- Frontpage

- Contents

- Foreword

- Acknowledgements

- Executive Summary

- Chapter 1. Nordic Countries are Committed to Carbon Neutrality

- Chapter 2. Five Solution Tracks to Carbon Neutrality

- Chapter 3. Direct Electrification, the Central Pillar of Decarbonisation

- Chapter 4. Power-to-X: A Potential Game Changer for the Power Sector

- Chapter 5. The Important but Shifting Role of Bioenergy

- Chapter 6. Carbon Capture and Storage, and Negative Emissions are Essential

- Chapter 7. How Behaviour and Acceptance can Influence Future Energy Systems

- Chapter 8. A Case for Nordic Collaboration and the Nordic's Role in the European Transition

- Chapter 9. Not Everything is Uncertain: Robust Results Across all NCES Scenarios

- Annex A. Flexibility Needs and Solutions in the NCES Scenarios

- Annex B. Nuclear Electricity Could Play a Long-Term Role, But is Unlikely to be a Dealbreaker

- Abbreviations

- References

- About this publication

MENU

Foreword

The Nordic countries have a unique and long-standing cooperation on energy, which has created a solid foundation for a sustainable and secure energy supply in the region. Now, it is time to further Nordic energy cooperation with the green transition as a new framework.

When the Nordic Prime ministers signed the joint Declaration on Nordic Carbon Neutrality in January 2019 – committing themselves to work towards carbon neutrality – Nordic Energy Research recognised the need for a publicly available research-based analysis, to gather Nordic perspectives on national and regional energy systems, and complement the ongoing work in each country.

Nordic Clean Energy Scenarios aim to identify and help prioritise – through scenario modelling – the necessary actions up to 2030 and map potential long-term pathways to carbon neutrality, and thereby support the joint Declaration on Carbon Neutrality. This work is both timely and important, considering that energy-related emissions make up almost four-fifths of Nordic emissions today.

This project guides you through the Nordic energy system and illustrates how the Nordic countries can achieve the Nordic Vision 2030, to become the most sustainable and integrated region in the world, and make the green transition towards carbon neutrality a reality.

The project builds on earlier Nordic Energy Research efforts. The Nordic Energy Technology Perspectives reports were published in 2013 and 2016 and drew on the best available knowledge at the time. However, the rapidly changing landscape of the energy sector has seen cost declines for energy technologies that were unimaginable a few years ago, while ambitions to curb climate change have risen around the world. These developments have changed the prospects for certain technologies and the energy system, highlighting the need for an updated analysis.

While previous reports analysed added costs and changes incurred from increased climate ambitions, the three Nordic Clean Energy Scenarios presented here reach carbon neutrality through different technological and societal pathways, illustrating how political choices can shape the future of the Nordic energy system.

However, important questions remain:

Will the necessary changes to achieve the current national plans, strategies, and targets, as described in the Carbon Neutral Nordic scenario be realised?

Will the Nordic countries have a greater role in the European energy transition, by providing carbon storage, and clean electricity and fuels, as envisioned in the Nordic Powerhouse scenario?

Will Nordic countries pursue additional energy and material efficiency across all sectors, and lower demand for energy services, as outlined in the Climate Neutral Behaviour scenario?

Klaus Skytte, CEO, Nordic Energy Research

It is likely we will see neither of the extremes, but rather a combination of all scenarios. This project shows the possibilities and potential barriers that lie ahead on the road to Nordic carbon neutrality.

Klaus Skytte

Acknowledgements

Nordic Clean Energy Scenarios –Solutions for Carbon Neutrality is a collaborative project between Nordic Energy Research who funded the project and is carried out by a Nordic team of researchers and consultants lead by Energiforsk.

Kevin Johnsen and Christian Kjaer at Nordic Energy Research were the coordinators of the project.

Markus Wråke (Energiforsk) was the overall project manager, Kenneth Karlsson (IVL) scientific manager, and Madelene Danielzon Larsson (Energiforsk) coordinated the design and drafting of the report.

Team at Nordic Energy Research

Kevin Johnsen

Senior Adviser

kevin.johnsen@nordicenergy.org

Christian Kjaer

Senior Adviser

Research and consultant team

Energiforsk

Markus Wråke, Project Manager

Madelene Danielzon Larsson, Project Coordinator

EA Energy Analyses

Anders Kofoed-Wiuff, Work Package Leader, Technology Catalogue & Balmorel

Andrea Pasquali, Modeller Balmorel, Technology Catalogue

Victor Duus Svensson, Modeller Balmorel

János Hethey, Modeller Balmorel

Energy Modelling Lab

Kenneth Karlsson, Scientific Manager

Mikkel Bosack Simonsen, Modeller ON-TIMES

Till Ben Brahim, Modeller ON-TIMES

IVL Swedish Environmental Research Institute

Kenneth Karlsson, Scientific Manager

Burcu Unluturk, Modeller ON-TIMES

Christin Liptow, Energy Technology Expert

Sofia Klugman, Energy Technology Expert

Norwegian University of Life Sciences

Torjus Folsland Bolkesjø, Work Package Leader, Project Scoping

Yi-kuang Chen, Literature Reviewer

Eirik Ogner Jåstad, Co-author & Model Results Reviewer

Jon Gustav Kirkerud, Model Results Reviewer

Profu

Martin Hagberg, Co-author Model Results Reviewer

Thomas Unger, Model Results Reviewer

Thema

Berit Tennback, Co-author & Model Results Reviewer

Anders Lund Eriksrud, Model Results Reviewer

Tøkni

Olavur Ellefsen, Webtool Developer

Bo Lærke, Webtool Developer

VTT Technical Research Centre of Finland

Tomi J. Lindroos, Co-author & Modeller ON-TIMES

Antti Lehtilä, Modeller ON-TIMES

Erkka Rinne, Work Package Leader, NCES Database

Tiina Koljonen, Work Package Leader, Framework Conditions

Nelli Putkonen, Literature Reviewer

Jiangyi Huang, Data collection NCES database

Steering group and funding body

The work was guided by a steering group, composed of:

-

Klaus Skytte, Nordic Energy Research

-

Jón Ásgeir Haukdal Þorvaldsson, Orkustofnun, Iceland

-

Jarmo Heinonen, Business Finland, Finland

-

Benjamin Donald Smith, The Research Council of Norway, Norway

-

Hanne Thomassen, Energistyrelsen, Denmark

-

Lars Guldbrand, Infrastrukturdepartementet, Sweden

The individuals and organizations that contributed to this study are not responsible for any opinions or judgements contained in this study.

Contact

Comments and questions are welcome and should be addressed to:

Kevin Johnsen, Nordic Energy Research, e-mail: kevin.johnsen@nordicenergy.org

For enquiries regarding the presentation of results or distribution of the report, please contact Nordic Energy Research.

Additional materials, press coverage, presentations etc. can be found at nordicenergy.org.

Nordic Clean Energy Scenarios in ten Messages

In 2019, the Nordic countries signed a joint Declaration on Carbon Neutrality, committing to make the Nordic countries carbon neutral, in line with the COP21 Paris Climate Agreement. To support this commitment, Nordic Energy Research commissioned the Nordic Clean Energy Scenarios project (NCES). The aim of this project is to identify and help prioritise, through scenario modelling, which actions will be necessary by 2030 and to map potential long-term pathways to carbon neutrality.

Current approaches, including underlying policy measures, have not delivered the required rate of change. Compared with the previous decade, the rate of emission reductions must increase fivefold. The transformation challenge is immense and a great deal of uncertainty remains, including how to strike a balance between what may be cost-effective and what will be politically, socially, and environmentally acceptable.

Across ten areas, the NCES analysis reveals robust results that identify no-regret actions that can be implemented in the near-term to set a strong foundation for achieving carbon neutrality.

Three scenarios show different pathways to carbon neutrality

The NCES project developed three scenarios, all designed to meet the carbon neutrality target by balancing carbon emissions and sinks. While acknowledging the importance of cost-effectiveness, the analytical approach recognised that considering only this criterion is too narrow in scope for policy planning and decision-making. As such, the NCES analysis seeks to balance multiple factors that will influence outcomes. Each of the three scenarios reflects a different core element:

- Carbon Neutral Nordic (CNN) seeks the least-cost pathway, taking into account current national plans, strategies, and targets.

- Nordic Powerhouse (NPH) explores the opportunity for the Nordics to play a larger role in the broader European energy transition by providing clean electricity, clean fuels, and carbon storage.

- Climate Neutral Behaviour (CNB) reflects Nordic societies adopting additional energy and material efficiency measures in all sectors, ultimately leading to lower demand for both.

Message

one

Nordic industry and transport are transformed, supported by clean electricity and decarbonised fuels

Driven by changes in industry and transport, the supply of energy to the Nordic countries is radically transformed in all NCES scenarios (Figure ES.1); as a result, carbon dioxide (CO2) emissions decline by 95% (Figure ES.2). Decisive action that facilitates clean electricity supply, supports sector coupling, and accelerates energy technology research and innovation can deliver this outcome. Wind power is central to the transition, enabled by large Nordic wind resources and supported by flexibility in hydropower reservoirs as well as successful efforts to enhance additional flexibility of the Nordic energy system (Figure ES.3). Clean electricity is a critical enabler of decarbonisation of industry and transport.

Message

two

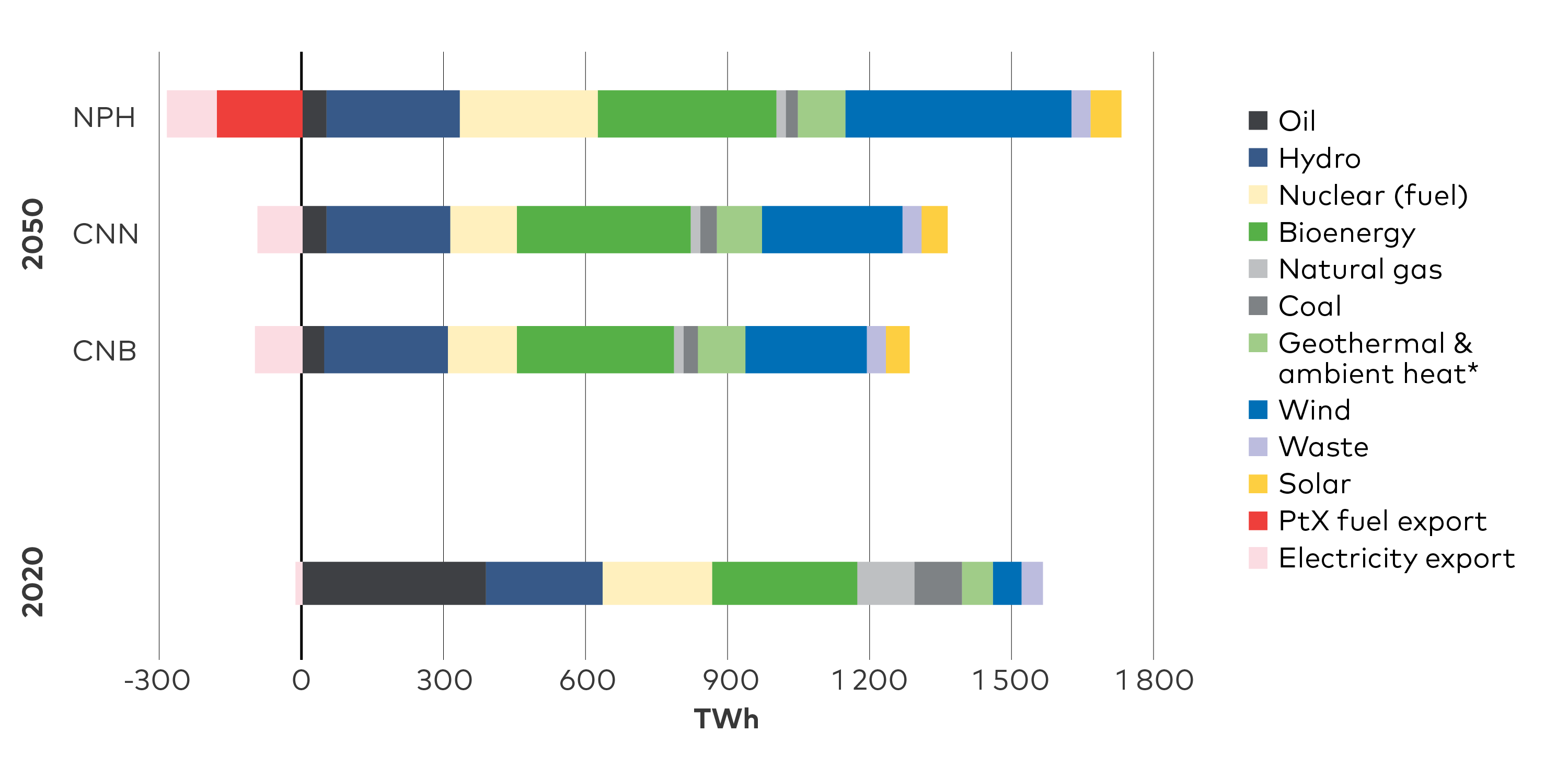

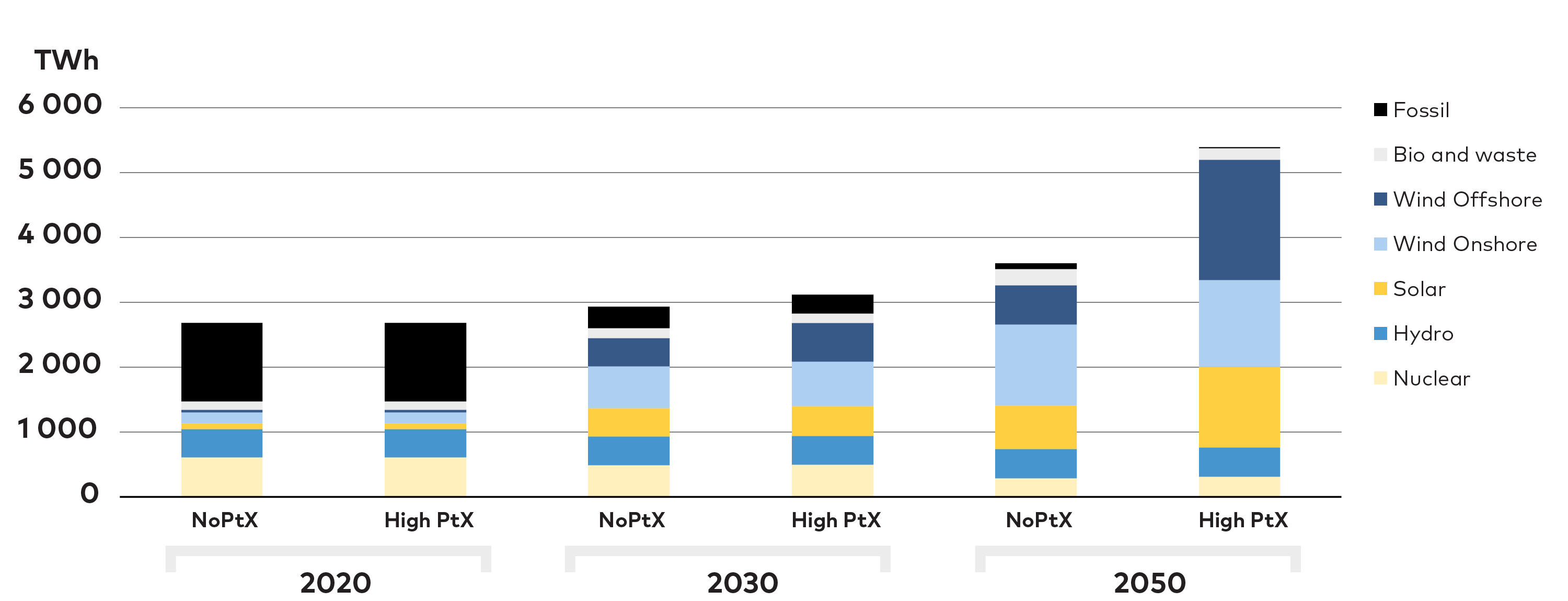

Figure ES.1. Nordic total primary energy supply in the NCES scenarios. In the NCES scenarios, the share of fossil fuels in Nordic total primary energy supply falls from 42% in 2020 to 6-9% in 2050. In parallel, export rises of electricity and power-to-X fuels, such as hydrogen or ammonia. Exports to non-Nordic countries are displayed as negative values. *Includes minor contribution from other sources.

Figure ES.2. Nordic energy-related CO2 emissions - CNN scenario. Action is needed to rapidly reduce CO2 emissions. In the CNN scenario, compared to the past decade, the rate of emissions reduction must increase fivefold.

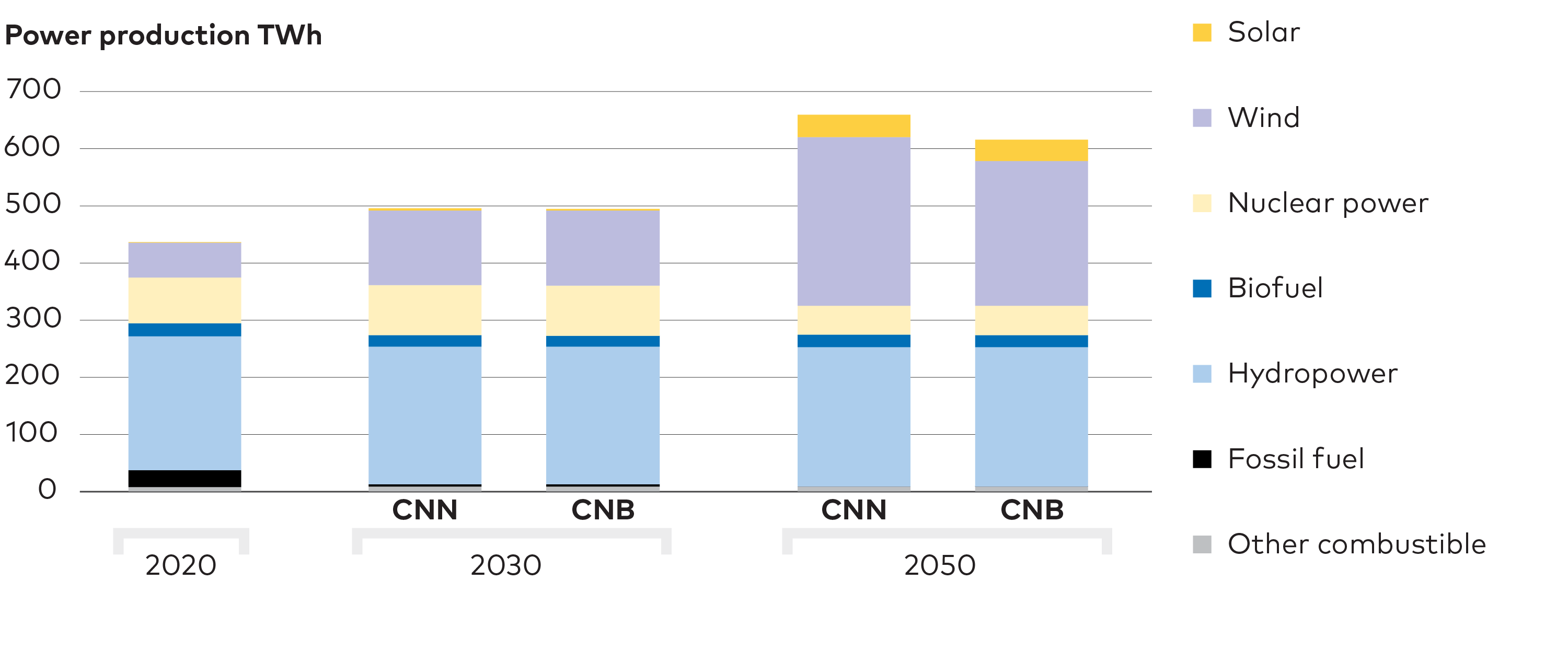

Figure ES.3. Nordic electricity generation in 2020 and the NCES scenarios. Wind power dominates new electricity investments in the NCES scenarios while the share of fossil fuels falls to below 5% by 2050 in all scenarios. This pattern is constant even as generation increases substantially from 455 TWh in 2020 to 650 TWh (CNB), 690 TWh (CNN) and 950 TWh (NPH) in 2050.

Five solution tracks towards carbon neutrality emerge in the NCES scenarios

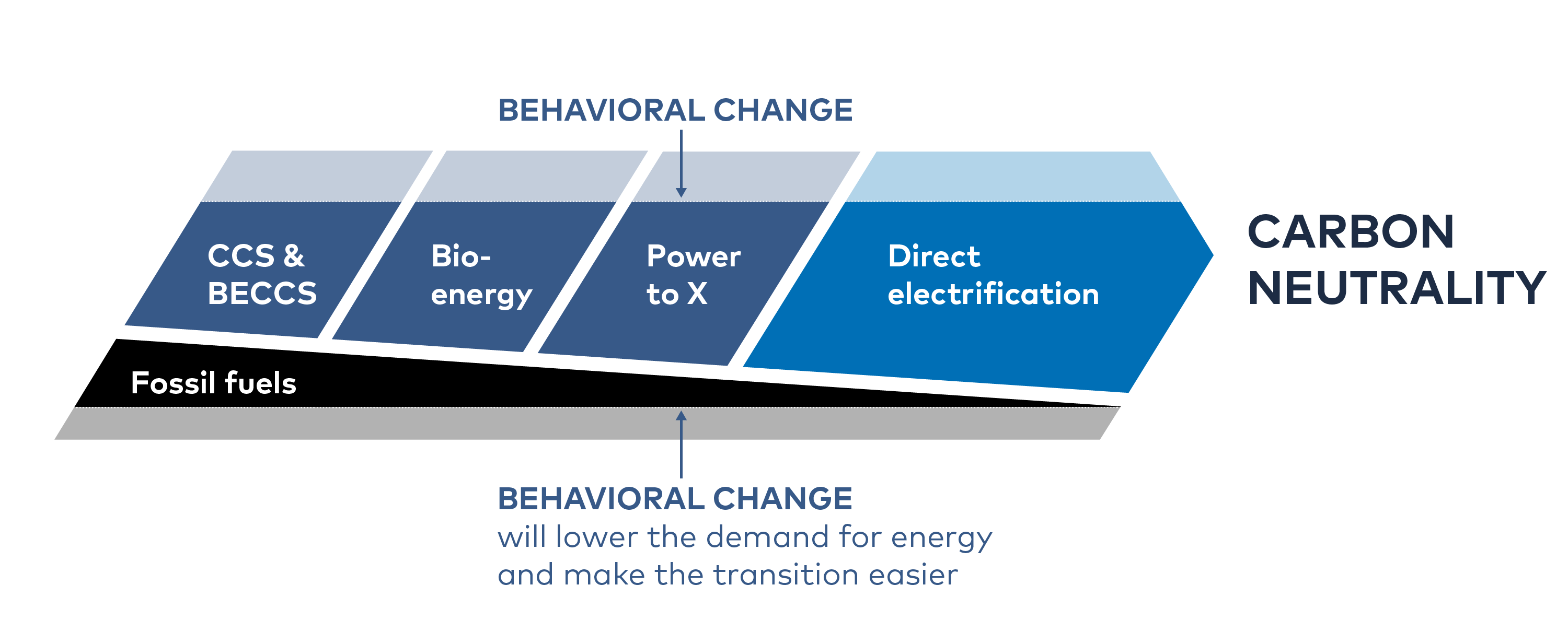

Five solution tracks capturing a majority of available mitigation options emerge from the analysis: direct electrification; power-to-X (PtX fuels); bioenergy; carbon capture technologies (CCS) including in combination with bioenergy (BECCS); and behavioural change (Figure ES.4). While direct electrification is at the core of all scenarios, a decarbonisation pathway that balances elements of all five solution tracks to accommodate national contexts will likely be easier to realise than a route completely dominated by any one set of solutions.

Message

three

Figure ES.4. Five solution tracks contribute to Nordic clean energy scenarios. Five solution tracks emerge from the analysis. Direct electrification forms the core of all scenarios, complemented by three other technology tracks: PtX, bioenergy and CCS technologies. Behavioural change will influence any pathway chosen.

Direct electrification is central to all decarbonisation strategies

Direct electrification of end-use sectors is central to all NCES scenarios. It implies clean electricity directly substituting fuel combustion, for instance in transportation, heating, or industrial processes. In addition to reducing emissions, direct electrification can dramatically improve energy efficiency. With strong electricity grids and large hydropower reservoirs, the Nordic region is well-positioned to leverage the falling costs of renewable electricity generation to accelerate deployment of electric end-use technologies.

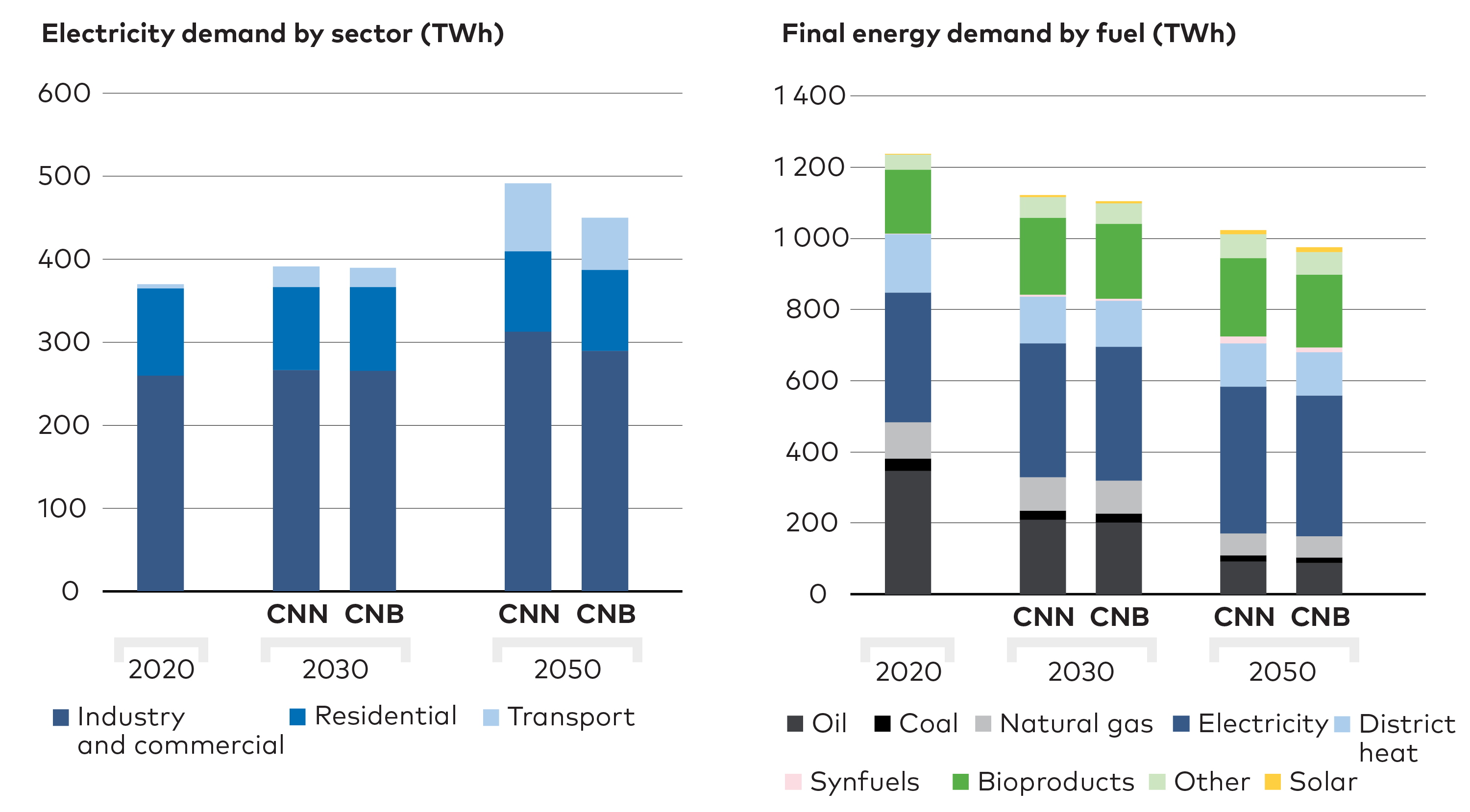

Electricity’s share of final energy consumption rises from around 30% in 2020 to 50% by 2050, and Nordic electricity demand increase by 40-100% across the scenarios (Figure ES.5). NCES analysis shows direct electrification gaining traction in applications that seemed out of reach only five years ago, including heavy-duty road transport and even some aviation, which would reduce pressure on bioresources.

Direct electrification is no panacea, however. In applications that require high temperatures, high energy density in storage, or high energy flow rates electrification has limitations and other solution tracks play crucial roles to fill the gaps.

Message

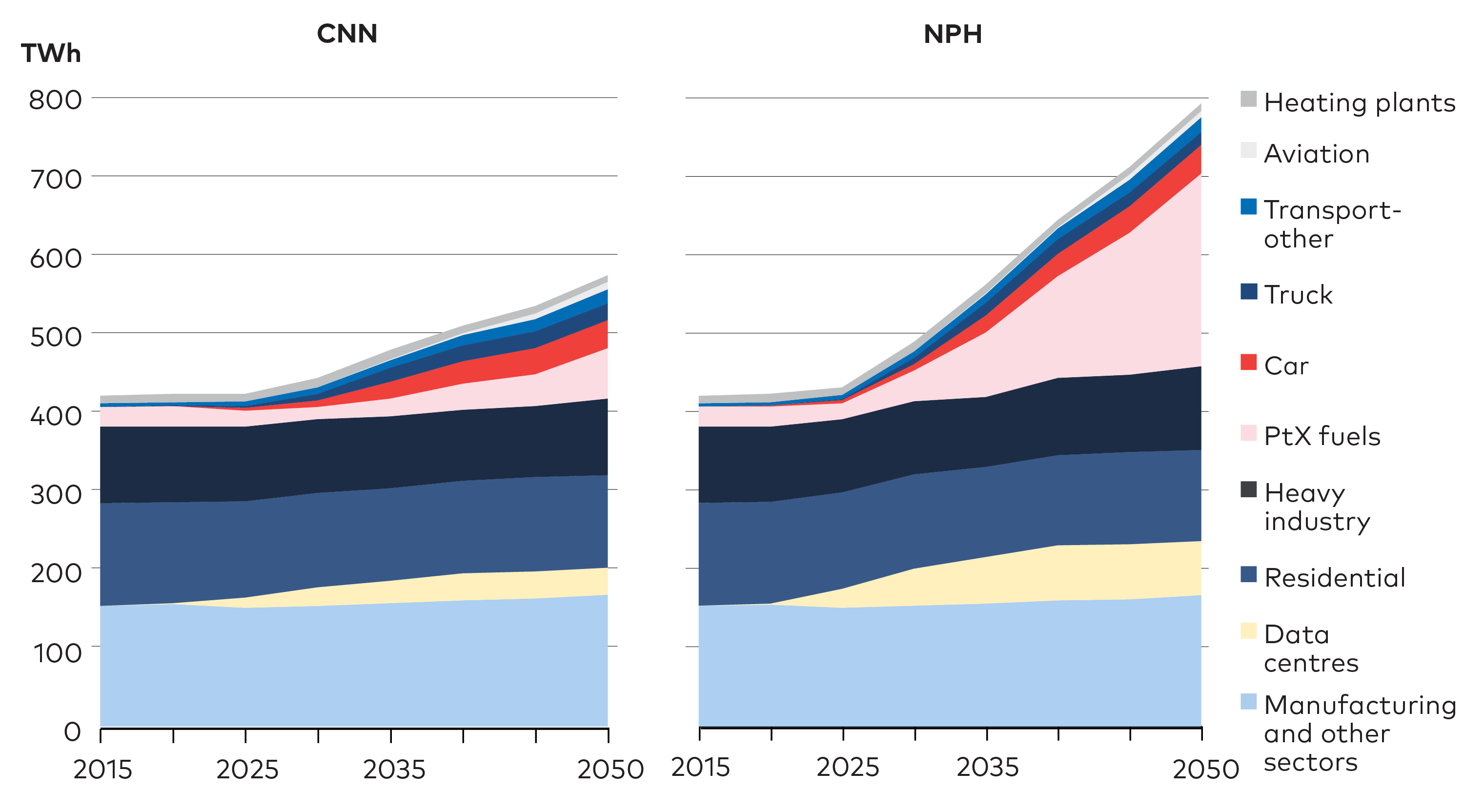

four

Figure ES.5. Projected growth in Nordic electricity demand. Nordic electricity demand grows in all NCES scenarios, with transport and PtX fuels being the main drivers. From 390 TWh in 2020 to about 535 TWh (CNN) and 760 TWh (NPH) in 2050.

Three no-regret actions for direct electrification:

-

Roll out vehicle charging infrastructure and continue incentivising electric vehicles (EVs); over time, shift the focus from personal EVs towards heavier vehicles.

-

Replace fossil boilers and direct electric household heating with heat pumps.

-

Ensure that regulation supports use of waste heat from industry, data centres, and other sources.

Power-to-X: A potential game-changer with profound impact on the Nordic power sector

Using hydrogen or synthetic methane produced through electric processes (PtX) offers some specific advantages over direct electrification. PtX fuels can deliver higher energy flow rates, lower-weight storage, and often higher temperatures, making them strong contenders to replace fossil fuels in industry and transport. PtX can also provide flexibility to the energy system, for example by adjusting production to fluctuations in electricity generation and prices. Finally, transporting PtX fuels can be less costly per kWh than transporting electricity, especially over long distances.

Nevertheless, the least-cost scenario (CNN) foresees only a modest Nordic demand for PPtX fuels, below 50 TWh in 2050, mainly because they are significantly more energy intensive than direct electrification as a decarbonisation option.

Message

five

However, strong arguments support pathways that emphasise the PtX solution track. Competition with direct electrification is close in some cases; should bioenergy become scarcer and more expensive than assumed in the scenarios, PtX would become more competitive. In addition, the EU is pursuing an aggressive hydrogen strategy and industry projects are already underway that could dramatically increase demand for hydrogen.

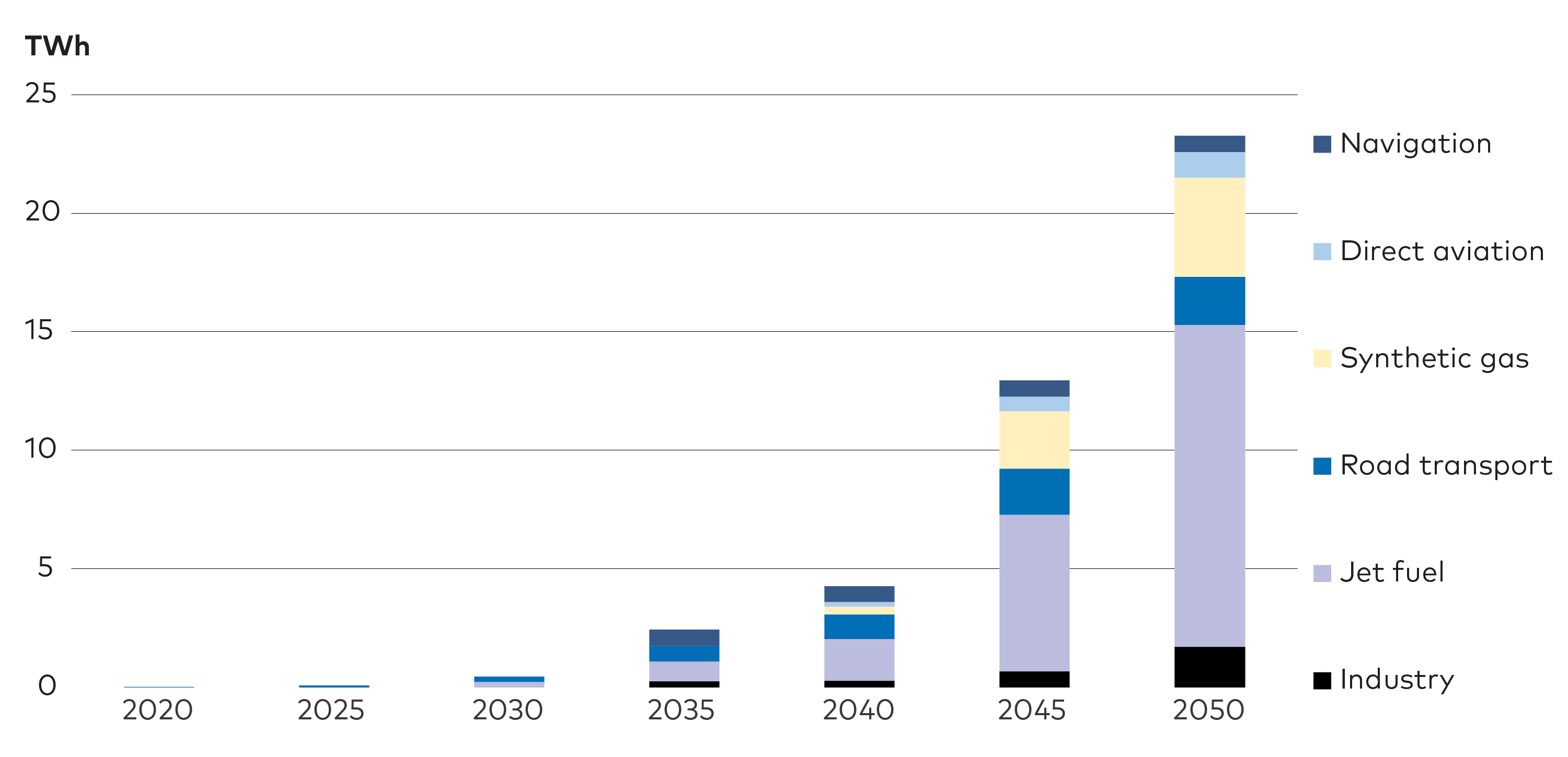

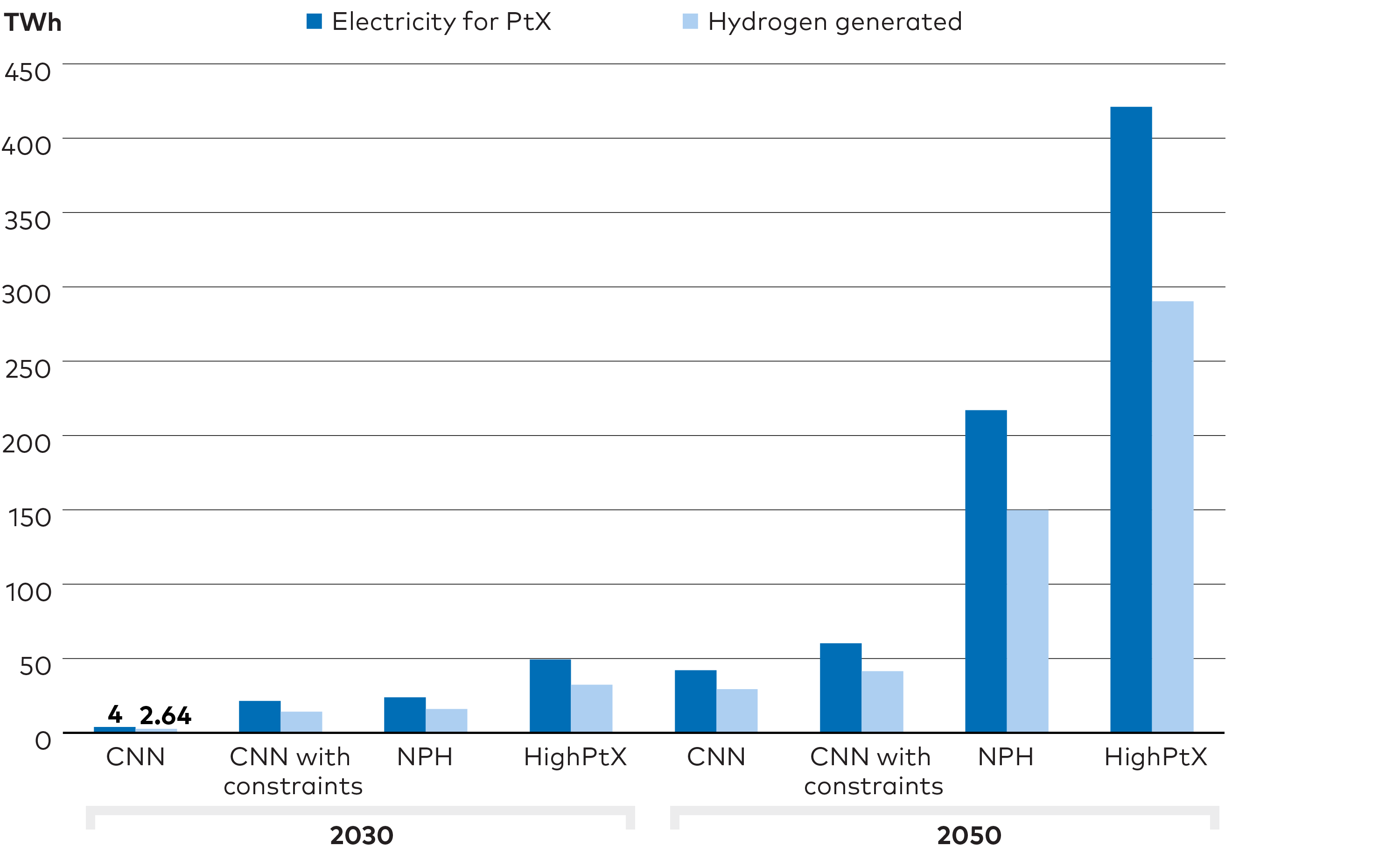

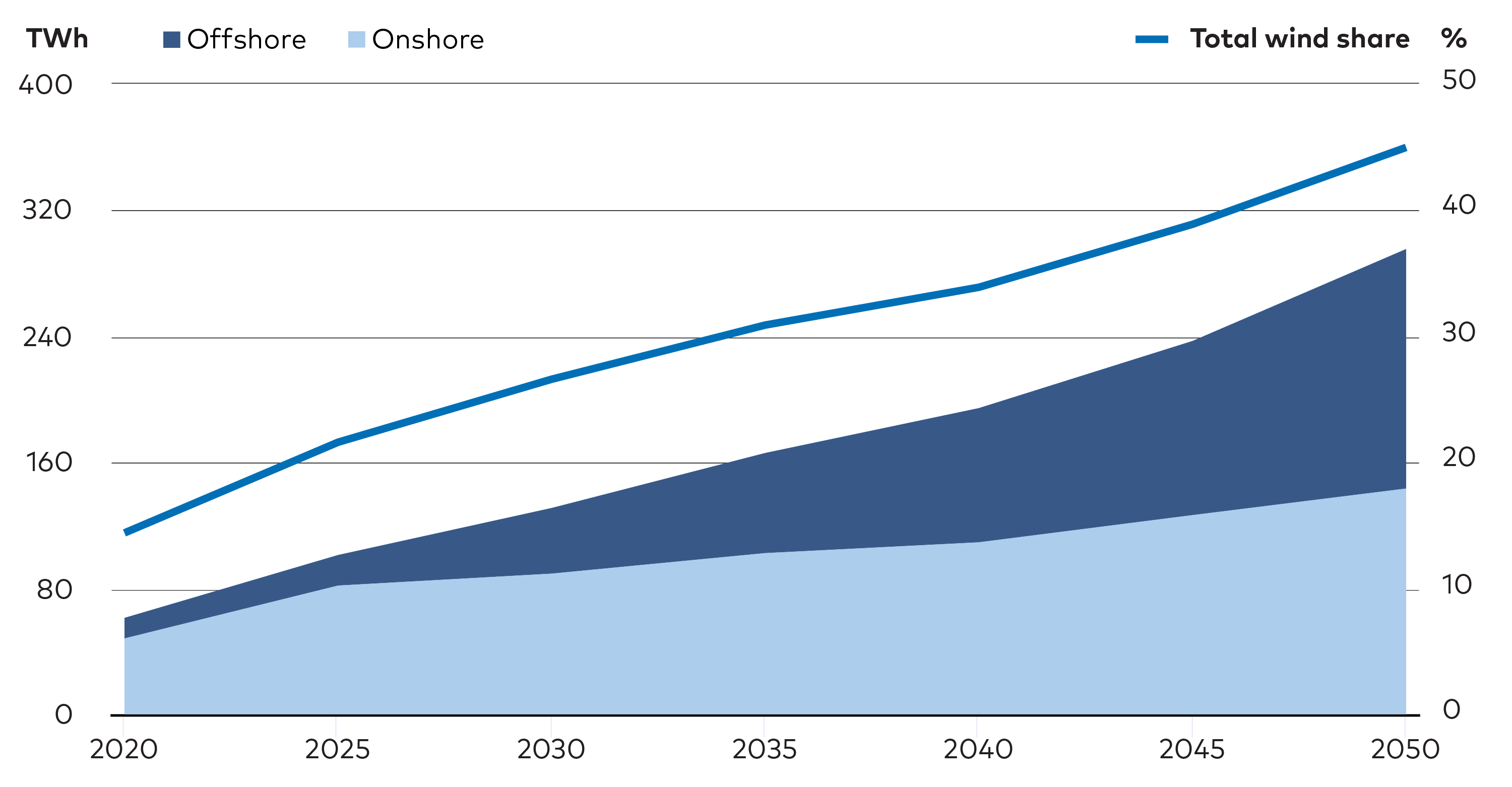

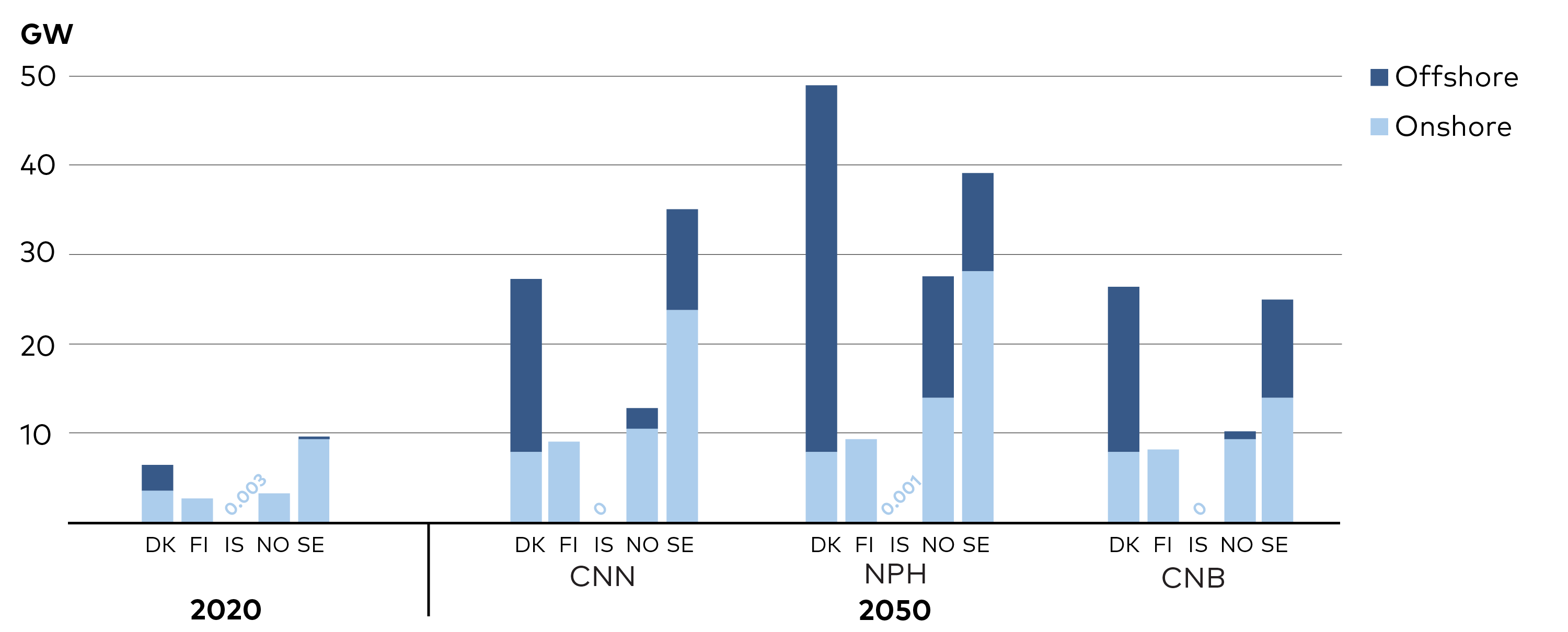

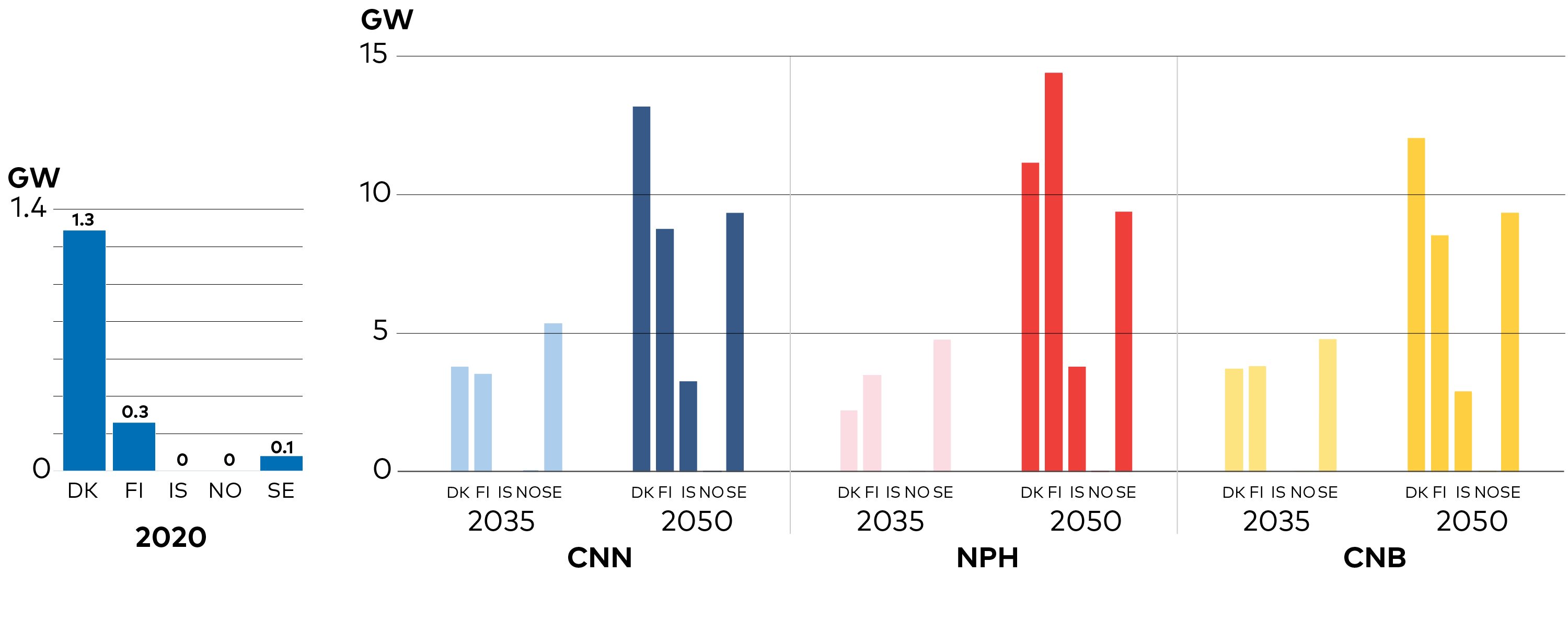

The NPH scenario shows Nordic hydrogen production reaching 135 TWh in 2050, requiring more than 20% of total Nordic electricity generation. Cases assuming higher European demand results in Nordic hydrogen production levels around 300-500 TWh/year (Figure ES.6).

NCES analysis shows that the potential development of PtX production will have major implications for the Nordic energy transition. For instance, fulfilling the Nordic PtX fuel export potential could require a tripling of Nordic power generation compared to current levels (Figure ES.6). Finally, producing hydrogen from fossil fuels combined with CCS, so-called blue hydrogen, should not be dismissed.

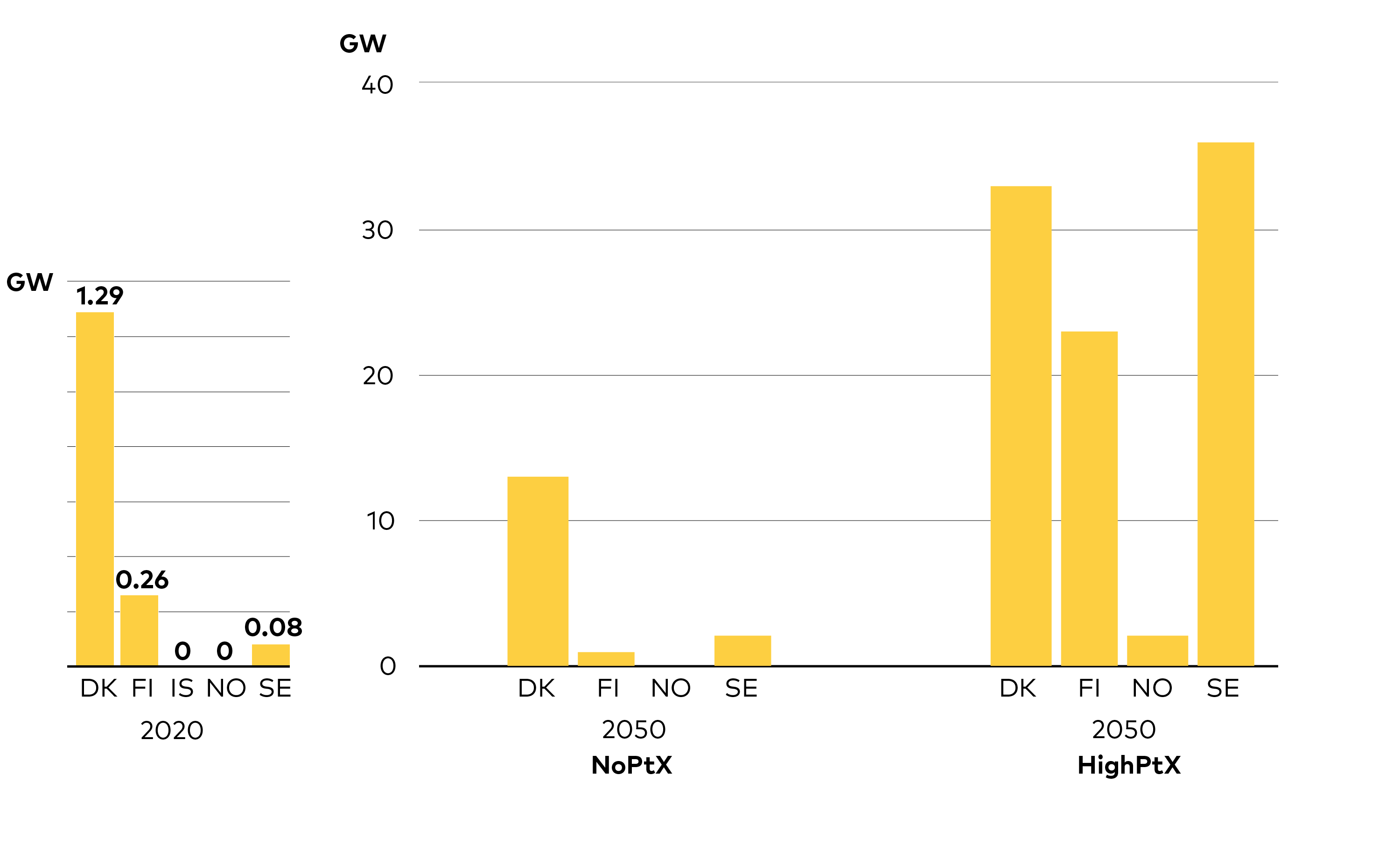

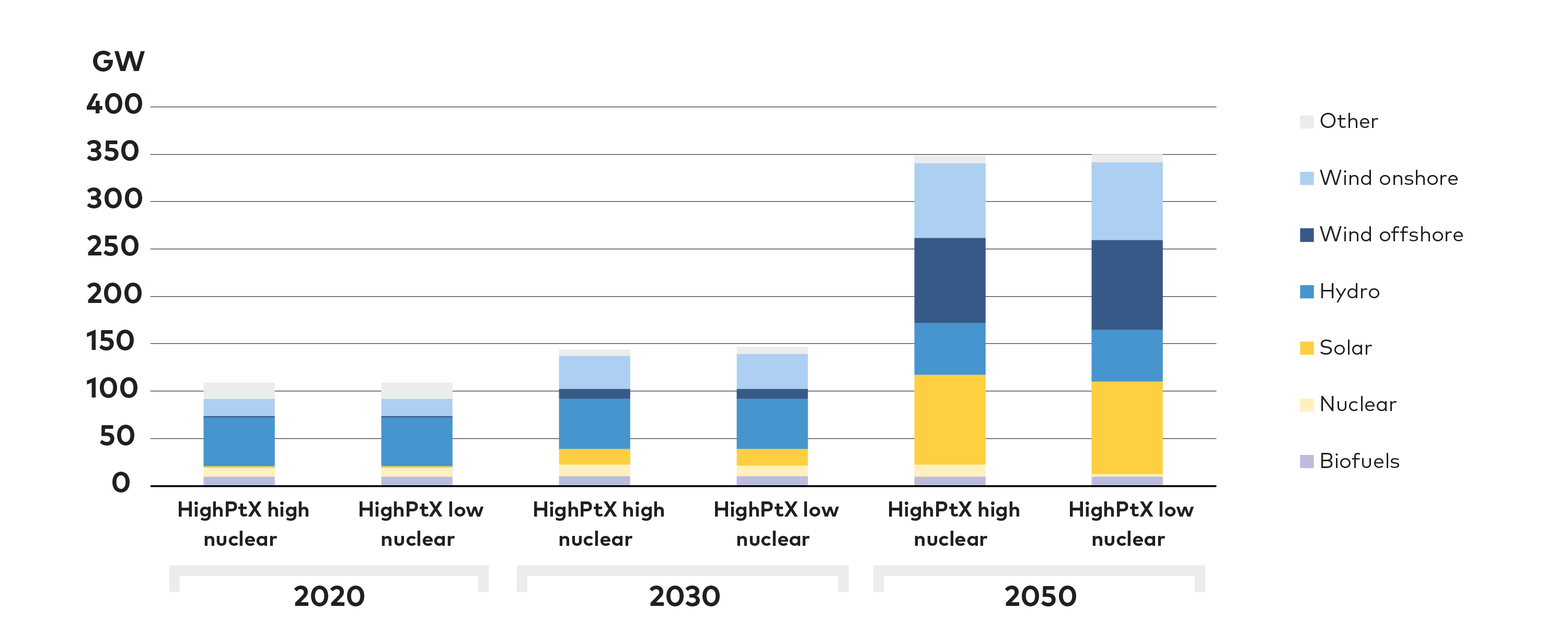

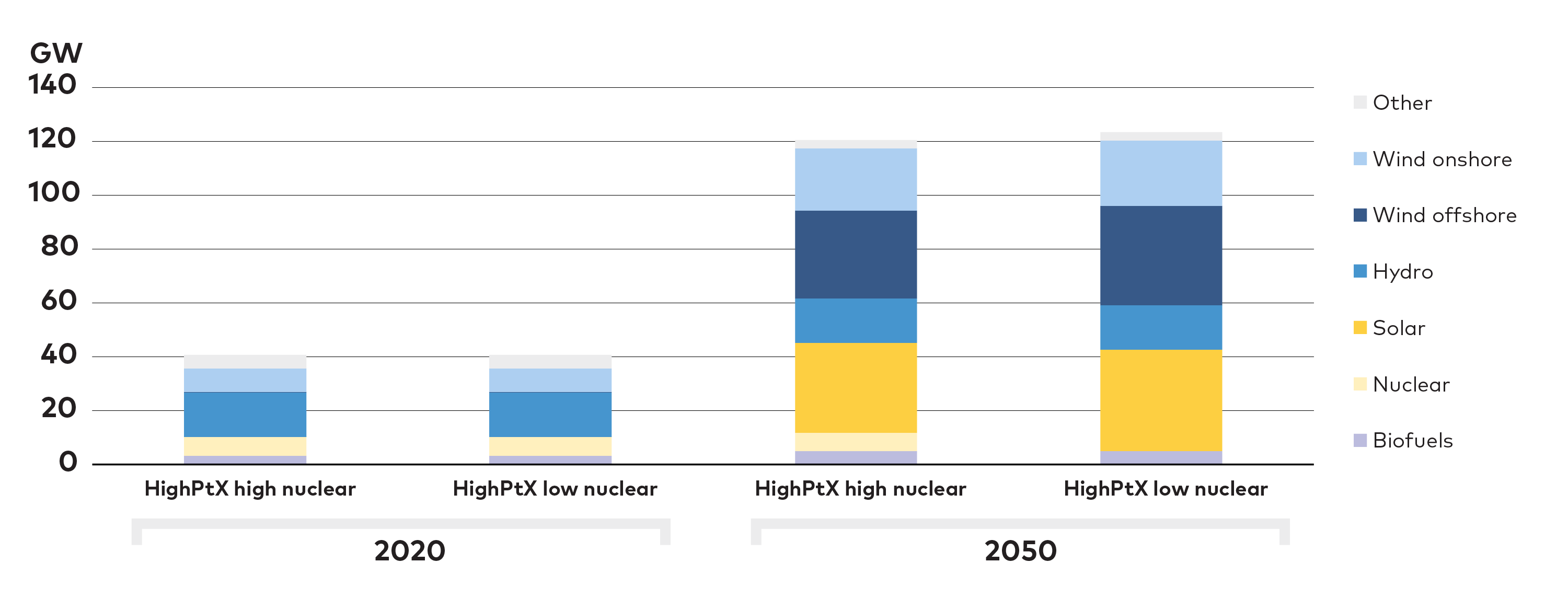

Figure ES.6. Nordic power generation in No, High, and Very High PtX cases, except Iceland. Hydrogen production is a major driver of Nordic power demand. The left panel shows total Nordic electricity generation, the right panel shows hydrogen production in 2050 and associated power demand. Increasing demand for PtX fuels in Europe creates incentives for Nordic countries to scale up power generation, potentially by more than a factor of three by 2050. Wind power, both onshore and offshore, and solar power supply this increase.

Three no-regret actions for PtX:

-

Demonstrate PtX technologies in real operating environments.

-

Strategically locate PtX production and RE refineries in proximity to strong power grids and district heating networks to minimise infrastructure cost and maximise energy efficiency.

-

Develop a roadmap for a Nordic hydrogen infrastructure that considers both green and blue hydrogen.

Bioenergy remains important, but with a shifting role

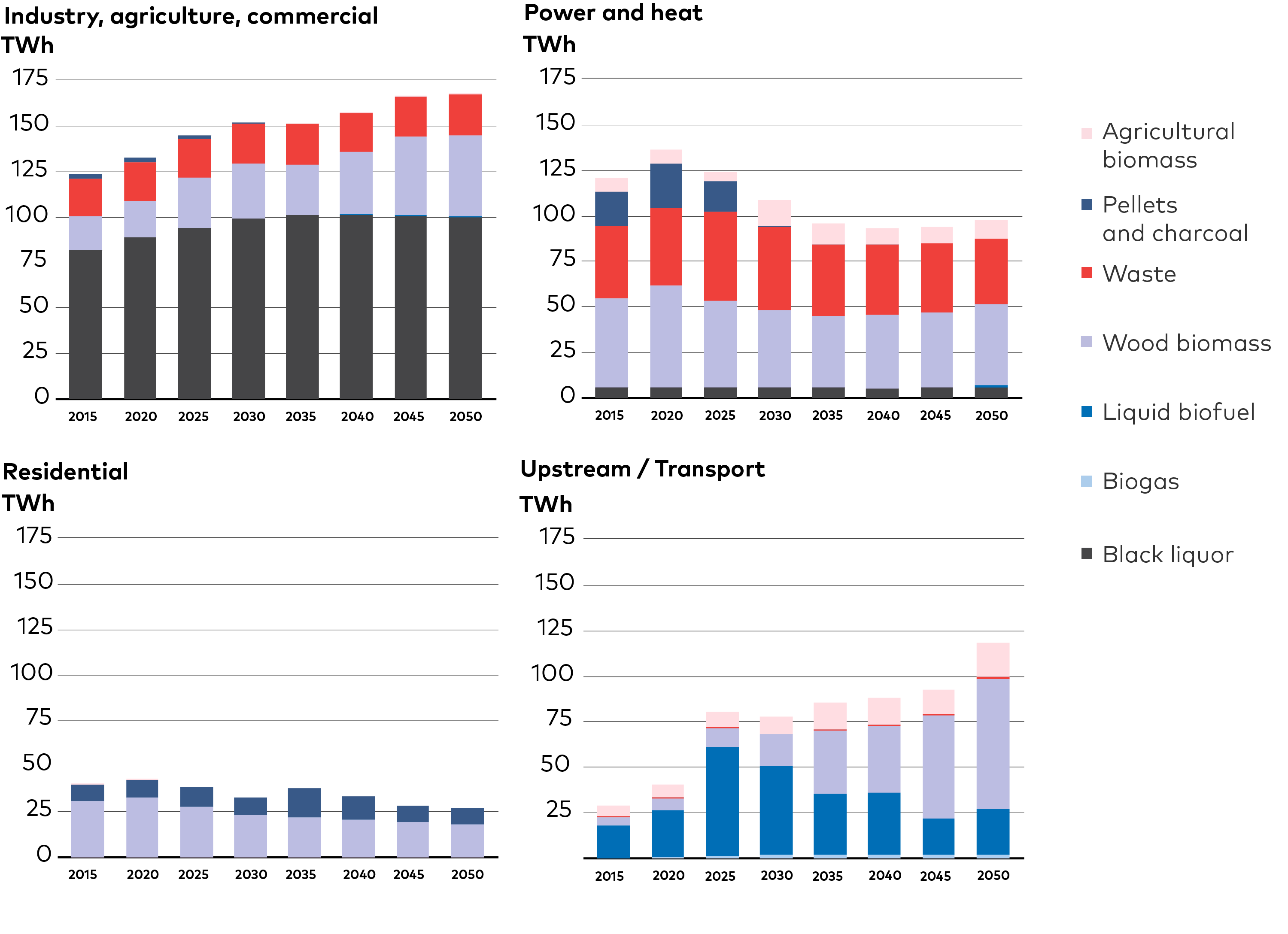

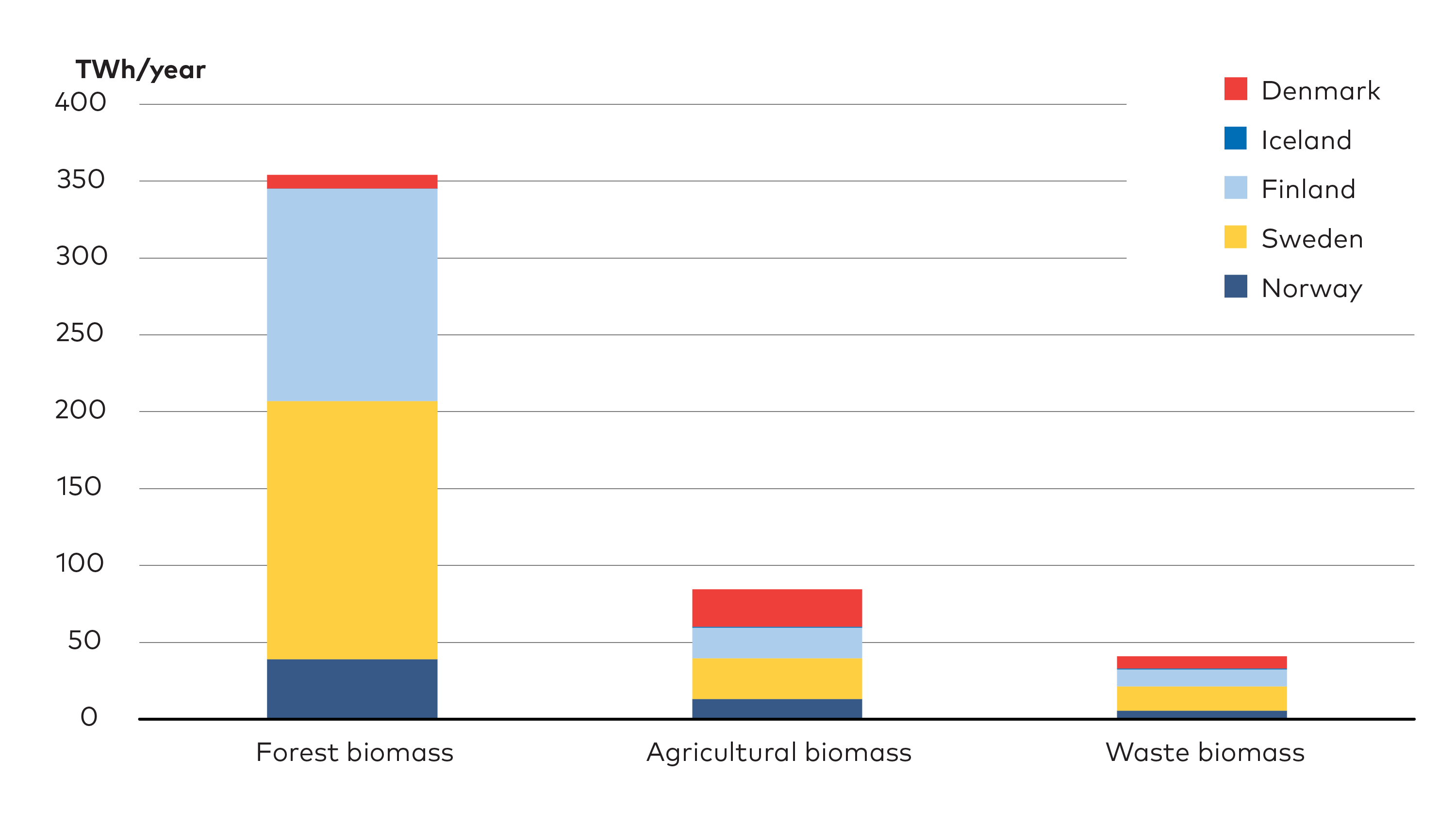

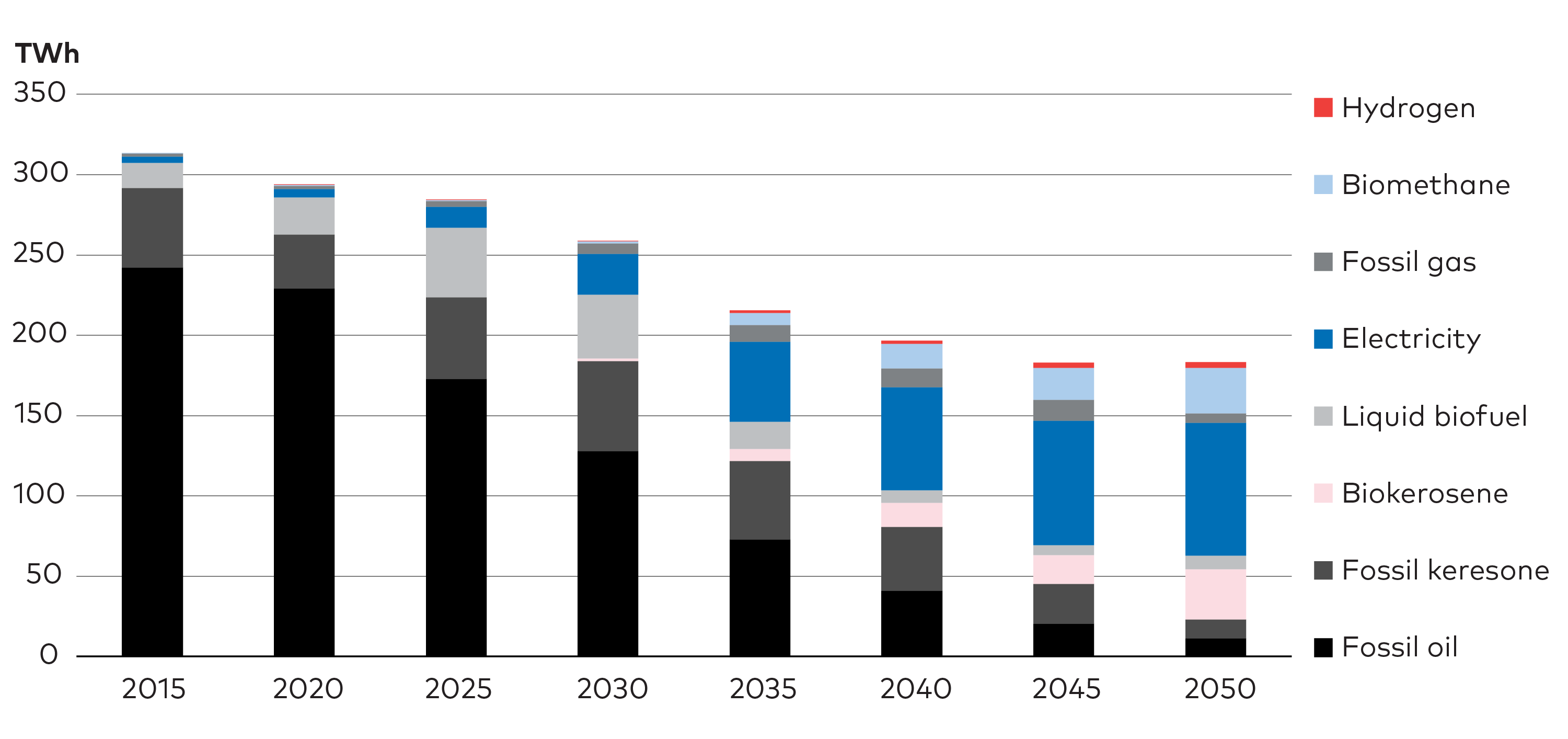

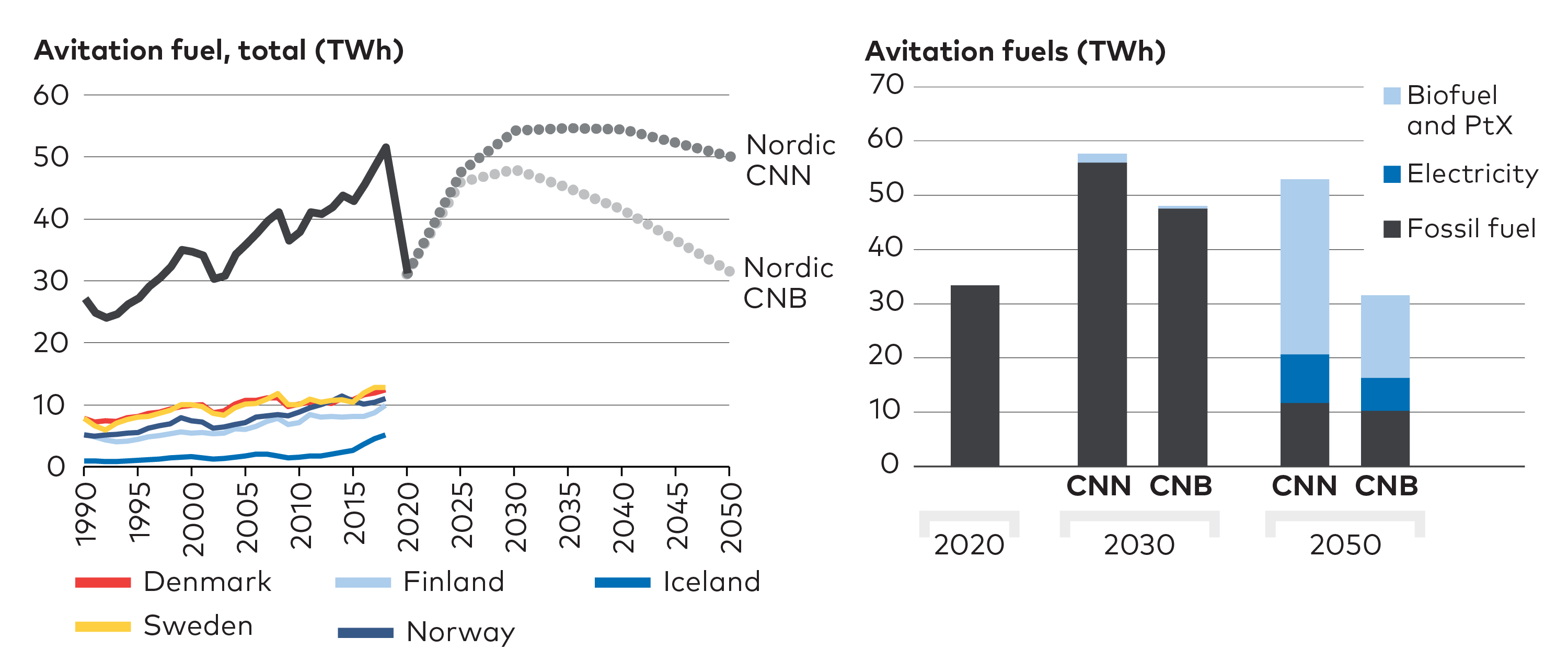

Bioenergy already plays an important role in Nordic energy systems, used extensively in district heating or as ‘drop-in’ fuels in transport and continues to do so in all NCES scenarios. Capable of being used directly or converted into other solid or liquid fuels, it shares advantages with PtX in versatility and potential to directly substitute fossil fuels. Towards 2050, in parallel with electrification, the use of biomass should, however, shift to increasingly be utilised in hard-to-abate sectors such as heavy transport, steel, and cement (Figure ES.7).

Message

six

Figure ES.7. Nordic bioenergy demand - CNN scenario. Nordic bioenergy use remains high towards 2050, with transportation and industry driving the increase in demand.

Producing synthetic fuels through the bioenergy route is currently less costly than through PtX; but fossil fuels and first-generation biofuels are cheaper still. Considering expected advances in electrification and other technologies for sustainable fuel production, progress in biorefinery technologies must accelerate to remain competitive even as fossil fuel and first-generation biofuels are phased out. In particular, production processes for advanced biofuels, such as gasification or pyrolysis, will require further development.

In the NCES scenarios, growth in demand for bioenergy is lower than in several previous Nordic scenario studies. As the sustainability of bioenergy is already a topic of concern and land-use pressure is increasing in most parts of the world, the NCES scenarios might thus be less challenging to realise than previous scenarios.

Three no-regret actions for bioenergy:

-

Ensure that mainly waste, wood waste, and forest industry residues are used for bioenergy applications.

-

Ensure adequate biofuel blending requirements in the Nordic countries, including increased mandates for advanced biofuels.

-

Increase and prioritise efforts to produce fossil free aviation fuels.

Carbon capture and storage, and negative emissions are essential

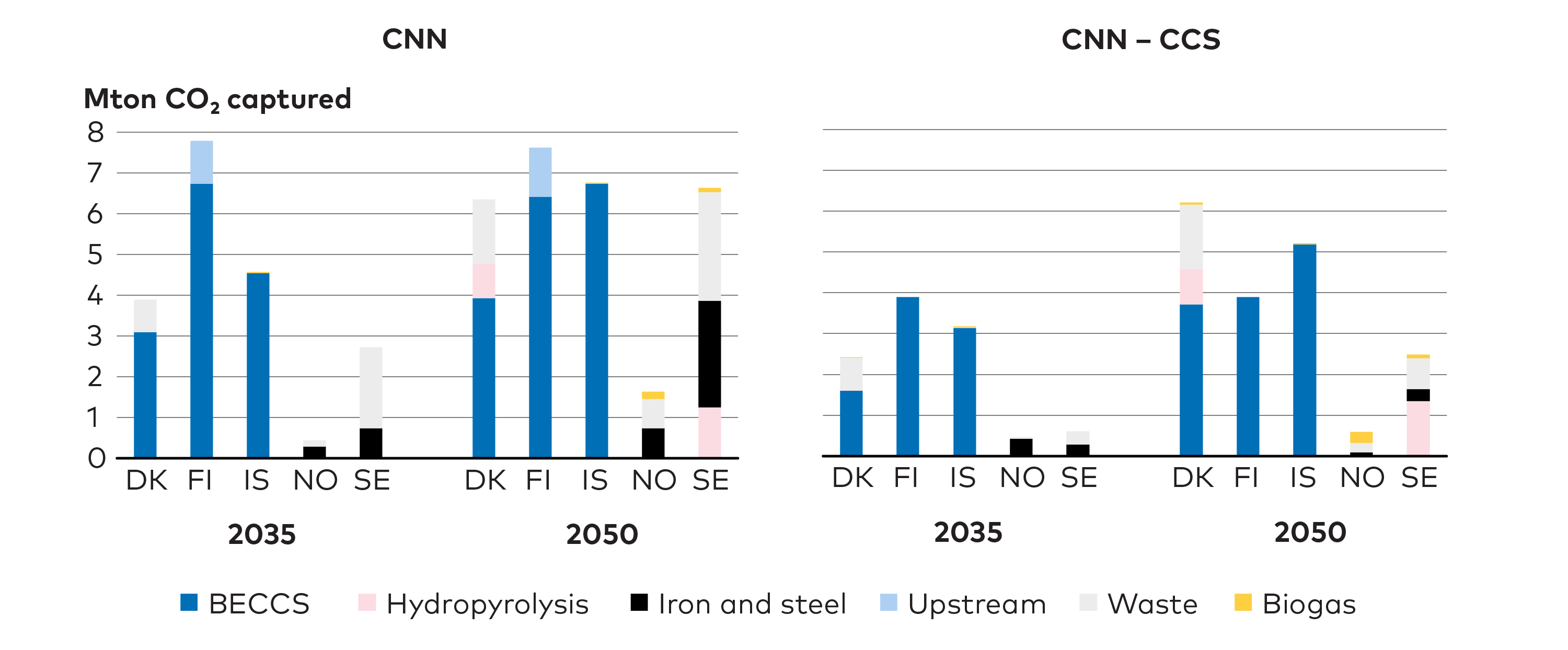

All NCES scenarios assert that achieving net zero emissions will be difficult without technologies for CCS, including technologies that would enable negative emissions. In sectors where no viable alternatives for reducing emissions yet exist, CCS or compensation with negative emissions becomes critical. The Nordic countries are well suited to develop and apply these technologies.

Long experience with the technology, coupled with offshore energy industries and large storage potentials, make Norway an emerging frontrunner. Additionally, the large presence of bio-based sectors, such as pulp and paper, and bioenergy in district heating, offers opportunities to achieve negative emissions through BECCS. Captured CO2 can be used as a raw material of certain PtX fuels, such as synthesised methane. Such use of captured CO2 would not eliminate emissions but could support the transition to decarbonised fuels.

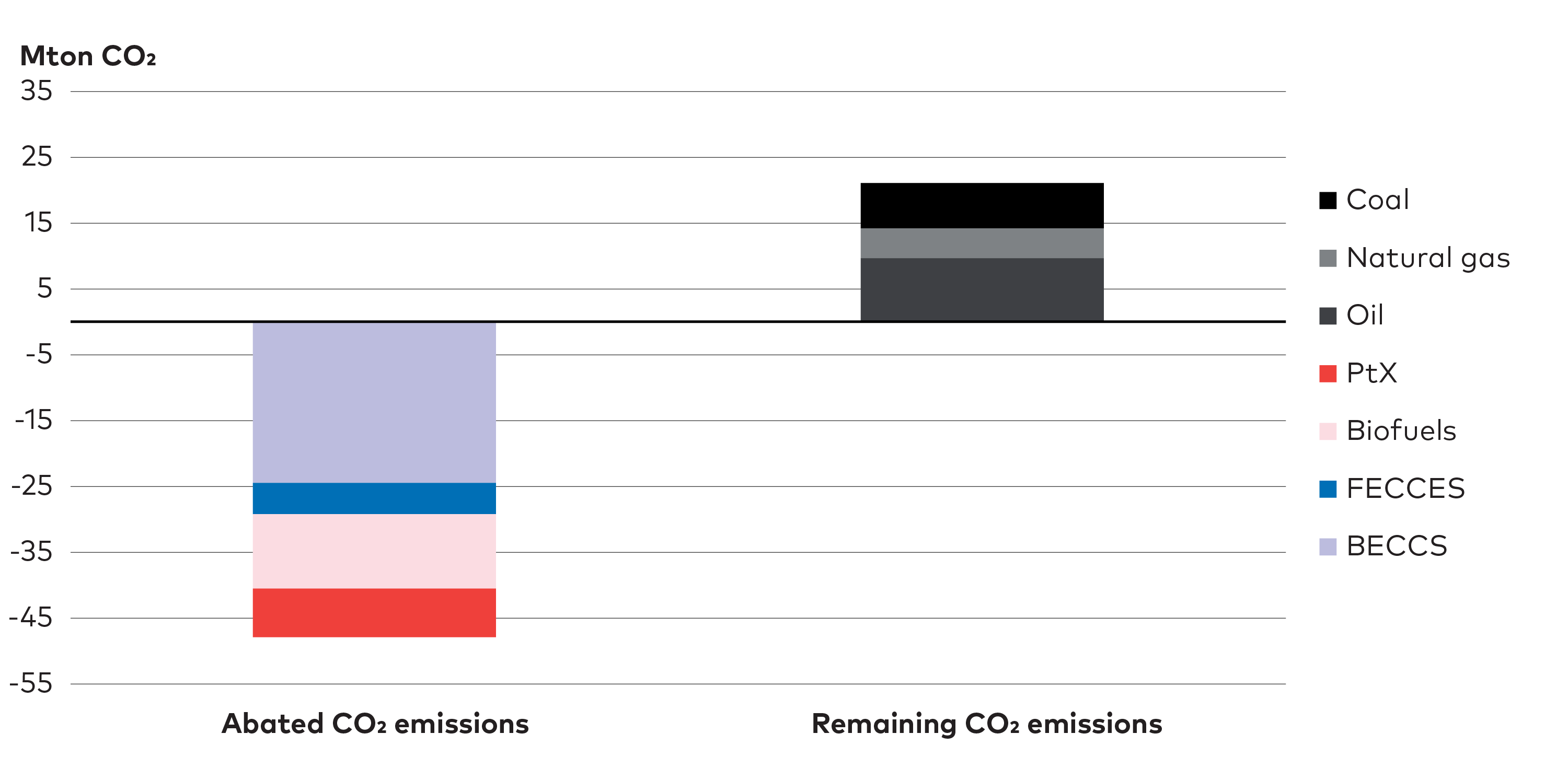

In the CNN scenario, the Nordic region captures and stores ~25 Mt of CO2 in 2050, about 12% of needed reductions from 2020 levels. Some 90% of captured CO2 in 2050 is from biogenic sources and municipal waste; less than 10% is from fossil sources. Large-scale roll-out of CCS is is required from 2030, underscoring the need to develop needed infrastructure and accelerate deployment through policy support.

Message

seven

Three no-regret actions for CCS and negative emissions:

-

Establish clear national positions in support of CCS technologies to build long-term market confidence.

-

Launch initiatives to create economic incentives for negative emissions.

-

Coordinate infrastructure development to reduce investor risk and entry barriers for individual actors.

Behavioural change and social acceptance for infrastructure must be considered

Changes in behaviour will directly impact the Nordic energy transition by affecting energy demand and the associated need for infrastructure. Such changes need to be significant to have a profound impact on scenario results.

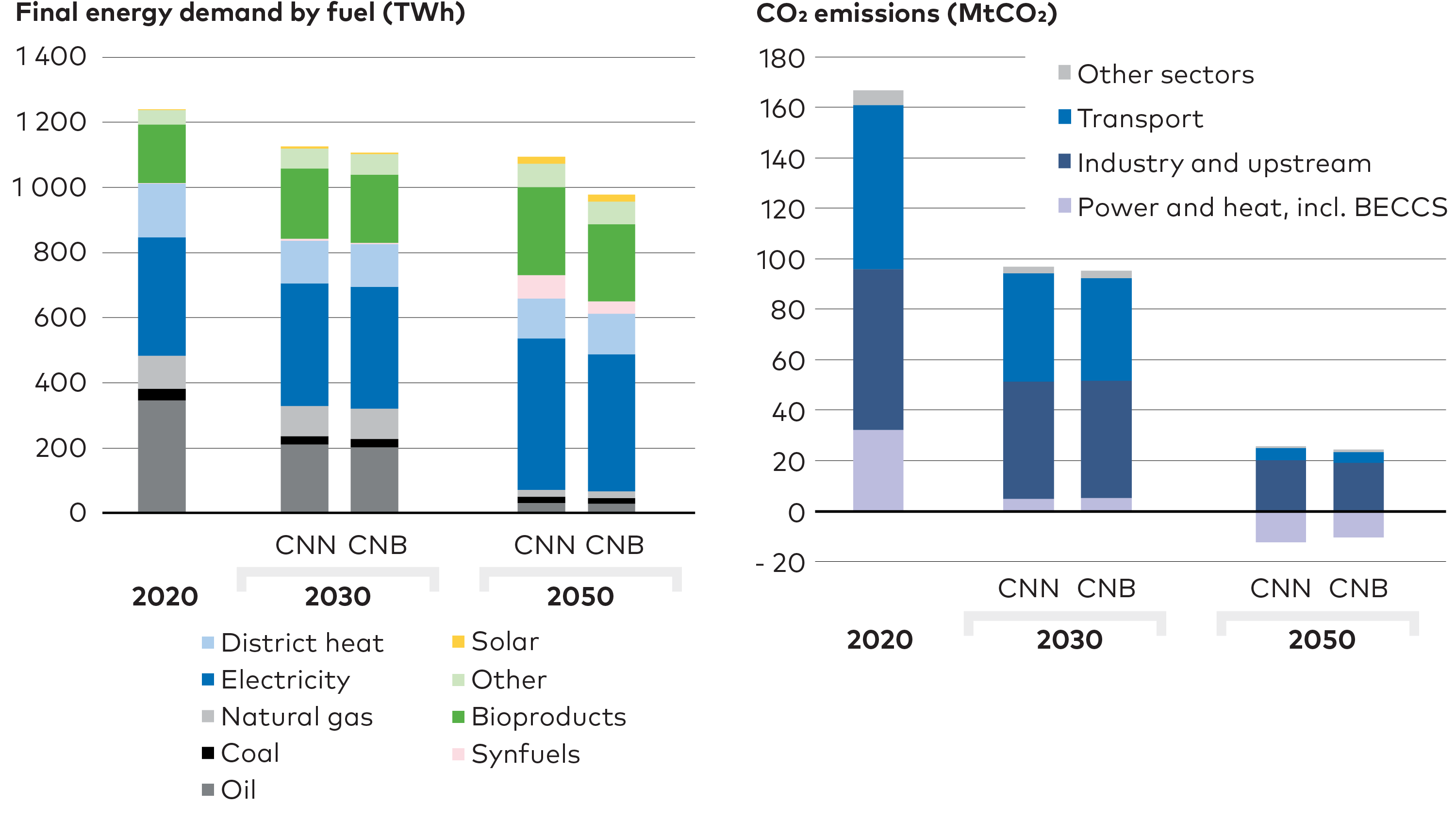

For instance, in the CNB passenger transport demand is reduced by 20%, industrial energy demand by 10%, and freight transport volumes by 5%, compared with the CNN. As a result, final energy demand falls by 17% and power demand by only 5% in the Nordic region by 2050, compared to CNN.

Message

eight

Since carbon neutrality is achieved in all NCES scenarios, these changes would lead to only minor differences in CO2 emissions (Figure ES.8). The power of behavioural change lies in its ability to buy time for the transition, reduce pressure on biomass resources, or reduce costs of infrastructure build-outs. Total system costs in the CNB scenario over the period 2020-2050 are about 10% lower than in the CNN scenario. Moreover, reducing transport demand can deliver additional benefits such as decreased congestion, less need for road and parking infrastructure, and improved air quality.

Figure ES.8. Final energy demand (left) and CO2 emissions (right) in CNN and CNB scenarios. Behavioural change must be significant to impact energy system development.

Aspects of behaviour and social acceptance will be very important: even CNB, the scenario with the lowest demand growth, requires a massive scale-up of electricity generation capacity. Already today, public resistance to infrastructure development for renewables and transmission pose a significant challenge. Policy action to promote behaviour changes that reduce energy demand could thus make the NCES scenarios easier to realise.

Three no-regret actions for behavioural change:

-

Improve and plan infrastructure development to promote cycling and public transport.

-

Strengthen policies to encourage lower consumption and preference for products with lower CO2 footprints, through price signals, labelling and information campaigns.

-

Implement measures to support social acceptance of onshore wind by highlighting social justice aspects while also ensuring transparent and inclusive decision-making.

Nordic collaboration is instrumental and would strengthen the Nordics’ Role in the European transition

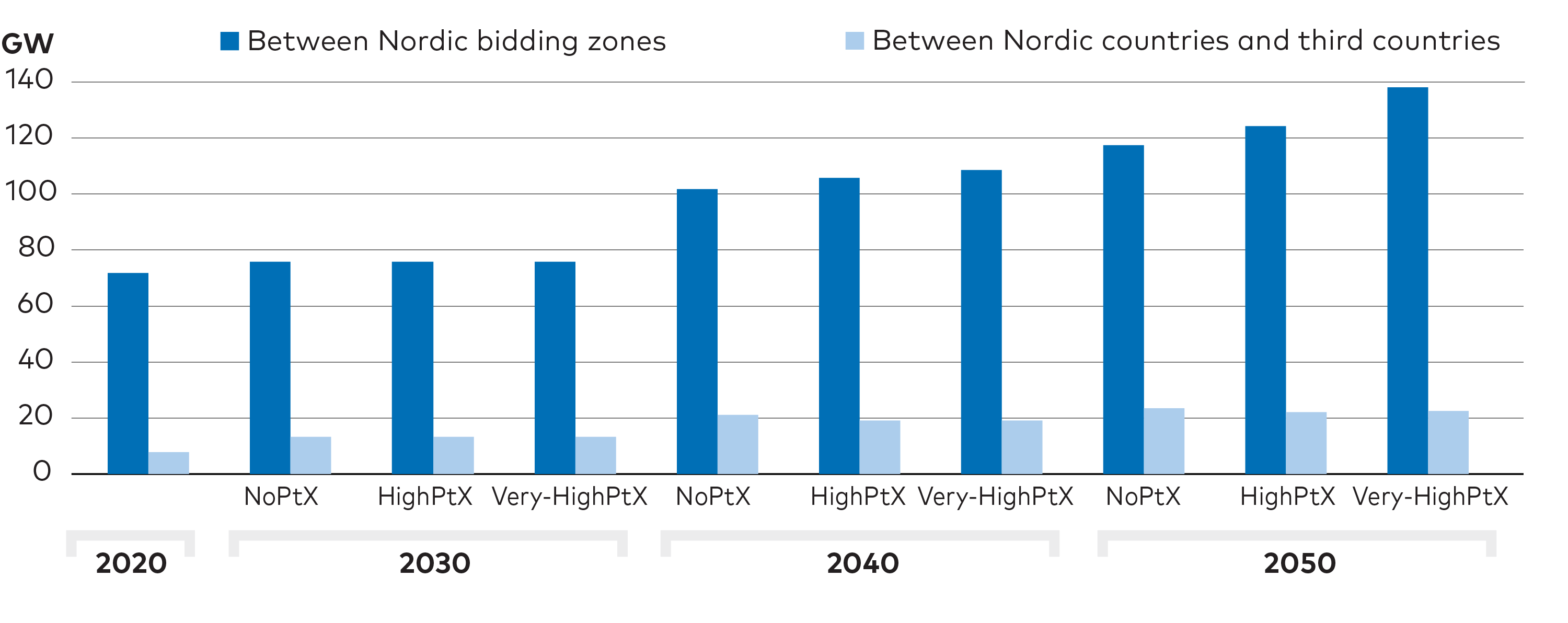

The potential of Nordic collaboration becomes more apparent as the generation mix in the Nordic electricity sector is transformed, electricity demand rises, and wind generation takes centre stage. The differences between the individual countries’ energy systems are a strength, while the development of necessary infrastructure emerges as a major coordination challenge in all NCES scenarios.

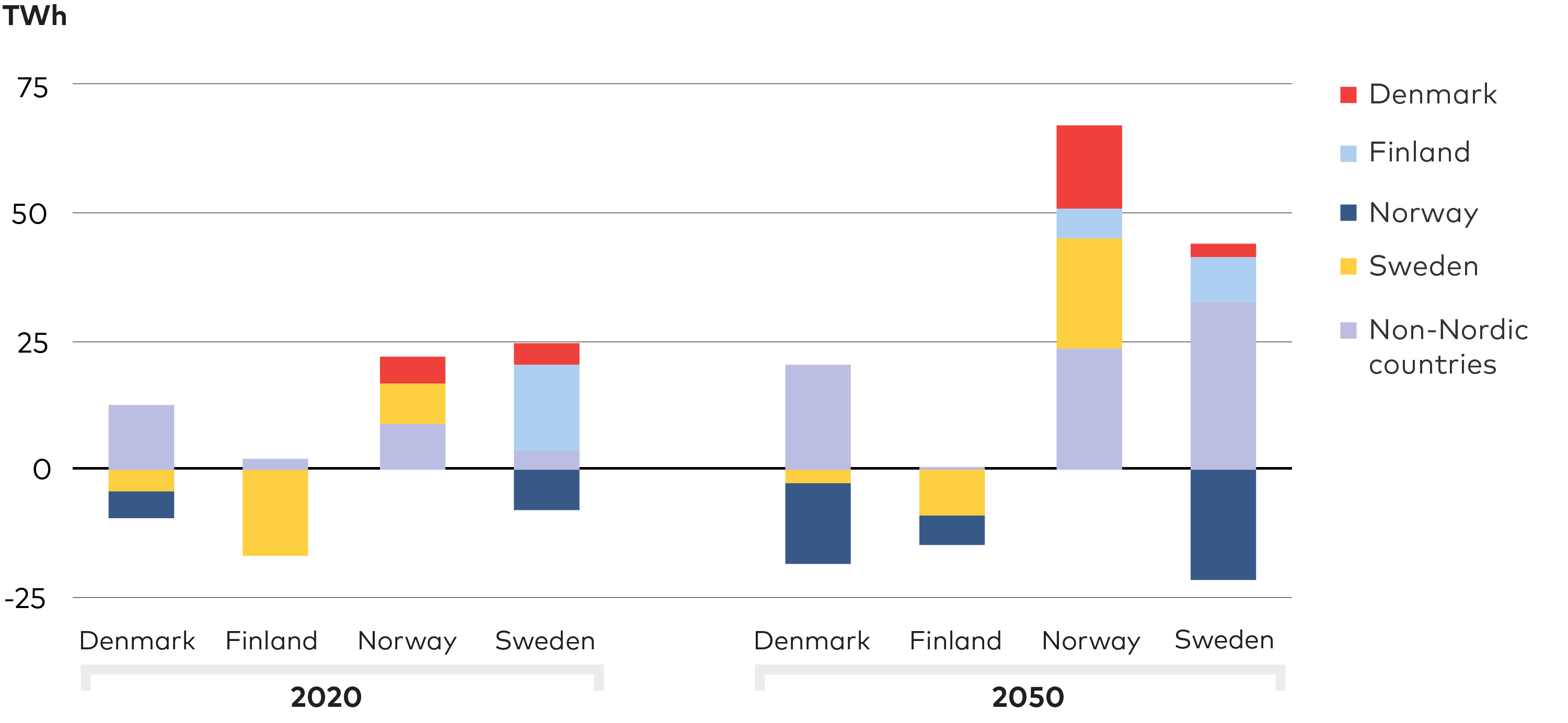

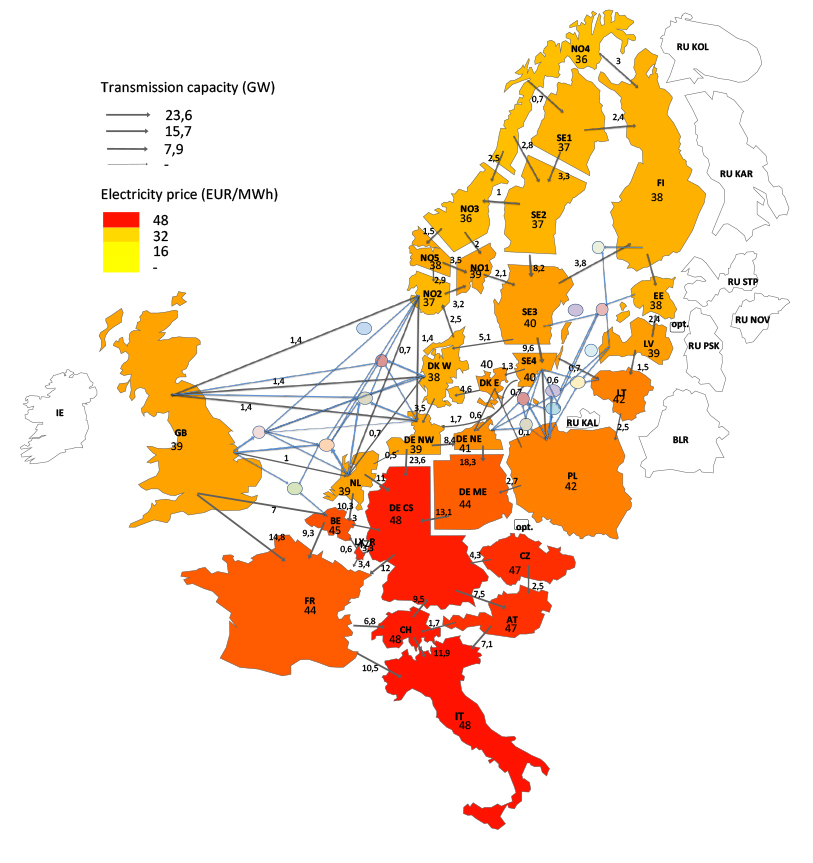

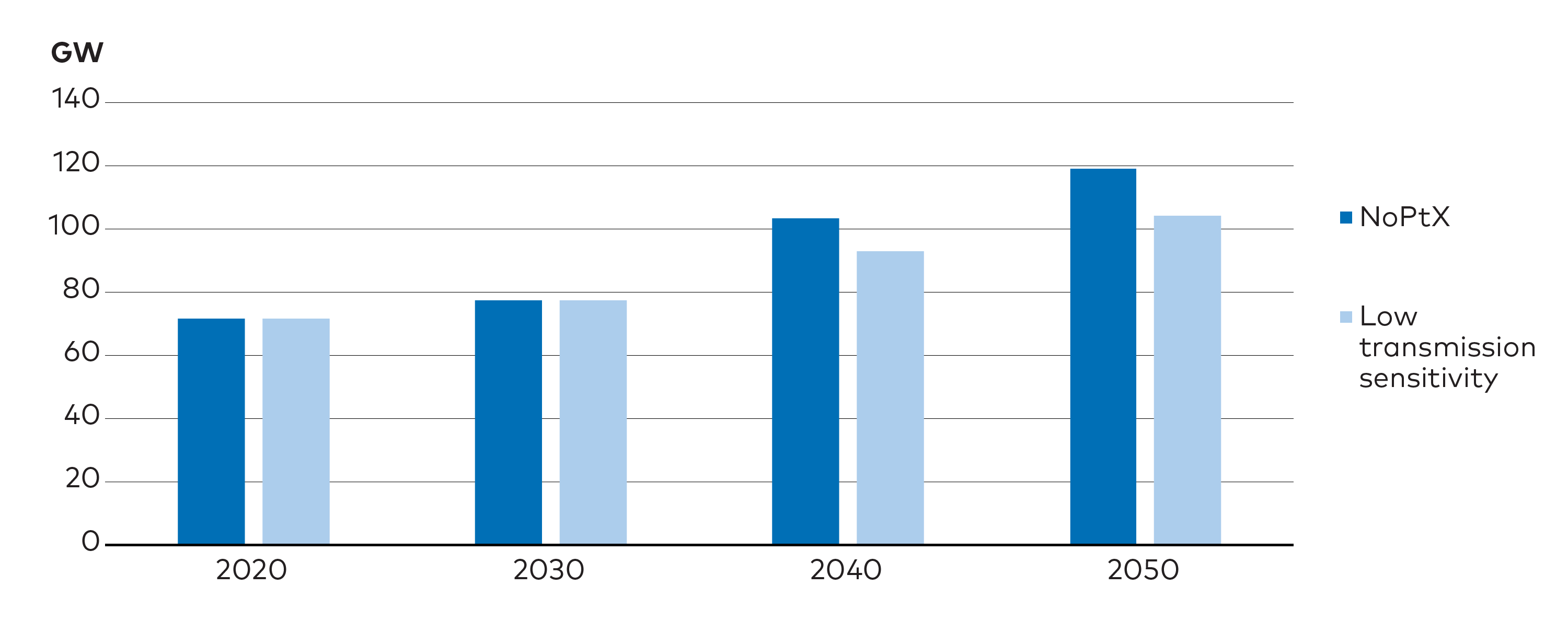

For example, changes in Nordic power flows occur in two dimensions: total trade volumes increase and the importance of Norwegian export grows stronger (Figure ES.9). Together, these shifts require a 60-70% increase in exchange capacity among Nordic bidding zones. In addition, considerable investments in both direct and hybrid interconnectors to neighbouring markets are envisaged.

Message

nine

Figure ES.9. Trade flows among Nordic countries - NoPtX case. Comparison of net trade flows among the Nordic countries in the NoPtX case in 2020 and 2050. Negative numbers indicate a net import while positive numbers indicate a net export.

The balancing offered by Norwegian hydropower may be instrumental in a future Nordic power system dominated by wind generation, while Swedish and Danish transmission grids and interconnectors facilitate the transit of large net electricity exports from Norway to continental Europe.

PtX offers flexibility to the power system and an alternative way of exporting Nordic power surplus, representing substantial potential export value for all the Nordic countries. In turn, PtX fuel export would relieve the electricity grid, deliver large revenues for Nordic energy companies, and have the potential to significantly reduce European greenhouse gas (GHG) emissions. But it would require infrastructure development that involves several Nordic countries.

With CCS emerging as an important element of Nordic decarbonisation, collaboration in infrastructure development would be beneficial. Synergetic effects exist here as well, for both the Nordic region and from a larger perspective within the overall European energy transition.

If, however, infrastructure investments are perceived as being made only for the sake of energy exports or for the benefit of other countries, they are likely to meet strong public resistance. That makes concerted planning, citizen involvement, and new cost distribution mechanisms instrumental for a cost-effective and socially acceptable transition of the Nordic energy sector and its contribution to Europe as a whole.

Three no-regret actions for Nordic collaboration:

-

Strengthen joint Nordic action plans for infrastructure needs and development.

-

Develop a joint Nordic roadmap for the role of PtX, including identification of the most promising sites for production in the Nordics.

-

Develop a joint Nordic CCS strategy to increase the potential to realise economies of scale in transportation and storage of captured carbon.

Robust results provide confidence for critical near-term actions

While the NCES scenarios identify uncertainties, their inevitable presence should not be used as a pretext for taking no action. Regardless of which decarbonisation pathway is pursued, certain near-term actions and investments clearly deliver substantial benefits.

Stronger grids, increased flexibility, wind and solar electricity deployment, electrification of transport, and CCS technologies are vital to all NCES scenarios. Existing solutions, such as bioenergy and district heating, continue to be important while innovative market developments can unlock the potential of both emerging and existing technologies. Importantly, NCES modelling finds that decarbonisation is unlikely to push wholesale electricity prices higher.

Energy demand reduction through efficiency improvements and behavioural change will make policy targets easier and less costly to reach. Decisive actions are required to realise the potential in all these areas; not acting undermines the achievement of stated goals and risks driving up the associated costs.

Message

ten

Three no-regret actions for near-term Nordic collaboration:

-

Reform grid planning to enable shorter lead times and more proactive expansion, while looking for system-smart local solutions that can reduce grid capacity needs.

-

Ensure that electricity markets are designed to incentivise investments aligned with decarbonisation targets as well as other policy objectives such as energy security.

-

Accelerate public investments in research, development, demonstration, and deployment (RDD&D), including in CCS technologies, biorefining and PtX.

PHOTO: JOHANNES JANSSON/NORDEN.ORG

PHOTO: JOHANNES JANSSON/NORDEN.ORG

Chapter 1

Nordic Countries are Committed to Carbon Neutrality

In 2019, the Nordic countries - Denmark, Finland, Iceland, Norway, and Sweden – signed a joint Declaration on Carbon Neutrality, committing to make the Nordic countries carbon neutral, in line with the COP21 Paris Climate Agreement. The declaration commits the Nordic countries to assess scenarios for how to achieve carbon neutrality, including the implications such scenarios would entail for various sectors. Individually and collectively, these countries already have among the most ambitious energy and climate policy agendas in the world. The declaration emphasised the necessity and benefit of collaborative action and invited the Nordic Council of Ministers to prepare a proposal on how to achieve this aim.

To support this commitment Nordic Energy Research (NER) commissioned the Nordic Clean Energy Scenarios project (NCES). The aim of this project is to identify and help prioritise, through scenario modelling, what actions will be necessary by 2030 and to map potential long-term pathways to carbon neutrality. Several shifts over the past decade have had significant influence on Nordic energy policy, making the region well positioned to pursue carbon neutrality:

Raised political ambitions for carbon neutrality – including through energy policy – is gaining momentum. NCES builds on work done in previous NER projects, such as the Nordic Energy Technology Perspectives projects (NETP), Flex4RES, and SHIFT, all assessing ways to reach carbon neutrality. The very first scenario analysis was published in 2013. At that time, Denmark, Norway, and Sweden were the only Nordic countries with national targets to become fossil free or carbon neutral, and the European Union (EU) had a target to reduce greenhouse gas (GHG) emissions by 40% from 1990 levels by 2030.

Less than a decade later, in April 2021, the EU strengthened its target to a 55% reduction by 2030 and to reach carbon neutrality by 2050. At the regional level, all five Nordic countries have now set carbon neutrality aims in their domestic policies and more specifically targeted the energy sector for ambitious climate mitigation targets. Being a corner stone of any society, the energy sector will be a main driver for deep decarbonisation of the Nordic economy as a whole, unlocking the ability for other sectors to follow.

Figure 1.1. Sum of Nordic historic GHG emissions and plotted sum of Nordic national targets. Sum of Nordic GHG emissions, with plotted emission trajectories for fulfilment of national targets. Note: The emissions of international transportation are not included in national targets.

Source: European Environment Agency (EEA), 2019a; European Commission (EC), 2020; EEA, 2019b; EEA, 2019c. Additional national documentations were used for Finland, Iceland, and Norway when more recent than common reports or additional details were needed for non-CO2 or Land Use, Land-Use Change and Forestry (LULUCF): Koljonen et al., 2020; Ministry for the Environment and Natural Resources, 2018; Government of Iceland, 2020; Miljødirektoratet, 2020.

Acknowledgement that current approaches are not delivering the rate of change required to achieve carbon neutrality. Nordic energy regulation has, broadly speaking, been focused on cost-effectiveness and liberalisation for the last 25 years, and in many respects this has worked well. However, over the period 2009-2018, energy related CO2 emissions in the Nordic fell by an average of 2% annually. This is well short of the pace needed to reach carbon neutrality. In the coming decade (2021-2030), it will be necessary to achieve annual emission reduction rates of around 10%.

As doubts arise, about the ability of technology neutrality and increased competition to make up the sole tools to stimulate the transition required, calls are emerging to make the pace of the transition a primary driver of decision-making and action.

Greater recognition of the need to incorporate decision-making criteria beyond cost-effectiveness to also include long-term technical potential, environmental protection, and social considerations. While achieving carbon neutrality will require large investments, several studies suggest that absolute costs are unlikely to be the main barrier to reaching the objective.[1]OECD/IEA & NER, 2016; NEPP, 2020. Thus, although cost-effectiveness remains important, using it as the only parameter against which to benchmark actions is too narrow in scope. Interlinked factors, such as political feasibility, public acceptance, and distributional impacts also need to be considered.

Footnotes

- ^ OECD/IEA & NER, 2016; NEPP, 2020.

Electrification, both direct and indirect, has emerged as a central strategy in reaching climate policy objectives. This is to some extent driven by continued cost reductions in key technologies, such as wind power and batteries, and partly by the realisation that electrification is one of few viable routes to reduce emissions in hard-to-abate sectors, such as steel and chemicals.

Moreover, the role of indirect electrification – through ‘power-to-X’ (PtX) and green hydrogen solutions – is receiving unprecedented public attention, and these technologies will be able to play an important role in the Nordic energy system. Consequently, the NCES shows electrification taking a much larger role in terms of importance to the clean energy transition compared with scenarios developed in the early 2000’s.

PROJECT SCOPE

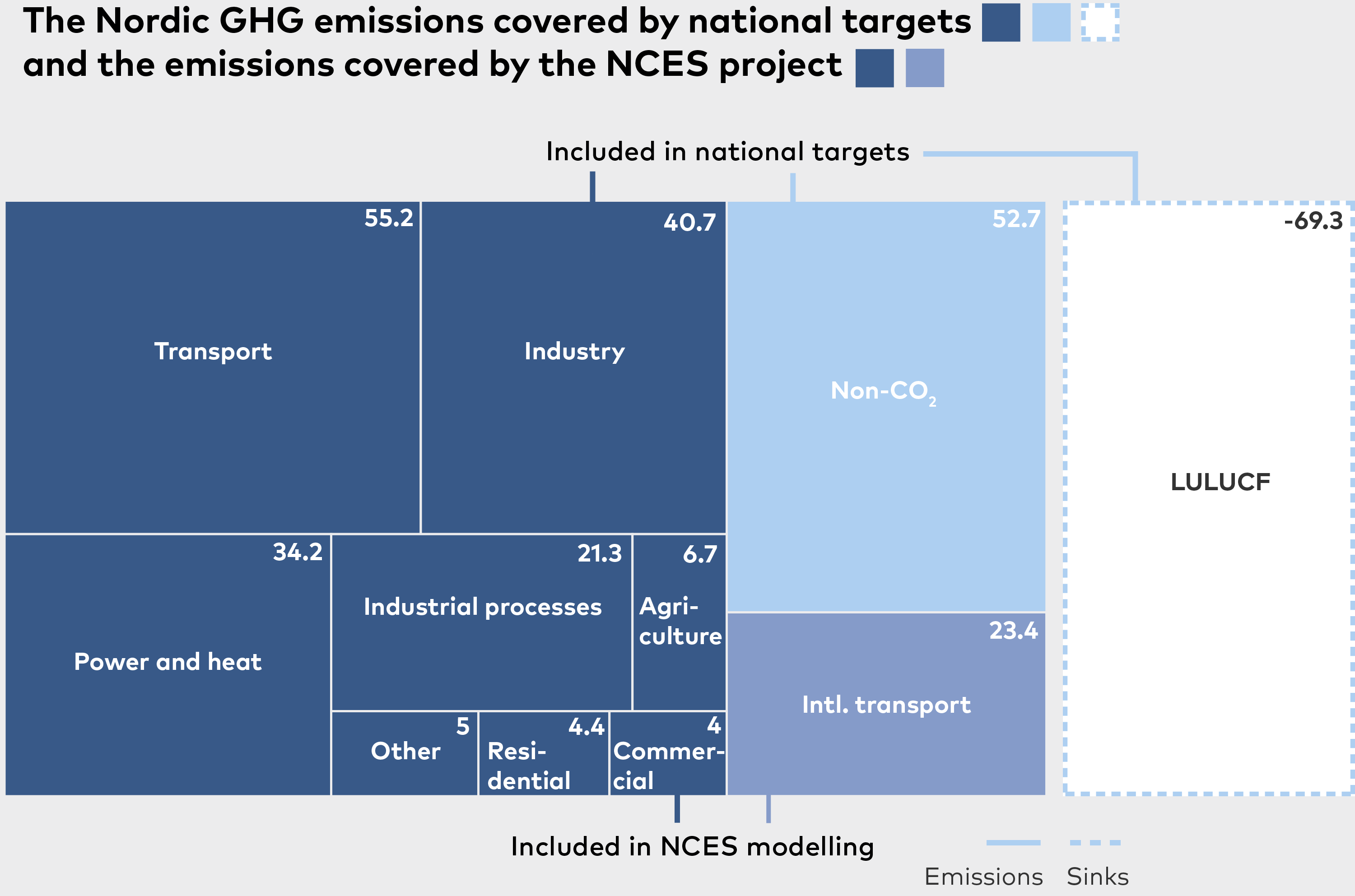

The NCES project focuses on activities that cause energy-related CO2 emissions, which represent ~80% of total Nordic GHG emissions. The adopted definition of carbon neutrality by this project sets the limit for total energy-related CO2 emissions in each modelled scenario without defining or prioritising specific measures in certain sectors. The project analyses all combustion of fossil fuels in the economy, including process-related CO2 emissions from industry. International transport, while not part of national targets, is included in the modelling. International aviation is allowed emissions at 2019 levels until 2030, then reduces linearly to zero by 2050, while emissions from international shipping are reduced by 90% from 2019 levels by 2050. The analysis excludes non-CO2 gases, which stem primarily from agriculture and waste management, and emissions related to land use, land-use change and forestry (LULUCF). The NCES scenarios do, however, include assumptions on non-CO2 gases and LULUCF, based on previous studies that assess how emission rates from these activities are likely to develop, in order to estimate total GHG emissions.

Figure 1.2. Scope of the NCES project. Note that NCES scenarios include international transport.

Why a carbon budget does not define the limits of the NCES

The concept of remaining carbon budgets – the representation of future cumulative CO2 emissions consistent with keeping global warming to a specified level – has gained broad acceptance among both policy makers and the public. Setting an absolute limit on global carbon emissions – as is done by the United Nations Intergovernmental Panel on Climate Change (IPCC) – provides a clear indication for limiting global warming to 1.5°C above pre-industrial levels. Meaning that carbon budgets and carbon neutrality targets, as investigated in this project, do not necessarily align: a target set for 2050 becomes irrelevant if the carbon budget is used up by 2030. Due to its ability to more definitively represent when the climate system will reach a tipping point application of a remaining carbon budget was requested in the commission of this project.

However, to apply a carbon budget in NCES would entail taking into account uncertainties at the global level along with the vast span of potential national budgets, where the methods used for allocation would aggregate economic, political, and ethical views. Depending on the allocation method used, the remaining carbon budget for the Nordic region ranges from a low of 100 MtCO2 to 2,000 MtCO2.

As the project aim is to illustrate pathways to achieve national targets, formulated to reach carbon neutrality, it therefore becomes difficult to use a carbon budget as the framework for providing the requested analysis. Therefore, the NCES scenarios aim to reach carbon neutrality in a given year, see table 1.1 below for the applied national targets and the resulting application in NCES modelling. However, the NCES project provides an opportunity to explore the potential span of remaining carbon budgets for the Nordic countries via an interactive web tool, developed by Energy Modelling Lab and Tøkni, that can be accessed at www.nordicenergy.org along with other resources from the NCES project.[1]Apart from this report and the mentioned carbon budget tool, the NCES project has produced a technology catalogue that details the costs and performance of a large suite of energy technologies and a database of Nordic energy indicators. These resources can all be accessed through the Nordic Energy Research website www.nordicenergy.org.

Footnotes

- ^ Apart from this report and the mentioned carbon budget tool, the NCES project has produced a technology catalogue that details the costs and performance of a large suite of energy technologies and a database of Nordic energy indicators. These resources can all be accessed through the Nordic Energy Research website www.nordicenergy.org.

Table 1.1. The main differences between the Nordic countries use of carbon neutrality targets arise in target years for reaching the goal, their mid-term targets, and in the use of carbon credits. The difference in target years cannot be directly compared as some countries allow the use of carbon credits and some will benefit from considerable forest carbon sinks. In this table a summary of the application of national carbon neutrality targets are presented.

| DENMARK | FINLAND | ICELAND | NORWAY | SWEDEN | NORDICS | |

| Target year for carbon neutrality | 2050 | 2035 | 2040 | 2030 | 2045 | No common Nordic target |

| Additional targets included in modelling | Domestic GHG -70% by 2030 from 1990. | Domestic GHG excl. LULUCF -80% by 2050 from 1990. | None | Domestic GHG excl. LULUCF -80% by 2050 from 1990. | None | N/A |

| Included domestic GHG emissions | All GHGs incl. LULUCF, but excl. international transport | All GHGs incl. LULUCF, but excl. international transport | All GHGs incl. LULUCF, but excl. international transport | All GHGs incl. LULUCF, but excl. international transport | All GHGs, partially included LULUCF | |

| Assumption for use of carbon credits | None. International credits might become an option in Denmark, but those are not assumed here. | None | Yes. Norway would reach the 2030 target with credits. Domestic measures would reduce net GHG by 67% by 2030 compared to 1990. | Yes. Sweden aims for 85% reduction from domestic GHG excl. LULUCF by 2045. The remaining 15% (10.7 MtCO2e) can be from additional LULUCF measures, BECCS, or international credits | N/A | |

| Modelled energy-related CO2 by 2050, excl. intl. transport | -5 MtCO2 | +8 MtCO2e | -5 MtCO2e | +5 MtCO2e | +1 MtCO2e | +4 MtCO2e |

| Net total GHG at 2050 (energy-related CO2 excl. intl. transport, LULUCF, and non-CO2) | 0 MtCO2e | -8 MtCO2e | -1 MtCO2e | -9 MtCO2e | -29 MtCO2e | -46 MtCO2e |

1.1 The Nordic region is well positioned to be a front-runner for carbon neutrality

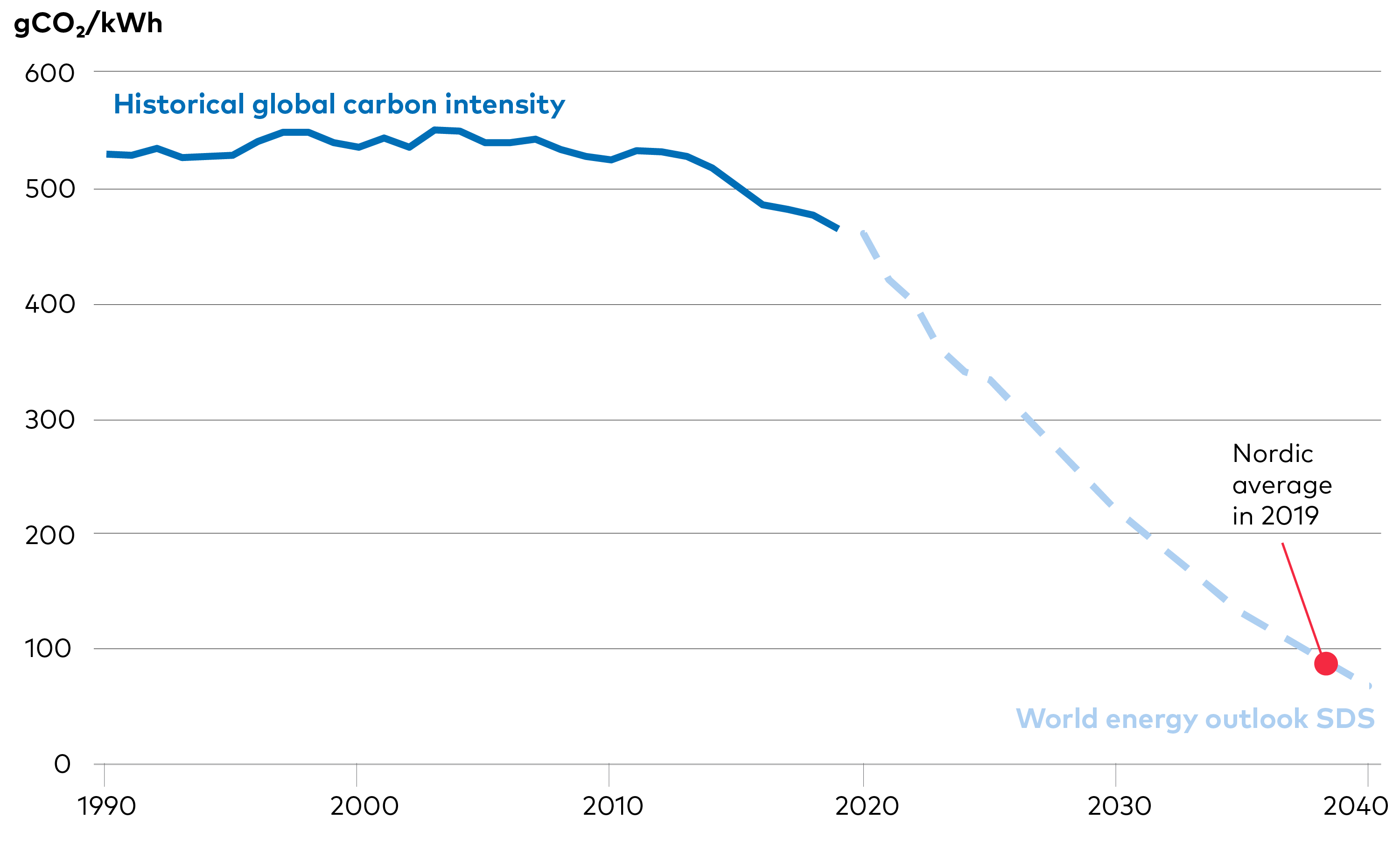

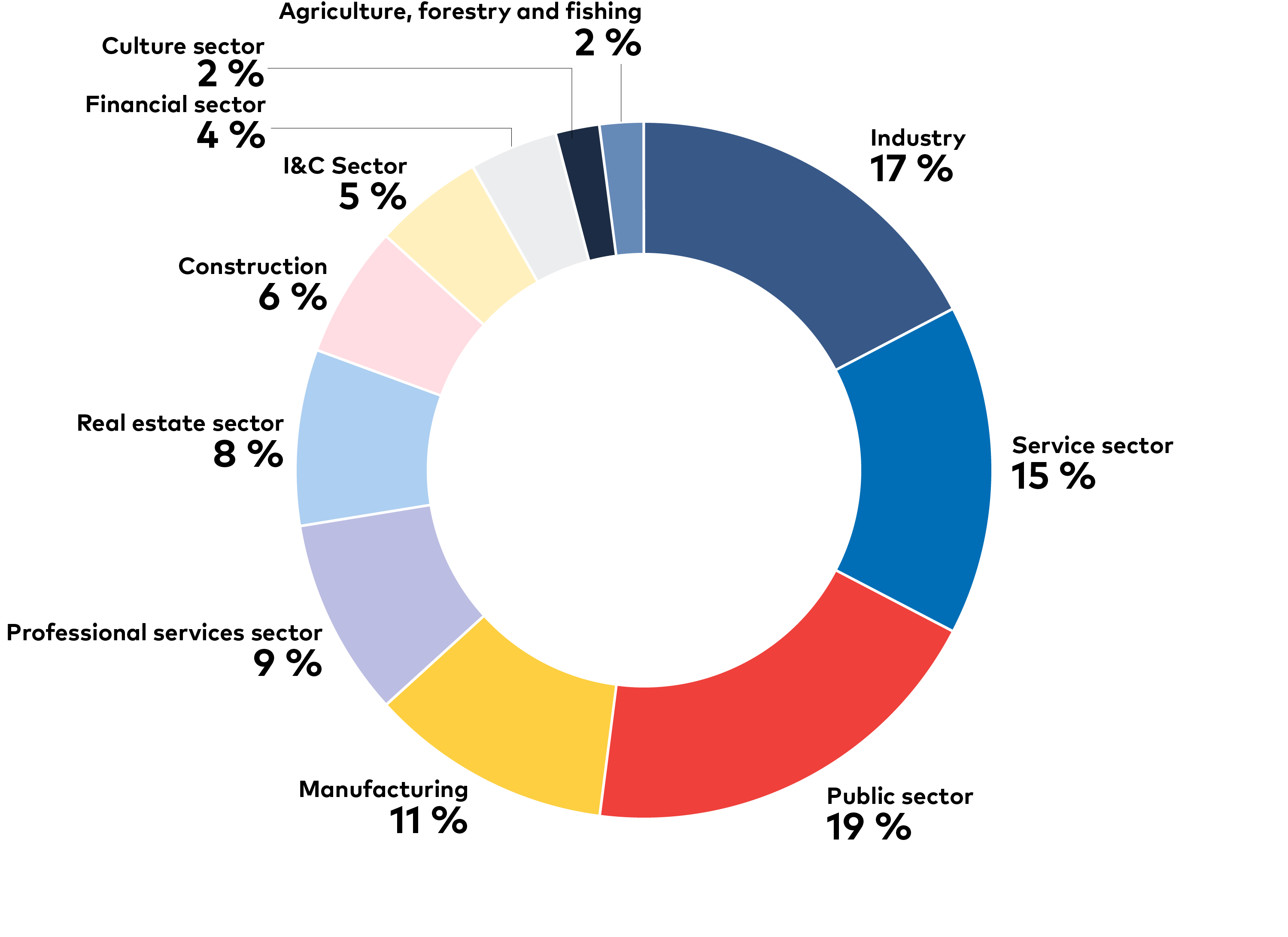

With a history of energy and climate policy that taps into extensive natural resources, the Nordic countries are in a good position, relative to both EU28 and global averages, to aggressively pursue a clean energy transition. In relation to the global CO2 intensity of electricity, Nordic generation is performing very well (Figure 1.3). This creates a strong starting point and will be a great asset in the years to come as clean electricity plays a central role in decarbonising sectors that account for a large CO2 footprint in relation to their gross value added contributions to the Nordic economy (Figure 1.4). Nordic heat supply, particularly for buildings, also has a low CO2 footprint.

Figure 1.3. Global CO2 intensity of electricity generation and Nordic Average. Current Nordic CO2 intensity in electricity generation, compared with global development in the International Energy Agency's (IEA) Sustainable Development Scenario. Source: IEA, 2020; Eurostat, 2020.

Figure 1.4. Gross value added by sector for the Nordics. Gross value added by sector in the Nordic countries in 2019. Source: Eurostat, 2020.

The region is also endowed with plentiful geothermal, hydro, wind, and bioenergy resources and over the last decades the Nordic countries have significantly increased the rate of renewables deployment. In parallel, governments have over the last 40 years implemented a suite of policies to drive energy efficiency and initiate a fuel shift – away from coal, oil, and gas towards increased use of biomass, waste incineration, renewable electricity, and geothermal. More recently, governments have taken steps to build a mature market for electric vehicles (EVs). Collectively, such efforts have resulted in a steady rate of decoupling economic growth from energy-related CO2 emissions.

As is becoming more evident, cost-effectiveness is not the only parameter for successfully reaching our carbon neutrality targets but it is important to not downplay its role neither. The relatively stable Nordic policy environment has also lowered the perceived risk for investors, driving down the cost of capital, which in turn has accelerated investments in, for example, wind power. This is true both in absolute terms and relative to other countries. Continuing the acceleration of investment in renewable energy (RE) technologies is key for reaching our targets and the NCES project provides detailed analysis of investment needs in different technologies across the energy system.

On a per-capita basis, however, Nordic emissions still significantly exceed the world average, and end-use sectors in all Nordic countries have high electricity demand relative to EU28 and global averages. These latter trends clearly illustrate that despite being well position for an energy transition, we still have ways to go and reinforces the need to accelerate decarbonisation to reach carbon neutrality by 2050. It is also worth noting that territorial emissions, which are used in this project, do not account for emissions embedded in imported goods.

THE NORDICS TODAY

A snapshot of how the Nordic countries perform today in key indicators for tracking developments towards carbon neutrality. These indicators are supported by the energy statistics database set up within the NCES project. For more information and access to data for all indicators, please visit www.nordicenergy.org.

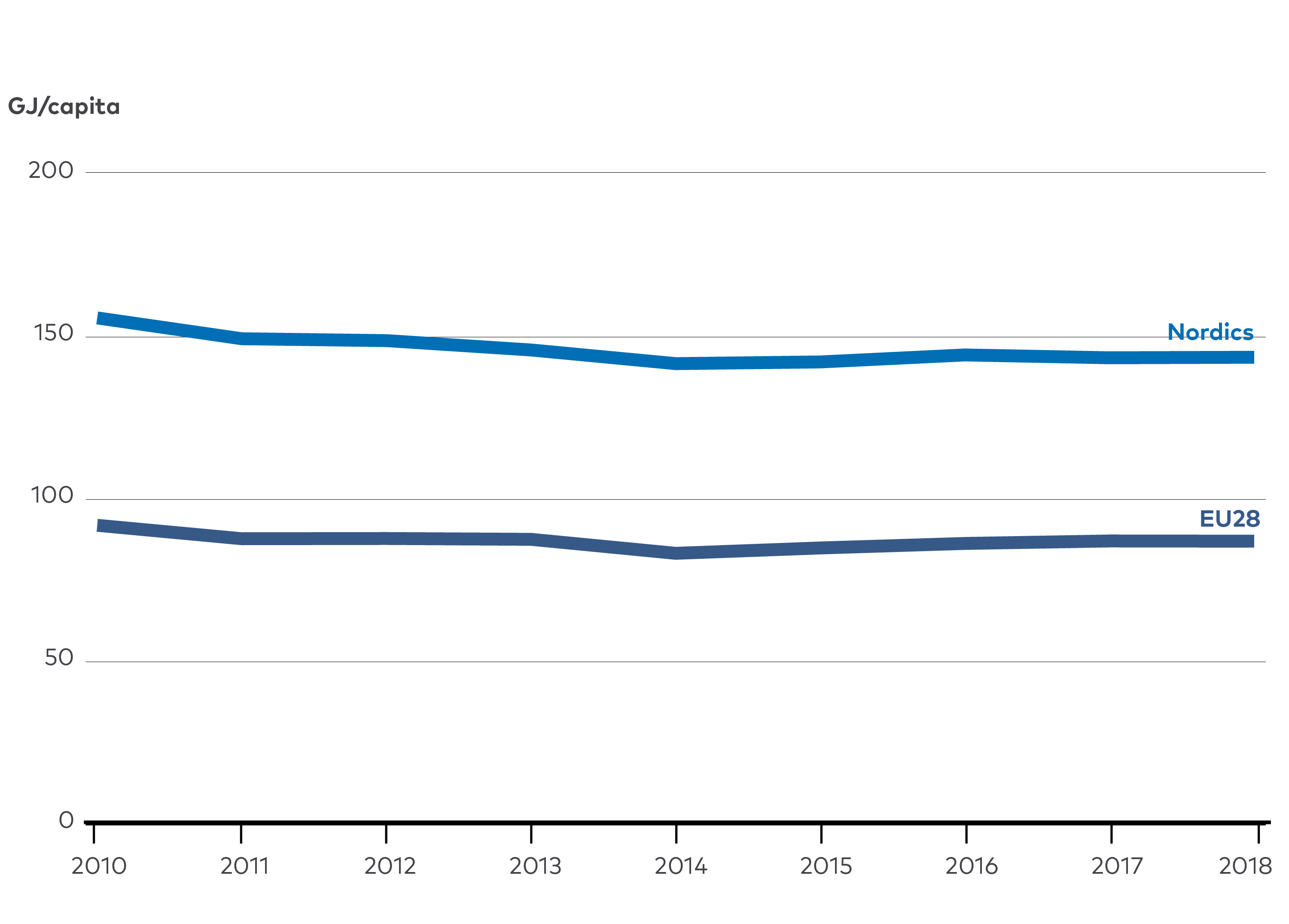

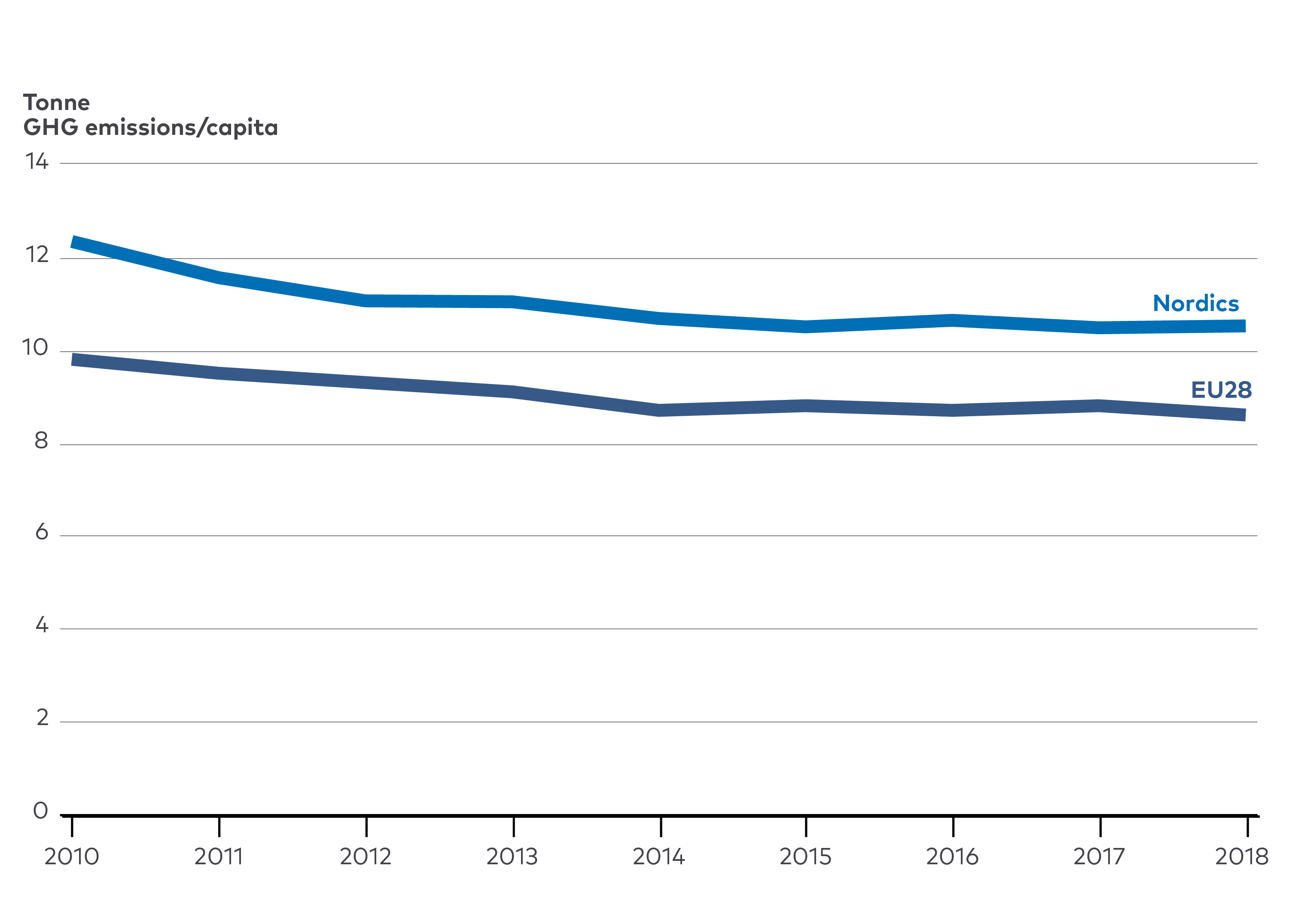

Despite progress, Nordic countries use more energy and emit more greenhouse gases per capita than the EU average.

Figure 1.5a and b. Energy consumption per capita and emission intensity of energy used. The left panel illustrates the difference in final energy consumption per capita between the Nordics and EU28. The right panel shows the difference in emission intensity per capita between the Nordics and EU28. Source: Eurostat, 2020.

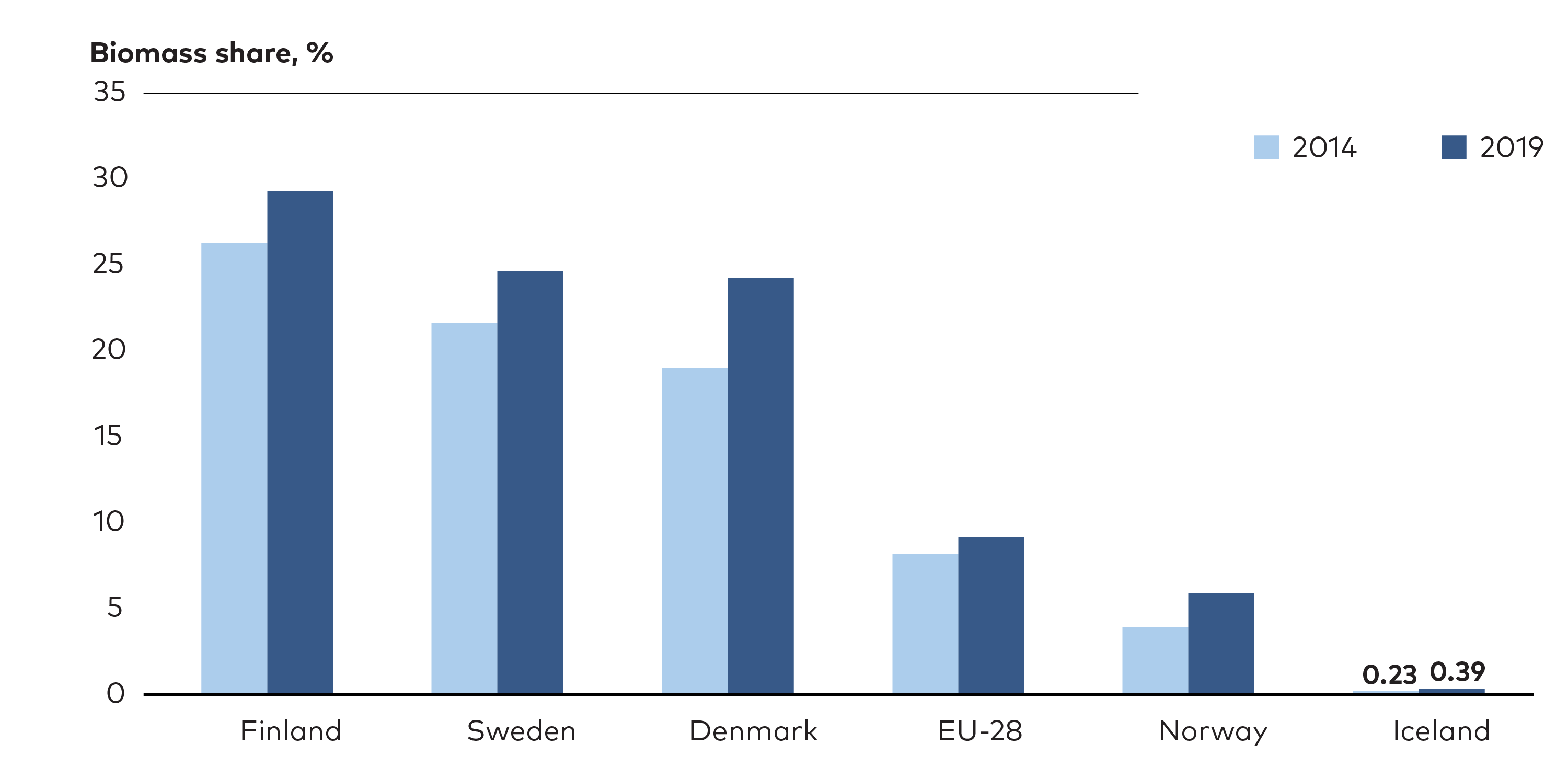

The Nordic region is endowed with plentiful geothermal, hydro-, wind-, and bioenergy resources, which together accounted for 44% of primary energy supply in 2018, compared with 16% for EU28.

Figure 1.6. Total primary Nordic and EU28 energy supply by energy source in 2018. The Nordic percentage of renewable energy and biofuels are significantly higher than in EU28 making the Nordics well positioned for extending its production of clean electricity, a central pillar for decarbonisation. Source: Eurostat, 2020

*Other RE; tide, wave, and ocean energy; heat pumps.

Figure 1.7a & b. This figure shows non-hydro renewable electricity generation in the Nordics, top, and EU28, bottom. What becomes clear is that the large share of the Nordic renewable energy supply comes from hydropower. Source, Eurostat, 2020.

Non-hydro renewable electricity represents about 12% of Nordic electricity generation, similar to the EU average.

Figure 1.8. Non-hydro renewable electricity generations share of total generation in the Nordics and EU28 follow a similar development. The Nordics are however falling behind. Source: Eurostat, 2020.

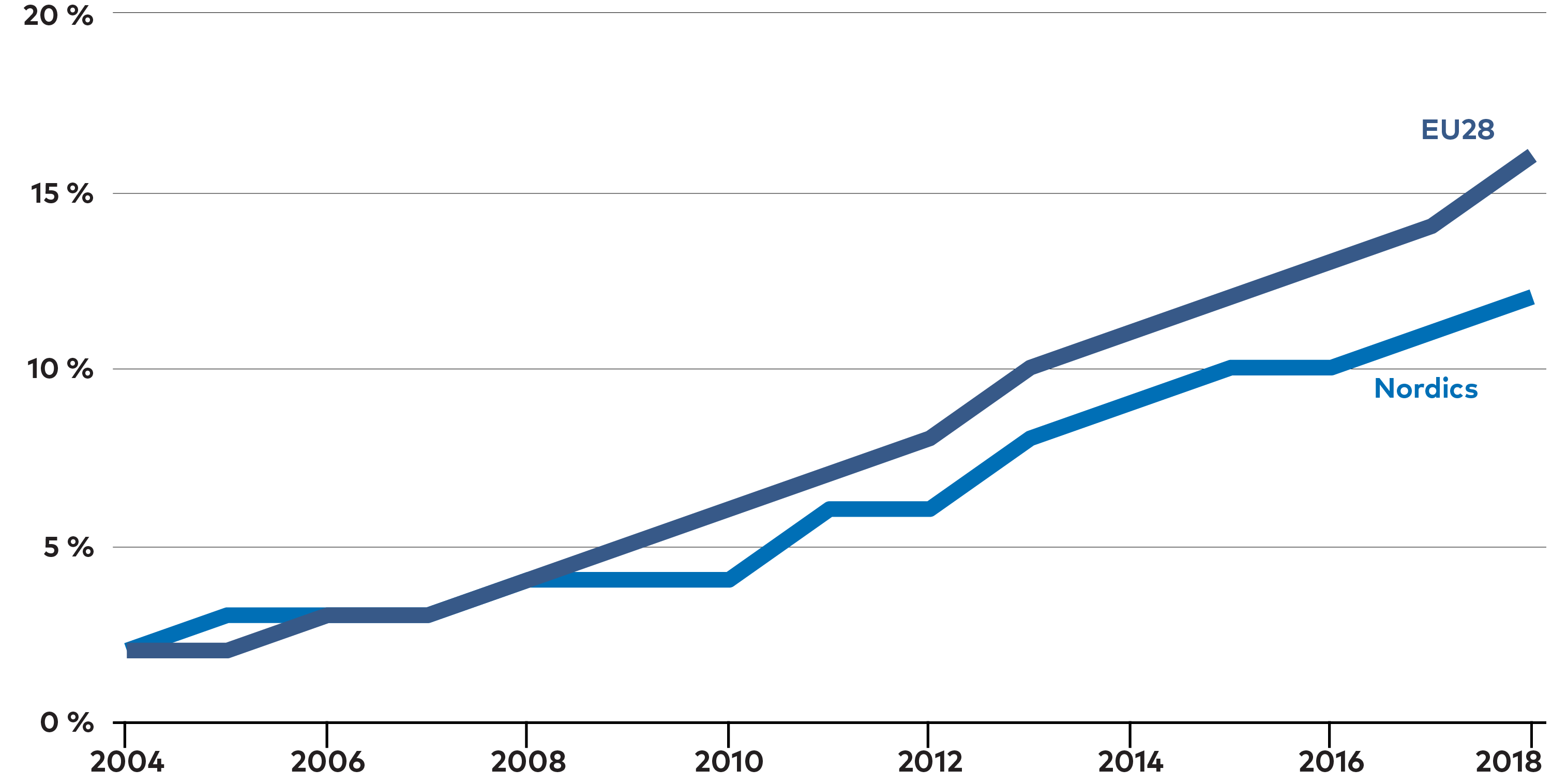

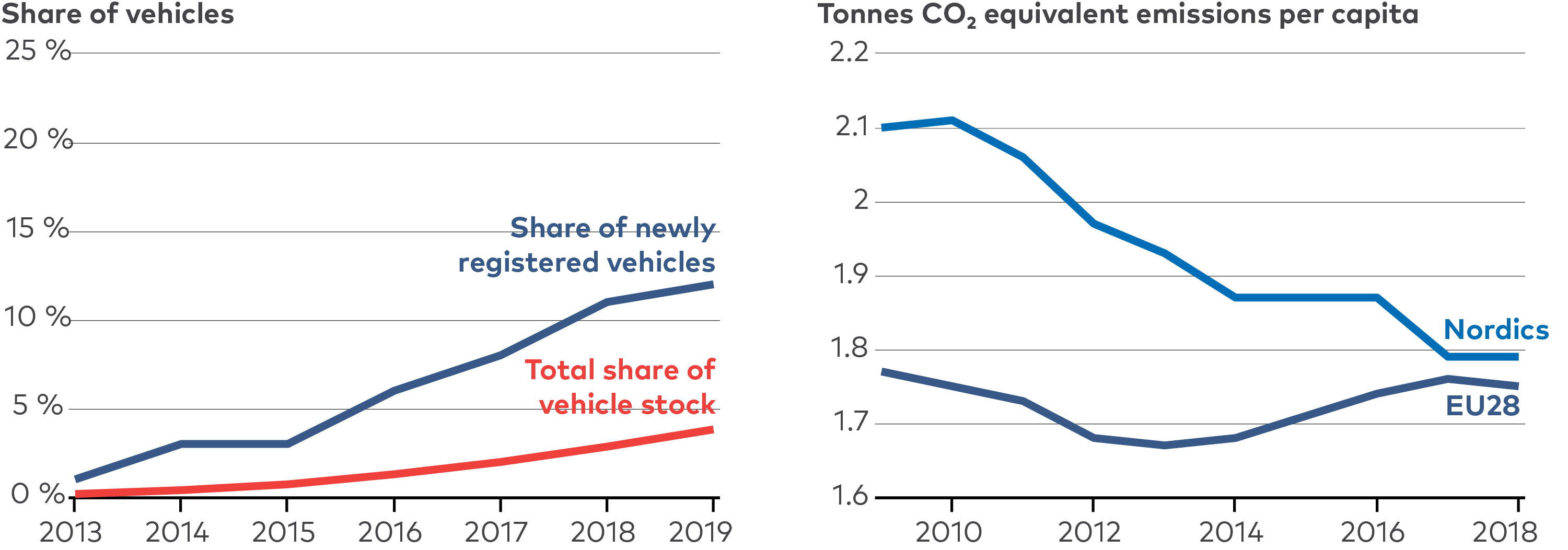

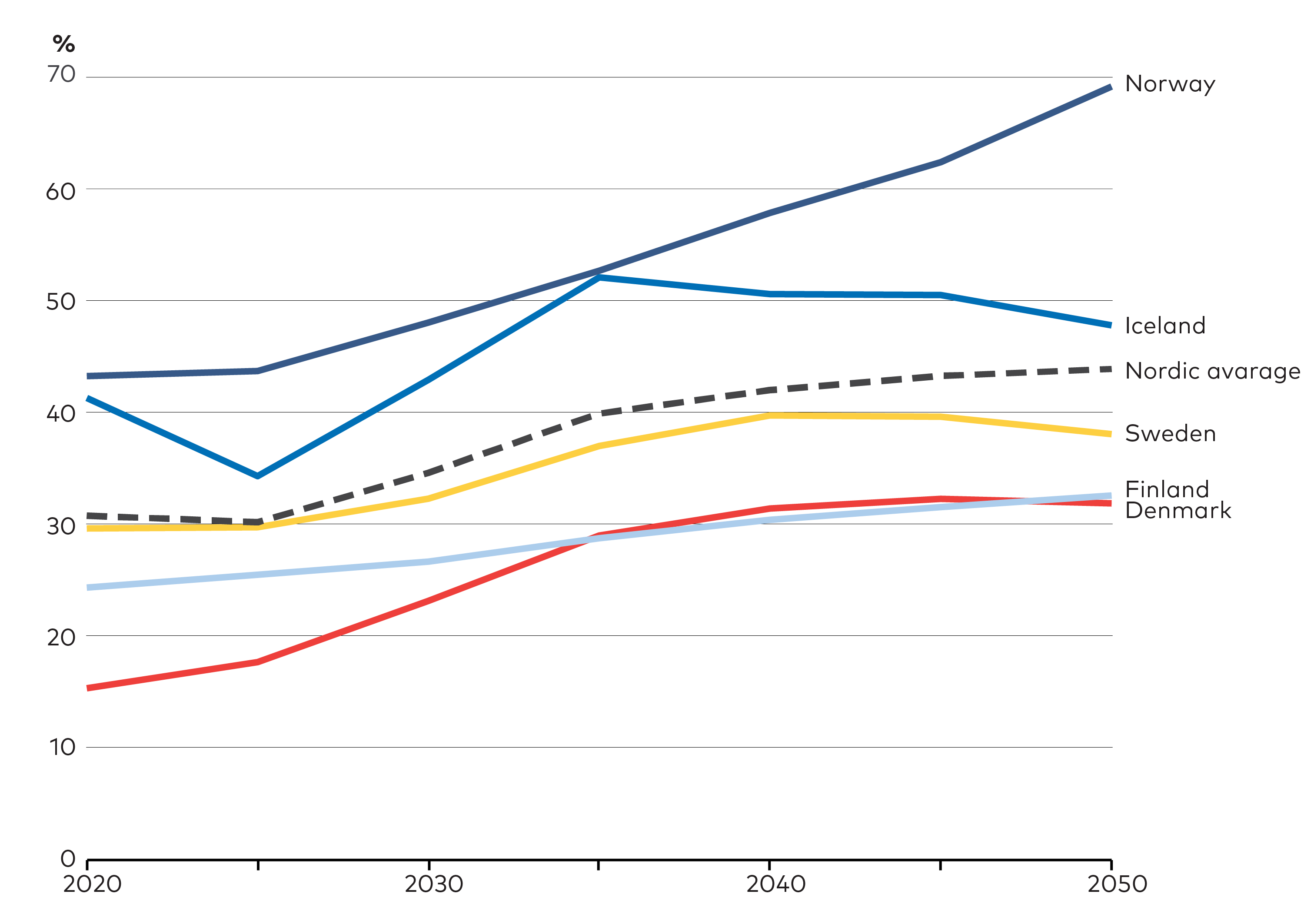

Electrification in passenger transport has started but need continued acceleration over the next decade.

Figure 1.9a & c. Percapita emissions in road transport. The left panel shows the growing share of newly registered BEV and PHEVs in the Nordics and the overall share of the total passenger vehicle stock. The right panel shows the resulting emission reduction in the Nordics generated from road transport in comparison to EU28 from 1990 to 2018. Source: EEA, 2020; Nordic Statistics database, n.d.

1.2 Choices ahead

The idea that any individual decision will affect the entire development of the energy system is false. Rather, a multitude of choices, drivers, and events will shape the future of the Nordic energy system.

However, to fulfill their role in achieving a clean energy system, decision makers must be prepared to act decisively on factors within their control while being fully aware of the implications of those that are not. The balance and prioritisation of such efforts will influence the performance of the Nordic energy system and determine its role in Europe as a whole. Several key aspects can – and will – be affected by policy, strategic decisions in industry, and research and development efforts.

1.2.1 Choice and coupling of energy carriers

Expanding electrification as a path to carbon neutrality holds great potential but is by no means a panacea for the Nordic region or the rest of the world. Local conditions, including resources, technology options, and policy decisions, will greatly affect the degree of electrification possible. Indirect electrification through the use of electricity to produce fuels - ‘power-to-X’, including hydrogen – will likely play an important role for decarbonising some hard-to-abate sectors, but will have a dramatic impact on electricity demand. Bioenergy has distinct advantages but is not an unlimited resource. Thus, a wise use of all energy carriers in the Nordic region will be vitally important.

1.2.2 The role of the Nordic energy system in Europe

Nordic hydro and wind resources can facilitate the energy transition in other countries, and substantial potential exists to export large quantities of clean electricity and PtX fuels. Most central European countries face bigger challenges as they do not have the same endowments of renewable resources as the Nordics, although progress in new technologies and shifting policy strategies in other European countries may improve their position. Even within the Nordic region, it may be necessary to balance various - and sometimes conflicting – policy objectives. Even when it is attractive from a climate and financial perspective, large expansions of energy infrastructure are challenging for other reasons, including public acceptance, perceived and real business risks, and conflicts with other social objectives and policy targets.

1.2.3 The importance of behavioural change and energy efficiency

Energy efficiency will ease the pressure on any future energy system and the investment needed to support it. Altered behaviour perhaps could do even more. Thus, quantifying and understanding how the potential of such aspects can be realised adds value. This is particularly true given that full decarbonisation will require significant citizen engagement and support for bold policy action.

PHOTO: MAMMUT MEDIA/NORDEN.ORG

PHOTO: MAMMUT MEDIA/NORDEN.ORG

Chapter 2

Five Solution Tracks to Carbon Neutrality

Based on the NCES results, the multitude of solutions available to decarbonise the energy system can be grouped into five solution tracks: direct electrification; PtX; bioenergy; carbon capture and storage (CCS) technologies; and behavioural change. While direct electrification emerges as the core strategy, the reality is that no individual decision or technology choice will drive the transformation of the entire energy system. Rather, achieving carbon neutrality will require balancing these tracks in relation to what is technologically possible, economically viable, and socially acceptable. The role Nordic countries choose to play in the European energy transition will affect this balancing act and have significant impact on how the regional Nordic energy system develops.

Key messages

-

Five solution tracks capture most options needed to reach carbon neutrality: direct electrification; PtX; bioenergy; CCS technologies; and behavioural change.

-

Direct electrification forms the core of all NCES decarbonisation pathways, while the other solution tracks have varying importance in the different scenarios.

-

A pathway based on a balanced mix of the five tracks will likely be easier to realise than one heavily dominated by any one set of solutions.

-

Domestic Nordic energy demand decreases in all scenarios, largely because of efficiency gains linked to direct electrification.

-

The share of fossil fuels in Nordic total primary energy supply falls, from ~40% in 2020 to less than 10% in 2050, across the NCES scenarios.

-

Nordic electricity demand rises by 40-100% from 2020 to 2050 in the NCES scenarios, showing the increasing importance of electricity as an energy carrier.

-

Direct electrification requires much less electricity generation than the PtX solution track, as production of PtX fuels is electricity intensive.

-

Behavioural change, including efficient energy use, can ease the transition regardless of technological mix.

2.1 The Nordic system through three carbon neutral scenarios

Nordic decision makers will play a lead role in shaping the future energy system, including the role Nordic countries could play in Europe as a whole. Policy action will underpin key areas of research and development (R&D), strategic decisions in industry, and levels of public acceptance. The NCES analyses are conducted through the lens of three main scenarios: The Carbon Neutral Nordic (CNN) scenario reflects current national plans, strategies, and targets to reach carbon neutrality, and seeks to identify the least-cost pathway. The Nordic Powerhouse (NPH) scenario reflects aggressive action to build out clean energy assets and infrastructure to support activities with high demand for electricity and PtX fuels. The Climate Neutral Behaviour (CNB) scenario sees politicians and citizens adopting additional energy and material efficiency measures in all sectors, ultimately leading to lower demand for both. It also assumes higher public acceptance for energy infrastructure development. For more information about the supporting assumptions in the NCES scenarios please see the section on NCES's analytical approach at the end of this chapter.

The main conclusions and results from these three scenarios are presented in this report. The NCES project contains much more to explore and all modelling results, including sensitivity analyses, can be fully reviewed via the NCES webtool. For full access to the entire suite of NCES products please visit the NER webpage.

2.1.1 Clean electricity and improved energy efficiency in end-use sectors underpin all pathways

All scenarios contain deep decarbonisation of energy supply (Figure 2.1), resulting in rapid decline in energy-related CO2 emissions (Figure 2.2). Clean electricity (Figure 2.3) underpins fossil fuel substitution through direct electrification and is also critical for PtX and energy efficiency.

Figure 2.1. Total primary energy supply. The share of fossil fuels in Nordic primary energy supply falls from 42% in 2020 to 6-9% by 2050 in the NCES scenarios, while export of electricity and PtX fuels rises (negative values indicate exports to non-Nordic countries). *Includes minor contribution from other sources.

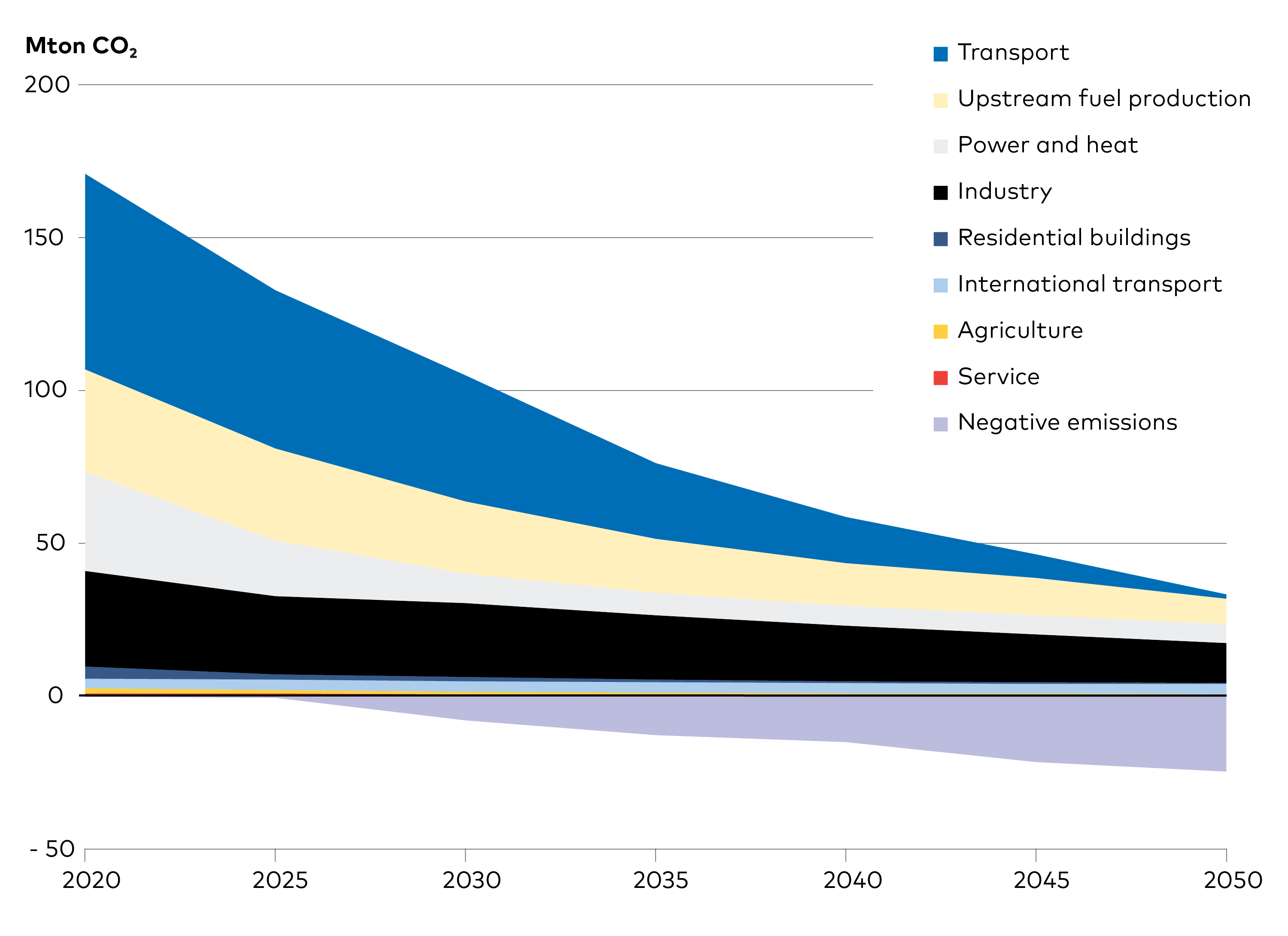

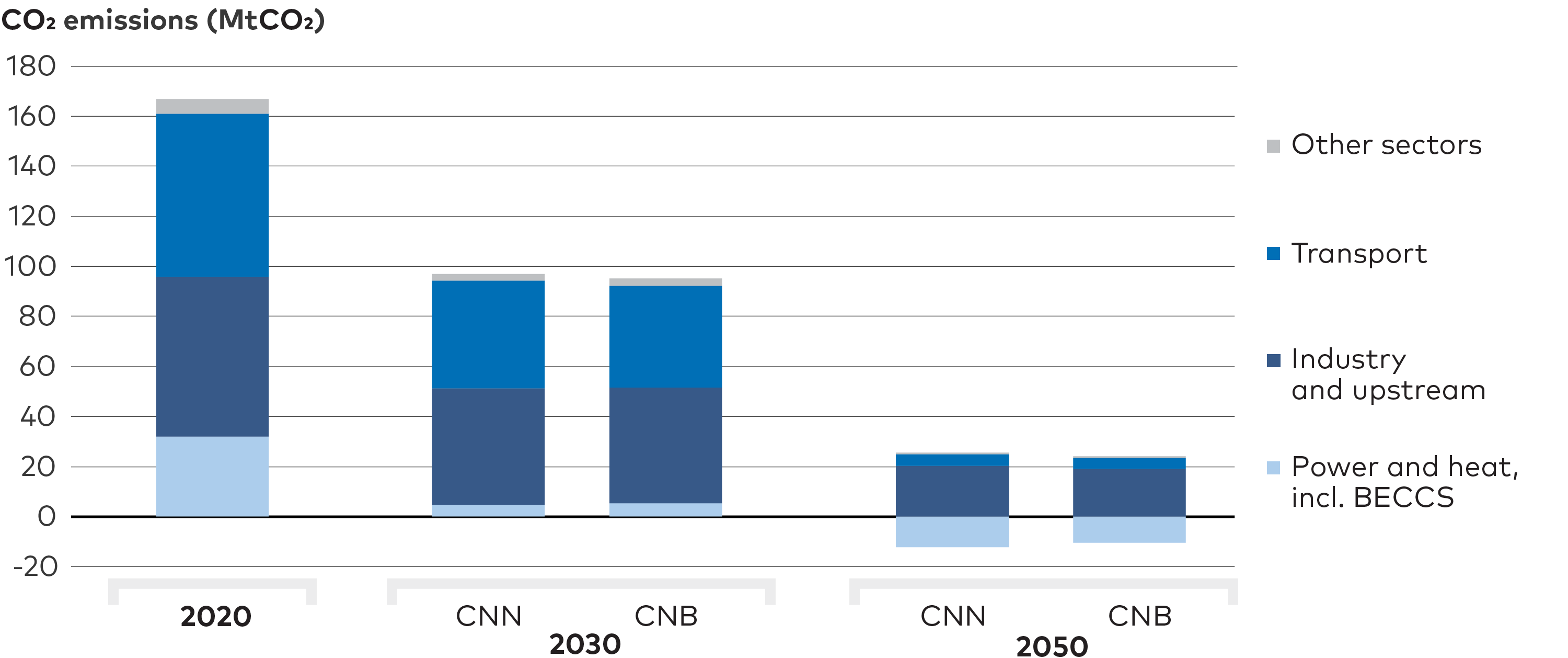

Figure 2.2. Nordic energy-related CO2 emissions - CNN scenario. Net energy-related CO2 emissions fall from approximately 167 Mt in 2020 to 13 Mt in 2050.

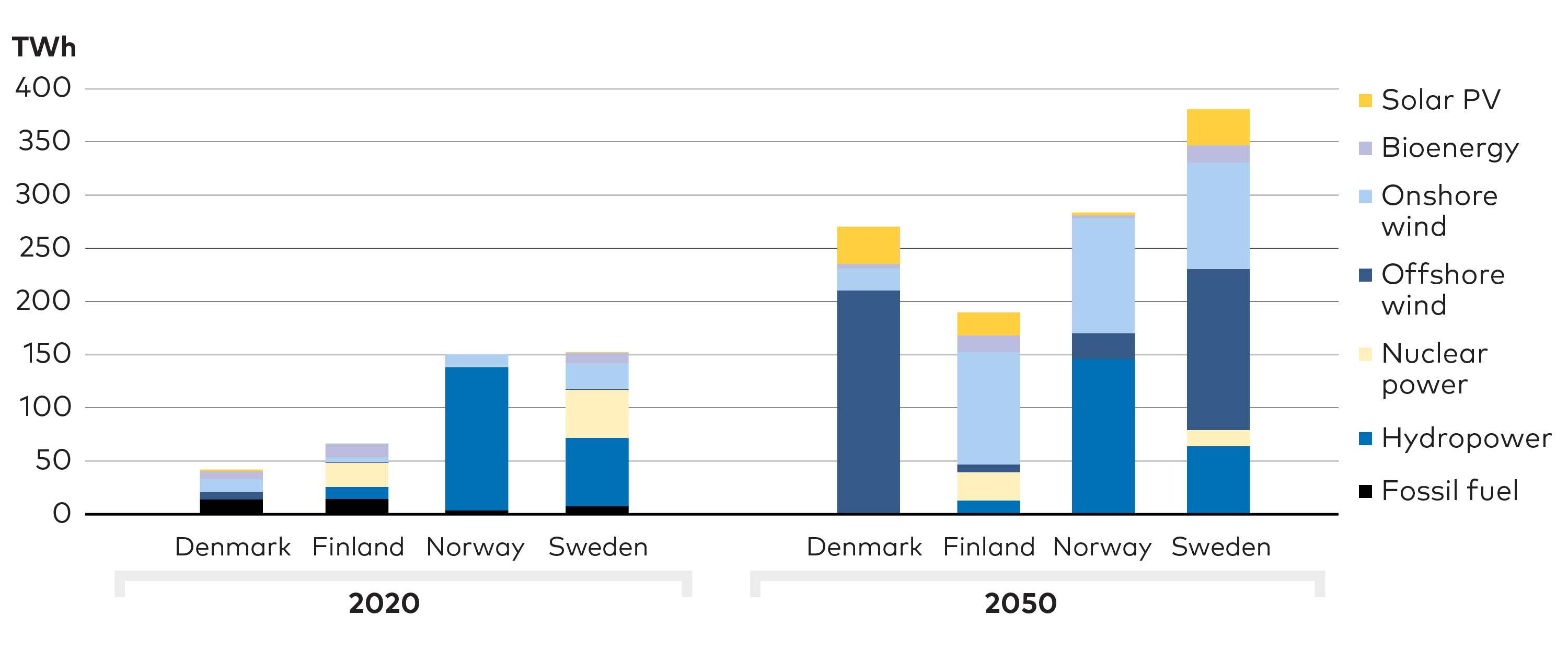

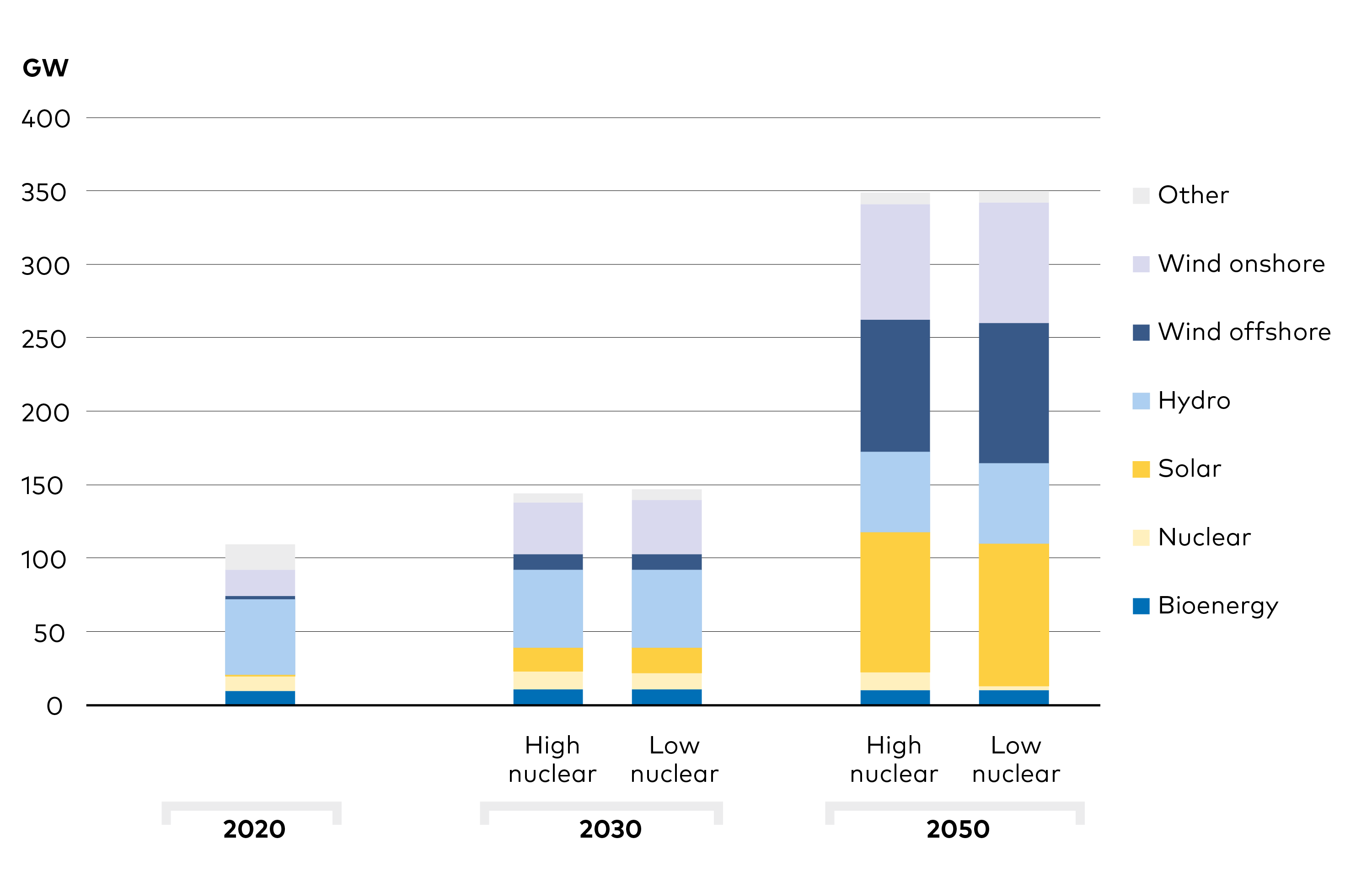

Figure 2.3. Nordic electricity generation. The fossil share of electricity generation in 2050 is below 5% in all NCES scenarios, even as generation increases from 455 TWh in 2020 to 615 TWh (CNN), 710 TWh (CNB) and 980 TWh (NPH) in 2050.

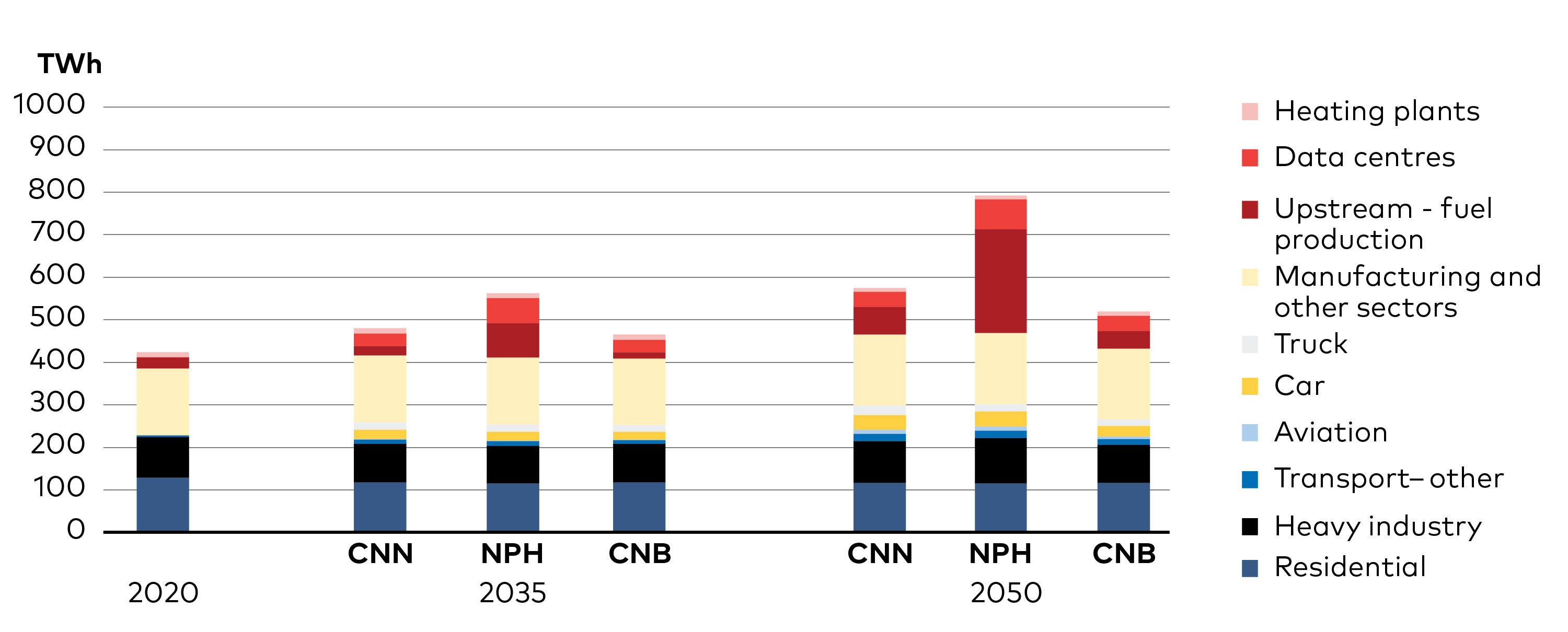

Figure 2.4. Domestic Nordic electricity demand. Domestic Nordic electricity demand increases from 370 TWh in 2020 to 450-680 TWh in 2050 in the three scenarios. Production of PtX fuels, 'upstream fuel production', is the single largest growth driver.

Nordic electricity demand increases by approximately 40% in the CNN scenario and up to 100% increase in the NPH scenario by 2050 compared with 2020 levels (Figure 2.4). Production of hydrogen and other PtX fuels is the biggest demand growth driver, as reflected in the NPH scenario.

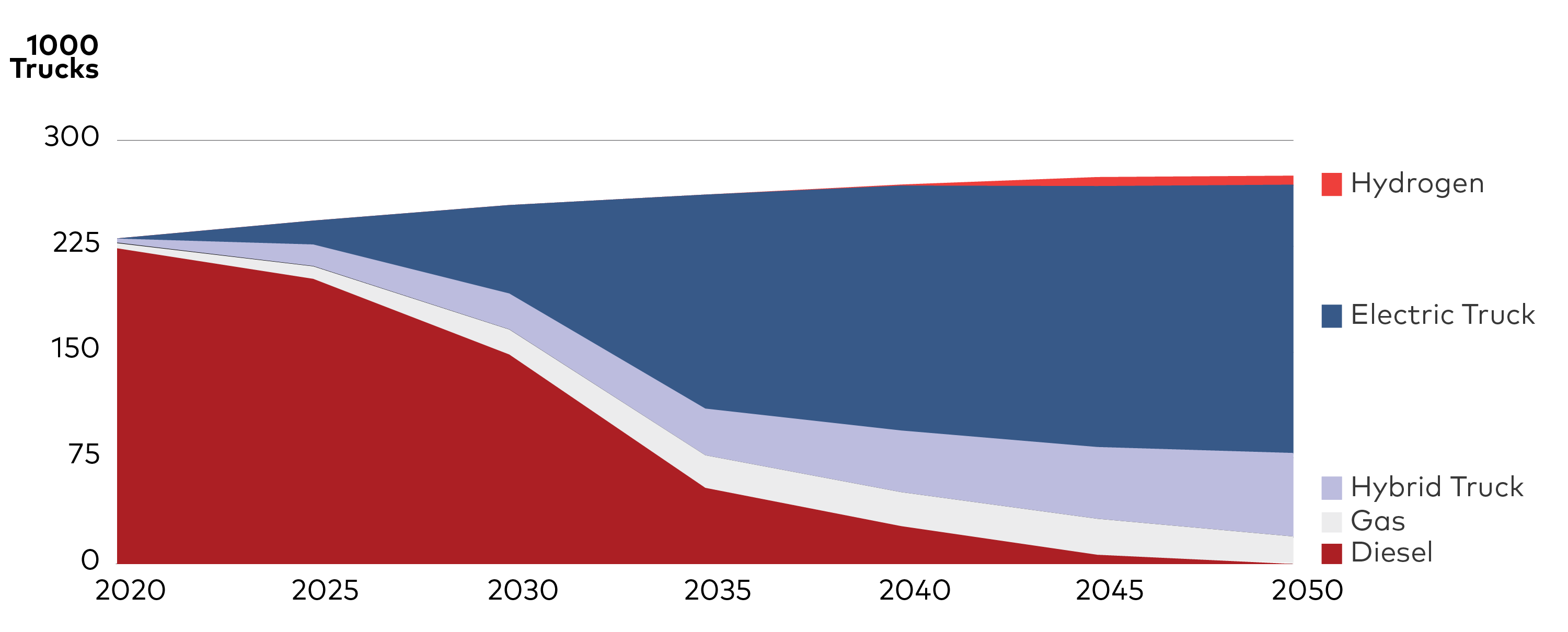

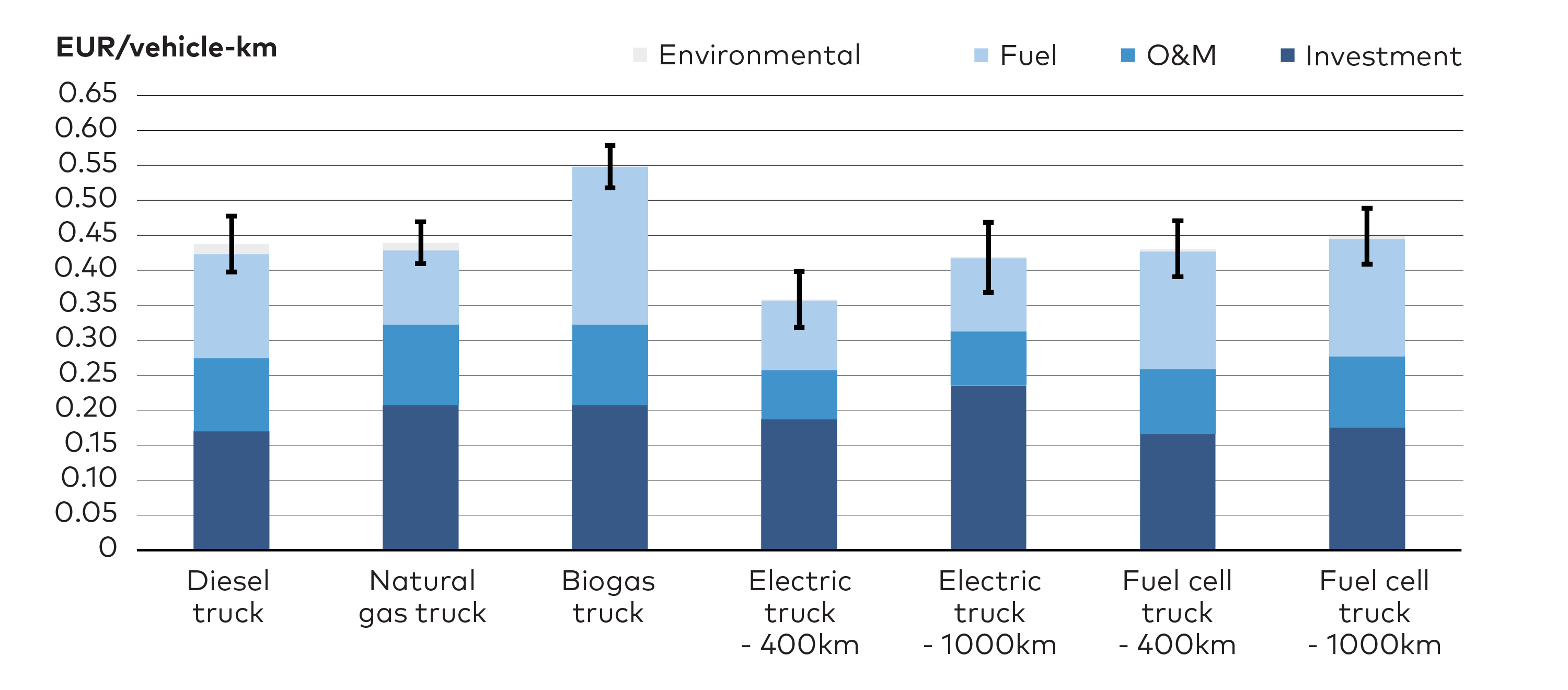

Prospects for direct electrification of end-use sectors seem more attractive now than in previous studies such as the NETP-projects (IEA/NER, 2013 & 2016). For example, in those studies biofuels, synthetic fuels, and fuel cells seemed like the cheapest option to decarbonise heavy trucks, while the NCES analysis shows direct electrification becoming competitive also for that application (Figure 2.5). This does require continued cost decreases for battery technologies and pro-active infrastructure development to alleviate charging and grid capacity challenges. Hydrogen fuel cell trucks can be an alternative route, but that looks more costly and has its own infrastructure challenges.

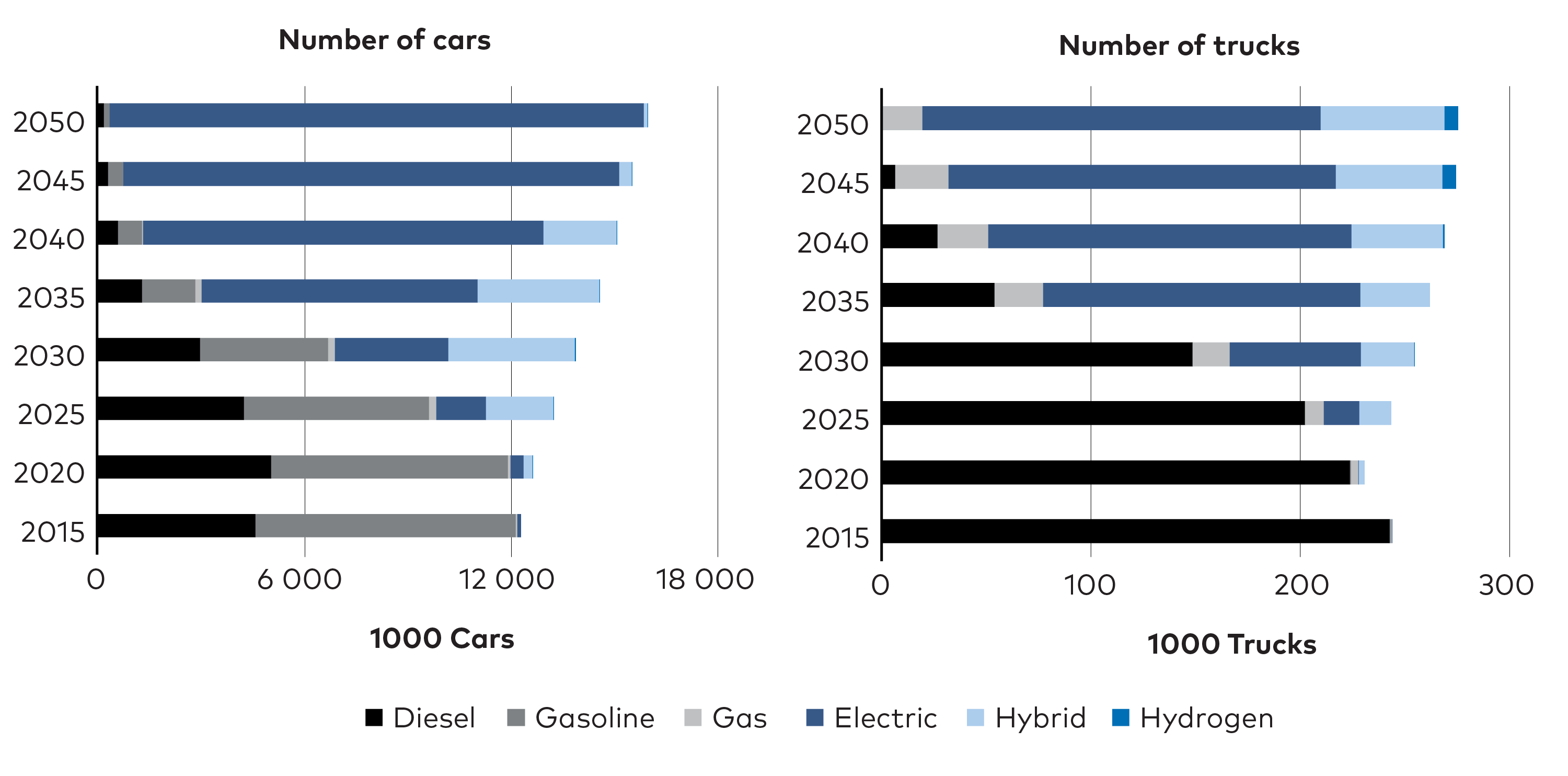

Figure 2.5. Stock development of heavy trucks in the Nordics - CNN scenario. Direct electrification, in the form of battery vehicles and/or electric roads, is seen to become competitive for heavy trucks in the CNN scenario. Both ‘diesel’ and ‘gas’ categories include increased blending of non-fossil fuels.

2.2 Five solution tracks capture most options

The Nordic region can become carbon neutral in several ways, using a mix of technological solutions, supported by behavioural changes. These can be categorised into five solution tracks (Figure 2.6).

Direct electrification is, among the five solution tracks, the most incontrovertible and remains a staple to all NCES scenarios. PtX, bioenergy, and CCS technologies – play decisive but varying roles depending on how the full range of parameters evolves. Efforts to reduce energy demand – i.e. the behavioural change track – will facilitate the transition regardless of which technology mix is used, particularly as lower demand significantly influence the need for infrastructure build out. Thus, behavioural changes constitute the fifth and last, cross cutting, track towards decarbonisation.

Figure 2.6. The five solution tracks of the Nordic Clean Energy Scenarios. The five solution tracks can be complementary. Direct electrification is the main pathway to decarbonisation, forming the core in all scenarios. The other three alternative technology tracks complement direct electrification. Behavioural change will be impactful in all pathways.

Diverse motivations drive technology development and deployment. The NCES project aims to provide a nuanced analysis of decisive factors that tip the scales towards or away from certain pathways. Ultimately, it shows that the Nordic energy transition will require a balance across all scenarios studied. All five solution tracks play different roles depending on what technological developments, political priorities, and social changes take place, and they each have advantages and barriers (Table 2.1). The sections below introduce and explain these five solutions tracks; the following chapters explore in fuller details their roles in the three scenarios.

Table 2.1. Overview of advantages and barriers of the five solution tracks.

| The five tracks towards carbon neutrality | Advantages | Barriers |

| Direct electrification | Very low emissions when sourced from clean electricity. | Batteries still have relatively low energy density. |

| Distribution system already in place. Often results in improved energy efficiency. | Less attractive for very high heat applications. Large infrastructure investments needed for e.g. heavy trucks. | |

| Power-to-X | PtX fuels typically have high energy/weight ratios. | Large infrastructure investments needed. |

| Can provide high energy flow rates Can provide flexibility to the energy system. | Energy penalty is significant. A typical commercial electrolyser for hydrogen production, for example, has an efficiency of 60-80%. | |

| Bioenergy | Readily available. | Risks of environmental damage and biodiversity loss. |

| Can directly substitute fossil fuels in many applications. | Lifecycle may span 60-100 years until carbon neutrality is achieved. | |

| Nordic countries have international expertise and technology leadership. | Increased competition for biomass from non-energy applications. | |

| Can be blended in with fossil fuels in a transition period. | ||

| Carbon Capture and Storage technologies | Would not require significant changes to production processes in industrial applications. | Few benefits beyond emissions reductions making costs harder to bear. |

| Could eliminate hard-to-abate emissions while providing feedstock for e-fuels. | Large infrastructure needs. | |

| Can provide negative emissions when CCS is combined with bioenergy (BECCS) | New value chain needs to be developed, network effects. | |

| Concern over lock-in effects, effectively supporting a continued demand for fossil fuels. | ||

| Behavioural change | Behavioural changes that lower demand for energy often have important synergetic effects influencing several sustainable development goals beyond climate change. | To have pronounced effects on the energy system, behavioural changes need to be significant. Without systemic level support for altered behaviour it will have low effect. |

2.2.1 Direct electrification, the central pillar of decarbonisation

The combination of fossil free, clean, electricity and direct electrification is key to reducing emissions in all end-use sectors in all three NCES scenarios.

Falling costs for renewable electricity generation, a distribution grid that already reaches most end-users, and accelerating development of electric end-use technologies make direct electrification central to a decarbonised Nordic region.

Additionally, clear paths exist for electrification of several emission-intensive sectors and applications, such as light-duty transport, and many applications that require heat. In fact, electrical processes are often more efficient than thermal ones. An EV, for example, can convert 80-90% of energy stored in its battery into mobility; an internal combustion engine in a car rarely reaches 25% efficiency.

These factors together result in electricity’s share of final energy consumption rising from approximately 30% in 2020 up to 50% by 2050 in the NCES scenarios.

In short, the NCES project finds that direct electrification built on clean electricity, is likely to play a larger role than suggested by many previous studies, including the NETP projects. This underlines the need to accelerate implementation of direct electrification technologies and infrastructure even though other more immature technologies will play crucial roles in the long-term. It also aligns with trends over the last 10 years, with most developments pointing toward increased rates of electrification. Still, the way forward depends on developments in competing technologies and the conditions created to support generation and distribution of electricity. Direct electrification is no panacea. In applications that require high temperatures, high energy density in storage, or high energy flow rates electrification has limitations. It is clear, however, that direct electrification is quickly becoming competitive in many applications in all sectors of the economy (Table 2.2).

Table 2.2. Long-term competing technology tracks for direct electrification in the NCES.

| Direct electrification competes with | Heavy-duty transport | Industry | Heating |

| PtX | X | X | X |

| Bioenergy | X | X | X |

| CCS/BECCS | X | X |

2.2.2 PtX fuels offer high density, high energy flow rates, and impressive versatility

PtX refers to electricity conversion and reconversion processes used to produce and store fuels, with the ‘X’ denoting the resulting fuel. Options include ‘power-to-’ ammonia, chemicals, fuel, gas, hydrogen, liquid, methane, food, power, and syngas. This report uses ‘PtX fuels’ to refer to all these fuels.

PtX fuels, such as hydrogen, is rapidly gaining attention in discussions for global energy planning, including in the Nordic countries, as it offers some of the advantages lacking with direct electrification.

PtX fuels can, for instance, deliver higher energy flow rates and higher temperatures compared to direct electrification in most applications, making such fuels a strong contender to replace fossil fuels in industry. Several high-profile projects are in the demonstration phase, such as hydrogen-based steel production to replace coal and blast furnaces. Decarbonisation of steel, and the choice of technology to do so, will significantly impact the entire Nordic energy system and associated infrastructure needs.

PtX fuels such as liquid hydrogen or ammonia can also offer three or four times the energy/weight ratio (gravimetrical density) compared with a lithium-ion battery. Beyond industry applications, in the NCES scenarios hydrogen and other PtX fuels come into use in heavy-duty road transport, fishing and other maritime applications, and aviation, where weight is a critical parameter.

PtX can also provide flexibility to the energy system, for example by using electrolysis to balance hydrogen production to align with fluctuations in electricity generation. The excess heat of electrolysers can be used in district heating, and the Nordic countries are well positioned in that regard. As PtX fuels can be a feedstock in chemical processes, in this application they offer both a source of flexibility and additional potential revenue stream. Electrolysers are capital-intensive, however; at present, their economics depend on high utilisation rates, which limits this flexibility potential. In addition, significant increase in demand for PtX fuels would also require a lot of dedicated generation.

Finally, the distribution factor needs to be considered. At least over long distances, transporting hydrogen can be less costly per kilowatt hour than transporting electricity.

In the NCES scenarios, PtX mainly competes with direct electrification and biofuels in transport, with fossil fuels combined with CCS in industry, and BECCS in power generation and district heating (Table 2.3)

Table 2.3. Long-term competing technology tracks for PtX in the NCES.

| PtX primarily competes with | Transport | Industry | Power and heat generation |

| Direct electrification | X | X | |

| Bioenergy | X | X | X |

| CCS/BECCS | X | X |

The primary drawback of PtX is that it is electricity-intensive and, compared with direct electrification or biofuels, carries a substantial energy penalty. A typical commercial electrolyser for hydrogen production, for example, has an efficiency of 55-80% (power to hydrogen). If hydrogen is used to produce electricity in a fuel cell to power a heavy-duty truck, the total round-trip efficiency from power-hydrogen-mobility is currently typically well below 50%. Other weaknesses of the PtX solution track include lack of infrastructure for production and distribution of fuels (in particular for hydrogen), and immature end-use technologies.

2.2.3 Bioenergy is important but limited, as increased use raises sustainability concerns

Bioenergy can be used directly, for example for heat in industry, or converted into other solid or liquid fuels. As such, it shares many of the advantages of PtX in terms of versatility and potential to directly substitute fossil fuels. Biofuels can be processed to have chemical properties almost identical to fossil counterparts, making them attractive as ‘drop-in’ fuels and easy to use in transport and industry applications. Some biofuel production processes are already mature, such as conversion of food crops or some forestry products, while technologies such as gasification or pyrolysis require further commercialisation. Although future cost projections are uncertain, currently it is cheaper to produce synthetic fuels through the bioenergy route than through PtX.

Bioenergy already plays an important role in the Nordic energy system and continues to do so in all NCES scenarios where it is used extensively for district heating. In the short- to medium-term, biofuels will continue to play an important role as a market ready alternative to PtX fuels and electrification for heavy-duty transport. Across the long-term NCES scenarios, bioenergy will primarily compete with direct electrification for heating, with PtX fuels in transport and industry, and with fossil fuels combined with CCS in industry. Considering expected advances in electrification and other technologies for sustainable fuel production, progress in biorefinery technologies must accelerate to remain competitive – particularly as demand for biomass for applications other than energy is expected to increase, for instance from the chemical industry.

Table 2.4. Long-term competing technology tracks for bioenergy in the NCES.

| Bioenergy primarily competes with | Heavy-duty transport | Industry processes | Heat |

| Direct electrification | X | X | |

| PtX | X | X | |

| CCS/BECCS | X |

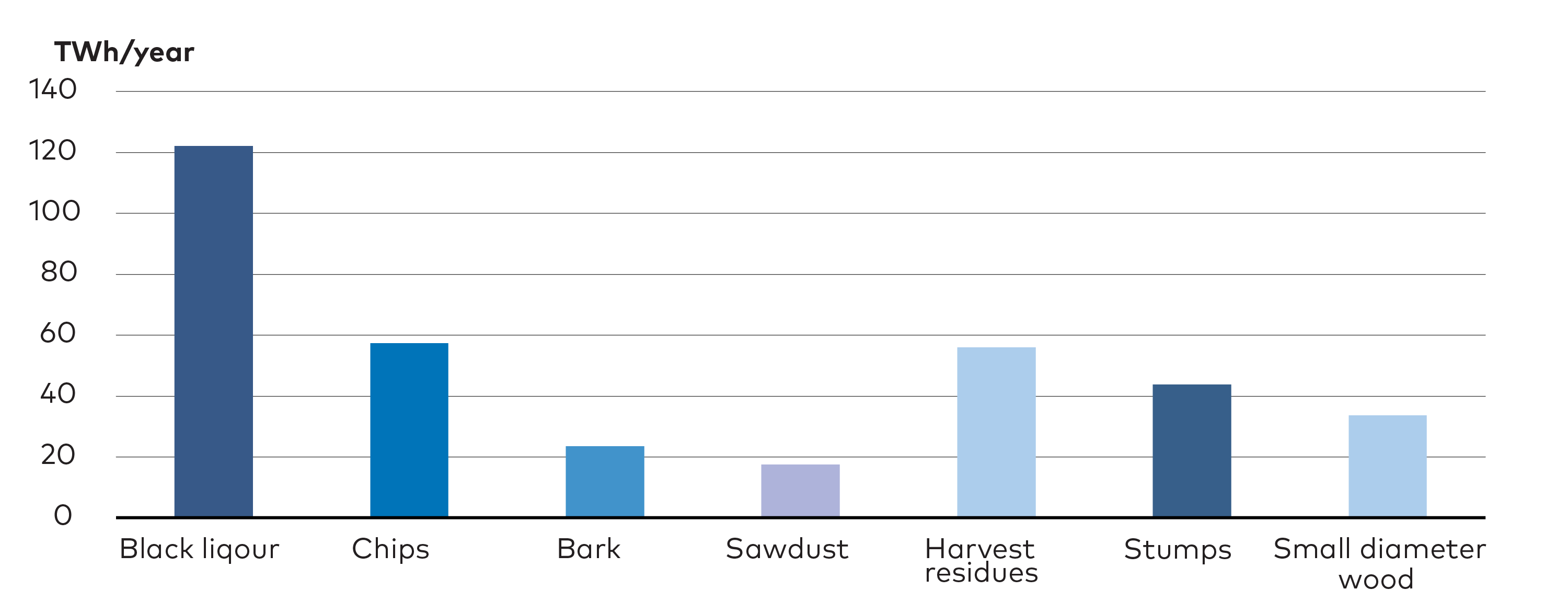

Ensuring a sustainable supply of bioenergy, particularly as demand rises, will be very important. While there is a large and growing stock of wood biomass available in the Nordics, provision of other ecosystem services from forests, and retained biodiversity, needs to be ensured.

The NCES analysis uses the same carbon accounting principles as the United Nations framework convention on climate change (UNFCC), where bioenergy is regarded as carbon neutral. Use of forest biomass for energy will increase atmospheric GHG concentrations in the short-term, whereas sustainably managed bioenergy has lower emissions than fossil energy over the long-term. Here, contextual parameters such as timing and production qualities make a difference. For this reason, it is critical that wood used for energy to the largest possible extent is based on waste and residues from forest products that stores carbon long-term, such as sawn wood used in buildings and furniture.

Sourcing is also of concern as, already today, the Nordic countries import a significant portion of the bioenergy used. Given increasing pressure on land use in most parts of the world, scaling up bioenergy production will be challenging.

2.2.4 CCS technologies work in hard-to-abate applications and enable negative emissions

Cement, and iron and steel manufacturing are notoriously energy and emission intensive sectors, with carbon emissions emanating from the processes themselves rather than from fuel combustion only. Rather than changing fuels or altering processes, it may be more cost-effective to capture and permanently store the resulting CO2. Since CCS basically allows the current processes to go on unchanged, albeit with some energy penalty, it offers a relatively straight forward solution with the potential to unlock room within the carbon budget across all sectors to ease the decarbonisation transition of the Nordic economy. Adding capture technology to a cement plant, for example, and transporting it to an underground facility for permanent storage could ensure that ~90% of potential CO2 emissions are never released to the atmosphere. This without fundamentally altering the basic production process or its feedstock.

While the technology may be effective, cost is a significant weakness of CCS: it drives up production costs while adding no extra value to existing products or outputs. This differs from EVs, for example, which in comparison to internal combustion engine vehicles (ICEVs) deliver additional value through reduced air pollution, less noise, and lower maintenance costs. Thus, even if the cost of CCS falls, the technology will continue to rely on carbon policies to make it competitive.

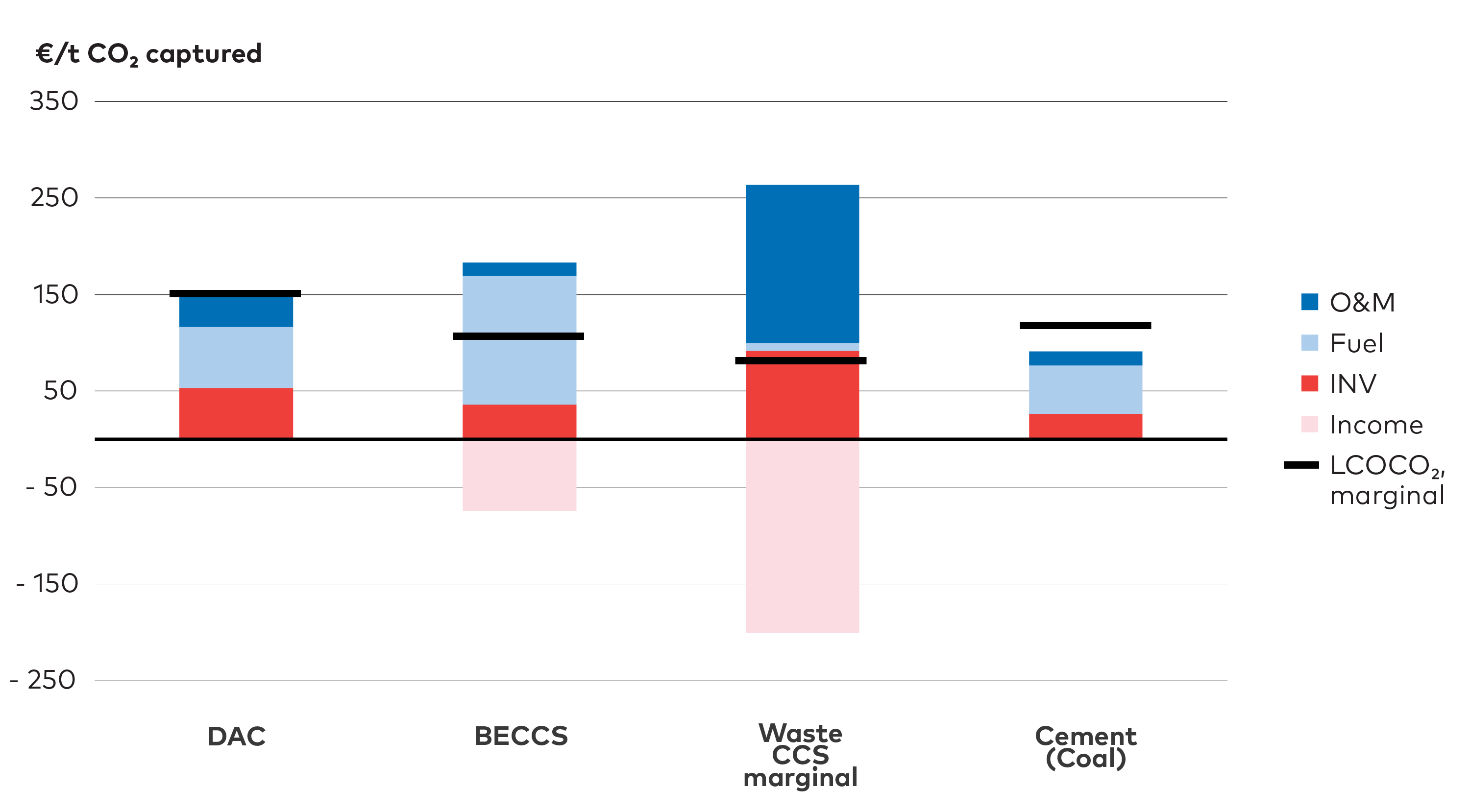

The combination of bioenergy and CCS (BECCS) can result in negative emissions. Once markets for negative emissions are developed, this could create an additional revenue stream for the operators of such plants. Additionally, some PtX fuels, such as e-methane, require CO2 that could be supplied through CCS. Combining biorefineries with CCS could be an interesting route for producing PtX fuels, which is an example of carbon capture and utilisation (CCU). As Nordic countries possess leading international expertise in the bioenergy and chemical sectors, this could be a particularly interesting avenue to pursue. The carbon benefit of CCU applications depends on the CO2 being captured and stored at the end of the lifecycle however, otherwise emissions are merely being delayed.

Direct air capture (DAC) is another emerging CCS technology. Rather than constraining emissions at point sources, DAC actively pulls existing CO2 from the ambient air. For DAC to become competitive, capture rates must be increased significantly while costs reduced dramatically. Current DAC technologies are much more energy intensive than, say, capturing CO2 from the flue gas at a power plant, mainly because of the much lower CO2 concentration in the air.

All NCES storylines include CCS in hard-to-abate industry sectors and some level of BECCS in refineries and district heating. The sensitivity analyses carried out in the project suggest that, should Nordic countries further tighten their climate targets, using more CCS and BECCS would likely be cheaper than eliminating fossil fuels completely.

CCS and BECCS mainly compete with PtX in industry, with hydrogen-based steel as a prime example of an alternative route to CCS (Table 2.5). They are also competitive with electrification of district heating. Combining CCS with conventional hydrogen production from natural gas, so-called blue hydrogen, could offer an alternative route to electrolysis for production of CO2-free hydrogen (see Chapter 4 for additional insights on PtX and blue hydrogen).

Table 2.5. Long-term competing technology tracks for CCS & BECCS in the NCES.

| CCS/BECCS competes with | Heavy-duty transport | Industry processes | Heating |

| Electrification | X | ||

| PtX | X | X | |

| Bioenergy | X | X |

2.2.5 Behavioural change could accelerate the most beneficial and cost-efficient transition

Behavioural changes that lower demand for energy could have important knock-on effects in the transition to carbon neutrality, including reduced investment in associated infrastructure regardless of which technology mix is pursued.

Behavioural change that lowers demand for energy can take many forms, with varying drivers and time perspectives. Short-term changes can be prompted through altered prices; higher fuel prices, for example, tend to reduce overall demand for transport services. Technology development can make it easier and less costly for consumers to choose more carbon-efficient options, such as an EV instead of a diesel vehicle. Shifting to new ways of meeting demand could deliver even larger impacts. In transport, modal shifts or transitioning to mobility as a service supported by autonomous vehicles are such examples. More radically, long-term changes in personal preferences may produce even larger shifts that further reduce energy demand.

Behavioural changes thus need to be understood at the individual level as well as at the systemic level. System level facilitation and technological development is needed to support day to day decisions that are more sustainable. The acceleration of short- and long-term developments is therefore dependent on shifts in policy, industry, as well as among citizens. Such shifts and actions need to recognise complex and non-technical aspects such as economic distribution, perceived fairness, and justice. This highlights the benefits of action in all dimensions related to behaviour: prices must incentivise efficient use of resources within the current regime, consumers must be encouraged to choose the best technologies available, and technologies and services that enable citizens to meet their preferences in radically more efficient ways need to be developed. Political ambition and leadership provide the foundation for such systemic shifts, ranging from the short- to the long-term.

The NCES explores the potential impact of some of these aspects, focusing on changes in transportation habits, attitudes toward onshore wind and CCS, as well as a shift in diets. Within the scope of energy system modelling, the scenarios include assumptions for reduced industry production and freight, higher acceptance of onshore wind, more efficient passenger transportation, and reduced agricultural emissions.

Under such assumptions, the need for new infrastructure decreases, and with it the overall cost of reaching carbon neutrality. Additionally, reduced Nordic demand could enable higher electricity export, generating additional revenue while facilitating the European clean energy transition.

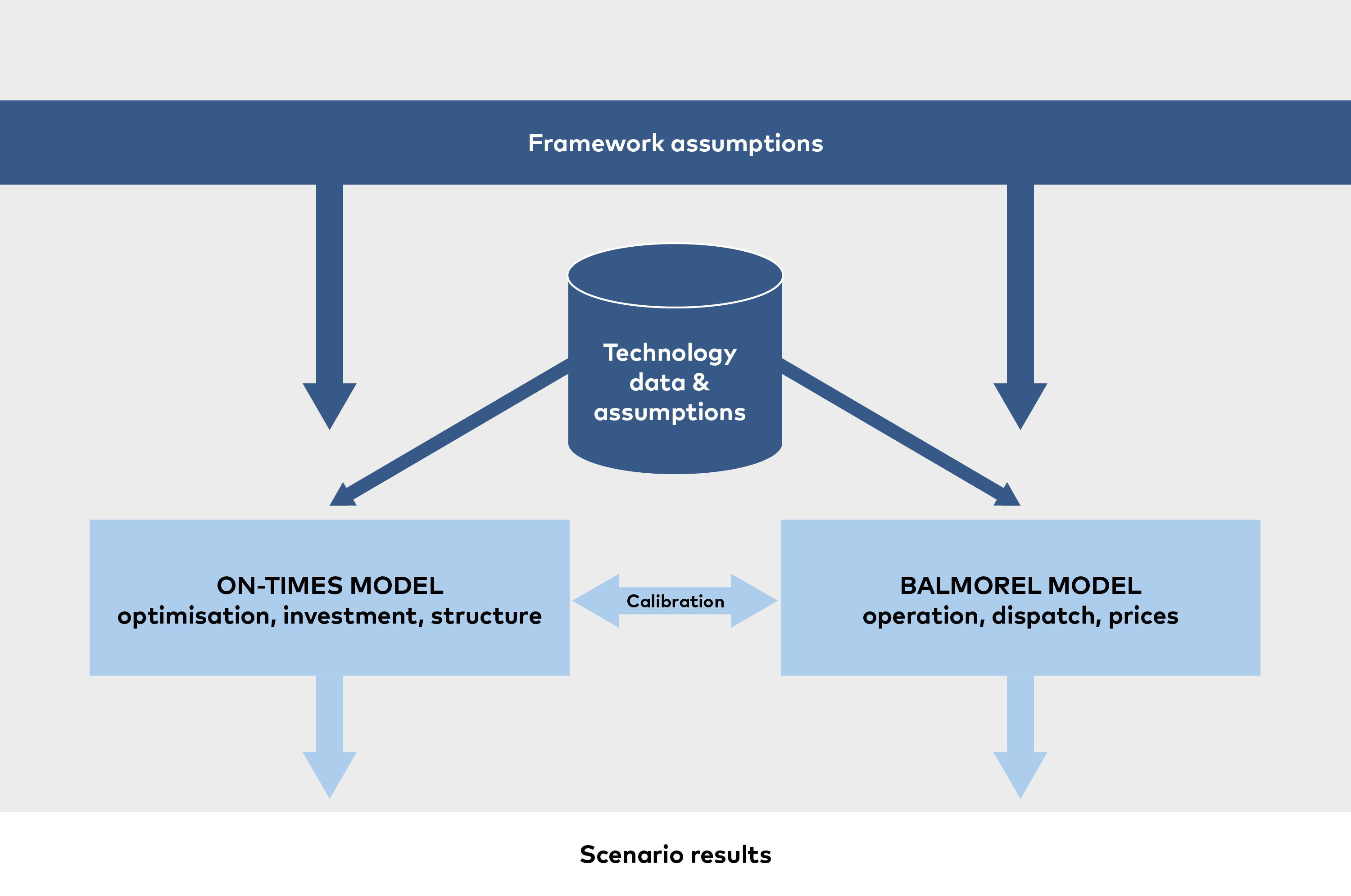

THE NCES ANALYTICAL APPROACH AND BASIC ASSUMPTIONS

Quantitative energy system modelling provides the backbone of the NCES analyses. Two modelling approaches are combined; optimisation analyses of investments in all sectors using the ON-TIMES model, and dispatch and operation analysis focused on the electricity system using the BALMOREL model (Figure 2.7). The sectors covered and their definitions are given in Table 2.6. ON-TIMES covers the five Nordic countries. BALMOREL covers Austria, Belgium, Czech Republic, Denmark, Estonia, Finland, France, Germany, Italy, Latvia, Lithuania, Luxembourg, Netherlands, Norway, Poland, Sweden, Switzerland, and the United Kingdom. Note that Balmorel does not cover Iceland. Therefore, the PtX cases described in Chapter 4 does not include Iceland. Additionally, all numbers for 2020 in the report are modelled results and may differ from official statistics.

Figure 2.7. The analytical toolbox of the NCES includes both qualitative and quantitative methods. Two energy system models, ON-TIMES and BALMOREL, were soft-linked to provide the quantitative backbone of the project. ON-TIMES is a linear optimisation model that covers all Nordic countries and all sectors shown in Table 2.6. BALMOREL is focused on the operation of the power and heat sector, including distribution and trade. BALMOREL covers 18 countries in northern and central Europe. Framework assumptions were informed by literature reviews and extensive stakeholder input.

Table 2.6. Overview of sector definitions used in the NCES analyses.

| Upstream/fuel production | Power and heat | Heavy industry | Other sectors | Residential | Transport |

| - Exploration/-mining of oil, gas and coal - Fossil refineries - Renewable refineries and biogas - PtX plants - CCS plants and storage | - Thermal power plants (fossil, bioenergy, and waste) - Nuclear - Variable renewables (wind, solar) - District heat production (incl. excess heat) - Geothermal energy | -Pulp and paper -Mining - Iron and steel - Aluminium -Cement | Manufacturing industries - Food - Chemical - Machinery - Wood products Services - Heating of commercial buildings - Use of appliances - Data centres - Other services Agriculture - Energy consumption in buildings and work machines | Appliances - Computers - Cooking - Lighting - Refrigeration - Machines - Other Heating - Buildings – before/after 1970 + new buildings (urban, suburban, rural) - Heat savings - Heat supply (individual boiler, district heat | Passenger - Car - Bus - Train - Bike - Walking - Ferries - Aviation Freight - Van - Truck - Train - Ship - Aviation International transport - Modelled separate from national transport |

The NCES scenarios are designed to reflect that cost is but one parameter to consider when assessing the many pathways by which Nordic countries – and the region as a whole – can achieve carbon neutrality. Moreover, technological progress depends on other societal developments, research and development priorities, industrial policies, level of Nordic collaboration, and which role the Nordic region wishes to play in Europe.

To capture this complexity of social, economic, and technological drivers, constraints and technology assumptions vary between the three main scenarios. Detailed descriptions and projections of technology costs and performance underpin the analysis. These assumptions are documented in the NCES technology catalogue, which can be downloaded at the Nordic Energy Research website. In addition, sensitivity analyses and scenario variants were set up to shed light on key issues. The scenario definitions were informed by literature reviews and a series of expert workshops conducted in 2020 and the main defining assumptions are summarised in Table 2.7.

Table 2.7. Table on the three main scenarios and primary assumptions.

| Key assumptions | Carbon Neutral Nordics, CNN | Nordic Power House, NPH | Climate Neutral Behaviour, CNB |

| Low bioenergy sensitivity variant | Biomass imports are linearly reduced from today’s levels to 0 in 2050 for all Nordic countries. 25% lower domestic bioenergy potentials. | ||

| High cost of CCS sensitivity variant | The total carbon abatement cost is increased by approximately 30 €/ton CO2, equivalent of 20-60% depending on technology. | ||

| GHG targets | National targets | ||

| Heavy industry | Sectoral production volumes from national projections. | Same as CNN except for in aluminium, and iron and steel where production is assumed to increase by 10% in 2050 compared to CNN. | Same as CNN up until 2030, thereafter reduces by 10% compared to CNN until 2050. |