- Full page image w/ text

- Table of contents

- FOREWORD

- ACKNOWLEDGEMENTS

- 1. EXECUTIVE SUMMARY

- 2. INTRODUCTION

- 3. METHODOLOGY

- 3.1 The Energy Trilemma

- 3.2 The energy crisis and security of supply

- 3.3 The energy value chain

- 3.4 Scope of the study

- 3.5 Delimitations

- 3.6 Data collection

- 3.7 Description of data sources

- 3.8 Interviews

- 3.9 Assessment of the data used

- 3.10 Report structure

- 4. INTERNATIONAL ENERGY SYSTEMS AND MARKETS

- 4.1 The electricity system

- 4.2 Natural gas and electricity prices in Europe

- 4.3 The energy system in Iceland

- 5. DRIVERS, PREPAREDNESS AND RESPONSES

- 5.1 Electricity market structure

- 5.2 Decommissioned controllable electric capacity

- 5.3 Balancing electricity supply and demand

- 5.4 Lack of electric grid infrastructure

- 5.5 Inflexible electricity demand

- 5.6 Weather-dependent energy supply

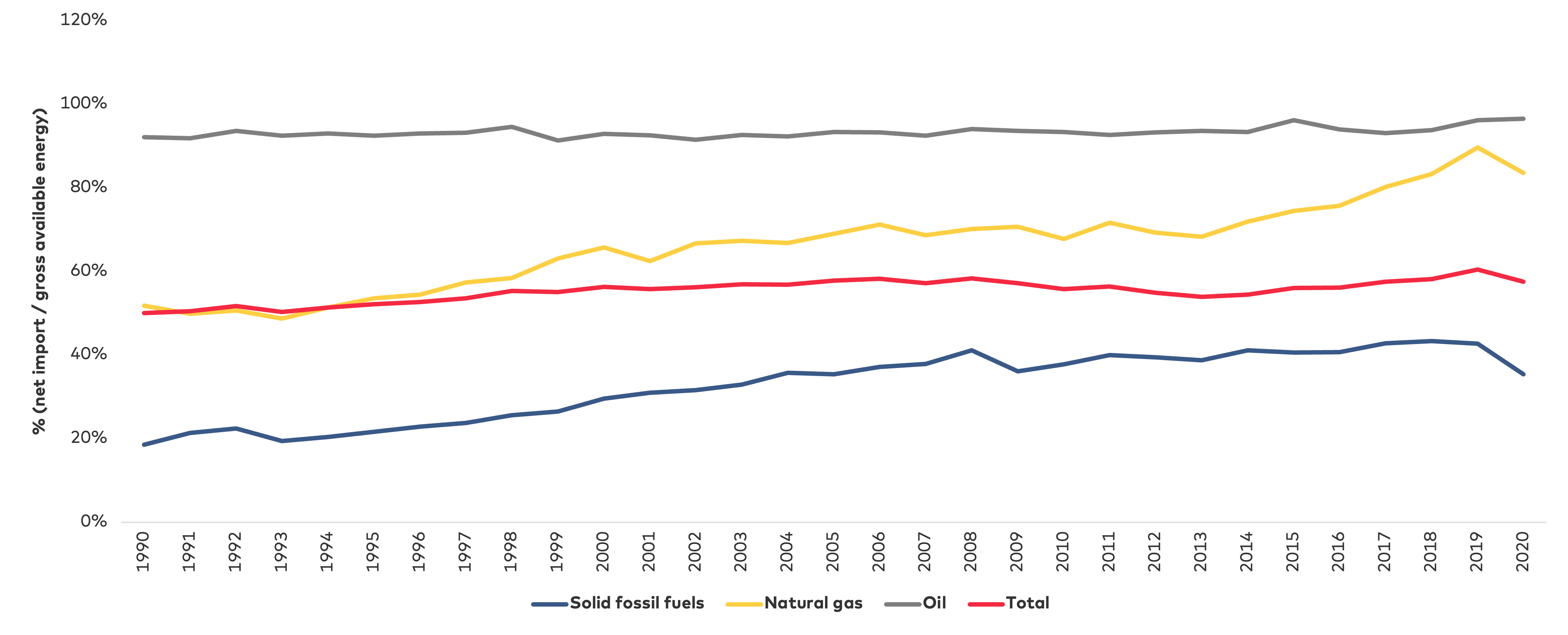

- 5.7 Increasing energy-import dependency

- 5.8 Reductions in natural gas supply

- 5.9 Preparedness of the Nordic countries

- 5.10 Responses to alleviate pressure on household finances

- 6. RISK SCREENING

- 6.1 Long approval processes

- 6.2 Modest public infrastructure acceptance

- 6.3 Inadequate electricity market design

- 6.4 High mineral and energy supply dependencies

- 6.5 Lack of electric grid infrastructure

- 6.6 Absence of sustainable long-term energy storage

- 6.7 Unchanged consumer behaviour

- 6.8 Increased weather dependence

- 6.9 Inadequate energy crisis management

- 6.10 Labour shortages

- 7. MITIGATION MEASURES AND GAP ANALYSES

- 7.1 Accelerated permitting for electricity generation and grid infrastructure

- 7.2 Public inclusion in energy infrastructure

- 7.3 Adapt electricity market design

- 7.4 Strategic sourcing of metals and minerals

- 7.5 Strategic sourcing of fuels

- 7.6 Development of electric grid infrastructure

- 7.7 Energy infrastructure and integration

- 7.8 Information campaigns and digital applications

- 7.9 Energy generation diversification

- 7.10 Energy crisis mechanisms

- 7.11 Tripartite negotiations

- 8. TARGETING NORDIC ADDED VALUE

- 8.1 Policy recommendations

- 9. BIBLIOGRAPHY

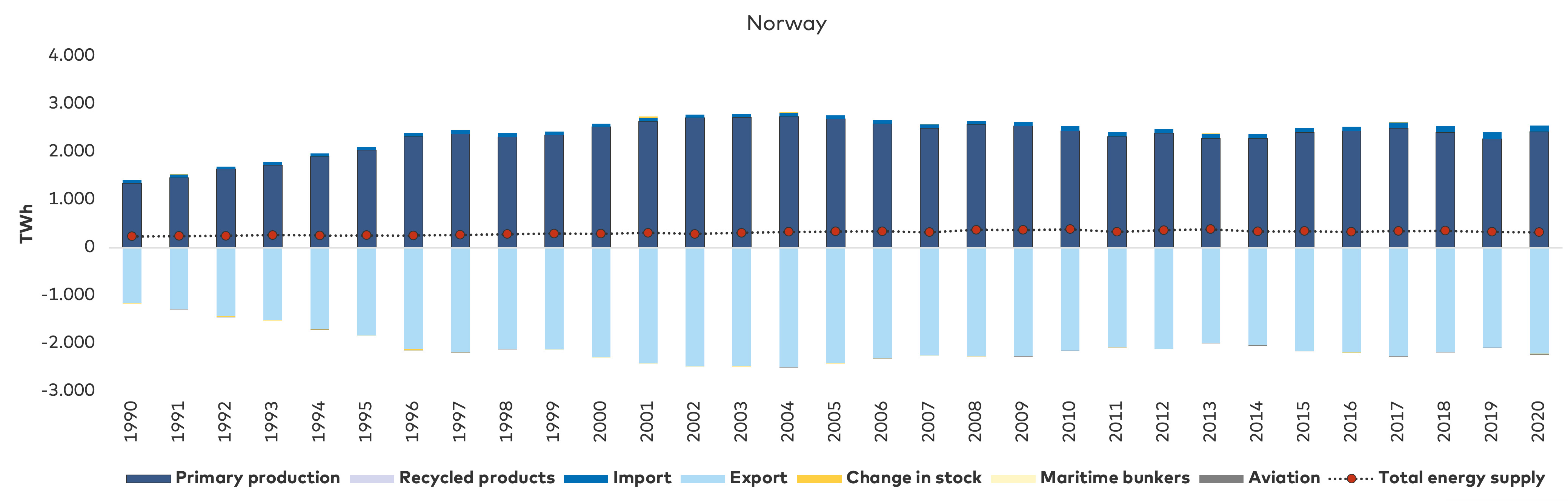

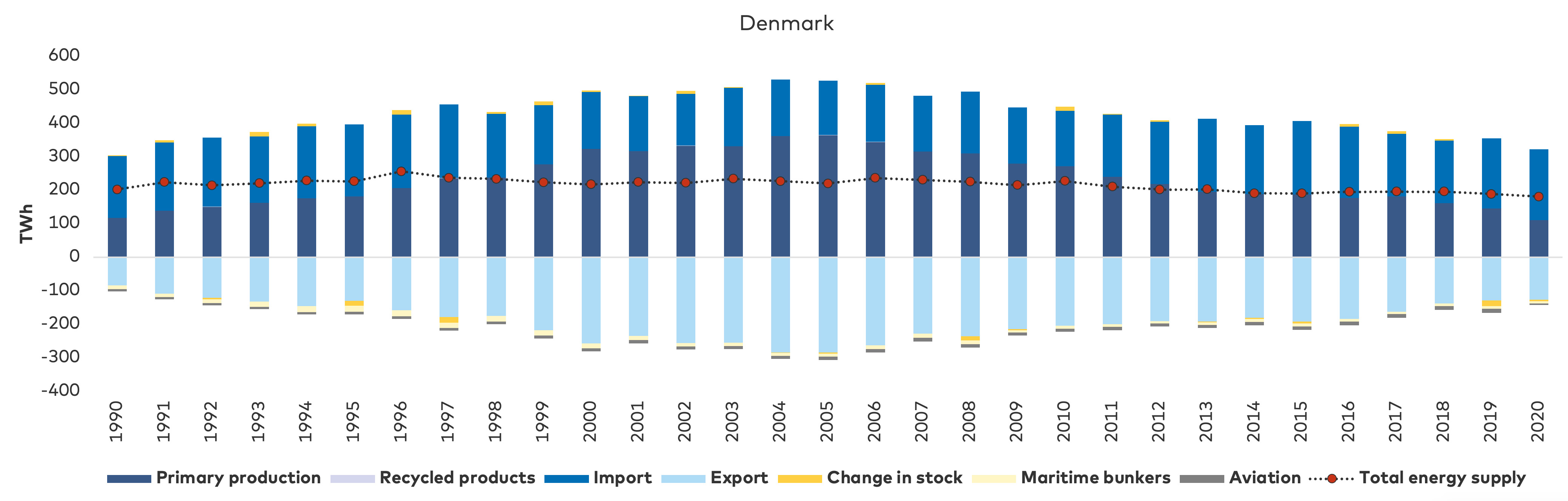

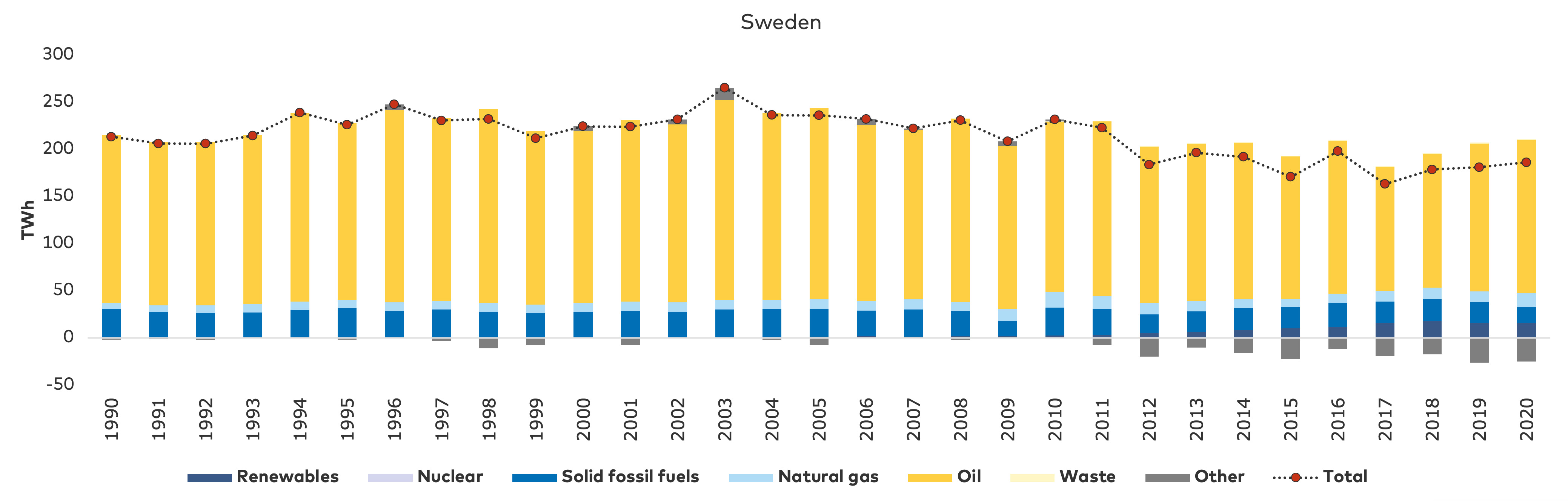

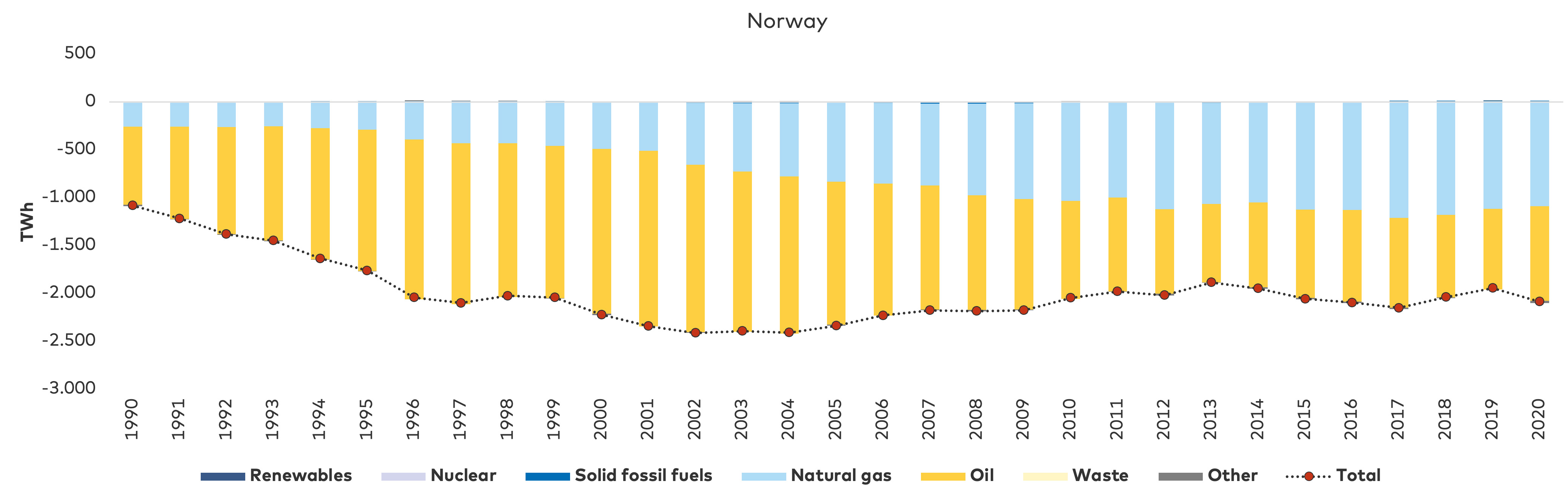

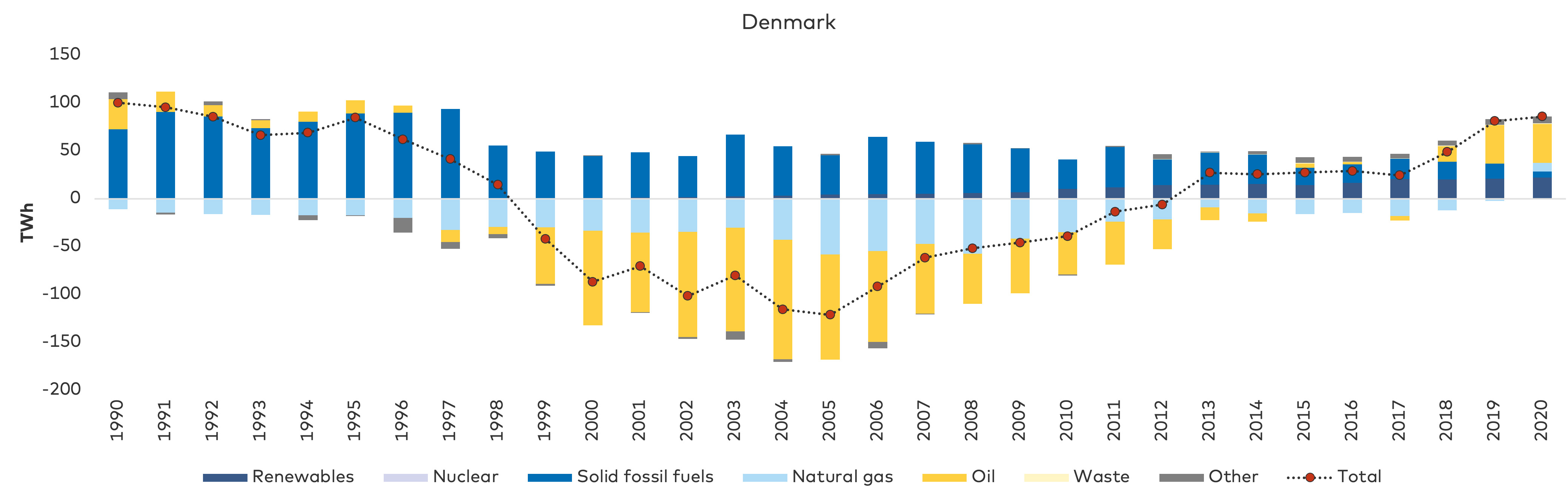

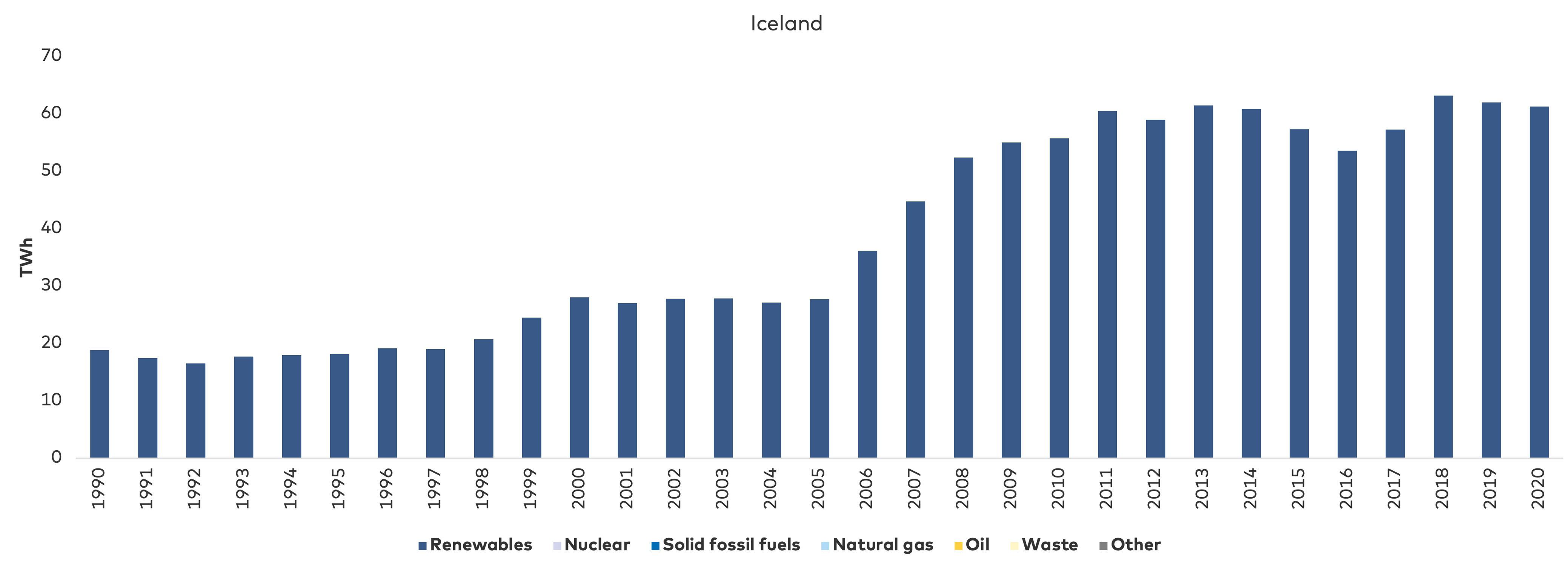

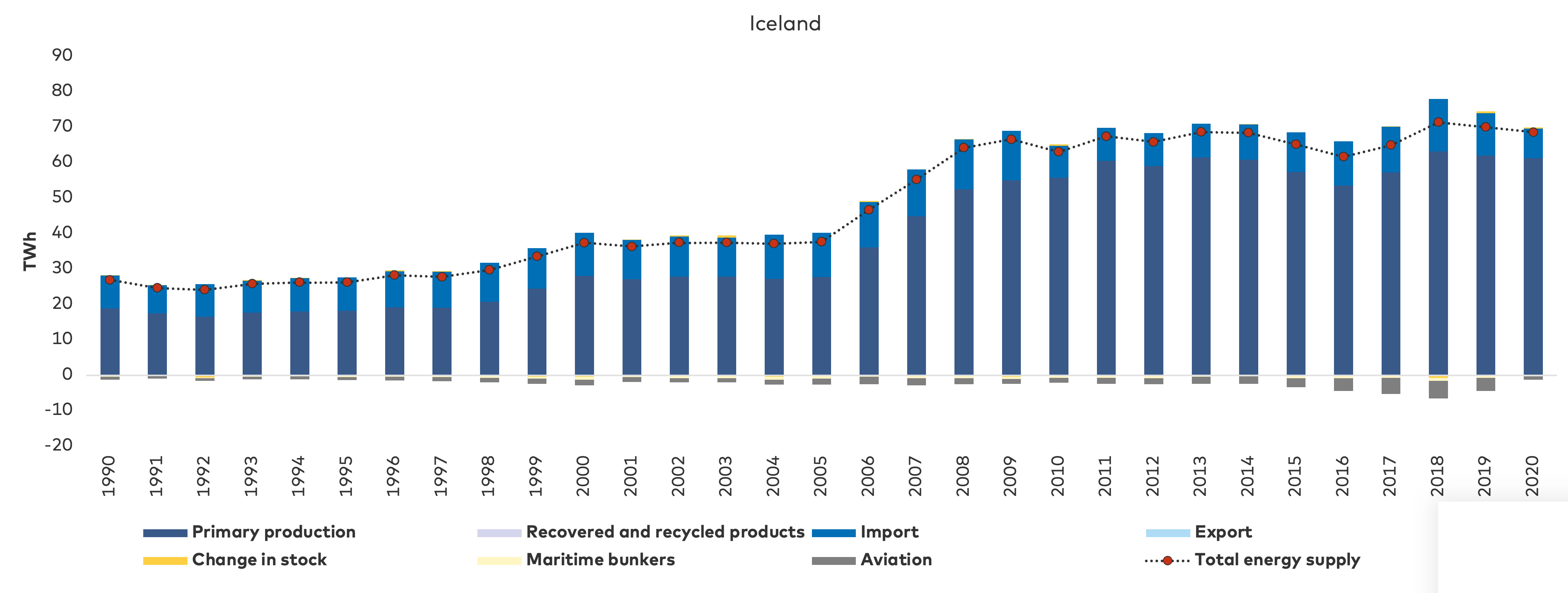

- 10. APPENDIX 1: ENERGY BALANCE PER COUNTRY

- 11. APPENDIX 2: BRIEF DESCRIPTIONS OF NON-HIGH RISK FACTORS

- 12. APPENDIX 3: NATIONAL RESPONSES TO RELIEVE PRESSURE ON HOUSEHOLD FINANCES

- About this publication

MENU

CONTENTS

This publication is also available online in a web-accessible version at https://pub.norden.org/nordicenergyresearch2023-02

FOREWORD

The Nordic region has a vision to become the most sustainable and integrated region in the world. Secure, affordable and clean energy is fundamental to realising this. Yet, in view of unprecedented energy prices and geopolitical risk, it remains unclear whether energy supply chains, power grids, raw materials, or enabling technologies can be secured to meet the demands of an electrified society in the long term.

Today, the Nordic region faces an energy trilemma – three conflicting challenges to delivering a secure, affordable, and sustainable energy transition. We must meet energy demand reliably, withstand system shocks, and prepare for a sharp increase in electrification, all while providing equitable access to abundant energy, and delivering a positive climate and environmental impact.

Recently, a confluence of factors led energy and commodity prices to surge in the Nordics and exposed the need for resilient energy infrastructure. As countries exited COVID-19 lockdown, energy demand exceeded fossil fuel supplies. The Russian invasion of Ukraine exacerbated supply disruptions. Energy annual inflation in Europe rose throughout 2022, pushing overall inflation to record levels. Meanwhile, rising prices of critical raw materials increased the cost of technologies enabling the energy transition.

In response, the European Commission created the Just Energy Transition Fund and a toolbox for action and support aimed at consumers and industry. The Nordic countries offered varying levels of support to households most affected by the high electricity prices. These actions demonstrate that energy security must be viewed in an economic, social, and sustainability context. Energy prices and infrastructure investment have societal consequences, for affordability, public acceptance, economic distribution, job creation, climate and environment.

Energy security is a prerequisite for national security and industry competitiveness, with strategic, political and economic implications for countries and individuals, as well as for Nordic and international cooperation. If the Nordic countries are to meet their ambitious electrification goals, policymakers must consider the vulnerabilities of a decarbonising energy system, and ensure our interlinked systems remain resilient.

This report reviews factors that drove the most severe energy crisis in recent memory, with an emphasis on electricity markets, the preparedness of the Nordic countries, and how they responded. Risks to the Nordic energy transition are identified, and measures in place to mitigate these risks are assessed. Where no such measures exist, actions are proposed to address the gaps. The recommendations herein define national, Nordic, and international actions to increase energy security and emergency preparedness, such that our societies are ready for the energy crises of the future.

Klaus Skytte

CEO, Nordic Energy Research

ACKNOW|LEDGE|MENTS

This publication was funded by the Energy Sector within the Nordic Council of Ministers. The report was prepared by Ramboll Management Consulting and Ramboll Energy (Ramboll). The Nordic Committee of Senior Officials for Energy Policies has overseen the preparation of this publication. Quality assurance has been provided by the Nordic Electricity Market Group. Nordic Energy Research was the contracting authority and coordinator of this work.

Jens Riis at Ramboll was the project manager and had overall responsibility for implementing the study. Ask Tonsgaard Hjordt Brüel is the project owner at Ramboll.

Marton Leander Vølstad at Nordic Energy Research coordinated the project.

Team at Nordic Energy Research

Marton Leander Vølstad

Adviser

Team at Ramboll

Ask Tonsgaard Hjordt Brüel

Global Head of Energy & Utility

Ramboll Management Consulting

Jens Riis

Senior Management Consultant

Strategic Sustainability Consulting, Denmark

Søren Møller Thomsen

Consultant

Ramboll Energy, Denmark

Line Knudsen

Consultant

Social and Economic Impacts, Denmark

Mikael Toll

Senior Advisor

Ramboll Resilience, Sweden

Per Jørgensen

Head of Gas Infrastructure

Ramboll Energy, Denmark

Disclaimer

The opinions expressed in this publication are those of the consultants. They do not necessarily reflect the views of the Nordic Council of Ministers, Nordic Energy Research, or any entities they represent. The individuals and organizations that contributed to this publication are not responsible for any judgements herein.

Christine Lunde Rasmussen

Senior Market Manager

Social and Economic Impacts, Denmark

Erik Vaet

Consultant

Strategic Sustainability Consulting, Norway

Jouni Laukkanen

Country Market Director

Ramboll Energy, Finland

Lauri Larvus

Market Director

Strategic Sustainability Consulting, Finland

André Smith

Country Market Director

Ramboll Energy, Norway

Dag A. Nilsen

Lead Business Developer

Ramboll Energy, Norway

John Ammentorp

Country Market Director

Ramboll Energy, Denmark

Simon Jansson

Country Market Director

Ramboll Energy, Sweden

The Nordic Committee of Senior Officials for Energy Policies

Julie Louring Eriksen

Danish Ministry of Climate, Energy and Utilities

Maria Kekki,

Finnish Ministry of Economic Affairs and Employment

Erla Sigríður Gestsdóttir

Icelandic Ministry of Environment, Energy and Climate

Johan Vetlesen

Norwegian Ministry of Petroleum and Energy

David Freed

Swedish Ministry of Rural Affairs and Infrastructure

Proofreading

The report was proofread by Alistair Gage at Samtext Norway AS.

Contact

Comments and questions are welcome and should be addressed to:

- Marton Leander Vølstad, Nordic Energy Research, e-mail: marton.leander.volstad@nordicenergy.org

- Jens Riis, Rambøll Management Consulting A/S, e-mail: jsrs@ramboll.com

For enquiries regarding the presentation of results or distribution of the report, please contact Nordic Energy Research.

Additional materials, press coverage, presentations etc. can be found at www.nordicenergy.org.

1. EXECUTIVE SUMMARY

The Nordic countries are experiencing an unprecedented energy crisis, characterised by dramatic increases in energy prices caused by a significant reduction in the primary energy supply. High electricity prices for end-consumers is one of the major spill-over effects from continental Europe, along with a reduction in natural gas supplies from Russia. The energy supply crisis has also prompted some regulators to warn of planned outages in winter 2022–2023. Faced with these interrelated problems, both the EU and individual member states, including the Nordic countries, have rolled out a raft of crisis management schemes to help consumers weather the situation financially. Energy cost increases have been felt across the Nordics, although the resulting negative socio-economic impacts such as energy poverty[1][1] The EU Commission defines energy poverty as follows: Energy poverty occurs when energy bills represent a high percentage of consumers’ income, or when they must reduce their household's energy consumption to a degree that negatively impacts their health and well-being. among the poorest income groups, have been felt less in the Nordic countries than in other European economies. In effect, the Nordic economies have shown a degree of socio-economic resilience in the face of the energy crisis.

In addition, recent underlying structural developments (e.g. decommissioning of controllable economic capacity, lack of infrastructure, inflexible demand, energy import dependency) have played a key role in the crisis, as described in the eight drivers of the crisis highlighted later in the report. The problems in energy markets in general, and electricity markets specifically, could impact security of supply in the years ahead.

This report aims to provide recommendations, at national, Nordic, EU, and international level to enable policymakers to ensure that energy systems can strike the desired balance between the elements of the Energy Trilemma of sustainability, affordability and security of supply. Critically, bearing in mind that factors relating to security of supply and electricity markets are the primary focus of the report, the report is structured as follows: identification and analysis of the drivers responsible for the electricity supply crisis, evaluation of individual Nordic countries’ exposure, preparedness and responses to these drivers, identification of the future risks that Nordic electricity systems will be exposed to, and an assessment of whether appropriate and effective risk-mitigation measures are in place. The report is subject to a number of delimitations, including relating to geopolitical threats, and is based on data collected up to 30 September 2022. The report had a submission deadline of the end of November 2022. This was followed by a review process involving Nordic Energy Research and the Nordic Council of Ministers and the report was finalised in January 2023.

Furthermore, although the Nordic energy systems are heterogeneous, the systems’ many shared characteristics mean that the recommendations formulated in this report can be used to inform national decision-making processes across the Nordics, and to strengthen inter-Nordic collaboration. Nonetheless, it should be noted that further analysis, i.e., in the form of detailed impact assessments, is needed to determine how each recommendation can, or should, be implemented in each country. This report makes 17 recommendations, at respectively national, Nordic and EU/International level, as listed below.

Footnotes

- ^ [1] The EU Commission defines energy poverty as follows: Energy poverty occurs when energy bills represent a high percentage of consumers’ income, or when they must reduce their household's energy consumption to a degree that negatively impacts their health and well-being.

Recommendations:

National

- Implement fixed timelines and shorten permitting processes for generation and infrastructure assets while considering the relevant perspectives of local communities.

- Ensure a high-quality labour supply for the energy sector by developing long-term national roadmaps, including to determine whether and how the sector should be prioritised.

- Apply goal-oriented impact assessments as a basis for decision-making, addressing short- and long-term system-wide perspectives. The goals and assessments should balance all aspects of the Energy Trilemma and consider the benefits that a reliable energy supply can create for other sectors of society. In this context, the number of scenarios in national energy planning should be increased to encompass multiple energy system changes.

- Increase system capacity and flexibility through existing energy assets that are currently not fully utilised, e.g., by prolonging lifetimes or other means, in order to maintain affordable prices and security of supply. This should not overly delay the green energy transition.

- Reinforce electricity crisis management so that it is properly dimensioned and well-planned at local, national and Nordic level. It should be borne in mind that since electricity is both a traded commodity and a basic societal need, adopting a cautious approach during crisis situations remains pivotal. This is because both inaction and suboptimal policy decisions could result in market disruptions and risk creating future, even more acute crises.

- Strengthen the energy industry’s long-term attractiveness and competitiveness within important sectors such as energy asset manufacturing, electricity generation, heat production, extraction of critical raw materials, energy service companies and grid infrastructure.

Nordics

- Diversify sources of energy generation, carriers, and storage in line with national climate targets, including hydrogen and biofuel infrastructure. Leverage the respective strengths of different technologies and energy carriers and opportunities to develop local energy systems while limiting excessive dependence on any single technology, facility or supply route.

- Review ways of continuously adapting the electricity market model to meet society’s needs and desires to deliver a green and just energy transition, while maintaining a high security of supply. Based on developments in 2022, markets have not been able to balance the various elements of the Energy Trilemma. In this context, adequate roles, responsibilities for market actors, governments and the number of market interconnections should be considered.

- Formulate shared plans and set requirements for yearly and multi-year long-term energy storage to replace fossil-fuel storage. This could involve different energy carriers, e.g., hydrogen, methanol, ammonia, pumped hydro storage and biogas.

- Strengthen and share the knowledge foundation for addressing public opposition to energy infrastructure, e.g., through various forms of financial compensation and enhanced stakeholder dialogue in project design and development.

- Support a flexible demand-side response by utilising existing knowledge and developing new technologies and infrastructure to facilitate energy efficiency, system flexibility and ancillary services.

- Strengthen Nordic electricity grid infrastructure to avoid bottlenecks and renewable energy curtailment in connection with the increased electrification of society.

- Re-emphasise the importance of Nordic collaboration across energy markets and systems while highlighting each country’s responsibility for positively contributing to regional, national and Nordic security of supply.

- Share findings from nationally applied financial support schemes to help consumers weather the current crisis and thereby safeguard future policymaking against undesired distributional effects relating to both energy poverty and long-term market developments.

- Limit import dependency on the metals and minerals required for the green energy transition by promoting sustainable mining in the Nordics. Consider making the region a global leader in mining on the back of high environmental and ethical standards.

EU and international

- Coordinate policy responses between Nordic countries around EU initiatives, thus making them increasingly applicable to the specific nature of the Nordic markets.

- Assess the need for setting up a comprehensive stockholding system for various types of fuels and energy carriers to improve security of supply through EU-wide regulations. This should be achieved by leveraging existing knowledge, including in relation to oil and international processes, in order to alleviate the current situation and prevent similar scenarios arising in the future.

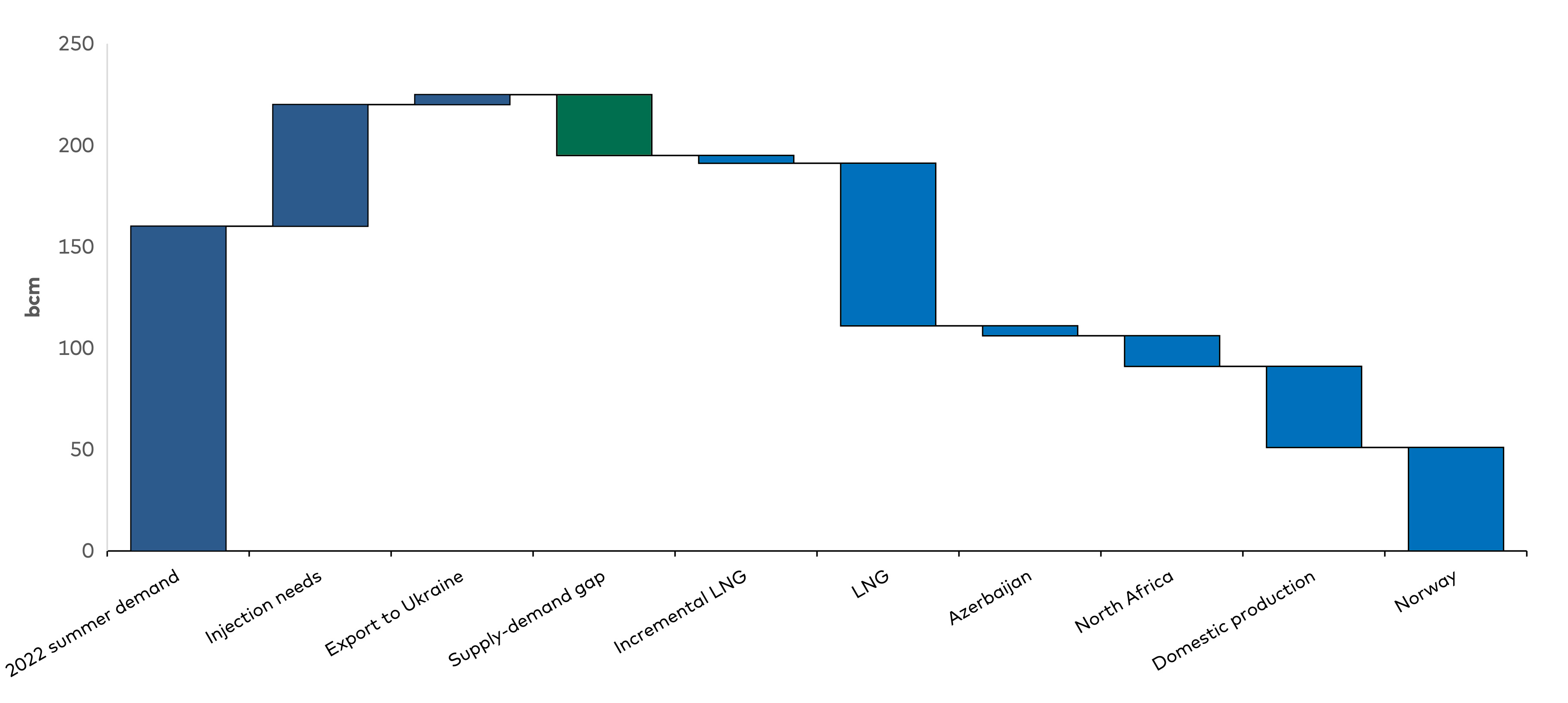

| A perfect storm – eight drivers impacting the Nordic energy crisis | |

| The crisis is complex and not caused by a single event or scenario. The study has identified eight drivers that collectively have played a key role in triggering the current electricity crisis, and jointly created a perfect storm of compounding problems. These eight drivers would therefore have been likely to impact the electricity system and led to long-term security of supply challenges, even if Russia had not reduced its supply of natural gas to Europe. The drivers are listed and described below, though the extent to which each driver has impacted the current situation is not quantified. | |

| Electricity market structure The structure of the electricity markets in the Nordic countries and Europe has produced a set of derivative effects that were not foreseen at their inception, for example in relation to the decommissioning of thermal capacity. Thus, some of the subsequent drivers of the crisis are a direct result of the electricity market structure. |

| Decommissioned controllable electric capacity The decommissioning of thermal power plants due to price competition, and nuclear power plants due to political opposition, have resulted in a lack of baseload capacity in the electricity system during periods of unfavourable weather conditions. |

| Balancing electricity supply and demand Decarbonisation targets and the resulting focus on the development of renewable energy have heightened the requirements for balancing supply and demand in the electricity system. Going forward, electricity prices are expected to be increasingly volatile, necessitating long-term energy storage. |

| Lack of electric transmission infrastructure Underinvestment in both electrical grid infrastructure capable of handling intermittent flows of energy and in cross-border interconnectors has created bottlenecks in Sweden and Norway, which in turn have led to asymmetric pricing trends in the Nordics. |

| Inflexible electricity demand Nordic electricity systems have historically been characterised by a high security of supply at low electricity prices and electricity is perceived as a public good throughout the region. Furthermore, the fact that demand in wholesale electricity markets is inflexible means that prices can dramatically increase, since decreases in consumer consumption are not enough to reduce demand and stabilise electricity prices. This has led to significant cost increases for consumers. |

| Increasing energy-import dependency Reduced exports of Russian oil, gas and coal have had a major impact on electricity prices in Europe. Energy supply disruptions are not unlikely for the winters of 2022–2023 and 2023–2024. While the Nordic countries are well prepared, connections to Europe make the region as a whole vulnerable. |

| Reduced supply of natural gas Reduced extraction of natural gas within the European Union, in combination with a gradual reduction in the foreign supply of natural gas, has created high sourcing prices for LNG and natural gas. Increasing production costs and costs of buying natural gas and electricity for end-consumers are some of the consequences of this development. |

| Weather-dependent electricity generation The Nordic countries are exposed to a weather-dependent electricity supply as baseload generation via hydro power and peak capacity are contingent on weather conditions. Other energy sources that will increasingly be utilised going forward such as wind and solar are naturally also dependent on weather conditions. |

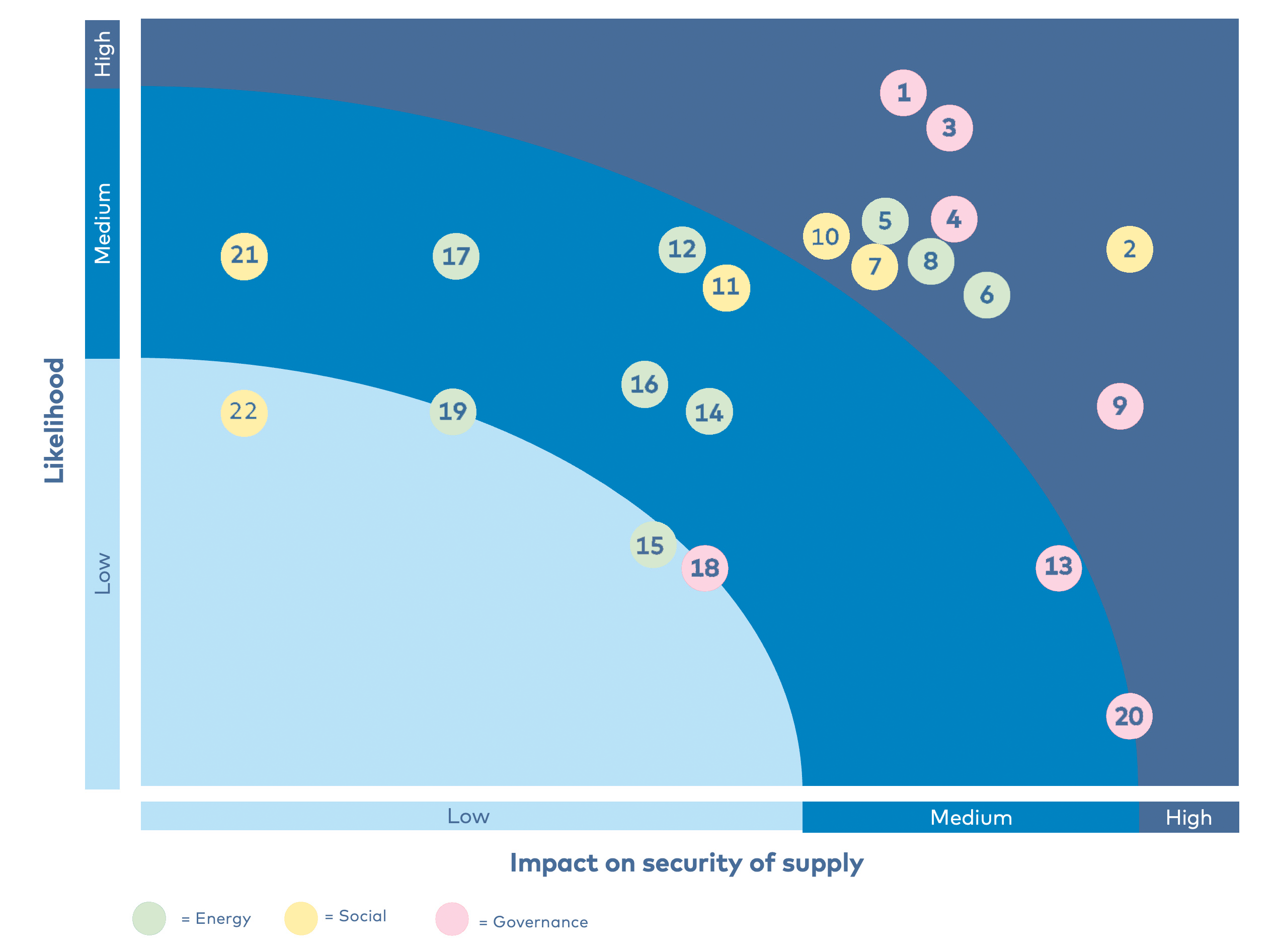

Risks influencing the Nordic security of electricity supply

The risk screening identified 22 risks which were ranked based on their likelihood and their impact on security of supply. This resulted in the identification of ten high-risk factors (shown below in

| RISK | POTENTIAL IMPACT ON THE VALUE CHAIN |

| Long approval processes | Long approval processes can hinder society’s ability to build enough renewable capacity and electric grid infrastructure at a quick enough pace to transmit electricity from the generation site to load centres to meet customer demand. Given the significant requirements for electrification associated with the green energy transition and the desire for energy independence, continued long approval processes could reduce the ability of the Nordic societies to meet these challenges. |

| Modest public infrastructure acceptance | This risk may impact the whole electricity value chain depending on the extent of public opposition to the installation of the infrastructure. Moreover, the problem is likely to increase over time as renewable electricity generation and additional electric grid infrastructure become more visible in the landscape. Renewable energy sources require more land per energy produced than traditional types of energy generation. |

| Inadequate electricity market design | There is a risk that the current electricity market is not designed to facilitate a smooth green energy transition while balancing the two other dimensions of the Energy Trilemma. Potential intervention from regulators has created insecurities in the market and affected market operations. For example, reduced controllable electricity generation capacity in the market could lead to load-shedding and price increases for consumers. Therefore, the existing market design should be developed to facilitate a suitable balance between the various dimensions of the Energy Trilemma. |

| High mineral and fossil energy supply dependencies | Supply dependencies could impact the ability of society to deliver the green energy transition at a sufficient pace, while creating security of supply issues around fossil fuels and minerals in the event of supply disruptions. This could impact consumers through high prices and the availability of electricity. |

| Lack of electric grid infrastructure | Appropriate and adequate electrical grid infrastructure is the foundation of a well-functioning energy system and electricity market. Transmission problems caused by lack of electrical infrastructure could therefore negatively impact the system’s entire value chain. |

| Lack of sustainable long-term energy storage | The potential lack of sustainable long-term energy storage as a means for supplying peak electricity demand during periods of unfavourable weather conditions could negatively impact overall security of supply and the resulting prices consumers pay. |

| Unchanged consumer behaviour | The inability of consumers to exercise demand-side response during peak hours, and change their behaviour impacts overall security of supply. |

| Increased weather dependence | A significant scarcity of generation capacity, i.e. as the result of limited availability of different energy sources (hydro and renewables), could impact the ability of society to meet electricity demand. |

| Insufficient energy crisis management | Energy-crisis management that does not consider the system-wide effects of initiatives at Nordic and EU levels could impact the entire electricity value chain. |

| Labour shortages | Any labour shortages in the energy sector have consequences throughout the value chain since assets cannot be developed and maintained. This makes labour shortages a system-wide risk. |

Mitigation measures and gap analysis on responses to the crisis

Following the risk screening, selected mitigation measures applied during the ongoing energy crisis were mapped against the identified high-risk factors. The main purpose was to identify whether the applied mitigation measures were an adequate and efficient response to the identified risks, or whether a risk-mitigation gap existed. The results of the gap analysis established that significant gaps are associated with one risk (“gap exists”), that gaps are partially addressed (“gap remains”) for eight risks and that gaps are fully addressed for one risk (“no gap”). The findings are based on a qualitative assessment of the data foundation for this report and have been subject to the report’s validation process (see Section 3.9.1).

The mitigation measures presented in Table 2 below demonstrate that the mitigation measures and cases discussed may not be the most appropriate options to implement in all the Nordic countries. They are merely examples of the applied mitigation measures, presented with the aim of assessing how well the Nordic electricity market is equipped to ensure supply security going forward.

| RISK | MEASURE | |

| Long approval processes | Accelerated permitting for electricity generation and grid infrastructure | GAP REMAINS |

| Modest public infrastructure acceptance | Public inclusion in electricity infrastructure | GAP REMAINS |

| Inadequate electricity market design | Analyse adaptation measures for electricity market design | GAP REMAINS |

| High mineral and fossil energy supply dependencies | Strategic sourcing of metals | GAP EXISTS |

| High mineral and fossil energy supply dependencies* | Strategic sourcing of fuels | GAP REMAINS |

| Lack of electric grid infrastructure | Electric grid infrastructure | GAP REMAINS |

| Lack of sustainable long-term energy storage | Energy infrastructure integration | GAP REMAINS |

| Unchanged consumer behaviour | Information campaigns and digital applications | NO GAP |

| Increased weather dependence | Electricity generation diversification | GAP REMAINS |

| Inadequate energy crisis management | Energy crisis management | GAP REMAINS |

| Low workforce availability | Tripartite negotiations | GAP EXISTS |

| *Separate mitigating measures are applied for the “high mineral and fossil energy supply dependencies”. The risk is addressed collectively as it relates to both dependencies. | ||

2. INTRODUCTION

Secure access to abundant and affordable energy is critical for societies and a cornerstone of well-functioning economies. The Nordic governments' participation in the Paris Agreement’s goal of limiting the global temperature increase to well below 2oC compared with pre-industrial levels has created a desire to accelerate the pace of the green energy transition. Governments are consequently being challenged to balance the three dimensions of the Energy Trilemma of security, affordability and sustainability, which, while often conflicting, do offer some synergies.

The current energy crisis in the Nordic region is the result of the decisions society has made regarding how energy systems are designed and has essentially been underway for some time. The crisis originated in the summer of 2021 following the European Union’s rapid economic recovery after the COVID-19 lockdowns, and the war in Ukraine has resulted in substantial energy price rises across Europe and the Nordic countries. (Prices in Iceland have remained stable.) Low water levels in Norwegian reservoirs, warm weather in Europe during the summer of 2022, reduced availability of French nuclear power, and a weakened energy infrastructure are other factors that have contributed to the crisis.

The energy crisis has raised concerns about the ability of Nordic societies to maintain secure access to abundant and affordable energy. This makes securing an appropriate balance within the Energy Trilemma a key priority for policymakers going forward.

This report aims to provide recommendations to enable policymakers to achieve the desired balance in the Energy Trilemma and to provide a basis for an affordable, secure energy transition. We have adopted the following approach to achieve this: (1) analyse the drivers of the crisis, (2) evaluate the Nordic countries’ exposure to the crisis, preparedness and responses to these drivers, (3) identify the future risks the Nordic electricity systems are exposed to and (4) determine whether appropriate and effective mitigation measures are in place to manage the identified risks. Based on this assessment, this report presents several national, regional and international policy recommendations. In light of current crisis, this report has been tasked with providing recommendations with an emphasis on how to achieve energy security, with affordability and sustainability as important second priorities.

3. METHODOLOGY

3.1 The Energy Trilemma

- Security is the ability to supply current and future energy demand reliably and withstand and recover from system shocks through effective crisis management.

- Affordability is the ability to provide universal access to reliable, affordable and abundant energy for residential and industrial consumers. This dimension also encompasses job creation in relation to expanding renewable energy and transmission infrastructure. Finally, it covers public acceptance of the implemented mitigation initiatives in general.

- Sustainability is the extent to which the green energy transition mitigates potential climate impacts by transitioning from fossil-based to renewable energy systems. This dimension focuses on the effectiveness of the decarbonisation process and the efficiency of energy generation, transmission and distribution.

Footnotes

- ^ World Energy Council, World Energy Trilemma Index, 2022. Website reference: https://www.worldenergy.org/transition-toolkit/world-energy-trilemma-index.

3.2 The energy crisis and security of supply

3.3 The energy value chain

3.4 Scope of the study

Electricity and gas markets

Affordability

Sustainability

3.5 Delimitations

- Cybersecurity: Applying novel digital solutions is a key element of many aspects relating to security of supply, for example, demand-side management and automated grid balancing. However, increasing digitalisation of critical electricity infrastructure presents a significant risk of cyberattacks that could potentially jeopardise electricity supply security.

- Geopolitics: An increasingly changed world order with energy as a central element of geopolitics could potentially affect the perceived credibility of various national trading partners. Moreover, geopolitical movements could also make electricity infrastructure vulnerable to sabotage or similar, potentially requiring increased operational security from asset owners.

- Inflation: Inflation effects from initiatives to address affordability concerns among Nordic households and corporates are not considered, although potentially relevant as these could further contribute to economy-wide inflation, and hence the ability to pay for electricity-related goods.

3.6 Data collection

Period for data collection

Focus on the Energy Trilemma

3.7 Description of data sources

3.8 Interviews

| NO. | ORGANISATION | COUNTRY FOCUS | ENERGY TRILEMMA FOCUS | VALUE CHAIN FOCUS |

| 1 | Ramboll Energy | Nordics general | The full Energy Trilemma | Full value chain |

| 2 | Svenska Kraftnät | Sweden | Security & Sustainability | Transmission |

| 3 | Energinet | Denmark | Security & Sustainability | Transmission |

| 4 | Ramboll Resilience | Nordics general | Security & Sustainability | Full value chain |

| 5 | Fingrid | Finland | Security & Sustainability | Transmission |

| 6 | Energia | Finland | Security & Sustainability | Full value chain |

| 7 | The National Energy Authority of Iceland | Iceland | Security & Sustainability | Consumers |

| 8 | Statnett | Norway | Security & Sustainability | Transmission |

| 9 | The Danish Utility Regulator | Denmark | Security | Generation; Consumption |

| 10 | The Nordic Council of Ministers | Nordics general | Affordability | Consumption |

| 11 | Mandag Morgen | Denmark | Affordability | Consumption |

| 12 | The Danish Energy Agency | Denmark | Security & Sustainability | Generation; Transmission |

| 13 | The Finnish Energy Authority | Finland | Security & Sustainability | Generation; Consumption |

| 14 | Samfunnsbedriftene | Norway | Affordability | Consumption |

| 15 | Concito | Nordics general | Affordability | Consumption |

| 16 | The Finnish Trade Unions | Finland | The full Energy Trilemma | Consumption |

| 17 | Landsnet | Iceland | Security & Sustainability | Full value chain |

| 18 | The Norwegian Energy Regulation Authority | Norway | Security | Generation; Transmission |

| 19 | Landsvirkjun | Iceland | Security & Sustainability | Generation; Transmission |

| 20 | Ørsted | Nordics general | Security & Sustainability | Full value chain |

| 21 | CPH Infrastructure Partners | Nordics general | Security & Sustainability | Generation; Transmission |

| 22 | Siemens Energy | Nordics general | Security & Sustainability | Transmission |

| 23 | DTU Wind And Energy Systems | Nordics general | Security & Sustainability | Full value chain |

| 24 | The Danish Trade Union Confederation | Denmark | Affordability | Consumers |

| 25 | The Swedish Energy Agency | Sweden | Affordability | Consumers |

3.9 Assessment of the data used

Consequently, this report relies on data with a ‘documented effect’ to map drivers and a ‘seeming effect’ for risks, mitigation initiatives and recommendations (see Figure 5). Specifically, data analysed from one source, has been compared with conclusions from other sources, ensuring the validity of the arguments despite the relative lack of proven effects of the data.

With this data foundation, the report mixes top-down and bottom-up analysis approaches. While reports considered from international institutions and regulatory interventions from the EU and at national level apply a top-down approach, insights from relevant stakeholders are considered through interviews that leverage bottom-up approaches.

3.9.1 Validation

3.10 Report structure

3.10.1 The European and Nordic energy systems

3.10.2 Mapping of drivers

3.10.3 Identifying and assessing key risks

As discussed previously, this report does not consider the changing geopolitical environment, which could potentially give rise to sabotage and cybersecurity concerns. These risk categories could potentially have disastrous consequences for security of supply and should be analysed in a separate report. The list developed for this report consisted of approximately 25 risks spanning the short, medium and long term. Each of the risks is plotted in a risk matrix, enabling the identification of high-risk factors, for which we will subsequently suggest several mitigation measures. The applied risk matrix is shown below in

3.10.4 Mapping mitigation measuremitigation measures and gap analyseis

3.10.5 Policy recommendations

4. INTERNATIONAL ENERGY SYSTEMS AND MARKETS

This section provides an overview of the European electricity and natural gas systems. We assess Iceland separately due to the fact that it is not experiencing the electricity crisis to the same extent as the rest of Europe. We present the existing systems rather than future scenarios, as the current electricity crisis is impacting the existing systems. Another important reason to focus on the European electricity and natural gas systems is that the underlying drivers causing the electricity crisis discussed in the subsequent chapter are propagated across European borders. Therefore what happens in Europe affects the Nordic countries.

Local energy systems such as district heating and cooling networks are not described, since these have not negatively impacted the current electricity crisis. District heating networks are significantly more expensive for long-distance energy transmission than gas and electricity, which is why the district heating zones are divided into geographically isolated areas. High heating prices in one area do not spread to adjoining areas as in the case of electricity and gas. While district heating and cooling systems could be part of a future solution to balance the Energy Trilemma, they have not negatively impacted the current electricity crisis.

Although we examine the Nordic countries as one, there are several differences between the individual countries’ energy supply systems worth highlighting:

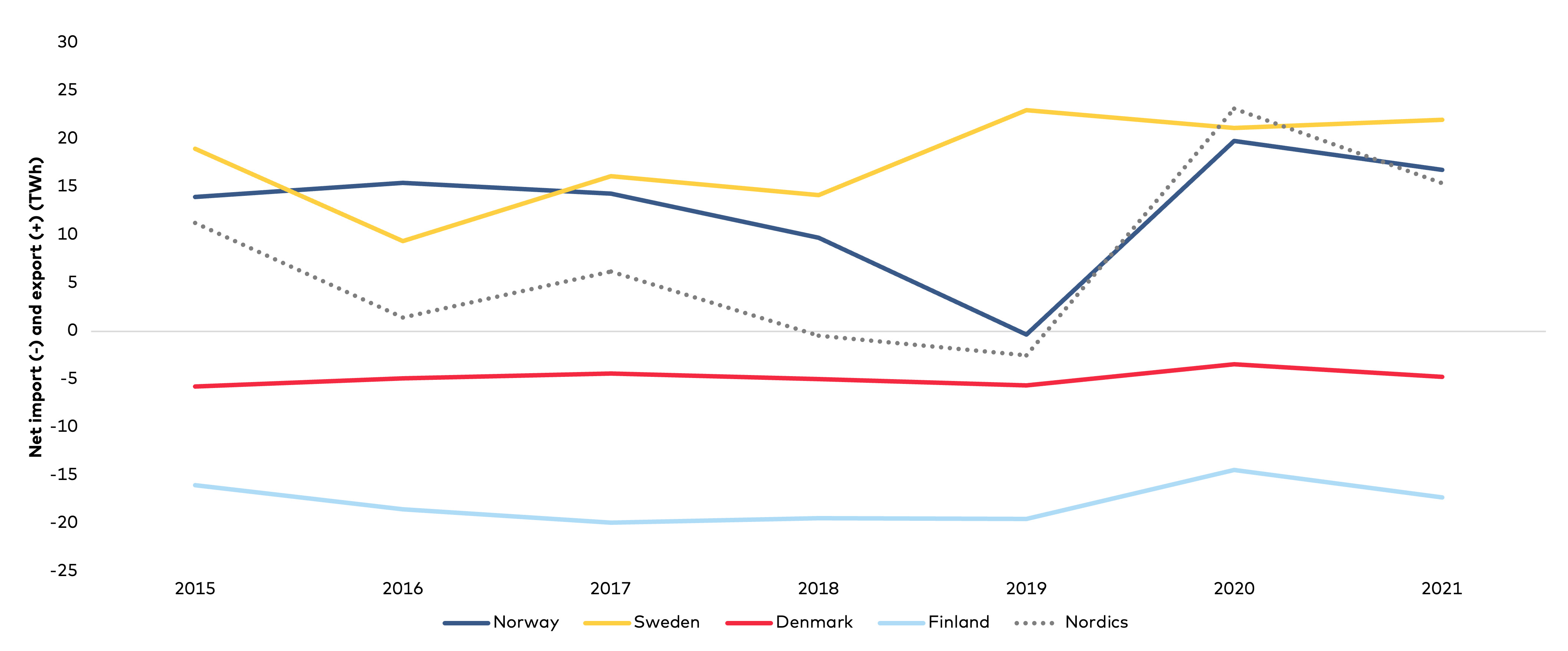

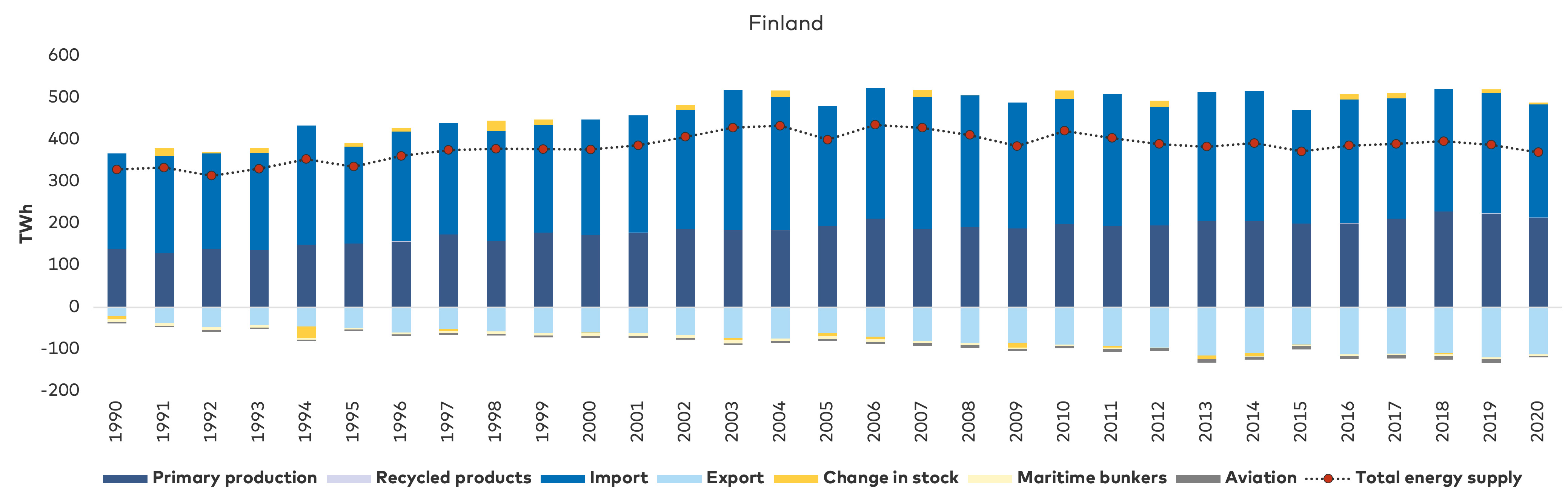

| Finland has historically relied on imports of energy. The primary energy production has been nuclear and renewables (mainly hydro and solid biomass). Importing oil from Russia for further refinement and exporting to the world market, with Sweden as the main customer, has been a profitable industry. Electricity is mainly imported from Sweden and Russia. |

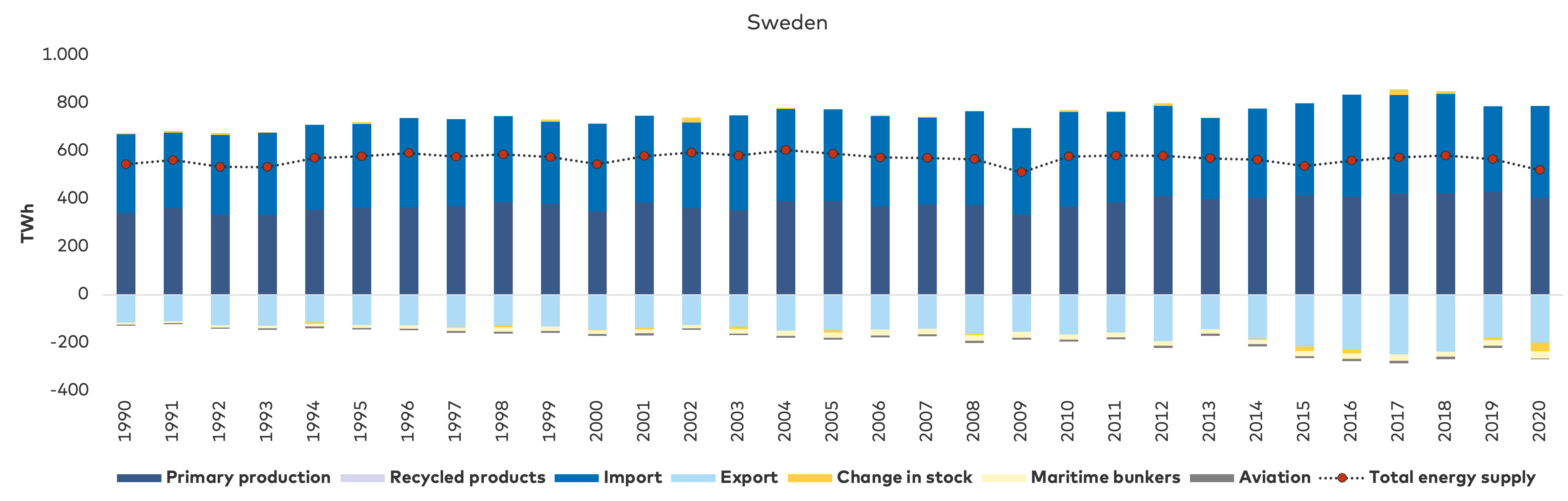

| Sweden has historically relied on imports of energy. The primary energy production has been nuclear and renewables (mainly hydro and solid biomass). In most years Sweden is a net exporter of electricity but a net importer of oil and natural gas. |

| Norway’s large hydrocarbon production capacity makes it a net exporter of energy. The main export product from oil and gas production has changed from oil to natural gas. In most years, Norway is also a net exporter of electricity from its hydropower plants – albeit at a comparatively much lower level than oil and natural gas. |

| Denmark has oscillated between being a net importer and exporter of energy depending on its oil and gas production in the North Sea. The main energy import has generally been coal for the large central power plants and oil for onward export. In recent years, electricity has also been net imported from neighbouring countries. |

| Iceland is in a unique situation compared to the other Nordic countries as it is nearly self-sufficient in energy, and its energy prices have remained stable. The competitive situation is also different as Landsvirkjun (the national energy company) is the majority shareholder in the TSO. Moreover, there is a lack of transparency in the market regarding pricing. Lack of rainfall has created supply issues for a few energy-intensive industries. |

In the following section we present the European electricity and natural gas system. The European electricity system is interconnected, and electricity is shared across borders. We also present the electricity market structure. Finally, we present an overview of the European natural gas system and the market. In

4.1 The electricity system

Due to the heightened focus on decarbonisation, the current electricity system is expected to change in the years to come. For example, new interconnectors will be built to ensure high supply security when domestic power plant capacity is reduced, and to develop a common European electricity market. Furthermore, a number of central power plants have been decommissioned, mothballed or converted to biomass with reduced capacity. Biomass-based power plants are expected to be gradually replaced by wind turbines and solar cells. The development of uncontrollable renewables like wind and solar will create a need for intermediate energy storage or alternative backup production. Controllable power generation (reservoir hydro, thermal power plants, nuclear) does not present the same problems.

Thermal power plants in Europe

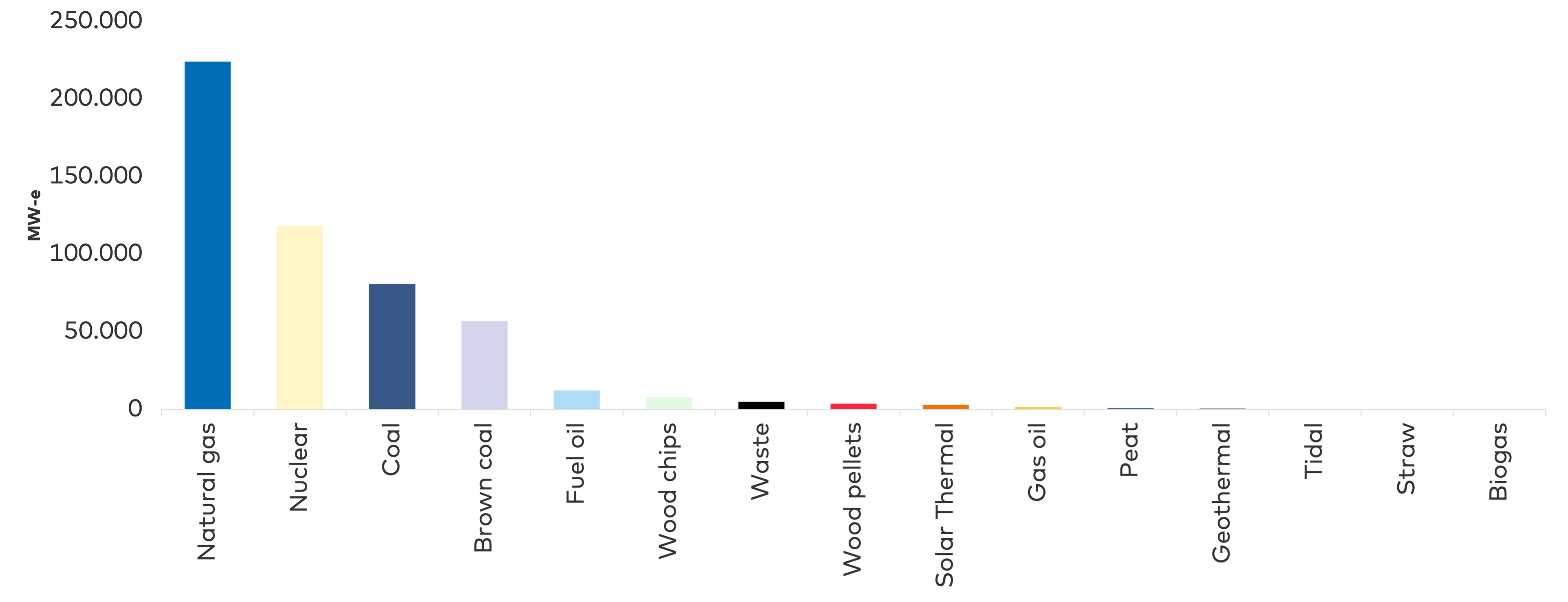

Historically, the European electricity system has largely relied on electricity production from power plants. With the exception of hydropower, the electricity produced has come from nuclear and fossil-fuelled power plants. With increasing renewable energy production, the requirement for power plants will switch from energy production to system-bearing properties. Today 73% of power plant capacity in Europe is based on fossil fuels, and 23% on nuclear. The remaining 4% is based on other energy sources.

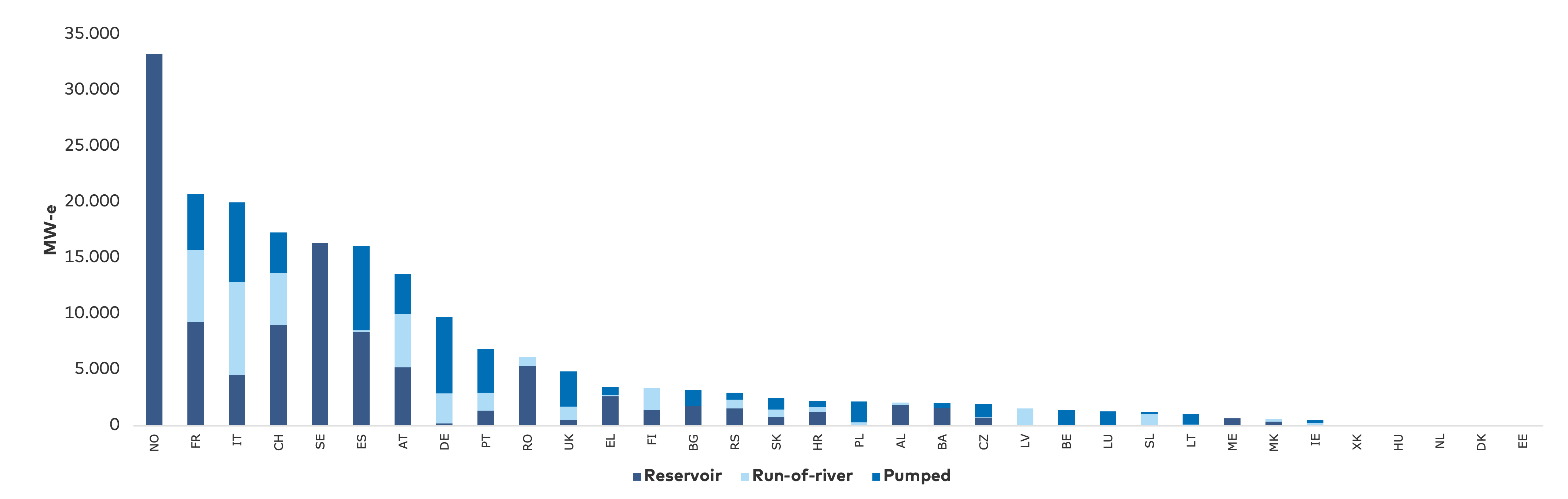

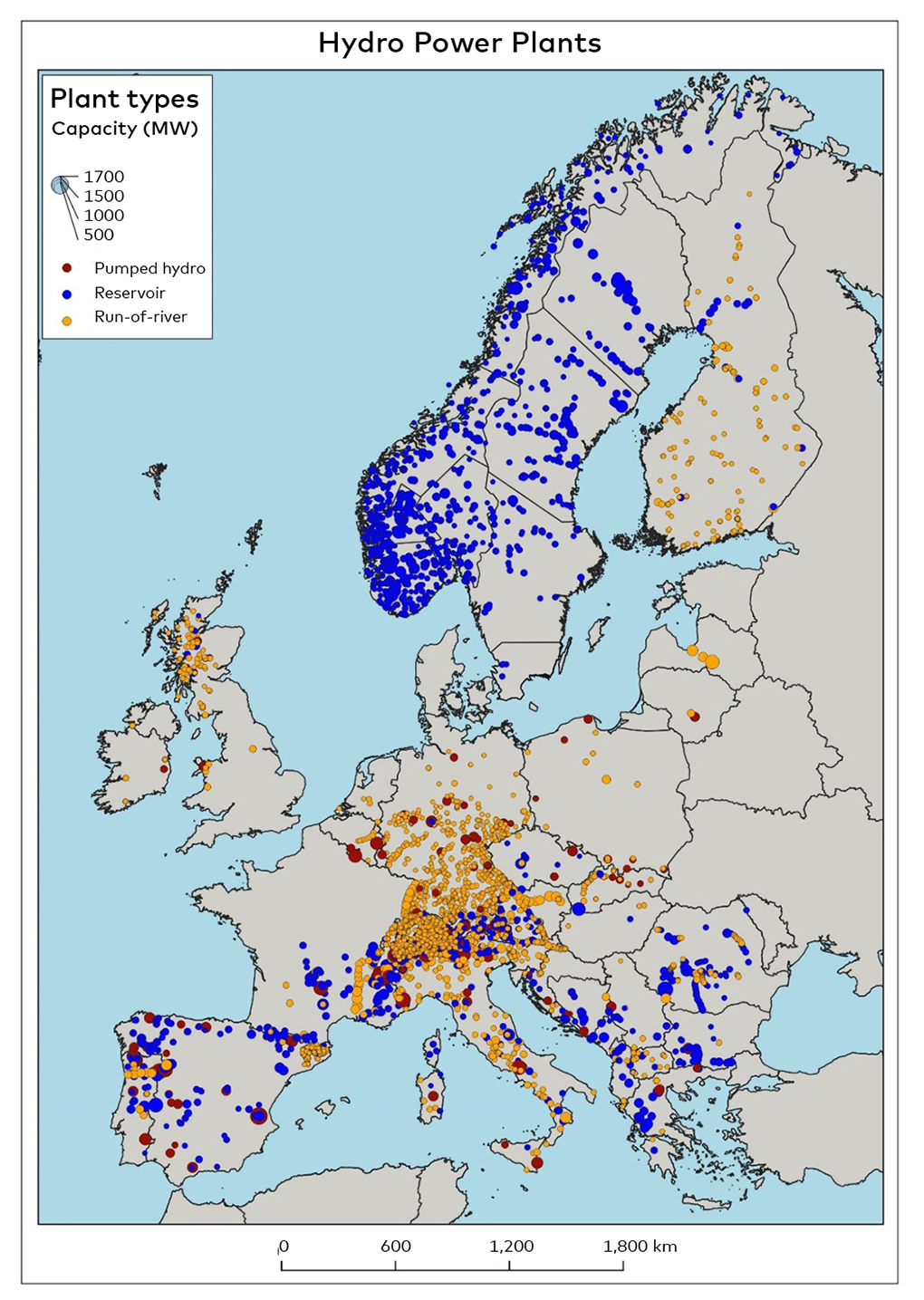

4.1.1 Hydropower plants in Europe

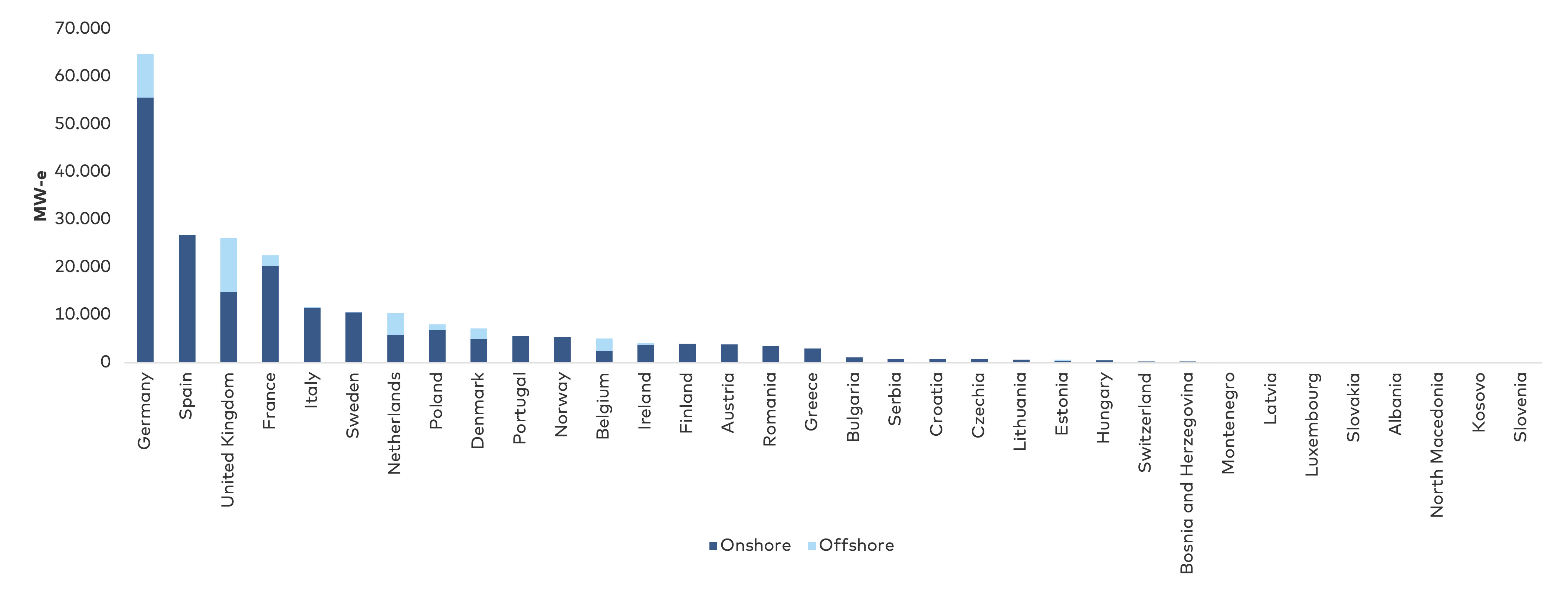

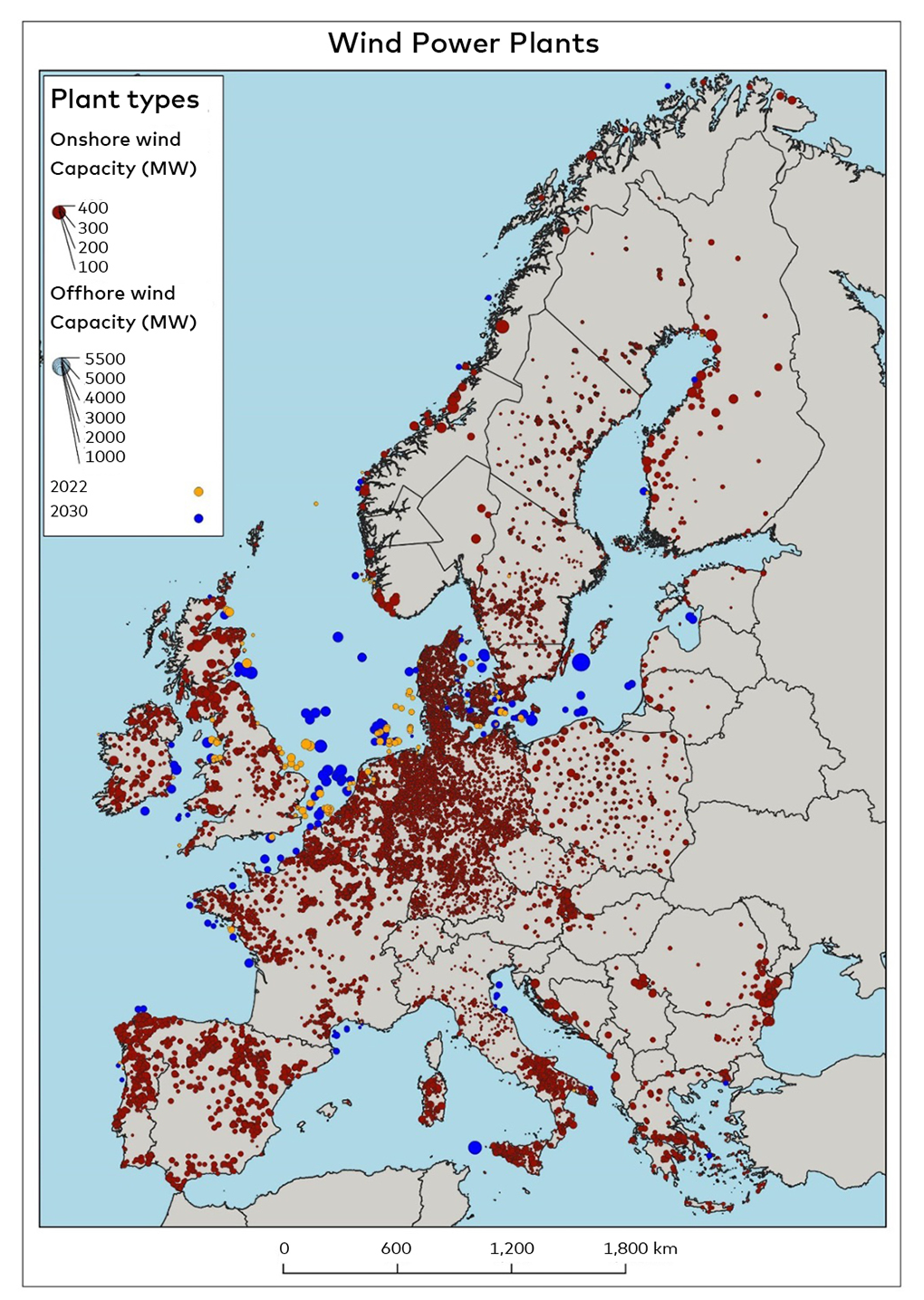

4.1.2 Renewable energy in Europe

4.1.3 Interconnectors and electric transmission in Europe

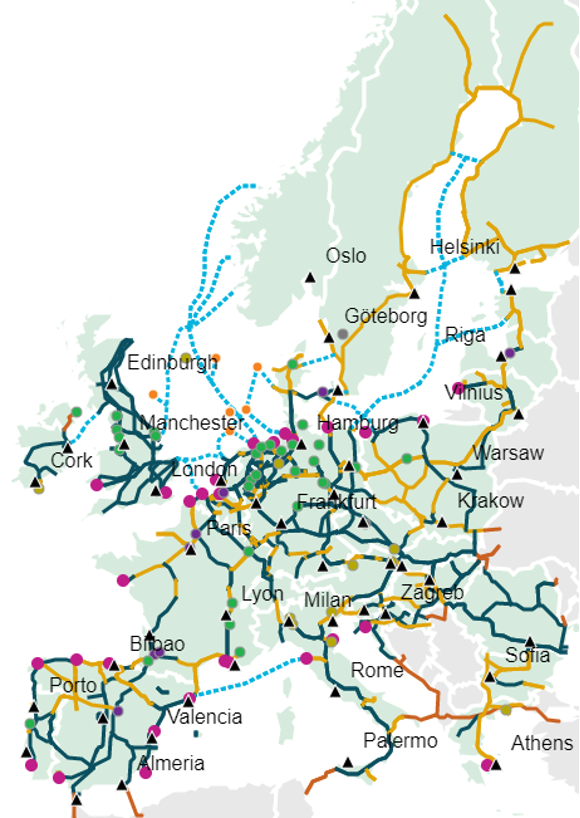

The electricity market zones with interconnectors within Europe are shown on the map in

The transmission system in Europe is shown on the map in

The development of cross-border energy infrastructure (electric, natural gas, hydrogen, etc.) is, to some extent, governed by the Projects of Common Interest (PCI) in the European Union.

4.1.4 The electricity market structure in the Nordic countries

The futures market is active from the day before operations until years ahead. On the day before operation, trading takes place on the day-ahead market. By noon 12.00 – after the market has closed – the balance-responsible parties submit binding action plans for consumption, production and trading for the following day. Operator plans are subsequently approved by the system operator but can be changed up to 45 minutes prior to operation via trading on the intraday market, which is open from 2 p.m. and up to one hour before operating hours. From this point, responsibility for balancing the system lies solely with the system operator, which can adapt production through several system services. The system operator maintains the balance by buying electricity (up-regulation) or selling electricity (down-regulation) in the regulation market. At the same time, the frequency of the network is stabilised by operating automatic reserves. The structure of the wholesale market is presented in

In addition to being responsible for the electricity markets as shown in

The natural gas system in Europe

The European natural gas system is shown on the map in

4.1.5 Natural gas market

- Shippers are commercial actors engaging in wholesale gas transport in the transmission system. The shippers purchase transport rights to deliver the gas to one or more gas suppliers in the distribution systems. The shipper is responsible for balancing deliveries into the transmission system and despatches out of the transmission system.

- Gas suppliers supply consumers with gas and invoice them for the gas received.

- The storage customer owns the gas that has been transferred by the shipper for storage in the gas storage facilities. The storage customer can sell the gas from the storage facility to a shipping company or another storage customer.

- The retail market is responsible for the distribution of gas from the transmission system to consumers and retail trade in gas to the end consumer.

- The gas transmission system is operated and owned by the TSO, who is responsible for volume balancing and the management of gas supply in the event of emergencies.

- The gas distribution systems are owned by the distribution companies.

- The gas storage facilities are owned and operated by GSOs or commercial actors. The storage facilities are operated on commercial terms. The storage facilities sell a product that allows the storage customer to store, inject and extract gas. This means that the storage facilities both compete with each other and are providers of other flexibility services.

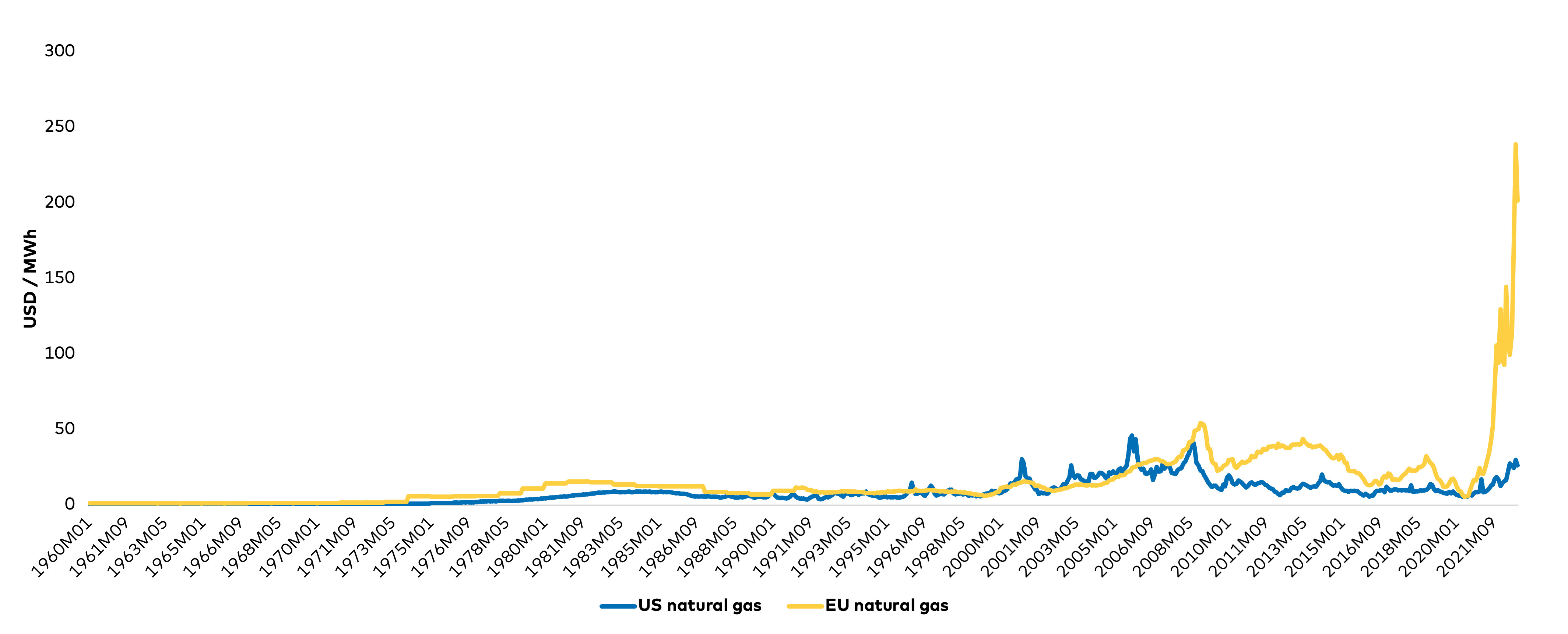

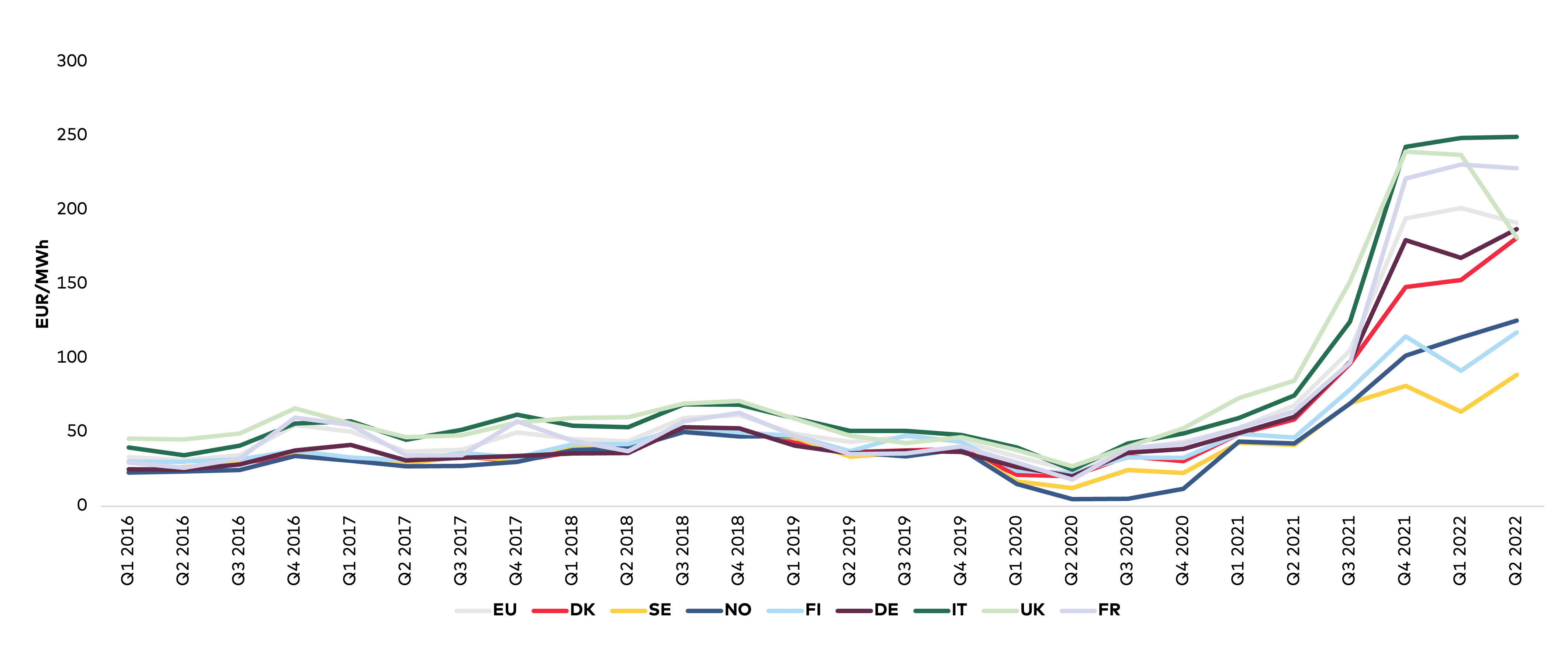

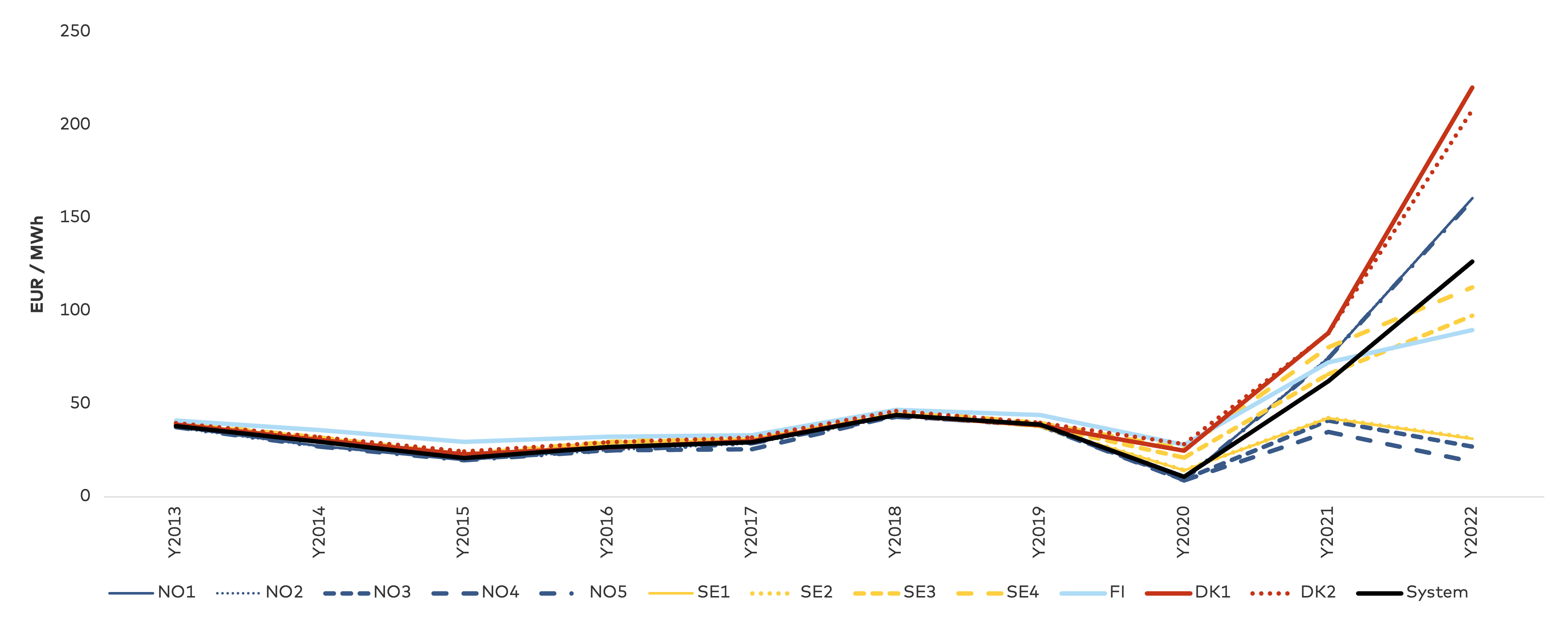

4.2. Natural gas and electricity prices in Europe

The energy crisis is generally manifesting in high natural gas and electricity prices increases. As shown in Figure 25, the natural gas price is more than four times higher than any previous peak price. The same can be said of the electricity price in

4.3 The energy system in Iceland

Power-intensive industries, mainly aluminium smelters, use around 80% of all electricity produced in Iceland, while other businesses use around 15% and homes 5%. A number of energy-intensive industries, combined with high heating demand, a small population and low-cost electricity production, make Iceland the largest per capita producer of electricity in the world.

One distinguishing feature of the electricity market in Iceland is the dominant size of the publicly owned generator Landsvirkjun. Today, most of the hydropower plants in Iceland are owned by Landsvirkjun, and the company generates about 73% of all electricity in Iceland. The company’s dominant position among energy producers in Iceland results in limited direct competition in the wholesale market. The largest share of Landsvirkjun’s energy generation goes to large industrial consumers (minimum of 80 GWh annual consumption), with most of the energy locked up in long-term power purchase agreements (PPAs).

The electricity transmission system is operated by Landsnet, and the company’s majority shareholder is the power producer Landsvirkjun (65%). While local distributors distribute energy to the retail market, large users are connected directly to the transmission network and contract with the TSO, Landsnet and Landsvirkjun on supply.

Due to its isolated energy system and limited import of fuels, Iceland is not directly affected by the current energy crisis in Europe. However, the effects can be felt indirectly through increased oil and petroleum prices, and air travel prices. Energy prices in Europe will also indirectly affect Iceland through higher goods prices as production costs rise in Europe.

While electricity prices have risen in Europe over the past year, they have remained stable in Iceland. This has resulted in growing demand for energy from industries in Iceland and increased interest from international industrial companies in relocating to Iceland. While Iceland has historically produced an energy surplus, growing demand from a diverse group of actors is putting pressure on the market. In recent years, a number of data centres have relocated to Iceland, and energy-intensive industries, such as food producers and the biotechnology industry, have also shown an interest in joining them. The increasing demand from larger consumers for renewable electricity, combined with a need for decarbonisation in the transport and the fishing industry, could affect the country's energy security.

5. DRIVERS, PREPAREDNESS AND RESPONSES

This section of the report analyses the drivers behind the crisis, the preparedness of each of the Nordic countries and their respective responses to the crisis. Before taking a closer look at each of these aspects, we briefly describe the drivers, preparedness and responses.

Drivers

The current energy crisis is ultimately the result of the decisions societies have made in planning their energy systems. The drivers described below could perhaps have been avoided if other technological visions and different energy infrastructure projects had been adopted. Discourse around our future energy supply is essential to ensure a successful green energy transition while balancing the three pillars of the Energy Trilemma of security, affordability and sustainability.

The drivers we have identified are shown in

This report argues that the current energy crisis has not been caused by a single incident or driver. Instead, it is a complex problem with several underlying causes triggered by the reduction in Russian fuel supplies, the unavailability of nuclear capacity in France, the drought in Europe and a speedy economic recovery following the COVID-19 lockdowns etc.

Even if Russia had not reduced its natural gas supply to Europe, the drivers we describe in the following would still have been present, creating issues for the energy system in terms of long-term security of supply. The drivers should not be viewed as standalone factors, since they are interdependent and consequently impact each other. While some of the drivers are already known to impact security of supply and energy prices, the manifestation of all drivers simultaneously has created a perfect storm, resulting in potential supply disruptions and high prices. In reality, it is the underlying risk factors, triggered by reduced fuel supplies from Russia, that have created the current energy crisis.

The extent to which each driver has impacted the current situation is not quantified. Such calculations are reserved for any subsequent report. For the time-being, we simply argue that there are a series of underlying causes that have contributed to the current energy crisis and that it is the manifestation of all the drivers simultaneously that has caused a perfect storm in the energy markets.

Preparedness

The energy system in each of the five Nordic countries is unique, even though the product consumers receive is the same – electricity, gas, heat, etc. The system each nation has built to generate and distribute electricity is different. These differences are attributable to natural conditions, organisational structures and investment in different technological visions.

Moreover, the relevance of security of supply, affordability and sustainability would essentially appear to change depending on current societal trends. There is generally a focus on one or two of these elements, which skews decision-making towards one of the three dimensions in the Energy Trilemma. With the advent of the energy crisis, we have recently gone from a situation with economic growth and low-interest rates and a focus on sustainability to a situation with a focus on security of supply and affordability of energy. Adopting a narrow focus on one of these factors generally appears to trigger a set of unintended effects with implications for security of supply.

The impact of the drivers in terms of security of supply at national level is analyzed by assessing each country’s exposure and comparing it to other countries. The Nordic countries have been impacted differently by each of the drivers, mainly as a consequence of the composition of each country’s energy system (mix of supply sources, infrastructure, degree of policy interventions and dependency on imports). This has resulted in different preparedness levels among the Nordic countries. The analysis also shows that each of the Nordic countries’ electricity systems offers its own distinct advantages, which can be leveraged in a common Nordic market.

Responses

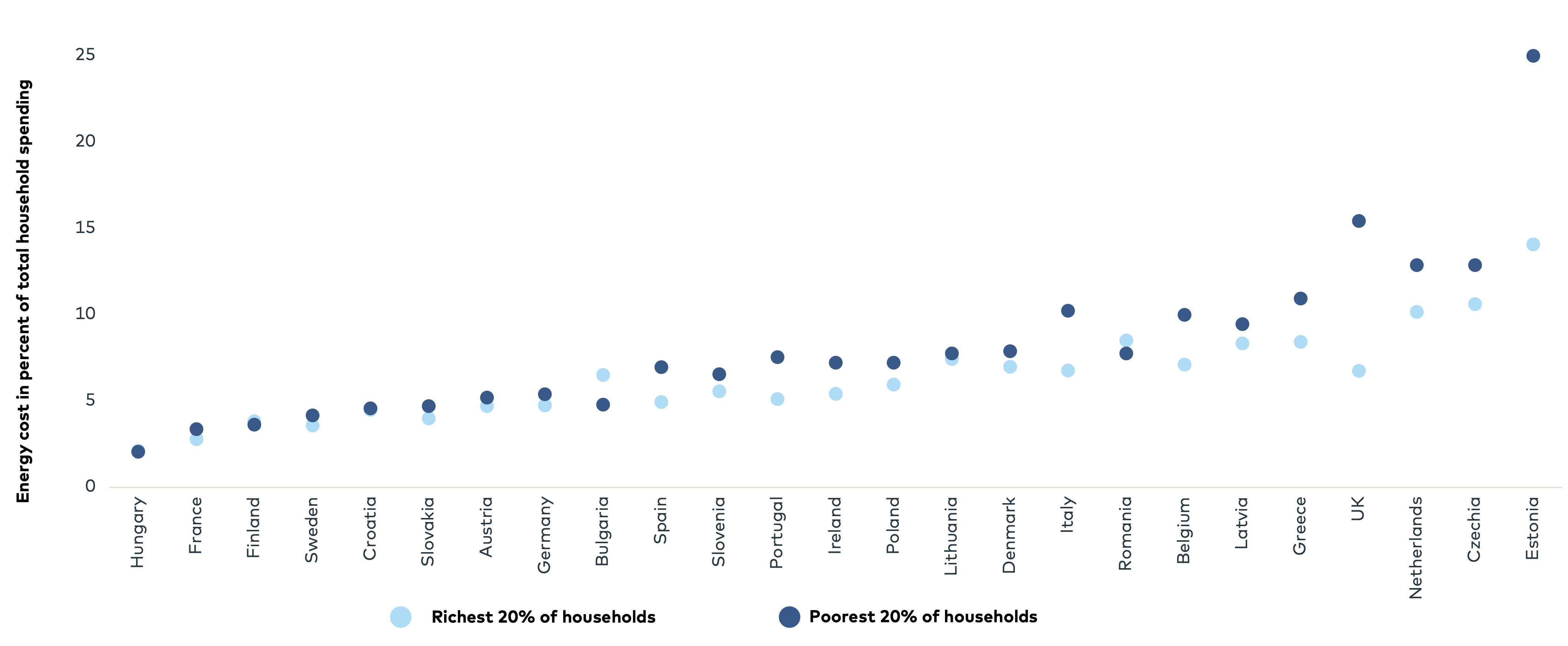

The Nordic governments have applied different initiatives to respond to the energy crisis with a view to mitigating energy poverty. While the increase in energy costs unleashed by the crisis have been felt by consumers, the Nordic countries have shown a degree of resilience and have been less affected by changes in energy poverty than other countries. Here it should be borne in mind that an increase in energy costs generally has a greater impact on the poorest households, and that this has also been the case in the Nordics, but to a substantially lesser degree than in the rest of Europe.

5.1 Electricity market structur

Influence on the energy crises

The electricity market structure in the Nordic countries and Europe had several unintended effects not envisioned at its inception. We will touch upon these separately in the following as we discuss the decommissioning of power plants and the introduction of subsidized renewable energy. The reason why some power plants were decommissioned is reflected in the dynamics of the marginal pricing principle applied in energy-only markets. The structure of the electricity market is viewed as a prerequisite for some of the subsequent drivers.

Context

The Nordic countries (excluding Iceland) were the first to reform electricity markets in Europe, together with England and Wales. While the Nord Pool electricity market traces its origins to 1932, it began to resemble its modern form with the deregulation of Norwegian electricity markets in 1991, followed by the addition of neighbouring Scandinavian countries Sweden (1996), Finland (1998) and Denmark (1999). The Baltic countries were added later, along with new transmission lines aimed at linking market areas. The electricity markets in the Nordic countries are closely connected to the rest of Europe, with a goal of creating an internal energy market connecting all EU member states via a single liberalised electricity market. The idea is based on the agenda of the free movement of capital, goods and people. The planning of energy infrastructure is mostly agreed upon at a national level. In contrast, the development of new Projects of Common Interest (PCI), such as interconnectors, is agreed upon at the EU level and between countries.

The reformed electricity markets in most western European countries are increasingly being coupled. Electricity is sold between the Nord Pool countries and the north-westnorth-western European markets through market coupling price mechanisms. In the event of In cases with no bottlenecks in the European electricity system, hydropower in Norway can, in principle, compete with nuclear power in France.

The electricity markets in Europe are developed as zonal markets. This means that the market operator has defined an area (market zone) where the electricity price is uniform. Any congestion within that zone is settled in the real-time markets or through bilateral contracts with the TSO. An internally congested zone will be expensive to operate, which calling s for either grid reinforcements or splitting of the zone into more zones. Such a situation can, for example, be seen in Germany, where there is only one one market zone is operated. Due to grid constraints, the wind farms in northern Germany cannot supply the electricity demand in the south of the country during periods of high windwindy periods, which causes wind production to be curtailed and conventional generators to be put into operation.

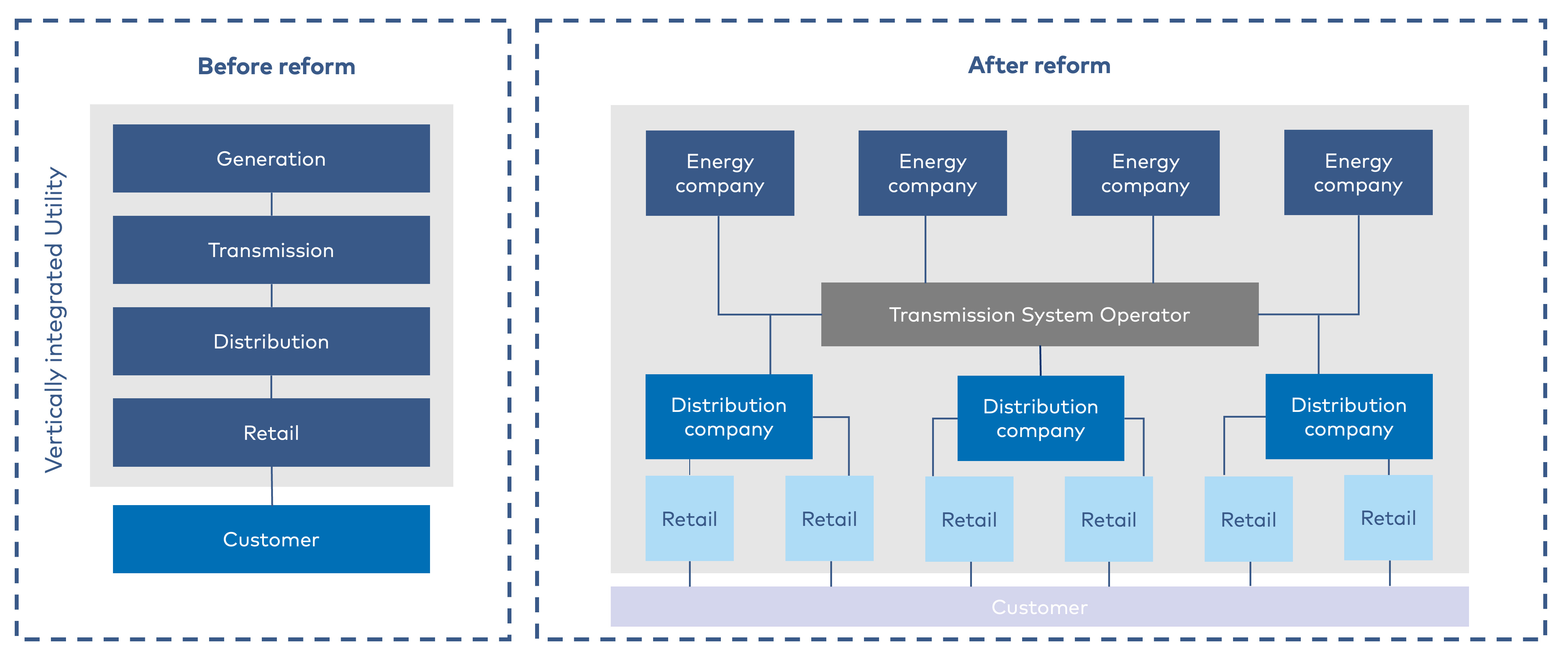

By reforming the electricity markets, vertically integrated monopolies were gradually dissolved with the aim of building a more competitive and flexible electricity market with competitive prices. As a result, companies could no longer generate, transport, trade and supply electricity while managing the transmission and distribution networks. Although there are national differences, today the effect of the reform today is a market that which operates based on the marginal pricing principle in energy-only market structures in which where new entrants can participate. The general reform of the operation of the electricity market is illustrated in

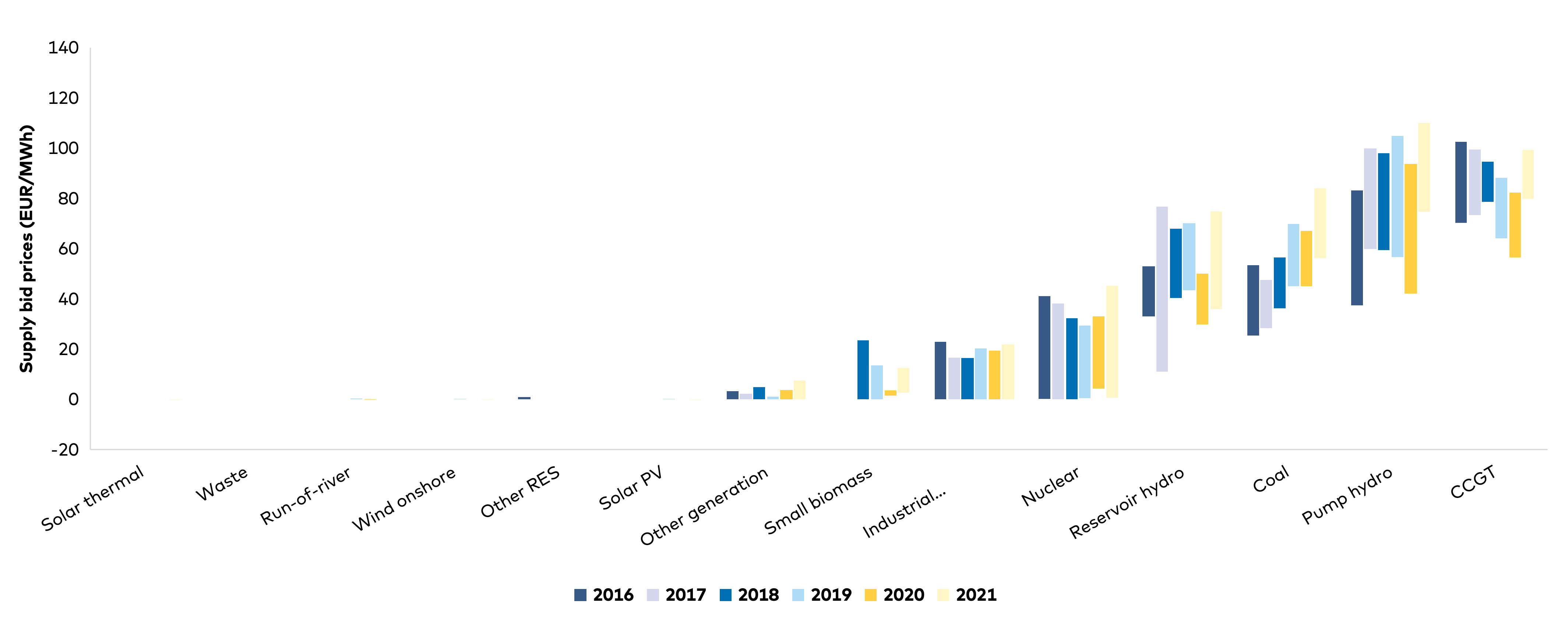

Consequences

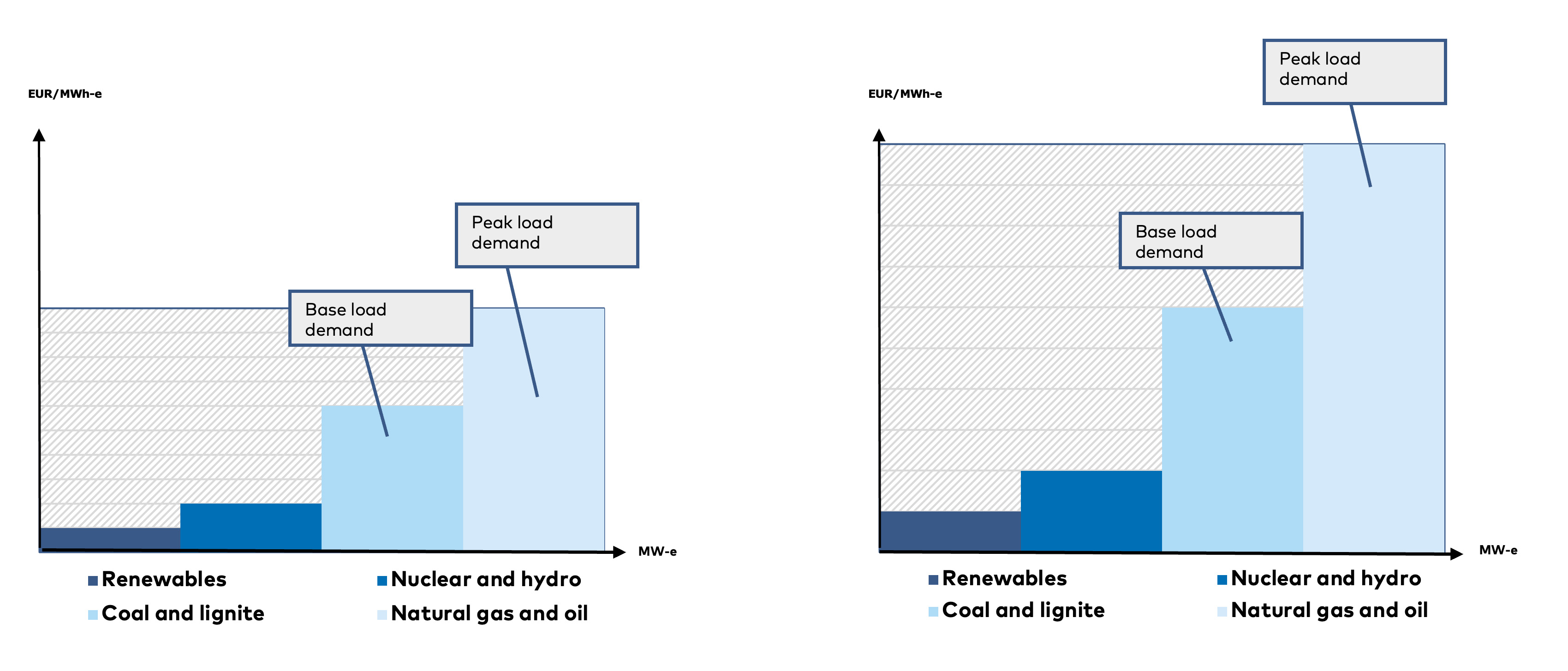

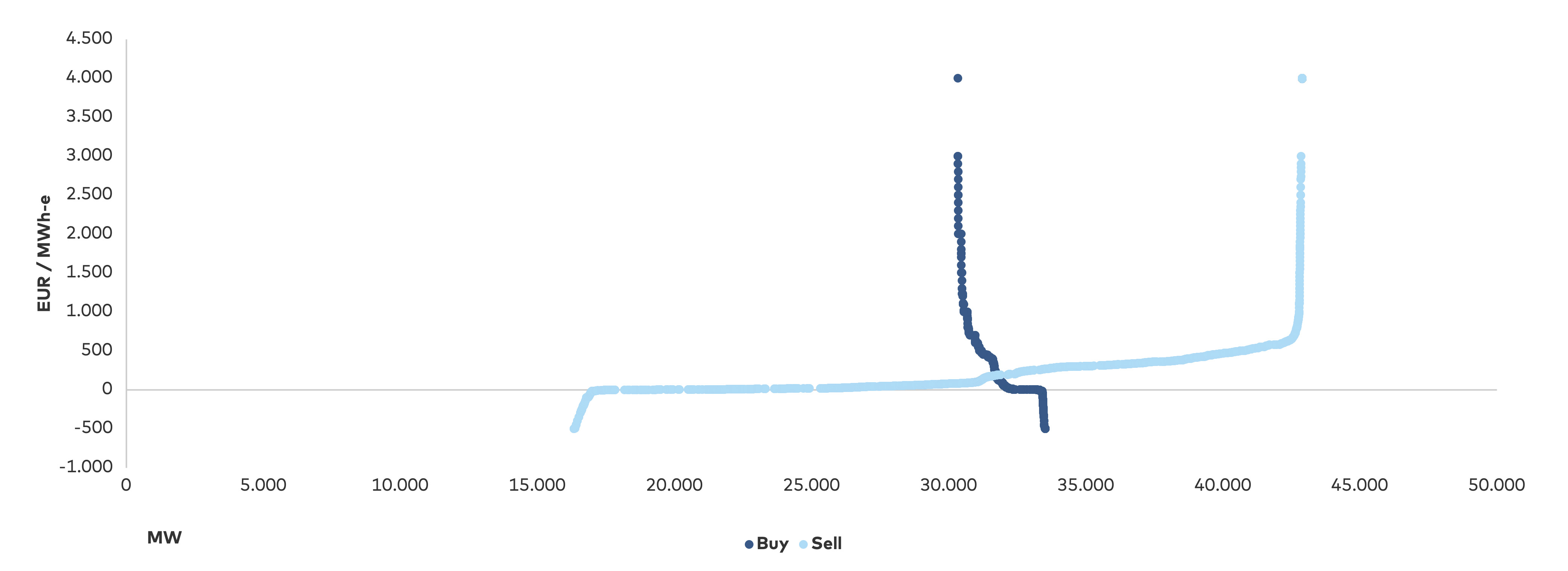

The principle of the energy-only market is that each supplier and consumer bid their marginal cost (excluding capital and fixed costs) of production and consumption into a market pool. Any profit made by the generators makes a contribution to capital and fixed costs. The demand curve reflects consumers’ willingness to pay for electricity. The intersection between the supply and demand curve sets the market price for electricity. Baseload generators with a low marginal cost recover their capital and fixed costs when more expensive generators are setting the market price. Peak load generators, with the highest marginal cost in the system, will only recover their capital and fixed costs when the market price is above the marginal cost of any generator – demand sets the price. Such price spikes occur when the total available generation capacity cannot supply demand. Peak-load generators hence only recover their capital and fixed costs when there is insufficient generation to supply demand, which in turn results in load-shedding and price spikes. The principle should, in theory, lead to investment incentives in new generation and an optimal mix of technologies.

Because price-setting in the European electricity markets is based on the last dispatched marginal unit (the most expensive unit required during operation), the electricity price is typically determined by gas- and sometimes oil-fired power plants – ultimately depending on the fossil fuel and CO2 prices and the renewable energy production.

The principle of the influence of increasing fossil fuel prices on market-wide electricity prices, as witnessed during the energy crisis, is outlined in

During the energy crisis, a price cap of 40 €/MWh was imposed on natural gas in the Iberian market. Direct payments to the gas-fired power plants cover the difference between the wholesale gas price and the cap, meaning that in practice the peak electricity price is capped. Consumers pay a lower price for the electricity provided that the government provides a direct payment. The net result is lower costs of energy for consumers.

Impact on the value chain

The impact of the marginal pricing principle in energy-only markets is primarily that generators must make the necessary revenue during peak price hours to cover capital and fixed costs and that consumers, in situations of bottlenecks between market zones, will be exposed to significant price increases. The following market drivers are a direct result of the operating principle of the energy-only market.

FOCUS ON ICELAND

The Icelandic parliament adopted the European Union Directive on competition and unbundling of the internal energy market in 2003 through The Electricity Act (no. 65/2003). With the new energy law, Landsvirkjun was no longer obligated to supply users in the country with an adequate supply of electricity; instead, the supply of electricity was to be determined by market dynamics. No public authority has responsibility for security of supply. Nonetheless, the Icelandic electricity market has a different structure to that of the other Nordic countries, as there are fewer actors throughout the value chain.

A long HVDC cable connecting Iceland and the United Kingdom, Icelink, has been proposed. Were the cable be built, the Icelandic electricity system would be connected to Europe.

5.2 Decommissioned controllable electric capacity

Impact on the energy crisis

Context

Consequences

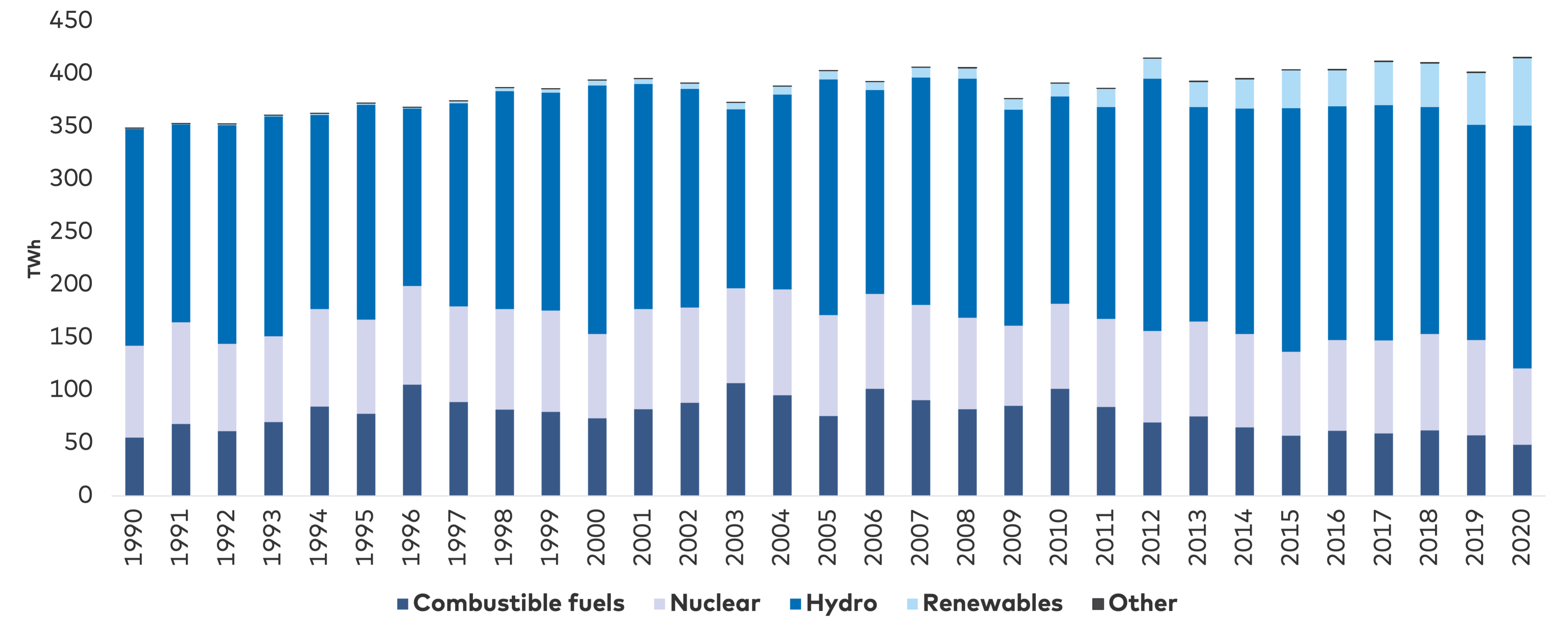

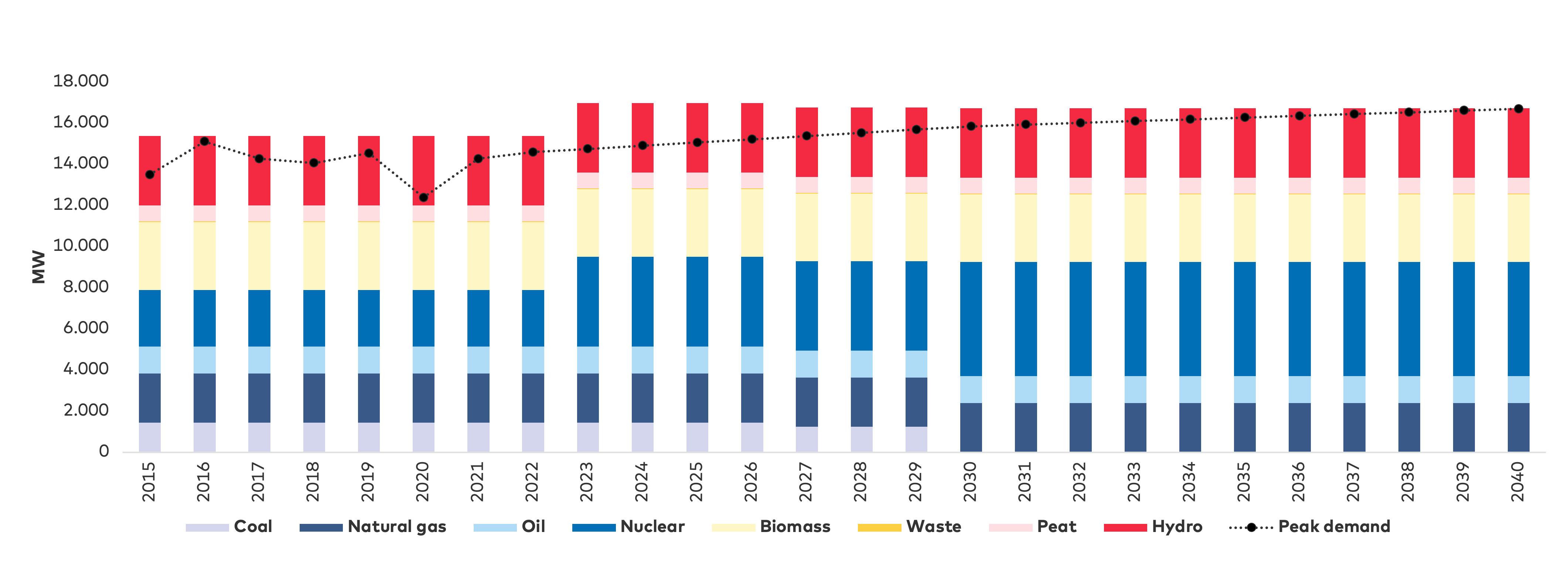

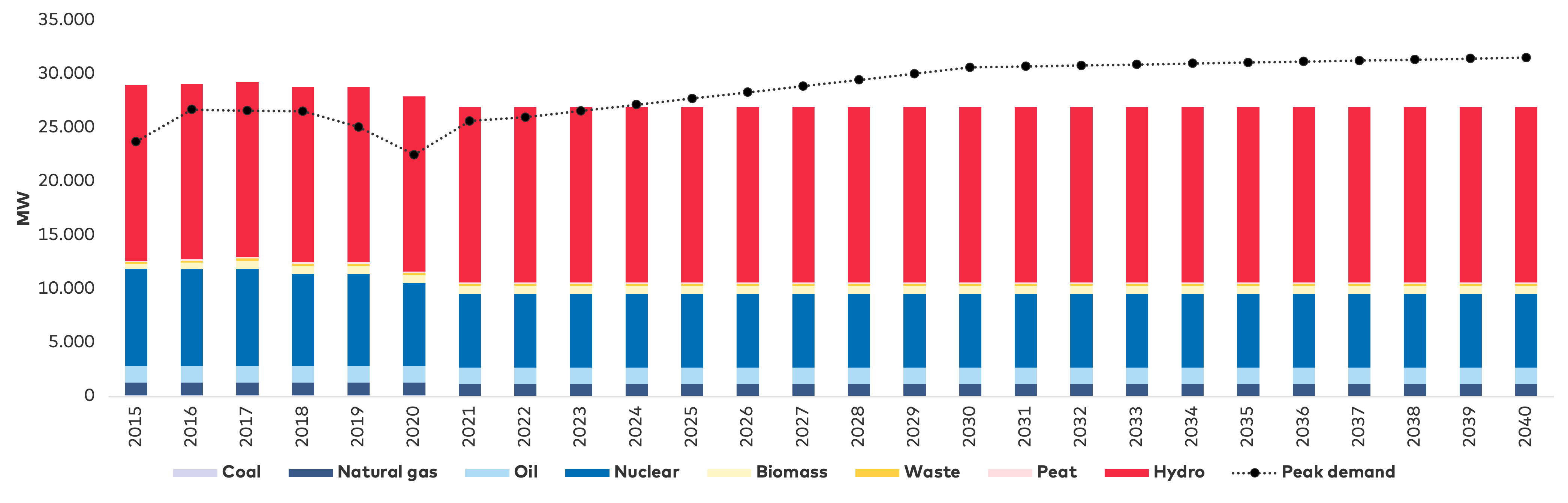

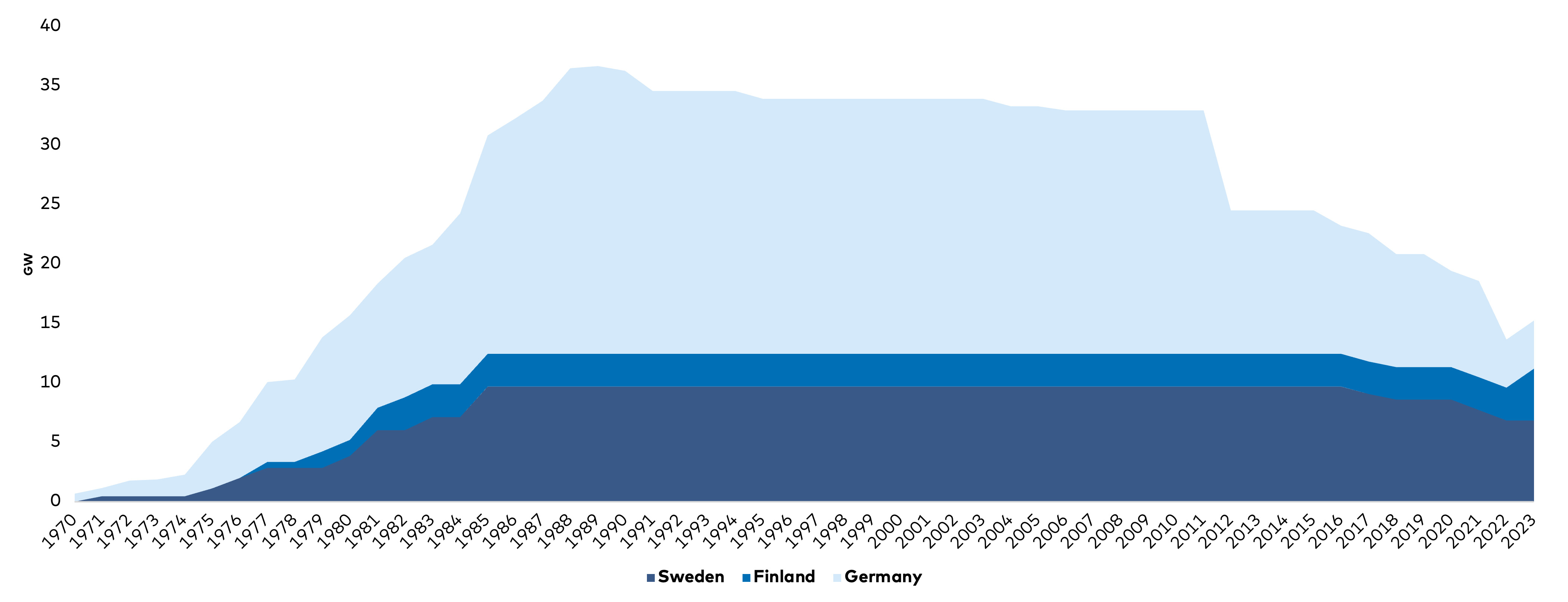

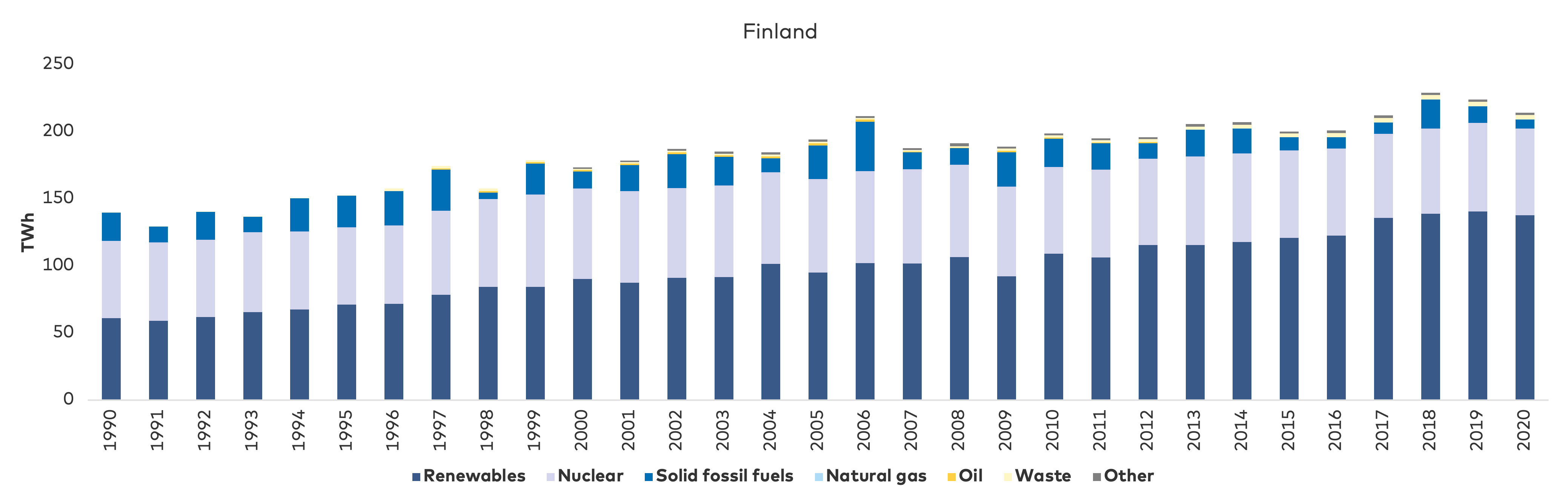

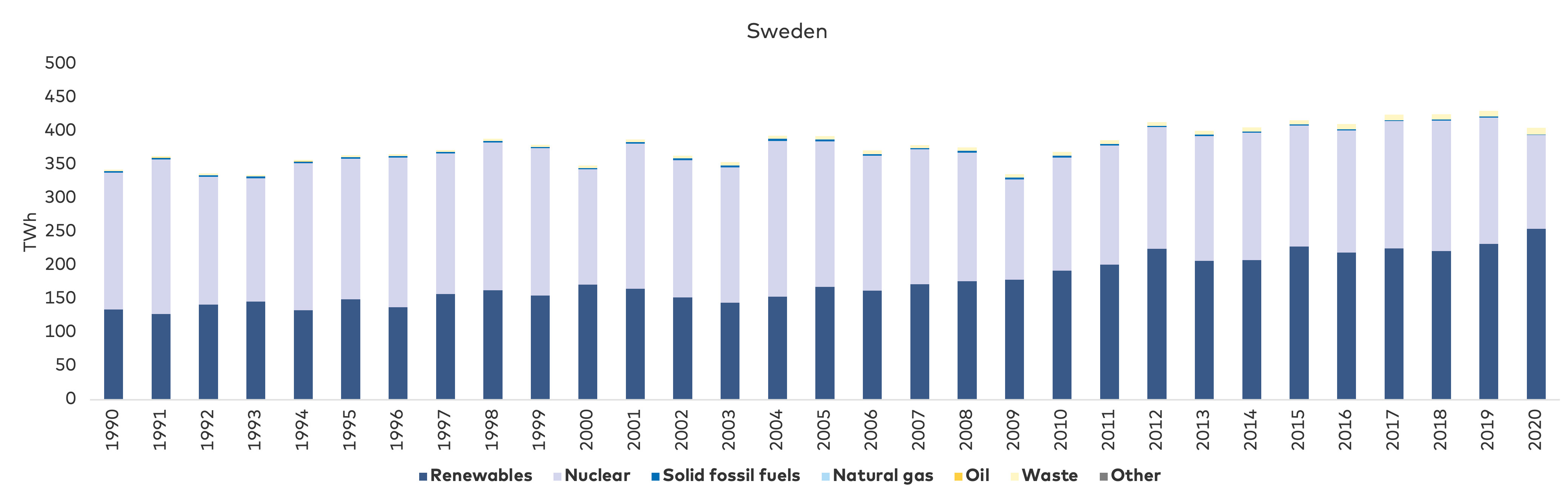

The development of nuclear power plant capacity in Finland, Sweden and Germany is shown in

Denmark

Denmark

Finland

Finland

Sweden

Sweden

Norway

NorwayThe development of nuclear power plant capacity in Finland, Sweden and Germany is shown in Figure 33. Germany had planned to close all its nuclear reactors by 2023, but has decided to keep the remaining plants in operation due to the energy crisis. Sweden has also closed some reactors, whereas Finland has increased capacity with the addition of the Olkiluoto 3 reactor. Overall, the total nuclear capacity in central/northern Europe has decreased significantly over the last decade.

High electricity prices throughout the day usually indicate a lack of baseload capacity, since peak plants dictate the price even at low demand. This development is most prevalent in countries where the majority of electricity production comes from thermal power plants. Although the Nordic countries generally appear to be safeguarded against a significant reduction in security of supply due to their reliance on hydro and nuclear power, a reduction in security of supply may be experienced, as power plants are decommissioned and electrification of society increases. Additionally, grid interconnectors from the Nordics to central Europe increase the likelihood of spill-over effects, thereby challenging generation capacity, security of supply and low electricity prices in the Nordics. Despite this, electricity demand in the Nordic countries is expected to increase due to the need for the electrification of society in order to fulfil national climate targets, although it is expected that much of this demand will be supplied by renewable energy. However, supply disruptions can occur during unfavourable conditions for wind and solar.

Nuclear power in France is an important part of the electricity mix in Europe and provides most of the country’s electricity production. However, only 30 out of 56 nuclear reactors are currently operating. This exposes France to potential electricity supply disruptions and increases in electricity prices in the rest of Europe. During 2022, nuclear reactors have been out of operation due to a mix of technical and environmental issues. The latter included biodiversity concerns in connection with increased water temperatures in rivers due to discharge of water from the reactors. Nuclear power plants in the Nordics are nonetheless located by the sea, making the risk exposure to environmental standards less than those experienced by France in 2022. However, technical issues are also present, including in the Nordics, as reflected in the delay in the start-up of the Olkiluoto 3 reactor.

Impact on the value chain

The main impact on the value chain is a lack of generation capacity in countries relying on power plants to supply electricity demand. The closure of nuclear power plants or decreased capacity due to a mix of technical and/or environmental issues also play a role here. Electricity exchange via interconnectors creates spill-over effects between countries. The security of supply is hence reduced in all countries. Furthermore, the lack of baseload capacity allows more expensive power plants, such as gas-fired power plants, to set the electricity price during many hours in line with the marginal pricing theory.

FOCUS ON ICELAND

There has been no significant decommissioning of controllable electric capacity in Iceland.

5.3 Balancing electricity supply and demand

Impact on the energy crisis

Context

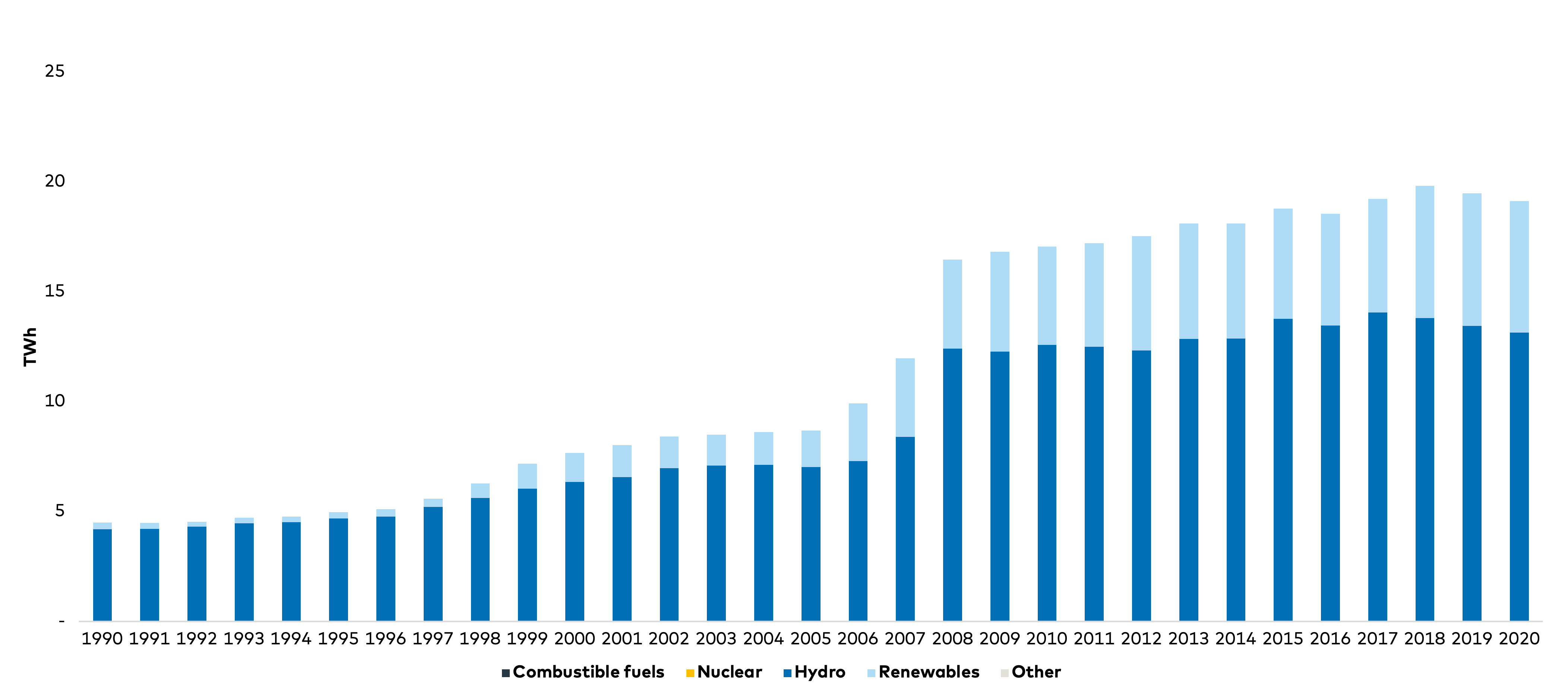

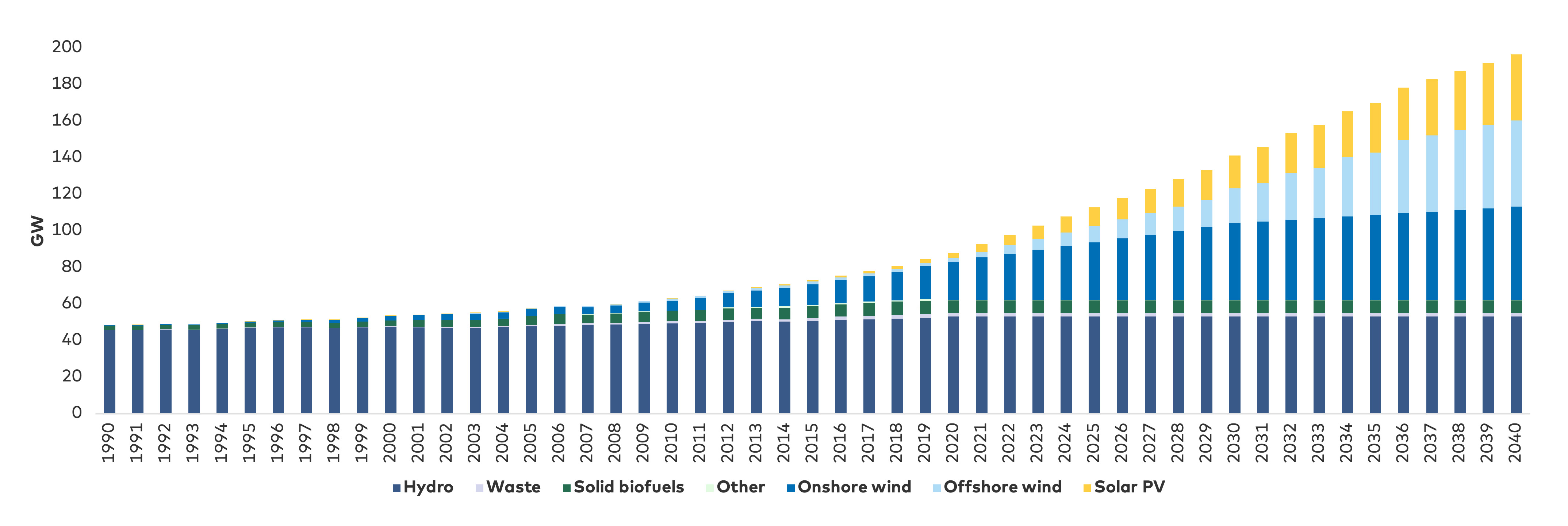

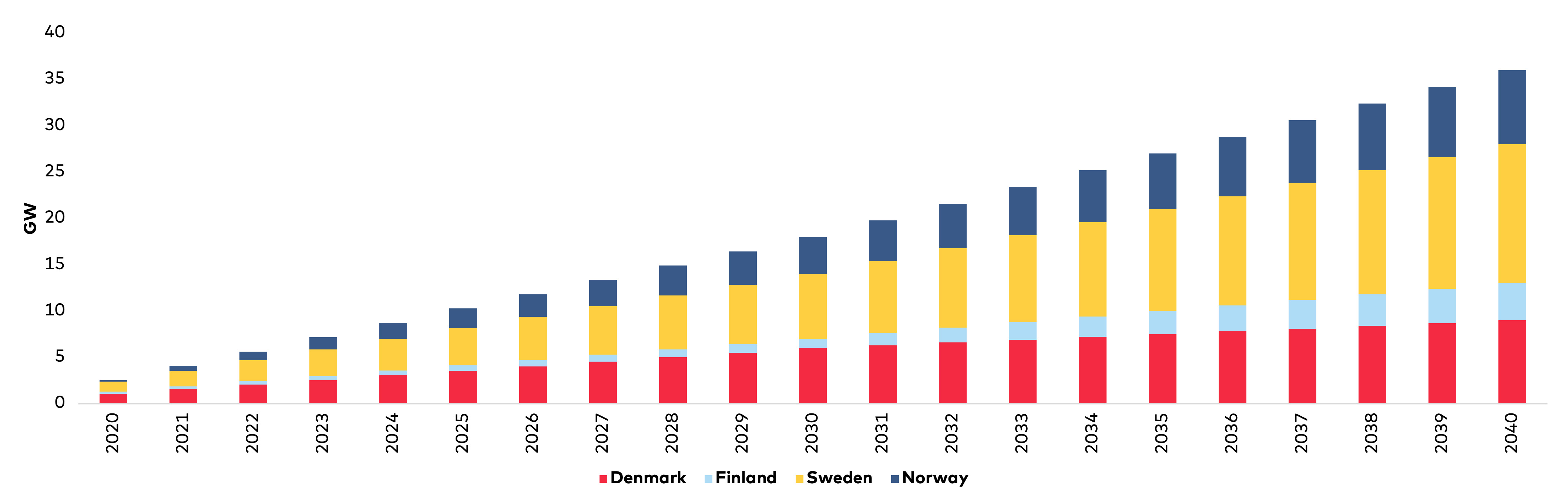

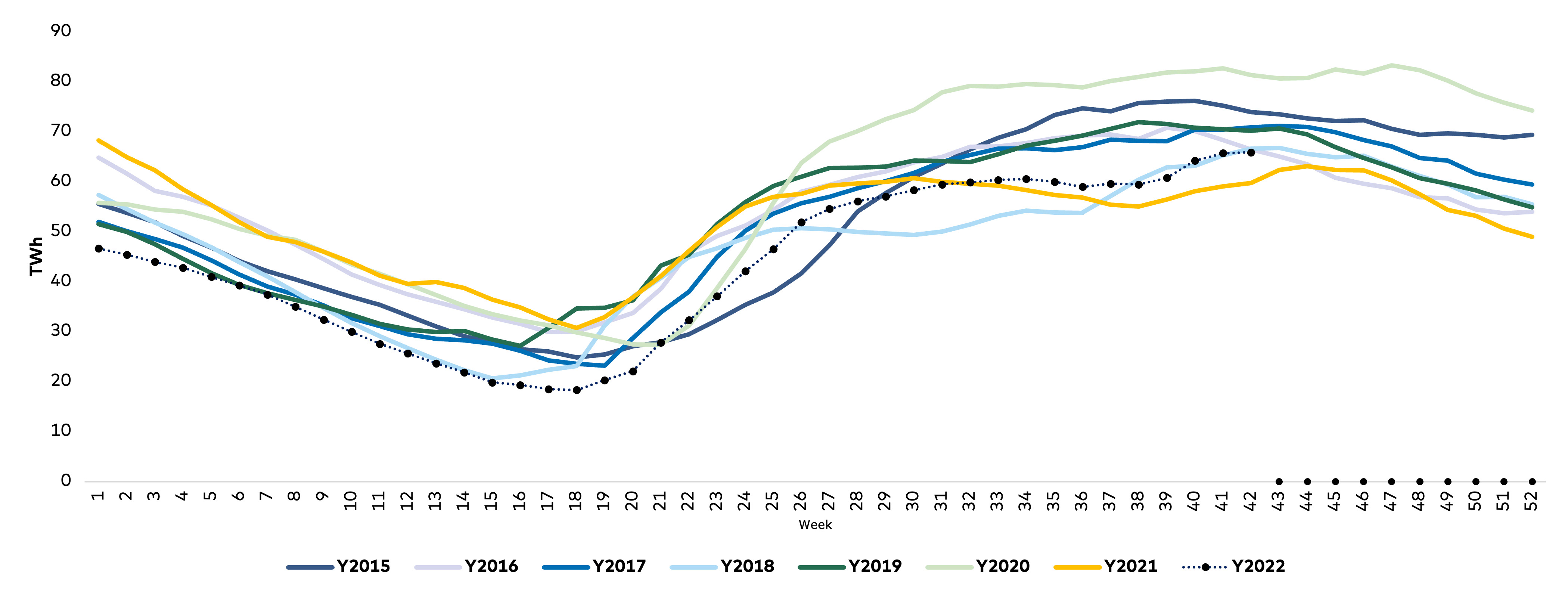

Given the importance of the energy sector for reaching these decarbonisation targets across society, the integration of renewable energy has become a key policy priority. Historically, the Nordic countries have led the way in integrating renewables into the energy mix. The high reliance on hydro and nuclear power has also ensured very low CO2 emissions from the electricity sector in comparison with other regions. Further development of wind and solar will increase the volume of renewables. The historical and projected development of low-carbon electric capacity in the Nordic countries are shown in

| Denmark | Finland | Iceland | Norway | Sweden | |

| Carbon neutrality | 2050 | 2035 | 2040 | 2030 | 2045 |

| Application of carbon sinks (offsetting) | Yes | Yes | Yes | Yes | Yes |

| 2030 CO2 reduction target | 70% | 60% | 40% | 50-55% | 63%* 70%** |

| 2050 CO2 reduction target | No | 90-95% | No | 90-95% | 85% |

| Legally binding | Yes | Yes | Yes | Yes | Yes |

| *Emission reduction covered by the EU Effort Sharing regulation ** Domestic transport excluding aviation | |||||

Consequences

One consequence of the increased integration of renewables in the electricity generation mix is a weather-dependent electricity system. This in turn necessitates a heightened focus on forecasting supply and demand to balance the system. The fact that demand from consumers does not coincide with renewable electricity production gives rise to a need for dispatchable energy resources to supply demand during these hours. The use of energy storage to reschedule production or a combination of energy storage and dispatchable energy is also possible. The Nordic countries have historically relied on conventional power plants and hydropower to provide this flexibility. Given the reduction in power plant capacity, there is a need to identify other sources that can reliably produce electricity during these periods.

The use of subsidies to stimulate interest in developing renewables has created a situation in the electricity market where renewable energy generators are able to bid at a very low (even negative) marginal price. This has increased the number of hours with negative electricity prices. Other issues relating to the integration of renewable energy include higher regulation costs and the creation of bottlenecks between electricity market zones as well as internally within countries due to major price variations caused by the lack of electric transmission infrastructure .

Impact on the value chain

Renewable energy integration impacts producers, grid operators and consumers throughout the value chain. Grid operators need to invest in balancing measures to avoid outages and strengthen electric transmission infrastructure in order to decrease the risk of congestion between the generation site and load centres. Consumers are required to deliver demand-side flexibility to reduce the price paid for electricity by spreading out the demand to match supply.

FOCUS ON ICELAND

Due to the isolated nature of the energy market in Iceland, production capacity must be higher than demand. This excess capacity has decreased in recent years and, according to Landsnet’s predictions, may fall below the threshold in the coming years. In 2021, electricity demand was approaching the power plants’ total installed capacity, complicating the balancing of electricity generation. Demand for electricity, combined with a dry year in 2021 and bottlenecks in the transmission system, led the National Power Company of Iceland to reduce the electricity supply to, among others, fishmeal factories. This meant that fishmeal factories had to burn oil to power their buildings. Electricity prices, however, remain stable.

Since variable renewable energy sources such as wind and solar have not been significantly developed in Iceland, the problems relating to shorter-term balancing are not relevant.

5.4 Lack of electric grid infrastructure

Impact on the energy crisis

Context

Improvements in the electric transmission network are mainly necessitated by imbalances between the regions where production and consumption take place, for example, northern Sweden, which has high production and southern Sweden, which has high demand. Improvements in the electric distribution networks (local networks) are required to reduce local/regional bottlenecks that create local capacity shortages. One challenge is that most renewable energy capacity has been connected at a low-voltage distribution level.

Another sometimes forgotten challenge with renewable energy development is that it requires more electrical infrastructure to transmit the energy from production sites to load centres compared to fossil-based generation. This is because the capacity factors for wind and solar are lower than fossil sources by nature. The fact that the energy crisis is partially attributable to the lack of electric grid infrastructure to handle fluctuating renewable electricity production leaves Europe highly vulnerable to changes in weather conditions and disruptions in fuel supply.

Consequences

Sweden’s central location means that other Nordic countries will be impacted by the resilience and stability of the Swedish transmission grid. Three significant changes have driven new electricity exchange patterns during the energy crisis: (1) decommissioning of nuclear power plants in Sweden, (2) increased wind power in northern Sweden and (3) new interconnectors between Norway and Germany and between Norway and the United Kingdom. These changes have increased electricity flows from Finland to SE3 and onwards to NO1 as well as from SE2 to SE3, resulting in congestion between SE2 and SE3 and reduced capacity between SE3 and NO1 to safeguard operational security. These flow patterns are expected to increase following the commissioning of Olkiluoto 3.

The reduced capacity in the corridor between NO1 and SE3, as well as between SE2 and SE3, affects power prices in the whole Nordic system by impacting the ability to trade energy east–west and north–south. This has created price differences between electricity market bidding zones, especially in the southern and northern parts of Norway and Sweden. Long lead times on the infrastructure between SE2 and SE3 have also contributed to this development.

Impact on the value chain

Underinvestment in electric grid infrastructure primarily impacts the ability to transport energy from production sites to load centres. Furthermore, the long lead times associated with developing infrastructure projects can impact the ability to respond to physical infrastructure challenges caused by the relatively rapid roll-out of renewable energy generation capacity. Both elements result in increased price differences between electricity market bidding zones.

FOCUS ON ICELAND

The transmission system in Iceland is ageing, and there are problems with expanding transmission capacity. Delays in the maintenance of the transmission system, lack of investment and increased electricity demand have caused tolerance limits of the network to be reached, and there are also transmission constraints between different parts of Iceland.

The average age of transmission lines (per km) in Iceland is 44 years, where the designated lifetime of lines is 50 years. System bottlenecks mean that many parts of Iceland are affected by transmission capacity constraints, which cause energy insecurity and hinder the development of industry in certain areas.

A storm in 2019 represented one of the most extreme weather events experienced by the Icelandic power system, causing major damage to transmission lines. As a result, a decision was made to speed up the construction of new transmission system lines. The development of a new transmission network started in 2019, and is due to be completed in 2030. The development has met some opposition, and approval procedures such as obtaining construction permits from municipalities and environmental impact assessments have made the process slower than expected.

5.5 Inflexible electricity demand

Impact on the energy crisis

Context

However, this does not necessarily mean that end-users do not reduce their electricity consumption during peak hours if electricity prices are high. Consumers are increasingly being exposed to real-time electricity prices, and are moving from fixed price to variable price contracts with electricity distributors in order to align consumption with periods of low electricity prices.

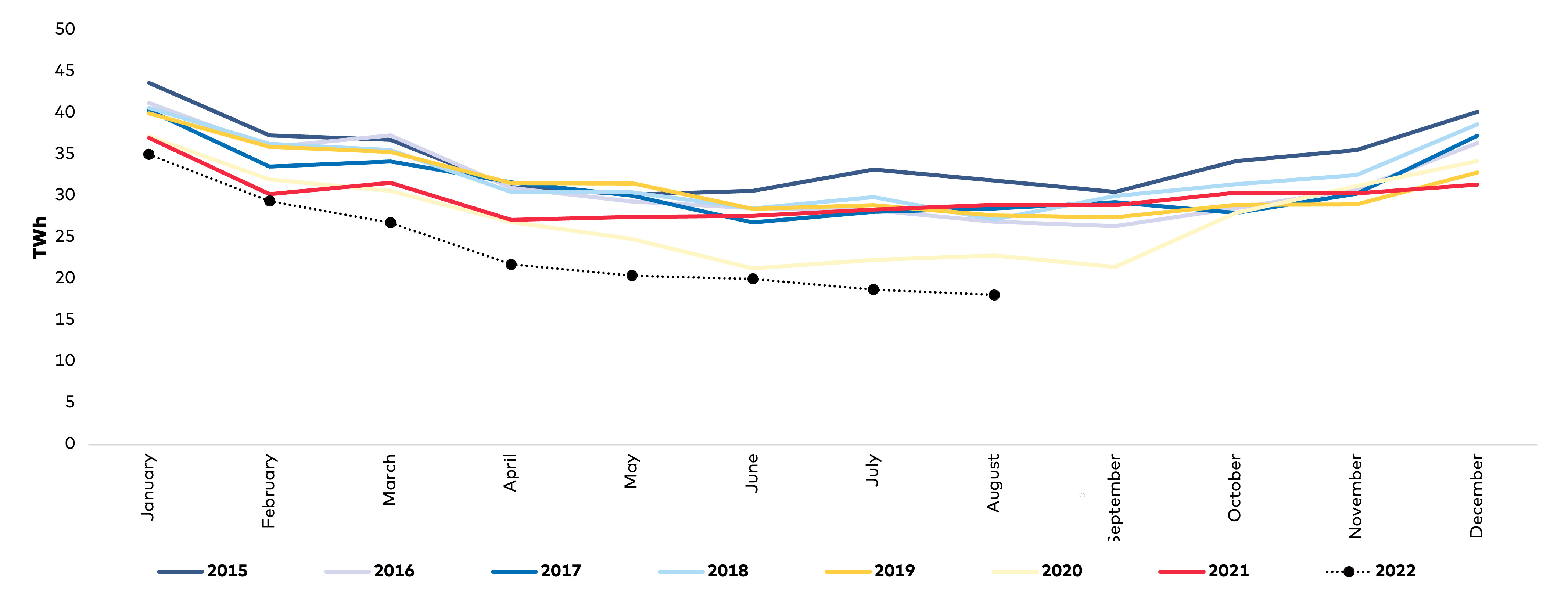

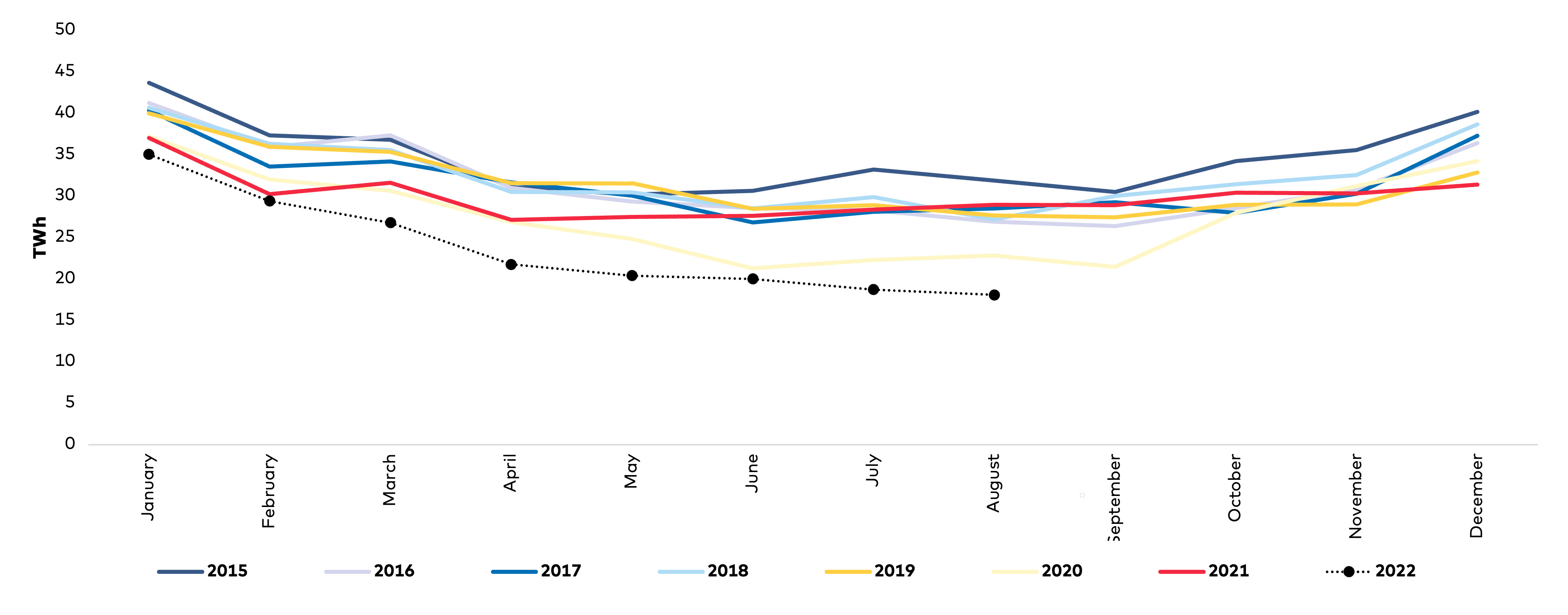

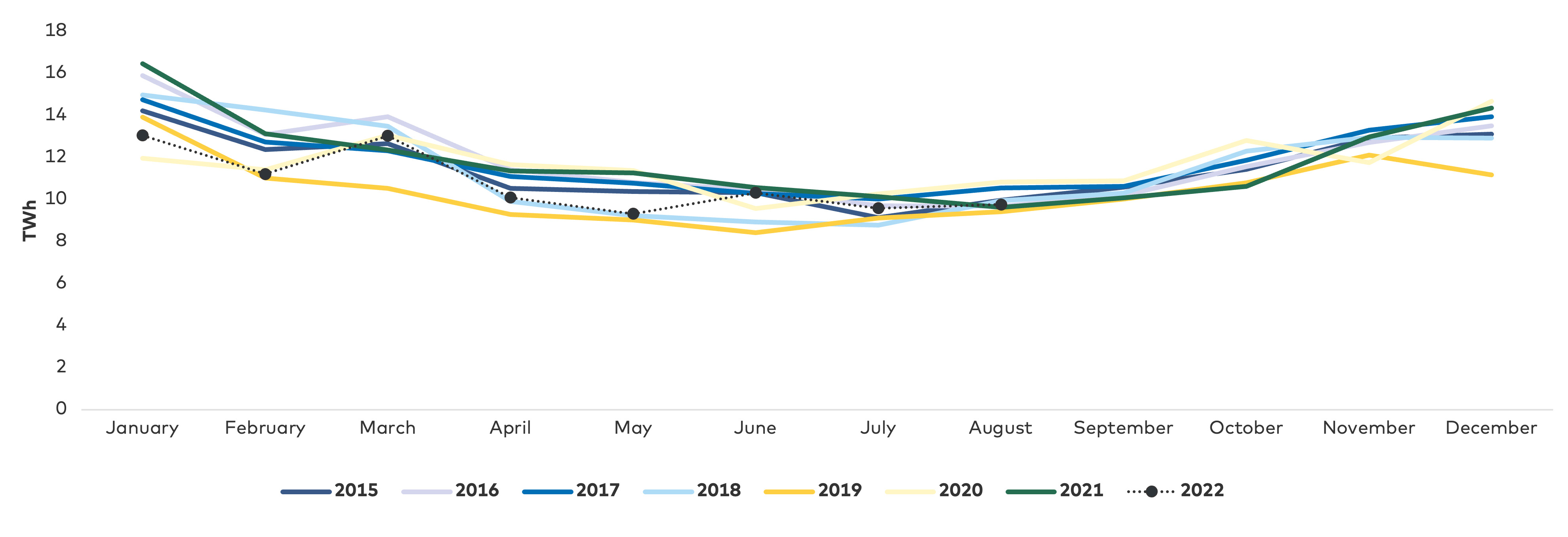

Realised Nordic electricity demand per month for the period 2015–2022 can also be seen in

Consequences

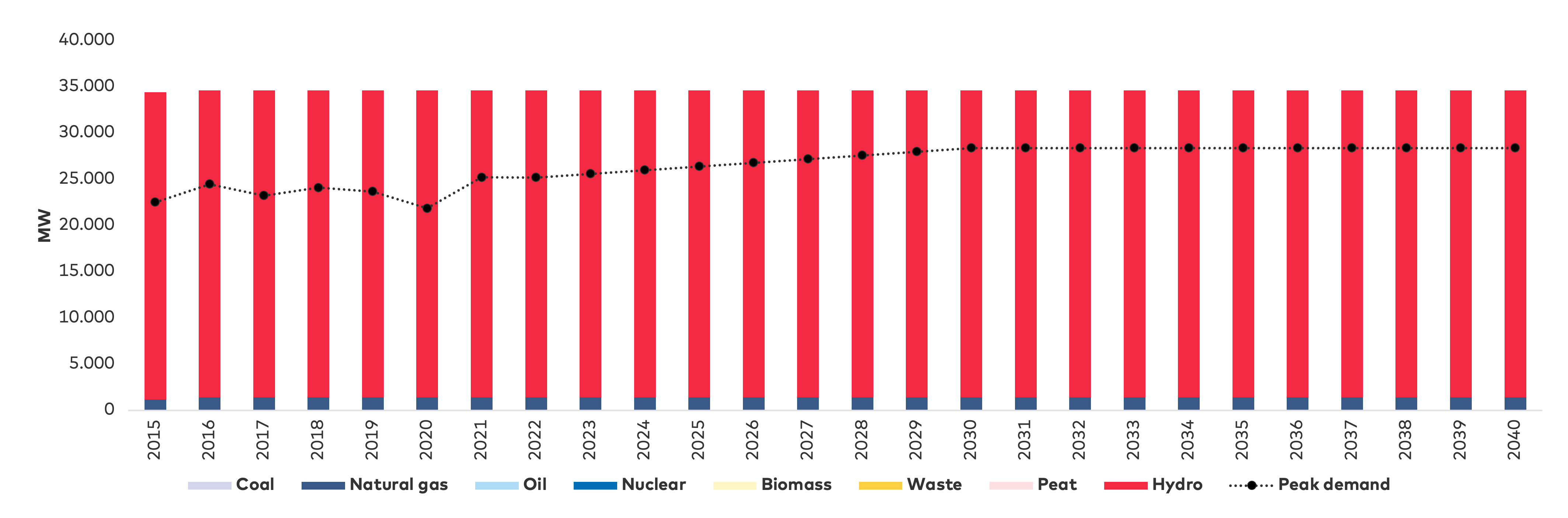

The inflexible demand and the decrease in baseload capacity from hydro and nuclear power has led to concerns about potential brownouts in the Nordic countries during hours of peak demand. A risk of power shortages for winter 2022–2023 has been highlighted in some of the Nordic countries, see

Impact on the value chain

| DENMARK | SWEDEN | NORWAY | FINLAND | ICELAND | |

| Risk reported publicly | ! | ! | ! | √ | X |

| √ = Risk reported X = Risk not reported. ! = Heightened awareness | |||||

FOCUS ON ICELAND

Around 80% of all electricity production in Iceland is used by a few large energy-intensive companies, with most of the energy locked up in long-term power-purchase agreements (PPAs). For example, the largest and longest PPA in Iceland is a 4.9 TWh/year contract between Landsvirkjun and Alcoa, with a duration of 40 years.

Historically, energy-intensive companies have shown an interest in relocating their operations to Iceland. For a long time, the majority of companies interested in Icelandic energy were aluminium smelters. However, in recent years more high-intensive electricity industries have joined this group, including data centres.

Iceland has enjoyed very stable electricity prices, and the government has not been required to intervene to support affordability. An inflexible demand side is not a problem if the production of electricity is controllable.

5.6 Weather-dependent energy supply

Impact on the energy crisis

Context

Consequences

Norwegian hydropower has generally benefitted from high electricity prices. However, low reservoir levels have resulted in calls to reduce Norway’s electricity exchange with other countries in order to conserve supplies. This illustrates that the weather has an influence not only on renewable energy production but also on other types of generation. However, the need to supply demand during periods of low wind and peak demand remains. For example, Denmark relies on power plants and electricity imports to meet demand when there is a lack of production from renewable energy. Going forward there is therefore a need for sustainable annual and multi-year long-term energy storage possibilities.

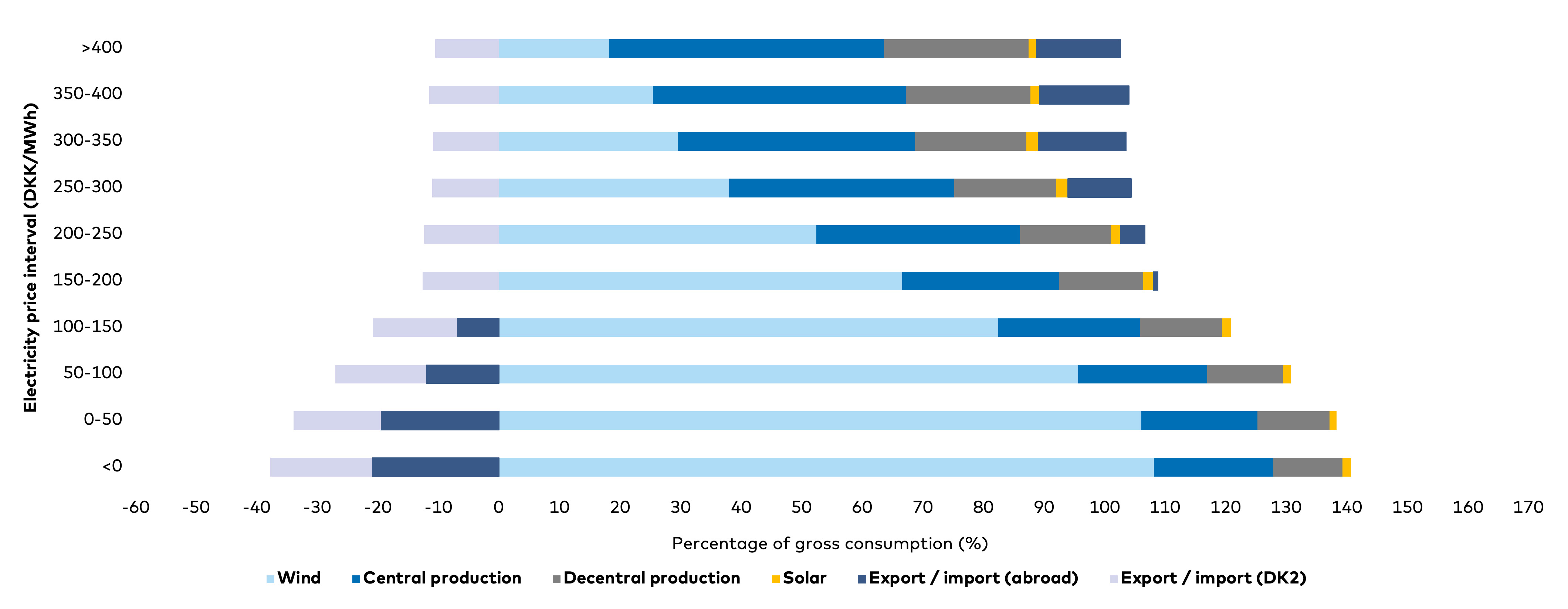

The general impact of wind energy on electricity prices and electricity flows is shown in

Impact on the value chain

Security of supply can be weakened when there is low availability of multiple energy supply options at the same time due to unfavourable weather conditions. Reduced availability of conventional power plants (as explained in

FOCUS ON ICELAND

Hydropower accounts for 70% of total electricity generation in Iceland. Since hydropower depends on weather conditions, power generation is likely to vary accordingly. Glaciers play an important role in the hydropower system in Iceland and glacier melt during warm and dry summer periods is likely to cause a variation in hydropower electricity generation. Wet, dry and normal years occur in Iceland, and in dry years, hydro facilities are at risk of water shortages. Conversely, extra power generation opportunities can be wasted in wet years due to a lack of buyers, i.e., demand, or transmission problems. Critically, as previously mentioned, there was a lack of water inflow in 2021, which led to the curtailment of the national electricity supply.

5.7 Increasing energy-import dependency

Impact on the energy crisis

Context

Consequences

Europe’s import dependency and reliance on Russian supply as its main source of energy imports is an important driver of the current energy crisis. Following the 1970’s oil crisis, most countries started to diversify their fuel purchases across countries to avoid becoming dependent on a single energy supplier. The problem then was reliance on oil supplies from OPEC; today, it is reliance on supplies from Russia. However, the two situations are comparable. Since Europe’s dependency on imports of Russian natural gas has been very high, energy supply disruptions cannot be disregarded for the coming winters before other energy supply chains are available at the same level as before the conflict with Russia. Connection to Europe via interconnectors and gas pipelines from the Nordic countries and the general global nature of fuel markets have created a spill-over effect for high energy prices. The energy supply challenges in Europe have been transplanted to the Nordic countries.

Impact on the value chain

The lack of diversification of energy resources and dependency on imports from Russia impact the value chain across primary energy sources. Mitigating the current situation will require diversification of energy resources and suppliers in order to provide the necessary level of security for the energy supply.

FOCUS ON ICELAND

The driver is not relevant to Iceland since 90% of primary energy use comes from domestic low-carbon energy sources. The other 10% mainly derives from oil imported from Norway.

5.8 Reductions in natural gas supply

Impact on the energy crisis

Context

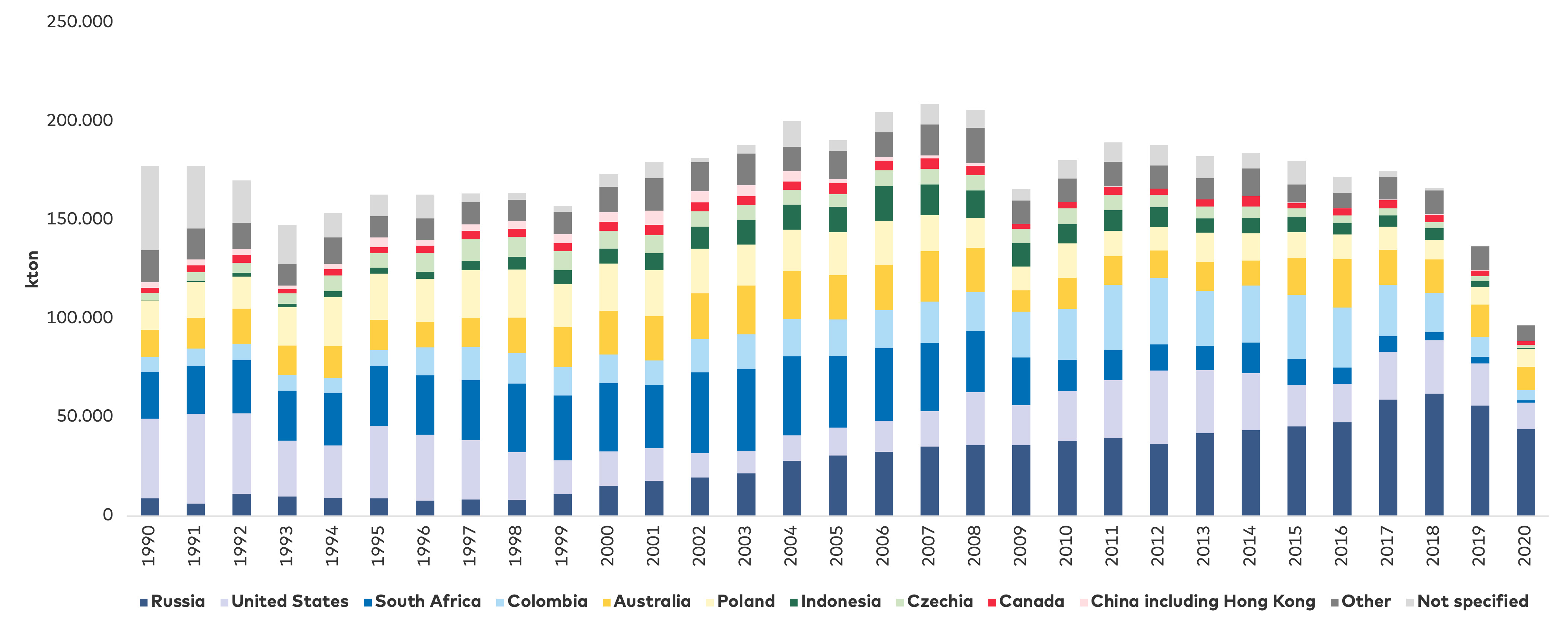

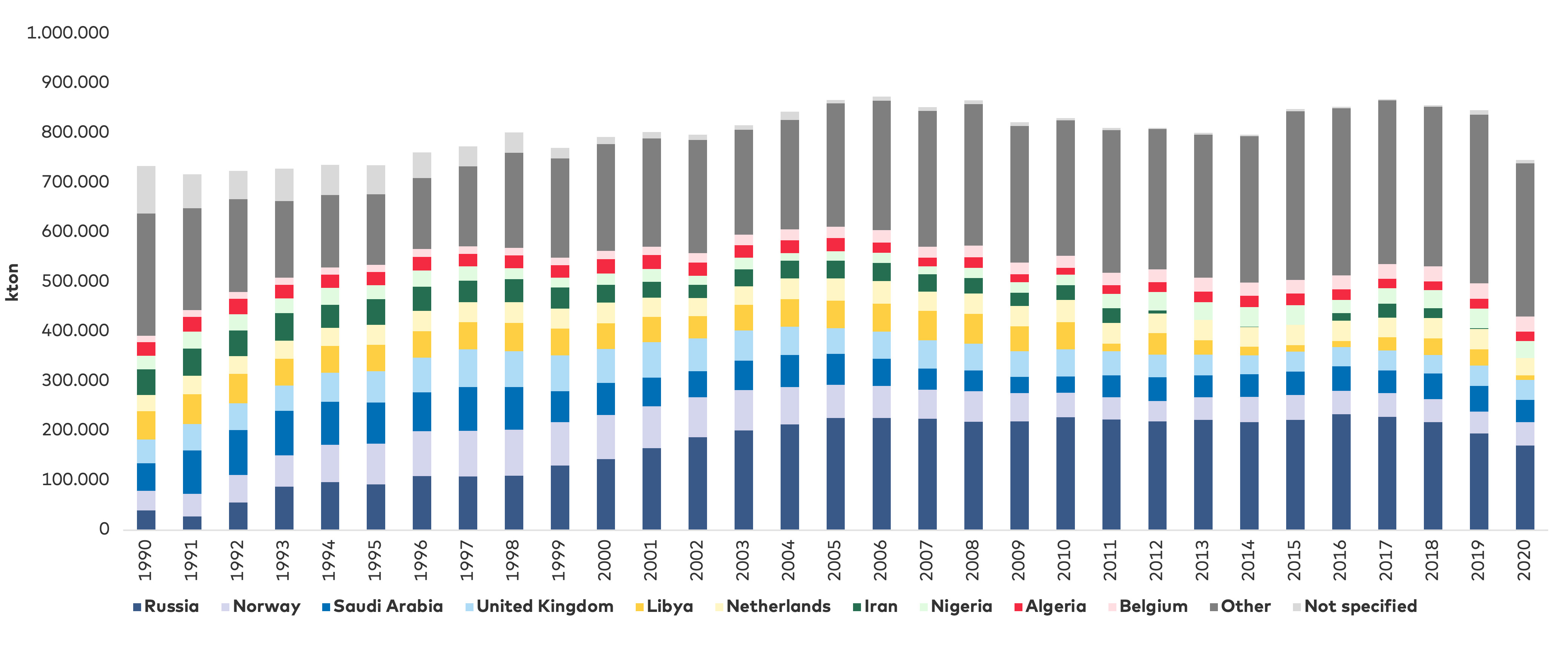

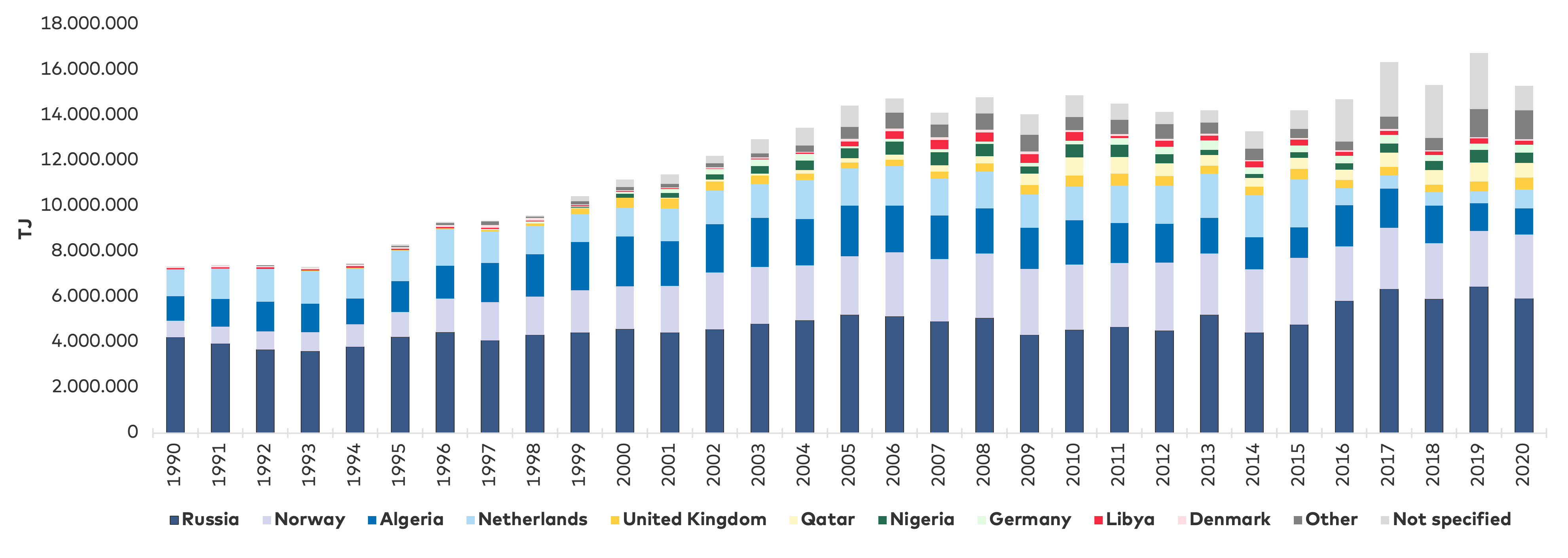

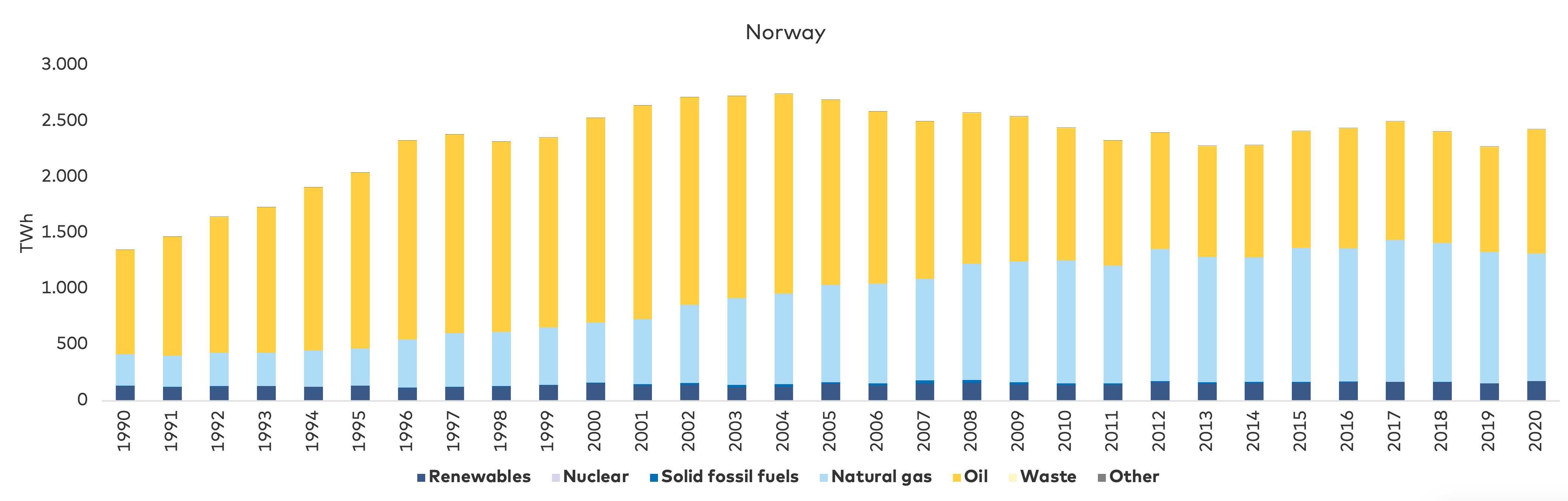

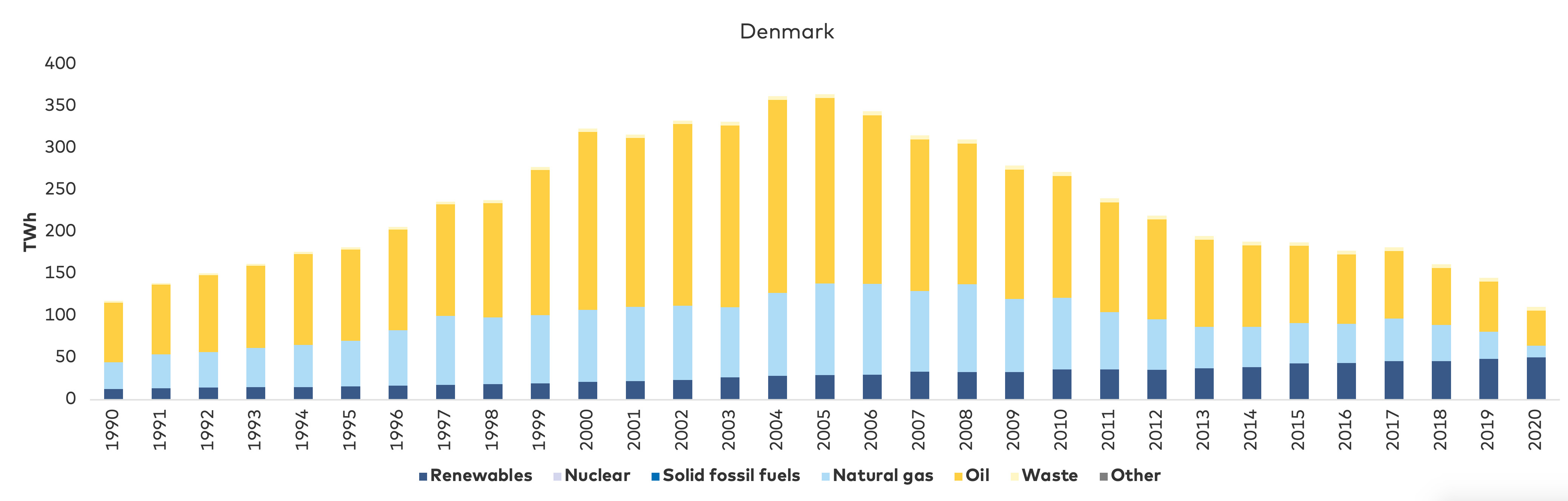

Norway is the largest producer of hydrocarbons within the Nordics. Denmark also produces hydrocarbons, albeit on a much smaller scale. A more comprehensive overview of the Nordic countries hydrocarbon activities based on data from 1990 to 2020 can be found in

Consequences

One consequence of underinvestment in natural gas production in the EU and a significant reduction in gas supplies from Russia is that power plants based on natural gas have been exposed to the historically high production costs impacting the electricity market. For example, in 2019 the decision was taken to close Europe’s largest natural gas field near Groningen in the Netherlands. Production was expected to cease in mid-2022, though this closure has since been postponed to 2023. Moreover, Denmark’s largest gas field, Tyra, will remain closed for redevelopment until 2023. Nonetheless, crisis management measures designed to increase the security of the natural gas supply have been implemented, including a requirement that natural gas storage facilities through LNG out-sourcing be filled to 80% capacity before the winter.

Following the reduction in natural gas supplies from Russia and within the EU, ENTSO-G concluded that the gas storage situation may well be worse in winter 2023–2024: “Without preparedness for Winter 2023–2024, the situation could deteriorate over the next gas year 2022–2023: storage facilities would be depleted in April 2023 and sites in Central and South-Eastern Europe would be less than 15% full on 1 October 2023, leaving the EU more exposed to risks of SoS in winter 2023–2024”[1].

Impact on the value chain

Lower natural gas production in the EU and a reduction in the supply of natural gas supplies from Russia have impacted the value chain through a lack of available natural gas as a primary energy source for storage and generation. This in turn has significantly affected both the natural gas and electricity price for end-consumers. Natural gas-fired power plants have been setting high electricity prices for many hours.

Footnotes

- ^ ENTSOG, Yearly Supply Outlook 2022/2023, 2022Website reference: https://www.entsog.eu/sites/default/files/2022-07/SO0036-22_Yearly_Supply_Outlook_2022-2023_2.pdf

FOCUS ON ICELAND

Not relevant as Iceland does not use natural gas.

5.9 Preparedness of the Nordic countries

| NO EFFECT | LOW | MEDIUM | HIGH | ||

| DRIVER | DENMARK | FINLAND | ICELAND | NORWAY | SWEDEN |