- Full page image w/ text

- Table of contents

- Acknowledgements

- Executive Summary

- Abbreviations

- 1. Introduction

- 2. The Trade Impacts of Fossil Fuel Subsidies

- 2.1 Types and Pathways of Fossil Fuel Subsidy Trade Impacts

- 2.2 Sense of Scale

- 2.3 Examples of Trade Impacts of Fossil Fuel Subsidies

- 3. Fossil Fuel Subsidies Under WTO Subsidy Rules

- 3.1 Subsidy Definition

- 3.2 Prohibited Subsidies

- 3.3 Actionable Subsidies

- 3.4 Notification

- 3.5 Potential for and Limitations of Challenging Subsidies through the ASCM

- 4. Disciplining Subsidies to Support the Clean Energy Transition

- 4.1 ASCM Remedies

- 4.2 WTO Reform: Fossil fuel subsidies

- 4.3 WTO Reform: Renewable energy subsidies

- 4.4 Plurilateral and Regional Trade Agreements

- 5. Conclusions and Recommendations

- References

- About this publication

MENU

Contents

Acknowledgements

The authors would like to thank the Nordic Council of Ministers for supporting the production of this report. We owe gratitude to Tristan Irschlinger and Alice Tipping for their guidance during the preparation of the report. We would also like to acknowledge and thank the following people for their insightful reviews: Dominic Coppens, Aaron Cosbey, Ilaria Espa, Gillian Moon, Christian Slattery, and Peter Wooders. Any mistakes are the responsibility of the authors. The opinions expressed and the arguments employed in this update do not necessarily reflect those of the peer reviewers and funder, nor should they be attributed to them.

Harro van Asselt

University of Eastern Finland Law School; Stockholm Environment Institute; and Copernicus Institute of Sustainable Development, Utrecht University

Tom Moerenhout

International Institute for Sustainable Development; and Columbia University School of International and Public Affairs

Global Subsidies Initiative

This report was produced as part of the International Institute for Sustainable Development's (IISD) Global Subsidies Initiative (GSI). GSI supports international processes, national governments and civil society organizations to align subsidies with sustainable development. GSI does this by promoting transparency on the nature and size of subsidies; evaluating the economic, social and environmental impacts of subsidies; and, where necessary, advising on how inefficient and wasteful subsidies can best be reformed. GSI is headquartered in Geneva, Switzerland, and works with partners located around the world. For more information, see: www.iisd.org/gsi.

Executive Summary

Subsidies for the production and consumption of fossil fuels, estimated at USD 478 billion in 2019, strain the public purse, contribute to climate change by supporting the burning of fossil fuels and slowing the uptake of renewable energy, and lead to local air pollution and associated impacts on public health. Fossil fuel subsidy reform can, therefore, lead to a wide range of socioeconomic and environmental benefits.

As the only global institution with binding rules to regulate subsidies, the World Trade Organization (WTO) would seem well suited to addressing fossil fuel subsidies. In contrast with measures to support renewable energy, however, fossil fuel subsidies have, by and large, remained unchallenged under the organization’s dispute settlement mechanism. Against this backdrop, this report explores whether WTO subsidy rules and practices are fit for purpose in addressing fossil fuel subsidies and supporting the clean energy transition, and how these rules and practices could be reformed to more effectively contribute to these important objectives. It also offers practical suggestions on what next steps could look like for WTO members and other stakeholders interested in moving this agenda forward.

Trade Impacts of Fossil Fuel Subsidies

The report shows that fossil fuel subsidies can lead to direct and indirect trade effects. The former means that the subsidy strengthens the competitiveness of the subsidized producer. The latter refers to pass-through trade effects that give downstream producers using subsidized inputs a competitive advantage, although they do not benefit directly from a subsidy. Relevant trade impacts include the reduction of a competitor’s world market share, the displacement of imports, and the reduction of the competitiveness of alternatives. These trade impacts can affect upstream fossil fuel products, refined energy carriers, and downstream non-energy products that use fossil fuel products as inputs (e.g., as feedstock or to produce fossil fuel-generated electricity). Moreover, the trade impacts of fossil fuel subsidies can affect trade and investment in renewable energy products, a particular challenge from the perspective of the much-needed clean energy transition. The likelihood of such trade impacts materializing is high due to the competitive densities of relevant industries (particularly oil, gas, petroleum products, and energy-intensive industries), the magnitude of trade volumes, and their monetary value.

Fossil Fuel Subsidies Under the Agreement on Subsidies and Countervailing Measures

Fossil fuel subsidies may therefore lead to a host of trade impacts. Taking the desirability of reforming fossil fuel subsidies as a starting point, an essential legal question thus concerns the extent to which existing WTO subsidy rules – in particular under the organization’s Agreement on Subsidies and Countervailing Measures (ASCM) – can effectively constrain the use of such support measures.

Subsidies under the ASCM are defined as a “financial contribution by a government or any public body” or “any form of income or price support” that confers a “benefit.” The ASCM definition covers fossil fuel subsidies provided by governments, other public bodies vested with government authority, and private bodies entrusted/directed by a government, potentially including state-owned enterprises. Fossil fuel subsidies can fall under several categories of the ASCM subsidy definition, including a direct transfer of funds, government revenue foregone, provision of goods and services, and/or income or price support. While demonstrating the existence of a fossil fuel subsidy may be fairly straightforward in some cases, it may be more difficult in others. For example, establishing that government revenue has been foregone can be challenging, as it requires identifying the benchmark (tax) treatment against which the preferential treatment for fossil fuels would be compared. If it can be shown that a government has foregone revenue, however, a benefit will be deemed to have been conferred. If a fossil fuel subsidy consists of a financial contribution on terms more favourable than the market (e.g., a loan with low interest rates), a benefit will also likely have been conferred.

WTO subsidy rules contained in the ASCM only apply if measures are “prohibited” or “actionable”. Prohibited subsidies include export subsidies and local content subsidies. Some fossil fuel production subsidies can be argued to constitute prohibited export subsidies if it can be established, among others, that the recipient is export-oriented and domestic markets are becoming saturated. Although the use of local content requirements is widespread in the fossil fuel sector, such measures should be considered investment measures rather than subsidies.

Subsidies are actionable if they are “specific”, meaning that they are aimed at certain enterprises or industries. Although consumption subsidies, which benefit a wide range of energy consumers, are unlikely to meet the specificity requirement, fossil fuel production subsidies are more likely to be deemed “specific”. Moreover, production subsidies benefiting several extractive industries (including fossil fuels) or certain enterprises within a specific geographical region could be argued to be “specific”.

If actionable subsidies create “adverse effects” for another WTO member, they may be challenged. “Adverse effects” refers to injury to the domestic industry of another member, nullification or impairment of the benefits gained from tariff concessions under the General Agreement on Tariffs and Trade (GATT), or serious prejudice to the interests of another member. Demonstrating “serious prejudice” is generally more difficult than demonstrating injury, as the former needs to be causally linked to the subsidy itself, whereas the latter needs to be caused by the subsidized import. Establishing that pass-through trade effects are caused by a specific fossil fuel subsidy will therefore be particularly challenging. Moreover, the trade effects of fossil fuel subsidies on renewable energy products (e.g., solar cells, wind turbines) are only disciplined to a minimal extent by the WTO’s current subsidy rules, which constitutes an important weakness in the context of the clean energy transition.

Information on fossil fuel subsidies can support a challenge under the ASCM. However, even though members have an obligation to notify all specific subsidies under the ASCM, notification rates have been low. Another way in which information on fossil fuel subsidies can be generated is through the WTO’s Trade Policy Review Mechanism, but members have made only limited use of that option so far.

Overall, the ASCM offers some potential to challenge fossil fuel subsidies, particularly production subsidies, but any such challenge faces strategic, political, and legal-evidentiary hurdles. If WTO subsidy rules are to play a role in supporting the transition to cleaner energy systems, however, the main limitation of the ASCM is that it focuses solely on (some of) the trade-distorting effects of subsidies. It does not take into account the social and environmental externalities of fossil fuel subsidies, including the effects on climate change. At a time when acting to tackle climate change is more important than ever, this shortcoming has led to growing interest within the multilateral trade policy community about possible ways in which it could be addressed.

Pathways to Reform

WTO members interested in changing the status quo could pursue several pathways to reform WTO rules and practices, acting alone, in a small coalition of members, or multilaterally.

Members could first explore the legal space offered by the ASCM to challenge fossil fuel subsidies. Although the outcome of any challenge is uncertain, members that experience adverse effects can initiate an investigation and – if the evidence suggests that a subsidy exists that leads to injury – impose countervailing duties. Alternatively, a member can challenge prohibited or actionable subsidies through the WTO’s dispute settlement mechanism. While challenging actionable subsidies requires a member to demonstrate adverse effects, prohibited fossil fuel subsidies could, in principle, be challenged by any member.

With a ministerial statement on fossil fuel subsidy reform, some WTO members have already sought to move the issue up on the multilateral agenda. Efforts to ensure that WTO rules and practices better address fossil fuel subsidies and support the clean energy transition could focus on strengthening transparency and/or developing new disciplines.

The transparency of fossil fuel subsidies is an important prerequisite for their phase-out. Efforts to improve transparency around such measures are already ongoing in various international forums, including through the United Nations Sustainable Development Goals (SDGs), under which countries can report subsidies following an internationally agreed methodology. These efforts could be complemented in the ASCM context by (1) members improving compliance with their notification obligations; (2) members making greater use of counter-notifications; or (3) making the notification of all fossil fuel subsidies mandatory. In addition, members could use the WTO’s Trade Policy Review Mechanism to either report on their own fossil fuel subsidies or raise questions about other members’ fossil fuel subsidies. Lastly, a group of WTO members could also, on a voluntary basis, pledge to undertake fossil fuel subsidy reform and review each other’s progress. To garner political support for these various options, they could be linked to broader WTO transparency reforms.

WTO members could also seek to negotiate new rules under the WTO, either through an amendment of the ASCM or through negotiating a stand-alone agreement on fossil fuel subsidies. The latter would seem to be an attractive option in that it would allow negotiators to start from a blank slate. Both options could lead to new subsidy prohibitions, with a greater focus on the environmentally harmful impacts of fossil fuel subsidies. Doing so will require methods to distinguish between (types of) fossil fuel subsidies, particularly with regard to their climate change effects. New disciplines could also specify possible exceptions to the rule, which could be temporary or permanent, for instance, for specific groups of countries and/or specific types of subsidies (e.g., subsidies aimed at providing energy access to low-income communities or that are not considered environmentally harmful). Moreover, a subsidy phase-out requirement could be linked to the provision of technical assistance and capacity building for some countries. Although a promising option from an ambition perspective, negotiating new rules will be challenging both technically and politically. Importantly, the successful adoption of new WTO disciplines on fisheries subsidies can help set the stage for such negotiations. The fisheries subsidies example also shows, however, that it can take a long time before any agreement is adopted.

In addition to reforming WTO rules to curtail fossil fuel subsidies, members could also provide further space for support to renewable energy. Fossil fuel subsidies can be considered market-distorting in that they cause environmental harm that is not reflected in the price of fossil fuels. Renewable energy subsidies, by contrast, can be viewed as correcting such a market distortion. To date, several renewable energy support measures have been deemed incompatible with WTO law, although this was mainly due to their use of local content requirements. Nevertheless, measures to support the production of (widely traded) renewable energy technologies, such as solar cells and wind turbines, may still be at risk. Several suggestions have been put forward to create more policy space under WTO rules, including (1) applying the environmental exceptions of Article XX GATT to the ASCM; (2) reviving the list of non-actionable subsidies under the ASCM so as to include renewable energy support measures; and (3) adopting a waiver to temporarily allow WTO members to subsidize renewable energy. However, for each of these options, a key challenge is to define what types of subsidy practices should be permissible, taking into consideration the local and global as well as short- and long-term environmental and economic effects of renewable energy subsidies.

At a time when the WTO is beset by broader challenges, including the Appellate Body crisis as well as persistent difficulties in progressing with negotiations, members could also negotiate plurilateral or regional trade agreements to address fossil fuel subsidies. One important forum in this regard is the recently launched negotiations for an Agreement on Climate Change, Trade and Sustainability (ACCTS), whose participants aim to develop rules based on the effects of fossil fuel subsidies on climate change. The negotiations could thus offer important lessons on how to design rules for fossil fuel subsidies that could work for the green economy, possibly encouraging broader efforts at the multilateral level at a later stage. Although some regional trade agreements include provisions on fossil fuel subsidies, they are limited in their level of detail and obligation.

Recommendations

Recommendation 1: WTO members should strengthen the transparency of fossil fuel subsidies, including through improved notification, the Trade Policy Review Mechanism, SDG reporting, voluntary peer reviews, and drawing on other sources.

There is an urgent need to strengthen the transparency of fossil fuel subsidies by governments, and WTO members can play a role in supporting this effort in various ways: (1) making use of the various WTO mechanisms, including the ASCM notification mechanism, counter-notifications, and Trade Policy Reviews; (2) voluntarily reporting fossil fuel subsidies under SDG 12.c following the methodology created for the indicator on fossil fuel subsidies; and (3) where relevant, undergoing a fossil fuel subsidy peer review through the G20 or Asia–Pacific Economic Cooperation or through a voluntary initiative to undertake a self- or peer-review. To improve the transparency of fossil fuel subsidies, WTO members can draw on external sources, including databases maintained by the Organisation for Economic Co-operation and Development and the International Energy Agency. These sources can be complemented by ongoing efforts by civil society organizations to shed light on members’ fossil fuel subsidy practices.

Recommendation 2: WTO members should explore the available space to challenge fossil fuel subsidies under existing subsidy rules.

Existing rules provide space to challenge other members’ fossil fuel subsidies before the WTO dispute settlement system, either as actionable subsidies or as prohibited subsidies. In some cases – where data availability is not a problem, where trade effects can be observed or are likely, and/or where an export subsidy is likely – fossil fuel subsidies may be deemed inconsistent with the ASCM. Although launching any such challenge will depend on broader political and strategic considerations, a dispute and the resulting jurisprudence could help shed light on the extent to which WTO disciplines can effectively address fossil fuel subsidies.

Recommendation 3: WTO members should launch an informal dialogue on the prospects and challenges of disciplining fossil fuel subsidies more effectively through the WTO at the next Ministerial Conference.

Creating new multilateral disciplines on fossil fuel subsidies will likely take a long time. Members interested in moving this idea forward therefore need to begin discussing the options for doing so as soon as possible. Efforts such as the ACCTS negotiations and the Fossil Fuel Subsidies Reform Ministerial Statement at the WTO should draw wider participation, at the very least from those countries and regions that have committed to phasing down fossil fuel subsidies, that have stated leadership aspirations in the area of climate change, and that have expressed their willingness to green trade agreements. In addition, it will be important to invite major subsidizing members to join the discussion so as to better understand the reservations and concerns that some may have with regard to the impact of any new disciplines on their economies. The next WTO Ministerial Conference, which was postponed due to the COVID-19 pandemic, offers a key opportunity for members to launch an informal dialogue to this end.

Recommendation 4: Further research should involve in-depth studies of the trade effects and legality of specific fossil fuel subsidies.

Further in-depth studies of particular fossil fuel subsidies could look into the trade effects of these subsidies and/or assess the legality of such subsidies in the context of the ASCM. Such research would contribute to further clarifying in which circumstances current WTO subsidy rules can really constrain the use of fossil fuel subsidies.

Recommendation 5: Practical analysis should be generated on the ways in which rules on fossil fuel subsidies could be crafted with a focus on their environmental impacts.

With a view to negotiating new, environmentally focused disciplines on fossil fuel subsidies, new analysis would be required to explore how such rules could best be crafted. Such analysis could help identify which (types of) fossil fuel subsidies should be subject to prohibitions based on their environmental harmfulness, what types of circumstances could warrant an exception, and how to apply rules to countries with different development priorities. Specifically, the analysis could point to potential trade-offs between the social and economic development priorities that countries may pursue through fossil fuel subsidies and the emissions associated with such subsidies. The analysis could further identify the prevailing types of subsidies that countries are struggling to reform.

Abbreviations

| ACCTS | Agreement on Climate Change, Trade and Sustainability |

| APEC | Asia–Pacific Economic Cooperation |

| ASCM | Agreement on Subsidies and Countervailing Measures |

| CPTPP | Comprehensive and Progressive Agreement for Trans-Pacific Partnership |

| G20 | Group of 20 |

| GATT | General Agreement on Tariffs and Trade |

| IEA | International Energy Agency |

| ITC | International Trade Centre |

| OECD | Organisation for Economic Co-operation and Development |

| OPEC | Organization of the Petroleum Exporting Countries |

| PTC | Production Tax Credit |

| SDG | Sustainable Development Goal |

| TRIMs Agreement | Agreement on Trade-Related Investment Measures |

| UNEP | United Nations Environment Programme |

| WTO | World Trade Organization |

1. Introduction

Subsidies for the production and consumption of fossil fuels constitute a sizeable burden for public finances. They further contribute to climate change – directly, by providing financial support for the burning of fossil fuels, and indirectly, by slowing the uptake of renewable energy and hampering the clean energy transition – as well as to local air pollution and subsequent impacts on public health. Reforming fossil fuel subsidies therefore is an opportunity to address global and local environmental challenges while saving money for the public purse. Despite these widely agreed benefits, subsidies continue to be handed out in many countries, with the Organisation for Economic Co-operation and Development (OECD) and International Energy Agency (IEA) estimating them at USD 478 billion in 2019 (OECD, 2020). This support can take many forms, including setting prices above or below-market rates, offering tax exemptions, providing favourable loans, or building a railroad from a coal mine to a port (Steenblik, 2007). Consumer subsidies usually aim at reducing the costs of fossil fuel for users and tend to be found more in developing countries. Producer subsidies provide support to fossil fuel producers by increasing the price or lowering exploration, extraction, research and development, and production costs, and are often found in both developed and developing countries.

As fiscal instruments of energy policy that can have numerous social, economic, and environmental effects, it is not surprising that fossil fuel subsidies are governed by a range of energy, trade, and sustainable development institutions (Van de Graaf & van Asselt, 2017). Among these institutions, the World Trade Organization (WTO) would seem well suited to address fossil fuel subsidies for various reasons. Not only can fossil fuel subsidies have distorting impacts on trade and investment (Burniaux et al., 2011; Moerenhout & Irschlinger, 2020), the WTO also has a wide membership, plays a key role in regulating trade-distorting subsidies across economic sectors, and hosts a strong dispute settlement system (Wooders & Verkuijl, 2017).[1]At the time of writing, the WTO dispute settlement system is under challenge due to the refusal by the United States to appoint new Appellate Body judges over concerns of judicial overreach. As a result, since December 2019, the Appellate Body no longer has the required minimum of three members to review appeals. However, although the WTO’s Agreement on Subsidies and Countervailing Measures (ASCM) does, in principle, also apply to fossil fuel support measures, fossil fuel subsidies have largely avoided challenges. This stands in stark contrast with renewable energy, with several high-profile WTO disputes revolving around the legality of renewable energy support measures (Espa & Marín Durán, 2018).

Against this backdrop, this report will explore the extent to which existing WTO subsidy rules are fit for purpose in addressing fossil fuel subsidies and supporting the clean energy transition, suggesting ways in which the multilateral trade body could more effectively contribute to these important goals. To do this, the report will start by highlighting how and the extent to which specific types of subsidies could have an impact on international trade (Section 2). Building on this, the report will assess the extent to which fossil fuel subsidies with a trade impact could be disciplined under current WTO subsidy rules, pointing to the potential as well as the shortcomings of the existing legal framework (Section 3). The report will then identify options for strengthening international trade rules, in particular at the WTO, so as to more effectively contribute to fossil fuel subsidy reform and the associated transition to clean energy alternatives (Section 4). With a view to advancing this crucial objective, the report will conclude by offering concrete recommendations on a possible way forward for WTO members and other interested stakeholders (Section 5).

Footnotes

- ^ At the time of writing, the WTO dispute settlement system is under challenge due to the refusal by the United States to appoint new Appellate Body judges over concerns of judicial overreach. As a result, since December 2019, the Appellate Body no longer has the required minimum of three members to review appeals.

2. The Trade Impacts of Fossil Fuel Subsidies

2.1 Types and Pathways of Fossil Fuel Subsidy Trade Impacts

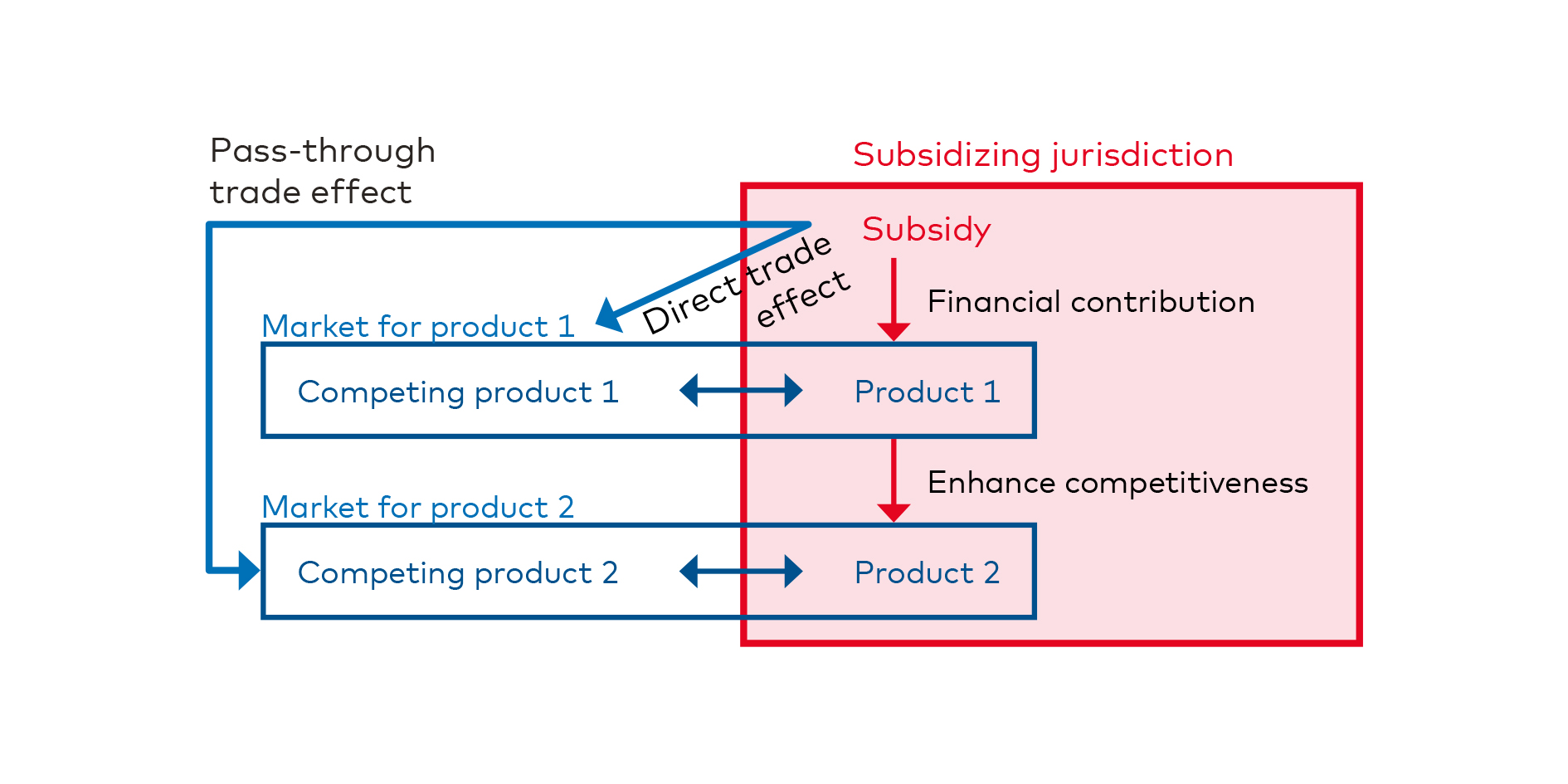

Subsidies to both the production and consumption of fossil fuels at different stages of the value chain can have an impact on international trade. These impacts can materialize through both direct effects and pass-through effects (Figure 1). Direct trade effects occur when a subsidy grants a financial contribution and benefit to the producer of a certain product and, as a result, increases its competitiveness vis-à-vis other producers of that specific product or producers of substitute products. Pass-through trade effects occur when a subsidy benefits the production and lowers the price of Product 1, which is then subsequently used as an input for the production of Product 2, thereby giving a competitive advantage to the producer of Product 2.

Figure 1. Direct and pass-through effects of fossil fuel subsidies

Source: Moerenhout & Irschlinger, 2020.

The key trade impacts that fossil fuel subsidies can have are in the reduction of a competitor’s world market share, the displacement of imports from a competitor, and the reduction of the competitiveness of alternatives. These trade impacts can occur for upstream fossil fuel products, refined energy carriers, and downstream non-energy products that use fossil fuel products as inputs. The latter include both industries that directly use fossil fuels as feedstock for their products (e.g., fertilizers, plastics) and energy-intensive industries that use a lot of fossil fuels or fossil fuel-generated electricity in their production process (e.g., steel, aluminum). Additionally, fossil fuel subsidies, in particular consumption subsidies, can also lead to the illicit smuggling of fuel products across borders.

The trade impacts generated by the direct effects of production subsidies can occur when subsidies provided to the producers of crude oil, natural gas, and coal affect upstream competition. In many countries, such production subsidies are often granted through mechanisms such as tax and royalty reductions. Generally, producer subsidies can affect upstream competition because of a price effect and an output effect. Fuel production subsidies can increase output and lower the price compared to competitors. That means that producing countries can cover more of domestic demand (i.e., import substitution) and export more (i.e., improve world market share), while the competitiveness of non-fossil fuel alternatives can also be reduced. Production subsidies can also be granted at the transformation stage to, for example, refineries and electricity producers.[1]Subsidies provided to the production or consumption of electricity are generally considered fossil fuel subsidies for the share of electricity that is produced from coal, natural gas, and oil. Similarly, this can have an impact on the competitive positions of their outputs.

Consumption subsidies that directly lower the end-use price of fossil fuel products can also generate trade impacts through direct effects when subsidies provided to fossil fuel consumers give them a competitive edge over competitors whose fossil fuel inputs are not subsidized. Such “consumers”, of course, include companies that transform raw fossil fuels into energy carriers, such as gasoline, diesel, and electricity, but also companies that use raw fossil fuels for the production of non-energy products, such as iron, steel, aluminum, and plastics. The resulting impacts are similar, as in the case of production subsidies and can include import substitution, an improvement of world market share, and reduced competitiveness of non-fossil fuel alternatives. These types of consumption subsidies also heighten the incentives for smuggling subsidized energy products to neighbouring countries with higher prices.

Finally, both fossil fuel production and consumption subsidies can have pass-through effects leading to trade impacts. This occurs when subsidies provided upstream lower the price of a product that is then used by companies downstream, which then get a competitive benefit from having lower-cost inputs. One example is how upstream natural gas extraction and transportation subsidies would lead to lower-priced natural gas that is then used by fertilizer producers, which would gain a comparative advantage vis-à-vis producers abroad that have to source natural gas at market prices. Just like subsidy reform can cause inflation that negatively affects industries that rely on energy products, fossil fuel subsidies can create pass-through effects that benefit industries vis-à-vis their international competitors.

Footnotes

- ^ Subsidies provided to the production or consumption of electricity are generally considered fossil fuel subsidies for the share of electricity that is produced from coal, natural gas, and oil.

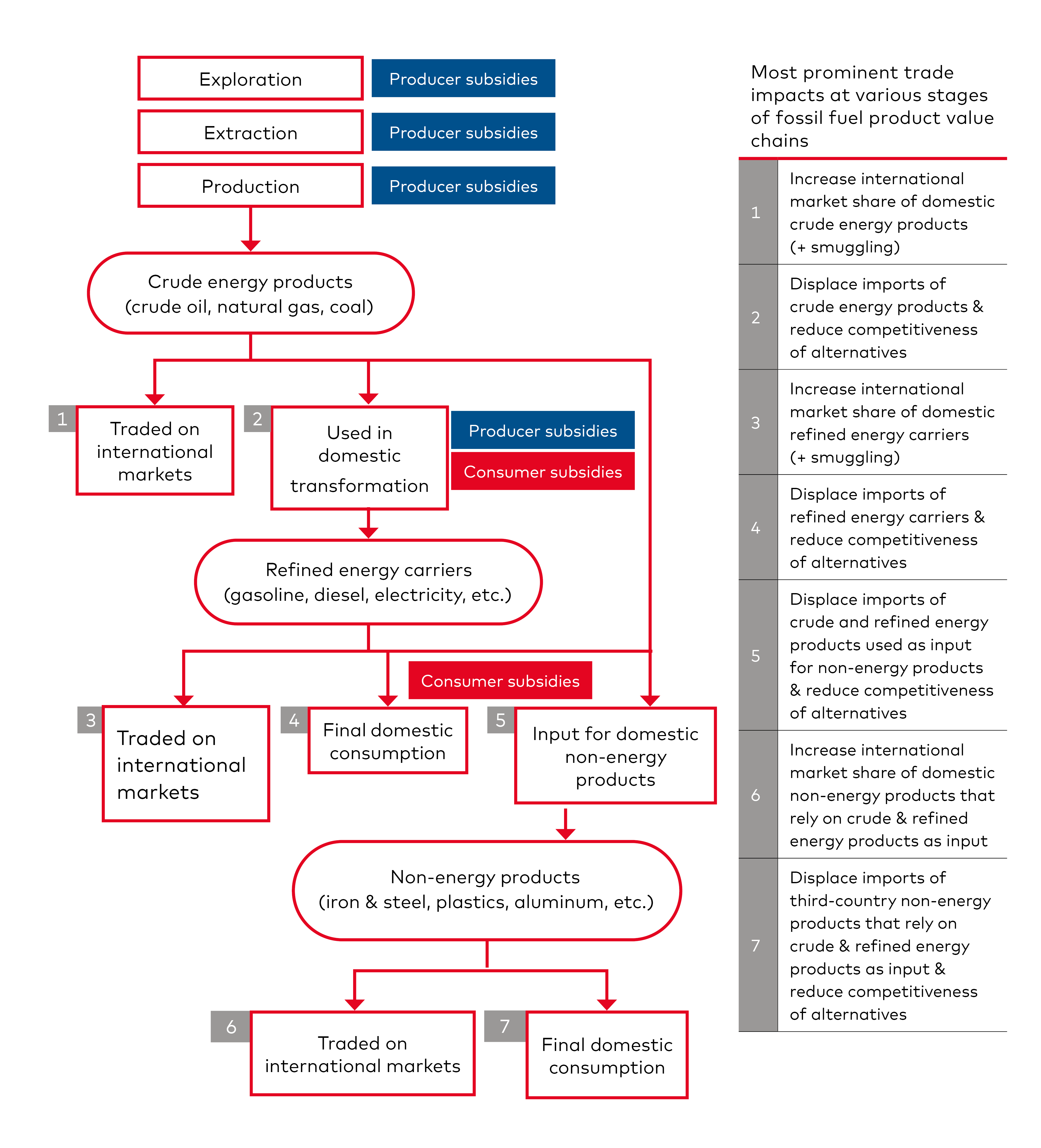

Figure 2. Trade impacts of fossil fuel subsidies at various stages of fossil fuel product value chains

Source: Moerenhout & Irschlinger, 2020.

2.2 Sense of Scale

The research on fossil fuel subsidy trade impacts is still in its infancy, but there are good reasons to believe that the scale of such impacts can be very large. Table 1 presents a summary of the main markets that can be affected and their trade exposure. In particular, it shows that the competitive densities of oil, gas, petroleum products, and energy-intensive industries are high. Such a competitive density indicates that there are a lot of suppliers and a lot of importers that use pricing to compete, which means that subsidies that help providers lower their market price can more easily have a decisive role in the battle for domestic and international market share. The competitive density of upstream coal is somewhat smaller but still open to significant competition among producers.

The trade volume of fossil fuel products and energy-intensive products is also very large. In 2018, 50% of crude oil, 25% of natural gas, 16% of coal, and 15% of petroleum products were exported before they were used (IEA, 2019a, 2019b, 2019c). Importantly, these trade volumes are associated with gigantic export values. In 2018, they represented a USD 2.3 trillion export market, which represented about 12% of the total value of all exported products worldwide or 3% of world GDP. Exports of crude oil alone were worth close to USD 1 trillion. Petroleum product exports were a close second, at about USD 800 billion.[1]The export value of fossil fuels in 2018 are based on data from the International Trade Centre (ITC), which can be accessed through its Trade Map tool: https://www.trademap.org/. With such enormously valuable markets, the scale of trade impacts of fossil fuel subsidies is likely significant, even in the case of low oil prices.

Footnotes

- ^ The export value of fossil fuels in 2018 are based on data from the International Trade Centre (ITC), which can be accessed through its Trade Map tool: https://www.trademap.org/.

Table 1. Affected markets and trade exposure

| Affected market | Annual trade volume (% of global prod.) | Annual trade value (USD, 2018) | Competitive density | Key trade impact |

| Upstream oil | ~ 50% | 943 billion | High | Battle for market share |

| Upstream gas | ~ 25% | 299 billion | High | Battle for market share |

| Upstream coal | ~ 16% | 124 billion | Medium | Battle for market share |

| Electricity | Very small | 35 billion | Small | Obstruction of trade |

| Petroleum products | ~ 15% | 779 billion | Very high | Battle for market share; smuggling of refined fuels |

| Energy-intensive industry | Industry-dependent | > 1 trillion | Very high for key industries | Battle for market share |

| Electricity-intensive industry | Industry-dependent | > 300 billion | Very high for key industries | Battle for market share |

Source: Moerenhout & Irschlinger, 2020.

Importantly, the trade impacts of fossil fuel subsidies are not only felt in fossil fuel markets but also in the markets for energy-intensive products that rely on fossil fuel products as an important input, such as fertilizers and plastics, as well as the markets for electricity-intensive products, like aluminum. The annual value of exports of energy-intensive industries is at the very least USD 1 trillion (based on four key energy-intensive industries). Electricity-intensive industries from their end are worth at least USD 300 billion.[1]The export values of energy-intensive industries in 2018 are based on data from the ITC, accessible via Trade Map: https://www.trademap.org/. The category “energy-intensive industry” is constructed by the authors and includes iron and steel, plastics and products made thereof, paper and pulp, base metals and products made thereof. “Electricity-intensive industries’” include aluminum and articles thereof. These conservative estimates show that fossil fuel subsidies have a sizeable potential impact on international trade because of their importance as an input for various industries.

Finally, it is very important to note that fossil fuel subsidies affect trade and investment in products that are alternatives to those that rely heavily on fossil fuels, such as renewable energy technologies and electric vehicles, and associated products such as high-capacity batteries. This trade – and more generally, economic – impact might not always be that clear because it is more diffuse. Fuel subsidies can affect underlying market conditions that can block the emergence and dissemination of alternative, potentially non-like products and services. It is nonetheless extremely important in relation to the widely recognized need to transition to cleaner and less carbon-intensive energy systems.

Footnotes

- ^ The export values of energy-intensive industries in 2018 are based on data from the ITC, accessible via Trade Map: https://www.trademap.org/. The category “energy-intensive industry” is constructed by the authors and includes iron and steel, plastics and products made thereof, paper and pulp, base metals and products made thereof. “Electricity-intensive industries’” include aluminum and articles thereof.

2.3 Examples of Trade Impacts of Fossil Fuel Subsidies

The following examples are intended to make the debate about the trade impacts of fossil fuel subsidies more tangible. It must be emphasized, however, that these subsidies are largely generic in nature, meaning that competitors in various countries often also benefit from similar measures. Having subsidies from different jurisdictions affecting the same international markets is not uncommon. These examples are thus illustrative. They have merely been chosen to illustrate the potential trade impacts of fossil fuel subsidies with concrete cases, but other examples could have been picked.

Coal and Electricity Subsidies to the Aluminum Industry in China

China has various subsidies across the aluminum value chain. These subsidies include both financial subsidies and non-financial input subsidies that include energy subsidies. Energy subsidies are especially important to support smelting, of which electricity costs represent about 40% of total production costs (OECD, 2019a).

In China, many aluminum producers rely on subsidized coal to power their own captive electricity plants, which leads to a lower per kWh cost than if coal had not been subsidized. Other aluminum producers rely on general electricity subsidies provided in the form of low power tariffs (OECD, 2019a). According to the IEA, such electricity subsidies in China amounted to USD 25 billion in 2018 alone (IEA, 2020). A third category of aluminum companies is able to receive direct electricity subsidies that lower the electricity price even more compared to other consumers. Such subsidies are then mostly provided by provincial governments (OECD, 2019a). These support measures related to coal production and electricity consumption can significantly increase aluminum producers’ competitiveness.

Work by the OECD strongly suggests that energy subsidies have spill-over effects on various segments of the aluminum value chain. In the last 15 years, China has become the leading producer of aluminum by far. China’s increase in aluminum output has depressed the global prices of various aluminum products and undermined the position of exporters elsewhere. This in itself would be a normal market adjustment if it were not for the fact that China’s aluminum prices are heavily influenced by these subsidies (OECD, 2019a).

One study estimated the trade impacts of China’s electricity subsidies to the aluminum industry in U.S. firms in 2008. Albeit slightly outdated, the study shows that trade impacts are likely significant. Results indicated that removing these subsidies would lead to a decrease in China’s exports and an increase in its imports. This would benefit the U.S. industry by increasing its own domestic market share, as well as picking up some of the global market share that China would no longer supply. This potential increase in U.S. exports was estimated at USD 100 million annually (Capital Trade Incorporated, 2009). As China’s subsidization practices continued, such associated losses ultimately led the United States to file a complaint with the WTO against Chinese aluminum subsidies, including electricity subsidies (WTO, 2017a).

Royalty Subsidies to the Adani Coal Mine in Australia

Adani Mining is an Indian company based in Queensland, Australia, that holds the licence to construct the Carmichael thermal coal mine in the Galilee Basin. The goal of the Carmichael coal mine is to produce thermal coal and export it to India with the purpose of being used in coal-fired power plants. The Queensland Government has announced that it would sign a “Royalties Deferral Agreement” with Adani Mining. It has also been noted that it would finance road infrastructure worth AUD 100 million (Swann, 2019). These measures can be considered as subsidies and could even constitute export subsidies (see Section 3).

Normally, companies pay mining royalties to the Queensland Government according to a sliding percentage of the price per tonne of coal exported (Queensland Government, 2019). Under the state’s “Resources Regional Development Framework”, it is possible for companies to defer the payment of royalties for a certain time and then pay them back, including interest. This Royalties Deferral Agreement, however, can only be signed if mining companies allow third-party access to its infrastructure and open up undeveloped resource basins.

A key factor that may plausibly make the Adani Royalties Deferral Agreement a subsidy (and perhaps a prohibited subsidy) is that the interest rate at which deferred royalty payments would be paid would be set at the state bond rate (Queensland Government, 2017), which is lower than commercial rates. This issue is further explored in Section 3.

Even though the size of the potential subsidy will ultimately depend on coal prices, some studies have suggested the value of the royalty deferral could be between AUD 215 million and AUD 318 million (Swann, 2019), while others suggest it might be worth around AUD 900 million over seven years (Buckley, 2019). It remains unclear, however, whether these figures measure the value of the deferral in total or the value based on the different interest rates. Regardless, it has been suggested that the potential subsidy may be very important for Adani Mining, given the difficulties it has had to finance the project and that, in fact, the royalty deferral may tip the balance between production and non-production (Smee, 2019).

Given that the clear and stated goal of the Carmichael project is exportation to India and other Asian countries (Adani Australia, 2019), the subsidy will automatically influence the international coal market. The exact production envisioned has been revised downward but would still be around 10 million tonnes per year (Smee, 2019), which is about 1% of current global thermal coal exports (IEA, 2019b). In Australia, thermal coal supply is saturated with demand, even decreasing (Cunningham et al., 2019). This is, among others, the result of various incentives given by Australia’s federal and state governments for renewable energy uptake, which reduces the need for domestic coal even more. The subsidy thus appears to have exportation as the primary objective, as evidenced by the fact that royalties are calculated based on the export price.

Upstream Production Subsidies to Shale Oil in the United States

The shale oil industry in the United States is undergoing a transformative time. Even before record-low oil prices and a crashing demand because of the COVID-19 crisis, the high debt of these companies and an unsustainable business model resulted in the downgrading of their stocks. Heralded as the bedrock of the United States’ “energy independence”, independent shale oil and gas producers have been able to rely on a wide range of fossil fuel subsidies that put them in a more competitive position than they would have been in without this type of support. U.S. shale oil and gas subsidies are a prime example of how many different subsidies at both the federal and state levels can affect the market for two products (crude oil and natural gas).

At the federal level, oil producers have been able to rely on generous subsidies, such as the expensing of intangible drilling costs (USD 1.6 trillion), excess of percentage over cost depletion[1]Natural resource firms are allowed to deduct from their taxable income the capital costs related the acquisition or creation of an asset through cost depletion (i.e., deductions in proportion to how much of the reserve has been depleted to generate income in a given year). Oil and gas companies are allowed to use percentage depletion (i.e., deductions as a percentage of the gross income generated, possibly up to 100% of the net income produced by the asset). This can allow them to deduct from their taxable income total amounts that are in excess of their original investment. See https://greenscissors.com/program/excess-percentage-cost-depletion-oil-gas/#:~:text=For%20natural%20resource%20assets%2C%20the,income%20in%20a%20given%20year. (USD 223 million in 2017), amortization of geological and geophysical expenditure (USD 60 million in 2017), and exception from passive loss limitation[2]Normally, taxpayers are allowed to deduct the losses they incur from passive activities but only to an amount equal to income generated from the activity. Oil and gas companies are allowed to deduct their excess passive losses against income generated from business activities in which they materially participate. See https://greenscissors.com/program/passive-loss-limitations-exemption/. (USD 40 million in 2017). Natural gas producers are often able to rely on similar subsidies but also specific ones, such as the accelerated depreciation of natural gas distribution pipelines (USD 140 million in 2017) (China et al., 2016; OECD, 2020). These estimates are often contested, with some research institutions estimating a higher monetary value for each of these subsidies (Oil Change International, 2017).

Fossil fuel companies are also allowed to undervalue their inventory and taxable income by “last-in, first-out” accounting, a scheme that is not unique to oil and gas producers but often used by them. This subsidy might have amounted to around USD 1.7 billion in 2017 for the entire fossil fuel industry (Oil Change International, 2017). There are also subsidies through the provision of infrastructure, such as inland waterways for the transport of oil, for which construction, operation, and maintenance are not covered by user fees (China et al., 2016; OECD, 2020). The shale oil and gas industry in the United States also had several state-level subsidies that benefited them. These included, among many others, property tax exemptions for oil and gas, expensing of intangible drilling costs from taxable income, and more favourable public leasing rules for fossil fuels vis-à-vis renewables (OECD, 2020). It should be noted that these subsidies are in addition to the billions of dollars of grants and loans that have been given to oil and gas producers under other non-fossil fuel-specific federal and state programs.

The fact that U.S. shale oil and gas production has changed world oil and gas markets in less than a decade is uncontested. It made the U.S. the world’s top oil producer and reduced the anticipated world market share of Russia and other members of the Organization of the Petroleum Exporting Countries (OPEC). This process started early on and accelerated strongly in the 2010s (Figure 3). In 2017 alone, exports from Saudi Arabia fell by 6.7%, from OPEC countries generally by 1.4% and from Russia by 0.8%. U.S. production, on the other hand, rose by nearly 16%, which made its imports fall compared to the years before and its exports rise, moving the country into the top 10 crude exporters, compared to 16th place in 2016 (IEA, 2019a).

Footnotes

- ^ Natural resource firms are allowed to deduct from their taxable income the capital costs related the acquisition or creation of an asset through cost depletion (i.e., deductions in proportion to how much of the reserve has been depleted to generate income in a given year). Oil and gas companies are allowed to use percentage depletion (i.e., deductions as a percentage of the gross income generated, possibly up to 100% of the net income produced by the asset). This can allow them to deduct from their taxable income total amounts that are in excess of their original investment. See https://greenscissors.com/program/excess-percentage-cost-depletion-oil-gas/#:~:text=For%20natural%20resource%20assets%2C%20the,income%20in%20a%20given%20year.

- ^ Normally, taxpayers are allowed to deduct the losses they incur from passive activities but only to an amount equal to income generated from the activity. Oil and gas companies are allowed to deduct their excess passive losses against income generated from business activities in which they materially participate. See https://greenscissors.com/program/passive-loss-limitations-exemption/.

Figure 3. Global oil production share of the United States, Saudi Arabia, and Russia (%)

Source: Author calculations based on BP, 2019.

The trade impact of shale oil production is thus crystal clear. The question is to what extent fossil fuel subsidies affected the level of production and therefore that trade impact. One study estimates that nearly half of discovered but not yet producing oil in the United States (or about 20 billion out of 43 billion barrels) would need subsidies to reach a minimum return on investment if the oil price were USD 50 per barrel. This share would decrease to 10% if the oil price were at USD 80 per barrel (Erickson et al., 2017).[1]At the time of writing, the international oil price is around USD 40 per barrel, after a period of severe volatility. Another study found that removing only the three largest tax subsidies would decrease U.S. oil and gas production by 4% to 5% (Metcalf, 2016). It has also been made clear by the industry itself that subsidies have played a big role in growth. In 2012, the CEO of Continental Resources (one of the largest independent shale oil producers in the United States) claimed before the House Committee on Energy and Commerce that oil and gas production could fall 40% if oil industry tax deductions were eliminated (Wertz, 2012).

From a more historical perspective, it should be noted that the shale oil industry was also assisted by more specific subsidies in its early years before shale oil became somewhat lucrative because of the development of hydraulic fracturing in combination with horizontal drilling (a “revolution” that started in the late 1990s). Most importantly, the U.S. government wrote out in 1980 a production tax credit (PTC) for unconventional fuels, often referred to as the Section 29 Unconventional Fuels PTC. This scheme ended in 1992 but covered production until 2002. Around 2000, support provided through the Unconventional Fuels PTC amounted to more than support through percentage depletion and expensing of intangible drilling costs together. In 1999, the cost of the other two subsidies amounted to USD 0.9 billion, whereas the Unconventional Fuels PTC cost USD 1.3 billion (Sherlock, 2011). During the subsidy period, shale gas production quadrupled and rose especially fast between the mid-1990s and 2002 (Burwen & Flegal, 2013). The subsidy also helped shale companies to cover the high costs of investing in shale and helped them survive frequent disappointments until the correct composition and pressure of slickwater were discovered.

Natural Gas Production and Consumption Subsidies and Fertilizer Prices in Russia

Natural gas is the most important raw material to produce any form of nitrogen fertilizer, as well as ammonia. The share of natural gas costs in the overall production costs of nitrogen fertilizers can go up to as much as 60%–70% of total production costs (Jones, 2020). That means that if natural gas prices are low, then nitrogen fertilizer prices are low as well. This has been shown in historical trends of natural gas and fertilizer prices (Beckman & Riche, 2015).

Russia has both natural gas consumption and production subsidies, which both can increase the competitiveness of producers of nitrogen fertilizers compared to a no-subsidy scenario by lowering the price of a key input. The government has employed administrative controls for domestic natural gas prices for a long time. These could be considered as consumption subsidies as long as they are below the long-run marginal cost of production of natural gas. Such subsidies provide natural gas at a cheaper cost for Russian fertilizer producers in comparison with their foreign competitors. Currently, Russian gas exports are indeed cross-subsidizing low domestic energy prices (Mitrova & Yermakov, 2019). In the recent past, because of decreasing export earnings from natural gas, Russia has aimed at liberalizing natural gas prices in the long term (Orlov, 2015), even though the exact prospect for this plan and the extent of envisioned price increases remain very unclear. Currently, it seems clear that existing natural gas consumption subsidies are therefore beneficial for Russian fertilizer producers since their foreign competitors do not have access to cheaper gas prices.

Even if that price liberalization were to happen, upstream subsidies to natural gas production might still lower the price of natural gas and generate a pass-through effect on nitrogen fertilizer production. Russian upstream gas subsidies pale in comparison to those to oil but are nevertheless large. In total, upstream natural gas production subsidies in 2017 were around USD 83 million (OECD, 2020). This, however, does not include government investment in Gazprom. Gazprom is a state-owned company that controls about 70% of total domestic gas production and most of the gas transmission sector (OECD, 2019b). The Russian government invests heavily in the company and gas transport infrastructure generally (Ogarenko et al., 2015).

The fact that low natural gas prices impact the cost of production and the price of fertilizers goes uncontested. The potential trade impact also appears to be large. Russia exports over 80% of most of its domestically produced fertilizers (Urea, NPK, and MOP). Knowing that Russia is one of the top five suppliers to the international market (Argus 2018), it is safe to say that their domestic production definitely influences world markets for fertilizers. At the same time, the rapid growth in Russia’s domestic agricultural production has increased domestic demand for fertilizers as well (Ram, 2018). That means that cheap Russian fertilizer could gain world market share but also displace potential imports from competitors. A more concrete example of the trade impact can be found in the EU market. The EU is dependent on imports of nitrogen-based fertilizers. In total, it imports over 3 million tonnes annually. It imports from only a handful of countries, with the main ones being Russia, Egypt, and Algeria (European Commission, 2019). As a result of generous input subsidies, Russia is thus likely to cover more European Union demand compared to other producers, such as Egypt and Algeria, now than it could have without subsidies. That being said, it is important to recognize that certain markets have several competitors that benefit from domestic subsidies themselves, so the level of analysis should not only focus on the differentiation between subsidizing and non-subsidizing countries but also on the levels of subsidization, as fossil fuel subsidies are both pervasive and widespread.

Footnotes

- ^ At the time of writing, the international oil price is around USD 40 per barrel, after a period of severe volatility.

3. Fossil Fuel Subsidies Under WTO Subsidy Rules

Fossil fuel subsidies, like other subsidies, are, in principle, covered by the WTO ASCM and could also be governed by relevant provisions of the 1994 General Agreement on Tariffs and Trade (GATT) and the Agreement on Trade-Related Investment Measures (TRIMs Agreement). GATT provisions may be invoked to challenge fossil fuel subsidies, for instance, because a subsidy may amount to an illegal quantitative export restriction. Moreover, the GATT contains several relevant provisions that are elaborated upon in the ASCM, notably Articles VI on anti-dumping and countervailing duties and Article XVI on subsidies. The TRIMs Agreement addresses investment measures related to the trade in goods that are inconsistent with the GATT’s obligations of national treatment and elimination of quantitative restrictions (Article 2.1 TRIMs Agreement). One of those measures, included in an Illustrative List in an Annex to the TRIMs Agreement, is the requirement to use local content. Together with the GATT’s national treatment obligation, these provisions have been relevant in the context of renewable energy disputes, with several renewable energy support measures – in Canada,[1]Canada – Certain Measures Affecting the Renewable Energy Generation Sector (Canada – Renewable Energy), Appellate Body Report, WT/DS412, 426 (24 May 2003). India,[2]India – Certain Measures Relating to Solar Cells and Solar Modules (India – Solar Cells), Appellate Body Report, WT/DS456 (14 October 2016). and the United States[3]United States – Certain Measures Relating to the Renewable Energy Sector (US – Renewable Energy), Panel Report, WT/DS510 (not yet adopted). – deemed incompatible with the GATT and TRIMs Agreement, though importantly not with the ASCM (see, e.g., Cosbey & Mavroidis, 2014; Espa & Marín Durán, 2018; Kulovesi, 2014; Rubini, 2015). Other agreements, such as the Agreement on Agriculture and the General Agreement on Trade in Services, may also assume relevance in the context of fossil fuel subsidies. However, the focus of this section will be on the most comprehensive set of subsidy disciplines, as contained in the ASCM.

Notwithstanding the potential impacts on international trade discussed in the previous section and the fact that several renewable energy subsidies have been successfully challenged in trade disputes, fossil fuel subsidies have remained largely unchallenged before the WTO dispute settlement system. Before discussing the reasons for this “undercapture” (Verkuijl et al., 2019, p. 335) that are related to the legal requirements under the ASCM, it is important to understand that the lack of challenges of fossil fuel subsidies under WTO law may also be due to strategic and political considerations. First, fossil fuel subsidies have arguably not been challenged because WTO members have been unwilling to do so for fear of, for instance, jeopardizing diplomatic relationships or possible retaliatory action (Asmelash, 2015), particularly if members have fossil fuel subsidies of their own (i.e., the “glasshouse” syndrome). Second, and related to the first explanation, domestic interest groups have largely refrained from putting pressure on their governments to launch a dispute against fossil fuel subsidies, possibly because long-standing fossil fuel subsidies—as compared to relatively new support measures for renewable energy— are already integrated into investment expectations (Meyer, 2017). Third, disputes are more likely if a country has a diversified economy, as this allows a complainant to retaliate against a broader set of products. This excludes some key fossil fuel-producing and exporting countries, such as Saudi Arabia (Meyer, 2017). Lastly, consumer subsidies may be viewed as trade facilitating (rather than trade distorting), as they also increase imports from third countries. Accordingly, this may lower the incentives for them to challenge such measures (Steenblik et al., 2018).

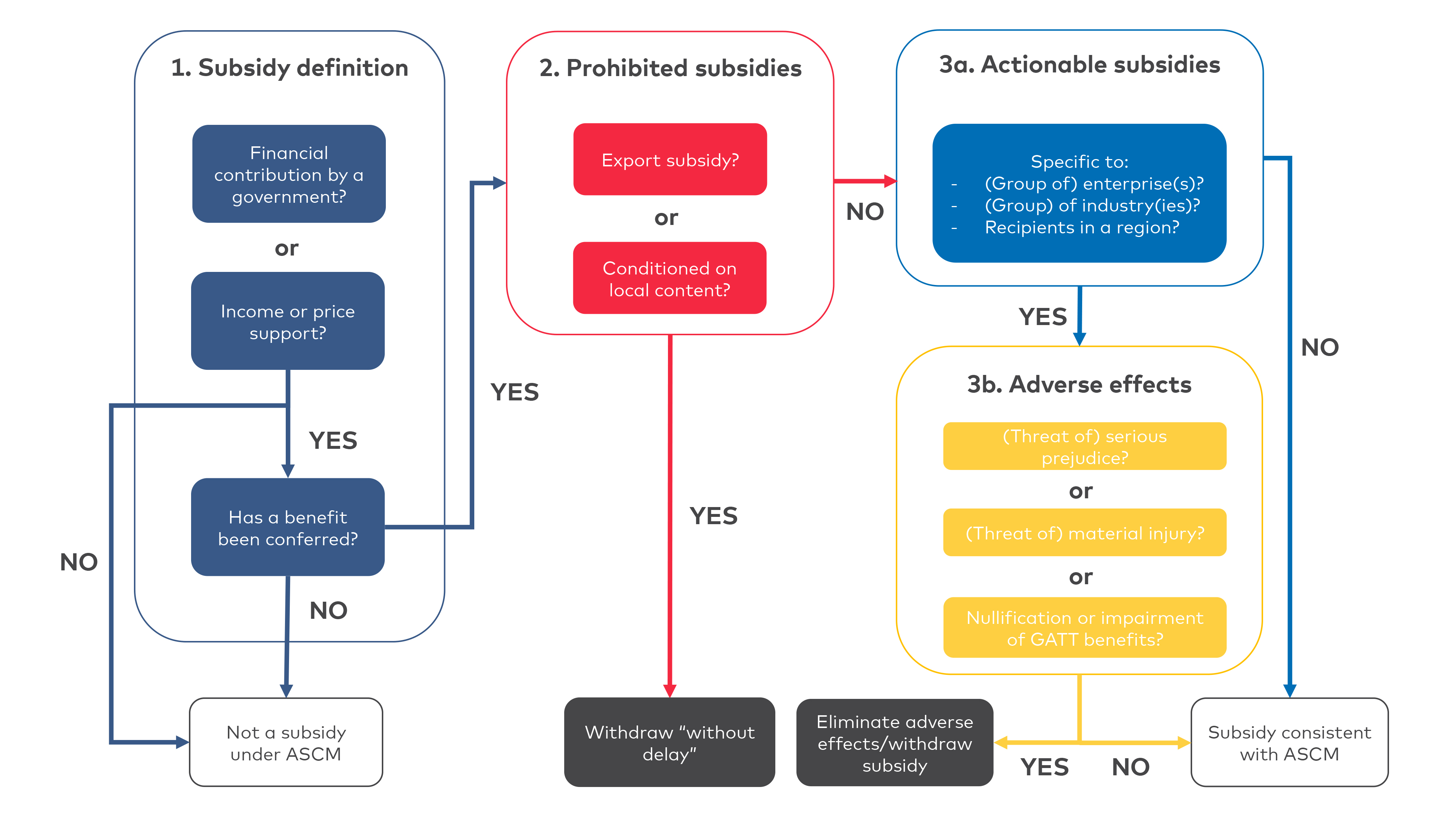

Although these considerations may help explain why fossil fuel subsidies have not yet attracted any challenges under the WTO, this explanation is incomplete without a discussion of the legal and evidentiary challenges posed by the ASCM (De Bièvre et al., 2017). Under the ASCM, a subsidy is defined as a “financial contribution by a government or any public body” or “any form of income or price support” that confers a benefit (Article 1.1 ASCM). WTO rules only apply if measures can be demonstrated to be either “prohibited” or “actionable” subsidies under the agreement.[4]While not all subsidies may be subject to a challenge pursuant to the ASCM, it is important to note that the terms of the ASCM can still be used to identify subsidies for other purposes, for example, to develop fossil fuel subsidy inventories to report under SDG Indicator 12.c.1 or other uses (see United Nations Environment Programme [UNEP] et al., 2019). Here, whether subsidies are trade distorting and either prohibited or actionable under the WTO may not be one of the purposes, for example, the analysis may be based on identifying subsidies that increase greenhouse gas emissions or that contribute to local air pollution. Prohibited subsidies are those contingent upon export performance or upon the use of domestic over imported goods (Article 3 ASCM). Subsidies are actionable if they are “specific” (aimed at certain enterprises or industries, Article 2 ASCM; prohibited subsidies are deemed to be specific, Article 2.3 ASCM). If actionable subsidies create “adverse effects” for another WTO member, they may be challenged. “Adverse effects” refers to injury to the domestic industry of another member; nullification or impairment of the benefits accrued by another member under the tariff concessions of the GATT; or, most relevantly, serious prejudice to the interests of another member (Article 5 ASCM). If a subsidy is not specific, it is not actionable. As this section will explain, the evidentiary challenges for complainants under the ASCM can be significant.

Figure 4 presents the key questions for testing whether a (fossil fuel) subsidy is consistent with the ASCM and what a dispute settlement panel might recommend depending on the outcome of the analysis. Accordingly, the remainder of this section will discuss the extent to which fossil fuel subsidies are captured by the subsidy definition of the ASCM (Section 3.1), as well as under which circumstances fossil fuel subsidies could constitute a “prohibited” subsidy (Section 3.2) or could be determined to be “actionable” and successfully challenged (Section 3.3). Lastly, it will briefly discuss relevant subsidy notification requirements under the ASCM (Section 3.4).

Footnotes

- ^ Canada – Certain Measures Affecting the Renewable Energy Generation Sector (Canada – Renewable Energy), Appellate Body Report, WT/DS412, 426 (24 May 2003).

- ^ India – Certain Measures Relating to Solar Cells and Solar Modules (India – Solar Cells), Appellate Body Report, WT/DS456 (14 October 2016).

- ^ United States – Certain Measures Relating to the Renewable Energy Sector (US – Renewable Energy), Panel Report, WT/DS510 (not yet adopted).

- ^ While not all subsidies may be subject to a challenge pursuant to the ASCM, it is important to note that the terms of the ASCM can still be used to identify subsidies for other purposes, for example, to develop fossil fuel subsidy inventories to report under SDG Indicator 12.c.1 or other uses (see United Nations Environment Programme [UNEP] et al., 2019). Here, whether subsidies are trade distorting and either prohibited or actionable under the WTO may not be one of the purposes, for example, the analysis may be based on identifying subsidies that increase greenhouse gas emissions or that contribute to local air pollution.

Figure 4. Decision chart for the ASCM in WTO dispute settlement

Source: Adapted from Verkuijl et al., 2017.

3.1 Subsidy Definition

The first key question is whether a given support measure constitutes a “subsidy” under the ASCM. To determine this, it needs to be established that a subsidy is either a “financial contribution” by a government or “income or price support” under Article 1.1 of the ASCM and that this leads to the conferral of a “benefit”.

The definition of a financial contribution, according to Article 1.1(a)(1) of the ASCM, includes:

(i) a government practice involves a direct transfer of funds …, potential direct transfers of funds or liabilities; (ii) government revenue that is otherwise due is foregone or not collected …; (iii) a government provides goods or services other than general infrastructure, or purchases goods; (iv) a government makes payments to a funding mechanism, or entrusts or directs a private body to carry out one or more of the type of functions illustrated in (i) to (iii) above.”

A first question is whether a financial contribution is granted by a government, which includes the “government or any public body within the territory of a Member” (ASCM, Article 1.1(a)(1)). This clearly includes any government at the national (e.g., the Russian government) or subnational (e.g., the Queensland Government) level. In addition, other bodies “that [possess, exercise or are] vested with government authority”[1]US – Definitive Anti-Dumping and Countervailing Duties on Certain Products from China, Appellate Body Report, WT/DS379/AB/R (11 March 2011), para. 317. are also included. This means that financial support for fossil fuels provided through state-owned enterprises (see Bast et al., 2015; Gensçü et al., 2020) or state-owned commercial banks are also covered by the ASCM if these bodies are vested with government authority. Moreover, indirect financial contributions made by private bodies that are “entrusted” or “directed” by a government are also covered. Instances of such entrustment or direction can be inferred from the facts, for instance, if a private body acts against its own commercial interests or if the government is a major shareholder. If a state-owned enterprise or another company would be charged with supplying fuels at below-market prices (a common example of a consumer subsidy), this would therefore likely be covered.

In some cases, it will be quite straightforward to establish whether a financial contribution exists. For example, direct financial support to a fossil fuel company in the form of a grant or a loan would fall within the ASCM category of a direct transfer of funds. In this regard, the Adani Royalties Deferral Agreement in Australia (see Section 2) can be classified as a direct transfer of funds (i.e., a loan) in that it obliges Adani to repay and interest is charged.[2]Japan – Countervailing Duties on Dynamic Random Access Memories from Korea, Appellate Body Report, WT/DS336/AB/R (17 December 2007), para. 251. The interest rate reduction granted to Adani could also be characterized as government revenue foregone to the extent that commercial rates can be taken as the benchmark. Another clear example of a subsidy is government funding for a railroad that is solely aimed at transporting coal from a mine to a port, which would be captured by the ASCM category of the provision of goods or services. Likewise, the leasing of federal lands that grants companies the right to extract fossil fuels can be considered the provision of a good (Erpenbach, 2020, p. 516).

In addition to a financial contribution by a government, fossil fuel subsidies may also constitute another category of subsidy, namely income or price support (ASCM, Article 1.1(a)(2)). A common type of consumption support measure – governments setting regulated prices for the sale of fuels (e.g., diesel) or directing others to do so, such as regulated prices of natural gas in Russia (see Section 2) – can be considered income or price support, as such support “includes direct government intervention in the market with the design to fix the price of a good at a particular level.”[3]China – Countervailing and Anti-Dumping Duties on Grain Oriented Flat-Rolled Electrical Steel from the US, Panel Report, WT/DS414/R (16 November 2012), para. 7.85. Moreover, if the regulated price leads to a cheaper input (i.e., fuels) being provided to a (subsidized) producer that uses this cheap product, it can be argued that the government has provided goods or services (i.e., that there is a “financial contribution”).

In other cases, it will be more difficult to determine whether specific fossil fuel subsidies fall under these categories. For instance, the expensing of intangible drilling costs from taxable income in the United States discussed in Section 2 could be qualified as government revenue foregone. However, to make such a finding under WTO law, it is necessary to compare the (preferential) tax treatment against a benchmark tax treatment (Coppens, 2014, pp. 46ff; Müller, 2017, pp. 92ff.). Although Verkuijl et al. (2019, p. 341) suggest that the treatment of oil and gas producers “appears to deviate from the norm and would therefore constitute the relevant challenged tax treatment,” they also indicate that any firm conclusion would need to be based on a detailed analysis of the U.S. tax regime.

In addition to finding whether the support can be deemed a “financial contribution” or “income or price support,” Article 1 of the ASCM requires the conferral of a benefit, shifting the focus to the recipient of support (Coppens, 2014, p. 60). To determine whether a benefit has been conferred, the WTO Appellate Body developed a “private market test” that specifies that a benefit is conferred when “the recipient has received a financial contribution on terms more favourable than those available to [it] in the market.”[4]Canada – Measures Affecting the Export of Civilian Aircraft, Appellate Body Report, WT/DS70/AB/R (20 August 1999), para. 158.

In some cases, it may be straightforward to establish this, for instance, if a subsidy consists of a favourable loan to a fossil fuel producer or if a subsidy results in consumers not paying the market price for certain fuels (Verkuijl et al., 2019). However, in light of existing WTO case law, proving a consumption subsidy provides a benefit under the ASCM is different for energy-importing countries and energy-producing countries. For consumption subsidies in producing countries, “it is difficult to argue that a benefit is conferred if the producing country provides fuel at above production cost, but below the international market price” (Moerenhout, 2020, p. 124). However, for energy-importing countries, it should be easier to establish that a benefit has been conferred if the fuel price is set below the international market price. In the specific cases where it can be established that government revenue has been foregone, a benefit can be deemed to be conferred (Coppens, 2014, p. 61). For instance, if there are tax breaks – for example, an exemption from paying value-added tax – for fossil fuel producers that cannot be justified with reference to the internal principles of a country’s tax regime, it is also likely that the benefit test will be passed.

Footnotes

- ^ US – Definitive Anti-Dumping and Countervailing Duties on Certain Products from China, Appellate Body Report, WT/DS379/AB/R (11 March 2011), para. 317.

- ^ Japan – Countervailing Duties on Dynamic Random Access Memories from Korea, Appellate Body Report, WT/DS336/AB/R (17 December 2007), para. 251.

- ^ China – Countervailing and Anti-Dumping Duties on Grain Oriented Flat-Rolled Electrical Steel from the US, Panel Report, WT/DS414/R (16 November 2012), para. 7.85. Moreover, if the regulated price leads to a cheaper input (i.e., fuels) being provided to a (subsidized) producer that uses this cheap product, it can be argued that the government has provided goods or services (i.e., that there is a “financial contribution”).

- ^ Canada – Measures Affecting the Export of Civilian Aircraft, Appellate Body Report, WT/DS70/AB/R (20 August 1999), para. 158.

Key points

- The ASCM covers fossil fuel subsidies provided by governments, by other public bodies vested with government authority, and by private bodies entrusted/directed by a government. Such bodies could include state-owned enterprises.

- Fossil fuel subsidies can fall under several categories of the ASCM subsidy definition, including a direct transfer of funds, government revenue foregone, provision of goods and services, and/or income or price support. The evidentiary burdens for establishing that government revenue has been foregone may be high.

- If a fossil fuel subsidy consists of a financial contribution on terms more favourable than the market, a benefit will be deemed to have been conferred. A benefit will also have been conferred if the government has foregone revenue.

3.2 Prohibited Subsidies

Assuming that support for fossil fuels meets the definition of a “subsidy” under Article 1 of the ASCM, the next question is whether it can be considered a “prohibited” subsidy under Article 3, which covers “subsidies contingent, in law or in fact … upon export performance” (export subsidies) and “subsidies contingent, whether solely or as one of several other conditions, upon the use of domestic over imported goods” (local content subsidies). These subsidies, according to Article 4.7 of the ASCM, must be withdrawn “without delay.”

For an export subsidy to be prohibited, it needs to be established that the subsidy is “contingent” on exportation. If any export conditionality is stated in a country’s legislation, this will be easy to prove. In addition, the ASCM further includes a non-exhaustive “Illustrative List of Export Subsidies” in its Annex I. In the context of fossil fuel subsidies, a first question thus arises as to whether a subsidy is included in the Illustrative List, in which case it is automatically prohibited. The Illustrative List includes a range of measures, such as the provision of goods and services by governments on terms more favourable for exports (item d), tax or duty rebates upon export (items e–i), and export credit support, although with an exception for certain export credits consistent with the OECD Arrangement on Officially Supported Export Credits (items j–k).

If a measure is not included in the Illustrative List, and assuming that a subsidy’s links to exportation are not provided for in law, it needs to be established that there has been (1) a granting of a subsidy that is (2) in fact tied to (3) actual or anticipated exportation or export earnings (ASCM, Article 3.1(a), footnote 4).[1]See also Canada – Measures Affecting the Export of Civilian Aircraft, Appellate Body Report, WT/DS70/AB/R (20 August 1999), para. 170–172. The first criterion means that the focus should be on the granting authority and not the recipient. To determine whether the granting of a subsidy is “in fact tied,” the claimant needs to demonstrate a “relationship of conditionality or dependence.”[2]Canada – Measures Affecting the Export of Civilian Aircraft, Appellate Body Report, WT/DS70/AB/R (20 August 1999), para. 171. To prove that the subsidy is tied to anticipated exportation, it further needs to be demonstrated that “the granting of the subsidy [is] geared to induce the promotion of future export performance by the recipient” in a way “that is not simply reflective of the conditions of supply and demand in the domestic and export markets undistorted by the granting of the subsidy.”[3]European Communities and Certain Member States – Measures Affecting Trade in Large Civil Aircraft, Appellate Body Report, WT/DS316/AB/R (1 June 2011), para. 1044 and 1053. This can be shown if the ratio between exports and domestic sales following a subsidy is higher than historical or hypothetical levels (Coppens, 2014, p. 121). With regard to the third criterion of actual or anticipated exportation or export earnings, the former refers to exports when the subsidy is granted, whereas the latter concerns the expectations of future exports (i.e., after the subsidy has been granted). Although the (subjective) expectations of a government in terms of export performance may inform the overall determination of contingency, any finding of whether exportation or export earnings were anticipated needs to be based on (objective) evidence.[4]European Communities and Certain Member States – Measures Affecting Trade in Large Civil Aircraft, Appellate Body Report, WT/DS316/AB/R (1 June 2011), para. 1050. For instance, if a company sells “much if not most of the production in export markets,” this could help establish the case that there was “anticipated exportation.”[5]European Communities and Certain Member States – Measures Affecting Trade in Large Civil Aircraft, Appellate Body Report, WT/DS316/AB/R (1 June 2011), para. 1076 and 1080.

While fossil fuel consumption subsidies in the form of universal low end-user prices are unlikely to be prohibited subsidies (Moerenhout, 2020), production subsidies could, in some cases, constitute prohibited export subsidies. Verkuijl et al. (2019) examine the expensing of intangible drilling costs in the United States (discussed in Section 2) in light of the test for prohibited export subsidies. They caution that increased exports as a result of a subsidy do not necessarily turn a measure into an export subsidy. This will only be the case if the intervention encourages exports over domestic sales (Verkuijl et al., 2019, p. 342). This may be easier to show in cases where the domestic market is saturated or declining, meaning that increasing production will likely have a stronger impact on exports than domestic sales. In an analysis of a potential loan by the Australian Government through its Northern Australia Infrastructure Facility to the Carmichael coal mine, Slattery (2019) concludes that de facto contingency can be established on the basis of the following set of facts: (1) the coal produced is not intended for domestic consumption, as the domestic market is already saturated; (2) the scale of exports is likely significant, with the coal mine increasing Australia’s export capacity by a quarter; and (3) government officials and documents point to the export orientation of the financial support. To be clear, this measure is a different one than the Adani Royalties Deferral Agreement discussed in Section 2, and some – though not all – facts are likely to be different in that case. Moreover, neither the export orientation of the enterprise receiving the subsidy nor the saturation of domestic markets alone would necessarily lead to a finding of contingency. Nevertheless, along with other information (if available), these facts may help craft the argument that a measure potentially constitutes a prohibited export subsidy.