- Full page image w/ text

- Authors

- Preface

- Table of contents

- Terms and abbreviations

- 1. Summary and conclusions

- 2. Introduction

- 2.1 Strong growth in aviation and its emissions

- 2.2 A regulatory gap in international aviation

- 2.3 Ambitious goals for GHG reductions in the Nordic countries

- 2.4 Strategies to reduce emissions from aviation

- 2.5 Sustainable aviation fuel (SAF)

- 2.6 Electrification

- 2.7 Report structure and scope

- 3. Overview of aviation in the Nordic countries

- 3.1 Internal and international travel patterns

- 3.2 Airline market shares

- 3.3 Future demand for aviation fuel

- 3.4 Biomass potential for sustainable aviation fuels in the Nordics

- 4. Aviation and climate policy: International context

- 4.1 Convention on International Civil Aviation, ‘The Chicago Convention’

- 4.2 International Civil Aviation Organization (ICAO) and CORSIA

- 4.3 EU regulation of relevance for common Nordic initiatives

- 5. Perspectives for sustainable aviation in the Nordics

- 5.1 Current national policies for sustainable aviation

- 5.2 Nordic initiatives dealing with sustainable aviation fuels

- 5.3 Electric aviation

- 5.4 Possibilities for Nordic cooperation on electric aircraft

- 6. Assessment of potential Nordic policy measures for sustainable aviation fuels

- 6.1 Blending mandate and CO2-reduction requirements

- 6.2 Taxation of aviation

- 6.3 Comparative impact assessment of the policy measures

- References

- Appendix A

- Appendix B

- Appendix C

- Appendix D

- About this publication

MENU

Nordic Sustainable Aviation

This report has been prepared by:

Transportøkonomisk institutt (TØI)

Inga Margrete Ydersbond

Niels Buus Kristensen

Harald Thune-Larsen

Preface

The Nordic countries have high ambitions to become more environmentally sustainable. This ambition was further strengthened in January 2019 when the Nordic Prime Ministers signed “Declaration on Carbon Neutrality”. This declaration highlights transport as an important common Nordic challenge in the fight to reduce Greenhouse gas emissions. Aviation is probably one of the most challenging sectors to decarbonize. Although the Nordics seek to maintain leadership and cooperation in their climate efforts, aviation is a global enterprise where regional frameworks such EU-ETS and global agreements and conventions restrict the Nordic policy menu.

The following publication was commissioned by the Danish presidency of the Nordic Council of Ministers (2020). The report has been prepared by the Institute of Transport Economics (TØI) and the process towards publishing and dissemination has been overseen by Nordic Energy Research (NER). NER is the platform for cooperative energy research and knowledge development that is used for policy development under the auspices of the Nordic Council of Ministers. NER also prepared a report in 2016 entitled “Sustainable Jet-Fuels for Aviation” and have since then worked closely with stakeholders in the Nordic aviation industry through the Nordic Initiative for Sustainable Aviation (NISA). In 2020, an update of the 2016 report was published. This report - “Nordic Sustainable Aviation”- complements the previous reports presenting current policy frameworks in each Nordic country and exploring alternative policy measures. Nordic Sustainable Aviation also explores sustainable aviation fuel (SAF) and the potential of electric aviation in the Nordics.

The intention of this report is to explore challenges and opportunities for increased Nordic cooperation to increase the sustainability of aviation in Nordics, possibly with a trickle-down effect on the aviation industry globally. Nordic Sustainable Aviation presents current policy frameworks in each Nordic country and explores alternative policy measures. The report covers five policy measures and possible combinations of these; blending mandates, CO2 equivalent reduction requirements, establishing a joint Nordic SAF-fund or parallel national SAF funds, as well as various types of fuel and passenger taxes. These measures are complemented by a summary of distances, passenger loads between all airports in the Nordics.

Suggested policy options include; A common Nordic vision for sustainable aviation backed by an ambitious joint target for the share of renewable energy in aviation by 2030. Such a plan should address both demand-side and supply-side measures with the aim of bringing up the share of SAF and stimulating the increased production of SAF internationally. Implementing a combination of a SAF-fund/SAF funds financed by joint Nordic passenger tax reduces the risk of carbon leakages and bridges the price gap between conventional jet-fuel and sustainable aviation fuels.

The COVID-19 outbreak has led to a temporary significant decline in air traffic, changes in Nordic policy frameworks, and an aviation industry in need of substantial governmental economic support to stay in business. These changes are not fully accounted for in this report. It is nevertheless our hope that this report offers Nordic politicians’ guidance as to what is possible to achieve on a Nordic level independently, and what needs to be addressed within EU and in global bodies such as ICAO and UNFCCC.

Klaus Skytte, CEO, Nordic Energy Research

Contents

Terms and abbreviations

| Advanced biofuel | Biofuel following specific criteria, various definitions are applied. According to the Renewables Directive, advanced biofuels are; mostly cellulosic and lingo-cellulosic materials that cannot be processed with first generation biofuel technologies. |

| Additionality | Carbon offsets should lead to additional projects that otherwise would not take place. |

| Aircraft | A vehicle that is able to fly by gaining support from the air. |

| Airplane | An aircraft with fixed wings. |

| ASK | Available Seat Kilometres = Seat supply x flight kilometres. |

| Biofuel | Fuel based on biologic materials. |

| Bio jet fuel | Jet fuel coming from biologic materials, including forest residues (cellulosic biofuel), plant oils, algae, organic waste. |

| Cabotage | Transport of goods or passengers between two places in the same country by a transport operator from another country. |

| CIS | Armenia, Azerbaijan, Belarus, Kazakhstan, Kyrgyzstan, Moldova, Russia, Tajikistan, Uzbekistan. |

| CO2 | Carbon dioxide. |

| CO2e | CO2-equivalents, a summary of measures where all GHG’s are converted to CO2e with their relative GHG-emissions. |

| CORSIA | Carbon Offsetting and Reduction Scheme for International Aviation. |

| DAC | Direct Air Capture of CO2. |

| EEA | European Economic Area = EU + Norway + Iceland + Lichtenstein. |

| E-fuels | or electro fuels, or synthetic fuels; Fuels where all or a significant share of the energy content stems from electricity based on renewable energy power to X (PtX). |

| E-jet fuel | E-fuels that can replace fossil jet fuel. Other terms; power-to-jet (PtJ). |

| EU | European Union. |

| Eurocontrol | The European Organisation for the Safety of Air Navigation. |

| ETS | Emission Trading Scheme, EU’s regulatory system for tradeable CO2 emission permits. |

| GHG-emissions | Greenhouse gas emissions; both CO2 and non-CO2 emissions. |

| HEFA | Hydrogenated Esters and Fatty Acids, types of biofuels. |

| HVO | Hydrogenated Vegetable Oils. |

| IATA | International Air Transport Association. |

| ICAO | International Civil Aviation Organization. |

| IEA | International Energy Agency. |

| ILUC | Indirect land use change. |

| Long-haul flights | Flights longer than 4,000 km. |

| LULUCF | Land use, land use change and forestry. |

| Medium-haul flights | Flights between 1,500 km and 4,000 km. |

| The Nordics | Short for the Nordic countries Denmark, Finland, Iceland, Norway and Sweden. |

| PJ | Petajoule = 1 million gigajoule (GJ) = 1 billion megajoule (MJ). |

| PSO | Public Service Obligation, a term used for services which are provided under public sector regulation, typically with financial support. Also linked to Public Procurement Agreement (PPA). |

| RD&D | Research, Development and Demonstration. |

| RTK | Revenue Tons Kilometers. |

| SAF | Sustainable aviation fuels. |

| Short-haul flights | Flights shorter than 1,500 km. |

| Seat supply | Number of seats summed over a set of flights. |

| T&E | The non-governmental organization (NGO) Transport and the Environment. |

| Tankering: | When an aircraft deliberately carries excess fuel in order to reduce or eliminate refueling at its destination in order to avoid higher fuel prices for example due to taxation. |

| TRL | Technology Readiness Stage, a method for estimating the maturity of technologies. |

| VAT | Value added tax. |

1. Summary and conclusions

Globally, aviation accounts for a modest share of World total greenhouse gas (GHG) emissions from today’s energy use. However, air transport has been rapidly increasing and many other sectors are expected to reduce their emissions. Hence, aviation’s share of global emissions can be foreseen to rise and will constitute a significant part of the problem unless strong counteracting initiatives are taken. However, regarding aviation, efforts have so far been limited, although aerospace industry has achieved significant technological improvements of aircraft energy efficiency over the past decades.

The Nordic countries all have high ambitions to become more environmentally sustainable. January 2019, the Nordic Prime ministers signed “Declaration on Nordic Carbon Neutrality”, committing their countries to strengthen mutual cooperation to attain carbon neutrality domestically. The declaration emphasizes decarbonization of the transport sector. The aim of this report is to examine challenges and opportunities for increased Nordic cooperation with regards to increasing sustainability of aviation and, based on evaluation of alternative options, propose common policy measures.

Current situation

All Nordic countries have plans for national GHG reduction toward 2030 and climate neutrality by 2050 or earlier. Only Sweden and Finland have reduction targets for the transport sector and none of the Nordics have specific targets for aviation. However, some economic measures with environmental purposes are implemented:

- Norway has a blending mandate for 0.5% advanced biofuels as of 2019. There are plans to increase it to 30% toward 2030, but this is not yet translated into legislation.

- Sweden and Norway have passenger taxes. The rates per departing passenger are:

76.5 NOK (7.8 EUR) and 62 SEK (5.9 EUR) for domestic and EEA[1]EEA = European Economic Area = EU + Norway, Iceland and Lichtenstein. destinations;

204 NOK and 260 or 416 SEK for longer routes. - Norway has a fuel tax on domestic flights with a rate equivalent to about 55 EUR / tonne CO2.

On the other hand, all Nordic countries have a reduced or zero VAT rate on domestic trips. In addition, all flights within the European Economic Area (EEA) are regulated by the EU Emission Trading System. The system de facto implies a price on CO2-emissions from aviation, although airlines receive tradeable allowances covering a certain level of emissions from their flights per year. The market price is about 25 EUR per tonne CO2 (August 2020). This level is far lower than national estimates of the marginal CO2 abatement costs to achieve the emission targets in the Nordics, in particular if we only look at contributions from the transport sector. The climate impact of these emissions is, moreover, estimated to be significantly larger than for surface emissions when flying in high altitudes due to contrails from fuel burn and other complex atmospheric chemical reactions. The total effect is uncertain but can add up to a more than doubling of the CO2-effect.

International aviation is subject to many international conventions and agreements as well as EU regulations that in practice limit what measures can be applied, although the exact interpretation is debated. International aviation is not subject to VAT and fuel taxes have to be bilaterally agreed.

Pathways to sustainable aviation

Although the need for significant reduction of the climate impact from aviation is politically recognized, the ultra-high mobility generated by air transport is also widely considered an important and highly valued factor in many people’s lifestyle in the Nordics. Hence, in the political mainstream, curbing air travel by strong demand side measures, strong enough to stop aviation growth, is not considered an attractive path to significantly reducing the GHG emissions from aviation. Alternative pathways to significant reductions are to:

- pursue continued energy efficiency improvements and/or

- replace fossil jet fuel with alternative energy sources with lower lifecycle GHG emissions

recognizing that this can also increase costs and ticket prices and thereby reduce air travel. Over the next two decades, achievable fuel efficiency improvements for new conventional aircraft are estimated to be at best about 40%, and air traffic management is expected to be able to generate another 5–10%. Adding that the significant GHG reductions required from aviation to reach the long-term targets implies that a major share of the reductions will expectedly have to come from replacing fossil energy with low-carbon alternatives.

Sustainable Aviation Fuels

A straight-forward approach is to replace fossil jet fuel with what is termed sustainable aviation fuel (SAF). SAF encompasses various fuels with very low lifecycle GHG emissions. However, high altitude effects will still be an issue. SAFs have to be certified as sustainable and, in particular, for safety and performance by independent third-party bodies. Six production pathways are currently certified with blending levels up to 50%, but levels are expected to be higher in the future.

Today, all SAF production pathways are far more expensive than fossil jet fuel. This is the main reason why current demand for SAF is insignificant compared to the total aviation fuel consumption and supply is considered scarce or unstable. Only about 0.05% of jet fuel used in the EU is SAF. It is mainly biofuel produced from waste oil and animal fat residues as feedstock, which is not scalable to significant shares of total aviation fuel demand. The largest volumes of biofuels are today used in other transport modes, predominantly road transport and are to a wide extent produced on a basis which can also be used for SAF. The sustainability of using food and feed crops as feedstock for fuel production is increasingly questioned, as there are severe risks of deforestation and other indirect land use change (ILUC) impacts. Biofuels that use waste and residues from agriculture or forestry as feedstock are considered more sustainable. A crucial issue is therefore which sustainability criteria biofuels must match to be labelled as SAF, especially regarding the origin of the feedstock.

Anyway, biomass for energy purposes will undoubtedly be a scarce resource over the next decades, in particular in a global perspective, but the scarcity will most likely also play out in a Nordic context. In early phases of the transformation, where SAF will only constitute a smaller share of total fuel consumption, this might not be an issue. However, full phase out of fossil fuels in aviation solely based on biofuels might be challenging, due to the availability of biomass that can be used sustainably. Therefore, the required biomass might come at a very high cost needed to divert it from other applications. Thus, aviation also needs other sources of sustainable jet fuel, and the currently promising alternative is electro-jet fuels or e-jet fuels.

Sustainable e-jet fuels are synthetic kerosene made by extracting hydrogen from water through electrolysis. The energy used for this process should come from renewable based electricity. The hydrogen is subsequently converted into e-fuels. The process requires carbon which can come from biomass, including forest or agriculture residues, or from CO2 captured from point sources or from the air (Direct Air Capture). The life cycle GHG emissions are very low compared to fossil jet fuel but the energy loss in the production pathway is significant. A main advantage of e-jet fuel is that renewable based electricity is not considered globally limited in the same way as biomass. The big challenge with e-fuels is the costs, due to the large amount of renewable energy needed to produce it and the technical development needed to commercialize it. Costs estimates for e-fuels vary widely but are generally expected to decrease over the next decade.

Direct combustion of liquid hydrogen (LH2) in turbines is an alternative pathway which has a considerably lower energy loss compared to e-jet fuels because liquefaction by cooling is less energy demanding than the conversion process from hydrogen to a hydrocarbon liquid fuel. However, hydrogen-based propulsion technology is still at a very low technology readiness level (TRL).

Electrification

Electric propulsion combined with battery storage has recently gained intense attention as an alternative to liquid fuel. The background is the last decades’ dramatic development in battery technologies which is expected to continue with higher energy intensity at significantly lower production costs as well as remarkable reduction in costs of solar and wind energy-based electricity.

The energy efficiency of electric motors is higher than for combustion engines and energy costs per MJ is lower for electricity than for jet fuel. In addition, local emissions can be eliminated, and noise nuisance significantly reduced.

Still, the main barrier is energy intensity (kWh per kg) of batteries. Future development in this area will be decisive for the role of battery-electric aircraft. Battery storage is essential for electrification to be a genuine alternative that circumvents the challenges described for SAF. The main disadvantage of batteries is their weight, which is a much bigger challenge for aviation than for surface transport. The energy density of the batteries needs to be increased significantly, but with the current rate of innovation this appears likely to be achieved within the next 5–10 years.

Expectations from the manufacturers of electric airplanes and others on the timeline of the introduction of electric airplanes vary widely, with optimistic views expecting it to be before 2030 for small aircraft for short distances.

Footnotes

- ^ EEA = European Economic Area = EU + Norway, Iceland and Lichtenstein.

Electric aviation comprises various types of aircraft technologies that use electric motors for propulsion. The propulsion system may be labelled battery electric or hydrogen electric depending on the energy storage. The latter use fuel cells to convert hydrogen to electric power. Hybrid-electric aircraft where one of the fuel-burning engines are replaced by an electric motor can a be first step toward "pure" electrification.

GHG reductions potential for Sustainable aviation fuels and electrification

Electrification holds significant potentials in coming years, in particular for small aircraft at short to medium distances. Over the next couple of decades, electric aircraft could possibly obtain significant market shares in some parts of the short distance market depending on further technological development and cost reductions as well as political commitment. Irrespective of the timeline, battery-electric aircraft will initially probably be most competitive:

- on routes with very short distances where cruise speed is less important and

- in sparsely populated regions, where passenger volumes are very small

Such routes could be existing services on Public service obligation (PSO) routes operated with subsidies or routes to one of the many existing small airfields without services today. This would also open up for significantly improved mobility in remote areas, which could be particularly interesting in the Nordics.

On the other hand, it is considered unlikely that fully electrified aircraft relying on battery stored energy will have any significance in scheduled operations on medium to long distances within the next two (or perhaps even three) decades. Taking into account medium to long flight distances' heavy share of total energy consumption, it seems fair to conclude that:

- SAF will be the dominant option for replacing fossil jet fuel toward 2030. Adding slow replacing rates of airplanes due to long service life SAF will most likely also be by far the main contributor to carbon neutral aviation toward 2050 in combination with expectedly strong progress in energy efficiency.[1]Hydrogen is a less developed alternative which has not been considered in this report. The energy density by weight is higher than for (other) SAF or fossil jet fuel, but the challenges include that energy density by volume of liquid hydrogen is only about one fourth (McKinsey 2020).

- However, the market readiness for both advanced SAF and electric propulsion is currently relatively low and intensified efforts in RD&D is needed for both SAF and electrification to reach maturity.

Progress toward sustainable aviation can be accelerated through political and financial support. Irrespective of considerations about SAF versus batteries as energy carrier, clear signals of political commitment can contribute to reassure investors and other stakeholders without favouring one of these technological paths over the other. At a strategic level this could be done by formulating:

A common Nordic vision for sustainable aviation backed by an ambitious joint target for the share of renewable energy in aviation by 2030.

In addition, Nordic cooperation, e.g. by a joint funding scheme, is likely to have potential gains beyond the sum of unilateral initiatives.

Strategies for promoting sustainable aviation fuels

Uncertainty is high about what will turn out as the preferred SAF solution(s) due to insufficient knowledge about sustainability, resource availability and full-scale production for the alternative production pathways. Technology readiness levels (TRL) are very different for the various pathways, but currently both already certified SAFs and new bio-jet fuel, as well as e-jet fuel, are potential outcomes and in the longer term – possibly also hydrogen.

For SAF to constitute a significant share of Nordic jet fuel consumption in 2030 the following considerations should be taken into account:

- Even with expected price reductions, the social costs of GHG-reductions are likely to be high for all SAFs compared to the costs of many available GHG reductions in other sectors. This means that bringing SAF to the market in significant quantities requires targeted political aviation initiatives, in addition to cross-sectoral measures such as the EU Emission Trading System or an economy wide CO2e-tax, which are generally held as cost-effective economic instruments to achieve overall national and EU-wide reduction targets.

- The strategy behind targeted policy measures for promoting SAF should be to reduce investors' risk by establishing economically attractive and stable framework conditions for a time horizon until at least 2030, rather than to push for use of high SAF volumes in the short term. This will be essential to bring on large scale production plants, which is necessary to bring down unit costs and increase production volumes to a scale with impact. A harmonised Nordic policy framework can make a difference, because the total Nordic consumption of jet fuel is more than four times that of any single Nordic country.

- A political commitment to implement a certain share of SAF in 2030 can create a strong and reliable long-term demand. Starting at very low levels and increasing progressively toward e.g. 30%[2]A target of about 30% is currently on the political agenda in Denmark, Norway, Sweden and Finland. in 2030 can allow for a gradual ramp up of supply based on large scale production.

Footnotes

- ^ Hydrogen is a less developed alternative which has not been considered in this report. The energy density by weight is higher than for (other) SAF or fossil jet fuel, but the challenges include that energy density by volume of liquid hydrogen is only about one fourth (McKinsey 2020).

- ^ A target of about 30% is currently on the political agenda in Denmark, Norway, Sweden and Finland.

Direct regulation and taxes toward sustainable aviation

This report considers five policy measures which have all been part of the public debate about policies to reduce the climate impact of aviation:

- Blending mandate

- CO2e reduction requirement

- SAF fund

- Fuel tax

- Passenger tax

Two approaches are applied to assess the policy measures:

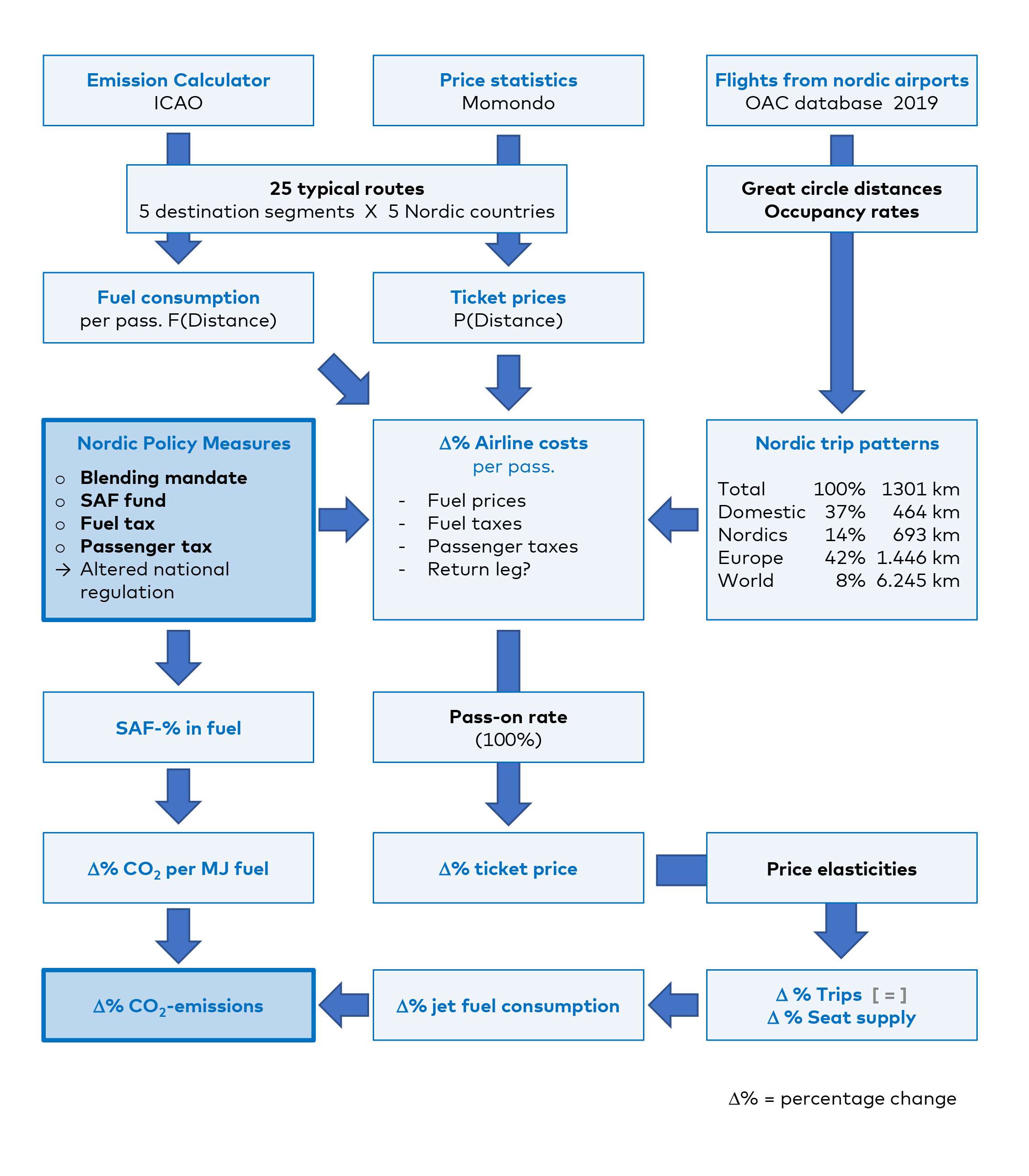

- A quantitative approach where the size of the impacts on ticket prices, air travel demand, CO2-emissions and tax revenue will be estimated based on simplified model calculations.

- A more qualitative approach based on literature reviews and with more principal arguments.

This section draws up the conclusions from the analyses which are subsequently in the next section summarized in a table with a comparative assessment of the relative advantages and disadvantages of each measure on twelve indicators.

Blending mandate, CO2-equivalent reduction requirement or a SAF fund?

Political measures can ensure a certain amount of SAF by direct regulation either as:

- a blending mandate requiring that SAF constitute a certain share of total jet fuel consumption, or a

- a CO2 reduction requirement setting a limit on CO2e-emission per MJ fuel consumed.

Raising the share or lowering the limit over time can achieve a gradual phase-in toward a target level, e.g. 30% in 2030.

The two measures are in practice rather similar depending on the criteria for SAFs which are allowed for to fulfil a blending mandate. In mutual comparison both measures have advantages and disadvantages:

- A CO2e reduction requirement has the advantage over SAF blending mandate in that it gives an incentive to use more expensive SAFs with lower lifecycle emissions if operators’ costs per litre can be compensated by meeting the requirement with a lower blending rate. The disadvantage is that the administrative costs to documentation, control and audit are higher.

- An administratively simpler, but less efficient alternative is to confine a blending mandate to advanced SAF. This will secure a high level of sustainability of the SAF but it will not necessarily minimize the GHG abatement costs. We consider a harmonized Nordic approach to be more important than the choice between a (advanced) SAF blending and CO2 reduction requirement.

- Both a SAF blending mandate and a CO2e reduction requirement are likely to increase airlines' fuel costs significantly if the SAF share is to increase toward 30% in 2030 given current price expectations. This will create severe risks of climate leakage through much stronger tankering incentives for airlines.

- Any regulation that increases airlines' fuel price will also amplify the already strong existing incentives to reduce fuel use and thereby GHG emissions. This might, in principle, lead to higher occupancy rates, extra seats in the aircraft, lower cruise speed, and/or other operational energy efficiency improvements, and not least choosing more fuel-efficient aircraft when reinvesting or advancing such reinvestments[1]In principle also to develop more fuel-efficient new aircraft. But in reality, the effect will be insignificant if confined to a solely Nordic effort, due to the countries' small share of world aviation market..

- A requirement or mandate should be levied on the fuel supplier, as in road transport, to be administratively most efficient, as they are quite few in number. To allow for maximal logistic flexibility, the fulfilment criteria should cover total annual sales as is the case for the road sector blending mandate.

- Uncertainties about the persistence of political commitment can be perceived as a severe risk by potential investors. Hence, a politically adopted target for the SAF share in 2030 might not be sufficiently stable framework conditions for the required investments described above.

An alternative to direct regulation is what is here called a SAF fund, i.e. allocating financial means for compensating the additional cost of SAF for replacing a certain volume of jet fuel. As for direct regulation, a gradual phase-in toward a target level, e.g. 30% in 2030, can be designed.

- A main advantage of a SAF fund is that it will eliminate the above-mentioned incentives to tankering by cancelling out the price differential “at the pump” between SAF-blended and fossil jet fuel, provided that the financing mechanism of the SAF fund is not directly related to the fuel price.

- Tendering of long termed purchasing or price guarantee contracts can be a strong tool to secure market demand and thereby lower investors' risks. The additional benefits of a joint Nordic SAF fund initiative will probably be very similar to those of a blending mandate or a CO2e reduction requirement.

- There are several options for the detailed design of the market creation mechanisms of a SAF fund. Pros and cons, including legal aspects, of various designs should be investigated in further detail, including whether to combine a SAF fund with a blending mandate.

- A SAF fund can be financed by Government budgets, but more likely from aviation taxes or payments from a polluter-pays-principle. Only fuel related taxes will give rise to the tankering issues of SAF blending and CO2e reduction requirements.

Footnotes

- ^ In principle also to develop more fuel-efficient new aircraft. But in reality, the effect will be insignificant if confined to a solely Nordic effort, due to the countries' small share of world aviation market.

Taxes for stimulating or financing sustainable aviation

An appropriate taxation approach to stricter regulation of climate impacts from aviation is complicated because of constraints from existing EU regulation and international agreements.

A carbon-based fuel tax is in principle an attractive instrument to secure cost-effective CO2e-reduction, both across and within sectors, in particular if implemented on a global, or at least European, scale. In practice, there are several issues related to implementing aviation fuel taxes, in particular on international flights:

- The smaller the region covered by the fuel tax, the bigger the issues of climate leakages by tankering and unfair competition will be.

- A common Nordic initiative to implement a fuel tax will reduce these unwanted effects of leakage as compared to a unilateral national implementation.

- EU regulation and international agreements limit the scope for a Nordic carbon-based fuel tax initiative. The juridical issues are complicated and subject to differing interpretations. Nevertheless, it seems safe to conclude that non-domestic fuel taxes on aviation will have to be bilaterally agreed. Therefore, a joint Nordic initiative will in the first place have to be restricted to flights within the Nordics.

- The added value of a bilaterally agreed fuel tax policy within the Nordics is additional coverage of 10% all CO2-emissions. This is because flights within the Nordics account for about 30% of all jet fuel consumption and related CO2-emissions from the Nordics, and two thirds of these emissions (about 20% of the total) would also be covered by unilateral taxes.

- A common Nordic implementation of aviation fuel taxes can subsequently be a platform for negotiating bilateral agreements on harmonized fuel taxes with neighbouring countries, such as Germany, the Netherlands and the United Kingdom. Such agreements could even be stepping stones toward a common European CO2e tax on aviation fuels which would increase the beneficial climate impacts significantly and could also minimise the leakage effects of the fuel tax. An alternative approach could be a radical reform of the EU ETS that would raise the price of emission allowances significantly.

- Finally, a carbon-based fuel tax can warrant a shift to SAF, but it is difficult to design a gradual phase-in: The tax should be high enough to match the price premium to make it profitable for airlines to substitute jet fuel with SAF. But then full shift to SAF will be more advantageous and airlines will, whether they shift to SAF or not, bear the full cost premium on all fuel consumption at once.

A passenger tax is a rather blunt instrument for promoting sustainable aviation in comparison with the previous measures. It only creates GHG reduction via demand side incentives to reduce the number of air trips.

- The clear advantage of a passenger tax is that it avoids the issues of climate leakage from tankering incentives by measures that increases fuel costs.

- To the extent that a passenger tax can be differentiated according to distance, it can be more closely related to CO2 emissions per trip and hence create a stronger incentive to reduce longer trips and thereby GHG-emissions. Similar arguments hold for differentiating the passenger tax according to aircraft specific fuel efficiency per seat.

- International agreements and EU legislation limit the options for differentiating passenger taxes. Interpretation of the scope for national possibilities to differentiate passenger taxes within EEA is disputed. Still, no European countries that have implemented passenger taxes have differentiated their rates between destinations within the EA, but higher rates for other destinations are common.

Comparative impact assessment of five policy measures

This section gives an overall comparative assessment of the policy measures using twelve indicators:

- Overall CO2 impact: To what extent can a joint Nordic implementation contribute to significant reductions of CO2 -emissions from domestic and international air travel from the Nordics?

- Flights outside the Nordics: Can the policy measure be imposed on flights to destinations to the rest of the EEA and the rest of the world?

- Reducing demand by fewer and shorter trips?

- More fuel-efficient operations, including more passengers per flight, energy optimizing speed, flight route and altitude, use and by energy efficient aircraft etc.?

- Using (more) sustainable fuels: Does the policy measure promote use of SAF and give incentives to prefer fuels with lower life cycle GHG emissions?

- Market creation for SAF: Will the policy measure guarantee a demand for SAF that will enable economics of scale and competition driven cost reductions?

- Avoid leakage risks: Can the policy measure avoid creation of or reduce incentives to tankering or to shifting operations to airports outside the Nordics with lower fuel prices?

- Government budget revenue: Does the policy measure have a net positive impact on Government revenue that can be used to promote sustainable aviation or other purposes?

- Polluter-Pays-Principle: Does the policy measure secure that social costs to prevent or remedy GHG-effects are financed by liable producer or consumer?

- Cost effectiveness: Does the policy measure give adequate incentives to choose or develop solutions that minimize the social costs of the reduction?

- Administrative burden: Are costs to the aviation industry, the regulatory body and the air travellers’ airlines to administrate the regulation ignorable or small compared to achieved effect?

- International regulation compliance: Is it certain that the policy measure is uncomplicated to implement in a Nordic context without conflicting with EU regulation or international conventions and agreements?

The comparison is summarized in the in Figure 1.1. The scores "YES", "yes", "no", and "NO" are to be interpreted as an assessment of relative ranking among the five policy instruments – "YES" in capital letters being the highest ranked, to "NO" in capital letters being the lowest. The ranking is extracted from the analyses above and not derived from exact criteria. Hence, refinements of the scores can be debated.

Figure 1.1 Comparative assessment of five policy measures for sustainable aviation

| Assessment of measure with regard to: | SAF blending requirement | CO2e reduction requirement | SAF Fund | Fuel tax | Passenger tax |

| Overall CO2-reduction impact | YES | YES | YES | yes | yes |

| Flights to outside the Nordics | YES | YES | YES | NO | YES |

| Reducing demand: Fewer trips | yes | yes | NO | YES | YES |

| Shorter distance | yes | yes | NO | YES | yes |

| Fuel efficient operations 1 | yes | yes | NO | YES | NO |

| Using (more) sustainable fuels | yes | YES | YES | yes | NO |

| Market creation for SAF | yes | yes | YES | no | NO |

| Avoid leakage risks 2 | NO | NO | YES | no | yes |

| Government budget revenue | no | no | NO | yes | YES |

| Polluter-pays-principle | yes | YES | NO | YES | yes |

| Cost effectiveness | NO | no | yes | YES | NO |

| Administrative burden minimised | no | NO | yes | no | yes |

| International regulation compliance | YES | YES | yes | yes | YES |

| (1) Including occupancy rate, cruise speed, etc. (2) Tankering or displacing operations abroad. The leakage risk is less for a fuel tax than for a SAF blending and CO2 reduction requirement because the fuel tax is assumed to be imposed only for flights within the Nordics. | |||||

The overall picture from the figure is that the counts of "YES"/"yes"/"no"/"NO" are not that different across policy measures. Although some indicators can be said to be more important than others, none of the policy measures stand out as either clearly advantageous or the opposite.

Passenger taxes will only reduce CO2-emissions through lower demand. Hence, rates have to be unrealistically high to result in significant CO2 reduction. The same applies to fuel taxes unless they are set high enough to eliminate the cost premium of SAF. In addition, a common Nordic fuel tax regime will only apply to flights within the Nordics, which will reduce the total demand driven reductions with two thirds, cf. above.

Significant CO2 reductions will require a blending or CO2 reduction requirement or a SAF fund, as these measures can be designed to secure a substantial use of SAF, even if implemented by the Nordics alone.

By increasing fuel costs, the two measures based on requirements will at the same time indirectly give (some) incentives for travellers to reduce travel demand and for airlines to improve energy efficiency of operations. However, this effect is a "double-edged sword" as the increased fuel costs at the same time creates risks of leakage effects.

Both the enhanced incentives to reduce fuel consumption and the risk of leakage is avoided by the SAF fund that eliminates the cost premium of the SAF. The main disadvantage of a SAF fund is that it demands funding, which in the table is assumed to be financed by the Government budget, – to illustrate its pure form. This will of course have costs elsewhere in society and thereby violates the fairness of the"'Polluter-Pays-Principle".

Combining a SAF fund with an earmarked passenger tax

Both the financing and polluter-pays-principle issues with a SAF fund can be addressed by combining it with a tax at a rate that generates a revenue of the estimated size to finance the price premium of SAF at the targeted share, e.g. 30% of total jet fuel volumes. If a fuel tax is chosen as the financing mechanism in a combined measure it can, as mentioned, only be levied on internal Nordic flights. Hence, to finance 30% SAF for all flights it has to be rather high. This will result in a quite distortive tax differential between internal Nordic and extra-Nordic flights. A passenger tax can be levied on all flights and set at higher rates outside to destinations outside the EEA to reflect the higher GHG impact of these long-haul flights. This might reduce long-haul trips or shift them to shorter distances and thereby reduce GHG-emissions. Hence, it will be more in accordance with the "polluter-pays-principle" than a fuel tax confined to flights within the Nordics.

Taxes will have to be implemented in national legislation, and this could be mirrored in parallel national SAF funds with harmonized setups. Still, a joint Nordic fund with unified tendering processes for greater volumes of SAF will have a stronger signaling effect.

Figure 1.2 presents an assessment of a combined SAF fund and a passenger tax along the same lines as for the single measures in Table 1.1. It appears that the combined measures generally have positive ratings on the twelve indicators, because one measure in many cases compensates for the disadvantage of the other. Only one negative rating stands out: The combined measure does not create incentives to more fuel -efficient operations. However, as mentioned above, this is the unavoidable downside of avoiding risks of leakage from increasing fuel costs at Nordic instead of an EEA or global level.

Figure 1.2 Assessment of SAF fund & earmarked passenger tax

| Assessment of measure with regard to: | SAF fund & Passenger tax | |

| Overall CO2-reduction impact | YES | |

| Flights to outside the Nordics | YES | |

| Reducing demand: – Fewer trips | YES | |

| – Shorter distance | yes | |

| Fuel efficient operations * | NO | |

| Using (more) sustainable fuels | YES | |

| Market creation for SAF | YES | |

| Avoid leakage risks ** | yes | |

| Government budget revenue | yes | |

| Polluter-pays-principle | yes | |

| Cost effectiveness | yes | |

| Administrative burden minimised | yes | |

| International regulation compliance | yes |

Note: To be compared with Figure 1.1

Given that a main reason for a combined measure is that the passenger tax is meant to establish a fair and feasible way of financing the extra costs of SAF compared to fossil jet fuel it makes sense to set the level of the passenger tax and the SAF share so as to obtain a revenue that approximately balances the total extra fuel costs.

It turns out from model calculations that these criteria might be fulfilled with a 30% SAF share and a common Nordic passenger tax with rates corresponding to the average of the current Norwegian and Swedish passenger tax rates. Based on model calculations it is estimated that this scenario will lead to:

- a passenger tax revenue of slightly more than 1 bill. EUR per year;

- extra fuel costs of about a little less than 1 bill. EUR per year; and that

- the common Nordic passenger tax amounts to about 4% of ticket prices on average.

Again it should be stressed that these figures and, hence, the relationship between the SAF share and the required tax rates depends heavily on the assumptions, and in particular the forecasted price premium of SAF compared fossil jet fuel price. This relationship will be strongly influenced by the future costs of EU ETS allowances. Depending on the price development of the allowances they fully or partially substitute passenger taxes for flights within EEA.

Main policy recommendations for promotion of SAF

To conclude, the above considerations leads to the following overall recommendations for the types of policy measures that are required and appropriate for promotion of SAF:

Supply-side measures with a long-term perspective are needed to promote sustainable aviation. In a 2030 perspective, this will in practice mean pushing for a gradual increase to significantly higher share of SAF of total jet fuel consumption. Demand-side measures in terms of increased taxation can remedy excessive air travel from under-taxation of aviation both with respect to its climate impact and to other modes of transportation, in particular road transport. However, national or Nordic taxes alone are not likely to lead to a profound leap forward toward sustainable aviation over the next decade under existing international regulation. A combination of establishing a SAF fund and a passenger tax or payment on all aviation might both minimise carbon leakage from tankering and provide financing mechanism for the additional costs of a significant share of SAF in total jet fuel consumption. A joint Nordic policy framework consisting of a joint Nordic (or parallel national) SAF fund financed by harmonised Nordic passenger taxes or payments will enhance efforts to create significant and stable volumes of demand for SAF towards 2030. Such long-termed demand commitments will enhance opportunities for large scale production by reducing investor risks.

Finally, when deciding on common Nordic initiatives for sustainable aviation the global dimension of climate change should be recalled. Reductions of GHG emissions stemming from Nordic aviation contribute little to the overall climate impact of global aviation. This is not to say that common Nordic initiatives are not essential, on the contrary. But arguably, the most significant overall impact might be via its influence on European and international climate change policies. The exact design of a common Nordic policy framework should also take into account how this influence can be maximized.

Initiatives to accelerate innovation in electric aviation

Electric propulsion can contribute to more sustainable aviation in two ways:

- Firstly, by higher energy efficiency of electric motors compared to conventional combustion engines.

- Secondly, by battery storage of electricity based on renewable energy.

Battery storage is essential for electrification to be a genuine alternative to SAF that avoids the challenges described above for SAF. The main disadvantage of batteries is their weight, which is a much bigger challenge for aviation than for surface transport. Hybrid-electric aircraft where one of the engines are replaced by an electric motor and SAF combined with hydrogen fuels cells can be first steps toward "pure" electrification (i.e. 100% battery energy storage).

The relatively low technology readiness level (TRL) of airplanes with electric propulsion means that it can be politically difficult to credibly commit to stable long-termed framework condition in general at the current stage of maturity where high uncertainty prevails.

Political initiatives should focus primarily on measures that can encourage and financially support RD&D and accelerate innovation. This could include programmes for Nordic cooperation, experience exchange etc. Widespread market creation in line with the strategy for SAF described above appear to be premature until higher levels of TRL is reached. Nordic cooperation to promote electric aviation should target short routes up to about 500 km. Toward 2030 this is most likely the only segment where electric airplanes will have potential. This includes some of the most travelled Nordic routes, but most will be domestic. Very short routes (<200 km) will be most suitable for the earliest demonstration projects. An agreement on financial support for parallel demonstration projects in all or several Nordic countries could be part of a common vision. All countries have suitable routes, but about two thirds of the very short routes are Norwegian due to the country's challenging geography with fjords and mountains which hampers surface transport.

Over the next decade, certified electric airplanes will predominantly be small; with up to 9 or 19 seats for certification reasons. This means that additional staff costs and other operational costs per passenger will be higher than today. This will counteract and possibly more than outweigh the potential cost savings on propulsion energy and technically lower maintenance demands. In that case, commercial operations will require political subvention.

- Clear signals of political commitment to financial support that can reduce risks and secure viable business cases for electrified routes are crucial to attract operators in the early phases.

- The financial implications of securing viable business cases for operating electric airplanes on a limited number of short routes are manageable. Many levers can be pulled to support operators willing to invest in electric aviation, for example:

- Environmental zero emission criteria in tendering of selected routes with public support

- Providing the necessary charging infrastructure in relevant airports

- Removing or reducing operators' financial risks of investment in through “pool purchasing” electric airplanes, e.g. by buying the aircraft and leasing it to the operator for the contracting period

- Passenger tax exemption for electric aircraft or similar economic support

- Harmonizing standards for electric airplanes, e.g.

- common charging standards

- common security standards

- prioritising joint efforts on standardisations in international fora

Several of these initiatives will be strengthened through a joint Nordic approach.

How to finance initiatives to promote electric aviation is basically a matter of political prioritisation. However, one solution that springs to mind is the combination of a SAF fund and passenger taxes. Extra finances to support developing electric aviation as well can be provided by phasing in common passenger taxes faster than the financial needs for the gradually increasing SAF share of fuels.

Next steps

This report has outlined overall recommendations for a joint Nordic approach to promoting more sustainable aviation in the Nordics. If the Nordic countries agree to move forward in line with the suggested approach next steps in the preparation of specific and joint initiatives could be to:

Conduct a juridical assessment of alternative models for construction of a Nordic or parallel National SAF fund(s), in particular which financing mechanisms that would be in accordance with the EU’s state aid regulation. Elaborate the detailed design of the financial support mechanism of a SAF fund, including sustainability criteria for eligibility of SAF. Nationally implemented and harmonized passenger taxes in each Nordic country, taking into consideration the size and structure of existing and expected passenger taxes in neighbouring European countries. Politically adopt a common Nordic commitment to pursue the potentials of electric aviation Finance a common Nordic research and innovation programme for SAF and electric propulsion Form a united position in EU and international fora pleading for EU-wide GHG taxation of fossil jet fuel or alternatively a wider scope for national implementation of distance-based passenger taxes.

2. Introduction

2.1 Strong growth in aviation and its emissions

Air transport of persons and goods has been steadily increasing with on average high growth rates in most part of world, including the Nordic countries. Globally, commercial aviation counts for around 2.4% of the global total greenhouse gas (GHG) emissions from energy use (Graver et al., 2019). In the EU, the aviation sector in 2016 was responsible for 3.6% of total GHG emissions (EEA et al., 2019, p. 8).

The substantial increase in aviation has caused large growth in the aviation sector’s total GHG emissions globally, despite significant improvements in the energy efficiency of airplanes in the last decades (Ministry of Transport, 2019). The climate impact of emissions in high altitudes is, moreover, significantly larger than for surface emissions due to contributions to e.g. cirrus cloud formation, condensation trails, emissions of soot and aerosols, when flying in high altitudes (e.g. IPCC, 1999; McKinsey, 2020; Aamaas & Peters, 2017).

Aviation is, moreover, also a source of local pollution, such as nitrogen oxides (NOx) emissions and ultrafine particles (e.g. Keuken et al., 2015), and it also leads to significant local noise nuisance (Basner et al., 2017; Krog et al., 2017), in particular around airports (EEA et al., 2019). Poor air quality is an important cause of premature deaths and ill health in Europe and elsewhere (European Environment Agency, 2019; Khreis et al., 2019). However, it seems that aviation’s impact on local particle pollution in at least some of the Nordic countries is rather modest, like at Oslo Airport, other Norwegian airports and at the Stockholm Airport (Avinor, 2020b; Krog et al., 2017; Swedavia Airports, 2020a).

Estimates of growth in international air transport over the next decades vary, but the general expectation is that aviation is expected to continue to grow at a rapid pace. The International Civil Aviation Organization (ICAO), estimates that aviation will increase 3.3 times measured in revenue tonne kilometers (RTK). Fuel consumption will, depending on the scenario, increase by 2.2–3.1 times in 2045 compared to 2015 (ICAO, 2019b). Increases in aviation are closely connected to economic growth, and the largest growth of aviation in the next two decades is expected to be in the Asia-Pacific area (Boeing, 2019; IATA, 2018b).

Thus, if measures are not implemented, growth in aviation seriously increases the sector’s contribution to global warming (EEA et al., 2019). Estimates of aviation’s share of the world’s remaining carbon budget are uncertain. The share of the remaining carbon budget is most likely going to increase, if the growth continues, because other sectors are reducing their GHG emissions (see e.g. Carbon Brief, 2016; McKinsey, 2020).

Aviation has also grown substantially within the European Union (EU) and the European Economic Area (EEA) in the last decades, up until the Covid-19 crisis hit the area. Aviation traffic in Europe has been expected to grow by 50% from 2012 to 2035 (European Commission, 2015, p. 9). Total airline activity in Europe, accounts for around 27% of total global airline activity and 25% of airline fuel consumption, excluding Russia and the rest of CIS (Strand, 2019).[1]Armenia, Azerbaijan, Belarus, Kazakhstan, Kyrgyzstan, Moldova, Russia, Tajikistan and Uzbekistan.

Footnotes

- ^ Armenia, Azerbaijan, Belarus, Kazakhstan, Kyrgyzstan, Moldova, Russia, Tajikistan and Uzbekistan.

2.2 A regulatory gap in international aviation

In other words, aviation has created important societal benefits, being a crucial factor in our long-distance mobility, but the downside is significant external costs in terms of contributions to climate change as well as other environmental impacts. The fact that there is almost no taxation of international aviation outside Europe, although a considerable share of the climate impact from aviation comes from medium and long-distance flights, suggests that additional measures are required to reduce these costs (Pirlot & Wolff, 2017; Schuknecht, 2019; Strand, 2019).

It has, so far, proven very hard to obtain international agreements on global standards that reduce aviation emissions in the next years and decades to levels that are compatible with the targets in the Paris agreement. International aviation is, for example, not subject to value added tax (VAT) or fuel charges (Amsterdam Economics & CE Delft, 2019). This has been intended policy from the side of ICAO (Pirlot & Wolff, 2017, Interviews 2020), as they have opted to develop aviation internationally to the largest extent possible. The lack of VAT in international transport is attributed to the fact that most goods are taxed either in the country where they are produced or consumed, and thus, international aviation and other international transport is excluded (Pirlot & Wolff, 2017).

In Europe, the EU Emissions Trading System has since 2012 applied to aviation within the European Economic Area. However, to date, most emission allowances have been given for free. In addition, some European countries have implemented passenger taxes, but many countries also either charge a low or even zero VAT rate on domestic flights (Amsterdam Economics & CE Delft, 2019; Faber & Huigen, 2018; Strand, 2019).

Comparison of fairness of operating conditions across for different modes of transport is, however, not straight forward: As the aviation industry itself points out, aviation pays fully for its own infrastructure, the airports, while for example the railways do not fully pay for railway stations or the railway lines (Pirlot & Wolff, 2017, Interviews, 2020). In road transport many parts of the network access are offered for free. Some countries have road user charges. All EEA countries have fuel taxes which can finance the infrastructure and cover at least some of the other external costs of related to driving.

2.3 Ambitious goals for GHG reductions in the Nordic countries

The Nordic countries Denmark, Finland, Iceland, Norway, and Sweden have all committed to becoming climate neutral within the next two or three decades and they all have high ambitions to become more environmentally sustainable (e.g. Danish Government, 2018; Karlsen, 2017; Ministry for the Environment and Natural Resources, 2018; Ministry of Finance, 2019; Ministry of the Environment, 2018). This is also the case for the transport sector: Sweden is at the forefront regarding using biofuels in road transport. Norway is leading internationally in electrification of cars and ferries.

The Nordic countries, the Nordics for short, have a long history of cooperation. For example, they created the Swan ecolabel. Norway and Sweden launched the world’s first international electricity market, NordPool, which today also includes the other Nordic countries (except Iceland) and the Baltic states. Sweden and Norway launched the world’s first international market for trade of green certificates to support the production of renewable energy. The Nordics also led the development in creating standards for telecommunication: NMT and GSM.

In January 2019, the Nordic Prime Ministers signed “Declaration on Nordic Carbon Neutrality”, committing their countries to strengthening mutual cooperation to attain carbon neutrality domestically. The declaration emphasizes decarbonization of the transport sector, such as through shifting between transport modes, enhancing energy efficiency, electrifying various transport modes, and using sustainable renewable fuels (Sipilä et al., 2019).

The aim of this report is to examine the opportunities for increased Nordic cooperation with regards to increasing sustainability of aviation and based on evaluation of alternative options propose common Nordic policy measures.

2.4 Strategies to reduce emissions from aviation

It is generally recognized that the ultra-high mobility generated by air transport is perceived as an important and highly valued factor in the lifestyle among the wealthy in the world, and is a crucial contributor to the benefits of globalization, including extensive international trade (see European Commission, 2015). Curbing air travel by strong demand-side measures that could stop aviation growth is seen by some as a necessity. In the political mainstream, however, this is not considered an attractive path to significantly reduce GHG from aviation. This is, of course, not an either-or situation, as a cost-efficient climate policy for aviation may very well include policies that both reduce GHG emissions per trip and incentivize customers to drop the least important trips, choose alternative modes of transportation or to choose destinations nearby.

A wide range of political measures can be used to reduce GHG emissions from aviation. All measures will in principle function through one or more of the following three sub-divided factors:

- Reduced air transport (passenger and tonne kilometers)

- Energy efficiency improvements, by:

- More passengers or freight per flight

- Air traffic management and operations

- Less fuel-consuming types of airplanes among existing types

- Technological development of aircraft and engines

- Replacing fossil jet fuel by energy carriers with lesser climate impact, through:

- Fuels with lower life cycle GHG emissions

- Electric propulsion instead of combustion engines

In the last decades, the average GHG emissions per passenger or tons per kilometer have declined significantly, mainly through energy efficiency improvements (IEA, 2020; McKinsey, 2020). For example, in Norway from 1998 to 2018, gradual improvements have been achieved adding up to more than a 50% reduction in CO2 emissions per passenger kilometer for the two largest airlines. Emissions have declined from 196 gCO2/km to 83.5 gCO2/km. These airlines, SAS and Norwegian, together cover more than 70% of the airline passengers in Norway (Ministry of Transport, 2019).

Over the next two decades, fuel efficiency improvements for new conventional aircraft are estimated to be at best about 40% compared to 2016 by 2034, if “all” cutting-edge fuel-saving technologies are implemented (Kharina et al., 2016). Air traffic management is expected to be able to generate another 5–10% of the potential improvements in the future.[1]ITF-workshop 24. Feb 2020 [no precise source can be listed due to Chatham House Rules]. However, this would probably at best just level out the effect of the expected demand growth (Fleming & Lépinay, 2019; ICAO, 2018; McKinsey, 2020). Adding that the significant GHG reductions required from aviation to reach long-term climate targets implies that a major share of the reductions will expectedly have to come from replacing fossil energy with low-carbon alternatives.

Footnotes

- ^ ITF-workshop 24. Feb 2020 [no precise source can be listed due to Chatham House Rules].

2.5 Sustainable aviation fuel (SAF)

As explained above, radical reductions of GHG emissions from aviation requires a shift away from fossil fuels, as there are physical and technical limits to how much can be achieved by fuel efficiency gains. Even though speeding up deployment of fuel saving technologies in new aircraft and development of completely new propulsion systems are crucial in the long run, the short- and medium-term effects will likely be modest due to a number of factors. A main factor is the long economic lifetime of aircraft: A modern aircraft is expected to be in service for two to three decades.

From an operational point of view, the easiest way to significantly improve the sustainability of each journey by airplane in the next years is probably to replace the jet fuel with what is termed sustainable aviation fuel (SAF). SAF is a term that encompasses various fuels that have been certified as sustainable according to independent third-party bodies such as Roundtable on Sustainable Biomaterials and certified for safety and performance by American Society for Testing of Materials (ASTM International). There are a number of high-carbon feedstocks that may be used to produce such fuels, including biomass, biogas, animal fat and bio oils (Wormslev & Broberg, 2020). SAFs are termed “drop-in fuels”, as they can be blended in fossil fuels immediately with minimal need for technical changes in the airplanes and other infrastructure. The maximal blending rates of SAFs today is 50% (Wormslev & Broberg, 2020).

Bio-jet fuels

Biomass constitutes an important part of the use of renewable energy in the Nordics, but very little is used in aviation. A number of projects have been launched for producing various types of sustainable aviation fuel (SAF), mostly advanced biofuel, in the Nordics. Market prices for SAF are today high and the production volumes are low (European Commission & DG Move, 2020; Swedish Government, 2019a). For example, only about 0.05% of jet fuel used in the EU is SAF. SAF consumption in 2050 in aviation will only contribute to 2.8% of total aviation fuel consumption in 2050, according to estimates (European Commission & DG Move, 2020, p. 3).

This could change in the future, depending on political commitment and what measures are implemented to increase it (Mortensen et al., 2019; Rambøll, 2017; Wormslev & Broberg, 2020; Wormslev et al., 2016). Various types of support are needed to establish higher production capacities, drive innovation and thus bring down prices:

In the absence of a long-term, stable policy framework with sufficient incentives, the necessary confidence for major investments in SAF production is not provided. Such investments would enable economies of scale in the production and drive production costs down. (European Commission & DG Move, 2020, p. 2).

E-jet fuels

A special type of SAF is electro-jet fuels or e-jet fuels (synthetic kerosene) where electricity is used to produce hydrogen (from water) which is subsequently converted to fuels. The process requires carbon which can come from either biomass, including forest residues, or from CO2 captured from point sources or from the air (DAC). According to some analyses, e-jet fuels are essential to make aviation fuel sustainable in the next decades, because of the globally limited sustainable feedstock potential for biofuels (Energinet, 2019; Mortensen et al., 2019; Wormslev & Broberg, 2020).

However, the big challenge with e-fuels is the costs, due to the large amount of renewable energy needed to produce it and the technical development needed to commercialize it. Cost estimates for e-fuels vary widely. A study found, for example, optimistically that in several scenarios, e-fuels can compete with fossil fuels in 2035 in Denmark (Energinet, 2019). E-fuels will likely be cheaper to produce sustainably than previously in the next decades anyway, due to the lower cost of producing electricity: Photovoltaic power and onshore wind power are for example likely reaching cost competitiveness with other types of electricity on the global markets in 2020 (IRENA, 2019).

Direct combustion of liquid hydrogen (LH2) in turbines is an alternative pathway which has a considerably lower energy loss compared to e-jet fuels because liquefaction by cooling is less energy demanding than the conversion process from hydrogen to a hydrocarbon liquid fuel. However, hydrogen-based propulsion technology is still at a very low TRL. Although promising, this alternative is far less mature than both bio-jet fuels and synthetic jet fuels and is therefore also outside the scope of this report. For an updated study of the hydrogen potential strategic overview, see McKinsey (2020).

2.6 Electrification

In the next decades, electrification also holds a lot of potential, at least for short distances. Electric aircraft is here defined as an aircraft that is fitted by one or more electric motors for propulsion (Avinor & Civil Aviation Authority, 2020, p. 50; McKinsey, 2020). Electrification could be a significant contributor to reducing the climate impact of aviation within the Nordics, where there is a large number of routes that are short (Avinor & Civil Aviation Authority, 2020; Roland Berger, 2017, see also Chapter 5.4 and Appendix B.4). Partial electrification, e.g. to launch hybrid electric motors with both combustion engine and electric engines could also help bring down GHG emissions on medium-haul and long-haul routes.

Electricity production in the Nordics is increasingly based on renewable sources and will in the future be close to 100% fossil free. Such electrification also reduces other negative externalities of using liquid fuel in aviation, namely the release of particles and contrails high up in the air, the potential use of crops that could be used for food or other purposes (LULUCF) and the noise from combustion engines. Analyses point in different directions as to when electric and hybrid electric airplanes will be introduced and how quickly they will replace airplanes with conventional and bio-based fuels (e.g. Avinor & Civil Aviation Authority, 2020; Roland Berger, 2017).

Electrification of the aviation sector is, however, challenging, for a number of reasons (Hanano, 2019; Roland Berger, 2017; WSDOT, 2019; Ydersbond & Amundsen, 2019, 2020). The most important issue is likely that the energy density of batteries needs to be significantly higher (at least 500 Wh/kg) than what is the case today (250 Wh/kg for batteries in commercial use to up to over 300 Wh/kg for new innovations) if they are to be used for commercial purposes (Roland Berger, 2017). Another issue is the low technological readiness level (TRL): only one electric airplane, a battery electric two-seater, is so far certified for ordinary flying (in 2020). It is impossible to predict the scale of introduction, and exact timing of introduction of aircraft with this group of propulsion technologies.

2.7 Report structure and scope

The report will focus on aviation in the Nordics, i.e. flights and trips within and between the five Nordic countries as well as to other countries. Only commercial, scheduled aviation will be considered, and focus will be on passenger transport. With regard to the potential for electric aviation the report will mainly focus on battery electric aircraft whereas hydrogen electric aircraft, i.e. hydrogen energy storage combined with a fuel cell for conversion to electric power, will not be considered due to its very early and uncertain stage of development. The same holds for hydrogen as a sustainable aviation fuel for combustion in turbines.

The next chapter gives an overview of travel patterns in the Nordics in terms of travel volumes within and between the Nordic countries as well as to Europe and the rest of the world. Subsequently, Chapter 3 and 4 give an overview of the international regulatory context and the current Nordic perspectives on sustainable aviation in terms of relevant existing policies and other initiatives with regard to sustainable aviation fuels and electrification. Finally, Chapter 6 analyses and assesses potential Nordic policy measures for promotion of sustainable aviation fuels in Nordic aviation.

Impacts of Covid-19 on this report

The Covid-19 crisis hit international aviation and other economic activity hard from the beginning of 2020 and led to a dramatic and unprecedented decline in the number of flights domestically and internationally (ICAO, 2020a). Several countries, including many countries in the EEA, closed their borders temporarily and launched travel restrictions (e.g. ICAO, 2020a; Isaksen, 2020). This led to an unprecedented economic crisis in the aviation industry. Different countries launched large rescue packages to save their airlines from bankruptcy (e.g. Mikalsen, 2020; Rasmussen, 2020; Trumpy, 2020).

How long this crisis will last is uncertain, and also what kind of consequences it will have for the national, European and international community. For example, if airlines go bankrupt, this may lead to lower competition and higher ticket prices. Moreover, the Covid-19 crisis may have profound long-term implications in terms of reducing passenger demand; Businesses have grown used to communicating via digital platforms rather than meeting in person (Sandberg, 2020), which make them demand less travel by airplane. This development is likely also stimulated by the fact that many businesses, an important customer group, have suffered and are suffering economically, and are thus reducing travel to cut their costs (Interview NEA, 2020).

However, in all previous crises the last decades, passenger volumes have rebounded after 1-2 years, or simply been stable for a period, and subsequently reached previously unprecedented growth levels (Boeing, 2019, p. 17). Probably, the aviation industry will, when the Covid-19 pandemic is over, return to normal business sooner or later, and passenger numbers will continue to increase. Some analysts argue that it may take at least until 2023 before the airlines are back to their passenger numbers pre COVID-19. In some scenarios, the current COVID-19 crisis may have a long-lasting impact on aviation travel demand (Curley et al., 2020). If activity rebounds to expected levels of growth, this will also be the case regarding GHG emissions.

In this study, we will not take into consideration the possible impacts of the Covid-19 crisis. The possible consequences for long-term growth are not assessed to be in an order of magnitude that is likely to influence the types of measures that are most suited to promote the transformation of the Nordic aviation sector to sustainability. However, the current crisis might very well influence how fast the measures should be implemented to take into account the weak financial situation of the industry and hence the capability to invest in and adjust to the transformation. The timing and pace of climate policy implementation is not considered in this study.

3. Overview of aviation in the Nordic countries

3.1 Internal and international travel patterns

The potential benefits from joint Nordic policies to promote sustainable aviation depends on the importance of air travel between the Nordic countries compared to total air travel volumes for these countries. Comprehensive data for total passenger volumes are not readily available. However, a good proxy indicator is the “Seat supply”. That is: the sum across all flights of the number of seats available. Seat supply in 2019 is shown for each Nordic country with a split on geographical destination segments:

- Domestic: Flights within each country

- Nordic: Flights between Nordic countries

- Europe: Flights to the rest of the Europe

- World: Flights to the rest of the world

Table 3.1 Seat supply from Nordic countries in 2019

| From: (population in mill.) | ||||||

| To: | Denmark (5,8) | Finland (5,5) | Iceland (0,4) | Norway (5,3) | Sweden (10,1) | Total (27,1) |

| Domestic (464 km) | 3,011,187 | 4,572,125 | 379,492 | 24,534,349 | 11,089,018 | 43,586,171 |

| Nordic (693 km) | 4,533,809 | 2,595,233 | 830,283 | 4,220,302 | 4,412,167 | 16,591,794 |

| Europe (1,446km) | 13,490,910 | 7,287,865 | 2,112,860 | 10,149,603 | 12,629,391 | 45,670,629 |

| World (6,245 km) | 2,253,201 | 2,293,167 | 1,247,102 | 799,050 | 1,496,849 | 8,089,369 |

| Total (1,301 km) | 23,289,107 | 16,748,390 | 4,569,737 | 39,703,304 | 29,627,425 | 113,937,963 |

| 20% | 15% | 4% | 35% | 26% | 100% | |

Source: Extracts from OAG-database (https://www.oag.com/).

Note: Return flights from outside the Nordics are not included.

In 2019 the overall seat supply was about 114 million seats per annum. The differences in total volumes across the Nordics reflect population size and country area. When correcting for population size, the figure corresponds to 4.2 seats per capita per year, with Iceland and Norway clearly above the rest. For Iceland, it is primarily a high seat supply to Europe, whereas Norway has a high domestic seat supply, most likely due to widespread mountains and fjords, and very long distances, making surface transport more complicated and expensive. Denmark's small size results in a low number of domestic trips because cars and trains are good alternatives. The hub function of Copenhagen Airport results in higher volumes to Europe and the rest of the world. The same is to some extent true for Reykjavik and Helsinki for flights to North America and East Asia, respectively. For Sweden, the regional distribution of flights is close to average for the Nordics.

Short, medium and long haul

It is common to distinguish flight distances by term short-, medium- and long-haul. There are no commonly agreed, exact definitions of limits between them, but for example Eurocontrol defines medium-haul routes as being between 1,500 and 4,000 km. Taking this definition as departure all domestic and practically all Nordic routes are short-haul, while routes to Europe will be classified as mainly short- and medium-haul, whereas almost all (direct) flights to the rest of the world will be long haul.

In addition, regional flights are sometimes used for the shortest short-haul routes, typically about one hour or less.

Seat supply is a relatively good indicator for demand for air trips, but for fuel consumption and GHG emissions flight lengths are obviously also important and need to be taken into account. The statistics on available seat kilometres (ASK) adds all flight lengths for every seat supplied. However, ASK is not a precise indicator for energy consumption because fuel consumption per seat kilometre varies with distance and other factors.

Figure 3.1 shows ASK distributed on 500 km flight length intervals by the blue bars whereas the accumulated distribution is illustrated by the curve. Long-haul flights (above 4,000 km) constitute a relatively small share of seat supply, but they account for about one third of the total ASK. Short-haul (under 1,500 km), which are the most and frequent, and medium haul (1,500-4,000 km) account for about another third each.

Figure 3.1 Available seat kilometres (ASK) in 2019 from Nordic countries distributed on flight lengths.

Source: Extracts from OAG-database combined with distances from www.gcmap.com

3.2 Airline market shares

The market structure within each geographical destination segment is also relevant with a view to possible policy instruments for promoting sustainable aviation. Table 3.2 shows the market share in 2019, again measured by seat supply, for all departures from each Nordic country. For the Nordics in total, the figures are split on destination segments. Market shares are shown for Nordic and foreign airlines and airlines with more than 1 million seats supplied are listed individually.

Table 3.2 Market shares in 2019, measured as seat supply with departure from a Nordic airport. Split on departing countries and on destination segments.

| From: | Denmark | Finland | Iceland | Norway | Sweden | Total | ||||

| To: | Total | Total | Total | Total | Total | Total | Domestic | Nordic | Europe | World |

| Totalsum | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% |

| Nordic Airlines | 60% | 87% | 80% | 87% | 69% | 77% | 100% | 98% | 49% | 63% |

| SAS | 34% | 4% | 3% | 38% | 35% | 30% | 40% | 49% | 16% | 15% |

| Norwegian | 18% | 12% | 3% | 34% | 19% | 22% | 27% | 22% | 19% | 10% |

| Finnair | 2% | 70% | 1% | 1% | 2% | 12% | 9% | 17% | 10% | 24% |

| Wideroe | 1% | 0% | 0% | 14% | 0% | 5% | 12% | 3% | 0% | 0% |

| Braathens Regional | 0% | 0% | 0% | 0% | 11% | 3% | 8% | 0% | 0% | 0% |