- Front page

- Image - page 2

- Contents

- Authors and Editors

- Harry Flam and Oskar Nordström Skans: The Nordic economies and the COVID-19 pandemic

- Torben M. Andersen, Steinar Holden, Seppo Honkapohja: Economic developments and policies during the COVID-19 crisis – Nordic experiences

- Werner Eichhorst, Johannes Brunner: Labour market and social policy responses to the COVID-19 pandemic in the Nordic countries – A view from the outside

- Comment by Ragnar Arnason

- Gylfi Zoega: Iceland’s fight against COVID-19 – An economic perspective

- Comment by Svend E. Hougaard Jensen

- Comment by Gylfi Magnússon

- Lars Hultkrantz, Mikael Svensson: The economic cost of COVID-19 – Iceland, Norway, and Sweden

- Comment by Tuulia Hakola-Uusitalo

- Comment by Ulf Persson

- Caroline Hall, Inés Hardoy, Martin Lundin: Schooling in the Nordic countries during the COVID-19 pandemic

- Comment by Hjördis Hardardottir

- Comment by Hanna Virtanen

- Kristiina Huttunen, Hanna Pesola: COVID-19 and labour market outcomes by gender in Finland

- Comment by Birthe Larsen

- Comment by Helena Svaleryd

- About this publication

MENU

Contents

This publication is also available online in a web-accessible version at https://pub.norden.org/nord2022-001

Authors and Editors

Editors: Harry Flam and Oskar Nordström Skans

Technical Editor: Hedda Thorell

Harry Flam, professor emeritus, IIES, Stockholm University.

Oskar Nordström Skans, professor, Uppsala University.

Torben M. Andersen, professor, University of Aarhus.

Steinar Holden, professor, University of Oslo.

Seppo Honkapohja, visiting professor, Aalto University School of Business.

Werner Eichhorst, professor, IZA institute of Labor Economics.

Johannes Brunner, student assistant, IZA institute of Labor Economics.

Comment by Ragnar Arnason, professor emeritus, University of Iceland.

Gylfi Zoega, professor, University of Iceland.

Comment by Svend E. Hougaard Jensen, professor, Copenhagen Business School.

Comment by Gylfi Magnússon, professor, School of Business, University of Iceland.

Lars Hultkrantz, professor emeritus, School of Business, Örebro University.

Mikael Svensson, School of Public Health & Community Medicine, University of Gothenburg.

Comment by Tuulia Hakola-Uusitalo, research director, Competition and Consumer Authority.

Comment by Ulf Persson, senior advisor, Swedish Institute for Health Economics (IHE).

Caroline Hall, IFAU and Uppsala Center for Labor Studies (UCLS).

Inés Hardoy, research professor, Institute for Social Research.

Martin Lundin, IFAU and Uppsala Center for Labor Studies (UCLS).

Comment by Hjördís Harðardóttir, postdoctoral researcher, University of Iceland.

Comment by Hanna Virtanen, head of research, ETLA Economic Research.

Kristiina Huttunen, research professor, Department of Economics, Aalto University School of Business, Helsinki GSE, VATT and IZA.

Hanna Pesola, senior researcher, VATT Institute for Economic Research, Helsinki GSE.

Comment by Birthe Larsen, associate professor, Copenhagen Business School.

Comment by Helena Svaleryd, professor, Uppsala University.

The Nordic economies and the COVID-19 pandemic

1 Background

The Nordic countries weathered the COVID-19 pandemic relatively well compared to most other high-income countries, both in terms of public health and economic repercussions. Infection and excess mortality rates were comparatively low in the Nordic Region, except in Sweden, where they relied more on recommendations and guidelines than mandatory measures to contain the spread of the virus. The fall in GDP was also comparatively small and short-lived in all of the countries except Iceland, where tourism plays a more prominent role in the economy.

This issue of the Nordic Economic Policy Review surveys the economic repercussions of the pandemic and the health and economic policies introduced to minimise its impact in the Nordic countries. Although national policies were broadly similar, they also differed in many respects. Given that some enjoyed greater success than others, comparing different policies and their effects may yield valuable lessons for the future.

Limitations of space and time have forced us to be selective in our choice of topics. Other subjects are covered, and covered more comprehensively, in the report by the Swedish parliamentary ‘Corona Commission’ (Coronakommissionen 2022) and in the online forum voxeu.org, which summarises hundreds of studies by economists and researchers from other disciplines.

Despite these constraints, we present a broad range of policy-relevant articles on a variety of issues. Two of the articles comparing economic policies and outcomes include countries from outside the Nordic Region. The article by Torben Andersen, Steinar Holden, and Seppo Honkapohja focuses on the macroeconomy. The one by Werner Eichhorst and Johannes Brunner focuses on the labour market.

Several of the articles highlight the difficult trade-offs facing decision-makers during a pandemic. Ideally, all decisions taken to minimise the costs of a pandemic – on public health and the economy – should be made within the same framework so that the economic effects can be compared with the impact on health and general welfare. Under this approach, public health effects are expressed in monetary terms, as seen in the article by Lars Hultkrantz and Mikael Svensson. They provide an example of the health benefits of school closures compared to the costs incurred in terms of reduced learning and reduced future incomes. Based on these criteria, they conclude that schools should have remained open. Gylfi Zoega’s article discusses health and economic policies in Iceland during the pandemic and reaches a similar conclusion on this point. Decisions on public health measures were made separately from those on economic policies. Zoega argues that if decisions had considered health and economic effects together, they would have resulted in better outcomes.

School closures were an important measure in suppressing the spread of the virus. In their article, Caroline Hall, Ines Hardoy, and Martin Lundin provide a comprehensive survey of research into the effects of school closures and distance learning on learning outcomes and future earnings.

Finally, Kristiina Huttunen and Hanna Pesola investigate whether the pandemic had differential earnings effects on men and women in Finland. Sectors with a relatively large share of women employees, such as health care and hotels and restaurants, were particularly affected by restrictive measures. At the same time, it was mainly women who bore the brunt of school closures and had to stay at home and take care of the children. Their results are, perhaps surprisingly, contrary to expectations.

2 Macro-economic effects and policies

Andersen, Holden, and Honkapohja’s article describes the macroeconomic effects of the pandemic in the Nordic countries and discusses the role played by the fiscal policy measures taken to mitigate these effects on incomes, employment, and companies.

The Nordic countries suffered relatively small decreases in GDP compared to the European average. GDP dropped by approximately the same amount in 2020 in Denmark, Finland, Norway and Sweden and had recovered to pre-pandemic levels by the second quarter of 2021. The authors attribute the relatively small downturn in economic activity in the Nordic Region to a high degree of digitalisation that facilitated a significant shift from the workplace to working from home. Iceland was hit harder than the other Nordic countries and took longer to recover due to its relative overreliance on the tourism industry.

The countries all introduced various forms of job retention and wage compensation schemes. At the peak of the pandemic’s effect on the labour market, in the second quarter of 2021, 8–12 percent of all employees were affected by such policies. The loss of working hours hit young, lower-skilled and immigrant workers the hardest. Andersen, Holden and Honkapohja argue that there are compelling arguments for maintaining jobs and incomes in the face of a pandemic: the measures can be seen as insurance against shocks that are outside the control of those affected and therefore have no adverse incentive effects; they prevent the destruction of human and company-specific capital; and they serve to maintain aggregate demand, which in turn shields other, less affected sectors and helps the economy to recover more rapidly once containment restrictions are lifted. However, the authors also stress that measures must be temporary and include sunset clauses. Otherwise, they risk triggering negative incentive effects.

Companies received various forms of support; for example, subsidies for fixed costs, subsidies based on loss in turnover and injections of liquidity. The authors provide a valuable discussion of the pros and cons of these different types of support. In general, governments have to balance the costs of letting otherwise profitable companies go bankrupt and losing company-specific tangible and intangible capital and the costs in terms of poorer economic efficiency of providing support. Offering the wrong incentives, the dead-weight costs of higher taxation and the preservation of inefficient structures are some of the causes of low economic efficiency.

The scale of the fiscal measures varied across the countries. Iceland, and to a lesser extent Norway, relied more on higher public spending than the other countries, while Denmark, and to a lesser extent Sweden, resorted to deferred tax payments and accelerated spending.

The Nordic countries were comparatively successful in handling the negative economic impact of the pandemic and achieving a rapid recovery by maintaining production capacity and job matches as well as aggregate demand. Andersen, Holden, and Honkapohja ascribe this to the general structure of the Nordic societies, with their high levels of trust and cooperation, reliance on digitalisation, and well-functioning public sectors with good social safety nets.

3 Labour market effects and policies

Despite initial concerns, the economic impact of the pandemic on the Nordic countries as a group appears to have been relatively modest. Focusing on the labour market, Werner Eichhorst and Johannes Brunner’s article presents evidence of the economic impact in the Nordic Region compared to other European countries.

Several different factors are discussed. One element is the role of digital preparedness. In contrast to other countries on the continent, such as Germany, Nordic countries were more digitally prepared at the start of the pandemic. A relatively high proportion of workers (except in Norway) were already working from home before the pandemic. This helped ease the transition to a more digital economy, in which larger numbers of people could work from home, and more economic activity could take place online.

The article also suggests that pre-existing social policies were important in the face of the emerging crisis. They argue that the Nordic model, with its extensive public transfers and labour market policies, may have proved beneficial in the pandemic. It is conceivable that the impact of economic uncertainty is less pronounced if unemployed workers can receive support within existing systems rather than through ad hoc constructs such as those introduced in the US at that time.

Another factor discussed in the article was the relative health of Nordic public finances, which compared favourably to those in many other countries before the pandemic. This ensured swift support to particularly badly affected sectors. Finally, the article discusses the various measures introduced to keep companies solvent, the measures implemented to stabilise income, and labour market policies to maintain employment.

Overall, the article paints a somewhat optimistic picture of the economic resilience of the Nordic countries. The authors argue that the countries faced the economic crisis from a comparatively favourable starting point. However, they also point to the need to confront ongoing structural change to limit the impact on income distribution. These are challenges politicians in Nordic and other countries must address in years to come.

4 The disconnect between economic and health policies in Iceland

Gylfi Zoega’s article compares Iceland’s performance in macroeconomic variables, infections and deaths to the other Nordic countries, other island economies and some larger economies that are similarly reliant on tourism. He then looks at the Icelandic economy and public health during the pandemic through the lens of basic concepts of economics and political economy: cost-benefit analysis, externalities, time inconsistency and the problem of public action. His discussion of Iceland’s experience provides lessons common to all countries during the pandemic.

The salient point made by Zoega is that there was a clear disconnect between the Chief Epidemiologist’s decisions that were directed at preserving public health on the one hand and the government´s decisions that were directed at minimising the negative impact on the economy on the other. He suggests that if both types of decisions had been taken within a unified and consistent framework, such as a cost-benefit analysis, in which the increased morbidity and mortality caused by the pandemic is expressed in monetary terms as in the paper by Hultkrantz and Svensson, the social cost of the pandemic would probably have been lower. In particular, Zoega contends that measures to prevent the spread of the virus were unnecessarily costly. Preventative and control measures at Iceland’s only international airport would have been less costly than social distancing or school closures and should have been maintained during the pandemic instead of the stop-and-go pattern that ensued.

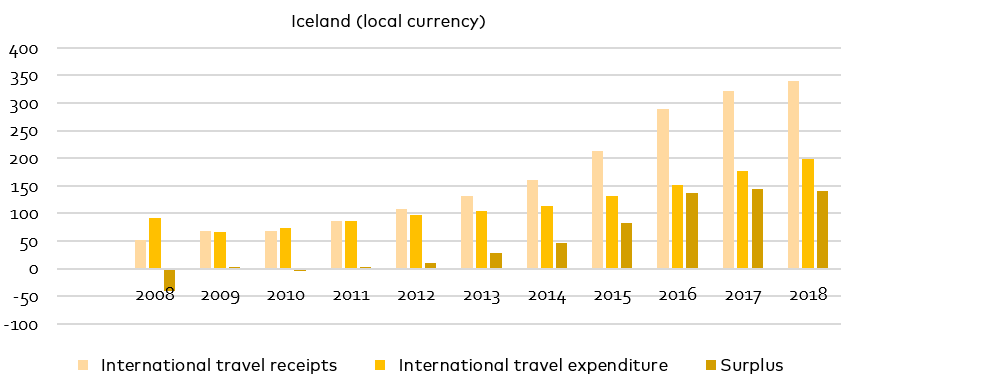

Zoega argues that the government had an inflated view of the importance of the tourism sector to the economy, which dictated its stop-and-go policy. Tourism is, however, also the main import item. An astonishing 83 percent of the Icelandic population made at least one trip abroad in 2019 and spent five times as much per day as tourists arriving in Iceland. Much of what tourists in Iceland consume is imported. Consequently, the share of tourism in GDP is not particularly high (approximately 8–9 percent) and is roughly the same as in Denmark, Finland and Germany.

The government eased containment measures to increase the inflow of tourists to Iceland as the number of infections within the country decreased. This occurred on four occasions between the start of the pandemic in 2020 and the end of 2021. It can be regarded as an example of time-inconsistency, in the same way as it may be tempting for a government to keep unemployment low by expansionary fiscal policy in the short term at the cost of higher inflation and contractionary fiscal policy in the longer term.

5 Health effects in monetary terms

The article by Lars Hultkrantz and Mikael Svensson estimates the health-related costs of the coronavirus in Iceland, Norway and Sweden from the start of the pandemic up to 15 August 2021. These costs include both premature mortality and morbidity. Sweden experienced much higher rates of mortality and morbidity per capita than both Iceland and Norway. This was most probably due in part to differences in policies. As documented elsewhere in this issue, Sweden relied primarily on recommendations to the general public and did relatively little testing early on in the pandemic, whereas Iceland and Norway relied more heavily on mandatory policies and more extensive use of testing as a preventive measure. Containment measures were adopted later in Sweden.

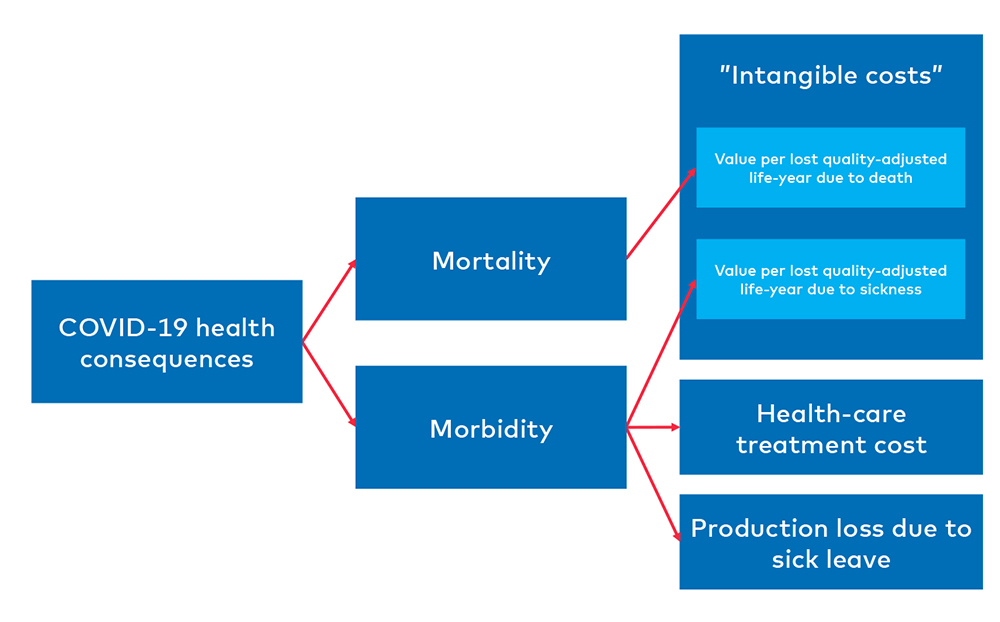

The social cost of mortality is commonly estimated by the value of a statistical life, a single figure being attached to each premature death regardless of age and health status. Hultkrantz and Svensson are the first researchers to estimate the cost of mortality in the Nordic countries based on the concept of quality-adjusted life-years. They base their estimate on people’s willingness to pay to avoid the risk of death multiplied by the estimated number of remaining life-years multiplied by the number of deaths due to COVID-19 or the number of excess deaths. The advantage of using these measures instead of the value of a statistical life is that those who died from the coronavirus were predominantly older people in comparatively poor health. Approximately 50 percent of those who died were living in nursing homes. The estimated morbidity cost is based on actual expenditure on health care, actual lost income and the intangible cost of having a lower quality of life due to illness.

The total cost of morbidity and mortality combined is estimated to equal 1.4 percent of GDP in Sweden, 0.2 percent in Norway and 0.08 percent in Iceland. This may represent an underestimation of the figures as the costs of longer-term effects of COVID-19 infections and the negative effects of social distancing and school closures on mental health and well-being are not included. It should be added that estimates based on the value of a statistical life arrive at much higher cost estimates precisely because older people in comparatively poor health were affected the most.

Ideally, it would be good to evaluate the different policy measures introduced to contain the pandemic (thereby reducing morbidity and mortality costs, which could be considered beneficial) against the economic costs of those measures. Hultkrantz and Svensson provide an interesting example of such a cost-benefit analysis. They estimate the earnings losses that upper secondary students will incur over their lifetime due to school closures against the health-cost benefits on mortality and morbidity of the closures. Intriguingly, they find that the net social cost of closures of upper secondary schools may have been high; the benefits in terms of health are estimated to be only a few per cent of the cost in terms of lost lifetime incomes.

6 School closures and distance learning

Caroline Hall, Inez Hardoy, and Martin Lundin review research on school closures and distance learning before and during the pandemic. They argue that the Nordic countries were in a better position to tackle the transition to distance learning than most other countries due to comparably reliable access to broadband and computers and high levels of digital preparedness among students, teachers and parents. Nonetheless, all of the Nordic countries underwent rapid transitions into a new style of teaching that forced many aspects of traditional schooling to change. The article accurately describes this as a transition into emergency remote teaching.

Although the Nordic countries all relied on school closures to mitigate the spread of the virus, the scope of such closures varied. In Sweden, pre-schools and schools up to ninth grade (age 16) remained open throughout the pandemic. However, even though schools remained open, many students in the Nordic countries had to participate from home due to COVID-19 symptoms or close contact with infected individuals.

The evidence presented in the article suggests that we may expect negative effects on learning from the rapid transition to distance learning. This appears to be a perception shared by teachers and students alike across the Nordic countries. The challenges of distance learning are multidimensional. There is no social interaction, and some students may lose motivation without their teachers having any real opportunity to counteract the process.

The negative effects are also likely to be unevenly distributed across student backgrounds. This makes intuitive sense as parents substitute for teachers when learning takes place in the home, which may reduce the equalising role played by schools. The article discusses the evidence supporting this intuitive and concerning conjecture. Although younger students may suffer the most from distance learning, the article notes that the learning loss may be most pronounced for upper secondary students, as they were subjected to the longest closures in all of the Nordic countries.

Overall, the results in the article convincingly show that the challenges faced by educators in the Nordic countries are likely to prevail well after the pandemic has subsided. The authors also point out that some of these learning losses may have gone undetected due to the cancellation of national exams. Dealing with the effects of learning loss among disadvantaged students is a challenge that will require the attention of policy makers for years to come.

7 Labour market effects for women and men

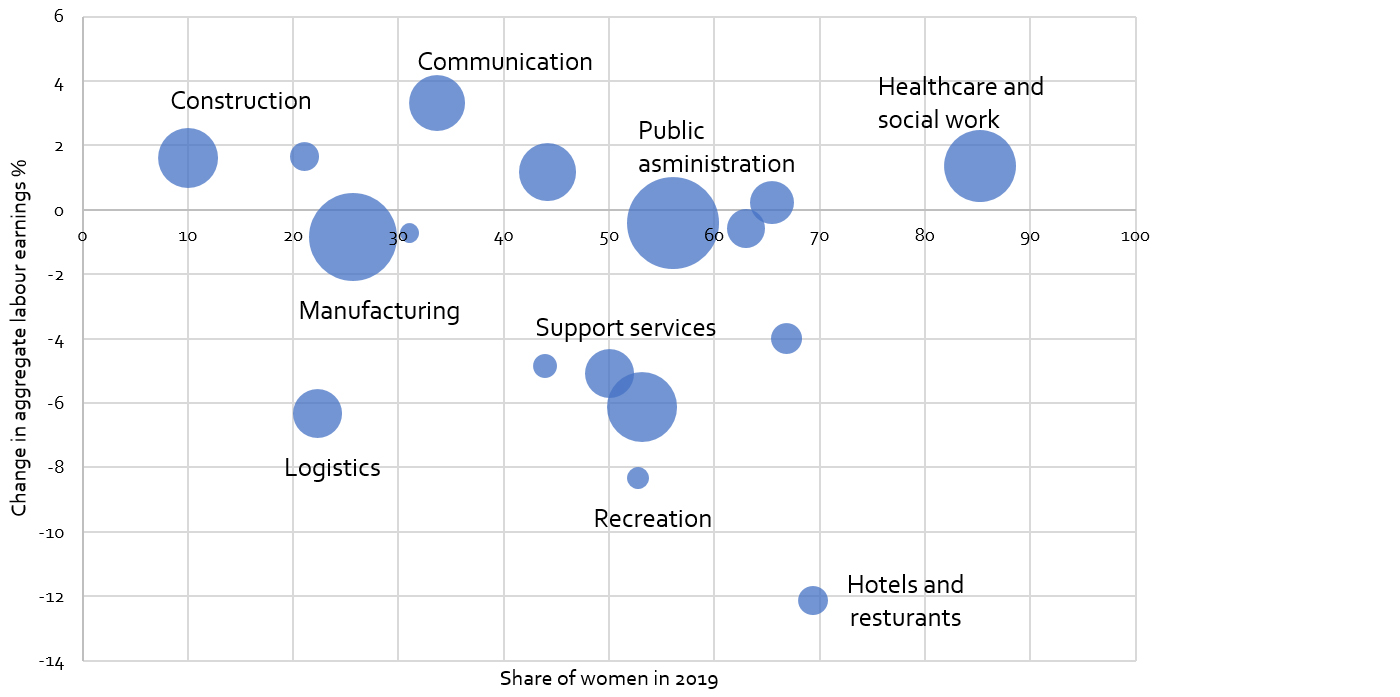

The conventional wisdom regarding economic recessions is that they predominantly affect males. The main reason is that men are overrepresented in highly cyclical industries such as manufacturing and construction and are therefore more significantly affected in terms of employment and earnings. However, Kristiina Huttunen and Hanna Pesola show that this conventional wisdom is not directly applicable to the pandemic recession.

Two factors may serve to disfavour women in this instance. The first is the large drop in labour demand in service sectors where women typically dominate, such as in hotels and restaurants. However, women are also overrepresented in the public sector, most notably in health care, where labour demand increased during the pandemic. The second factor is found on the supply side. Closures of schools and pre-schools increased the demand for working parents to provide childcare at home during the pandemic. Typically, women are more likely to bear the brunt of domestic childcare, which may negatively affect their earnings. The impact of these two factors on women’s earnings versus men is not clear a priori.

Huttunen and Pesola use Finnish register data to show how the earnings of unemployed or furloughed men and women during the pandemic were affected. Somewhat unexpectedly, overall earnings losses are shown to be considerably greater for men than for women. The greatest earnings losses occurred in the most affected sectors, as could be expected, but they were evenly distributed between men and women. In addition, the authors show that earnings losses were, in fact, neither greater nor more persistent for families with children, which is contrary to expectation. This holds true both for men and women with families.

Overall, the evidence shows that women and men suffered earnings losses due to job loss or similar during the pandemic. However, gender differences, and differences dependent on family status, were, in fact, negligible. The authors conclude that the recession caused by the pandemic seems to have been more gender-neutral than an average recession, at least in Finland.

Reference

Coronakommissionen (2022). Sverige under pandemin, slutbetänkande av Coronakommissionen [eng: Sweden during the pandemic, final report from the Corona commission]. (SOU 2022:10). Stockholm, Sweden: Coronakommissionen.

Economic developments and policies during the COVID-19 crisis – Nordic experiences

Abstract

The paper reviews economic developments and policy measures in the Nordic countries during the pandemic focusing in particular on the unconventional policies deployed to protect incomes, jobs, and firms in the short run. The recession was the deepest but also shortest on record, which indicates that the underlying economic policy logic of preserving production capacity and job matches to make a swift recovery possible worked. The policies also maintained domestic demand. The general structure of the Nordic societies, with a high level of trust and cooperation, a high degree of digitalization, and a comprehensive social safety net, contributed to the recovery process.

Keywords: Pandemic, lockdown, recession, unconventional policies.

JEL codes: E2, E3, E6, H2, H3, H5, H6, I1, J3.

1 Introduction

In response to the COVID-19 pandemic, countries have resorted to both unconventional containment policies to reduce the spread of the virus and unorthodox economic policy measures in the form of emergency or relief packages to support households, job -matches and companies.

The pandemic has had severe health and economic consequences worldwide. A summary of the development until mid-2021 is given in Figure 1, showing a cross-plot for OECD countries of the accumulated decline in economic activity relative to the fourth quarter of 2019 (2019.4), for the period 2020.1 to 2021.2, as well as the total number of confirmed deaths due to COVID-19 until the end of March 2021. Most countries have had declines in economic activity, which were unprecedented, large in scale, and abrupt compared to other crises. Global GDP declined by 9.1 percent in 2020.2 and in the Euro-area by no less than 14.6 percent. Countries that were most severely affected in terms of the health dimension also tend to have been most affected economically. These differences reflect not only different policy strategies for health and the economy but also structural differences, e.g., the importance of tourism, digitalisation, demographic factors and other related aspects.

Figure 1 The COVID-19 crisis, accumulated number of deaths and decline in economic activity per 2021.2

Of the Nordic countries, Denmark, Finland, and Norway had the mildest health and economic consequences. The economic repercussions in Sweden are at approximately the same level as the other Nordic countries, but the health consequences have been more grave. Conversely, in Iceland, the economy was severely hit, but the health consequences were mild.

In response to the COVID-19 pandemic, numerous containment policies and restrictions (or non-pharmaceutical interventions NPI) have been deployed to contain the spread of the virus. These include both containment (lockdowns, restrictions on gatherings, travel restrictions etc.) and health-oriented measures (test, trace and isolate, hygiene measures, masks etc.). Relief packages were also introduced to compensate for some of the economic consequences of the restrictions imposed, a topic to which we will return below.

There were large differences between countries in the choice of strategies to contain the virus (see Baker et al. (2021) for descriptions of different health strategies and Han et al. (2020) for a survey of strategies taken in various countries). In high-income countries in Europe and North America, most countries chose a suppression strategy, aiming to push infection rates down to very low numbers. Some countries started out with a mitigation strategy, trying to contain the pandemic to avoid capacity in health care systems becoming overwhelmed. However, in several cases, infection rates increased sharply, causing a switch to a suppression strategy with strict containment measures. China and several other Asian countries, as well as Australia and New Zealand, chose an elimination strategy with more severe lockdown measures in an effort to stop transmission completely. Among the Nordic countries, Denmark, Finland, Iceland, and Norway implemented strict measures to suppress the pandemic, while Sweden adopted a less strict strategy. Sweden did not adopt stringent lockdown restrictions with compulsory stay-at-home orders, school closures or mandated working from home. It relied to a greater extent on recommendations and softer containment measures and restrictions.

This paper provides an overview of economic developments in the Nordic countries during the pandemic and considers and discusses the economic policy measures put in place, focussing in particular on the unconventional policies deployed to protect incomes, jobs, and companies in the short term. This paper does not address health developments and containment policies. For a discussion and references on these issues, see Andersen et al. (2022).

A general caveat is that the pandemic is not yet over and continues to have a considerable impact. The Omicron strain is highly contagious and has become dominant. The outlook for the future is uncertain, both in relation to the severity of Omicron infection and, more generally, around the future development of the pandemic.

The paper starts by providing an overview of the economic developments in the Nordic countries seen in a comparative perspective (Section 2). The principal arguments underlying the use of relief packages and instruments are reviewed (Section 3). This is followed by a more in-depth discussion of key elements of the relief packages: job-retention schemes (Section 4), direct support to companies (Section 5) and monetary and macroprudential policies (Section 6). Finally, we assess the role of relief packages and provide some concluding remarks (Section 7).

2 Economic Developments

The pandemic caused a sharp decline in economic activity at the start of 2020, although Denmark, Finland, Norway and Sweden were less affected than most other countries. Iceland is an exception as the initial recession was deeper and the economic recovery to the pre-crisis GDP level took longer than in the other four Nordic countries (see Figures 2a–2f below).

In the second half of 2020, activity started to recover, and a second round of containment policies in winter 2020/2021 has not had the same negative effects on activity as the first round. By 2021.2, economic activity had recovered to a level close to the level prior to the pandemic (2019.4), and in Denmark had even surpassed it. Iceland’s GDP only returned to the pre-pandemic level at the end of 2021. In short, with the exception of Iceland, the decline in economic activity in the four Nordic countries was smaller than in most other countries, and activity has quickly recovered to pre-pandemic levels.

The smaller negative effect in the second round is interesting since the second round of containment measures was approximately as strict or stricter than the previous round. This suggests a difference between the unanticipated and unexperienced event in the first round (the onset of the pandemic) and subsequent adaptation and learning processes applied during the second round.[1]Gamtkitsulashvili and Plekhanov (2021) conclude, based on an empirical analysis covering 53 countries, that economic activity became less sensitive to mobility during the pandemic which shows an adjustment to containment measures and restrictions. However, economic activity remains closely correlated with mobility, and increased activity has been primarily associated with increased mobility. The economic support policies and private sector knowledge that were in place the second time may also have played a role.

Footnotes

- ^ Gamtkitsulashvili and Plekhanov (2021) conclude, based on an empirical analysis covering 53 countries, that economic activity became less sensitive to mobility during the pandemic which shows an adjustment to containment measures and restrictions. However, economic activity remains closely correlated with mobility, and increased activity has been primarily associated with increased mobility.

Looking closer at the aggregate demand components, a typical business cycle picture emerges with declines in private consumption (and hence imports), investments and exports.[1]With the very significant fluctuations in exports and imports, Iceland differs from the more moderate developments in the other four Nordic countries. However, these declines were not driven by the usual business cycle mechanisms or economic imbalances (e.g., as during the financial crisis in 2008–2009) but by lockdown restrictions and behavioural responses to the pandemic. This is also important for the recovery since, in combination with economic policies, the aggregate demand potential was maintained and could be released in tandem with the reopening of the economies.

The similar responses in terms of private consumption during the first phase of the pandemic across the Nordic countries, despite the differences in health strategies, is particularly noteworthy. Andersen et al. (2020b) explores this issue in a comparison of Sweden and Denmark using real-time transaction data from a large bank in Scandinavia (see also Andersen et al. 2020a). They find a drop in aggregate spending of around 25 percent in Sweden and approximately 29 percent in Denmark, indicating a strong behavioural response in Sweden despite much more lenient policy measures in that country. There is also an interesting age gradient in the behavioural response, as spending dropped much less in Sweden than in Denmark for the young low-risk group and more for the older high-risk group. Thus, the containment policies in Denmark reduced the economic activity of the low-risk population, which provided protection for the older high-risk group, implying that the latter group did not cut their spending as much.

The quick recovery in activity in the Nordic countries (except Iceland), despite the initial sharp drop, stands in contrast to the financial crisis, which also saw large declines in economic activity (except for Norway), but a much slower recovery (see Andersen et al. 2022). This underlines how the COVID-19 crisis differs from a typical business cycle downturn.

Footnotes

- ^ With the very significant fluctuations in exports and imports, Iceland differs from the more moderate developments in the other four Nordic countries.

Figure 2a Key facts on economic developments – Nordic countries and EU, GDP

Figure 2b Key facts on economic developments – Nordic countries and EU, government consumption

Figure 2c Key facts on economic developments – Nordic countries and EU, investments

Figure 2d Key facts on economic developments – Nordic countries and EU, private consumption

Figure 2e Key facts on economic developments – Nordic countries and EU, exports

Figure 2f Key facts on economic developments – Nordic countries and EU, imports

While some developments in key macro-variables are similar to previous downturns, there are also some notable differences. One striking fact is that house prices generally rose in 2020–2021 (see Andersen et al. 2022). The rises were greatest in Denmark and Sweden, but also noticeable in Norway and the Euro area, and somewhat smaller in Iceland and Finland. House price increases are a surprising phenomenon, as an economic downturn is normally associated with falling house prices due to declining incomes, higher unemployment and greater economic uncertainty. However, low and falling interest rates have helped support house prices, and stay-at-home policies may also have increased demand for housing. It could also be interpreted as showing that, perhaps due to the relief packages, the crisis did not trigger a very significant increase in economic uncertainty perceived by consumers.

There are large sectoral differences in both the impact of the pandemic and the subsequent recovery rate in the four larger Nordic countries (see Figures 3 and 4). Some sectors were barely affected or may even have had increased activity, while others were severely affected. Although the recovery has been rather broad-based, trade, tourism, entertainment, and recreation have not yet recovered to pre-crisis levels of activity.

Figure 3 presents noticeable differences between the four Nordic countries (comparable data for Iceland is not available). Sweden had larger falls in the industry and manufacturing sectors in the second quarter of 2020 than the other Nordic countries, which probably reflects a negative impact of reduced foreign demand. On the other hand, activity in the ‘Other’ sector, which includes the arts, entertainment, recreation and other service activities, fell much less in Sweden than in the other Nordic countries in 2020.2. This suggests that the weaker restrictions in Sweden had some economic benefits in the form of smaller reductions in activity in these sectors, even if the difference is not pronounced in the aggregate.

Bougroug et al. (2021) analyse the role of the sectoral structure for the economic responses to the pandemic in Denmark, Norway and Sweden. Sweden has a relatively significant industrial sector and a smaller service sector than Denmark and Norway. The authors conclude that differences in sector structure account for only a small fraction of the differences in overall economic performance in the three countries.

Figure 3 Sectoral changes in value added. Decline 2020.2 relative to 2019.4

Figure 4 Sectoral changes in value added. Recovery gap: Value added 2021.2 relative to 2019.4

It is now widely recognised that both the health and economic implications of the corona pandemic and lockdown policies depend not only on policies related specifically to these areas but also on behavioural responses, national characteristics, including population structure, urbanisation, health care system, sector structure, degree of digitalisation, and the economic situation at the outset of the pandemic (see, e.g. Furceri et al. 2021 and Sapir 2020). One important factor is the degree of digitalisation as it enables transition from physical to virtual activities (e-commerce, meetings, teaching, working from home etc.). The higher the degree of substitution between physical and virtual activities, the lower the economic consequences of containment restrictions. The degree of substitution depends on the sectoral composition of the economy and the level of digitalisation. Empirical evidence documents that digitalisation played a significant role in how the pandemic affected economic performance see, e.g., Zhuang (2021). The Nordic countries are among the most digitalised in Europe, and this is a contributing factor to the relatively smaller decline in economic activity in the bigger Nordic countries than elsewhere. Dingel and Neiman (2020) also report that the Nordic countries are among those where the greatest proportion of jobs can be done at home.

2.1 Labour market

The pandemic and containment policies caused an abrupt reduction in the activity level in all the Nordic countries, and in particular, contact intensive sectors were severely affected. Working hours fell sharply in some sectors, and the Nordic Region and other OECD countries employed new or existing job retention schemes to prevent permanent job losses, cf. section 4 below. Juranek et al. (2021) point out that the negative labour market effects in the early phase of the pandemic were slightly smaller in Sweden than in the other Nordic countries, reflecting the lighter restrictions introduced in Sweden. The gross number of workers in job-sharing, temporary layoff or wage-compensation schemes are shown in Figure 5 (data unavailable for Iceland). The figure displays gross numbers based on available statistics. It is informative in relation to the number of workers affected but who nonetheless have maintained a relationship to their job. A measure in full-time equivalents would have been useful to show the effects in terms of hours not worked, but comparable data is not readily available. The use of these schemes was most prevalent during the first wave of the pandemic, and they have subsequently been of less importance.

Figure 5 Work sharing/Wage compensation/short-time work/temporary layoffs, Nordic countries 2019.4 to 2021.3

The sectoral composition of the decline in activity had important implications for which groups of workers were the most affected. Contact-intensive sectors typically employ more young and low-skilled workers, as well as more immigrants, and consequently, working hours fell much more sharply for these groups (Alstadsæter et al. 2020a, 2020b, Campa et al. 2020, Hansen et al. 2020). The unequal effects are amplified by the tendency for teleworking to be easier for white-collar workers than blue-collar (Hansen et al. 2020). The labour market effects seem to be relatively balanced between the genders.

The increase in short-time work is not reflected in the employment and unemployment statistics from the Labour Force Surveys, in which employees are typically classified as employed as long as they have a job, even if they are on a job retention scheme and not actually working.[1]In Norway, employees on furlough are classified as employed in the Labour Force survey for the first six months on furlough. In Finland, temporary lay-off is not considered unemployment if the period is under three months. As a result, there is only a modest increase in unemployment rates, and a corresponding modest decrease in employment rates during the pandemic, with no noticeable gender differences. These modest effects reflect the role of relief packages (work sharing, wage compensation, see below).

Footnotes

- ^ In Norway, employees on furlough are classified as employed in the Labour Force survey for the first six months on furlough. In Finland, temporary lay-off is not considered unemployment if the period is under three months.

Figure 6a Employment rates

Figure 6b Unemployment rates

2.2 Public Finances

As expected, there was a significant deterioration in public finances, as indicated by Figure 7.a for net lending. This deterioration was not as severe in the Nordic Region (except Iceland) as it was in many other countries, which reflects that the downturn was not as deep as in other countries. The initial levels of public debt levels were low, which afforded some economic leeway to cope with the crisis (In Finland and Iceland, the effects were more severe, see Figure 7.b. Both had a higher initial debt level, and their projected debts exceeded the 60 percent limit). It should be noted that the final calculation of the cost to the public finances has not yet been carried out, as liquidity and loan arrangements were one of the fiscal tools deployed in the crisis. It should also be noted that a counterfactual approach involving no fiscal relief packages would have resulted in a deeper recession with a considerably greater impact on public finances.

Figure 7a Net lending

Figure 7b Public debt

3 Economic policies – relief packages

The imposition of containment measures and restrictions was largely an unanticipated event. The lockdown restrictions were motivated by the externalities arising from the spread of the virus caused by close contact between people. These restrictions may thus be interpreted as an unanticipated ‘market-closure’ or ‘business interruption’ shock, an event that is largely non-insurable.

The containment measures constrain the market mechanism. In the first instance, this takes place in areas where there is close contact between customers and employees, but also in workplaces where employees are in close contact with each other. While the lockdown regulations address a health externality and thus have a collective justification, individual companies, workers, and households must bear the consequences and costs.

As a consequence, governments have launched relief packages ranging from direct support to companies for loss of revenue, coverage of fixed costs, work-sharing arrangements, and liquidity and loan arrangements.[1]Some of the support measures conflict with the EU rules for state aid. In response to the COVID-19 pandemic, the EU Commission determined general rules for support and specific rules allowing temporary support. EU rules have influenced the specific design of some of the support measures. This also involved existing tax and welfare schemes, which in some cases were extended. These schemes are collectively financed via the public budgets. While activity declined, in part due to behavioural responses, traditional aggregate demand measures to support economic activity were not appropriate in the situation since attempting to boost activity would conflict with the overriding health concern of reducing physical contacts and thus reducing the spread of the virus.

Unconventional measures were needed instead. These are not part of standard economic toolkits, not even when steps are taken to affect activity or employment during deep recessions. There are three key arguments in support of such unconventional measures.

Footnotes

- ^ Some of the support measures conflict with the EU rules for state aid. In response to the COVID-19 pandemic, the EU Commission determined general rules for support and specific rules allowing temporary support. EU rules have influenced the specific design of some of the support measures.

The first type of argument is that the containment measures and lockdown policies can effectively be viewed as expropriation of market opportunities, justifying compensation. It could be argued that suppressing the pandemic is a common good, and the sectors which carry the burden of the measures should be compensated. The same could be said in respect of workers prevented from working, where the usual supports offered by the social safety net may be considered insufficient for this particular shock (here, too, there is no ex-ante moral hazard problem). The compensation measures may also be interpreted as an ex-post insurance of an unanticipated aggregate shock. Since companies and workers had no influence on the occurrence of this shock (no ex-ante moral hazard), there is no direct incentive issue in providing these supports. In particular, the support to companies has been contested, and it raises difficult issues, including which events to cover (demand may fall for many reasons) and whether there are alternative ways for business to cope with such situations. See the discussion in Section 5 below.[1]Henriksen et al. (2020) also argue that the insurance argument applies to households and not to companies – based on the view that capital owners receive high profits in good times, and may choose to diversify, so they should not be provided with insurance in bad times. Thus, the authors conclude that support to companies can be justified only in terms of efficiency (as is included in the second type of argument for support) and not insurance arguments. See e.g., OECD (2021b) for a discussion of insurance of economic losses triggered by a pandemic.

The second type of argument for support is that it is important to preserve production capacity to increase the likelihood of a V-shaped path for economic activity when containment policies are relaxed. In other words, perceiving the health situation and the containment measures to be temporary in order to minimise the risk that the economic repercussions become persistent. The negative effects of the containment measures and restrictions cannot be avoided, but a removal of them will only result in a rapid economic recovery if the production and demand capacity remains intact.[2]Guerrieri et al. (2020) show how the lockdown of some sectors (a supply shock) can reduce demand for sectors still open, a so-called ‘Keynesian supply shock’ where the change in aggregate demand is larger than the initial supply shock. In a setting with capital market failures (borrowing constraints, incomplete insurance) company closures and lay-offs may be excessive, providing a rationale for supporting companies, including support for job retention. Layoffs of workers breaking job-matches and closure of companies, followed by the hiring of workers and (re)opening of (new) companies, is associated with substantial transactions costs, time lags and loss of both real and human capital. From a societal perspective, this process is associated with excessive social costs (including fiscal costs), which leads to an efficiency argument in favour of support.

Thirdly, support for workers also helps to maintain income/consumption and reduce risks. This supports aggregate demand by preventing reduced demand in other sectors that remained open. Financial support to affected households also implies that aggregate demand can quickly pick up again when the economy reopens. The support includes work sharing/wage compensation but also temporary changes to the social safety net, e.g., extended benefit periods or higher benefit levels. Note that this argument applies not only to the sectors directly affected by containment measures but also to other more indirectly affected sectors by reducing risk and preventing a decline in aggregate demand.

Footnotes

- ^ Henriksen et al. (2020) also argue that the insurance argument applies to households and not to companies – based on the view that capital owners receive high profits in good times, and may choose to diversify, so they should not be provided with insurance in bad times. Thus, the authors conclude that support to companies can be justified only in terms of efficiency (as is included in the second type of argument for support) and not insurance arguments. See e.g., OECD (2021b) for a discussion of insurance of economic losses triggered by a pandemic.

- ^ Guerrieri et al. (2020) show how the lockdown of some sectors (a supply shock) can reduce demand for sectors still open, a so-called ‘Keynesian supply shock’ where the change in aggregate demand is larger than the initial supply shock. In a setting with capital market failures (borrowing constraints, incomplete insurance) company closures and lay-offs may be excessive, providing a rationale for supporting companies, including support for job retention.

All three arguments above apply to containment measures and restrictions, while arguably only the last two are relevant for the behavioural responses triggered by the pandemic (reduced activity due to behavioural responses are different since they are not the result of lockdown restrictions).

The ‘relief’ packages raise several issues in terms of design and implementation. Some of the key instruments used have no precedents and had to be implemented at short notice; hence they have a ‘crude’ design. This was also necessitated by the need for simple and easily administrative arrangements. The timeliness of the support was essential and, given the immense uncertainty at the start of the pandemic, the quick launch of the relief measures served as an important signal to households and companies. The choice of measures at the onset of the pandemic represented a largely improvisational response to a situation requiring acute action and where experience and knowledge on the effects of these interventions, both for the individual’s health and for society more generally, was largely absent. There was little time for detailed planning, and most countries launched a ‘package’ of unconventional initiatives within a small time window in response to the new situation.

The design of support measures is also complicated by the difficulty of separating the direct effects deserving support from other changes caused by general business cycle repercussions or second-round effects arising from the global economic impact of the pandemic. Such business cycle fluctuations are normally not insured at company level since this creates obvious incentive problems and disrupts the market mechanism. The schemes are based on simple criteria like, e.g., the decline in turnover or the risk of layoffs. Such measures reflect the effects of the pandemic, but they are not perfectly targeted. Many companies also experience declines in turnover, layoffs etc. during normal economic times, and such criteria do not directly identify the effects of the pandemic. In the unusual crisis situation of the pandemic, it can be argued that guaranteeing support was more important than its precise targeting and justified the more lenient criteria. The flipside is the placing of a large burden on the public budget and possible misallocation of real and human capital (see the discussion below).

A key problem with the emergency packages and unconventional measures is that they have a status quo bias. This applies particularly to measures covering part of fixed costs or loss of income and work-sharing arrangements that restrict the reallocation of capital and labour. Incentive problems also arise as companies may have insufficient incentives to adjust to the new situation (ex-post moral hazard problem: the consequences of the shock are worsened). These measures thus contain a locking-in problem in relation to both real and human capital. Accordingly, it is important that they are temporary in nature and have well-defined sunset clauses.

3.1 Policy instruments[1]Andersen et al. (2022), Table 2 compares the instruments for the four Nordic countries. IMF (2021) gives more information about the policy measures in Iceland.

The list of unconventional policy measures includes:

- Liquidity/loans/guarantees

- Subsidies

- Fixed costs

- Job matches (work sharing/wage compensation)

- Specific sectors, e.g., tourism

- Miscellaneous, e.g., culture - Income support

- Self-employed

- Households generally

More conventional measures include:

- Fiscal policy

- Expenditures

- Taxation - Monetary policy

- Macroprudential policy

Table 1 shows the discretionary fiscal measures in the Nordic countries as percentages of GDP. The numbers represent decisions about measures taken for 2020, 2021 and beyond. They denote upper limits for spending items as the actual uptakes are a lot smaller in some cases (see examples in the note below). The magnitudes of the items in the different countries are broadly similar.[2]It should be emphasised that there are uncertainties in the details of classifications. IMF warns about these problems when making comparisons between countries.

Footnotes

- ^ Andersen et al. (2022), Table 2 compares the instruments for the four Nordic countries. IMF (2021) gives more information about the policy measures in Iceland.

- ^ It should be emphasised that there are uncertainties in the details of classifications. IMF warns about these problems when making comparisons between countries.

Table 1 Decisions on discretionary fiscal measures during the COVID-19 crisis since January 2020, percent of GDP

| Denmark | Finland | Iceland | Norway | Sweden | |

| Additional spending or foregone revenue | 3.4 | 4.8 | 10.1 | 7.4 | 4.2 |

| Accel. spending, deferred revenue | 13.7 | 0.2 | 0.3 | 6.7 | |

| Equity, loans, asset purchase | 12.1 | 0.5 | 0 | 2 | 0.2 |

| Guarantees | 3.5 | 5.2 | 1.1 | 2.6 | 5 |

| Quasi-fiscal operations | 1.7 |

One particular measure taken in Denmark, alongside reopening, was the ‘unfreezing’ of holiday pay.[1]In Denmark, a proportion of wage income (typically 12.5 percent) is reserved for holiday pay, paid out during holiday periods. In the past, holiday pay depended on wage income earned in a previous period (i.e., there was a lag between accrual of holiday allowances and the pay-out period). A recent reform synchronised the earnings and the holiday period, and to avoid a double pay-out of holiday allowance, one part was frozen until retirement. In response to the COVID-19 crisis, it was decided to allow individualsto demand pay-out of the frozen holiday pay in two rounds (autumn 2020 and early 2021). This is an example of an (unconventional) aggregate demand policy that simultaneously directly improved the disposable income of households and tax revenue since holiday pay is taxable income. In autumn 2020, holiday pay corresponding to DKK 31 billion (1.4 percent of GDP) was paid out, and in early 2020, DKK 22 billion (1 percent of GDP). This had a considerable impact on households’ disposable income.

The following sections discuss the more specific design of labour market and employment support schemes (Section 4), support for companies (Section 5) and monetary and macroprudential policy instruments (Section 6). Note that the schemes are interdependent, as support to workers in the form of job-sharing (to avoid layoffs) also benefit companies, while support to companies preventing job losses and redundancies also benefit workers. The support schemes also reduce layoffs, unemployment and bankruptcies, thus benefitting financial institutions.

4 Labour market and employment support schemes

The pandemic and resulting lockdowns led to a sharp reduction in economic activity and employment levels all over the world. On average, in OECD countries, hours worked fell by 15 percent from 2019.2 to 2020.2, cf. Figure 8 below.[1]The figures in this section are based on OECD Employment Outlook (2021a). The reduction in total hours was smaller in the Nordic countries, at around 5 percent, varying from 10 percent in Iceland, 6 percent in Finland, 5.5 percent in Denmark, 4.7 percent in Sweden and 3.7 percent in Norway. The smaller reduction in the Nordic Region also reflected the shorter duration of the first wave and associated lockdown, as activity then picked up towards the summer.

Footnotes

- ^ The figures in this section are based on OECD Employment Outlook (2021a).

Figure 8 Decomposition of total hours change, 2019.2–2020.2, selected countries, percent change over the year

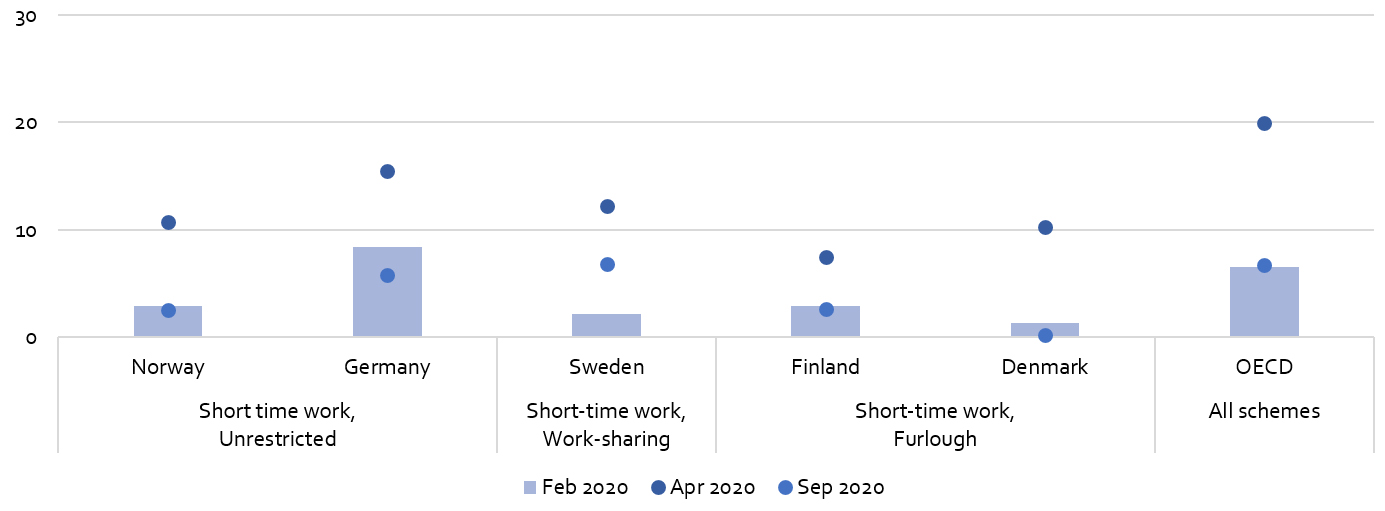

To prevent job losses and cushion the income loss for households, almost all OECD countries applied some form of job retention scheme. Many OECD countries had job-retention schemes in place prior to the pandemic, but most nevertheless modified their schemes to increase take-up, and/or they introduced new schemes (see OECD 2021a). On average, in the OECD countries, the take-up rate of retention schemes corresponded to 20 percent of dependent employment in April/May 2020. In the Nordic countries, the take-up rate was lower, at 10–12 percent in Denmark, Norway, and Sweden at the peak in April/May 2020, and 7.5 percent in Finland.

There are notable differences between the schemes in the Nordic countries. The description below focuses on the main aspects of the schemes during the first phase of the pandemic, omitting details and subsequent changes.

In Denmark, the new furlough scheme (‘lønkompensationsordningen’) was introduced to compensate companies that would otherwise have laid off at least 30 percent of their employees, or more than 50 employees. The furloughed workers were not allowed to work, although they received regular wages. For every three months on the scheme, five days were counted as holidays. The compensation for companies was 75 percent of the wage cost of a white-collar worker and 90 percent for blue-collar workers, in both cases with a maximum wage cap of DKK 30 000 per month. Companies were not allowed to lay off employees permanently while accepting help from the scheme. There was a degree of flexibility involved, allowing companies to take back employees if needed, with a corresponding reduction in the support they received.

In the work-sharing arrangement in Denmark (‘arbejdsfordelingsordningen’), companies could reduce working time partially for some or all workers, while workers received unemployment benefit (‘dagpenge’) for the days they do not work. Companies covered the costs of the benefits for the first two days when employees were not working, and they were subsequently only required to cover other costs such as insurance, etc.

For many years, Norway has had a furlough or short-time work scheme (‘permitteringsordning’), allowing companies to temporarily lay off workers if there is a temporary and unforeseen reduction in activity. The reduction in working hours must be at least 40 percent, and workers receive regular unemployment benefit while not working. In the pre-pandemic scheme, companies were required to pay full wages for the first 15 days, but this was reduced to two days, early in the lockdown, with the government subsidising the full wages (up to about NOK 50 000 per month) for the first 20 days. Unemployment benefit was increased to 80 percent of salary for the first NOK 25 000 per month and 62.4 percent of salary between NOK 25 000 and NOK 50 000 per month.

In Sweden, a new short-time work scheme was introduced in April 2020 for companies suffering temporary serious financial difficulties due to circumstances beyond their control. In contrast to the schemes in the other Nordic countries, working time can only be reduced up to a maximum of 60 percent or 80 percent (the maximum has varied over time). A reduction in working time of 80 percent involves a reduction in wage costs for the company of 72 percent and a reduction in employee wages of 12 percent (Tillväxtverket 2021).

In Finland, a system for temporary layoffs (furloughs) was already in place. Furlough may be for a specific period of time or until further notice. A shortened working week is also possible. Employees on furlough receive unemployment benefit, which is partially paid for collectively by both the employers and employees. The compensation for employees is lower than in the other Nordic countries, with 56 percent for a salary of 3000 euros per month and slightly less than 50 percent for 4000 euros per month (TYJ 2021). However, part-time furloughed workers may receive partial unemployment benefits on top of partial wages and considerably higher replacement rates (Juranek et al. 2021).

In Iceland, the government introduced an option for full-time workers to move to part-time work with government support. Employees could reduce their hours or salary down to 25 percent and supplement their earnings with government support. Companies with revenue loss above 75 percent were given the opportunity to apply for government support to recompense a portion of salary costs during the notice period (Government of Iceland 2020).

The key motivation for job retention schemes is to reduce wage costs for companies in severe financial difficulties, to prevent bankruptcies and avoid permanent layoffs. Job retention schemes allow companies to reduce working hours instead of laying off workers on a permanent basis. Another motivation was to mitigate the costs for the companies and employees most affected by the pandemic, as these costs were unevenly distributed.

However, job retention schemes also involve efficiency costs as well as financial costs to the government. When the government subsidises reduced working hours and furlough, companies may reduce hours worked even if the marginal productivity of labour is higher than in relevant alternatives because companies want to save on wage costs. To mitigate this problem, companies can be allowed to pay some of the wage costs, e.g., by requiring that they cover the wage costs for the first 15 days (as in the Norwegian scheme pre-corona) or that only a portion of the wage costs is covered (as in the Danish and Swedish schemes). Another efficiency cost is that furloughed workers are not usually available for other vacant jobs.

Another potential problem is that if companies incur little or no costs for furloughed employees, it may be tempting to keep them furloughed, even if the probability of reemployment is low, in the hope that business eventually improves. As the probability of finding a new job is likely to fall over a long period on furlough, this may reduce the overall probability of employment for those employees.

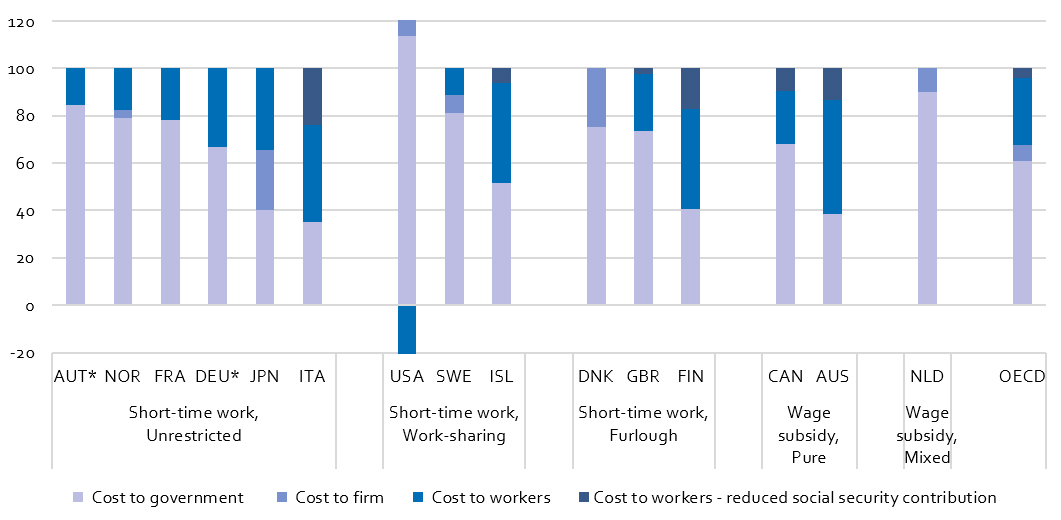

Figure 9a The costs of hours not worked for the government, companies and workers, selected countries – at the average wage level

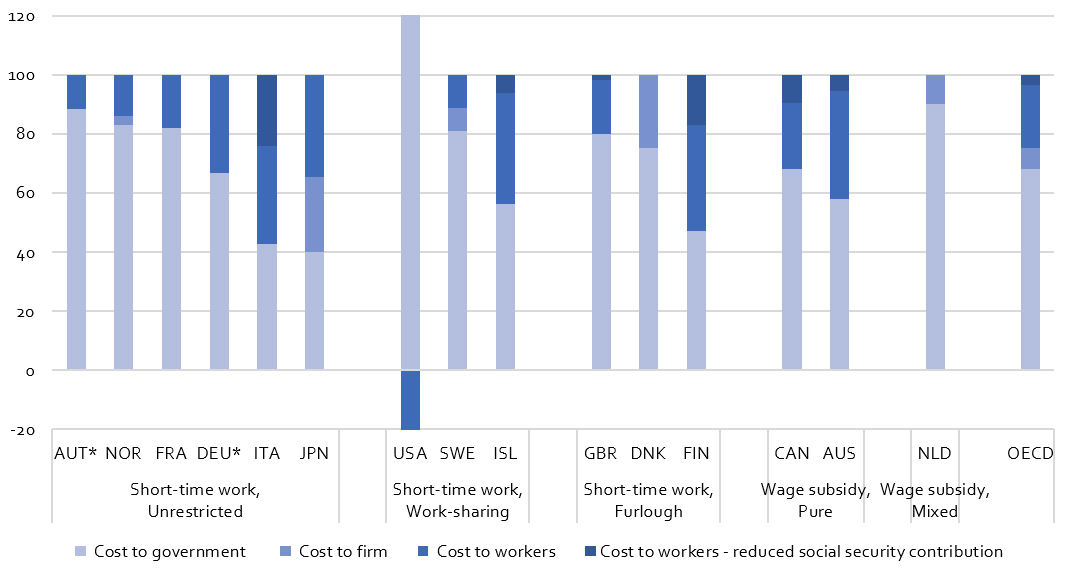

Figure 9b The costs of hours not worked for the government, companies and workers, selected countries – at the 67 percent of the average wage level

Compensating employees in a job retention scheme consists of recognisable trade-offs between insurance and welfare on the one hand and incentives and costs on the other. Full compensation would be good for the insurance and welfare of employees, while concerns about incentives and costs to the government would suggest lower compensation so as to lower public costs and incentivise employees on furlough to look for other jobs. During the pandemic, this trade-off is tilted toward the welfare of employees in order to share the burden and to increase trust and public support. Furthermore, during a situation with widespread lockdowns, there are fewer vacant jobs and thus less need to incentivise unemployed or furloughed individuals to look for other jobs.

Overall, the Finnish and Icelandic job retention systems seem to be the most favourable for employers, and the Danish system the least. For the employees, the Danish scheme is the most favourable and the Finnish and Icelandic system the least, while the Norwegian and Swedish systems fall somewhere in the middle.

It is difficult to assess the extent to which job retention schemes have contributed to the recovery in employment as the economy has improved because we have no counterfactual. There are, however, several studies indicating that the schemes have contributed positively to the prevention of layoffs. Bennedsen et al. (2020) collected survey data for some 10 000 Danish companies and matched them to furlough and administrative-accounting data. Comparing actual outcomes with the counterfactual, they estimate that the support schemes led to 285 000 workers being furloughed while there was a reduction of layoffs corresponding to 81 000 workers.

Most observers argue that job retention schemes have helped to save jobs by preventing bankruptcies and large numbers of permanent redundancies (see OECD 2021a, Hansen et al. 2020, da Silva et al. 2020). This is consistent with our own assessment. Without the support of such schemes, profit maximisation or strict short-run financial constraints might have caused companies to terminate more jobs. This could involve efficiency costs due to permanent job losses and increased macroeconomic uncertainty. However, it also seems likely that many of the furloughed employees would have been kept on by the companies even if there had been no furlough scheme. In these cases, the furlough scheme reduces costs to companies but at a considerable cost to the state. Overall, there appear to be positive efficiency and stabilisation arguments for extensive job retention schemes in a crisis like the pandemic.

5 Support for companies

Financial relief packages for companies are not standard parts of the economic toolkit and have no precedents, even in major crises in the past. They consist of two classes of instruments: liquidity/loan facilities and support for fixed costs. In addition, there are other instruments targeting specific sectors and schemes providing income support for the self-employed, which are not discussed here.

A key element in liquidity provision runs through the tax system via postponement of tax and VAT payments, lower penalties for late payments (reduced or no interest rates) or explicit loan arrangements based on tax and VAT payments and pension contributions by the company.[1]In addition, various loan arrangements have been extended either in the form of guarantees or explicit loans. This is a swift channel for providing liquidity to companies. It is targeted at companies with positive tax and VAT liabilities, and since this depends on past performance, the provision of liquidity is positively correlated with the viability of the firm.

Footnotes

- ^ In addition, various loan arrangements have been extended either in the form of guarantees or explicit loans.

Figure 10 Compensation scheme for fixed costs – 2020

In Denmark, Finland, Norway and Sweden, there are schemes in place to support the fixed costs of companies based on the decline in turnover,[1]Iceland has offered resilience support to help companies maintain a minimum level of activity while the impact of the pandemic persists. The subsidy amounts are based on operating expenses but may not exceed the amount of the revenue loss during the period in question, and there are upper caps across two groups with losses between 60 and 80 percent and losses between 80 and 100 percent. and the main features of these schemes, implemented during the first wave, are illustrated in Figure 10. These have subsequently undergone several adjustments, e.g., Denmark has adopted a smoother compensation curve and other schemes for second-round effects after the reopening of the economy. Support for the decline in turnover is increasing in the decline in turnover, but with a lower threshold determining eligibility and an upper cap (except for 100 percent lockdowns) on the support. In general, support is higher for moderate declines in turnover in Norway and Sweden, compared to Denmark, and the opposite for large declines in turnover. The Finnish scheme is the least generous. In addition, there are country-specific details on the measurement of turnover, the reference period and the definition of fixed costs.

The schemes aim at avoiding companies closing or having to face dire financial strain, and they are, by nature, company-specific. This raises a number of questions. In a normal situation, positive and negative shocks affect business opportunities, and in the process, some businesses may go bankrupt due to mismanagement or if demand for products/services declines for various reasons. Such closures do not represent a policy problem but are part of the market mechanism and serve to reallocate resources and ensure an efficient allocation of these. However, when many companies are affected simultaneously, a systemic issue arises. A small number of companies going bankrupt is not necessarily a problem, but the simultaneous bankruptcy of multiple companies may be. However, company-specific compensation policies interfere with the market mechanism and have a status quo bias by supporting existing companies based on historical performance measures such as turnover. If the support measures are left in place too long, they may impair adjustment and efficient use of real and human capital. Incentive problems also arise as companies may lack sufficient motivation to adjust to the new situation, e.g., by adapting their business model (for example, through e-commerce).

Footnotes

- ^ Iceland has offered resilience support to help companies maintain a minimum level of activity while the impact of the pandemic persists. The subsidy amounts are based on operating expenses but may not exceed the amount of the revenue loss during the period in question, and there are upper caps across two groups with losses between 60 and 80 percent and losses between 80 and 100 percent.

The company-specific nature of the intervention raises the question of whether businesses could either self-insure or insure against such events.[1]The nature of the ‘pandemic’ shock makes it impossible to diversify the shock in financial markets since that would require assets offering contingencies depending on the pandemic. They can self-insure either via financial buffers or loan financing. However, this raises other issues, especially for small and medium-sized enterprises. While companies generally retain buffers to cope with normal variations in business, the situation created by the pandemic is different and self-insurance under these circumstances is far from unproblematic. During a lockdown, when a company is precluded from operating, no revenue is generated, but there are irreversible/fixed costs that accumulate into a total lockdown cost. Especially for businesses operating in a competitive environment with small profit margins, it may be difficult to bear such costs and/or cover them through external financing. A business generating rent has a liquidity problem only, whereas one in a more competitive environment is more likely to have both a liquidity and solvency problem. Relying on self-insurance via capital markets during the pandemic thus has important implications for competition and is not as market-conform as it may first appear.

In addition, financing opportunities may be affected by the severity of containment policies and behavioural responses, past performance, solvency, changes in business opportunities post-pandemic, uncertainty about the length of the disruption of business, entrepreneurial skills, etc. Given the systemic nature of the event, a credit squeeze may also arise. In addition, decisions by financial institutions do not take the excessive social costs of bankruptcy into account, and hence the borrowing options may be too restrictive from a social point of view. Conversely, when otherwise financially viable businesses are in trouble, creditors (financial institutions, landlords etc.) may accept a haircut to avoid a more costly firm closure.[2]However, the large number of companies affected may trigger a financial accelerator effect arising from the declining value of collateral for loans. In this way, the negative shock is diversified. This mechanism is weakened by direct support to companies, which shifts the burden to the public purse and excludes private financing.

There is an important difference between schemes providing direct support and liquidity/loan arrangements.[3]Tax credits are effectively loans without any credit assessment. This allows the swift provision of liquidity but creates a risk that excessive tax/VAT liabilities are accumulated which later results in defaults (and loss of tax revenue). This is clearly an extreme alternative to market-based financing since it relies on self-selection by companies (provided they meet the conditions for ‘tax loans’). Ex-post, a difficult problem arises for tax authorities on how to handle defaults on tax loans. Each case would require a credit assessment to decide whether the company is viable, and whether a haircut on the debt is optimal. Such assessments are outside the normal competencies of tax authorities. Liquidity/loan arrangements overcome a short-run problem but are effectively implying self-financing or insurance, in the sense that businesses are offered the possibility of smoothing out the effects over time. Due to market imperfections, the risk of a credit squeeze and the urgency of providing liquidity/loans to a large number of companies, there is, therefore, an argument to be made for such schemes. However, they do not resolve the liquidity/solvency dilemma raised above, which pertains to business in more competitive environments.

Supporting companies’ fixed costs is far from unproblematic and raises many design issues. The design of the relief packages has three key dimensions: i) when is a business eligible for support, ii) what kind of support is available, and iii) for how long it be received? The eligibility conditions are crucial, and in the schemes applied, they are relatively broad, depending on the decline in turnover. This criterion is simple and relatively easy to implement, but it is not precisely targeted at companies adversely affected by the pandemic. A further problem is that fixed costs are not a well-defined term, and there may be different adjustment possibilities (including re-contracting, e.g., of leasing contracts). In addition, there are wide differences in the importance and nature of fixed costs between different businesses.

Footnotes

- ^ The nature of the ‘pandemic’ shock makes it impossible to diversify the shock in financial markets since that would require assets offering contingencies depending on the pandemic.

- ^ However, the large number of companies affected may trigger a financial accelerator effect arising from the declining value of collateral for loans.

- ^ Tax credits are effectively loans without any credit assessment. This allows the swift provision of liquidity but creates a risk that excessive tax/VAT liabilities are accumulated which later results in defaults (and loss of tax revenue). This is clearly an extreme alternative to market-based financing since it relies on self-selection by companies (provided they meet the conditions for ‘tax loans’). Ex-post, a difficult problem arises for tax authorities on how to handle defaults on tax loans. Each case would require a credit assessment to decide whether the company is viable, and whether a haircut on the debt is optimal. Such assessments are outside the normal competencies of tax authorities.

The decline in turnover is determined by relating turnover in a specific period to a reference period (typically the same period the previous year). While this is relatively simple, it raises issues since turnover in the reference period may be low or high for various reasons, and in any given period, some companies go through changes in turnover relative to their past performance. Although a 30 percent decline in turnover is large, it is not unusual even in a normal business cycle situation, as shown by data for Denmark reported in Andersen et al. (2021). The length of the reference period also matters. A short period implies that short-term variations are eligible for support, while a longer period implies some smoothing out and therefore only support in the event of more long-lasting declines in turnover (more self-insurance). The criteria should also be seen relative to the administrative costs for both business and the public sector and the risk of errors and fraud. There can be measurement issues around concepts like turnover and fixed costs, and while such schemes are relatively easy to administer, neither concept precisely targets the consequences of the pandemic for the individual company. More specific criteria easily become more complicated when more detailed measures are involved, for example, which is a cause of uncertainty for companies and administratively demanding.

These schemes should be temporary due to the implied status quo bias impeding structural adjustments,[1]The direct support to specific companies and industries in the emergency packages also have implications for industrial policy and trade policy. These measures have the bias that they support companies located within the country, and therefore could only be implemented through exemptions from EU rules. and they should have an explicit sunset clause both to give companies a clear planning platform and to signal that the scheme is an unusual solution for an unusual situation. However, the unpredictability of the pandemic has made it difficult to predetermine the duration of the schemes. Across the Nordic Region, the approach has been different. In Denmark, explicit sunset clauses have been included, and the cessation of the schemes followed reopening (with a short lag); in Finland, some schemes ceased at the end of 2020 and most of the rest at the end of 2021; in Norway, the schemes, for the most part, continued until the autumn or end of 2021, (although there were changes introduced over time) and finally, Sweden has not included sunset clauses but announced that ad hoc decisions would be made over time.