- Full page image w/ text

- Table of contents

- Summary

- Introduction

- Literature review

- 1. Overview of pay systems for commercial fishers

- Denmark

- Faroe Islands

- Greenland

- Iceland

- Norway

- Discussion and conclusion

- References

- Appendix 1. A note on socio-economic returns in fisheries

- 2. Denmark

- Introduction

- Fleet structure

- Wage determination system

- Interviews with relevant persons participating in the negotiations of the Agreement on Working Conditions (AWC) for the Danish Fisheries Sector, 2020 to 2023

- Rent calculations

- References

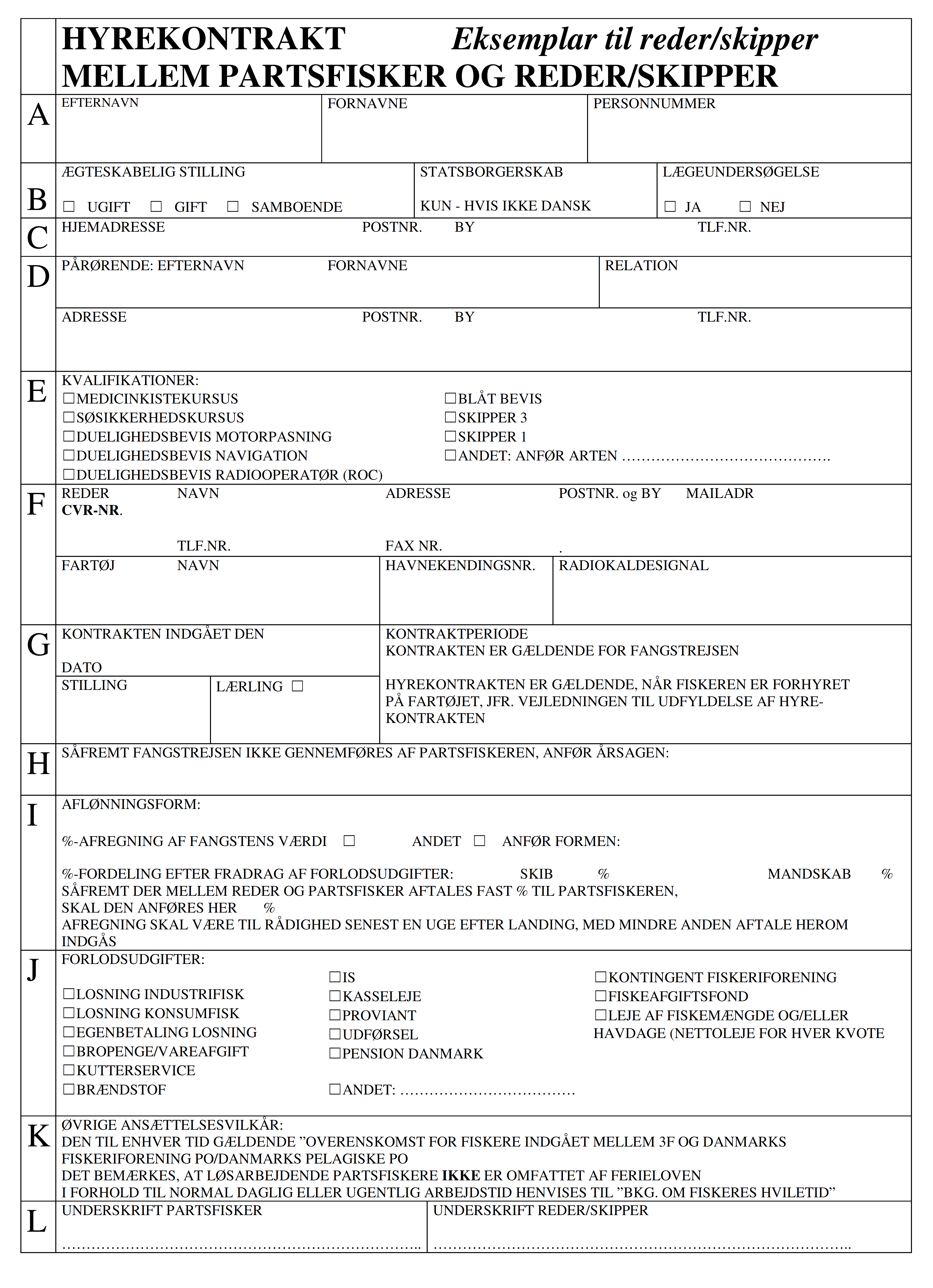

- Appendix: Hire contract

- 3. Faroe Islands

- Introduction

- Faroese fishery

- Wage determination system

- Resource rent

- Interviews

- Calculation of the size and allocation of the resource rent in the Faroe Islands

- References

- 4. Greenland

- Introduction and background

- Greenlandic fishery

- Employment in Greenlandic fisheries

- Wage determination system

- Salary developments

- Resource rent

- Taxation of commercial fishers

- References

- Appendix

- 5. Iceland

- Introduction

- Fisheries management, catch and the fleet

- Literature review

- Payment system

- Interviews with key players in Iceland

- References

- Rent calculations

- 6. Norway

- Introduction

- Norwegian fishery structure

- Wage determination system

- Interviews

- Resource rent in Norwegian fisheries

- References

- Resource rent

- About this publication

MENU

Contents

This publication is also available online in a web-accessible version at https://pub.norden.org/temanord2022-515.

Summary

Share pay, or lay, for commercial fishers is an old way of sharing both risk and benefits from fishing between boat owner and hired crew. Since time immemorial, such share systems have been part and parcel of the Nordic fisheries sector. Yet, when fisheries management reform was introduced, the share system remained in place, thus ‘institutionalising’ it. With the reform of fisheries management towards market-based economic instruments, fisher pay has augmented this, which suggests that fishers are able to share in the increased rent accruing from more sustainably managed fisheries. Fishers can leverage some of the efficiency gains obtained through investments in better gear and vessels. This is a unique feature of the fisheries sector with share payments. Although minimum wage provisions are in place, they are rarely applied. Commercial fishers are generally well paid compared to other occupations in the economy, albeit with differences between the various fisheries segments. Earlier work on fisher pay systems tends to ignore how the dynamics of the fisheries sector influence production risk. This includes changes to fisheries technology and changes in fisheries management settings. Furthermore, previous studies do not consider that differences in marketing schemes influence the price risk, such as through landings via auction or direct landings to processors, or, as in the notable cases in Greenland and Iceland, through forward integrated companies. The findings in this study suggest that fishers are very well paid compared to other occupations. Although this may reflect several factors, including a risk premium for being a fisher, we also observe that in line with the introduction of new management regimes, the fishers who remain in the sector continue to bring home substantial salaries that are well above the wage levels one might expect from land-based jobs. This is likely to reflect the fact that the increased rent in the fishery is captured by the fishers due to the share system, and not only by the vessel or quota owners. This has implications for resource rent taxation. The interviews carried out as part of this study broadly confirmed that fishers are well paid.

Introduction

As an overarching theme, this work looks at the effects on commercial fisher pay when market-based economic instruments (MBEI) are introduced through fisheries management reforms. Theoretically, the introduction of MBEIs in fisheries characterised by overfishing and overcapacity leads to adjustments to the fishing fleet and fishers with both being reduced to better match capacity with available resources. In principle, this should lead to pressure on the fisheries’ income as derived demand for fishers decreases. Concurrently, the introduction of MBEIs will lead to improvements in the fisheries economy, increase profits and rents, and hence also augment wages for fishers in share systems (Asche et al., 2018). Meanwhile, other factors may also influence the wage level of fishers including the price obtained for the catch and the variable costs of the fishing operation, which are generally deducted before shares are obtained.

Different pay systems (e.g. crew shares and its distribution among participating fisher groups, fixed salary with or without bonus) give rise to different incentive structures and may or may not support overall sustainability objectives for fisheries, or objectives for making the fleet more efficient. Different fisheries participants – that is to say the quota owners, vessel owners and crew – also have different incentive structures. For example, in pay systems based on a share of fishing trip grossing the fishers on board will be interested in maximising the quality and quantity of the fish landed to ensure highest prices and highest pay. The incentive to improve quality, however, depends on the pricing mechanism used to determine the ex-vessel price. On the contrary, fishers in systems based on fixed ‘salaried’ income may not be quite so interested in ensuring quality since their salary is paid regardless of the outcome of the fishing operation.

Differences in fisher pay incentive structures may also be found with respect to discards, since in share pay systems it may be considered better to discard fish to ensure the greatest turnover based on the retention of higher quality fish. Accordingly, there is a direct link between fisher pay systems and whether this works for or against fisheries’ sustainability objectives. Vessel and quota owners also have different incentives. Vessel owners’ investments extend over several decades and in a specialised market for second-hand fishing vessels, which may be very thin. Depending on the nature of the property rights of the quota, the quota can resemble any other financial asset and may be in a market where it can be readily sold. This implies that the participants in the fisheries (crew, vessel owner, quota holder) have different incentives, potentially leading to some principal-agent problems.

It has been observed (Nielsen et al., 2018) that in some countries that have introduced market-based economic instruments (MBEI) in their fisheries management, the pay for fishers has increased less than the pay for quota owners. Likewise, Høst and Christiansen (2018) observe that, in MBEI systems, it may be difficult for fishers to become quota owners or skippers. Consequently, there are issues of social equity and the acceptance of such management systems, which may have their origins in the way the pay/salary system works.

Although the resource rents in Nordic fisheries have been identified based on different assumptions of the opportunity costs of labour (Holland, 2011; Nielsen, Flaaten and Waldo, 2012; Waldo et al., 2016; Nielsen et al., 2017; Flaaten and Heen, 2017; Hammerlund et al., 2018), earlier work does not consider fisher pay systems directly, nor that the fisheries sector in the Nordic countries has undergone profound management reforms over the past decades. Nor is there a discussion to be found on the influence on fisher pay systems depending on whether fish landings are channelled as direct landings to processors or through auction markets. This work seeks to bring these two aspects into the discussion, thus highlighting the dynamic nature of the fisheries sector. While fisher pay systems based on share or lay are the most commonly uses in the Nordic countries, they have also proven very resilient over time considering the major structural changes towards MBEI systems.

This work seeks to map out the pay systems in the fisheries sector of five Nordic countries: Denmark, the Faroe Islands, Greenland, Iceland, and Norway. A key question that arises is whether changes in management regimes across the Nordic Region in recent years have benefitted fishers, considering the use of share-based salary systems. In making the harvesting sector more efficient and sustainable, one would expect that overall fishery grossing will increase for two reasons: firstly, the balance between stock size and capacity ought to improve; and secondly, profitability ought to increase due to technological developments. More specifically, the purpose of this work is to shed light on how changes to fisheries management settings in selected Nordic countries has influenced economic outcomes with an emphasis on fishers’ revenues.

Indeed, the findings in this study suggest that fishers are very well paid compared to other occupations. Although this may reflect several factors, including a risk premium for being a fisher, we also observe that in line with the introduction of new management regimes, the fishers who remain in the sector continue to bring home substantial salaries that are well above the wage levels one might expect from similar land-based jobs. This is likely to reflect the fact that the increased rent in the fishery is captured by the fishers due to the share system, and not only by the vessel or quota owners. This has implications for resource rent taxation policy.

This chapter is structured as follows. The next section reviews the relevant literature for the pay systems for commercial fishers. There is scant published material in this field and, as noted above, the material does not consider the dynamic nature of the fisheries sector against the background of fisheries management reform. The following section provides an overview of the pay systems for commercial fishers in Denmark, the Faroe Islands, Greenland, Iceland, and Norway. Finally, the last section provides a discussion of the results and some concluding observations.

Literature review

(Sutinen, 1979) develops an analytical model for the remuneration of fishers with a view to assessing under which conditions fisher and fisheries entrepreneurs consider the share system to benefit both. He concludes that if the share system were to be replaced with a wage system, then the total number of fishers and their individual incomes would fall. He furthermore observes that fishing entrepreneurs are better off in a share system as that system allows some sharing of the risk involved in fishing operations.

A recent article (Matthiasson, 2020) suggests that the ‘share’ or ‘lay’ system used in most fisheries has its origins in medieval times. He observes that “the lay system in use in medieval times in Scandinavia long predates the industrial revolution and may well reflect the social relations of pre-industrial societies that based their subsistence on hunting”.

In other words, the share system is not new and has deep historical roots. It is therefore interesting to observe that little research has been done in this area. Also, the little research that has been done has been rather selective and consider that the prevalent use of the share or lay system in fisheries is motivated by the vessel owners’ preference to share risk (McConnell and Price, 2006). Meanwhile, the risk-sharing perspective does not consider the dynamics of the fisheries sector, such as the introduction of new fisheries technologies or changes in management settings, and how this alters the production risk (output). Furthermore, previous studies fail to consider that the price risk has altered due to changes to the traditional marketing scheme. For example, landings are now sold via auction or landed directly to processors, possibly through forward integrated companies. In addition, over the past two decades, many countries have reformed their fisheries sector to put their fisheries on a more sustainable footing, while also shrinking the number of vessels and fishers to a size commensurate with the available resources. These changes have implications for fisheries’ revenues defined as a share of earnings from fishing trips and their incentives, such as in order to improve catch quality.

Substantial changes to fisheries management regimes in Nordic fisheries have been introduced over the past several decades in response to the need to put fisheries on a more sustainable footing (Nielsen et al., 2018). In most cases, these changes have been gradual in the Nordic countries. Iceland first introduced MBEIs into its fisheries management in 1984 when a demersal ITQ management system was established. In 1990 a system of ITQ covering almost all fisheries in Iceland was established, with almost full transferability of quotas. This system led to very dramatic increases in profitability and rent generation (Knutsson et al., 2015, Gunnlaugsson et al., 2019 and 2020). Norway, Denmark and the Faroe Islands later followed suit by introducing variants of MBEIs. In the meantime, the fisheries were regulated with various forms of regulated restricted access with different forms of licenses and quotas, through regulated fishing days, as well as technical measures such as mesh size regulations to ensure a minimum size of the fish caught, and seasonal closures.

Nielsen et al., (2018) suggests that fishers’ income in the Nordic countries that their study covered has increased substantially in recent decades. Their study also underscores, and our own literature review confirms this, that most studies looking at fisher revenues are local in nature in that they study only specific fisheries and communities. A publication by the Nordic Council of Ministers (Nielsen et al., 2017) notes that “knowledge on salary levels in fisheries is sparse in the scientific literature, with knowledge on salary during fisheries reforms being largely non-existent”.

Nevertheless, some studies have been published that analyse the use of share systems and the implication of this for fisheries. (Matthiasson, 2020) looks at the specificities of Icelandic fisheries and how fundamental changes to the Icelandic fisheries management systems have influenced remuneration. A particular trait of the Icelandic fisheries is that many vessels are part of vertically integrated organisations, often owned by land-based processors. This arrangement creates an issue of internal prices between fishing and processing. This led to some disputes between fishers and operators, which resulted in the creation of the Fish Price Resolution Committee in 1998. Its objective is to assist in negotiations between fisher unions and vessel owners, chaired by the Ministry of Industries and Innovation.

Another study explores the effects on crew remuneration and rent distribution by estimating several management targets (Guillen et al., 2015). Such modelling requires detailed data, which is available for the French Bay of Biscay Norway lobster fishery. In the study, they conclude that “in a share remuneration system, crew salaries can significantly increase when economic performance of the fleet improves […], allowing the crew to capture a portion of the fisheries’ rent”. This leads the authors to observe that in such circumstances ‘economic rents’ are not equal to ‘profits’. In a later article Guillen et al. (2017) concluded that “in shared remuneration systems, therefore, fisheries management measures also have an impact on labour costs and crew wages”. It follows that any analysis of fisher pay should consider the management regime.

In their analysis of Bering Sea/Aleutian Islands crab fisheries Abbott et. al. (2010) report that following the introduction of individual fishing quotas, remuneration increased, often substantially. “Given that the share formulas used to pay crew have remained fairly stable, this implies that the base on which the share is calculated (essentially revenues net of most variable costs) has increased substantially on a daily basis for many vessels – a consequence of IFQ-induced cost reductions and/or increases in live landings per day”. As such, it makes sense to discuss whether resource rent seeps into the remuneration of fishers.

1. Overview of pay systems for commercial fishers

Denmark

The number of employed and those in full-time employment fell between 2010 and 2018 by 8% and 15% respectively. In 2000, 3,410 people were in full-time employment. The major structural adjustment in Danish fisheries with the introduction of individual transferable quotas and vessel quota shares between 2004 and 2007 spurred a substantial reduction in employment. Between 2000 and 2010, the number of employed fell from 3,410 to 1,158 – a reduction of 66%. While employment continued to fall between 2010 and 2018, the reductions are smaller and relatively stable.

From 2010 to 2018, the Danish fishing fleet shrank by 686 vessels, or 24%, to 2,123 vessels. The number of active vessels fell by 178 vessels over the same period, corresponding to a decline of 26%. The number of less active vessels fell by 299, while the number of inactive vessels was down by 209. Measured as tonnage, the registered fleet contracted by 10%, while engine power decreased by 13% during the period (Nielsen et al., 2019).

Danish landings consist of fish for human consumption and fish for reduction (animal feed), see Table 1.1. The most important species for human consumption are mackerel and herring as well as the demersal species cod, plaice and Norway lobster. The most important industrial species for reduction to fishmeal and oil are sandeel, sprat and Norway pout. The small Danish vessels are mainly fishing with nets for demersal species, while the larger vessels use trawl and seines. The largest vessels target pelagic fish and fish for reduction. Some vessels specialise in fishery for mussels and horse shrimp.

| Landing quantity (1,000 tonnes) | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | Percentage change (2010-2018) |

| Fish for consumption | 166 | 171 | 191 | 196 | 194 | 207 | 226 | 216 | 225 | 36% |

| Fish for reduction | 541 | 446 | 205 | 353 | 412 | 543 | 334 | 570 | 465 | -14% |

| In foreign ports | 121 | 100 | 107 | 121 | 139 | 120 | 111 | 118 | 99 | -19% |

| Total | 828 | 717 | 503 | 670 | 745 | 870 | 671 | 904 | 789 | -5% |

| Landing value (EUR million) | ||||||||||

| Fish for consumption | 207 | 245 | 237 | 210 | 203 | 231 | 292 | 272 | 281 | 35% |

| Fish for reduction | 118 | 101 | 57 | 94 | 82 | 125 | 91 | 91 | 107 | -10% |

| In foreign ports | 75 | 80 | 98 | 99 | 103 | 97 | 106 | 93 | 83 | 11% |

| Total | 400 | 427 | 393 | 404 | 389 | 453 | 489 | 455 | 470 | +18% |

Table 1.1: Landings and landing values of active Danish vessels in Danish and foreign ports, 2018

The average salary cost per person in full-time employment in 2018 is EUR 125,000. This number, however, hides the substantial differences between vessel sizes and type of fishery, as shown in Table 1.2.

The average salary cost per person in full-time employment spans from EUR 62,065 for dinghies to EUR 248,406 for vessels above 40 metres in length using a combination of trawl and seines. These numbers reveal that salary costs per person in full-time employment increase with vessel size. Although it is expected that the same can be said for salary, crew costs are also higher for the large vessels as the fishing trips last longer and so crew costs are higher.

| Vessel group | Net | Dinghies | Seines | Combi | Trawl | Other |

| <12 m | 74,810 | 62,065 | 82,780 | 73,107 | ||

| 12-15 m | 104,677 | 92,056 | 82,272 | 95,051 | ||

| 15-18 m | 103,185 | 103,252 | 100,500 | |||

| 18-24 m | 107,278 | 117,000 | 126,698 | |||

| 24-40 m | 121,130 | 124,466 | ||||

| >40 m | 248,406 | 152,513 | ||||

| Horse shrimp | 130,629 | |||||

| Mussels | 112,465 |

Table 1.2: Salary costs per person in full-time employment on active vessels, allocated per vessel and gear, 2018, EUR[1]Full-time employment is calculated as total working days on active vessels, set at 220 working days per year.

Footnotes

- ^ Full-time employment is calculated as total working days on active vessels, set at 220 working days per year.

Nielsen et al., (2017; 2018) made a study where data on the vessel, catch, landing and sale register from the Directorate of Fisheries were merged with data from the register of taxable income from Statistics Denmark. The average income of a full-time fisher in 2012 was EUR 57,614, of which 14% was non-fishery income. For all persons with any income from fishery, the average income was EUR 56,500, with 31% being non-fishery income. The average income of coastal fishers, defined as working on board vessels up to 17 metres in length, was EUR 45,800. In 2012, the average income comparably measured for all Danish citizens including the employed, unemployed and retired was EUR 34,000. This rises to EUR 48,700 in agriculture, to EUR 54,100 for craftspeople, to EUR 48,500 for commerce and office workers, and to EUR 58,200 for process/machine operators (Nielsen et al., 2018). To this end, fishers are relatively well paid.

Minimum wages are determined through collective negotiations between employers and employees on board fishing vessels. Together, the Danish Fishermen Producer Organisation and the Danish Pelagic Producer Organisation cover more than 95% of total catches and represent the vessel owners, while the organisation 3F United Federation of Workers in Denmark represents the hired fishers.

These two parties negotiate a collective Agreement on Working Conditions (AWC) in the Fisheries Sector including on minimum wages and pension. The current AWC of 9 March 2017 runs for three years from 2017 to 2020 (Danish Fishermen Producer Organisation and 3F United Federation of Workers in Denmark 2014; Danish Fishermen Producer Organisation 2017). The agreement establishes that crew members work with all kinds of jobs on board the fishing vessel, without official titles and salary levels, although these may be established outside the collective agreement in the crew share system. The agreement guarantees fishers a minimum salary per fishing day of EUR 171 and a pension of EUR 34 per day in 2020. As for the minimum wage, there is no difference between fishery types or between types of work on board. A price index regulates the minimum salary.

While the agreement is negotiated between the two parties it is important to note that Danish fisheries are characterised by many vessels which are owner-operated, often with very few or no hired crew members. Although updated numbers are not available, in 2012, 20% of the active vessels were owner operated (Nielsen et al., 2018). In these cases, the collective agreement is only of minor importance.

The negotiations follow the rules of the Danish Labour Market Model that was established in 1899. The partners decide individually their demands for the negotiations and the normal negotiating period is between one and three months. If the partners cannot agree, then first a mediator steps into the process. If this fails, strikes and lockouts can be effective. After some time, the Danish parliament can intervene.

The crew share system allocates vessel earnings to each crew member. It works by fixing shares of the landing value for each crew member on each fishing trip, excluding some specified costs paid beforehand. Crew shares are decided by way of individual negotiations between the vessel owner and each hired member of crew and agreed in the hire contract for each fishing trip. The position on board and the experience of the hired fishers determine the crew shares. Typically, the shares lead to a higher salary than the minimum salary. If not, the vessel owner must pay the minimum salary to the hired crew.

Crew shares are calculated as the gross value of the catch minus costs paid beforehand, including unloading, bridge toll paid to harbours, vessel servicing, fuel, ice, box rent, provisions, pensions, union fees, fees for the producer organisations, and renting of fishing rights.

With both catches and costs differing according to vessel size, area fished, type of gear etc., the shares allocated to each crew member differ between vessels. For example, a vessel of 22 metres may have a skipper that owns the vessel, two crew members and an apprentice. The shares could be 60% for the vessel, 20% for the skipper, 8% for each senior crew member and 4% for the apprentice. For a six-day fishing trip, the catch value could be EUR 50,000 and cost paid beforehand EUR 15,000, leaving EUR 35,000 for sharing. Accordingly, EUR 21,000 goes to the vessel, EUR 7,000 to the skipper, EUR 2,800 to each senior crew member and EUR 1,400 to the apprentice. Since all crew shares are higher than the minimum salary for six days, the crew shares are paid.

Other types of vessels may have different crew sizes, different costs paid beforehand, and different allocations of crew shares. For smaller vessels with only one crew member, crew shares are higher and consequently the vessel share lower.

The income of fishers is taxed as for everybody else in Denmark. The only difference between fishers and other payers of income tax is that fishers have a ‘fisher deduction’ of EUR 25 per day with a maximum of EUR 5,573 per year in 2018.

To support this study, interviews with several centrally placed persons from the fisheries sector were conducted in August 2021, supplemented with informal talks with skippers and fishers. Those interviewed agreed that the fisheries sector is unique in the way pay is agreed, in that the fisher contract is for the duration of the fishing trip only.

Fishers are paid based on a share system. The vessel’s share and variable costs such as fuel and ice are deducted from the gross value of landings. The rest is then divided among the crew and skipper according to a fixed percentage. Crew members are paid in case of sickness and there is a common agreement on pensions. The general observation is that the parties are satisfied with the system and that it is unlikely to change much in the foreseeable future.

All interviewed persons agree that the fishers are paid a fair share and that salary levels are well above the average of Danish workers. Salaries have been on the increase following the introduction of the ITQ system as overall returns are shared among fewer crew and vessels. In addition, the Danish fishing fleet lacks fishers due to a skewed age structure (many fishers and skippers are retiring) and because of the existence of alternative jobs in the offshore and windfarm sectors.

Two major initiatives have started to address the lack of fishers. One concerns the contracting of foreign fishers from other EU countries, Iceland and the Faroe Islands. Another initiative concerns the recent Apprentice Agreement whereby vessel owners pay into a fund in return for hiring an apprentice on board, a system which is run by the Danish Fishermen Producer Organisation.

The interviewees are generally content with the present system which is robust and worth defending. In respect of future negotiations on the agreement, a holiday arrangement may form part of the discussions. In addition, it was observed that as fisher pay is irregular and highly variable, a system with regular payments could form part of future talks. This may also help address the problems of the recruitment of younger people to the fisheries sector.

The socio-economic return in 2018 stood at EUR 120 million, corresponding to 25% of the total landed value of the Danish fleet (see Appendix 1 for a technical description of socio-economic returns in fisheries). This is higher than before the introduction of the individual transferable quota system, which highlights the importance of the fisheries’ management settings. Between 2002 and 2018, the distribution of the socio-economic return between labour, capital and the public sector changed considerably. While in 2002 labour received 42%, this fell to 13% in 2018. The corresponding figures for capital are 34% and 63%, and for the public sector 24% and 24%. It can be concluded that it is the fishers that bear the burden of the Danish fishery reform in the sense that they receive a smaller share of the overall socio-economic returns. Capital (vessel/quota owners), meanwhile, has been able to secure a major part of the socio-economic return following the introduction of the ITQ system.

However, between 2002 and 2018, full-time employment fell from 3,087 to 983 fishers and so their socio-economic return in real terms stood at EUR 32 million in 2002 compared with EUR 16 million in 2018. These figures suggest an average increase for labour’s socio-economic return of just shy of 60% over the same period. As the interviews revealed, this may be the reason why the crew still seems to be content with the situation and their salary levels.

Faroe Islands

Commercial fishers’ pay in the Faroe Islands is almost entirely based on a revenue sharing system. There is a minimum wage system of DKK 1,100 per fishing day (the equivalent to EUR 150) when catches are low. This is financed by the fishing industry through a levy of 0.6% on landed value. This is sometimes used in demersal long-line fishing around the islands, whereas pay far exceeds the minimum for larger vessels. It should be noted that the minimum wage is not part of the vessel’s accounts, so the figures below do not include this. The fishers and vessel crew also get a 14% tax break (compared to workers in the rest of the economy) for income up to DKK 470,000 per year (approx. EUR 63,000).

The share of the total revenue that the fishers earn is determined by way of negotiations between the shipowners and the fishers’ organisations that take place every other year. The last negotiations concluded in May 2020. The Faroese government has no role in these negotiations. The different shares are often based on historical conditions and do not change much over time. The system of pay is quite complex and differs across different vessel groups.

In general, fishers on long-liners get a much larger share of the revenue than fishers on purse seiners, with trawlers and factory trawlers somewhere between the two. On the vessels, the different roles of the crew give them different salaries. The captain usually earns around two to three times the salary of the deckhand, while the engineer and cook get half of the extra pay that the captain earns.

Table 1.3 below gives examples of share distributions for the different groups of vessels. Table 1.3 does not explain all the complexities of the agreements between the fishers and the shipowners. The first column is the percentage of the sales (turnover) which determines the basic share or part. The captain, for example, gets one additional part on trawlers. This means that if the sales were DKK 100 million for a trawler with 27 men on board, then the deckhands get DKK 27 million divided by 27, which is DKK 1 million each. The captain then earns DKK 2 million, the engineer DKK 1.75 million, and the cook DKK 1.25 million. The parts differ according to the type of vessel.

| Calculation of basic part for deckhand | Captain | Engineer | Cook | |

| Long-liners | 43% | 2.15 parts added | 0.8 parts added | 0.25 parts added |

| Trawlers | 27% | 1 part added | 0.75 parts added | 0.25 parts added |

| Factory trawlers | 37.75% | 2 parts added | 1 part added | 0.25 parts added |

| Pelagic vessels | 17.5% | 1.75 parts added | 0.9 parts added | 0.25 parts added |

Table 1.3: Parts for crew members

Figure 1.1: Salaries as a percentage of sales (= turnover) for the different groups of fishing vessels, 1996-2017

Although the salaries are negotiated as a stable percentage of sales, actual salaries can vary considerably over the years (see for example the long-liners in Figure 1.1). One reason for this can be that long-line shipowners can subtract some of the costs, such as oil, before calculating fishers’ pay. Oil prices fluctuate, often making such costs considerable and highly variable, which can in turn affect the percentage in the figure above.

In recent years, fishers have had a large increase in their salaries which is particularly true for fishers and crew on pelagic vessels. Figure 1.2 shows the salaries per full-time employee for the vessel groups (Salaries per full-time employee for the different groups of fishing vessels, 1996-2017 in DKK thousand). This is what one would get if one participated in every fishing trip. However, it should be observed that there are typically two crews on pelagic vessels, so one would only get half that salary if one was on this vessel. On the other hand, small vessels such as long-liners have a much lower salary, and there is often only one crew.

Figure 1.2: Salaries per full-time employee for the different groups of fishing vessels, 1996-2017 in DKK thousand

Although the annual pay on pelagic vessels and factory vessels is quite large, trawlers and especially long-liners do not have this level of salaries. For all groups, the salaries have been on the increase since 1996. While these numbers are not adjusted for inflation, there has nevertheless been an increase in real salary levels over the period.

The number of fishers has been declining in the Faroe Islands (see Figure 1.3). However, for the groups included in this analysis there has not been a large decline. The decline has been among small-scale fishers. As Figure 1.3 shows (number of full-time fishers for the different groups of fishing vessels 1996-2017, right scale shows total, left scale shows individual vessel groups) there were almost 1,000 fishers at the start of the century but this has since declined to around 700. It is particularly in demersal fishing that the number of fishers has fallen.

The interview part for this study was carried out in June 2021 through talking to the chair of the Faroese Fishermen’s Association, Mr. Jan Højgaard. There is a general feeling that fishers are well paid, and this is true in particular for the roughly 200 fishers participating in pelagic fisheries in the North-East Atlantic and the cod fishery in the Barents Sea. At the other end, smaller scale fishers fishing with long-lines and nets have long workdays, less turnover and do not feel overpaid.

It is observed that vessels today are better and that working conditions have improved considerably. This has been thanks to improvements in fishing gear and fishing technology. As a result, fishers have better work/life conditions. When considering the level of fisher pay, the possibility of injury and early retirement must be taken into account due to the hard work involved in some fleet segments. Meanwhile, the interviewee noted that low salaried fishers have difficulties in obtaining bank loans (such as for a home) as their income stream is uncertain.

Figure 1.3: Number of fishers (FTEs) in the different groups of fishing vessels from 1996 to 2017 (estimated from number of vessels in 2016/17).

Fishers are included in the general unemployment insurance system of the Faroe Islands. This general system does not have any fisheries-related provisions such as compensation for poor catches. It is also noted that few fishers benefit from the system.

Socio-economic returns have been identified for two vessels groups commercially active in the Faroe Islands for both 1997 and 2017. The two groups are smaller demersal fishing vessels operating around the isles and regulated through effort regulations system, and demersal factory vessels fishing in the Barents Sea regulated by an ITQ system. The main observation from comparing the two fleet segments relates to costs. The smaller vessels under effort regulation have been subjected to considerable costs increases and, despite a 50% increase in turnover for the group, costs have increased far more and rendered this fleet segment unprofitable in 2017. Conversely, factory vessels with the same 50% increase in turnover have been much better at managing costs and pre-tax profits more than tripled between 1997 and 2017. This suggests that there are benefits accruing to the fleet under an ITQ system in a way that enables them to manage the cost structure of their fishing operations more easily.

As to salary levels, both vessel segments have fared well. The annual average salary for the smaller vessels has almost doubled between 1997 and 2017 and almost tripled in the case of the factory vessels. Compared to salaries in alternative employment, the 2017 figures are telling: at EUR 82,345 per annum for the smaller vessels and EUR 163,569 for the factory vessels, compared to EUR 53,333 for alternative employment. Consequently, fishers are paid considerably more than comparable land-based jobs.

The calculated socio-economic returns for the two fleet segments also paints an interesting picture for the Faroe Islands. Figures reveal that the principal ‘winners’ are the public sector and labour. The returns to capital (vessels and quota owners) have fared poorly in the case of both the small-scale segment and factory vessels. These observations underscore the importance of the regulatory system in generating socio-economic returns. Conversely, however, as returns to labour have increased over the years in both fleet segments, it does not seem plausible to conclude that returns to labour hinge on the different management settings.

Greenland

Greenland and the Greenlandic economy is highly dependent on the fishing industry. The fishing industry accounts for 95% of total exports. The importance of fishing is also evidenced by the large number of people employed in the industry.

In 2018, the Greenlandic workforce totalled 26,848 of which 4,332 people were employed in the ‘fishery and fishery-related industry'[1]Includes both employment in the primary catch activity as well as processing. as their main occupation. This means that approximately 16% of the total Greenlandic workforce receives their main salary from the fishery and fishery-related industry.

Figure 1.4 shows that in 2018, in Greenland 7,772 people had ‘fishery or fishery-related industry’ as their primary income for at least one month per year. This may include seasonal employment in the processing industry and activities connected to dinghies and hunting. The relatively large number of people who receive some income from the industry for at least one month each year indicates that the industry is largely seasonal and that weather can have a considerable impact on the activity over the year.

Footnotes

- ^ Includes both employment in the primary catch activity as well as processing.

Figure 1.4: Number of people occupied in the Greenlandic fishing industry, 2008-2018

In recent years the number of vessels fishing with line and fishing from a dinghy has increased while the number of vessels fishing with trawl, net and pot has decreased. This development may be a sign of better profitability for the halibut and cod fisheries, which are harvested with line by dinghies. We also observe that the trawl, net and pot fleet segments have contracted and, in so doing, have become more efficient.

Inshore fishing is characterised by landings of whole non-processed fresh, iced fish landed by small vessels, and dinghies at shore-based collection points in the settlements. Offshore fishing is characterised by big oceangoing vessels with on-board processing facilities to cook and freeze, for example, shrimp and Greenland halibut and packaging for direct sale to the retail sector for processing.

| 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | |

| Offshore trawler | 119,310 | 172,538 | 196,590 | 175,271 | 159,658 | 195,420 | 193,268 | 152,399 |

| Offshore trawler, foreign | 29,896 | 29,617 | 55,591 | 23,447 | 24,504 | 24,636 | 24,853 | 25,280 |

| Total offshore | 149,206 | 202,155 | 252,181 | 198,718 | 184,162 | 220,056 | 218,121 | 177,679 |

| Inshore trawler | 58,206 | 43,654 | 38,168 | 33,944 | 41,349 | 44,125 | 39,876 | 42,893 |

| Inshore vessel | 22,421 | 22,792 | 23,102 | 24,987 | 30,817 | 26,719 | 23,684 | 24,016 |

| Inshore dinghy | 25,211 | 32,537 | 33,578 | 35,228 | 42,308 | 40,614 | 37,009 | 37,887 |

| Total inshore | 105,838 | 98,983 | 94,848 | 94,159 | 114,474 | 111,458 | 100,569 | 104,796 |

| Total (tonnes) | 255,044 | 301,138 | 347,029 | 292,877 | 298,636 | 331,514 | 318,690 | 282,475 |

Table 1.5: Total landings from Greenlandic and foreign vessels in Greenland by vessel group (tonnes)

Table 1.5 shows that inshore and offshore trawlers catch the largest number of fish landed in Greenland. Overall Greenlandic vessels land most of the fish in Greenland, while foreign fleets contribute around 10%.

Table 1.5 also shows the value of the total inshore landings according to vessel type. This statistic is only available for inshore fishing vessels. The relatively large increase in the total landed value attributed to dinghies could have several explanations. Firstly, and perhaps most importantly, improvements in control functions have increased the registration of landings. Secondly, it may also be a consequence of the modernisation of the value and logistics chains. Options related to transport and conservation, such as freezing, have improved opportunities to sell the fish to a larger market and at a better quality, which raises prices and revenues. Improvements to the value chain are especially relevant to the Greenland halibut, which has experienced an 41% increase in landing volume, while the landing value has increased 84%.

As seen in Table 1.6, dinghies, dog sleds and the like experienced the largest increase in total landing value with an increase of 127% in 2019 compared to 2012. The other vessel size categories experienced a somewhat similar increase in total value at 43%, 53%, and 64% respectively for the groups < 10m, 10-20m, and > 20m.

| 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | % change 2012 to 2019 | |

| Dinghies, dogsled etc, | 176 | 175 | 202 | 232 | 255 | 262 | 285 | 256 | 45 |

| < 10m | 346 | 332 | 494 | 492 | 748 | 563 | 575 | 633 | 83 |

| 10-20m | 1,296 | 1,199 | 1,580 | 1,524 | 2,027 | 1,844 | 1,949 | 2,232 | 72 |

| > 20m | 21,805 | 16,233 | 14,101 | 12,933 | 12,361 | 10,748 | 12,941 | 16,419 | -25 |

Table 1.6: Average landing value per individual vessel, DKK thousand

One of the most important companies is Royal Greenland, which is owned by the Greenlandic self-government. Another important company is the privately owned Polar Seafood. Both companies have factory and fishing vessels able to operate offshore as well as smaller inshore fishing vessels. In addition, the two companies have onshore processing plants focusing on cold water shrimp, Greenland halibut, and other species.

Niisa Trawl Aps, Sikuaq Trawl A/S, Artic Prime Fisheries ApS, Qaleralik A/S, Sigguk A/S, Angunnguaq A/S and Qajaq Trawl A/S are all private Greenland-based companies operating in the fishing sector using larger fishing vessels. Beside these, the companies operate smaller vessels of less than 30 metres in length that are typically family owned.

A central element of the fishing sector is vertical integration. For example, Royal Greenland and Polar Seafood have internal trade between the vessels and the landing points and processing facilities. This may create situations where it is difficult to establish the ‘right’ market price for the landed fish on which the crew remuneration is calculated, a situation which may create dissatisfaction among the crew members.

With respect to wage determination systems, the fishing fleet can be divided into three main categories:

- Corporate-owned large vessels, typically involved in offshore fishing activities where the workforce is covered by a collective agreement;

- Smaller and mid-size vessels, typically involved in inshore fishing activities, landing in local villages and settlements without a collective agreement; and

- Dinghies, which are either owner-operated or part of a loyalty system with the bigger corporations.

For the crew on vessels operated by the big corporations, there is a collective agreement system for determining crew payment. For the other vessels, crew payments are based on an informal system. Wages and part-sharing are determined from vessel to vessel and from settlement to settlement. Bear in mind that, in many cases, small-scale fishing is operated as a family business in small-scale fishing communities.

The big vessels in Greenland are generally owned by bigger companies like Royal Greenland, Polar Seafood, Niisa Trawl, and the like. Royal Greenland is government-owned and has a collective agreement with the Greenlandic trade union, SIK.[1]SIK, Sulinermik Inuussutissarsiuteqartut Kattuffiat, is the biggest trade union in Greenland The collective agreement is written in Danish and covers the crew on Royal Greenland trawlers of more than 300 GT. The crew consists of various skilled and unskilled labour, and engine technicians. The privately owned companies Polar Seafood Greenland and companies organised under APK[2]APK, Aalisariutinik Piginneqatigiiffiit Kattuffiat, The Greenlandic Offshore Fishing and Export Association have a collective agreement with the Faroese Maskinmeistarafelagið.[3]Maskinmeistarafelagið, a Faroese trade union for engineers also covering fishers in Greenland The agreement is written in Danish and is intended for engine technicians on board the two vessels ‘Polar Princess’ and ‘Polar Nanoq’.

Royal Greenland wage system – SIK

Specific data on the separate bonus agreements is only available for one collective agreement between SIK and Royal Greenland. The specific agreement has been in place since December 2000 and is still valid today. Royal Greenland is the largest fishing company in Greenland and, as mentioned, is the only company with publicly available information on their agreement. It would, however, be safe to assume that Royal Greenland, in some way, sets the standard and framework which other companies benchmark against.

For Royal Greenland crew, their wage consists of a) a fixed share determined by one of six different job positions and level of education, and b) a bonus determined by a share of the revenue from the sale of the landing, contingent on the total number of crew members. As an example, a fisher aged 18 or over working on a prawn trawler receives a salary of DKK 12,440 and a bonus of 0.42% of the revenue if there are 25 persons on board the vessel. If it is a halibut boat with 25 crew members the salary is the same, but the bonus share increases to 0.62%.

Polar Seafood – Maskinmeistarafelagið wage systems for big vessels

The Faroese Engineers Union has a collective agreement with Polar Seafood and other members in The Greenlandic Offshore Fishing and Export Association (APK), apart from Royal Greenland.

Compared to the Royal Greenland agreement, the Faroese Engineers Union agreement is more performance based. The wage system in the Faroese Engineers Union agreements solely takes the form of a part-based system, where all the crew receive an equal share of a crew-part, but with additional parts depending on job position and experience.

The crew-part share of the landed value is 37.75% for cod and demersal fisheries, and 28% in pelagic fisheries. The landed value is the sale at the first link in the value chain, less the cost of fuel (cod and demersal fisheries only) and other related costs (transport, sales costs, insurances, taxes and fees).

This crew-part is then divided equally by the number of crew and additional parts are added. As an example, a chief engineer will normally receive 1 part plus 1 part (in total 2.0 parts), while a lower-ranked engineer on board may receive 1 part plus 0.5 parts (in total 1.5 parts) and a fisher with more than 18 years of experience will receive 1 part.

In the agreement between Polar Seafood and Maskinmeistarafelagið, the crew share varies with the number of crew. The starting point in pelagic fisheries is 28% for 30 crew members with an increase/decrease of 0.45% per additional/fewer crew member. This means that if the fishing trip is made up of 24 crew members, they get to share 25.30% (28-(6*0.45) =25.30) of the landed value. When additional crew members are included on the trip, a smaller share goes to Polar Seafood. This arrangement helps to maintain the performance-based wage system. Finally, Polar Seafood crew receive a yearly bonus of 14% of the wage, which the company can withhold if there is misconduct.

Small and mid-size vessels (< 10m and 10-20m)

Small and mid-size vessels only account for 9% of total landings. The wage systems are usually very informal and based on unwritten customary rules. According to KNAPK[4]KNAPK, Kalaallit Nunaanni Aalisartut Piniartullu Kattuffiat, an interest group for Greenlandic fishers and hunters, a general wage determination system does not exist.

Wage determination often takes the form of a revenue sharing system, which is determined from vessel to vessel and village to village. There are examples of a wage sharing system among mid-size vessels, where the crew will share 45% of the landing revenue (gross) after the deduction of oil, supplies and the like, that is to say net landed revenue. How the 45% crew share is distributed among the crew is subject to changes and negotiation on board each vessel and for each fishing trip depending on the location and particular circumstances.

Dinghies

Dinghies are of great importance to the Greenlandic fishery economy and social fabric, especially in relation to the vessel size and geographical distribution, and its social importance to small and remote fishing communities. Dinghies accounted for 34% of the total landed value in 2019.

There is no singular wage system for this segment and the area is not regulated. Rather, this is a traditional community-based fishing operation by one or two people, often as a family operation, and is informal in nature. In this regard it should also be mentioned that due to its informal nature, there is likely to be an element of this fishery which is not accounted for officially and may be part of the ‘informal economy’ in Greenland.

There are cases where the big fishing companies such as Royal Greenland and Polar Seafood provide loans and/or help to fishers to enable them to become the operator and owner of a dinghy. In return, the loan is conditional on the understanding that the operators sell their catch to the company (e.g. Royal Greenland[5]Greenlandic media Sermitsiaq AG, https://sermitsiaq.ag/node/199971) in the local settlement.

There are also examples of Royal Greenland financing dinghies which then are leased to local fishers. In this way, Royal Greenland and Polar Seafood broaden their resource base of fish and provide opportunities for communities that depend on the fishing industry and fishers with limited resources of their own.[6]Royal Greenland news, August 2017 and January 2018

This way of financing a dinghy ensures the fishers’ loyalty and cements a dependency between the companies and the individual operator. There are known cases where Royal Greenland issues loans to fishers who are denied loans from commercial banks. In this way, Royal Greenland assumes the responsibility and risk of supporting local development in the settlements and villages.

Greenlandic income tax ranges from 42% to 44% depending on the municipality.[7]Greenland Tax Agency, Tax percentages Based on data from Greenland Statistics, actual taxation on inshore fishers’ salary after deductions has grown from 29% in 2008 to 36% in 2018.[8]Greenland Statistics [FID001]

For several years, it has been the goal of the Greenlandic government to impose a new uniform resource rent system across fishery sector. A task force consisting of the government and the fishing industry, among others, was established in 2016. The work of the task force resulted in the “Report on the Resource Rent in the Greenlandic Fishery and Proposals for New Resource Rent Models” (Ögmundsson & Haraldsson, 2017).

Prior to the reform of the resource rent in 2015, the report conducted by the task force established that, in total, Greenland receives DKK 0.78 per kilo of catch in tax, while Iceland and the Faroe Islands receives DKK 0.29 and DKK 0.24 per kilo respectively. This means that Greenland receives three times as much as the two countries that appear as the most comparable countries in the region (Ögmundsson & Haraldsson, 2017). The primary aims of the task force were to compare taxation systems in different countries and propose a revision of the resource rent in Greenland. Additionally, the task force was to develop concrete proposals for uniform, transparent and simple models for charging resource rent from fishery.

The Greenlandic government devised a new simple resource rent model valid from 1 January 2018. The resource tax rates are determined and published every quarter by the Greenland Tax Agency. The resource rent differs between catches that are landed and sold for domestic processing (indhandling) and for catches that are directly exported and not used in the local processing industry. Furthermore, a special regulation applies to pelagic species (Naalakkersuisut, 2017).

For the first quarter of 2018, landings for domestic processing are charged a resource rent of 5% of the landing value and, if the landing value accounts for less than DKK 8 per kilo, a basic tax of DKK 0.05 per kilo is paid (Naalakkersuisut, 2017). For catches that go directly to export, the resource rent amounts to a 5% charge of the export value if the price is between DKK 12 and DKK 17 per kilo. The resource rent increases by 1% per additional DKK 1 per kilo until the price per kilo is DKK 29. Exports with a value above DKK 29 per kilo are charged a resource rent of 17.5%. If the price per kilo is lower than DKK 12, the resource rent is DKK 0.2 per kilo, which corresponds to 1.6% (Naalakkersuisut, 2017).

The resource rent of pelagic species is based on a fixed price per kilo depending on whether the vessel is domestic or foreign, and depending on the species. For instance, for mackerel a domestic vessel pays DKK 0.40 per kilo, while a foreign vessel pays DKK 1.00 per kilo. (Naalakkersuisut, 2017).

Footnotes

- ^ SIK, Sulinermik Inuussutissarsiuteqartut Kattuffiat, is the biggest trade union in Greenland

- ^ APK, Aalisariutinik Piginneqatigiiffiit Kattuffiat, The Greenlandic Offshore Fishing and Export Association

- ^ Maskinmeistarafelagið, a Faroese trade union for engineers also covering fishers in Greenland

- ^ KNAPK, Kalaallit Nunaanni Aalisartut Piniartullu Kattuffiat

- ^ Greenlandic media Sermitsiaq AG, https://sermitsiaq.ag/node/199971

- ^ Royal Greenland news, August 2017 and January 2018

- ^ Greenland Tax Agency, Tax percentages

- ^ Greenland Statistics [FID001]

Iceland

Generally, Icelandic commercial fishers are paid catch shares. This has secured them a share of the high profitability of the fishing sector, making fishers among the best-paid professions in Iceland. Figure 1.5 shows a comparison of wages across selected professions.

Figure 1.5: Wages for selected professions in Iceland.

All the employed fishers are grouped as one, regardless of their job on board and the fleet segment. Fishers have similar pay systems with the difference mostly being how big of an extra share they receive. There are more differences in which kind of fisheries they take part in, the size of their vessel and type of gear. Self-employed fishers mostly use small boats and determine their own salary. They can be quota-owners or lease most or all of their catch quota, only owning their vessel.

Most of the quota is, however, owned by companies. Quotas are allocated to vessels, which can be run independently or by vertically integrated companies, which also run a processing plant and maybe even a sales company. That leaves fish processors without quotas. They must buy their fish from auction markets or through agreements with vessel operators to buy some of their catch. They routinely pay a higher price for the catch.

Fisher pay is determined based on collective agreements between organisations of vessel operators/owners and fishers. If the catch value does not reach a certain minimum, fishers get a fixed salary. One share corresponds to a deckhand share. This forms the basis from which the skipper gets one extra share (can be less for the smallest boats), the first mate half an extra share (second mate one-quarter, third mate one-eighth), the main engineer half an extra share (second engineer one-quarter, third mate one-fifth for larger engine vessels or one-eighth for smaller engine vessels), the cook a one-quarter extra share. On freezer trawlers, some extra shares are distributed to the boatsman, netting man and supervisor.

All vessel operators, except for freezer trawlers, must make a formal agreement with the crew of each vessel on the fish price and how the catch will be sold. There is a collective agreement for the minimum catch price for cod, haddock, redfish and saithe for direct sales in vertically integrated companies. This also influences some other catch values, such as for ‘development quota catches’. The minimum price is negotiated on a monthly basis by an official committee with representatives from fishers and vessel owner organisations (úrskurðarnefnd sjómanna og útvegsmanna). The price of other species is negotiated with each crew separately for direct sales. So, in some sense, the catch unit value represents an agreement of pay rather than the true price of fish.

If the catch is sold to a third party, the vessel operator negotiates the price of direct sales. If the catch is sold in auction markets, domestically or abroad, the price is fixed there.

Before the crew shares are calculated, vessel operators can deduct various costs from the gross value of the catch. They can deduct operating costs, which is a fixed percentage linked to the global market price of oil. A maximum cost of 30% of catch value has been most common for over a decade, with a temporary clause of a 0.5% deduction between 2017 and 2020 for direct sales in vertically integrated companies. For freezer trawlers it is a little less or a little more depending on whether sales are FOB or CIF. Also deducted are the cost of auction (around 5%), the cost of investment in new vessels (up to 10%) if the catch value is high enough, and the cost of transportation and customs for auction markets abroad (around 15% to 20%) with auction costs.

Smaller vessels of less than 30 GRT and 15 metres in length can only deduct auction costs and transport to auction markets abroad. However, they can also deduct the cost of gutting on land when the catch is sold at auction.

Crew share percentages per deckhand differ mostly by the size of the vessels in terms of gross registered tonnage, fishing gear, and how many crew members are on each fishing trip. For trawlers, their length is also considered, but for freezer trawlers the shares depend mostly on the number of crew.

A rule of thumb is that the smaller the boat, the higher the percentage of catch value per deckhand, but the catch is of course significantly less. Vessels of less than 30 GRT and 15 metres in length which qualify for the hook-and-line quota system, have a separate agreement that depends mostly on the number of crew, although if the hooks are baited on land the share per deckhand is less. There are also differences in extra shares per station; if there are very few on board they have less of an extra share. The crew should be able to choose which agreement is used.

Fishers who own their vessel and/or quota determine their own pay. They may not be paying themselves maximum salaries, for example for tax reasons. They also do have a reputation of receiving quotas at no cost in exchange for a lower price of fish.

The negotiation of general wage agreements is carried out on a national basis. It is primarily in the hands of fisher organisations (SSÍ/Sjómannasamband Íslands), engineer organisations (VM/Félag vélstjóra og málmtæknimanna) and skipper/mate organisations (FS/Félag skipstjórnarmanna) on one side, and the Federation of Icelandic Fishing Companies (SFS/Samtök fyrirtækja í sjávarútvegi) and the Confederation of Icelandic Enterprise (SA/Samtök atvinnulífsins) on the other. This major collective agreement sets the minimum wages for all employed fishers.

A special collective agreement for employed crews on smaller vessels was finally reached in August 2012. The agreement is between SSÍ/VM/FS and the National Association of Small Boat Owners (LS/Landssamband smábátaeigenda). At the time, the upper size limit was less than 15 GRT, thought to correspond to 12 metres in length at most. This was also the size limit for the hook-and-line quota system. In July 2013, the upper size limit for the hook-and-line quota system was changed to less than 30 GRT and 15 metres in length by law. There was some debate as to whether the agreement would follow the change in size limit. This not only affects pay systems but also which of the vessels can go fishing in the event of a fisher strike. According to a ruling of the Icelandic Labour Court (Félagsdómur) in 2017, the agreement can include vessels up to 30 GRT and 15 metres in length.

The duration of collective agreements is usually set at around two years but can have a much longer actual duration. The current agreement is from February 2017 and followed ten weeks of fisher strikes, with the previous agreement set in January 2009 and expiring in January 2011. Negotiations on new agreements were stalled by COVID-19 restrictions in 2020. In February 2021, the negotiations were referred to the State Conciliation and Mediation Officer and, as of September 2021, the fishers have terminated the negotiations. Future developments are unclear.

Over the years, the Icelandic government has regularly stepped into debates and negotiations in many ways. Fisher strikes have sometimes been stopped by law and been subject to arbitration, and there have been a number of attempts to introduce some sort of law regarding fish price and fisher pay. In 1998, the Directorate of Fresh Fish Price was established, working alongside an appointed price ruling committee of representatives established from earlier debates. The objective was to ensure public surveillance of fisher pay by surveying fish prices and to ensure that the objectives of the collective agreements were upheld, thus promoting fair wages for fishers.

One of the biggest issues at the time the directorate was established was the deduction of the cost of quota buying or leasing from catch value before the calculation of crew shares, which is prohibited by law and agreements. Although this is not as big a problem today, the issue still exists. Another issue was the price fixing of catch sales in vertically integrated companies, which continues to be a major challenge today particularly in pelagic fisheries.

There is a rich tradition for unionisation in Iceland among fishers. Separate unions exist for fishers, skippers and mates (officers), and marine engineers. During the interviews, which took place in early 2021, both fishers and quota/vessel owners agreed that the introduction of the ITQ system has had a major impact on wage negotiations. Fishers observe that there is a lack of transparency regarding the price obtained from the catch (when not landed via auction). There is also disagreement on the cost sharing, in particular related to pension contributions and government fees (fishing fees and carbon taxes). In addition, there is a sense that negotiations and general debates between fishers and their employers are getting tougher and harsher.

Leaders of fisher unions agree that fishers are well paid compared to other industries. Being a fisher/deckhand requires little formal education and even when compensated for harsh working conditions and the sacrifices of being away from home for long periods of time, fishers are well paid. On the other hand, for fishers’ unions, the introduction of the ITQ system seems to have mostly benefitted the vessel/quota owners. This is a feeling that is not shared to the same extent by the vessel/quota owners themselves.

The introduction of the Icelandic ITQ system has led to capital accumulation by vessel/quota owners and to a highly improved fisheries economy. This observation is shared by all stakeholders in the fishing industry. As for the representatives from the vertically integrated companies interviewed for this work, they note that the ITQ system saved fish stocks and the companies. For the most part, fishing companies are now thriving and resilient and profitable enough to enable them to invest in technology, marketing and innovation. Fishers, on the other hand, feel that the ITQ system has concentrated power, quotas and wealth in few companies. They also note a dichotomy in that the Fisheries Management Act states that fish stocks are the common property of all Icelanders. When a fishing fee was introduced by the government, this situation led to a dispute as to who was to bear the costs of this, i.e. the fishers or the quota owners.

Characterised by many companies that are forwardly integrated, the calculation of resource rents is complex and requires assumptions about the ‘true’ price of fish sold from vessels to processing facilities. Such ‘transfer pricing’ has similarities to what happens in multinational conglomerates where there is extensive selling and buying between companies withing the same family of operations. But it is unique in the Nordic fisheries sector, except for Greenland, and a main characteristic of the Icelandic fishing setup.

While Iceland was one of the first countries in the Nordic Region to introduce MBEIs in its fisheries sector, it was very slow to produce the desired economic outcomes. Introduced in 1991 in Iceland’s most important fisheries, it took two decades before some stability was found due to falling catches, fleet over-capacity, and lack of consolidation, which could possibly have its origins in the forward integration nature of the industry. Another reason could be the debt burden and subsequent financial costs of quota holdings that were purchased in order to remain in the industry. In this regard, it is observed that an important part of the potential rent generated was grandfathered by the initial quota holders when they left the industry. Since 2010, however, things have improved and the industry has been profitable.

Wages to fishers are high compared to similar land-based work. In 2019, wages were 41% higher than that of land-based work and fisher salaries have increased significantly over the past two decades. In terms of resource rent, the Icelandic calculations made for this study show that, in recent years, the part of the rent going to capital and the public has been increasing while the rent to labour has been relatively stable. However, when compared to earlier years when the industry was undergoing adjustment, the rents going to labour and the public have been declining.

Norway

The Norwegian pay system for commercial fishers is relatively egalitarian based on the ‘lott’ revenue sharing system and where the income is shared among the participating fishers albeit with differences reflecting experience. ‘Lott’ is the term used for the revenue resulting from the fisheries catch. In Norway, collective agreements between fishers’ unions and the boat owners federations detail how the ‘lott’ is to be distributed between the boat owner and the fishers (Bergland & Pedersen, 1999). For the coastal fleet, the collective agreements are between the crew section and boat-owner sections in Norges Fiskarlag (The Norwegian Fishermen’s Association), while for the trawler and purse seine fleet the agreement is between Norsk Sjømannsforbund (The Norwegian Seafarers Union) and Det Norske Maskinistforbund (Norwegian Union of Marine Engineers) on the one side, and Fiskebåt – Havfiskeflåtens forbund (The Norwegian Boat Owners Association and High Sea Fleet Association) on the other.

Two types of revenue sharing scheme are used. Coastal fisheries using conventional fishing gear apply the net income to calculate the ‘lott’, whereas for pelagic fisheries the ‘lott’ is calculated from the gross revenue. Bergland and Pedersen (1999) discuss why the two fisheries apply different ‘lott’ calculations. Firstly, in the pelagic fleet, the use of larger and more mobile vessels results in comparatively more predictable catches, that is to say less ‘risk in catch volumes’. In addition, the price also helps to stabilise incomes in those fisheries. Secondly, pelagic fishing vessel companies are often listed on the stock exchange and may therefore be less reliant on risk-sharing with crew than what is the case for the mostly smaller vessels in coastal fisheries.

In the coastal fisheries, Norges Fiskarlag (The Norwegian Fishermen’s Association) details the distribution of the ‘lott’ based on the fishing gear used, vessel length (feet) and storage volume (m3), and the number of fishers on board. For example, for a vessel of 30ft and 6m3 of storage using line fishing and with two fishers on board, the ‘lott’ should be 60% of net revenue (Norges Fiskarlag, 2019, p.22). After the deduction of operating costs, the two fishers (one being the owner) should share 60% of the net revenue, while the vessel receives the remaining 40%. A tradition is to share the ‘lott’ equally among the fishers, but considerations like experience and responsibilities can affect distribution. For example, an apprentice will typically receive half of what the regular fishers receive. In terms of the operating costs, an exceptionally long list of 34 items that may be deducted from the gross sales value has been established.

There is also a scheme to guarantee a minimum salary. This is triggered if the salary is below NOK 2,550 per week during the fishing period – that is the period in which there is fishing activity. The daily payment is calculated as 0.024 times the annual salary, as long this is does not exceed around NOK 600,000. The scheme is little used. The most common users are fishers in the Nordland County of Northern Norway using small vessels and who fish using nets (Svorken, Hermansen & Isaksen, 2012). The scheme does not appear to be misused and works as intended (Svorken, Hermansen & Isaksen, 2012).

Figure 1.6 shows fishers’ average nominal annual income levels by groups of vessel type. The highest income groups are fishers on board large cod trawling vessels, and vessels using purse seine or trawls for pelagic fisheries. Conversely, the lowest income levels are the coastal fisheries based on conventional gear and seine, which are also smaller units compared to the trawl and purse seine vessels. Consequently, capitalisation and economies of scale seem to play an important role for the level of fisher pay. As the graph shows, all the groups have had positive income development. The rate of income growth exceeds inflation, meaning it also represents real income growth.

The average income level in fisheries has, as depicted in Figure 1.7, been high relative to the average income level nationally in Norway in recent years. This underscores the fact that current economic conditions are good for fishers and there is no indication that recruitment to fisheries is difficult (Sønvisen, Johnsen and Vik, 2017). This suggests that the findings in Nielsen et al. (2018) about fishers being well off remains true to this date.

Figure 1.6: Average nominal annual fisher income levels by groups of vessel types.

Figure 1.7: Fishers’ pay compared to average income level in Norway.

Figure 1.8: Average nominal annual fisher income levels by size in cod/whitefish fisheries.

The role of vessel size is even clearer in Figure 1.8, which shows average nominal annual fisher income levels by vessel size in cod/whitefish fisheries including coastal vessels using traditional gear and cod trawlers. These fleets normally target cod and other demersal whitefish species. Fishers’ average income increases with vessel size and, for the largest cod trawlers, exceeds NOK 2 million per fisher for 2017 and 2018, while for the smallest vessels it was just above NOK 460,000 per fisher in 2018.

In support of this work, several interviews were carried out among stakeholders in Norwegian fisheries in June 2021. These included interviews with representatives of the fishing vessel owners in pelagic and demersal fisheries, the union of naval officers, as well as representatives of fishers and vessel owners in coastal fisheries. The interviewees share the view that fisher salaries have developed favourably following the restructuring of the industry with fewer vessels. In this regard, a consequence of the share system is increasing salaries for the vessels that have accumulated quotas.

By way of a background, it should be noted that the fisheries sector has been subject to significant structural change following the transition to a tradeable quota system in the early 2000s. This system has concentrated the ownership of fishing rights with the strongest concentration taking place in the ocean fleet (pelagic and cod fisheries) while the coastal cod fishing fleet has retained the most dispersed ownership.

An area of contention between vessel/quota owners and fishers is the extent to which the returns on additional quotas should be reflected in crew shares. On the one hand, the vessel/quota owners believe that the returns on their investments in additional quotas should not be shared with the crew, which acknowledges that they are providing the capital and assuming the risk for the restructuring of the fleet.

This point of contention exists in both the coastal and ocean fisheries sector and has been ongoing for several years. Due to the disagreement, the pay agreement from 2014 was not replaced until January 2021. As for the fisher representatives, they reported high levels of stress and fatigue during this period as they fought hard to maintain the status quo. Nevertheless, the overall feeling is that fishers have come out as ‘winners’ in terms of pay (and as a direct consequence of the lay share system) while quota and vessel owners are not content with the present sharing of profits.

Recently, young people training to become fishers through the public education system have become vocal about the difficulties they face in entering the fisheries due to the current individual quota system. In March 2021, a new branch exclusively for young people (Ungdommens fiskaralag) was formed within the fishers’ union. Although it is not obvious that this group yet has any real power, the existence of a youth branch serves as an indicator of the complexity of managing the diverging interests held by the different groups in the fisheries system.

In terms of the resource rent accruing between 2003 and 2018, thus covering the introduction of the tradeable quota system, the overall resource rent from both pelagic and the demersal fisheries has increased considerably. In the pelagic fisheries, total resource rent increased from NOK 371 million in 2003 to NOK 1,426 million in 2018. Comparable figures for the demersal fisheries are NOK 249 million NOK and NOK 2,005 million.

Meanwhile, in the pelagic fisheries the distribution of the resource rent shows that the public sector, capital and labour have all fared well, with labour taking slightly more than the other two. This contrasts with the demersal sector where the public and labour take the largest share, while the net remuneration of capital is low. Consequently, these calculations underscore the feeling among the interviewees that quota/vessel owners feel that they have not been sufficiently compensated for their investments.

Finally, the views of fishers that have exited the fisheries due to the restructuring have not been heard in this process. We are unaware of their situation. However, the fishers’ unions expressed that the consolidation has gone far enough. According to them, further accumulation of fishing quotas on individual vessels is not called for, since they feel that vessel owners already earn sufficient profits. This stance signals that it is now more important to protect fishers’ employment than to raise their salaries.

Discussion and conclusion

This work has explored the fisher remuneration systems used in five of the Nordic countries: Denmark, the Faroe Islands, Greenland, Iceland, and Norway. The share, or lay, pay system is widely used. Even with the introduction of the far-reaching reform of fisheries management, the share system is remarkably stable and may be considered an ‘institutionalised’ part of the fisheries economy. In addition, over the past decades, technological advances in fisheries operations have substantially reduced the risk for returning to ports empty handed and have made fishing a less physically demanding undertaking. This can be observed by the marginal use of minimum salary provisions in fisheries.

Fishers have a clear interest in keeping the share system as changes in fisheries management settings and investments in equipment that improves efficiency have increased salary levels. In all the surveyed countries, average fisheries income is above that of similar occupations on land. Granted, we would expect a premium paid to fishers due to the job characteristics such as being away from home over several days, the physical demands of the job, and the risk involved. However, the figures from across the Nordic countries suggest that fishers are compensated far beyond their job characteristics and well above alternative job possibilities. Due to the share pay system, fishers, even when not quota owners, may also capture part of the resource rent.