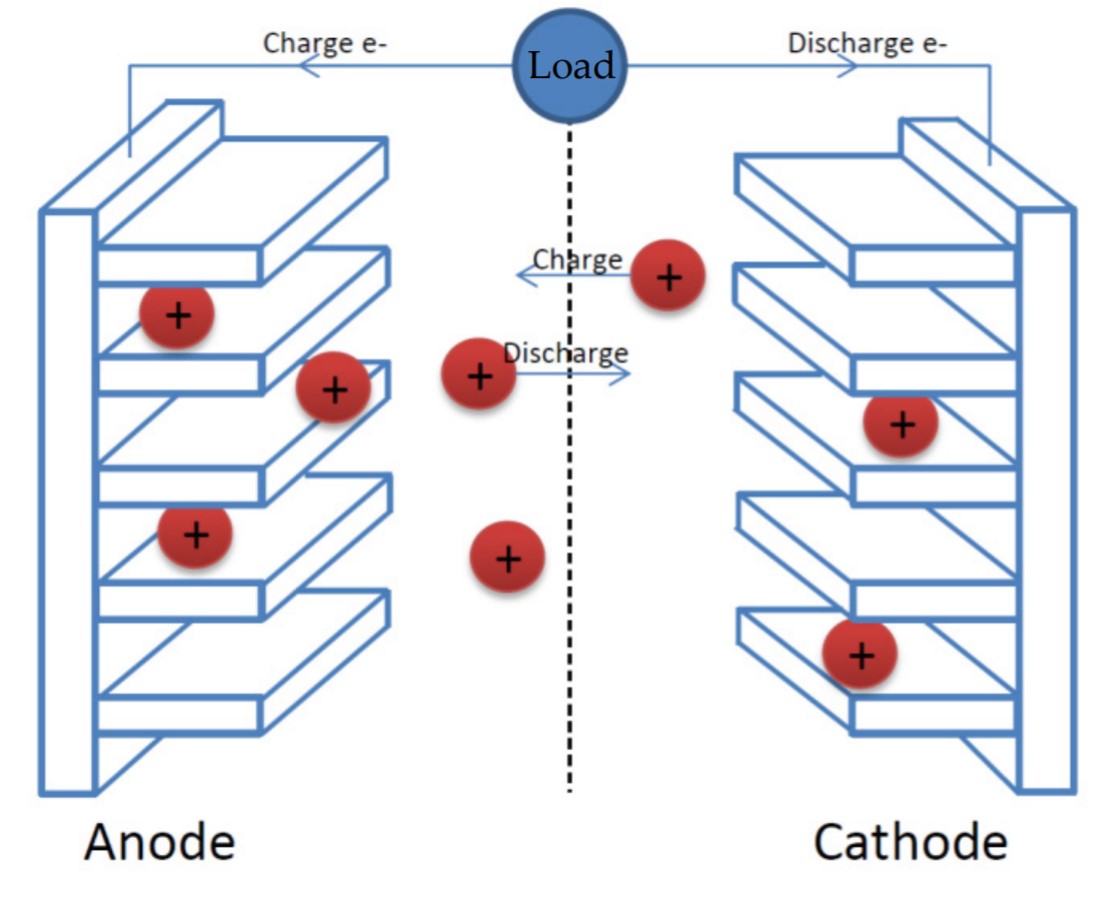

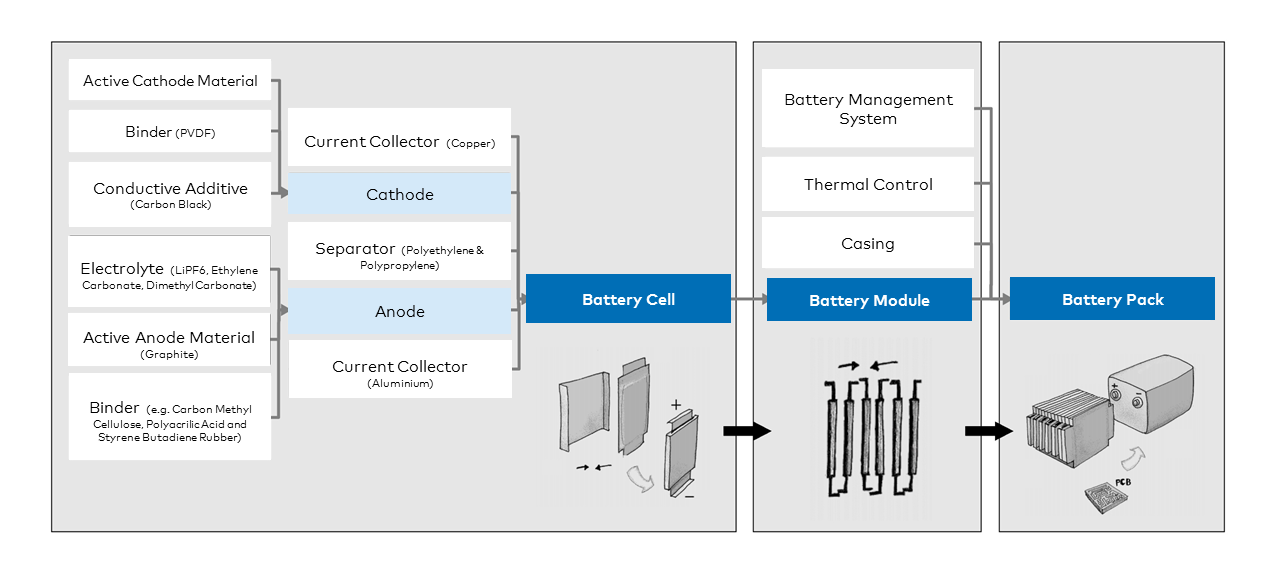

Metals are mined for the cathode and they are refined to sulphates or in the case of lithium, sometimes used as hydroxide. After mining and refining, the active cathode material is produced. The extraction of metals is highly impacting the environment and people working and living near the extraction sites. The battery cell is constructed with the anode, cathode, electrolyte, separator, plastics, steel, copper and aluminium. The cathodes are made of different chemistries depending on the application and the anode is usually based on graphite with the exception of LTO chemistry.

The trends for coming years for the battery chemistries in products is not only relevant for the raw material required at the production, but also for the volumes of batteries entering recycling. This is because the chemistries determine the amount of specific raw materials (e.g., cobalt and nickel), which can be recovered.

There is much research going on for new chemistries, and the main drivers are energy density increase to increase the range for cars, to reduce costs and to reduce the need for critical raw materials such as cobalt.

The key market sectors in the EU for LIBs are automotive and to a smaller extent portable device. The growth for markets sold in each market in the coming 10–15 years will probably mainly be on the automotive side. Sales for pure electric (BEV) passenger cars are dominating the growth. Other important products - which are growing considerably up to 2030 - are passenger car PHEVs, busses, and LCV (light commercial vehicles). Also batteries in power tools and tablet and smartphones have been sold more and will continue to increase until 2030.

Use

The main use is for automotive application and the second largest use is for portable devices, assuming that the pattern seen in Europe also applies for the Nordics.

For some usages, for example for power tools, high power and thus high C-rate (high current) is needed from the battery, but the energy storing capacity may be lower. Since it varies how much time people use the tool per use, the battery is often one-dimensional for private use.

For portable batteries for portable electronics such as smartphones, laptops, tablets, loudspeakers, the batteries are built-in and laymen often may not be able to replace them; especially for waterproof products.

Especially for replaced automotive batteries, typically, the batteries still have energy capacity left, which give opportunities for refurbishment or remanufacturing and achieving a second life in vehicles or in other application e.g. for energy storage in buildings or as electric grid support. As long as there is a market and a value of these second life batteries, a larger part of the technical lifetime of the batteries are likely to be achieved before scrapped.

For EV batteries, it is common to send for a second life for industrial or commercial energy storage. In Sweden for example, many used EV batteries are sent to the real estate market and used in the rooftops of buildings to store energy produced by solar panels. For electronic devices, the main approach currently is to fully replace the batteries with new ones rather than to repair old batteries.

End of life

After the user is no longer using the product and wants to scrap it, the ownership of the battery becomes of high importance. The Extended Producer Responsibility (EPR) for batteries means that the company placing the batteries on the market is responsible for their collection when they are scrapped by the consumer.

There are no legal requirements for the owner of a battery to send it for recycling when it is no longer used by the consumer, which is why many end-of-life batteries for consumer electronics may stay in with the original owner for many years instead of getting recycled. For EV batteries, like LFP batteries, batteries may be disassembled from buses and left in storage indefinitely until a purpose for them is found.

Many small batteries are not collected for battery recycling because they are integrated into the device and cannot be disassembled. They may therefore end up in electronic (WEEE) recycling instead where there is only little chance for the battery metals to be recycled.

EV batteries are supposed to be removed during the pre-treatment process to comply with the ELV Directive (Directive on end-of-life vehicle), and the percent of batteries for which it takes place should be high as it directly correlates with the stock available for the recycling industry.

Recycling

There is a lot of variation when it comes to recycling between what types of recycling is performed and what actors are involved. Even within the bigger recycling categories, such as hydrometallurgy or pyrometallurgy, there can be major differences in how companies perform the recycling. Differences that different actors in the recycling chain choose may include: what metals and other materials are recovered, what percentage of cobalt/nickel/lithium/manganese are recovered, what type of solvents are used in hydrometallurgical recycling and what type of pretreatment is done.

The main categories of recycling today are hydrometallurgical or pyrometallurgic with subsequent hydrometallurgy. Both have different pros and cons with regard to costs, recovery efficiency, flexibility/adaptability to different battery chemistries, the need for a disassembly step, and energy use.

Pyrometallurgy means heating of batteries to smelt the metals while hydrometallurgy uses acids or bases for dissolving them. But first dismantling of parts and other pre-treatments need to be done. For hydrometallurgical recycling knowledge about the cathode chemistry is important why it is recommended to clearly mark the battery with this information, perhaps with electronic tags to facilitate sorting.

In battery recycling, the chemistry of the electrodes matters, especially the cathode. Most of the value is found in the cathode, which is where valuable metals such as cobalt, nickel, and lithium are found. Mobile phones, tablets and computers use Li-ion batteries with high-quality Co content (>12%), and this high Co concentration means that it is profitable both for the producers of these products and the recyclers to try to recycle the metals in these batteries. On the other hand, tool batteries usually contain around 6%, which is why it is not as profitable to handle (recyclers typically do not pay for these batteries but charge a fee for recycling them).

Currently, the volumes of batteries are not sufficient for hydrometallurgy of black mass in the Nordics. There are also other challenges that have to be overcome for a functioning LIB recycling.

The current battery directive does not place specific limitations on the recycled con-tent of lithium-ion batteries, meaning that recyclers would usually recycle the easiest-to-recycle or most valuable materials. The proposal for the new regulation will likely require recyclers to introduce different methods of recycling in order to adjust the percentage of metals which are recovered.

One problem when reducing cobalt in the batteries is that the value for the recycler is reduced. LFP is therefore not recycled at all in Europe at the moment. This obstacle may be mitigated by the proposed battery regulation with its proposed recovery rates of cobalt, lithium and nickel as well as the proposed recycled contents in the production of new batteries. The proposed directive will also force the companies in the bat-tery supply chain to be more transparent regarding ensuring recyclability (enabling disassembly).

Sustainability of batteries

Some may consider sustainability as another wording for environmental development, while others also consider the economic and social impacts. However, regarding batteries, it is important to consider all aspects of sustainability, as battery technology is a key cornerstone in the green transition towards a fossil-free society by replacing products, appliances, and transport means that requires fossil fuels.

It is important to consider all aspects of sustainability, which is in line with the Sustainable Development Goals (SDGs) that aims to: "ensure all human beings can enjoy prosperous and fulfilling lives and that economic, social, and technological progress occurs in harmony with nature." Sustainability and sustainable development are often referred to as the three Ps (People, Planet, and Prosperity).

People: There are significant social and environmental consequences in connection with the extraction of several of the raw materials in lithium-Ion batteries, particularly regarding conflict minerals. Minerals are considered conflict minerals if they are sourced from politically unstable areas and where the minerals trade can be used to finance armed groups, fuel forced labour and other human rights abuses, and support corruption and money laundering. There are several primary raw materials used to manufacture lithium-Ion batteries, which can have adverse impacts on its entire value chain. Cobalt is the most problematic raw material of all listed raw materials, as it is mined mainly in countries with poor regulation and disorganized small-pits i.e. mining by hand using rudimentary and basic tools, often without adequate protective equipment. Over 50 percent of the world's cobalt is mined in the DRC (Democratic Republic of the Congo).

Planet: Batteries impact the environment both positively and negatively and environmental impact affects people. Both the pros and cons need to be considered in connection with the increased demand for different types of batteries to avoid rebound effects. The greenhouse gas emissions of producing a battery is about the same as the rest of the car itself, and thus the greenhouse gas emissions from production of an electric car are about twice as much as they are for a car that runs on only an internal combustion engine. In other impacts categories, it is clear that an electric car also produces significantly higher emissions of other types during the production.

Prosperity: Many of the Sustainable Development Goals aim to improve various areas related to the environment, people, and economic opportunities. Economic opportunities aim to provide decent work such as safe working conditions, living wages, compassionate leadership, and economic growth for those in specific communities. From a more strictly company perspective, the economic part is, of course, important. If a company has a deficit, it cannot continue to operate unless it somehow makes a turnaround. A company can focus on social and environmental impacts, but if they do not make any money, they cannot continue their liveable work (social and environ-ment).

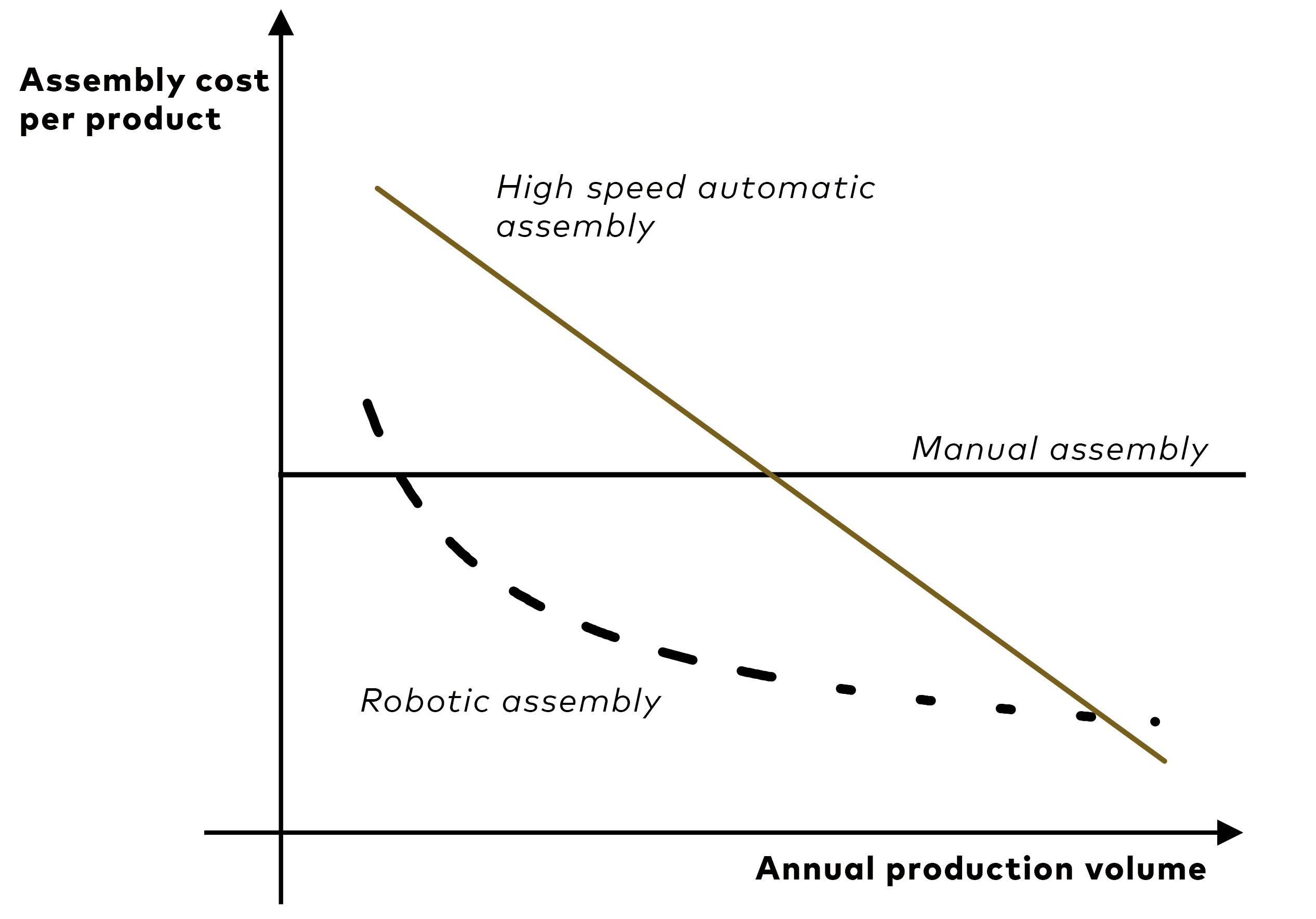

To ensure sustainability, the solution must be economically viable. Previously, companies were focused on profits obtained through a linear business model where higher sales equalled higher profits. The high-speed automatic assembly favours linear business models. Sustainability is a business approach to creating long-term value by considering how a given organization operates within the three Ps (People, Planet and Prosperity).

Sustainability is built on the assumption that developing such strategies foster company longevity. Without a focus on sustainability, it can be questioned how long the company can continue to operate as the expectations on corporate responsibility increases. Transparency becomes more prevalent, and more companies recognise the need to act on sustainability. Professional communications and good intentions are no longer enough as green claims are investigated, and greenwashing will hurt the reputation of the company.

Without a broad focus on sustainability, it may become increasingly difficult for companies to compete in the market. These considerations may increase the focus on the Nordics as a suitable place for production, as the green energy supply can help companies fulfil their sustainability goals and increase their market value.

Key barriers towards increased circularity today

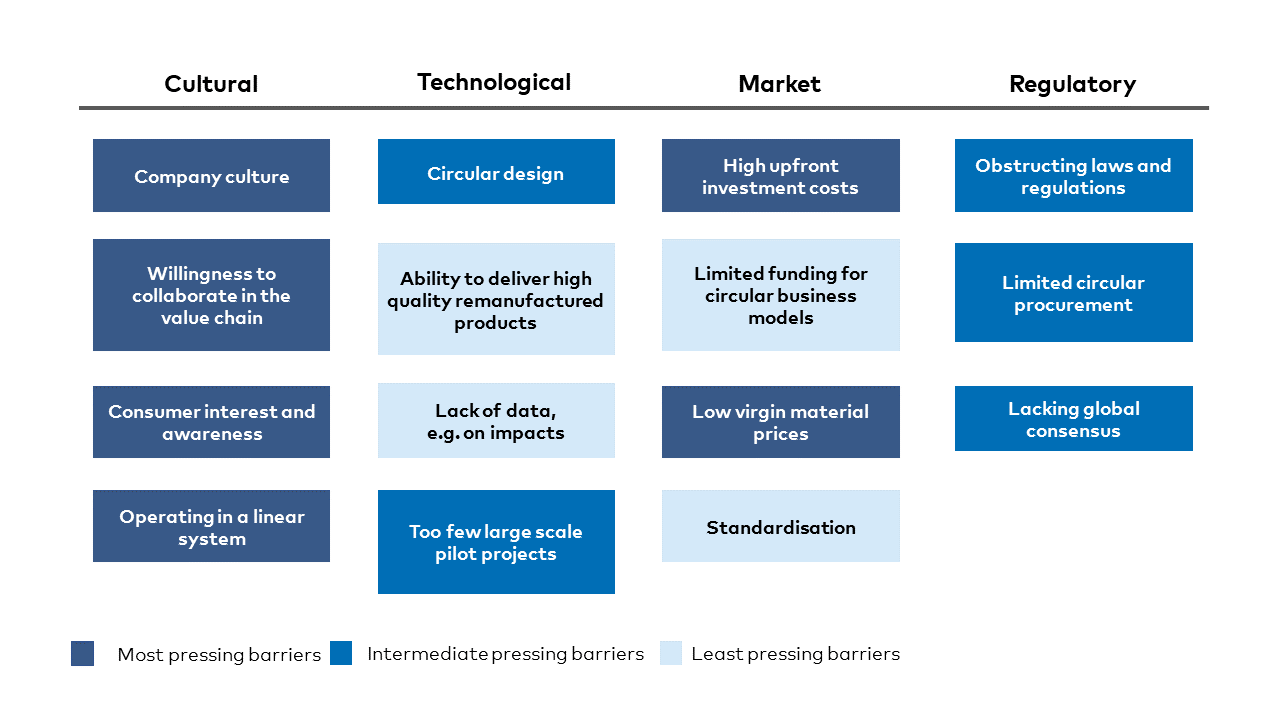

Though there are numerous possibilities and advantages to the circular economy, still several barriers limit the increase in circularity. Key barriers include:

- Company culture, which often can be a major obstacle regarding shifting from a well-established linear economy to circular economy, changing the mindset of consumers, involving full-life-cycle collaboration, and changing mindsets within companies.

- Lack of circular design opportunities especially within the electronics and batteries due to the complexity of small components and compact products, which makes dismantling tricky for the recyclers or refurbishers and because batteries have varying dimensions, forms, and compositions of chemicals and metals, making it challenging to establish an efficient standardised system for battery recycling.

- Lack of legislation, which can inhibit CE, however the Nordics and EU are still ahead due to national regulation and coming EU legislation on batteries.

- Lack of consumer interest and awareness because some consumers simply like new items before their old ones are worn out, which is particular for trend-based, hi-tech and fast-paced products, such as mobile phones, which discourages manufacturers from making robust and more expensive products, as there is less market demand for such product for some product segments.

- Low raw material prices because the fluctuating price of raw materials, like plastics or metals, hinders the economic incentive for purchasing recycled materials, when there are low raw material prices. This further discourages investments in improving the current recycling systems which could help reducing the prices of regenerated resources. Furthermore, some primary raw materials are subject to subsidies making the market price of recycled materials even more unfavourable.

- Black battery market and illegal exports, because between 30 and 40 percent of the EVs are exported before the end of their lifes but the degree of illegal export is unknown because data on illegal export of WEEE is minimal. This leads to circularity challenges that include the batteries ending up for recycling in other parts of the world resulting in increased emissions for transportation, less efficient recycling facilities thus lower output quality, and lastly a reduced amount of recycled materials for the Nordic battery production industry.

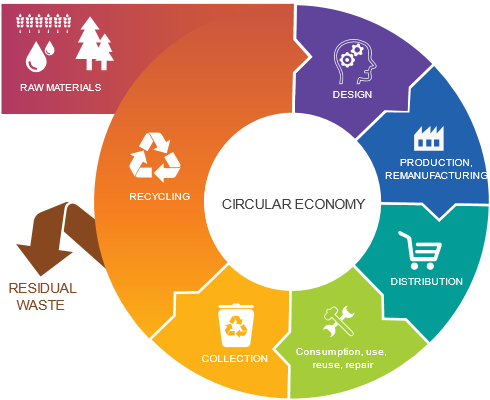

Best practice and design for increased circularity

In this section, content is provided for separate handbooks for businesses and for consumers on best practice and design for increased circularity. For businesses, inspiration from concrete case examples is provided, while for consumers, advices on what they can do when purchasing and using the products.

For businesses

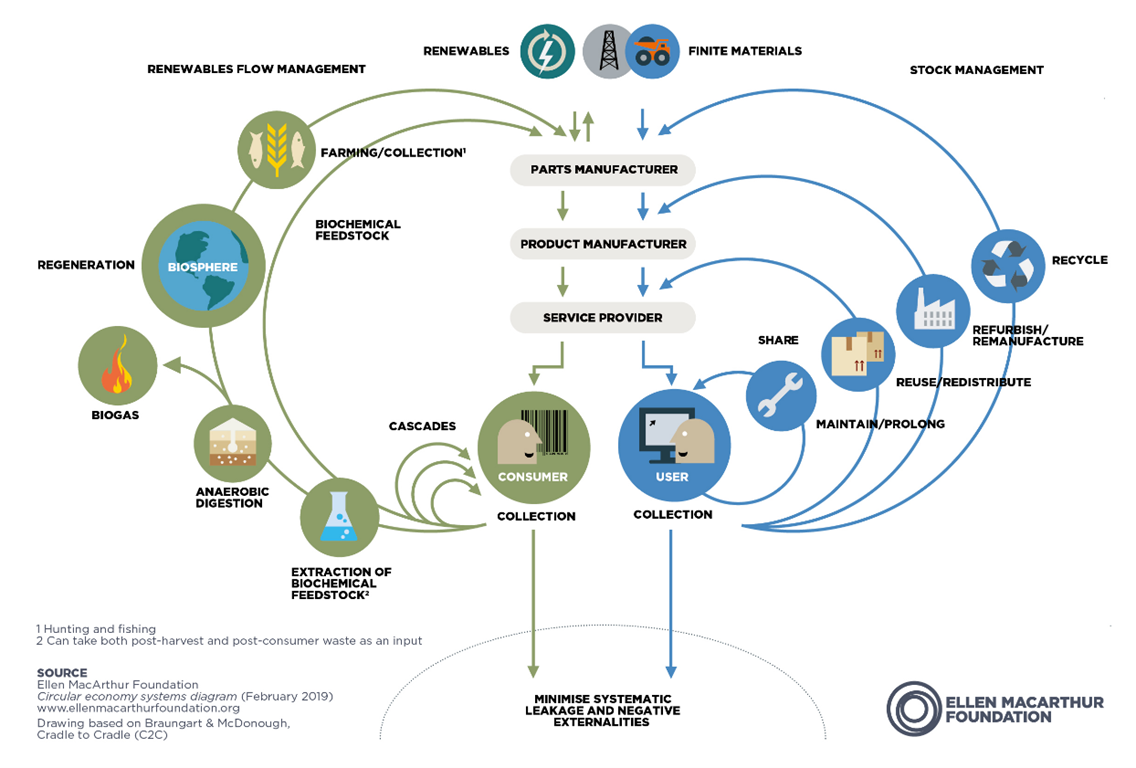

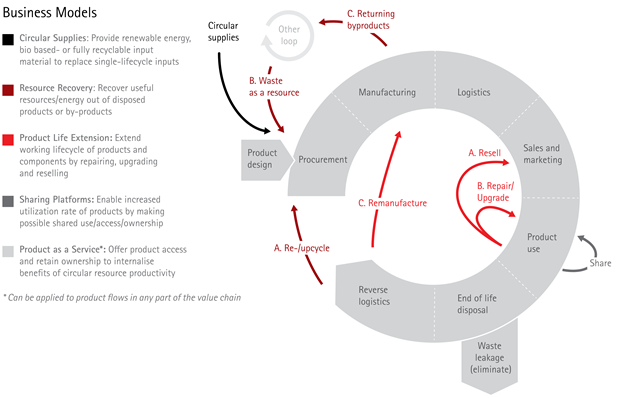

Many businesses are currently exploring the countless possibilities of working with circularity of batteries and battery-driven products through new business models and improved ways of using the batteries more efficiently. To unlock these innovative business potentials, new practices are needed in procurement, design and production departments. The handbook contains inspiration for businesses for establishing these new practices. The basis for the inspiration topics is an evolution of the Ellen MacArthur Foundation’s model, where the focus on business models is stronger.

Five business model types have been explored and case examples have been provided of companies that have adopted these approaches and initiatives that consumers can apply to support the circular economy of batteries. The models cover:

- Circular supplies that describe how to support sustainability and circular economy looking upstream in the value chain and demanding sustainable materials.

- Resource recovery that describes actions that can ensure reuse and recycling by applying actions downstream in the value chain.

- Product life extension that includes all the actions consumers and manufacturers can apply to increase the lifespan of products and components during the use phase.

- Sharing platforms that help to decrease the need for products by effectively sharing fewer amenities among more users.

- Products as a service where product ownership is never transferred to the consumer thus supporting maintenance, product life extension, and resource recovery.

For consumers

Consumers can support the development towards circularity of batteries and battery-driven products through new business models and improved ways of using the batteries more efficiently via their purchases and at the same time achieve economic benefits for themselves and help protecting the environment.

The handbook describes the principles behind circular design to better understand the following best practice recommendations and suggest what consumers can do via their action at the purchase situation and during use of the purchased products.

Circular ways to buying, using and disposing batteries are presented together with case examples of companies that have adopted circular initiatives within the five business model types described above. The models cover:

- Circular supplies that describe circularity in the materials that go into the products.

- Resource recovery that describes actions that can ensure reuse and recycling of batteries.

- Product life extension that includes all the actions that can increase the lifespan of battery products and components during the use phase.

- Sharing platforms that help to decrease the need for products by effectively sharing fewer amenities among more users.

- Products as a service where product ownership is never transferred to the consumer thus supporting maintenance, product life extension, and resource recovery.

Policy recommendations

Based on the analyses recommended policy options for the Nordics have been provided on two categories of options:

- Policy recommendations for the Nordic countries to improve circularity of batteries and equipment

- Policy recommendations for the Nordic countries to contribute to creating the needed framework conditions

The policy recommendations for the Nordic countries to improve circularity of bat-teries and equipment focuses on existing and known technologies, including batteries, through these activities:

- Adopt the measures from the working documents for smartphones regarding relevant measures for batteries across all product groups containing batteries that fall under the Ecodesign Directive. One of the most comprehensive sets of measures relevant for products containing batteries is found in the working documents for smartphones, where both ecodesign requirements and energy label are proposed. Adoption of these measures can be a good example to be used when setting or reviewing requirements for other product groups.

- Create a new metric regarding battery performance, allowing manufacturers a higher degree of freedom to develop the best-suited batteries for the specific application. Instead of setting requirements on cycles, it could be relevant to develop a metric that calculates the lifetime of the battery, which needs to fit the expected life of the product.

- Ensure interoperable batteries across product groups with batteries that have many similarities in order that detachable rechargeable batteries can be used across a range of different products.

- Support the battery proposal. The proposed Battery Regulation is quite comprehensive and covering many relevant areas. In the current policy process, the Nordics may discuss internally and with other Member States if common positions can be reached how it can be supported.

- Use Green Public Procurement to increase the demand for sustainable batteries, where the Nordics can suggest the European Commission and the GPP Advisory Group to include batteries in a technical study aiming at setting GPP criteria for batteries.

- Support a far-reaching review of the Ecodesign directive and push for inclusion of the transport sector, where the Nordics should push to remove the exemption for means of transport from the Ecodesign Directive - or at least that the exemption should not apply to batteries for means of transport. This can be fed into the current process of Sustainable Products Initiative amending or replacing the current Ecodesign Directive.

Policy recommendations for the Nordic countries to contribute to creating the needed framework conditions focuses on recommendations on what the Nordic countries can do to contribute to creating the right framework conditions for the Nordic countries to be centrally placed in an innovative, sustainable and competitive battery ecosystem in Europe through these activities:

- Positioning the Nordic countries to benefit from sustainability requirements in the new EU Regulatory Framework for Batteries proposed by the Commission and expected to be adopted during 2022. The Nordic countries should position themselves to support and subsequently benefit from the expected (i) rules on recycled content; (ii) measures to improve the collection and recycling rates of all batteries; (iii) progressively phasing out non-rechargeable batteries; and (iv) sustainability and transparency requirements for batteries (carbon footprint, ethical sourcing of raw materials, security of supply, and facilitating reuse, repurposing and recycling).

- Preparing Nordic project developers for participation in the available financial support for European projects demonstrating and scaling up innovative sustainable battery technologies and business models, which will include making public funding or financing for battery cells manufacturing projects available in order to incentivise, leverage and 'de-risk' private sector investment through Horizon Europe, Invest EU, LIFE and the Innovation Fund in support of innovative battery-related deployment projects.

- Facilitating Nordic research project participation in the improved European research and innovation funding opportunities for battery technology, which will include making available, research and innovation funds (Horizon Europe) for battery-related innovation projects and - in the longer term - the launch of a large-scale Future Emerging Technologies Flagship research initiative, which could support long-term research in advanced battery technologies for the 2025+ timeframe.

- Working with TSOs (Transmission System Operator) and national energy market regulators to ensure that the necessary regulatory framework and pricing mechanisms allow for sustainable battery technology demonstration and scaleup for battery technology for decentral storage of intermittent renewable energy. This is on one side essential for the electrification of large parts of the Nordic economies and meeting climate goals by 2030 and 2050 and on the other side provides a range of services which is not currently priced in the market (frequency response, reactive power, provision of system inertia).

Executive summary – Danish

Introduktion

Det overordnede formål med dette projekt er at fremme de nordiske lande som en foregangsregion ift. at efterspørge og bruge bæredygtigt design af forbrugerelektronik, og at identificere nøglemuligheder, barrierer og udfordringer i overgangen til en mere bæredygtig brug af batteriteknologier, herunder transportsektoren. Æstetikken i designet skal gå hånd i hånd med den overordnede bæredygtighed: høj kvalitet, holdbarhed og smart montering for let renovering og reparation.

Projektet er bestilt og betalt af Nordisk Arbejdsgruppe for Cirkulær Økonomi (NCE) under Nordisk Ministerråd. Projektet er udført af Viegand Maagøe A/S (Danmark) og IVL Swedish Environmental Research Institute (Sverige) i perioden 20. oktober 2020 til 31. december 2021.

Der er nedsat en referencegruppe med repræsentanter fra Norden, som har givet værdifulde input til undersøgelsen.

Lovmæssige rammer og relevante initiativer

EU-lovgivning og -initiativer har direkte eller indirekte indflydelse i Norden på batterier og de produkter, der indeholder batterier.

Den foreslåede nye batteriforordning, der skal erstatte batteridirektivet, forventes at blive en vigtig drivkraft for batteriernes cirkulære karakter og for at minimere batteriernes negative miljøpåvirkning. Det nuværende batteridirektiv gælder for alle batterier, der markedsføres i Den Europæiske Union og fastlægger formål og mål (f.eks. om indsamling og genbrug); specificerer foranstaltninger (såsom udfasning af kviksølv eller etablering af nationale indsamlingsordninger) og muliggør foranstaltninger (f.eks. rapportering eller mærkning) for at opnå dem.

Direktivet har været EU's bedste værktøj til at sikre genanvendelse og gavnlig miljøhåndtering af batterier på det europæiske marked og har derfor også påvirket de nordiske medlemslandes håndtering af batterier. Alligevel sikrer direktivet ikke, at alle batterier indsamles og genbruges korrekt ved slutningen af deres levetid, hvilket øger risikoen for at frigive farlige stoffer og spilde værdifulde og kritiske ressourcer. Det eksisterende direktiv dækker heller ikke fuldt ud hensigterne med den cirkulære økonomi. Derfor er der foreslået en ny batteriforordning, der ophæver det eksisterende direktiv, for bedre at afspejle cirkulariteten, forbedre bæredygtigheden og holde trit med den teknologiske udvikling.

Den foreslåede batteriforordning (offentliggjort den 10. december 2020) omfatter:

- introduktion af en ny kategori af batterier til elektriske køretøjer sideløbende med de eksisterende for mobilt udstyr, biler og til industrielt formål;

- gradvist forøget krav for at minimere CO2-fodaftrykket for elbilsbatterier og genopladelige industribatterier: et krav om deklaration af CO2-fodaftryk, der gælder fra 1. juli 2024, suppleret med klassificering i en CO2-foraftryksydelseskategori og tilhørende mærkning (pr. 1. januar 2026); og et krav om at overholde maksimale tærskelværdier for CO2-fodaftryk i livscyklussen (fra 1. juli 2027);

- et krav om deklaration af genanvendt indhold, som fra 1. januar 2027 vil gælde for industribatterier, elbilsbatterier og bilbatterier, der indeholder kobolt, bly, lithium eller nikkel i aktive materialer. Obligatoriske minimumsniveauer for genanvendt indhold vil blive fastsat for 2030 og 2035 (dvs. 12% kobolt; 85% bly, 4% lithium og 4% nikkel pr. 1. januar 2030, stigende til 20% kobolt, 10% lithium og 12% nikkel fra 1. januar 2035, idet andelen for bly er uændret);

- minimumskrav til elektrokemisk ydeevne og holdbarhed for bærbare batterier til almindelig brug (gælder fra 1. januar 2027), samt for genopladelige industribatterier (fra 1. januar 2026). Kommissionen vil vurdere gennemførligheden af at udfase ikke-genopladelige bærbare batterier til almindelig brug inden udgangen af2030;

- en ny forpligtelse til batteriudskiftning for bærbare batterier; sikkerhedskrav til stationære batterienergilagringssystemer;

- forsyningskædens due diligence-forpligtelser for økonomiske aktører, der bringer genopladelige industribatterier og elbiler på markedet. For dette krav om ansvarlig råvareindkøb (såvel som for dem, der er relateret til CO2-fodaftrykket og niveauerne for genbrugsindhold) forudser Kommissionens forslag obligatorisk tredjepartsverifikation gennem bemyndigede organer;

- øgede mål for indsamlingsprocenten for udtjente bærbare batterier, undtaget udtjente batterier fra letvægtstransportmidler (65% ved udgangen af 2025, stigende til 70% ved udgangen af 2030);

- med hensyn til genanvendelseseffektivitet, øgede mål for blybatterier (genanvendelse af 75% af gennemsnitsvægten af blybatterier i 2025, stigende til 80% i 2030) og nye mål for lithium-baserede batterier (65% i 2025, 70% i 2030). Den foreslåede forordning forudser også specifikke materialegenvindingsmål, nemlig 90% for kobolt, kobber, bly og nikkel, og 35% for lithium, som skal nås inden udgangen af 2025. Inden 2030 bør genvindingsniveauerne nå 95% for kobolt. kobber, bly og nikkel og 70% for lithium;

- krav i forbindelse med genanvendelse og genfremstilling for en anden levetid for industri- og elbilsbatterier;

- mærknings- og informationskrav. Fra 1. januar 2027 skal batterier være mærket med en etiket med oplysninger, der er nødvendige for identifikation af batterier og deres vigtigste egenskaber. Forskellige etiketter på batteriet eller batteriemballagen vil også give oplysninger om levetid, ladekapacitet, krav til separat indsamling, tilstedeværelsen af farlige stoffer og sikkerhedsrisici. Genopladelige industribatterier og EV-batterier bør indeholde et batteristyringssystem, der gemmer de oplysninger og data, der er nødvendige for at bestemme batteriernes helbredstilstand og forventet levetid. Dette system bør være tilgængeligt for batteriejere og uafhængige operatører, der handler på deres vegne (f.eks. for at lette genbrug, genbrug til andet formål eller genfremstilling af batteriet);

- oprettelse senest den 1. januar 2026 af et elektronisk udvekslingssystem for batteriinformation med oprettelse af et batteripas (dvs. elektronisk registrering) for hvert industribatteri og EV-batteri, der markedsføres eller tages i brug;

- overvejer udviklingen af obligatoriske minimumskriterier eller mål for grønne offentlige indkøb.

Direktivet om miljøvenligt design fastsætter en ramme for fastlæggelse af krav for energirelaterede produkter såsom husholdningsapparater, forbrugerelektronik og informations- og kommunikationsteknologi. I de senere år er der implementeret ressourceeffektivitetskrav i ecodesign-forordningerne, herunder krav om adskillelse til reparation og genbrug og for produkternes indbyggede batterier. Disse omfatter kravene til computere og til virksomheds- og datacenterservere og datalagringsprodukter og foreslåede krav i arbejdsdokumenterne for smartphones og tablets. Disse krav kan være yderst relevante for cirkulariteten af selve batterierne og også for at forlænge levetiden af produkterne ved brug af indbyggede batterier på grund af længere batterilevetid og mulighed for nem udskiftning af batterierne.

Grønne offentlige indkøbskriterier (GPP) for computere, skærme, tablets og smartphones omfatter krav til indbyggede batterier relateret til forlængelse af produktets levetid, energiforbrug, farlige stoffer, efterbrugs-management og renoverede/genfremstillede produkter. At stille sådanne krav til batterier bør skabe et økonomisk incitament til at producere og sælge batterier med længere levetid. GPP giver også incitamenter til at producere batterier med høj holdbarhed og kvalitet ved at sikre, at de er testet i henhold til international standard, dvs. EN 61960-3:2017.

Andre relevante love omfatter:

-

Direktivet om affald af elektrisk og elektronisk udstyr (WEEE).

-

EU-liste over affald

-

Forordningen om forsendelse af affald

-

Forordningen om CE-mærkning

-

Direktivet om begrænsning af farlige stoffer (RoHS).

-

Forordningen om registrering, vurdering, godkendelse og begrænsning af kemikalier (REACH)

-

EU's konfliktmineralforordning

Ud over de lovgivningsmæssige initiativer omfatter andre vigtige initiativer herunder 2021 Industrial Strategy Update, hvor et strategisk område er lithium-ion-batterier (LIB'er); og den strategiske handlingsplan for at udvikle en europæisk batterivær|di|kæ|de, der omfatter råvareudvinding, indkøb og forarbejdning, batterimaterialer, celleproduktion, batterisystemer og genbrug og genanvendelse. Desuden støttede Europa-Kommissionen oprettelsen af The European Battery Alliance (EBA).

Endelig har EU finansieringsordninger for forskning, pilotprojekter, demonstratorer, opskalering og udrulning i batterier, såsom Horizon 2020, Horizon Europe, Innovationsfonden og Important Projects of Common European Interest (IPCEI).

Nuværende praksis vedrørende lithium-ion batterier

Produktion

LIB-produktion er meget kompleks og involverer mange trin fra minedrift til batteripakkeproduktion. Udvinding af metaller forekommer i forskellige dele af verden. Kina dominerer dog i øjeblikket med hensyn til celleproduktion, herunder katode- og anodeproduktion. Nogle råmaterialer er kritiske (høje forsyningsrisici og økonomisk meget vigtige) for EU, herunder kobolt, grafit og lithium.

Metaller udvindes til katoden, og de raffineres til sulfater eller i tilfælde af lithium, nogle gange brugt som hydroxid. Efter minedrift og raffinering fremstilles det aktive katodemateriale. Udvinding af metaller har stor indvirkning på miljøet og mennesker, der arbejder og bor i nærheden afudvindingsstederne. Battericellen er konstrueret med anode, katode, elektrolyt, separator, plast, stål, kobber og aluminium. Katoderne er lavet af forskellige kemier afhængigt af anvendelsen, og anoden er normalt baseret på grafit med undtagelse af LTO-kemi.

De kommende års tendenser for batterikemi i produkterne er ikke kun relevante for de råvarer, der kræves ved produktionen, men også for mængden af batterier, der skal genanvendes. Dette skyldes, at kemien bestemmer mængden af specifikke råmaterialer (f.eks. kobolt og nikkel), som kan genvindes.

Der foregår meget forskning i nye kemier, og de vigtigste drivkræfter er øget energitæthed for at øge rækkevidden for biler, reducere omkostningerne og reducere behovet for kritiske råmaterialer såsom kobolt.

De vigtigste markedssektorer i EU for LIB'er er bilindustrien og i mindre grad bærbare enheder. Væksten for solgte markeder på hvert marked i de kommende 10–15 år vil formentlig hovedsageligt ligge på bilsiden. Salget af rene elektriske (BEV) personbiler dominerer væksten. Andre vigtige produkter - som vokser betydeligt frem til 2030 - er PHEV'er for personbiler, busser og LCV (lette erhvervskøretøjer). Også batterier i elværktøj og tablet og smartphones er blevet solgt mere og vil fortsætte med at stige frem til 2030.

Brug

Den primære anvendelse er til bilindustrien, og den næststørste anvendelse er til bærbare enheder, forudsat at det mønster, der ses i Europa, også gælder for Norden.

Til nogle anvendelser, for eksempel til elværktøj, kræves høj effekt og dermed høj C-rate (høj strøm) fra batteriet, men energilagringskapaciteten kan være lavere. Da det varierer, hvor meget tid man bruger værktøjet pr. brug, er batteriet ofte overdimensioneret til privat brug.

For bærbare batterier til bærbar elektronik såsom smartphones, bærbare computere, tablets, højttalere, er batterierne indbyggede, og lægfolk er ofte ikke i stand til at erstatte dem; især til vandtætte produkter.

Især for udskiftede bilbatterier har batterierne typisk stadig energikapacitet tilbage, hvilket giver muligheder for renovering eller omfabrikation og opnåelse af et nyt liv i køretøjer eller i anden anvendelse, f.eks. til energilagring i bygninger eller som el-netunderstøttelse. Så længe der er et marked og en værdi af disse second life-batterier, vil en større del af batteriernes tekniske levetid sandsynligvis blive opnået, før de kasseres.

For EV-batterier er det almindeligt at give dem et nyt liv til industriel eller kommerciel energilagring. I Sverige bliver mange brugte elbatterier brugt i ejendomme og fx brugt på hustage til at opbevare energi produceret af solpaneler. For elektroniske produkter er tilgangen i øjeblikket helt at udskifte batterierne med nye i stedet for at reparere gamle batterier.

Efterbrug

Efter at brugeren ikke længere bruger produktet og ønsker at skrotte det, bliver ejerskabet af batteriet af stor betydning. Det udvidede producentansvar (Extended Producer Responsibility (EPR)) for batterier betyder, at den virksomhed, der bringer batterierne på markedet, er ansvarlig for deres indsamling, når de kasseres af forbrugeren.

Der er ingen lovkrav til, at ejeren af et batteri skal sende det til genbrug, når det ikke længere bruges af forbrugeren, hvorfor mange udtjente batterier til forbrugerelektronik bliver hos den oprindelige ejer i mange år i stedet for at blive genbrugt. For EV-batterier, som LFP-batterier, kan batterier adskilles fra busser og opbevares på ubestemt tid, indtil et formål med dem er fundet.

Mange små batterier bliver ikke indsamlet til batterigenbrug, fordi de er integreret i enheden og ikke kan skilles ad. De kan derfor ende i elektronisk (WEEE) genanvendelse i stedet, hvor der kun er ringe chance for, at batterimetallerne kan genanvendes.

EV-batterier formodes at blive fjernet under forbehandlingsprocessen for at overholde ELV-direktivet (direktivet om udtjente køretøjer), og procentdelen afbatterier, som det finder sted for, bør være høj, da den direkte korrelerer med lageret til rådighed for genbrugsindustrien.

Genbrug

Der er stor variation, når det kommer til genanvendelse mellem hvilke former for genbrug, der udføres, og hvilke aktører, der er involveret. Selv inden for de større genbrugskategorier, såsom hydrometallurgi eller pyrometallurgi, kan der være store forskelle på, hvordan virksomheder udfører genanvendelsen. Forskelle, som forskellige aktører i genbrugskæden vælger, kan omfatte: hvilke metaller og andre materialer, der genvindes, hvor stor en procentdel af kobolt/nikkel/lithium/mangan, der genvindes, hvilken type opløsningsmidler der bruges i hydrometallurgisk genanvendelse, og hvilken type forbehandling der udføres.

Hovedkategorierne for genanvendelse i dag er hydrometallurgisk eller pyrometallurgisk med efterfølgende hydrometallurgi. Begge har forskellige fordele og ulemper med hensyn til omkostninger, genvindingseffektivitet, fleksibilitet/tilpasning til forskellige batterikemier, behovet for et demonteringstrin og energiforbrug.

Pyrometallurgi betyder opvarmning af batterier for at smelte metallerne, mens hydrometallurgi bruger syrer eller baser til at opløse dem. Men først skal demontering af dele og andre forbehandlinger foretages. For hydrometallurgisk genbrug er viden om katodekemien vigtig, hvorfor det anbefales at markere batteriet tydeligt med denne information, måske med elektroniske tags for at lette sorteringen.

Ved batterigenbrug har elektrodernes kemi betydning, især katoden. Det meste af værdien findes i katoden, hvor værdifulde metaller såsom kobolt, nikkel og lithium findes. Mobiltelefoner, tablets og computere bruger Li-ion-batterier med højkvalitets Co-indhold (>12%), og denne høje Co-koncentration betyder, at det er rentabelt både for producenterne af disse produkter og genbrugerne at forsøge at genanvende metallerne i disse batterier. Til gengæld indeholder værktøjsbatterier normalt omkring 6%, hvorfor det ikke er lige så rentabelt at håndtere (genbrugere betaler typisk ikke for disse batterier, men tager et gebyr for at genbruge dem).

I øjeblikket er batterivolumen ikke tilstrækkelig til hydrometallurgi af sort masse i Norden. Der er også andre udfordringer, der skal overvindes for et fungerende LIB-genbrug.

Det nuværende batteridirektiv sætter ikke specifikke begrænsninger på det genbrugte indhold af lithium-ion-batterier, hvilket betyder, at genbrugsvirksomheder normalt vil genbruge de lettest kan genbruge eller har de mest værdifulde materialer. Forslaget til den nye forordning vil sandsynligvis kræve, at genbrugsvirksomhederne indfører forskellige metoder til genanvendelse for at justere procentdelen af metaller, der genvindes.

Et problem ved at reducere kobolt i batterierne er, at værdien for genbrugsvirksomhederne reduceres. LFP genanvendes derfor slet ikke i Europa i øjeblikket. Denne hindring kan afbødes af den foreslåede batteriregulering med dens foreslåede genvindingsprocenter for kobolt, lithium og nikkel samt det foreslåede genanvendte indhold i produktionen af nye batterier. Det foreslåede direktiv vil også tvinge virksomhederne i batteriforsyningskæden til at være mere gennemsigtige med hensyn til at sikre genanvendelighed (som muliggør adskillelse).

Bæredygtighed af batterier

Nogle vil måske betragte bæredygtighed som en anden formulering for miljøudvikling, mens andre også overvejer de økonomiske og sociale konsekvenser. Hvad angår batterier, er det vigtigt at overveje alle aspekter af bæredygtighed, da batteriteknologi er en nøglehjørnesten i den grønne omstilling til et fossilfrit samfund ved at erstatte produkter, apparater og transportmidler, der kræver fossile brændstoffer.

Det er vigtigt at overveje alle aspekter af bæredygtighed, hvilket er i overensstemmelse med FN's udviklingsmål (Sustainable Development Goals (SDG'erne)), der har til formål at: "sikre, at alle mennesker kan nyde velstående og tilfredsstillende liv, og at økonomiske, sociale og teknologiske fremskridt sker i harmoni med natur."

Bæredygtighed og bæredygtig udvikling omtales ofte som de tre P'er ift. den engelske udgave af mennesker, planet og velstand (People, Planet og Prosperity).

Mennesker: Der er betydelige sociale og miljømæssige konsekvenser i forbindelse med udvinding af flere af råvarerne i lithium-ion-batterier, især hvad angår konfliktmineraler. Mineraler betragtes som konfliktmineraler, hvis de kommer fra politisk ustabile områder, og hvor mineralhandelen kan bruges til at finansiere væbnede grupper, udbrede tvangsarbejde og andre menneskerettighedskrænkelser og støtte korruption og hvidvaskning af penge. Der er flere primære råmaterialer, der bruges til at fremstille lithium-ion-batterier, som kan have en negativ indvirkning på hele værdikæden. Kobolt er det mest problematiske råmateriale af alle listede råvarer, da det hovedsageligt udvindes i lande med dårlig regulering og uorganiserede små gruber, dvs. udvinding i hånden ved hjælp af rudimentære og basale værktøjer, ofte uden tilstrækkeligt beskyttelsesudstyr. Over 50 procent af verdens kobolt udvindes i DRC (Den Demokratiske Republik Congo).

Planet: Batterier påvirker miljøet både positivt og negativt, og miljøpåvirkning påvirker mennesker. Både fordele og ulemper skal overvejes i forbindelse med den øgede efterspørgsel efter forskellige typer batterier for at undgå rebound-effekter. Drivhusgasemissionerne ved at producere et batteri er omtrent det samme som resten af bilen selv, og dermed er drivhusgasemissionerne fra produktion af en elbil cirka dobbelt så meget som for en bil, der kun kører ved hjælp af forbrændingsmotor. I andre påvirkningskategorier er det tydeligt, at en elbil også producerer væsentligt højere emissioner af andre typer under produktionen.

Velstand: Mange af bæredygtighedsmålene har til formål at forbedre forskellige områder relateret til miljø, mennesker og økonomiske muligheder. Økonomiske muligheder sigter mod at give anstændigt arbejde såsom sikre arbejdsforhold, lønninger til at leve af, indlevende lederskab og økonomisk vækst for dem i specifikke samfund. Fra et mere stramt virksomhedsperspektiv er den økonomiske del naturligvis vigtig. Hvis en virksomhed har et underskud, kan den ikke fortsætte med at fungere, medmindre den på en eller anden måde laver en vending af udviklingen. En virksomhed kan fokusere på sociale og miljømæssige påvirkninger, men hvis de ikke tjener penge, kan de ikke fortsætte deres levedygtige arbejde (socialt og miljø).

For at sikre bæredygtighed skal løsningen være økonomisk bæredygtig. Tidligere var virksomheder fokuseret på overskud opnået gennem en lineær forretningsmodel, hvor højere salg var lig med højere fortjeneste. Den automatiske samlebåndsproduktion favoriserer lineære forretningsmodeller. Bæredygtighed er en forretningstilgang til at skabe langsigtet værdi ved at overveje, hvordan en given organisation opererer inden for de tre P'er (People, Planet og Prosperity).

Bæredygtighed bygger på den antagelse, at udvikling af sådanne strategier fremmer virksomhedens levetid. Uden fokus på bæredygtighed kan der stilles spørgsmålstegn ved, hvor længe virksomheden kan fortsætte med at fungere, efterhånden som forventningerne til virksomhedernes ansvar øges. Gennemsigtighed bliver mere udbredt, og flere virksomheder erkender behovet for at handle på bæredygtighed. Professionel kommunikation og gode intentioner er ikke længere nok, da grønne krav undersøges, og greenwashing vil skade virksomhedens omdømme.

Uden et bredt fokus på bæredygtighed kan det blive stadig sværere for virksomheder at konkurrere på markedet. Disse overvejelser kan øge fokus på Norden som et velegnet sted for produktion, da den grønne energiforsyning kan hjælpe virksomheder med at opfylde deres bæredygtighedsmål og øge deres markedsværdi.

Vigtigste barrierer mod øget cirkularitet

Selvom der er mange muligheder og fordele ved den cirkulære økonomi, er der stadig flere barrierer, der begrænser stigningen i cirkulariteten. Vigtigste barrierer omfatter:

- Virksomhedskultur, som ofte kan være en stor hindring i forhold til at skifte fra en veletableret lineær økonomi til cirkulær økonomi, ændre forbrugernes tankegang, involvere hele livscyklussamarbejde og ændre tankegange i virksomheder.

- Mangel på cirkulære designmuligheder især inden for elektronik og batterier på grund af kompleksiteten af små komponenter og kompakte produkter, der gør demontering vanskelig for genbrugs- og renovationsvirksomhederne, og fordi batterier har forskellige dimensioner, former og sammensætninger af kemikalier og metaller, hvilket gør det udfordrende at etablere et effektivt standardiseret system for batterigenanvendelse.

- Manglende lovgivning, som kan hæmme CE, dog er Norden og EU stadig foran på grund af national lovgivning og kommende EU-lovgivning om batterier.

- Manglende forbrugerinteresse og bevidsthed, fordi nogle forbrugere simpelthen kan lide nye varer, før deres gamle er slidt op, hvilket er særligt for trendbaserede, højteknologiske produkter med konstant modeludvikling, såsom mobiltelefoner, hvilket afskrækker producenter fra at fremstille robuste og dyrere produkter, da der er mindre markedsefterspørgsel efter sådanne produkter for nogle produktsegmenter.

- Lave råvarepriser, fordi den svingende pris på råvarer, som plast eller metaller, hæmmer det økonomiske incitament til at købe genbrugsmaterialer, når der er lave råvarepriser. Dette afskrækker yderligere investeringer i forbedring af de nuværende genbrugssystemer, som kan hjælpe med til at reducere priserne på regenererede ressourcer. Desuden er nogle primære råvarer underlagt tilskud, hvilket gør markedsprisen på genbrugsmaterialer endnu mere ugunstig.

- Sort batterimarked og ulovlig eksport, fordi mellem 30 og 40 procent af elbilerne eksporteres inden slutninger af deres levetid, men graden af ulovlig eksport er ukendt, fordi der kun er få data om ulovlig eksport af WEEE. Dette fører til cirkularitetsudfordringer, som inkluderer, at batterierne ender til genanvendelse i andre dele af verden, hvilket resulterer i øget emission til transport, mindre effektive genbrugsfaciliteter og dermed lavere outputkvalitet, og endeligt en reduceret mængde genbrugsmaterialer til den nordiske batteriproduktionsindustri.

Best practice og design for øget cirkularitet

I dette afsnit præsenteres indhold til separate håndbøger til virksomheder og til forbrugere om bedste praksis og design for øget cirkularitet. For virksomheder gives inspiration fra konkrete case-eksempler, mens der til forbrugere gives råd om, hvad de kan gøre ved køb og brug af produkterne.

For virksomheder

Mange virksomheder udforsker i øjeblikket de utallige muligheder for at arbejde med cirkularitet af batterier og batteridrevne produkter gennem nye forretningsmodeller og forbedrede måder at bruge batterierne mere effektivt på. For at udløse disse innovative forretningspotentialer er der behov for ny praksis i indkøbs-, design- og produktionsafdelinger. Håndbogen indeholder inspiration til virksomheder, så de kan etablere disse nye praksisser. Grundlaget for inspirationsemnerne er en udvikling af Ellen MacArthur Fondens model, hvor fokus på forretningsmodeller er stærkere.

Fem forretningsmodeltyper er blevet undersøgt, og der er givet case-eksempler på virksomheder, der har taget disse tilgange og tiltag, som forbrugerne kan anvende for at understøtte batteriernes cirkulære økonomi. Modellerne dækker over:

- Cirkulære forsyninger, der beskriver hvordan bæredygtighed og cirkulær økonomi kan understøttes ift. opstrømsværdikæden og efterspørgsel af bæredygtige materialer.

- Ressourcegenvinding, der beskriver handlinger, der kan sikre genbrug og genanvendelse ved foranstaltninger ift. nedstrømsværdikæden.

- Produktlevetidsforlængelse, der inkluderer alle de handlinger, forbrugere og producenter kan anvende for at øge levetiden for produkter og komponenter i brugsfasen.

- Delingsplatforme, der hjælper med at mindske behovet for produkter ved effektivt at dele færre faciliteter blandt flere brugere.

- Produkter som en service, hvor produktejerskab aldrig overføres til forbrugeren, hvilket understøtter vedligeholdelse, forlængelse af produktets levetid og ressourcegendannelse.

For forbrugerne

Forbrugerne kan støtte udviklingen mod cirkularitet af batterier og batteridrevne produkter gennem nye forretningsmodeller og forbedrede måder at bruge batterierne mere effektivt på via deres indkøb og samtidig opnå økonomiske fordele for sig selv og være med til at beskytte miljøet.

Håndbogen beskriver principperne bag cirkulært design for bedre at kunne forstå følgende best practice-anbefalinger og foreslå, hvad forbrugerne kan gøre via deres handling i købssituationen og under brugen af de købte produkter.

Cirkulære måder at købe, bruge og bortskaffe batterier præsenteres sammen med case-eksempler på virksomheder, der har taget cirkulære initiativer inden for de fem forretningsmodeltyper beskrevet ovenfor. Modellerne dækker over:

- Cirkulære forsyninger, der beskriver cirkularitet i de materialer, der indgår i produkterne.

- Ressourcegenvinding, der beskriver handlinger, der kan sikre genbrug og genbrug af batterier.

- Produktlevetid forlængelse, der inkluderer alle de handlinger, der kan øge levetiden for batteriprodukter og komponenter i brugsfasen.

- Delingsplatforme, der hjælper med at mindske behovet for produkter ved effektivt at dele færre faciliteter blandt flere brugere.

- Produkter som en service, hvor produktejerskab aldrig overføres til forbrugeren, hvilket understøtter vedligeholdelse, forlængelse af produktets levetid og ressourcegendannelse.

Anbefalede politik-muligheder

Baseret på analyserne er anbefalede politiske muligheder for Norden blevet givet på to kategorier af muligheder:

- Politiske anbefalinger til de nordiske lande for at forbedre cirkulariteten af batterier og udstyr

- Politiske anbefalinger til de nordiske lande for deres bidrag til at skabe de nødvendige rammebetingelser

De politiske anbefalinger til de nordiske lande om at forbedre cirkulariteten af batterier og udstyr fokuserer på eksisterende og kendte teknologier, herunder batterier, gennem disse aktiviteter:

- Vedtage foranstaltningerne fra arbejdsdokumenterne for smartphones vedrørende relevante foranstaltninger for batterier på tværs af alle produktgrupper, der indeholder batterier, der falder ind under Ecodesign-direktivet. Et af de mest omfattende sæt af foranstaltninger, der er relevante for produkter, der indeholder batterier, findes i arbejdsdokumenterne for smartphones, hvor både krav til miljøvenligt design og energimærke foreslås. Vedtagelse af disse tiltag kan være et godt eksempel til brug ved opstilling eller revision af krav til andre produktgrupper.

- Udvikle en ny målemetode vedrørende batteriydelse, hvilket giver producenterne en højere grad af frihed til at udvikle de bedst egnede batterier til den specifikke applikation. I stedet for at stille krav til cyklusser, kunne det være relevant at udvikle en målemetode, der beregner batteriets levetid, som skal passe til produktets forventede levetid.

- Sikre kompatible batterier på tværs af produktgrupper med batterier, der har mange ligheder, så aftagelige genopladelige batterier kan bruges på tværs af en række forskellige produkter.

- Støtte batteriforslaget. Den foreslåede batteriregulering er ret omfattende og dækker mange relevante områder. I den nuværende politiske proces kan de nordiske lande diskutere internt og med andre medlemsstater, om der kan opnås fælles holdninger til, hvordan det kan understøttes.

- Bruge grønne offentlige indkøb (GPP) til at øge efterspørgslen efter bæredygtige batterier, hvor de nordiske lande kan foreslå Europa-Kommissionen og GPP’s rådgivende gruppe at inkludere batterier i en teknisk undersøgelse, der sigter mod at opstille GPP-kriterier for batterier.

- Støtte en vidtrækkende revision af Ecodesign-direktivet og skubbe på for inklusion af transportsektoren, hvor Norden bør presse på for at fjerne undtagelsen for transportmidler i ecodesign-direktivet - eller i det mindste at undtagelsen ikke skal gælde for batterier til transportmidler. Dette kan indgå i den nuværende proces med initiativet for bæredygtige produkter, der ændrer eller erstatter det nuværende ecodesign-direktiv.

Politiske anbefalinger til, at de nordiske lande bidrager til at skabe de nødvendige rammebetingelser fokuserer på anbefalinger til, hvad de nordiske lande kan gøre for at bidrage til at skabe de rette rammebetingelser for, at de nordiske lande kan placeres centralt i et innovativt, bæredygtigt og konkurrencedygtigt batteriøkosystem i Europa gennem disse aktiviteter:

- Positionering af de nordiske lande for at drage fordel af bæredygtighedskravene i den nye batteriregulering foreslået af Kommissionen, som forventes vedtaget i løbet af 2022. De nordiske lande bør positionere sig til at støtte og efterfølgende drage fordel af de forventede (i) regler om genbrugsindhold; (ii) foranstaltninger til at forbedre andelen af alle batterier, som bliver indsamlet og genanvendt (iii) gradvis udfasning af ikke-genopladelige batterier; og (iv) krav til bæredygtighed og gennemsigtighed for batterier (CO2-fodaftryk, etisk indkøb af råmaterialer, forsyningssikkerhed og fremme af genanvendelse, genbrug til andet formål og genbrug).

- Forberedelse af nordiske projektudviklere til deltagelse i den tilgængelige økonomiske støtte til europæiske projekter, der demonstrerer og opskalerer innovative bæredygtige batteriteknologier og forretningsmodeller, hvilket vil omfatte at stille offentlig støtte eller finansiering til rådighed for battericelleproduktionsprojekter for at give incitamenter, udnytte og reducere risiko for private sektorinvesteringer gennem Horizon Europe, Invest EU, LIFE og Innovationsfonden til støtte for innovative batterirelaterede implementeringsprojekter.

- Facilitering af nordisk forskningsprojektdeltagelse i de forbedrede europæiske forsknings- og innovationsfinansieringsmuligheder for batteriteknologi, som vil omfatte tilgængeliggørelse af forsknings- og innovationsmidler (Horizon Europe) til batterirelaterede innovationsprojekter og - på længere sigt - lancering af et stor-skala flagskibsforskningsinitiativ inden for fremtidige nye teknologier, som kunne støtte langsigtet forskning i avancerede batteriteknologier inden for 2025+tidsrammen.

- Samarbejde med TSO'er (transmissionssystemoperatører) og nationale energimarkedsregulatorer for at sikre, at de nødvendige lovgivningsmæssige rammer og prismekanismer muliggør demonstration af bæredygtig batteriteknologi og opskalering af batteriteknologi til decentral lagring af fluktuerende vedvarende energi. Dette er på den ene side essentielt for elektrificeringen afstore dele af de nordiske økonomier og opfyldelse af klimamålene i 2030 og 2050, og på den anden side giver mulighed for at levere en række tjenester, som i øjeblikket ikke er prissat på markedet (frekvensrespons, reaktiv effekt, levering af systeminerti).

1 Introduction

1.1 Introduction to the study

The overall aim of this project is to promote the Nordic countries as a forerunner region in demanding and using sustainable design of consumer electronics and such appliances, and to identify key opportunities, barriers and challenges in the transition towards a more sustainable use of battery technologies, including the transport sector. The aesthetics of the design should meet with the overall sustainability: high quality, durability and smart assembly for refurbishing.

The project is funded by the Nordic Working Group for Circular Economy (NCE) under the Nordic Council of Ministers. The project has been carried out by Viegand Maagøe A/S (Denmark) and IVL Swedish Environmental Research Institute (Sweden) in the period 20 October 2020 to 31 December 2021.

A reference group with representatives from the Nordics has been established, who provided valuable input to the study. A number of organisations have been interviewed, who also have provided valuable input to the study, see Annex A.

1.2 Background

Batteries are expected to play an important role in the transition to more clean energy in the EU, the Nordics, and globally where batteries, e.g. can displace fossil based mobility solutions, store energy from the grid and overall be used to utilise better electricity produced from renewable sources. At the same time, batteries are also playing an important role in consumer products, where cordless alternatives are the main drivers in the market.

The transition to more battery-driven products is enabled by the batteries' advancements and more energy-efficient products, allowing them to be used in more consumer products such as e.g. speakers, vacuum cleaners, cars, etc. Although many batteries today are significantly improved over the last decade and holds more energy (greater capacity), the products powered by batteries have increased their performance, meaning that the battery life of many products has not improved significantly. This is a driver for both more efficient products and bigger and better batteries.

Ideally, the advancement in the efficiency of the products and better batteries will reduce the need for more batteries. However, this is not the case currently, and more batteries are needed to fulfil climate goals and meet the increasing demands of cordless products, which means that the demand for batteries is expected to grow rapidly in the coming years.

Even though increased use of batteries brings many benefits for the environment and the consumers, the increased consumption of batteries may lead to:

- Shortage of needed raw materials to produce the batteries

- Geopolitical concerns regarding the location of the raw materials (lithium, nickel, cobalt, manganese, and graphite) and increased dependency of countries outside the EU

- Social concerns regarding local pollution and poor working conditions where the raw materials are mined

- High pollution related to the production of batteries as the manufacturing process is energy-intensive

- Concerns regarding the low share of batteries manufactured in Europe currently, meaning that European countries become heavily dependent on batteries produced outside of Europe

- More products may become obsolete due to degradation of batteries in cases, where they cannot be replaced or only with high cost

It is important to address these shortcomings of the increased use of batteries, but there is no straightforward solution. However, the idea of the circular economy may be a solution to minimise the shortcomings of the increased use of batteries.

1.3 This report

The study and the report have been structured in two parts:

- Part 1: Legal framework and relevant initiatives; today’s practice regarding lithium-ion batteries; sustainability of batteries and key barriers towards increased circularity today

- Part 2: Best practice and design for increased circularity for businesses and for consumers (handbooks) and recommended policy options (policy brief)

The content of Part 2 has been transformed to separate inspirational best practice handbooks for businesses and for consumers, respectively, and to a separate policy brief with recommended policy options.

2 Legal framework and relevant initiatives

This section presents the current and expected future framework conditions for lithium-ion batteries in the Nordics. Legislation, standards and voluntary initiatives are important to consider within the objectives of this study. The current framework conditions may contain barriers for increased circularity today and may lack measures to remove barriers and to push for greater circularity for batteries.

Even though this report focuses on Nordic countries, it is relevant to consider the EU legislations as these regulations directly impact Nordic countries.

The following sections present:

- Relevant EU legislation and initiatives

- Relevant national legislation in the Nordics

- Other initiatives such as the Nordic Swan, EPEAT, Eco Rating scheme and the battery passport

- Relevant standards

Note that this section is not an in-depth review of all relevant legislation, initiatives and standards but a brief overview of the most relevant ones related to the scope of this study at the time of producing this report.

2.1 EU legislation and initiatives

EU legislation and initiatives have a direct or indirect influence on batteries and the products containing batteries. In this section, we describe the most relevant EU legislation and initiatives providing an overview of the current and expected future regulations and provide suggestions of potential measures that could impact more sustainable production, use and disposal of batteries.

2.1.1 The Battery Directive and the proposed Battery Regulation

2.1.1.1 Background

The first battery directive was published in March 1991: the Council Directive 91/157/EEC of 18 March 1991 on batteries and accumulators containing certain dangerous substances. This was replaced in 2006 by the Battery Directive 2006/66/EC. Since then, batteries and accumulators have played a continuously increasing role in our daily lives and the transition to a fossil-free future. Batteries are integral parts of many daily-used products, appliances and electric vehicles and other mobility products.

Currently, approximately 800,000 tons of automotive batteries, 190,000 tons of industrial batteries, and 160,000 tons of consumer batteries enter the European Union every year. This number is only expected to increase in the coming years. Hence, increased focus is put on batteries in the Nordics and Europe.

In May 2018, the European Commission announced as part of the action plan Europe on the Move, a Strategic Action Plan for Batteries[1]https://ec.europa.eu/transport/sites/default/files/3rd-mobility-pack/com20180293-annex2_en.pdf aiming at creating a competitive and sustainable battery ecosystem in Europe. The Action Plan contained among others that the Commission would “put forward battery sustainability 'design and use' requirements for all batteries to comply with when placed on the EU market (this comprises an assessment and suitability of different regulatory instruments such as the Ecodesign Directive and the Energy Labelling Regulation and the EU Batteries Directive)”.

On this background, the Commission launched an Ecodesign and Energy Labelling preparatory study and impact assessment on batteries (performed by VITO, Viegand Maagøe and Fraunhofer ISI). Because the study revealed that the main part of the batteries used is for means of transportation, which is not in scope of the Ecodesign and Energy Labelling regulations, the Commission decided to use the content of the study for preparing a proposal for a new Battery Regulation.

On 10 December 2020, the Commission presented this proposal for Battery Regulation repealing the existing Directive 2006/66/EC[2]https://ec.europa.eu/environmenttemanord2022-523.pdfwaste/batteries/Proposal_for_a_Regulation_on_batteries_and_waste_batteries.pdf [3]https://ec.europa.eu/info/law/better-regulation/have-your-say/initiatives/12399-Modernising-the-EU-s-batteries-legislation_en. The proposal has three objectives: (1) strengthening the functioning of the internal market (including products, processes, waste batteries and recyclates) by ensuring a level playing field through a common set of rules; (2) promoting a circular economy; and (3) reducing environmental and social impacts throughout all stages of the battery life cycle.

Next sections present the Battery Directive and the new Battery Proposal and these are further discussed in Section 2.5.

Footnotes

- ^ https://ec.europa.eu/transport/sites/default/files/3rd-mobility-pack/com20180293-annex2_en.pdf

- ^ https://ec.europa.eu/environmenttemanord2022-523.pdfwaste/batteries/Proposal_for_a_Regulation_on_batteries_and_waste_batteries.pdf

- ^ https://ec.europa.eu/info/law/better-regulation/have-your-say/initiatives/12399-Modernising-the-EU-s-batteries-legislation_en

2.1.1.2 The Battery Directive 2006/66/EC

The directive aims at ensuring the protection and preservation of the environment. This is done by setting specific objectives of minimising the negative impact of batteries and waste batteries on the environment, maximising the separate collection of waste batteries, minimising the disposal of batteries as mixed municipal waste, and achieving a high level of material recovery. Furthermore, the directive aims at improving the environmental performance of both batteries themselves and the activities of all economic operators involved in the life cycle of batteries (producers, distributors and end-users) while also lowering the amount of dangerous substance contained in batteries[1]https://www.europarl.europa.eu/RegData/etudes/BRIE/2020/654184/EPRS_BRI(2020)654184_EN.pdf.

The Battery Directive applies to all batteries placed on the market within the European Union. It categorises batteries as portable (e.g. for power tools, laptops, smartphonesa and computers), industrial or automotive. The directive establishes objectives and targets (e.g. on collection and recycling); it specifies measures (such as phasing out mercury or establishing national schemes for collection) and enables actions (e.g. reporting or labelling) to achieve them.

The directive has been the EU’s best tool in ensuring recycling and beneficial environmental handling of batteries on the European market and have therefore also impacted the Nordic Member States’ handling of batteries. Overall, the directive is still in accordance with current needs and has not lost its relevance. No Member State has experienced unnecessary regulatory burdens related to the directive and a majority of participants in a public consultation see benefits incurred as a result of the directive implementation.